Do Green Banking Activities Improve the Banks’ Environmental Performance? The Mediating Effect of Green Financing

Abstract

:1. Introduction

2. Literature Review and Hypotheses Development

2.1. Green Banking

2.2. Green Banking Initiatives in Bangladesh

2.3. Green Finance

2.4. Environmental Performance

2.5. Research Hypotheses

2.6. Challenges and Benefits of Green Banking Development

3. Research Methods

3.1. Study Sample and Data Collection

3.2. Survey Instrument

3.3. Data Analysis Technique

4. Results and Findings

4.1. Descriptive Statistics

4.2. Discriminant Validity

4.3. Measurement Model of the Study

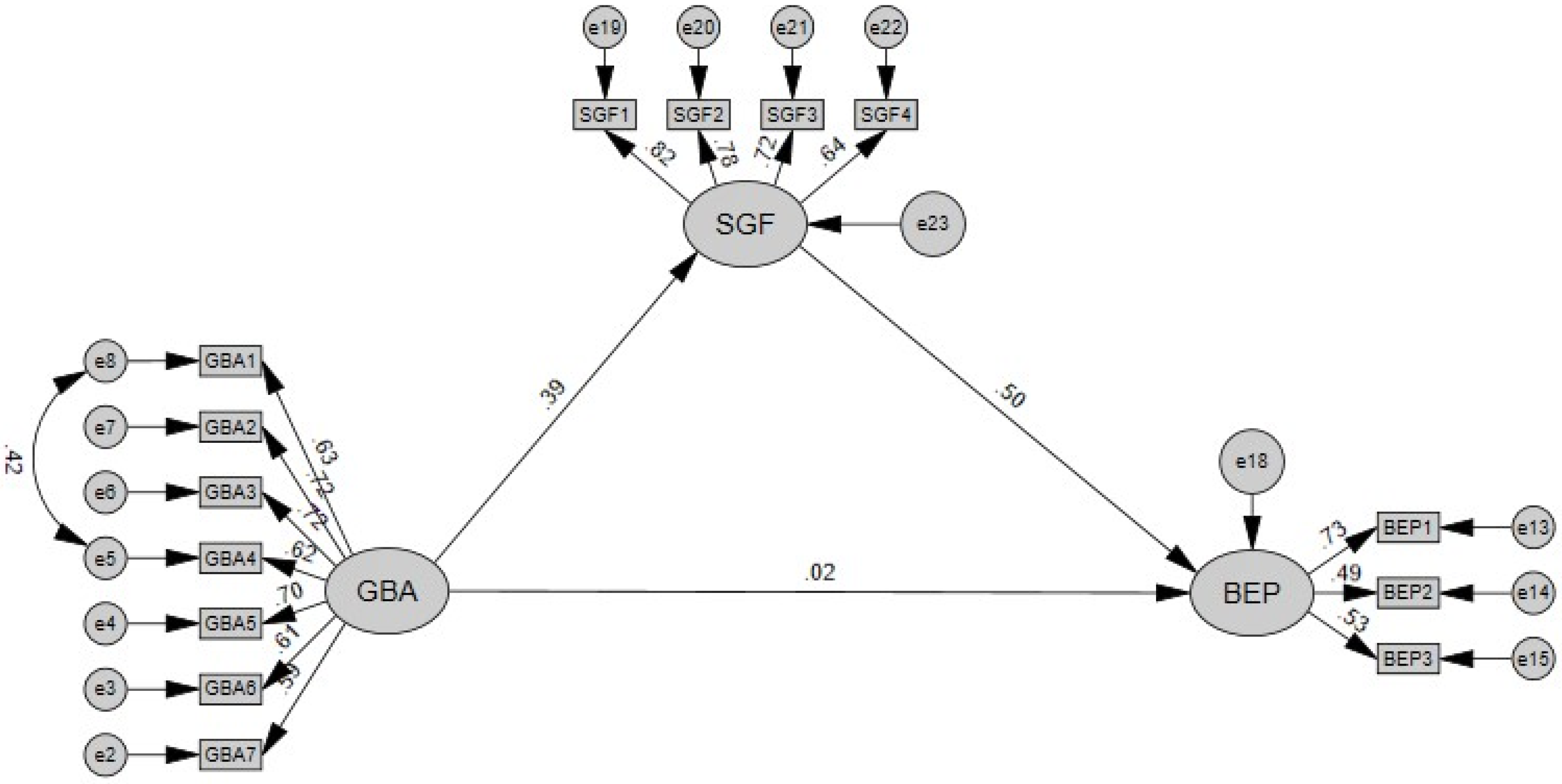

4.4. Structural Model of the Study

4.5. Test of Research Hypotheses

4.6. Major Challenges of the Green Banking Implementation in Bangladesh

4.7. Major Benefits of Green Banking

5. Discussion and Conclusions

6. Managerial Implications of the Study

7. Study Limitations and Future Directions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Model Fit Indices | Measurement Model | Structural Model | Standard Value |

|---|---|---|---|

| χ²/df | 2.357 | 1.675 | <0.05 |

| p-value | 0.000 | 0.000 | *** p < 0.001 |

| SRMR | 0.068 | 0.068 | <0.08 |

| GFI | 0.931 | 0.953 | >0.900 |

| AGFI | 0.902 | 0.932 | >0.900 |

| RMSEA | 0.062 | 0.044 | <0.08 |

| CFI | 0.936 | 0.969 | >0.900 |

| IFI | 0.937 | 0.961 | >0.900 |

| TLI | 0.921 | 0.969 | >0.900 |

References

- Zheng, G.W.; Siddik, A.B.; Masukujjaman, M.; Fatema, N.; Alam, S.S. Green finance development in Bangladesh: The role of private commercial banks (PCBs). Sustainability 2021, 13, 795. [Google Scholar] [CrossRef]

