3.1. Energy Consumption and Annual Bills

As stated in

Section 2.5, the tariff is used to calculate the energy bill. The total of 1–200 kWh tariff adds up to RM 87.00. Therefore, to ease the calculation method, and since all the bills are more than 200 kWh, the total bill calculation is taken by multiplying to a factor of RM 0.509 per kWh. Hence, the RM 87.00 is assumed to be a negligible sum for this purpose.

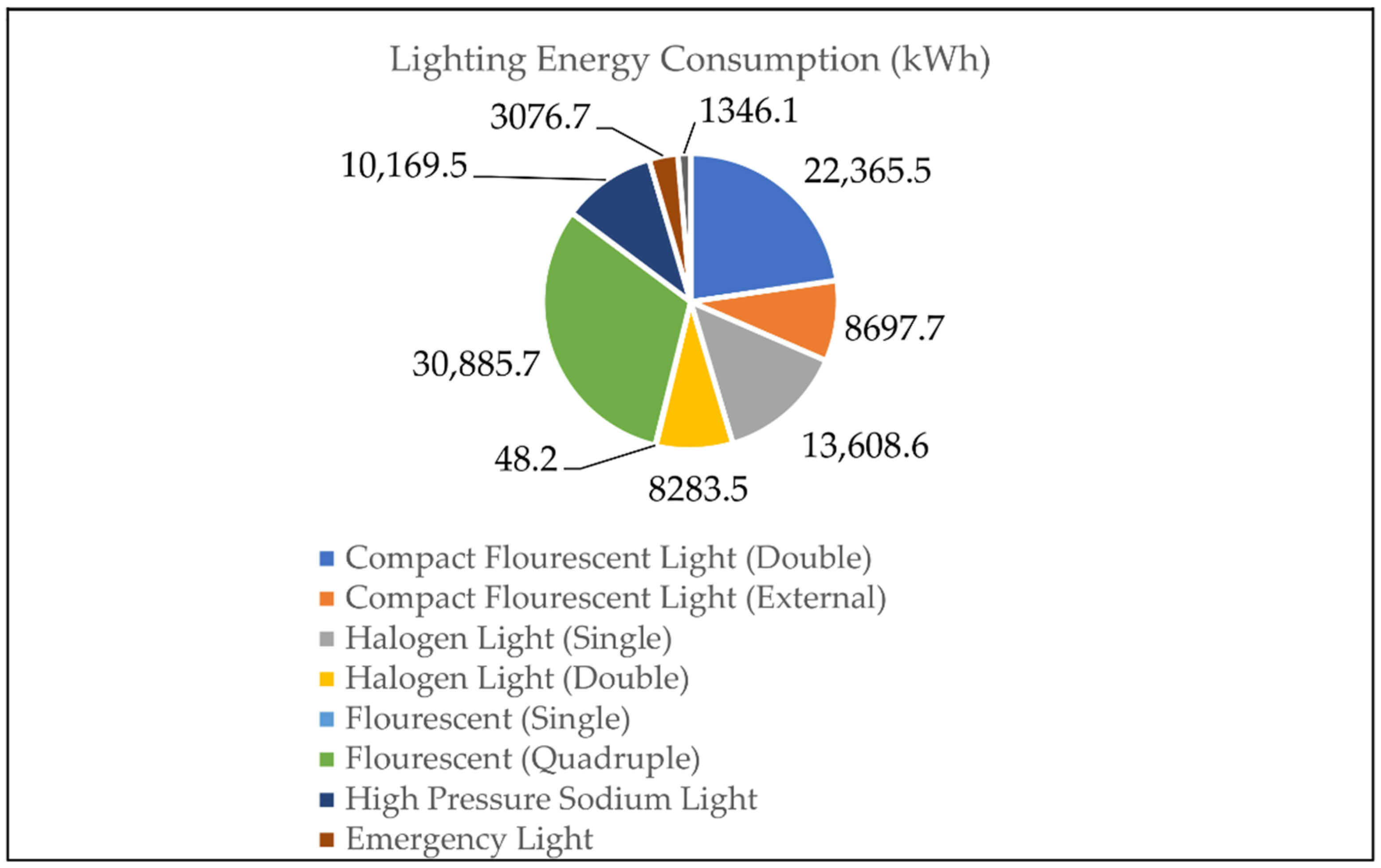

Figure 1 shows the energy consumption for lights used in fast-food restaurants. In order to suit the business needs and to have a cosy eating environment, the indoor lights are turned on throughout the day, even with the presence of natural lighting. Therefore, indoor lighting such as CFL, Halogen (single & double), ‘K’ Light, and Emergency light are turned on as long as there is a use for it. The external lights, such as CFL (external) and high-pressure sodium lights, are switched on during the absence of natural lighting. Since the usage of internal lighting is higher than the external, this justifies the energy consumption.

From the energy audited data collected at fast-food restaurants, the energy consumption and cost contribution for lights, other appliances, and kitchen equipment are presented in

Figure 2,

Figure 3,

Figure 4 and

Figure 5.

Figure 1.

Annual energy consumption for lights.

Figure 1.

Annual energy consumption for lights.

Figure 2 shows the energy consumption for other equipment that is indirectly essential for a fast-food operation. The water heater motor, water pump motor, dumbwaiter, and grease trap operate only when there is a demand. On the other hand, the exhaust fan and capture jet fan equipment operational hours are as long as the business hours. The hydrant pump motor is part of the fire suppression system. Hence, the usage is minimal for yearly testing and verification.

The annual energy consumption of kitchen core equipment is presented in

Figure 3. As described above, the equipment operating characteristics influence the operation hours of the equipment directly. The air-conditioning system is part of the core kitchen equipment, as it is important to operate related equipment at a particular ambient temperature. Apart from the overall thermal transfer and rooftop thermal transfer, the air-conditioning capacity of the kitchen needs to cater to reasonable heat