The Impact of Digital Technology Use on Passive Entrepreneurial Exit in Rural Households: Empirical Evidence from China

Abstract

:1. Introduction

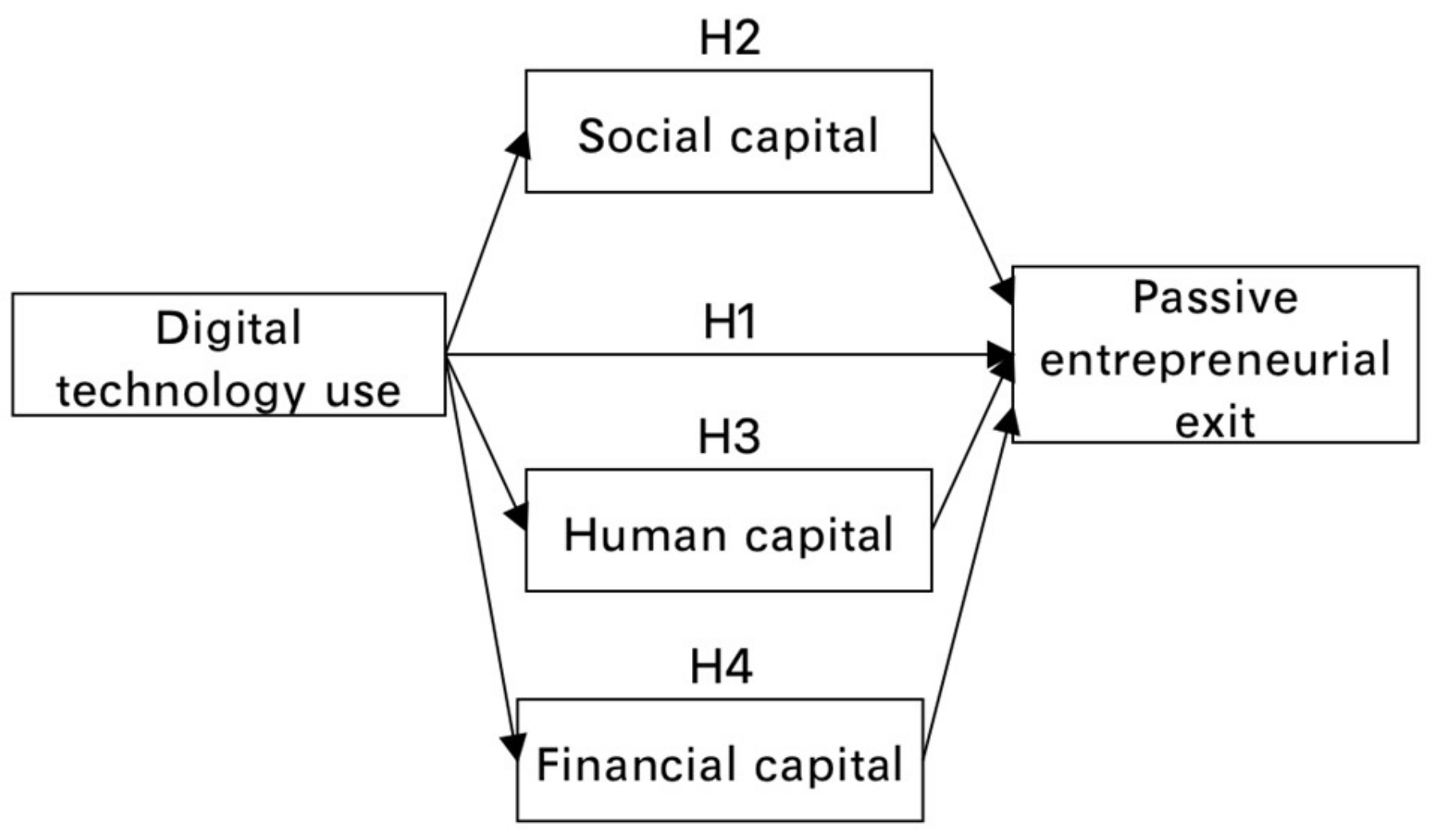

2. Theoretical Analysis

2.1. Why People Quit Entrepreneurship

2.2. Digital Technology Use and Passive Entrepreneurial Exits

2.3. Mechanisms of the Role of Digital Technology Use on Passive Entrepreneurial Exit

3. Data, Variables and Methods

3.1. Data Source

3.2. Variable Selection

3.3. Model Construction

4. Empirical Results and Analysis

4.1. Baseline Return

4.2. Robustness Tests

4.3. Mechanism Testing

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Wei, H.K.; Jiang, C.Y.; Kong, X.Z.; Zhang, T.Z.; Li, X.Y. Comprehensively promoting rural revitalization: Authoritative experts’ in-depth interpretation of the spirit of the Fifth Plenary Session of the Nineteenth Central Committee. China Rural. Econ. 2021, 1, 2–14. [Google Scholar]