- Nawaz, M.A.; Seshadri, U.; Kumar, P.; Aqdas, R.; Patwary, A.K.; Riaz, M. Nexus between green finance and climate change mitigation in N-11 and BRICS countries: Empirical estimation through difference in differences (DID) approach. Environ. Sci. Pollut. Res. 2020, 28, 6504–6519. [Google Scholar] [CrossRef]

- Khairunnessa, F.; Vazquez-Brust, D.A.; Yakovleva, N. A Review of the Recent Developments of Green Banking in Bangladesh. Sustainability 2021, 13, 1904. [Google Scholar] [CrossRef]

- Zhixia, C.; Hossen, M.M.; Muzafary, S.S.; Begum, M. Green banking for environmental sustainability-present status and future agenda: Experience from Bangladesh. Asian Econ. Financ. Rev. 2018, 8, 571–585. [Google Scholar] [CrossRef] [Green Version]

- Akter, N.; Siddik, A.B.; Mondal, M.S.A. Sustainability Reporting on Green Financing: A Study of Listed Private Sustainability Reporting on Green Financing: A Study of Listed Private Commercial Banks in Bangladesh. J. Bus. Technol. 2018, XII, 14–27. [Google Scholar]

- Julia, T.; Kassim, S.; Julia, T. Exploring green banking performance of Islamic banks vs conventional banks in Bangladesh based on Maqasid Shariah framework. J. Islam. Mark. 2019, 11, 729–744. [Google Scholar] [CrossRef]

- Hoque, N.; Mowla, M.M.; Uddin, M.S.; Mamun, A.; Uddin, M.R. Green Banking Practices in Bangladesh: A Critical Investigation. Int. J. Econ. Financ. 2019, 11, 58. [Google Scholar] [CrossRef]

- Hossain, M. Green Finance in Bangladesh Barriers and Solutions. In Handbook of Green Finance, Sustainable Development; Springer: Berlin/Heidelberg, Germany, 2019; pp. 1–26. [Google Scholar]

- Rehman, A.; Ullah, I.; Afridi, F.-A.; Ullah, Z.; Zeeshan, M.; Hussain, A.; Rahman, H.U. Adoption of green banking practices and environmental performance in Pakistan: A demonstration of structural equation modelling. Environ. Dev. Sustain. 2021, 23, 13200–13220. [Google Scholar] [CrossRef]