from the equipment. The temperature of the thermostat is set at between 24 °C and 26 °C. Even by doing this, it is observed that the compressor start-stop interval is small, due to a quick rise in temperature beyond the desired temperature, due to heat rejection from the equipment. Hence, the high energy usage from the air-conditioning system is observed.

Even though the business operation is for 20 h a day, it has to be noted that some core equipment will continue to operate for 24 h. This operation is to suit the needs of the business. For example, the freezer and chiller will continue to operate to maintain the temperature to ensure the food product remains frosted. Though the operation is beyond the business operation hours, the equipment operation hours seem to be less. This is because the freezer and chiller in a conditioned room are equipped with an appropriate seal door and stripe curtain, which ensure that the pressure difference is minimal. Hence, the temperature retention time is longer when the door is closed correctly. A similar case is applied to heat treatment machines, ice machines, juice dispensers, multiplexers, Milo machines, and water heaters.

Other than those stated above, the equipment operates only during business hours for food cooking purposes. Hence, the energy intensity is for that reason.

Figure 3.

Annual energy consumption for core equipment.

Figure 3.

Annual energy consumption for core equipment.

Figure 4.

Percentage of energy consumption by different types of appliances.

Figure 4.

Percentage of energy consumption by different types of appliances.

The total energy consumption in the restaurant over a year is presented in

Figure 4, and was acquired from a walk-through energy audit conducted in 2021. The detailed energy breakdown of the appliances was then analysed and is shown in

Figure 3.

From the audit, it can be perceived that the air-conditioning system contributes to the highest power consumption, a total of 42%, which is RM 182,143 per annum, followed by kitchen equipment at 25%, which corresponds to RM 112,051. Other appliances including a freezer, cooler, and water heater contribute to 22%, which equals RM 98,270. The lowest contribution of 11% comes from lighting, with a total of RM 50,127 per year. These compute the total energy consumption of 869,533.4 per year, billing RM 442,592.5 per annum.