- Zhong, Z.; Kong, X.Z. Rural innovation and entrepreneurship in the new era: Mechanism, situation and strategy. J. Jianghai Stud. 2020, 63, 98–106. [Google Scholar]

- Justo, R.; DeTienne, D.R.; Sieger, P. Failure or voluntary exit? Reassessing the female underperformance hypothesis. J. Bus. Ventur. 2015, 30, 775–792. [Google Scholar] [CrossRef]

- Tian, F. Research on the development status of small and micro enterprises. Res. World 2015, 128, 7–10. [Google Scholar]

- Zhu, M.F. Analysis of the factors influencing farmers’ entrepreneurial behavior: The case of Hangzhou, Zhejiang. China Rural Econ. 2010, 26, 25–34. [Google Scholar]

- Zhao, P.F.; Wang, H.J.; Zhao, X. A study on the differential impact of human capital on urban and rural household entrepreneurship--an empirical analysis based on CHFS survey data. Popul. Econ. 2015, 36, 89–97. [Google Scholar]

- Ju, Q. The impact of household wealth on entrepreneurial decisions—A study based on CFPS data in 2018. Res. Financ. Econ. 2020, 66–74. [Google Scholar]

- Wang, W.; Xian, J.K. Population aging and family entrepreneurship decisions. China Popul. Sci. 2020, 34, 113–125, 128. [Google Scholar]

- Cai, L.; Shan, B.A. Entrepreneurship research in the Chinese context: A review and outlook. Manag. World 2013, 29, 160–169. [Google Scholar]

- Zhu, H.G.; Kang, L.Y. Financial environment, policy support and farmers’ willingness to start a business. China Rural Obs. 2013, 5, 24–33, 95–96. [Google Scholar]

- DeTienne, D.R. Entrepreneurial exit as a critical component of the entrepreneurial process: Theoretical development. J. Bus. Ventur. 2010, 25, 203–215. [Google Scholar] [CrossRef]

- Yang, C.; He, S.; Zhu, L.; Wang, B.L. Vertical pay gap and innovation spirit of start-up companies. Financ. Econ. Res. 2017, 43, 32–44, 69. [Google Scholar]

- DeTienne, D.R.; Chirico, F. Exit Strategies in Family Firms: How Socioemotional Wealth Drives the Threshold of Performance. Entrep. Theory Pract. 2013, 37, 1297–1318. [Google Scholar] [CrossRef]

- Kato, M.; Honjo, Y. Entrepreneurial Human Capital and the Survival of New Firms in High- and Low-Tech Sectors. J. Evol. Econ. 2015, 25, 925–957. [Google Scholar] [CrossRef]

- Rocha, V.A.; Carneiro, A.; Varum, C.A. Entry and Exit Dynamics of Nascent Business Owners. Small Bus. Econ. 2015, 45, 63–84. [Google Scholar] [CrossRef]

- Shane, S. A General Theory of Entrepreneurship: The Individual-Opportunity Nexus; Edward Elgar Publishing: Cheltenham, UK, 2003. [Google Scholar]

- Huang, X.Y.; Du, D.B.; Yang, W.L. A preliminary investigation on the clustering characteristics and location factors of Internet entrepreneurship in China. Scientol. Res. 2018, 36, 493–501. [Google Scholar]

- Zhang, F.; Li, D. Regional ICT access and entrepreneurship: Evidence from China. Inf. Manag. 2018, 55, 188–198. [Google Scholar] [CrossRef]

- Yang, X.R.; Zou, B.L. Imitation or Innovation: An Empirical Study on Identifying Entrepreneurial Opportunities for New Generation Migrant Workers in the Internet Era. Acad. Res. 2018, 61, 77–83. [Google Scholar]

- Zhang, X.; Wan, G.H.; Zhang, J.J.; He, Z.Y. Digital Economy, Inclusive Finance and Inclusive Growth. Econ. Res. 2019, 54, 71–86. [Google Scholar]

