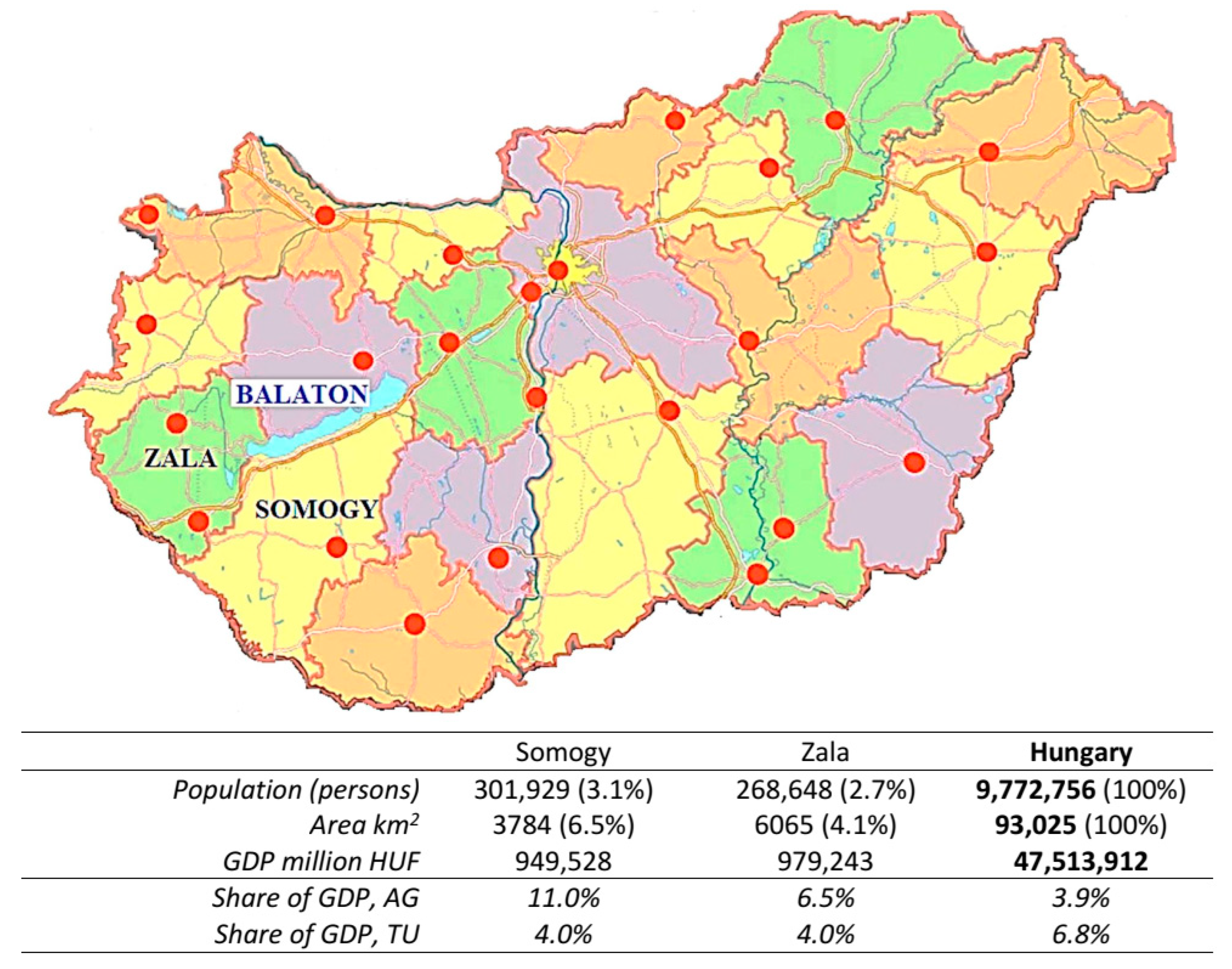

3.4. Annual Patterns of Total Assets, Labour Force, Sales Revenues, and Productivity

To evaluate annual tendencies in more detail, mean values were computed separately for industries. The trends of annual means are clearly different for the two sectors with regard to labour force, total assets, sales revenues, and labour productivity, but TFP has no clearly distinguishable pattern. This is reflected by the regression lines fitted to the annual mean values, the parameters of which are presented in

Figure 4.