In order to optimize energy usage, the restaurant management needs to identify, measure, and evaluate the contributors to the total energy consumption, whereby an energy-efficiency initiative can be established during peak and non-peak hours, on a daily basis. It is essential to have a walk-through energy audit as there is an absence of a building energy management system to address this issue. Every piece of installed equipment is precisely identified, and the building management needs to take note of the energy profile of specific equipment, which is the result of this research.

3.2. Energy, Cost Savings, and Payback Period Assessment by Using Energy-Efficient Equipment

With the advent of technology, the implication of potential energy-saving devices such as LED, LHTES air-conditioning systems, and water heaters, has shown tremendous changes in total power consumption. In addition, to utilize the space found on the metal-deck rooftop, a 27.14 kWp solar panel system has been mounted.

Lights are very important for restaurants, as the design of their temperature and illumination play a vital role in ensuring the proper appearance of the food, the correct eating ambiance, and the provision of cosiness. Hence, these lights are specifically chosen to suit the exact criteria of the above considerations, and not to change the design criteria. In

Figure 5 and

Table 8, conversion to LED has reduced the energy consumption to 58,109.4 kWh, equivalent to RM 30,086.7. This reduction contributes to an energy reduction of 40%. The biggest contributor to the percentage of savings is the ‘K’ Sign light, at 77% reduction by using LED. However, when observed overall, the power consumption for all conversion to LED has managed a reduction of above 50%.

By implementing the LHTES on the water heater and air-conditioning system, the energy consumption has been reduced to 11,414.2 kW and 268,382.6 kW per annum, respectively. Hence, the bill has been reduced to 5809.8 and RM 136,606.7 for the LHTES water heater and air-conditioning system, respectively. This contributes to a saving of approximately 67% and 25%, respectively [

19,

21,

22].

The energy production of solar PV for a year is projected to be 39,624.4 kWh. This means a saving of RM 20,168.8.

From the cumulative implementation of all the above-mentioned energy-saving initiatives, there is a reduction in energy consumption of about 22% per annum, which results in total bill savings of RM 97,365.9 per annum.

Figure 5.

Energy savings using energy-efficient lights.

Figure 5.

Energy savings using energy-efficient lights.

Table 8.

Energy Savings Using RE & EE.

Table 8.

Energy Savings Using RE & EE.

| Description | RE & EE Energy Reduction (kWh) | Energy Bill (RM) |

|---|

| Solar Thermal Water Heater | 11,414.2 | 5809.8 |

| LHTES Air-Conditioning System | 268,382.6 | 136,606.7 |

| Solar PV 27.14 kWp | 39,624.4 | 20,168.8 |

From the analysis carried out due to the implementation, the power contribution in total is measured as presented in

Figure 6. The air-conditioning systems’ power consumption has dropped to 2.4%. However, the kitchen equipment contributes to a larger proportion now, since there was no integration of technology due to the effect on food quality and safety. However, the total power consumption of kitchen equipment remains the same as in

Table 4. Due to the reduction in cumulative electricity consumption, the percentage contributions from kitchen equipment and other appliances have an increment of 7.5% and 3%, respectively. The lightings contribution percentage has been reduced to about 2.3% of total energy. Another contributor to the reduction of utility is solar, which adds up to 5.8% of the total electricity bill. Since solar is not consuming electricity and is producing instead, the negative (−) symbol is used.

3.3. Payback and Return on Investment (ROI)

When analysing the individual payback and ROI for lighting, as in

Table 9, the overall payback is less than four years. Some lighting computes to very high payback, such as T8 LED, outdoor LED, emergency light LED, and ‘K’ light LED. There are some identifiable reasons for this long payback. The T8 LED and outdoor LED are being used for a short period of time. For instance, the outdoor LED operates only after dark, which is about 12 operating hours daily. The T8 LED is being used for only about 454 h a year. This usage has resulted in a longer payback period since the savings could not be optimized due to the shorter operating hours. On the other hand, although the emergency LED and ‘K’ sign are operating for longer hours, they still give a very low wattage. However, in totality, the payback is still less than five years.

