Evaluating the D&M IS Success Model in the Context of Accounting Information System and Sustainable Decision Making

Abstract

:1. Introduction

2. Literature Review

2.1. Accounting Information System

2.2. Information Quality

2.3. System Quality

2.4. Service Quality

2.5. AIS Usage

2.6. User Satisfaction

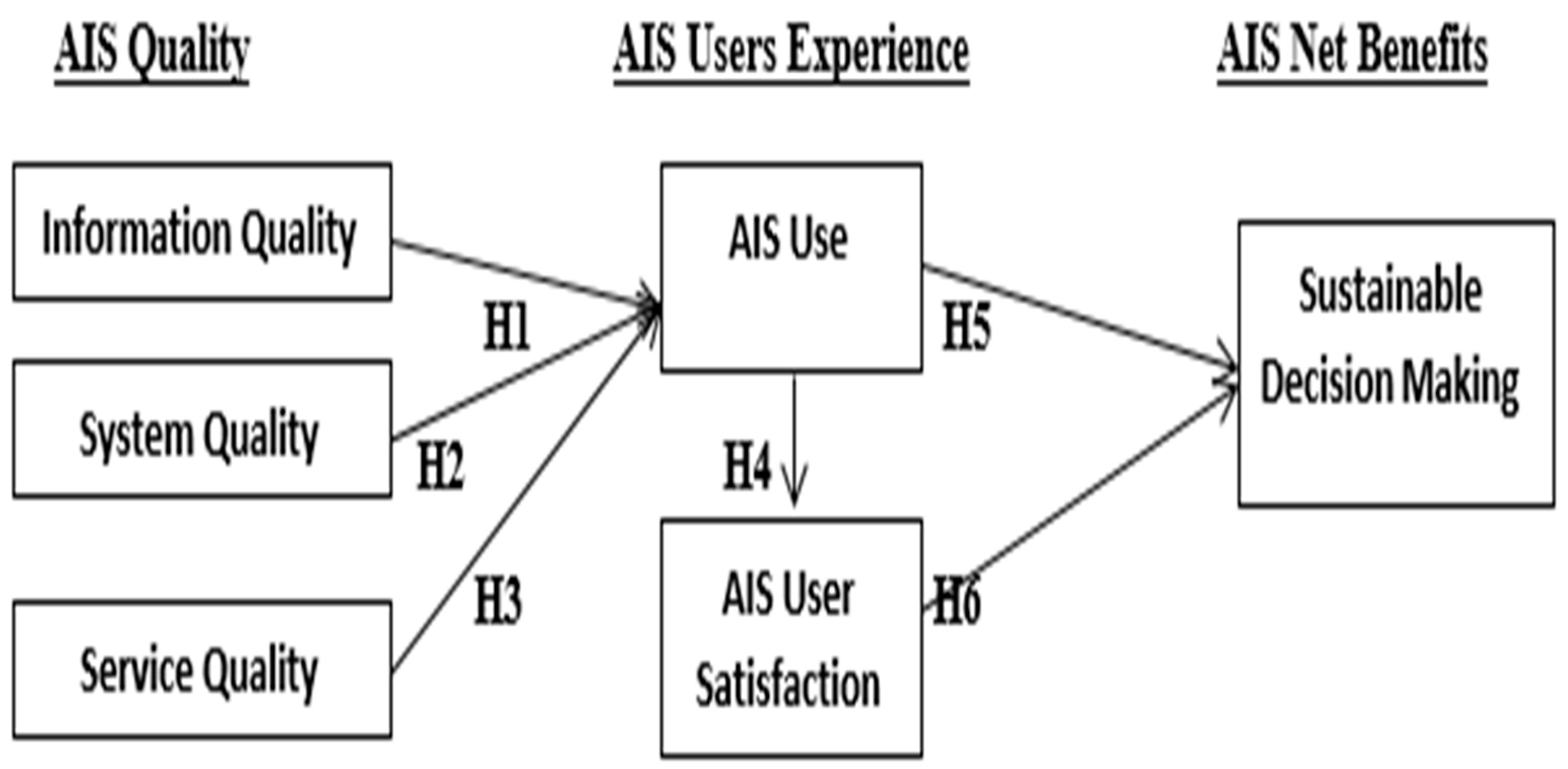

3. Theoretical Background and Framework

3.1. D&M IS Success Model

3.2. Theoretical Framework

4. Research Methodology

4.1. Measurement Development

4.2. Data Collection

5. Analysis and Results

5.1. Internal Consistency Reliability

5.2. Discriminant Validity

5.3. Assessing Predictive Relevance Q2 and Coefficient of Determination (R2)

6. Discussion and Implications

7. Conclusions, Limitations and Directions for Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Information Quality (InfQ) | Items | Reference |

| InfQ1 | Information from the AIS is always timely | [59] |

| InfQ2 | data provided by the AIS is useful | |

| InfQ3 | information provided by the AIS is accurate | |

| InfQ4 | Information from the AIS is easy to understand and related to decision-making | |

| System Quality (SysQ) | Items | Reference |

| SysQ1 | AIS user interface can be easily adapted to one’s personal approach. | [59] |