- Yao, Z.; Luo, J.L.; Zhang, X.C.; Zhang, L.L. Internet embedding, dual entrepreneurial learning and farmers’ entrepreneurial performance. Scientol. Res. 2020, 38, 685–695. [Google Scholar]

- Jenkins, A.; Mckelvie, A. What is Entrepreneurial Failure? Implications for Future Research. Int. Small Bus. J. 2016, 34, 176–188. [Google Scholar] [CrossRef]

- Yang, J.; Zhang, Y.L. The construction of a theoretical model of social capital, entrepreneurial opportunities and initial entrepreneurial performance and the formulation of related research propositions. Foreign Econ. Manag. 2008, 30, 17–24. [Google Scholar]

- Porter, M.; Li, M.X. National Competitive Advantage; Huaxia Publishing House: Beijing, China, 2002; pp. 70–79. [Google Scholar]

- Yuan, F.; Zhong, T.; Qiu, W.N.; Shi, Q.H. The exit of peasant families returning to their hometown to start a business: An empirical study based on the experience of working outside and the configuration of decision-making power. Yunnan Soc. Sci. 2021, 101–109. [Google Scholar]

- Ge, B.S.; Wang, H.Y. Research on resource integration, entrepreneurial learning and innovation. South. Econ. 2017, 35, 57–70. [Google Scholar]

- Shi, J.C.; Wang, W.W. The impact of Internet use on entrepreneurial behavior--an empirical study based on micro data. J. Zhejiang Univ. (Humanit. Soc. Sci. Ed.) 2017, 47, 159–175. [Google Scholar]

- Wang, J.J.; Li, Q.H. Multidimensional Education and Entrepreneurial Choice of Rural Residents in E-Commerce Environment—An Empirical Analysis Based on CFPS2014 and CHIPS2013 Data of Rural Residents. Nankai Econ. Res. 2017, 33, 75–92. [Google Scholar]

- He, J.; Li, Q.H. Digital Financial Use and Farmers’ Entrepreneurial Behavior. China Rural. Econ. 2019, 35, 112–126. [Google Scholar]

- Yang, J.; Zhang, Y.L. Analysis of entrepreneurial behavior process based on entrepreneurial resource endowment. Foreign Econ. Manag. 2004, 26, 2–6. [Google Scholar]

- Guo, X.B. A study of three-dimensional entrepreneurial capital of entrepreneurs. J. Northwest Agric. For. Univ. Sci. Technol. (Soc. Sci. Ed.) 2014, 14, 110–116. [Google Scholar]

- Burt, R.S. The Gender of Social Capital. Ration. Soc. 1998, 10, 5–46. [Google Scholar] [CrossRef]

- Granovetter, M.S. The Strength of Weak Ties. Am. J. Sociol. 1973, 78, 1360–1380. [Google Scholar] [CrossRef]

- Wang, Z.M. Internet, social networks and employment income of rural migrant population. J. Dalian Univ. Technol. (Soc. Sci. Ed.) 2019, 40, 15–23. [Google Scholar]

- Zhu, X.M.; Li, M.F. The dynamic impact of entrepreneurial network characteristics on resource acquisition-evidence based on China’s transition economy. Manag. World. 2011, 6, 105–115, 188. [Google Scholar]

- Liu, Y.G.; Wang, X.D.; Yin, M.M.; Dong, C. A study on the influence of Internet embedding on the resource acquisition behavior of entrepreneurial teams—the mediating role of entrepreneurial learning. Scientol. Res. 2016, 34, 916–922. [Google Scholar]

- Liu, Z.Y.; Liu, S.T.; Liu, Z.H. Does depression affect entrepreneurial exit—micro evidence from Chinese farmer entrepreneurs. Nankai Manag. Rev. 2022, 25, 92–106. [Google Scholar]

- Song, Q.Y.; Wu, Y.; Yin, Z.C. Financial literacy and the survival of family entrepreneurship. Res. Manag. 2020, 41, 133–142. [Google Scholar]

- He, X.G. Entrepreneurial Competence and Firm Growth: An Extended Model of Competence Theory. Sci. Technol. Prog. Countermeas. 2006, 123, 45–48. [Google Scholar]

- Dimaggio, P.; Bonikowski, B. Make Money Surfing the Web? The Impact of Internet Use on The Earnings of U.S. Workers. Am. Sociol. Rev. 2008, 73, 227–250. [Google Scholar] [CrossRef] [Green Version]