- Masukujjaman, M.; Aktar, S. Green Banking in Bangladesh: A Commitment towards the Global Initiatives. J. Bus. Technol. 2014, 8, 17–40. [Google Scholar] [CrossRef] [Green Version]

- Islam, M.A. Green Banking and Its Potentiality & Practice in Bangladesh. Int. J. Sci. Res. Methodol. 2018, 10, 17–27. [Google Scholar] [CrossRef] [Green Version]

- Qureshi, H.; Hussain, T. Green Banking Products: Challenges and Issues in Islamic and Traditional Banks of Pakistan. J. Account. Financ. Emerg. Econ. 2020, 6, 703–712. [Google Scholar]

- Sharma, M.; Choubey, A. Green banking initiatives: A qualitative study on Indian banking sector. Environ. Dev. Sustain. 2021, 24, 293–319. [Google Scholar] [CrossRef] [PubMed]

- Miah, M.D.; Rahman, S.M.; Haque, M. Factors affecting environmental performance: Evidence from banking sector in Bangladesh. Int. J. Financ. Serv. Manag. 2018, 9, 22–38. [Google Scholar] [CrossRef]

- Ngwenya, N.; Simatele, M.D. The emergence of green bonds as an integral component of climate finance in South Africa. S. Afr. J. Sci. 2020, 116, 10–12. [Google Scholar] [CrossRef]

- Sarma, P.; Roy, A. A Scientometric analysis of literature on Green Banking (1995-March 2019). J. Sustain. Financ. Invest. 2020, 11, 142–162. [Google Scholar] [CrossRef]

- Sharmeen, K.; Hasan, R.; Miah, M.D. Underpinning the benefits of green banking: A comparative study between Islamic and conventional banks in Bangladesh. Thunderbird Int. Bus. Rev. 2019, 61, 735–744. [Google Scholar] [CrossRef]

- Bose, S.; Khan, H.Z.; Rashid, A.; Islam, S. What drives green banking disclosure? An institutional and corporate governance perspective. Asia Pac. J. Manag. 2018, 35, 501–527. [Google Scholar] [CrossRef]

- Bose, S.; Khan, H.Z.; Monem, R.M. Does green banking performance pay off? Evidence from a unique regulatory setting in Bangladesh. Corp. Gov. Int. Rev. 2020, 29, 162–187. [Google Scholar] [CrossRef]

- Kala, K.N.; Vidyakala, K. A Study on The Impact of Green Banking Practices on Bank ’ s Environmental Performance With Special Reference To Coimbatore City. Afr. J. Bus. Econ. Res. 2020, 15, 1–6. [Google Scholar] [CrossRef]

- Malsha, K.P.P.H.G.N.; Arulrajah, A.A.; Senthilnathan, S. Mediating role of employee green behaviour towards sustainability performance of banks. J. Gov. Regul. 2020, 9, 92–102. [Google Scholar] [CrossRef]

- Rifat, A.; Nisha, N.; Iqbal, M.; Suviitawat, A. The role of commercial banks in green banking adoption: A Bangladesh perspective. Int. J. Green Econ. 2016, 10, 226–251. [Google Scholar] [CrossRef]

- Tu, T.T.T.; Dung, N.T.P. Factors affecting green banking practices: Exploratory factor analysis on Vietnamese banks. J. Econ. Dev. 2017, 24, 4–30. [Google Scholar] [CrossRef]

- Srivastava, A. Green Banking: Support and Challenges. Int. Adv. Res. J. Sci. Eng. Technol. 2016, 3, 135–137. [Google Scholar] [CrossRef]

- Raihan, M.Z.; Khan, M.S.U. Sustainable Finance—A Prerequisite for Growth & Development of Banking Industry in Bangladesh. In Proceedings of the Finance for Sustainable Growth and Development; Department of Finance, Faculty of Business Administration, University of Chittagong: Chittagong, Bangladesh, 2018; pp. 29–49. Available online: https://mijst.mist.ac.bd/mijst/index.php/mijst/article/view/135 (accessed on 1 December 2021).