| SysQ2 | AIS is easy to use. | |

| SysQ3 | AIS responds quickly enough. | |

| SysQ4 | AIS is always up and running as necessary. | |

| Service Quality (SerQ) | Items | Reference |

| SerQ1 | The information I receive from the IS department is accurate. | [72,40] |

| SerQ2 | Training provided by the IS department improves my quality of work. | |

| SerQ3 | The IS department solves my problems and provide me prompt service. | |

| AIS Use | Items | Reference |

| Use1 | AIS is used frequently. | [60] |

| Use2 | I spend most of time per day using AIS for job-related work. | |

| Use3 | I depend highly on AIS use. | |

| AIS USat | Items | Reference |

| USat1 | I am satisfied with the SysQ. | [62] |

| USat1 | I am satisfied with the InfQ. | |

| USat1 | I am satisfied with the SerQ. | |

| Quality Decision Making (QDM) | Items | Reference |

| QDM1 | Based on the information from AIS, the outcome of the decision that I make is usually precise (the AIS will lead to the same outcome every time I face the same problem). | [68] |

| QDM2 | Based on the information from AIS, the outcome of the decision that I make is usually dependable. | |

| QDM3 | Based on the information from AIS, the outcome of the decision that I make is usually correct (the outcome may have minor errors). | |

| QDM4 | Based on the information from AIS, the outcome of the decision that I make is usually accurate (the outcome has no errors at all). |

References

- AL-Mugheed, K.; Bayraktar, N.; Al-Bsheish, M.; AlSyouf, A.; Jarrar, M.; AlBaker, W.; Aldhmadi, B.K. Patient Safety Attitudes among Doctors and Nurses: Associations with Workload, Adverse Events, Experience. Healthcare 2022, 10, 631. [Google Scholar] [CrossRef] [PubMed]

- Lutfi, A.; Al-Khasawneh, A.L.; Almaiah, M.A.; Alsyouf, A.; Alrawad, M. Business Sustainability of Small and Medium Enterprises during the COVID-19 Pandemic: The Role of AIS Implementation. Sustainability 2022, 14, 5362. [Google Scholar] [CrossRef]

- Alsyouf, A. Self-efficacy and personal innovativeness influence on nurses beliefs about EHRS usage in Saudi Arabia: Conceptual model. Int. J. Manag. (IJM) 2021, 12, 1049–1058. [Google Scholar]

- Almaiah, M.A.; Al-Otaibi, S.; Lutfi, A.; Almomani, O.; Awajan, A.; Alsaaidah, A.; Awad, A.B. Employing the TAM Model to Investigate the Readiness of M-Learning System Usage Using SEM Technique. Electronics 2022, 11, 1259. [Google Scholar] [CrossRef]

- Lutfi, A. Factors Influencing the Continuance Intention to Use Accounting Information System in Jordanian SMEs from the Perspectives of UTAUT: Top Management Support and Self-Efficacy as Predictor Factors. Economies 2022, 10, 75. [Google Scholar] [CrossRef]

- Jaber, M.M.; Alameri, T.; Ali, M.H.; Alsyouf, A.; Al-Bsheish, M.; Aldhmadi, B.K.; Jarrar, M.T. Remotely Monitoring COVID-19 Patient Health Condition Using Metaheuristics Convolute Networks from IoT-Based Wearable Device Health Data. Sensors 2022, 22, 1205. [Google Scholar] [CrossRef]

- Lutfi, A. Understanding Cloud Based Enterprise Resource Planning Adoption among SMEs in Jordan. J. Theor. Appl. Inform. Technol. 2021, 99, 5944–5953. [Google Scholar]

- Bani-Khalid, T.; Alshira’h, A.F.; Alshirah, M.H. Determinants of Tax Compliance Intention among Jordanian SMEs: A Focus on the Theory of Planned Behavior. Economies 2022, 10, 30. [Google Scholar] [CrossRef]

- Lutfi, A. Understanding the Intention to Adopt Cloud-based Accounting Information System in Jordanian SMEs. Int. J. Digit. Account. Res. 2022, 22, 47–70. [Google Scholar] [CrossRef]

- Lutfi, A.; Alshira’h, A.F.; Alshirah, M.H.; Al-Okaily, M.; Alqudah, H.; Saad, M.; Ibrahim, N.; Abdelmaksoud, O. Antecedents and Impacts of Enterprise Resource Planning System Adoption among Jordanian SMEs. Sustainability 2022, 14, 3508. [Google Scholar] [CrossRef]

- Syahidi, A.A.; Asyikin, A.N. Strategic planning and implementation of academic information system (AIS) based on website with D&M model approach. In IOP Conference Series: Materials Science and Engineering; IOP Publishing: Bristol, UK, 2018; Volume 407, p. 012101. [Google Scholar]

- Lutfi, A. Investigating the moderating effect of Environment Uncertainty on the relationship between institutional factors and ERP adoption among Jordanian SMEs. J. Open Innovat. Technol. Market Complex. 2020, 6, 91. [Google Scholar] [CrossRef]