- Zheng, Q.H.; Lai, D.S. A study of regional differences in human capital and urbanization in China. China Popul. Sci. 2008, 22, 59–66, 96. [Google Scholar]

- Bauernschuster, S.; Falck, O.; Woessmann, L. Surfing Alone? The Internet and Social Capital: Evidence from an Unforeseeable Technological Mistake. J. Public Econ. 2014, 117, 73–89. [Google Scholar] [CrossRef]

- Qin, F.; Wang, W.C.; He, J.C. The impact of financial literacy on commercial insurance participation—An empirical analysis from China Household Financial Survey (CHFS) data. Financ. Res. 2016, 59, 143–158. [Google Scholar]

- Bae, K.H.; Ozoguz, A.; Tan, H.; Wirjanto, T.S. Do Foreigners Facilitate Information Transmission in Emerging Markets? J. Financ. Econ. 2012, 105, 209–227. [Google Scholar] [CrossRef]

- Mao, Y.F.; Zeng, X.Q.; Zhu, H.L. Internet use, employment decisions and employment quality—Empirical evidence based on CGSS data. Econ. Theory Econ. Manag. 2019, 38, 72–85. [Google Scholar]

- Zhang, X.; Wan, G.H.; Wu, H.T. Bridging the Digital Divide: Digital Financial Development with Chinese Characteristics. China Soc. Sci. 2021, 42, 35–51, 204–205. [Google Scholar]

- Stiglitz, J.E. Capital Market Liberalization, Economic Growth, and Instability. World Dev. 2000, 28, 1075–1086. [Google Scholar] [CrossRef]

- Janson, M.A.; Wrycza, S. Information Technology and Entrepreneurship: Three Cases from Poland. Int. J. Inf. Manag. 1999, 19, 351–367. [Google Scholar] [CrossRef]

- Mostafa, R.H.A.; Wheeler, C.; Jones, M. Entrepreneurial orientation, commitment to the Internet and export performance in small and medium sized exporting firms. J. Int. Entrep. 2005, 3, 291–302. [Google Scholar] [CrossRef]

- Batjargal, B. Internet Entrepreneurship: Social Capital, Human Capital, and Performance of Internet Ventures in China. Res. Policy 2007, 36, 605–618. [Google Scholar] [CrossRef]

{kind=link}

| Variable Name (Abbreviation) | Dummy Variable Definition | Average Value | Standard Deviation | Sample Size |

|---|---|---|---|---|

| Passive entrepreneurial exit | Passive Entrepreneurial Exit = 0, Entrepreneurial Continuity and Active Entrepreneurial Exit = 1 | 0.418 | 0.493 | 1767 |

| Digital technology use | Using a computer or smartphone = 1, otherwise = 0 | 0.720 | 0.449 | 1767 |

| Age | Unit: years | 51.339 | 11.141 | 1767 |

| Age squared | Age × age/100 | 27.597 | 11.947 | 1767 |

| Health | Normal and above = 1; otherwise 0 | 0.853 | 0.354 | 1767 |

| Gender | Male = 1, Female = 0 | 0.918 | 0.274 | 1767 |

| Education level | Unschooled = 1, PhD = 9 | 2.800 | 0.972 | 1767 |

| Party members | Yes = 1, No = 0 | 0.123 | 0.329 | 1767 |

| Marriage | Married, remarried = 1, otherwise = 0 | 0.957 | 0.202 | 1767 |

| Business insurance | With commercial insurance = 1, otherwise = 0 | 0.585 | 0.493 | 1767 |

| Family size | Number of family members | 3.602 | 2.276 | 1767 |

| Parent is the head of the unit or more | Yes = 1, No = 0 | 0.013 | 0.116 | 1767 |

| Fixed deposit | Take logarithm | 1.265 | 3.470 | 1767 |

| Income other than business and industry | Total revenue-business and industry revenue | 8.387 | 4.230 | 1767 |

| Variables | (1) | (2) | (3) |

|---|---|---|---|

| Digital technology use | −0.449 ** (0.067) | −0.382 *** (0.072) | −0.389 *** (0.072) |