- Risal, N.; Joshi, S.K. Measuring Green Banking Practices on Bank’s Environmental Performance: Empirical Evidence from Kathmandu valley. J. Bus. Soc. Sci. 2018, 2, 44–56. [Google Scholar] [CrossRef]

- Shaumya, S.; Arulrajah, A. The Impact of Green Banking Practices on Bank’s Environmental Performance: Evidence from Sri Lanka. J. Financ. Bank Manag. 2017, 5, 77–90. [Google Scholar] [CrossRef] [Green Version]

- Yadav, R.; Pathak, G.S. Environmental Sustainability through Green Banking: A Study on Private and Public Sector Banks in India. OIDA Int. J. Sustain. Dev. 2013, 6, 37–48. [Google Scholar]

- Hossain, M.A.; Rahman, M.M.; Hossain, M.S.; Karim, M.R. The Effects of Green Banking Practices on Financial Performance of Listed Banking Companies in Bangladesh. Can. J. Bus. Inf. Stud. 2020, 2, 120–128. [Google Scholar] [CrossRef]

- Shakil, M.H.; Azam, M.K.G.; Tasnia, M.; Munim, Z.H. An Evaluation of Green Banking Practices in Bangladesh. IOSR J. Bus. Manag. 2014, 16, 67–73. [Google Scholar] [CrossRef]

- Rahman, M.M.; Ahsan, M.A.; Hossain, M.M.; Hoq, M.R. Green Banking Prospects in Bangladesh. Asian Bus. Rev. 2015, 2, 59. [Google Scholar] [CrossRef] [Green Version]

- Dörry, S.; Schulz, C. Green financing, interrupted. Potential directions for sustainable finance in Luxembourg. Local Environ. 2018, 23, 717–733. [Google Scholar] [CrossRef]

- Liu, N.; Liu, C.; Xia, Y.; Ren, Y.; Liang, J. Examining the coordination between green finance and green economy aiming for sustainable development: A case study of China. Sustainability 2020, 12, 3717. [Google Scholar] [CrossRef]

- Rawat, S.K. Recent Advances in Green Finance. Int. J. Recent Technol. Eng. 2020, 8, 5528–5533. [Google Scholar] [CrossRef]

- Wang, C.; Li, X.; Wen, H.; Nie, P. Order financing for promoting green transition. J. Clean. Prod. 2021, 283, 125415. [Google Scholar] [CrossRef]

- Zhou, X.; Tang, X.; Zhang, R. Impact of green finance on economic development and environmental quality: A study based on provincial panel data from China. Environ. Sci. Pollut. Res. 2020, 27, 19915–19932. [Google Scholar] [CrossRef] [PubMed]

- Wang, Y.; Zhi, Q. The Role of Green Finance in Environmental Protection: Two Aspects of Market Mechanism and Policies. Energy Procedia 2016, 104, 311–316. [Google Scholar] [CrossRef]

- Zheng, G.; Siddik, A.B.; Masukujjaman, M.; Fatema, N. Factors Affecting the Sustainability Performance of Financial Institutions in Bangladesh: The Role of Green Finance. Sustainability 2021, 13, 10165. [Google Scholar] [CrossRef]

- Klassen, R.D.; Whybark, D.C. The Impact of Environmental Technologies on Manufacturing Performance. Acad. Manag. J. 1999, 42, 599–615. [Google Scholar] [CrossRef]

- Zhu, Q.; Geng, Y.; Fujita, T.; Hashimoto, S. Green supply chain management in leading manufacturers. Manag. Res. Rev. 2010, 33, 380–392. [Google Scholar] [CrossRef]

- Nie, P.-Y.; Wang, C.; Wen, H.-X. Optimal tax selection under monopoly: Emission tax vs carbon tax. Environ. Sci. Pollut. Res. 2021. [Google Scholar] [CrossRef] [PubMed]

- Tung, A.; Baird, K.; Schoch, H. The relationship between organisational factors and the effectiveness of environmental management. J. Environ. Manag. 2014, 144, 186–196. [Google Scholar] [CrossRef]