- Bokhari, R.H. The relationship between system usage and user satisfaction: A meta-analysis. J. Enterp. Inform. Manag. 2005, 18, 211–234. [Google Scholar] [CrossRef] [Green Version]

- Al-Frijat, Y.S. The impact of accounting information systems used in the income tax department on the effectiveness of tax audit and collection in Jordan. J. Emerg. Trends Econ. Manag. Sci. 2014, 5, 19–25. [Google Scholar]

- Ahmad Farhan, A.; Hijattulah, A.; Abdul-Jabbar, H. Moderating role of patriotism on sales tax compliance among Jordanian SMEs. Int. J. Islam. Middle Eastern Fin. Manag. 2020, 13, 389–415. [Google Scholar] [CrossRef]

- Fadelelmoula, A.A. The effects of the critical success factors for ERP implementation on the comprehensive achievement of the crucial roles of information systems in the higher education sector. Interdiscip. J. Inform. Knowl. Manag. 2018, 13, 21–44. [Google Scholar] [CrossRef] [Green Version]

- Alshirah, A.; Magablih, A.; Alsqour, M. The effect of tax rate on sales tax compliance among Jordanian public shareholding corporations. Accounting 2021, 7, 883–892. [Google Scholar] [CrossRef]

- Das, A. Integrable Models; World Scientific: Singapore, 1989; Volume 30. [Google Scholar]

- Al-Dalaien, B.O.A.; Dalayeen, O.A. Investigating the Impact of Accounting Information System on the Profitability of Jordanian Banks. Res. J. Fin. Account. 2018, 9, 110–118. [Google Scholar]

- Nguyen, H.; Nguyen, A. Determinants of accounting information systems quality: Empirical evidence from Vietnam. Accounting 2020, 6, 185–198. [Google Scholar] [CrossRef]

- Alshira’h, A.F.; Alsqour, M.D.; Lutfi, A.; Alsyouf, A.; Alshirah, M. A Socio-Economic Model of Sales Tax Compliance. Economies 2020, 8, 88. [Google Scholar] [CrossRef]

- Lutfi, A.A.; Idris, K.M.; Mohamad, R. The influence of technological, organizational and environmental factors on accounting information system usage among Jordanian small and medium-sized enterprises. Int. J. Econ. Fin. Issues 2016, 6, 240–248. [Google Scholar]

- Ibrahim, F.; Ali, D.N.H.; Besar, N.S.A. Accounting information systems (AIS) in SMEs: Towards an integrated framework. Int. J. Asian Bus. Inform. Manag. (IJABIM) 2020, 11, 51–67. [Google Scholar] [CrossRef]

- Khassawneh, A.A.L. The influence of organizational factors on accounting information systems (AIS) effectiveness: A study of Jordanian SMEs. Int. J. Market. Technol. 2014, 4, 36. [Google Scholar]

- Monteiro, A.; Cepêda, C. Accounting information systems: Scientific production and trends in research. Systems 2021, 9, 67. [Google Scholar] [CrossRef]

- Lutfi, A.A.; Idris, K.M.; Mohamad, R. AIS usage factors and impact among Jordanian SMEs: The moderating effect of environmental uncertainty. J. Adv. Res. Bus. Manag. Stud. 2017, 6, 24–38. [Google Scholar]

- Fitrios, R. Factors that influence accounting information system implementation and accounting information quality. Int. J. Sci. Technol. Res. 2016, 5, 192–198. [Google Scholar]

- Ghobakhloo, M.; Azar, A.; Tang, S.H. Business value of enterprise resource planning spending and scope: A post-implementation perspective. Kybernetes 2019, 48, 967–989. [Google Scholar] [CrossRef]

- Eid, M.I.M.; Abbas, H.I. User adaptation and ERP benefits: Moderation analysis of user experience with ERP. Kybernetes 2017, 46, 530–549. [Google Scholar] [CrossRef]

- Okon, E.E.; Otuza, C.E.; Dada, S.O. Effect of Human Resource in Accounting Information System on Management Decision-Making in Seventh-day Adventist Institutions in Eastern Nigeria. Adv. Soc. Sci. Res. J. 2021, 8, 117–129. [Google Scholar] [CrossRef]

- Alzoubi, M.M.; Snider, D.H. Comparison of factors affecting enterprise resource planning system success in the Middle East. Int. J. Enterp. Inform. Syst. (IJEIS) 2020, 16, 17–38. [Google Scholar] [CrossRef]

- DeLone, W.; McLean, E. The DeLone and McLean model of information system success: A ten-year update. J. Manag. Inform. Syst. 2003, 19, 3–9. [Google Scholar]

- Sinarasri, A.; Zulaikha, F. The antecedents and consequences of accounting information system implementation: An empirical study on MSMEs in Semarang City. In Proceedings of the 5th International Conference on Accounting and Finance 2019 (ICAF 2019), Yogyakarta, Indonesia, 9–10 April 2019. [Google Scholar]

- Rasit, M.H.H.; Ibrahim, M.A. Factors influencing ais capability and performance of Malaysian co-operatives: A conceptual framework. Int. J. Account. 2018, 3, 71–82. [Google Scholar]