The air-conditioning and water heater give an attractive payback and ROI as shown in

Table 10: 1.3 years and 77.5% ROI for the water heater, and 3.5 years and 28.5% for the air-conditioning. A comparison of solar panel prices from 2019 to 2022 has been analysed, and it has been observed that the price of solar panels is lower from year to year in the Malaysia case scenario. In addition, the Malaysian government has introduced tax incentives that reduce the taxation of green products.

Table 11 shows a comparison of payback and ROI with and without the tax incentives reduction of 48%, and its impact on the payback period [

25]. The two types of tax incentives provided by the government of Malaysia are capital allowance (CA), applicable for any capital expenditure of the company, and the investment tax allowance (ITA), which is an additional tax allowance introduced and applicable only for green procurement.

Table 11 presents the payback and ROI, which have been calculated with and without both of these tax incentives for the solar PV system. The payback and ROI are calculated to be highest for 2019, which is 9.1 years and 10.9%, and lowest at 6.3 years and 15.9% for 2022, as presented in

Table 11. From the historical evidence of prices gathered for solar panels, it is predicted that the price will keep reducing over time. This positive sign will result in increasing penetration of alternative energy generation for building usages in Malaysia [

40,

41].

The total energy-saving initiative is contributed to by each and every piece of equipment, which results in the reduction of the utility bill. Therefore, for any sector, it is of utmost importance to evaluate the cumulative payback and ROI, since they could produce attractive savings in monthly billing. The cumulative payback and ROI are 3.7 years and 27.3%, respectively, as shown in

Table 12.

3.4. Building Energy Index

In Malaysia, the performance of a commercial building is measured by using the building energy index (BEI). BEI is described as the energy consumption per annum per sqm of the building, commonly referred to as MS 1525:2014 [

36,

37]. This states that the energy-efficient commercial building needs to have an improved BEI of less or equal to 135 kWh/m

2/year. Many studies have been conducted for multiple commercial buildings such as institutions, hospitals, offices, and large governmental buildings, using the mathematical equation as shown in Equation (10) [

30,

33,

36,

37]. Since no BEI measurement has been analysed for an operational restaurant building, this research measures the concentric BEI among fast-food restaurant buildings without and with renewable energy and energy-efficient implementation.

In this research, the BEI value for a 20-h fast-food restaurant without any energy-efficient implementation is found to be 1097.9 kWh/m2/year. At post-implementation of energy-efficient equipment, the BEI value is calculated to be 856.4 kWh/m2/year. Hence, the improved BEI shows a reduction of 22%

3.5. Impact on Emission Reduction with Energy Efficient Equipment

The introduction of energy-efficient devices and the addition of renewable generation not only save energy but also contribute to the decline in pollutants from the building. The three parameters which raise concern for the rising of sea levels due to an increase in ground temperature are SO2, CO, and CO2. Hence, the reduction of these pollutants will be presented in this section.

The emission reduction is calculated using Equation (9), Malaysia energy mix data, and the energy-saving data from

Table 10,

Table 11 and

Table 12.

Figure 7 presents the emission reduction amount per annum of each piece of equipment. The biggest reduction in pollutant emission is contributed by the air-conditioning system, and is related to its functioning capacity. As it consists of 42% of total energy consumption and uses an energy-efficient system, a total of 33.42 kg of CO

2, 355.3 kg of SO

2, and 155.3 kg of CO have been omitted.

The installation of renewable energy (solar) will substitute the usage of fossil fuel-generated power, and the capacity is variable based on space availability. For the studied site, a total of 29,074.7 kg of CO2, 271.5 kg of SO2, and 118.9 kg of CO pollutants can be omitted by applying Solar PV and a Solar Thermal Water Heater.

From energy reduction obtained by using energy-efficient equipment, a total of 91,392.1 kg CO2, 881.8 kg SO2, and 385.5 kg of CO have been omitted.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}