- Li, S.; Liu, X.; Wang, C. The influence of internet finance on the sustainable development of the financial ecosystem in China. Sustainability 2020, 12, 2365. [Google Scholar] [CrossRef] [Green Version]

- Qi, G.Y.; Zeng, S.X.; Shi, J.J.; Meng, X.H.; Lin, H.; Yang, Q.X. Revisiting the relationship between environmental and financial performance in Chinese industry. J. Environ. Manag. 2014, 145, 349–356. [Google Scholar] [CrossRef]

- Jayadatta, S.; Nitin, S.N. Opportunities, Challenges, Initiatives and Avenues for Green Banking in India. Int. J. Bus. Manag. Invent. 2017, 6, 10–15. [Google Scholar]

- Dörnyei, Z. Research Methods in Applied Linguistics; Oxford University Press: New York, NY, USA, 2007. [Google Scholar]

- Zheng, G.W.; Siddik, A.B.; Masukujjaman, M.; Alam, S.S.; Akter, A. Perceived environmental responsibilities and green buying behavior: The mediating effect of attitude. Sustainability 2021, 13, 35. [Google Scholar] [CrossRef]

- Yan, C.; Siddik, A.B.; Akter, N.; Dong, Q. Factors influencing the adoption intention of using mobile financial service during the COVID-19 pandemic: The role of FinTech. Environ. Sci. Pollut. Res. 2021. [Google Scholar] [CrossRef]

- Barclay, M.J. The Determinants of Corporate Leverage and Dividend Policies. J. Appl. Corp. Financ. 1995, 7, 4–19. [Google Scholar] [CrossRef]

- Rahman, F.; Perves, M.M. Green Banking Activities in Bangladesh: An Analysis and Summary of Initiatives of Bangladesh Bank. Res. J. Financ. Account. 2016, 25, 1–9. [Google Scholar]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 4th ed.; Prentice Hall: Hoboken, NJ, USA, 2010. [Google Scholar]

- Gerbing, D.W.; Anderson, J.C. An updated paradigm for scale development incorporating unidimensionality and its assessment. J. Mark. Res. 1988, 25, 186–192. [Google Scholar] [CrossRef]

- Hu, L.T.; Bentler, P.M. Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Struct. Equ. Model. 1999, 6, 1–55. [Google Scholar] [CrossRef]

- Nunnally, J.; Bernstein, I. Psychometric Theory, 3rd ed.; McGraw-Hill: New York, NY, USA, 1994. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. J. Mark. Res. 1981, 18, 39. [Google Scholar] [CrossRef]

- Chin, W. The Partial Least Squares Approach to SEM chapter. Mod. Methods Bus. Res. 1998, 295, 295–336. [Google Scholar]

- Anderson, J.C.; Gerbing, D.W. Structural Equation Modeling in Practice: A Review and Recommended Two-Step Approach. Psychol. Bull. 1988, 103, 411–423. [Google Scholar] [CrossRef]

- Cortina, J.M. What is coefficient alpha? An examination of theory and applications. J. Appl. Psychol. 1993, 98, 98–104. [Google Scholar] [CrossRef]

| Guidelines of Green Banking | Year | References |

|---|---|---|

| 2011 | BRPD Circular No. 01/No.02 |

| 2012 | BRPD Circular No. 07 |

| 2014 | GBCSRD Circular No. 04 |

| 2015 | GBCSRD Circular No. 04/2015 |

| 2016 | SFD Circular No. 02 |

| 2017 | SFD Circular No. 02/ No. 04 |

| 2018 | SFD Circular No. 01 |

| 2019 | SFD Circular No. 01 |

| 2020 | SFD Circular Letter No. 05/2020 |

| Variable | Items | Frequency (N) | Percentage (%) |

|---|---|---|---|

| Gender | Male | 282 | 80.12 |

| Female | 70 | 19.88 | |

| Age (years) | 18–25 | 50 | 14.20 |

| 26–35 | 185 | 52.56 | |

| 36–45 | 80 | 22.73 | |

| 46 and Above | 37 | 10.52 | |

| Educational qualification | Bachelor | 94 | 26.71 |

| Masters | 240 | 68.18 | |

| PhD | 18 | 05.11 | |

| Working experience | Less than 2 years | 135 | 38.35 |

| 3 to 5 years | 185 | 52.56 | |

| Above 5 years | 32 | 09.09 |

| Item | Description | References |

|---|---|---|

| Green banking activities (GBA). | ||

| GBA1 | Introducing energy efficient systems, solutions and practices. | [5,9,26,27] |