- Trabulsi, R.U. The Impact of Accounting Information Systems on Organizational Performance: The Context of Saudi’s SMEs. Int. Rev. Manag. Market. 2018, 8, 69–73. [Google Scholar]

- Lutfi, A.; Al-Okaily, M.; Alsyouf, A.; Alsaad, A.; Taamneh, A. The Impact of AIS Usage on AIS Effectiveness among Jordanian SMEs: A Multi Group Analysis of the Role of Firm Size. Global Bus. Rev. 2020, 21, 0972150920965079. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Ayouni, S.; Hajjej, F.; Lutfi, A.; Almomani, O.; Awad, A.B. Smart Mobile Learning Success Model for Higher Educational Institutions in the Context of the COVID-19 Pandemic. Electronics 2022, 11, 1278. [Google Scholar] [CrossRef]

- DeLone, W.; McLean, E. Information systems success: The quest for the dependent variable. Inform. Syst. Res. 1992, 3, 60–95. [Google Scholar] [CrossRef] [Green Version]

- Anggadini, S.D. The effect of top management support and internal control of the accounting information systems quality and its implications on the accounting information quality. Inform. Manag. Bus. Rev. 2015, 7, 93–102. [Google Scholar] [CrossRef] [Green Version]

- Alzoubi, A. The effectiveness of the accounting information system under the enterprise resources planning (ERP). Res. J. Fin. Account. 2011, 2, 10–19. [Google Scholar]

- Al-Hiyari, A.; Al-Mashregy, M.H.H.; Mat, N.K.; Alekam, J.E. Factors that affect accounting information system implementation and accounting information quality: A survey in University Utara Malaysia. Am. J. Econ. 2013, 3, 27–31. [Google Scholar]

- Daoud, H.; Triki, M. Accounting information systems in an ERP environment and tunisian firm performance. Int. J. Digit. Account. Res. 2013, 13. [Google Scholar] [CrossRef]

- Lutfi, A.; Saad, M.; Almaiah, M.A.; Alsaad, A.; Al-Khasawneh, A.; Alrawad, M.; Alsyouf, A.; Al-Khasawneh, A.L. Actual Use of Mobile Learning Technologies during Social Distancing Circumstances: Case Study of King Faisal University Students. Sustainability 2022, 14, 7323. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Hajjej, F.; Lutfi, A.; Al-Khasawneh, A.; Shehab, R.; Al-Otaibi, S.; Alrawad, M. Explaining the Factors Affecting Students’ Attitudes to Using Online Learning (Madrasati Platform) during COVID-19. Electronics 2022, 511, 973. [Google Scholar] [CrossRef]

- Quintero, J.M.M.; Pedroche, E.G.; de la Garza Ramos, M.I. Influence of the implementation factors in the information systems quality for the user satisfaction. J. Inform. Syst. Technol. Manag. 2009, 6, 25–44. [Google Scholar] [CrossRef]

- Xu, J.; Benbasat, I.; Cenfetelli, R.T. Integrating service quality with system and information quality: An empirical test in the e-service context. MIS Q. 2013, 37, 777–794. [Google Scholar] [CrossRef]

- Nelson, R.R.; Todd, P.A.; Wixom, B.H. Antecedents of information and system quality: An empirical examination within the context of data warehousing. J. Manag. Inform. Syst. 2005, 21, 199–235. [Google Scholar] [CrossRef]

- Negash, S.; Ryan, T.; Igbaria, M. Quality and effectiveness in web-based customer support systems. Inform. Manag. 2003, 40, 757–768. [Google Scholar] [CrossRef] [Green Version]

- Jiang, J.J.; Klein, G.; Crampton, S.M. A note on SERVQUAL reliability and validity in information system service quality measurement. Decis. Sci. 2000, 31, 725–744. [Google Scholar] [CrossRef]

- Arshah, R.A.; Desa, M.I.; Hussin, A.R.C. Establishing important criteria and factors for successful integrated information system. Glob. J. Technol. 2012, 10, 22–32. [Google Scholar]

- Chang, Y.K.; Zhang, X.; Mokhtar, I.A.; Foo, S.; Majid, S.; Luyt, B.; Theng, Y.L. Assessing students’ information literacy skills in two secondary schools in Singapore. J. Inform. Lit. 2012, 6, 19–34. [Google Scholar] [CrossRef]

- Trice, A.W.; Treacy, M.E. Utilization as a dependent variable in MIS research. ACM SIGMIS Database Database Adv. Inf. Syst. 1988, 19, 33–41. [Google Scholar] [CrossRef]

- Tarhan, C.; Aydın, C. Why Should Municipalities Use Management Information Systems in Their Decision-Making Processes? Int. J. Inform. Technol. Comput. Sci. 2019, 11, 1–8. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Hajjej, F.; Lutfi, A.; Al-Khasawneh, A.; Alkhdour, T.; Almomani, O.; Shehab, R. A Conceptual Framework for Determining Quality Requirements for Mobile Learning Applications Using Delphi Method. Electronics 2022, 11, 788. [Google Scholar] [CrossRef]