| Age | −0.019 (0.019) | −0.022 (0.019) | |

| Age squared | 0.001 (0.001) | 0.001 (0.001) | |

| Health | −0.068 (0.088) | −0.0589 (0.088) | |

| Gender | 0.092 (0.114) | 0.083 (0.115) | |

| Education level | −0.089 ** (0.035) | −0.085 ** (0.035) | |

| Party Members | −0.018 (0.096) | −0.020 (0.097) | |

| Marriage | −0.203 (0.160) | −0.221 (0.159) | |

| Business Insurance | 0.080 (0.01) | −0.070 (0.102) | |

| Family size | 0.49 *** (0.018) | ||

| Parent is the head of the unit or more | −0.042 (0.259) | ||

| Fixed Deposit | −0.024 *** (0.009) | ||

| Income other than business and industry | 0.011 (0.007) | ||

| Year Characteristics | Control | Control | Control |

| R-squared | 0.019 | 0.025 | 0.033 |

| Observations | 1767 | 1767 | 1767 |

| Variables | (1) | (2) | (3) |

|---|---|---|---|

| Explained Variables of the First Stage Model: Whether to Use Digital Technology | |||

| Average network communication costs in villages | 0.177 *** (0.026) | 0.167 *** (0.025) | 0.167 *** (0.025) |

| Householder characteristics | Control | Control | |

| Family Characteristics | Control | ||

| Variables | Explained variables of the second stage model: passive entrepreneurial exit | ||

| Digital technology use | −1.163 *** (0.229) | −1.092 *** (0.261) | −1.147 *** (0.262) |

| Householder characteristics | Control | Control | |

| Family Characteristics | Control | ||

| atanhrho_12 | 0.482 ** | 0.346 *** | 0.373 *** |

| R-squared | 0.019 | 0.148 | 0.151 |

| Observations | 1767 | 1767 | 1767 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| Digital technology use | −0.726 *** (0.107) | −0.610 *** (0.116) | −0.618 *** (0.116) | −0.414 *** (0.076) | −0.324 *** (0.082) | −0.332 *** (0.083) |

| Householder characteristics | Control | Control | Control | Control | ||

| Family Characteristics | Control | Control | ||||

| R-squared | 0.019 | 0.025 | 0.032 | 0.016 | 0.025 | 0.031 |

| Observations | 1767 | 1767 | 1767 | 1328 | 1328 | 1328 |

| Variables | Heckman Model | |

|---|---|---|

| Select Equation (to Enter or Not) | Exit Equation (Whether to Exit) | |

| Digital technology use | - | −0.156 *** (0.029) |

| Individual Characteristics | Control | Control |

| Family Characteristics | Control | Control |

| Observations | 17,405 | 1767 |

| Insigma | −0.701 | |

| Sigma | 0.493 | |

| Prob > chi2 | 55.35 *** | |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| Digital technology use | 1.033 *** (0.148) | 0.611 *** (0.148) | 0.321 *** (0.031) | 0.262 *** (0.034) | 1.341 *** (0.219) | 0.851 *** (0.238) |

| Control variables | Control | Control | Control | |||

| R-squared | 0.033 | 0.129 | 0.051 | 0.093 | 0.021 | 0.050 |

| Observations | 1767 | 1767 | 1767 | 1767 | 1767 | 1767 |

| Variables | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| Low | High | Low | High | |

| Digital technology use | −0.347 *** (0.119) | −0.520 *** (0.129) | −0.328 *** (0.097) | −0.435 *** (0.112) |

| Control variables | Control | Control | Control | Control |

| R-squared | 0.033 | 0.049 | 0.0391 | 0.0355 |

| Observations | 698 | 596 | 881 | 886 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, Y.; Cai, Z.; Wang, J. The Impact of Digital Technology Use on Passive Entrepreneurial Exit in Rural Households: Empirical Evidence from China. Sustainability 2022, 14, 10662. https://doi.org/10.3390/su141710662

Wang Y, Cai Z, Wang J. The Impact of Digital Technology Use on Passive Entrepreneurial Exit in Rural Households: Empirical Evidence from China. Sustainability. 2022; 14(17):10662. https://doi.org/10.3390/su141710662

Chicago/Turabian StyleWang, Yiran, Zhijian Cai, and Jie Wang. 2022. "The Impact of Digital Technology Use on Passive Entrepreneurial Exit in Rural Households: Empirical Evidence from China" Sustainability 14, no. 17: 10662. https://doi.org/10.3390/su141710662

APA StyleWang, Y., Cai, Z., & Wang, J. (2022). The Impact of Digital Technology Use on Passive Entrepreneurial Exit in Rural Households: Empirical Evidence from China. Sustainability, 14(17), 10662. https://doi.org/10.3390/su141710662