| GBA2 | Introducing online banking facilities. | |

| GBA3 | Providing loans for ecofriendly projects. | |

| GBA4 | Organizing seminars and symposiums to promote ecofriendly practices. | |

| GBA5 | Establishment of more green branches. | |

| GBA6 | Reduction in paper consumption. | |

| GBA7 | Encouragement of customers to indulge in ecofriendly-banking activities such as online bill payment, remote deposit, and e-statements. | |

| Sources of green financing (SGF). | ||

| SGF1 | My bank has invested more on renewable energy sectors. | [1,5,8,38] |

| SGF2 | My bank has invested more on energy efficiency projects. | |

| SGF3 | My bank has invested more on recycling and recyclable products. | |

| SGF4 | My bank has invested more on waste management and other ecofriendly projects. | |

| Bank’s environmental performance (BEP). | ||

| BEP1 | Reducing energy consumptions. | [20,26,27] |

| BEP2 | Reducing carbon emissions. | |

| BEP3 | Providing green training to staff on energy and paper savings. | |

| Variables | Item | Mean | SD | CA (α) | EV | FL |

|---|---|---|---|---|---|---|

| Green banking activities (GBA) | GBA1 | 4.50 | 0.964 | 0.845 | 3.642 | 0.740 |

| GBA2 | 4.52 | 0.936 | 0.737 | |||

| GBA3 | 4.34 | 0.986 | 0.731 | |||

| GBA4 | 4.55 | 0.932 | 0.724 | |||

| GBA5 | 4.50 | 0.993 | 0.723 | |||

| GBA6 | 4.42 | 0.966 | 0.677 | |||

| GBA7 | 4.13 | 0.969 | 0.653 | |||

| Sources of green financing (SGF) | SGF1 | 3.63 | 1.192 | 0.823 | 2.619 | 0.858 |

| SGF2 | 3.86 | 1.137 | 0.850 | |||

| SGF3 | 3.72 | 1.214 | 0.812 | |||

| SGF4 | 3.95 | 1.116 | 0.686 | |||

| Bank’s environmental performance (BEP) | BEP1 | 3.39 | 1.244 | 0.831 | 1.671 | 0.765 |