- Chou, H.W.; Chang, H.H.; Lin, Y.H.; Chou, S.B. Drivers and effects of post-implementation learning on ERP usage. Comput. Human Behav. 2014, 35, 267–277. [Google Scholar] [CrossRef]

- Chou, J.S.; Hong, J.H. Assessing the impact of quality determinants and user characteristics on successful enterprise resource planning project implementation. J. Manuf. Syst. 2013, 32, 792–800. [Google Scholar] [CrossRef]

- Lin, H.F. An investigation into the effects of IS quality and top management support on ERP system usage. Total Qual. Manag. 2010, 21, 335–349. [Google Scholar] [CrossRef]

- Zybin, S.; Bielozorova, Y. Risk-based Decision-making System for Information Processing Systems. Int. J. Inform. Technol. Comput. Sci. 2021, 13, 1–18. [Google Scholar] [CrossRef]

- Lin, H.Y.; Hsu, P.Y.; Ting, P.H. ERP systems success: An integration of IS success model and balanced scorecard. J. Res. Pract. Inform. Technol. 2006, 38, 215–228. [Google Scholar]

- Rajan, C.A.; Baral, R. Adoption of ERP system: An empirical study of factors influencing the usage of ERP and its impact on end user. IIMB Manag. Rev. 2015, 27, 105–117. [Google Scholar] [CrossRef] [Green Version]

- Ramli, A. The impact of external factors on accounting information system (AIS) usage. J. Entrep. Bus. (JEB) 2013, 1. Available online: http://journal.umk.edu.my/index.php/jeb/article/view/24 (accessed on 8 May 2022).

- Hsu, P.F.; Yen, H.R.; Chung, J.C. Assessing ERP post-implementation success at the individual level: Revisiting the role of service quality. Inform. Manag. 2015, 52, 925–942. [Google Scholar] [CrossRef]

- Wixom, B.H.; Todd, P.A. A theoretical integration of user satisfaction and technology acceptance. Inform. Syst. Res. 2005, 16, 85–102. [Google Scholar] [CrossRef]

- Alsyouf, A.; Lutfi, A.; Al-Bsheish, M.; Jarrar, M.; Al-Mugheed, K.; Almaiah, M.A.; Alhazmi, F.N.; Masa’deh, R.; Anshasi, R.J.; Ashour, A. Exposure Detection Applications Acceptance: The Case of COVID-19. Int. J. Environ. Res. Public Health 2022, 19, 7307. [Google Scholar] [CrossRef]

- Alsyouf, A.; Ishak, A.K. Understanding EHRs continuance intention to use from the perspectives of UTAUT: Practice environment moderating effect and top management support as predictor variables. Int. J. Electron. Healthcare 2018, 10, 24–59. [Google Scholar] [CrossRef]

- Alsyouf, A.; Masa’deh, R.E.; Albugami, M.; Al-Bsheish, M.; Lutfi, A.; Alsubahi, N. Risk of Fear and Anxiety in Utilising Health App Surveillance Due to COVID-19: Gender Differences Analysis. Risks 2021, 9, 179. [Google Scholar] [CrossRef]

- Arora, M.; Kumar, A. An Empirical Study on Make-or-buy Decision Making. Int. J. Educ. Manag. Eng. 2022, 12, 19–28. [Google Scholar] [CrossRef]

- Alalwan, J.A.; Thomas, M.A.; Weistroffer, H.R. Decision support capabilities of enterprise content management systems: An empirical investigation. Decis. Support Syst. 2014, 68, 39–48. [Google Scholar] [CrossRef] [Green Version]

- Bhattacherjee, A. Understanding information systems continuance: An expectation-confirmation model. MIS Q. 2001, 3, 351–370. [Google Scholar] [CrossRef]

- Mason, R.O. Measuring information output: A communication systems approach. Inform. Manag. 1978, 1, 219–234. [Google Scholar] [CrossRef]

- Petter, S.; McLean, E.R. A meta-analytic assessment of the DeLone and McLean IS success model: An examination of IS success at the individual level. Inform. Manag. 2009, 46, 159–166. [Google Scholar] [CrossRef]

- Petter, S.; DeLone, W.; McLean, E. Measuring information systems success: Models, dimensions, measures, and interrelationships. Eur. J. Inform. Syst. 2008, 17, 236–263. [Google Scholar] [CrossRef]

- Urbach, N.; Ahlemann, F. Structural equation modeling in information systems research using partial least squares. J. Inform. Technol. Theory Appl. 2010, 11, 5–40. [Google Scholar]

- Cullen, A.J.; Taylor, M. Critical success factors for B2B e-commerce use within the UK NHS pharmaceutical supply chain. Int. J. Operat. Prod. Manag. 2009, 29, 1156–1185. [Google Scholar] [CrossRef]

- Ifinedo, P.; Rapp, B.; Ifinedo, A.; Sundberg, K. Relationships among ERP post-implementation success constructs: An analysis at the organizational level. Comput. Hum. Behav. 2010, 26, 1136–1148. [Google Scholar] [CrossRef]