As is shown in

Figure 4, total assets show an increasing trend in agriculture; while in tourism it does not show any change by time, the two industries are clearly different in their annual mean values. Annual mean sales revenues show an increasing trend in both industries, but agriculture has about three times as high values as tourism. The same pattern holds for labour productivity.

The annual mean labour force levels show definite decreasing patterns in both industries, agriculture starting from a higher value in 2008 than tourism. The decreasing trend in agriculture is much faster than in tourism, and the employment levels of the two industries converge to a nearly equal level by 2019. In TFP, no clear trend can be identified. TFP values are dispersed between 0.8 and 1.1 except for 2011, when they are between 1.1 and 1.25. No clear tendency can be seen comparing the industries; during the 16 years, tourism has higher means in 6 years and agriculture in 10 years.

Fitting a regression line to the overall values, the R2 values, indicating goodness of fit, are quite high for both industries and all indicators except for TFP, where the small R2 and the very small slope in the regression equation indicate the lack of any identifiable time pattern. Negative slopes for labour force, and positive slopes for total assets and sales revenues suggest that increasing labour productivity is as much the result of using more technological resources as employing less human resources. We must note that total assets and sales are measured at current price levels not corrected for inflation, thus the annual growth rates during 2004–2019 of about 3% include the average annual inflation rate of 2.58% during these years.

3.5. Results of the Panel Analysis

The analysis of annual means indicates that tourism and agriculture possess clearly different characteristics. However, the means fail to grasp the fact that the annual samples are not independent, but contain the same firms, allowing panel regression analysis to distinguish fixed effects from random effects (if any). Therefore, a more detailed panel analysis is carried out.

Total assets, labour force, sales revenues, labour productivity, and TFP (z-score transformed values) were analysed with industry, county, and year as independent variables. The size categories and total asset values (except for TA as the dependent variable) were also included, together with the random effects of year in the analysis. Industry effects—either by themselves, or in interaction with time—were found to have significant fixed effects, except for z-TFP as dependent variable. The random effects of year were also significant (

Table 5).

Looking at the actual effects in more detail, the analysis results are shown in

Table 5 giving the actual estimates of fixed effects and random effect variances.

Industry-fixed effects are significant for z-SR and z-LP and the industry and year interactions are significant for z-TA and z-LF. Thus the industries differ in their total assets, sales revenues, labour force, and labour productivity, but not in TFP. The earlier found differences in TFP are more the results of subject-specific differences, than industry-specific traits. The fixed effect of counties is significant for all dependent variables, except TFP. Year has a significant fixed effect on all indicators except z-TA, but its impact is significant for total assets in interaction with industry, i.e., the time slope of agriculture is positive, differing from the zero slope of tourism. County–year interactions are not significant for any dependent variable, meaning that the time slopes for the same groups of firms are the same in both counties.

Looking at the variables of size categories, all these categories significantly differ in their fixed effects on total assets, sales revenues, and labour force, but regarding labour productivity, the two largest categories do not differ, and for TFP, none of the size categories differ.

The random effects variances of the year are also significant, although rather small compared to any of the fixed effects, and especially to the residual variances, which measure the variances caused by factors not included in our models. The model fits, i.e., the R2 values between the observed and the predicted values, are reasonably good, with the smallest value found for z-TFP (0.449), while for the other dependent variables, it is between 0.648 and 0.769.

To make the parameters easier to interpret, a summary table is presented describing individual fixed effects for each county, industry, and size combination (

Table 6). The individual fixed effect parameters are computed by using the baseline value and adding the relevant estimate for the specific group when it is significant. The baseline group is Z-Year = 0 − TU-S4, i.e., county Zala in 2004, tourism industry, and large firms; and all parameters in

Table 5 give the difference to this baseline group.