| BEP2 | 3.51 | 1.344 | 0.722 | |||

| BEP3 | 2.52 | 1.534 | 0.707 |

| GBA | SGF | BEP | AVE | CR | |

|---|---|---|---|---|---|

| GBA | 0.634 | 0.402 | 0.965 | ||

| SGF | 0.168 | 0.739 | 0.546 | 0.827 | |

| BEP | 0.052 | 0.258 | 0.787 | 0.620 | 0.829 |

| Construct | Item No | SRW | S.E. | CR | p-Value |

|---|---|---|---|---|---|

| GBA → | GBA1 | 0.830 | 0.086 | 9.612 | *** |

| GBA → | GBA2 | 0.865 | 0.086 | 10.007 | *** |

| GBA → | GBA3 | 0.679 | 0.090 | 11.084 | *** |

| GBA → | GBA4 | 0.958 | 0.085 | 11.300 | *** |

| GBA → | GBA5 | 0.685 | * | * | |

| GBA → | GBA6 | 0.964 | 0.085 | 11.312 | *** |

| GBA → | GBA7 | 0.700 | 0.088 | 11.365 | *** |

| SGF → | SGF1 | 0.816 | * | * | |

| SGF → | SGF2 | 0.777 | 0.063 | 14.325 | *** |

| SGF → | SGF3 | 0.715 | 0.068 | 13.215 | *** |

| SGF → | SGF4 | 0.635 | 0.063 | 11.674 | *** |

| BEP → | BEP1 | 0.726 | * | * | |

| BEP → | BEP2 | 0.724 | 0.120 | 6.044 | *** |

| BEP → | BEP3 | 0.899 | 0.143 | 6.274 | *** |

| Hypotheses | Path | Standardized Estimate | p-Value | Decisions |

|---|---|---|---|---|

| H1 | GBA→BE P | 0.269 *** | 0.000 | Accepted |

| H2 | GBA→SGF | 0.389 *** | 0.000 | Accepted |

| H3 | SGF→BEP | 0.499 *** | 0.000 | Accepted |

| H4 | GBA→SGF→BEP | 0.194 *** | 0.000 | Full Mediation |

| SL | Challenges of GB | Mean | SD | Rank |

|---|---|---|---|---|

| 1 | Insufficient awareness of customers regarding GB. | 4.15 | 0.711 | 1 |

| 2 | High investment costs. | 4.15 | 0.784 | 2 |

| 3 | Technical obstacles | 4.14 | 0.822 | 3 |

| 4 | Lack of capable and well-trained staff in appraising green credits/ loans. | 4.11 | 0.844 | 4 |

| 5 | Difficulties and complexity in assessing green projects. | 4.09 | 0.835 | 5 |

| 6 | Diversification issues | 4.08 | 0.818 | 6 |

| 7 | Credit risks | 4.07 | 0.836 | 7 |

| 8 | Reduction in banks’ competitiveness in short terms | 4.06 | 0.807 | 8 |

| 9 | Operational self-insufficiency | 4.03 | 0.848 | 9 |

| 10 | Low demand for green credits/loans. | 3.98 | 0.846 | 10 |

| SL | Benefits of GB | Mean | SD | Rank |

|---|---|---|---|---|

| 1 | Increase in bank competitiveness. | 4.18 | 0.687 | 1 |

| 2 | Reduction in long term costs and expenses. | 4.16 | 0.854 | 2 |

| 3 | Provision of online banking facilities. | 4.15 | 0.711 | 3 |

| 4 | Improvement of customers’ goodwill. | 4.12 | 0.747 | 4 |

| 5 | Reduction in the carbon footprint. | 4.08 | 0.857 | 5 |

| 6 | Provision of environmental related benefits. | 4.07 | 0.789 | 6 |

| 7 | Conservation of energy. | 4.07 | 0.836 | 7 |

| 8 | Provision of ecofriendly products. | 4.07 | 0.849 | 8 |

| 9 | Contribution towards the attainment of a sustainable economic development of the country. | 4.06 | 0.852 | 9 |

| 10 | Higher profits for banks in long terms. | 4.03 | 0.716 | 10 |

| 11 | Tax advantages. | 4.01 | 0.801 | 11 |

| 12 | Economy in paper consumption. | 3.99 | 0.846 | 12 |

| 13 | Promotion of reputation. | 3.98 | 0.846 | 13 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, X.; Wang, Z.; Zhong, X.; Yang, S.; Siddik, A.B. Do Green Banking Activities Improve the Banks’ Environmental Performance? The Mediating Effect of Green Financing. Sustainability 2022, 14, 989. https://doi.org/10.3390/su14020989

Zhang X, Wang Z, Zhong X, Yang S, Siddik AB. Do Green Banking Activities Improve the Banks’ Environmental Performance? The Mediating Effect of Green Financing. Sustainability. 2022; 14(2):989. https://doi.org/10.3390/su14020989

Chicago/Turabian StyleZhang, Xin, Zhihui Wang, Xiaobing Zhong, Shouzhi Yang, and Abu Bakkar Siddik. 2022. "Do Green Banking Activities Improve the Banks’ Environmental Performance? The Mediating Effect of Green Financing" Sustainability 14, no. 2: 989. https://doi.org/10.3390/su14020989

APA StyleZhang, X., Wang, Z., Zhong, X., Yang, S., & Siddik, A. B. (2022). Do Green Banking Activities Improve the Banks’ Environmental Performance? The Mediating Effect of Green Financing. Sustainability, 14(2), 989. https://doi.org/10.3390/su14020989