- Kharuddin, S.; Foong, S.Y.; Senik, R. Effects of decision rationality on ERP adoption extensiveness and organizational performance. J. Enterp. Inform. Manag. 2015, 28, 658–679. [Google Scholar] [CrossRef]

- Xie, Y.; Allen, C.J.; Ali, M. An integrated decision support system for ERP implementation in small and medium sized enterprises. J. Enterp. Inform. Manag. 2014, 27, 358–384. [Google Scholar] [CrossRef]

- Hambali, A.J.H. The success of e-filing adoption during COVID 19 pandemic: The role of collaborative quality, user intention, and user satisfaction. J. Econ. Bus. Account. Vent. 2020, 23, 57–68. [Google Scholar] [CrossRef]

- Dehghanpouri, H.; Soltani, Z.; Rostamzadeh, R. The impact of trust, privacy and quality of service on the success of E-CRM: The mediating role of customer satisfaction. J. Bus. Ind. Market. 2020, 35, 1831–1847. [Google Scholar] [CrossRef]

- Chen, J.V.; Chen, Y.; Capistrano, E.P.S. Process quality and collaboration quality on B2B e-commerce. Ind. Manag. Data Syst. 2013, 113, 908–926. [Google Scholar] [CrossRef] [Green Version]

- Ritchi, H.; Evayanti, N.F.; Sari, P.Y. A Study on Information Systems Success: Examining User Satisfaction of Accounting Information System:(A Study on whole City/Regency Governments of West Java Province). Bina Ekon. 2020, 24, 1–14. [Google Scholar] [CrossRef]

- Cheng, Y.M. A hybrid model for exploring the antecedents of cloud ERP continuance: Roles of quality determinants and task-technology fit. Int. J. Web Inform. Syst. 2018, 15, 215–235. [Google Scholar] [CrossRef]

- Ladan Shagari, S.; Abdullah, A.; Mat Saat, R. Accounting information systems effectiveness: Evidence from the Nigerian banking sector. Interdiscip. J. Inform. Knowl. Manag. 2017, 12, 309–335. [Google Scholar] [CrossRef] [Green Version]

- Li, Y.; Wang, J. Evaluating the Impact of Information System Quality on Continuance Intention toward Cloud Financial Information System. Front. Psychol. 2021, 12, 713353. [Google Scholar] [CrossRef] [PubMed]

- Purwati, A.A.; Mustafa, Z.; Deli, M.M. Management Information System in Evaluation of BCA Mobile Banking Using DeLone and McLean Model. J. Appl. Eng. Technol. Sci. (JAETS) 2021, 2, 70–77. [Google Scholar] [CrossRef]

- Sabah, M.I.A.; Rashid, U.K.; Nasuredin, J.; Hamawandy, N.M.; Bewani, H.A.W.A.; Bdulmajeed Jamil, D. The Effect of Delone and Mclean’s Information System Success Model on The Job Performance of Accounting Managers in Iraqi Banks. J. Contemp. Issues Bus. Gov. 2021, 27. [Google Scholar] [CrossRef]

- Hamdan, M.; Al-Hajri, N. The effect of information systems success factors on user satisfaction in accounting information systems. Manag. Sci. Lett. 2021, 11, 2045–2052. [Google Scholar] [CrossRef]

- Shagari, S.L.; Abdullah, A.; Mat Saat, R. The influence of system quality and information quality on Accounting Information System (AIS) effectiveness in Nigerian bank. Int. Postgrad. Bus. J. 2015, 58, 58–74. [Google Scholar]

- Tajul Urus, S.; Hasim, K.; Syed Mustapha Nazri, S.N.F.; Tuan Mat, T.Z. Critical success factors of accounting information systems (AIS): Empirical evidence from Malaysian organizations. Manag. Account. Rev. (MAR) 2020, 19, 233–266. [Google Scholar] [CrossRef]

- Memon, M.A.; Ting, H.; Ramayah, T.; Chuah, F.; Cheah, J.H. A review of the methodological misconceptions and guidelines related to the application of structural equation modeling: A Malaysian scenario. J. Appl. Struct. Equat. Model. 2017, 1, 1–13. [Google Scholar] [CrossRef]

- Sekaran, U.; Bougie, R. Research Methods for Business: A Skill-Building Approach; John Willey & Sons Ltd.: London, UK, 2013. [Google Scholar]

- Hwang, Y.; Al-Arabiat, M.; Shin, D.H.; Lee, Y. Understanding information proactiveness and the content management system adoption in pre-implementation stage. Comput. Human Behav. 2016, 64, 515–523. [Google Scholar] [CrossRef]

- Hair, J.F.; Risher, J.J.; Sarstedt, M.; Ringle, C.M. When to use and how to report the results of PLS-SEM. Eur. Bus. Rev. 2019, 31, 2–24. [Google Scholar] [CrossRef]

- Alrawad, M.; Lutfi, A.; Alyatama, S.; Elshaer, I.A.; Almaiah, M.A. Perception of Occupational and Environmental Risks and Hazards among Mineworkers: A Psychometric Paradigm Approach. Int. J. Environ. Res. Public Health 2022, 19, 3371. [Google Scholar] [CrossRef]