Therefore, the actual equations describing the fixed effects for the county industry-size groups and years are of the following structure, with relevant parameter values given in

Table 6.

The different parameters clearly show that industries differ in their initial value from 2004 (see the Const column), or in their time dependence (column of slopeYr), and by their size-related traits, too. The exception is TFP, where no significant difference was found in any of these aspects, i.e., neither county, nor industry, nor size, showed any significant impact, only time had a small positive effect on its evolution.

Altogether we may conclude that tourism and agriculture considerably differ regarding total assets, sales revenues, and labour productivity, while spatial differences also influence these indicators. Industries, however, show different growth rates by time with regard to employment. Regarding the effects of size, smaller firms have less assets and lower sales revenues, but higher labour productivities in both industries.

Employment shows a decreasing pattern in time, but the decrease is about 50% faster in agriculture than in tourism, so, starting from a much higher employment rate at the beginning of the time period, agricultural firms end up with no more workforce on average in 2019 than tourism firms. At the same time, total assets in tourism do not increase by time, while there is a moderate increase in agriculture. Regarding revenues, both industries show the same increase by time, but initial differences in the advantage of agriculture prevail throughout the analysed time period. As agriculture firms reflect rising total assets and decreasing labour force, this indicates an increasing level of mechanisation and exchange of human inputs for fixed assets. This trend does not exist in tourism, where, being a service industry, the delivered product depends crucially on personalised human contributions. Therefore, there is much less of a chance of swapping labour for technology. Looking at the productivity indicators, labour productivity increases in time at the same rate in tourism and agriculture, but agriculture has an initial better position, therefore its advantage is kept throughout the years. However, this is not so in TFP, where practically no difference can be identified between the two sectors. With better labour productivity in agriculture, it means that capital assets—although of lower values than in agriculture—are used more productively in tourism. Another (not surprising) finding is that higher asset levels are beneficial for sales revenues and labour productivity, and allow for employing more labour; but contrary to the general assumptions, they have no impact on total factor productivity—i.e., increasing total assets does not necessarily mean investment in more productive technology in these two sectors.

Finally, firm sizes also impact firm performance in all aspects (total assets, sales revenues, labour force, and labour productivity) except TFP, and micro and small firms turned out to be more labour efficient, in spite of having less assets, less staff, and less sales revenues. As TFP did not show any difference in size, this means that by their higher labour productivity, small firms can compensate for their lower capital assets and less resources. Thus, returning to our original research questions, the following answers can be given:

The research focused on five questions and proved the following:

Regarding the composition of firms by size and temporal changes, our findings show that in both industries, the micro-enterprises dominate the industrial structure, and their share increases with time.

Regarding the relationship of firm performance (productivity) and firm size, we can state that labour productivity is higher in micro-enterprises than in larger ones, while TFP does not show any difference with regard to firm size. There is a slight improvement by time, but its speed is similar in both industries and all the four size categories.

Regarding differences of size and performance in different geographical areas, our results show that labour productivity is somewhat better in Zala than in Somogy, both in tourism and in agriculture. The labour force is also somewhat higher in Zala, having higher values than Somogy, and both counties showing a decreasing trend with time. However, regarding TFP, the two countries show no difference. The total asset levels and sales revenues are also higher in Zala than in Somogy, and in agriculture, both assets and sales increase with time—the speed is the same in both counties. However, in tourism, neither county shows any increase in assets, but both show the same pattern in both industries. Regarding TFP, the two counties show no difference at all.

Temporal changes were discussed above. It is worth pointing out that while labour force decreases with time, all the other indicators show positive changes.

Differences between the two industries were also mentioned above, and, as a summary, we can say that except for TFP, the two industries considerably differ. Regarding sales revenues and labour productivity, the two industries differ in their mean levels, and regarding total assets and labour force, they differ by the rate of temporal change, with tourism changing slower than agriculture.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}