- Alshira’h, A.F.F. The Effect of Peer Influence on Sales Tax Compliance among Jordanian SMEs. Int. J. Acad. Res. Bus. Soc. Sci. 2019, 9, 710–721. [Google Scholar] [CrossRef] [Green Version]

- Alshirah, M.H.; Alshira’h, A.F.; Lutfi, A. Political connection, family ownership and corporate risk disclosure: Empirical evidence from Jordan. Medit. Account. Res. 2021. [Google Scholar] [CrossRef]

- Cohen, J. Statistical power analysis. Curr. Direct. Psychol. Sci. 1992, 1, 98–101. [Google Scholar] [CrossRef]

- Alshirah, M.; Alshirah, A.; Lutfi, A. Audit committee’s attributes, overlapping memberships on the audit committee and corporate risk disclosure: Evidence from Jordan. Accounting 2021, 7, 423–440. [Google Scholar] [CrossRef]

- Alshirah, M.; Lutfi, A.; Alshirah, A.; Saad, M.; Ibrahim, N.; Mohammed, F. Influences of the environmental factors on the intention to adopt cloud based accounting information system among SMEs in Jordan. Accounting 2021, 7, 645–654. [Google Scholar] [CrossRef]

- Sekaran, U.; Bougie, R. Research Methods for Business, 5th ed.; John Wiley & Sons: Hoboken, NJ, USA, 2010. [Google Scholar]

- Duarte, P.A.O.; Raposo, M.L.B. A PLS model to study brand preference: An application to the mobile phone market. In Handbook of Partial Least Squares; Esposito Vinzi, V., Chin, W.W., Henseler, J., Wang, H., Eds.; Springer Handbooks of Computational Statistics; Springer: Berlin/Heidelberg, Germany, 2010; p. 449. [Google Scholar]

- Falk, M.; Miller, A.G. Infrared spectrum of carbon dioxide in aqueous solution. Vibrat. Spectrosc. 1992, 4, 105–108. [Google Scholar] [CrossRef]

- Yakubu, M.N.; Dasuki, S. Assessing eLearning systems success in Nigeria: An application of the DeLone and McLean information systems success model. J. Inform. Technol. Educ. Res. 2018, 17, 183–203. [Google Scholar] [CrossRef] [Green Version]

- Jaafreh, A.B. Evaluation information system success: Applied DeLone and McLean information system success model in context banking system in KSA. Int. Rev. Manag. Bus. Res. 2017, 6, 829–845. [Google Scholar]

- Tajuddin, M. Modification of DeLon and Mclean Model in the Success of Information System for Good University Governance. Turkish Online J. Educ. Technol. TOJET 2015, 14, 113–123. [Google Scholar]

- Ghobakhloo, M.; Tang, S.H. Information system success among manufacturing SMEs: Case of developing countries. Inform. Technol. Dev. 2015, 21, 573–600. [Google Scholar] [CrossRef]

- Marble, R.P. A system implementation study: Management commitment to project management. Inform. Manag. 2003, 41, 111–123. [Google Scholar] [CrossRef]

- Heo, J.; Han, I. Performance measure of information systems (IS) in evolving computing environments: An empirical investigation. Inform. Manag. 2003, 40, 243–256. [Google Scholar] [CrossRef]

- Hou, C.K. Measuring the impacts of the integrating information systems on decision-making performance and organisational performance: An empirical study of the Taiwan semiconductor industry. Int. J. Technol. Policy Manag. 2013, 13, 34–66. [Google Scholar] [CrossRef]

- Ouiddad, A.; Chafik, O.K.A.R.; Chroqui, R.; Hassani, I.B. Does the adoption of ERP systems help improving decision-making? A systematic literature review. In Proceedings of the 2018 IEEE International Conference on Technology Management, Operations and Decisions (ICTMOD), Marrakech, Morocco, 21–23 November 2018; IEEE: Manhattan, NY, USA, 2018; pp. 61–66. [Google Scholar]

- Lutfi, A.; Alsyouf, A.; Almaiah, M.A.; Alrawad, M.; Abdo, A.A.K.; Al-Khasawneh, A.L.; Ibrahim, N.; Saad, M. Factors Influencing the Adoption of Big Data Analytics in the Digital Transformation Era: Case Study of Jordanian SMEs. Sustainability 2022, 14, 1802. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Hajjej, F.; Shishakly, R.; Lutfi, A.; Amin, A.; Awad, A.B. The Role of Quality Measurements in Enhancing the Usability of Mobile Learning Applications during COVID-19. Electronics 2022, 11, 1951. [Google Scholar] [CrossRef]

| Author | Domain | Quality Constructs | User Experience Construct | Net Benefits |

|---|---|---|---|---|

| [78] | E-Filing Adoption | Information Quality System Quality Service Quality | User Intention User Satisfaction | Net Benefit |

| [79] | electronic customer relationship management (E-CRM) | Service Quality | Customer Satisfaction | Success of ECRM systems |

| [80] | B2B e-commerce | Information Quality System Quality Service Quality | Usefulness User Satisfaction | customer loyalty |

| [81] | AIS | Information Quality System Quality Service Quality | User Satisfaction | Non |

| [44] | Online Learning | Information Quality System Quality Service Quality | Online Learning Adoption (Madrasati Platform) | Non |

| [82] | cloud ERP continuance | Information Quality System Quality | Satisfaction Confirmation Perceived Usefulness | Continuance Intention |

| [83] | AIS | Information Quality System Quality Service Quality | Non | AIS effectiveness |

| [84] | cloud financial information system, | Information Quality System Quality Service Quality | Satisfaction Trust | Continuance Intention |

| [85] | Mobile Banking | Information Quality System Quality Service Quality | User Satisfaction | Net Benefit |

| [86] | AIS | Information Quality System Quality Service Quality | User Satisfaction | Job Performance |

| [31] | ERP | Information Quality System Quality Service Quality | Non | Individual Impact |

| [87] | AIS | Information Quality System Quality Service Quality | User Satisfaction | Non |

| [88] | AIS | Information Quality System Quality | Non | AIS effectiveness |

| [89] | AIS | System Quality Service Quality | User Intention User Satisfaction | Net Benefit |

| Constructs | Cronbach’s Alpha | Composite Reliability | AVE |

|---|---|---|---|

| AIS Information Quality | 0.915 | 0.936 | 0.747 |

| AIS System Quality | 0.826 | 0.884 | 0.657 |

| AIS Service Quality | 0.911 | 0.933 | 0.737 |

| AIS Use | 0.901 | 0.938 | 0.835 |

| AIS User Satisfaction | 0.944 | 0.960 | 0.857 |

| Decision-making sustainability | 0.797 | 0.868 | 0.624 |

| Constructs | Mean | SD | 1 | 2 | 3 | 4 | 5 | 6 | |

|---|---|---|---|---|---|---|---|---|---|

| 1 | DM-Q | 3.634 | 0.691 | 0.791 | |||||

| 2 | IQ | 3.908 | 0.931 | 0.458 | 0.864 | ||||

| 3 | SQ | 3.456 | 0.822 | 0.281 | 0.535 | 0.858 | |||

| 4 | SyQ | 3.514 | 0.894 | 0.447 | 0.662 | 0.564 | 0.811 | ||

| 5 | AIS Usage | 3.901 | 0.851 | 0.448 | 0.498 | 0.428 | 0.520 | 0.914 | |

| 6 | AIS US | 3.707 | 0.895 | 0.550 | 0.616 | 0.522 | 0.581 | 0.557 | 0.926 |

| Hypothesis | Paths | Sta. Beta | Sample Mean | Stan Errors | t-Values | f2 | p-Values | Results |

|---|---|---|---|---|---|---|---|---|

| H1. | IQ—Usage | 0.233 | 0.241 | 0.118 | 1.961 | 0.041 | 0.051 | Sig |

| H2. | SyQ—Usage | 0.285 | 0.279 | 0.136 | 2.089 | 0.060 | 0.037 | Sig |

| H3. | SQ—Usage | 0.142 | 0.143 | 0.111 | 1.281 | 0.019 | 0.200 | Insig |

| H4. | Usage—US | 0.251 | 0.241 | 0.095 | 2.648 | 0.088 | 0.008 | Sig |

| H5. | Usage—DM-Q | 0.215 | 0.209 | 0.088 | 2.112 | 0.045 | 0.037 | Sig |

| H6. | US—DM-Q | 0.441 | 0.450 | 0.090 | 5.056 | 0.197 | 0.000 | Sig |

| Dependent Latent Variable | Predictive Relevance (Q2) | Coefficient of Determination (R2) |

|---|---|---|

| AIS Usage | 0.645 | 0.314 |

| AIS User Satisfaction | 0.143 | 0.523 |

| Decision Making sustainability | 0.528 | 0.324 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lutfi, A.; Al-Okaily, M.; Alsyouf, A.; Alrawad, M. Evaluating the D&M IS Success Model in the Context of Accounting Information System and Sustainable Decision Making. Sustainability 2022, 14, 8120. https://doi.org/10.3390/su14138120

Lutfi A, Al-Okaily M, Alsyouf A, Alrawad M. Evaluating the D&M IS Success Model in the Context of Accounting Information System and Sustainable Decision Making. Sustainability. 2022; 14(13):8120. https://doi.org/10.3390/su14138120

Chicago/Turabian StyleLutfi, Abdalwali, Manaf Al-Okaily, Adi Alsyouf, and Mahmaod Alrawad. 2022. "Evaluating the D&M IS Success Model in the Context of Accounting Information System and Sustainable Decision Making" Sustainability 14, no. 13: 8120. https://doi.org/10.3390/su14138120

APA StyleLutfi, A., Al-Okaily, M., Alsyouf, A., & Alrawad, M. (2022). Evaluating the D&M IS Success Model in the Context of Accounting Information System and Sustainable Decision Making. Sustainability, 14(13), 8120. https://doi.org/10.3390/su14138120