Abstract

This research aims to explore the impact of corporate governance on firm performance while considering financial leverage as a mediating variable. This study was conducted in the non-financial sector of Pakistan, and data was collected from financial statements. A sample of 150 firms was selected from those registered on the Pakistan Stock Exchange during the period of 2011–2021. Results show that corporate governance is associated with firm performance. Board size has a positive relationship with firm performance; as board size increases, the performance of the firm also increases. Board independence is positively and significantly associated with firm performance. Audit committee size is also positively associated with firm performance. Female directors on the board are also associated with positive firm performance. Board independence, board size, audit committee, and female directorship were positively associated with financial leverage. Corporate governance protects the interest of shareholders and transfers risk from shareholders to debt holders. Results show that corporate governance enhances the financial distress cost by enhancing the debt ratio in the financial leverage. Financial leverage partially mediates the board size and board independence with firm performance, while audit committee size and female directorship relationship with firm performance are fully mediated.

1. Introduction

After the incidence of the financial crunch of 1998 in Asia, Brazil, and Russia, corporate governance regulations are considered important for financial decisions. Corporate governance is a combination of supervision, which is considered productive and worthwhile, direction, and control to minimize agency conflicts [1]. The basic aim of corporate governance is that the firm operates in the interest of shareholders [2]. The capital structure (CS) of a firm relates to how that firm is funded by a ratio of equity and debt resources [3]. Few theories recommend that capital structure is a critical decision made by the directors because a firm’s performance is associated with it. Financial leverage relates to the ratio of entire debts and total capital employed [4]. Thus, financial problems caused by capital structure not only impact the profitability of the company but also powerfully affect macroeconomic results. Previous research information related to corporate governance mainly focuses on the consequences of corporate governance as a factor on financial performance as an outcome [1,5]. However, past studies presented contradictory results and did not investigate the combined impact of capital structure and corporate governance on firms’ performance in the Pakistani context [6]. Therefore, the impact of corporate governance on financial performance while mediating capital structure needs to be investigated.

Corporate governance in Pakistan was presented in 1991 due to many scandals traced in various sectors that destroyed the belief of the nation [7]. Pakistan Institute of Corporate Governance, in compliance with SECP, presented an improved version of corporate governance. Finally, Pakistan’s corporate sector got its amended version of the code for corporate governance in 2012 [8]. Rules adopted by public sector companies of Pakistan were moving in the right step. Improved corporate governance has increased Pakistan’s GDP and overall growth economically.

The literature review in Pakistan mainly provides evidence about (1) equity ownership and its impact on firms’ profitability [9,10]; (2) impact of corporate governance quality on capital structure choice in cement industry [11,12]; (3) the impact of corporate governance on firm performance during the COVID-19 pandemic [13,14]; (4) impact of corporate governance on trust and discloser practices banking sector [14]; (5) corporate governance and cost of capital [15]; (6) intellectual capital corporate governance and Islamic bank’s performance [16]; and (7) impact of corporate governance and financial performance in the cement industry, banking industry, and pharmaceutical industry [17,18,19,20]. Hence the relationship between corporate governance, financial performance, and mediation of financial leverage in the overall non-financial sector of Pakistan is missing. This study contributes to the literature in the Pakistani non-financial context on the relationship between corporate governance and firm performance. This study is a pioneering attempt to explore the mediating role of capital structure between corporate governance and firm performance in the non-financial sector.

The question about the mediating role of capital structure among corporate governance and firm performance is considerable for the following reasons. First, a direct effect of corporate governance might be negative on firm performance. If the indirect relationship of corporate governance on firm performance prevails, examining the capital structure as a mediator for firm performance could elaborate the mixed consequences of the effect of corporate governance on firm performance. Second, by putting capital structure as a mediator, we would have an influential argument of how changes in corporate governance can impact firm performance. The study related to corporate governance practices’ impact on financial performance while mediating the role of financial leverage is a concern for the non-financial sector of Pakistan, so that this research could make a huge difference in stability.

The remaining part of this research investigation is arranged as follows: In the second part, an extensive literature review is elaborated in relation to corporate governance, capital structure, and firm performance. This is followed by further explanation of the research methodology, results, discussion, and conclusion.

2. Literature Review

Corporate governance contains all rules and regulations by which companies are directed and controlled. Different participants of corporate governance are considered important for making decisions with relative power and being providers of capital. Capital structure refers to the way a corporation finances its assets through a combination of equity and debt. Different theories were presented by [21], and according to their finding, the value of the firm is not affected by the mixture of capital structure. The company can use any combination of debt-to-equity ratios. According to the [22], capital structure is discussed and how it can maximize firm value. The corporate governance mechanism has been divided into two groups: internal, which includes employees, suppliers, and customers; and external, which includes the market, politics, culture, and communities. The board of directors makes decisions about the portion of debts and equity in the capital of the firm [23]. However, this decision is affected by the external environment of the organization. Political instability, market environment, and the culture of the country with community norms are main indicators of this decision [2].

Firm performance is elaborated as value of the firm which should be maximized for stakeholders’ concerns. Further literature is discussed on how corporate governance practices and capital structure are related with firms’ performance.

2.1. Board Size and Firm Performance

Board size is considered as an important corporate governance element which impacts firm performance. There is evidence by [24] that larger board size in firms of Africa, Asia, Europe, Latin America, North America, and Oceania influence a firm’s performance significantly. According to the authors, these firms should be concerned about increasing the number of board directors to act efficiently for enhancing profitability of firms. Firms of developing countries are keenly practiced to enhance their performance, for which larger board size has great contribution [25]. Recent research by [26] intimates that board size enhances firms profit on all levels of profitability such as being low, moderate, and high among Indian firms. They argued that larger board size consists of rich intellectual property of the board which accelerates the profit due to effective decision making. In contrast, according to [27], board size negatively impacts profitability of firms listed in Nigeria and depicts that larger board size increases expenses related to BOD salaries and their personal interests which causes a decrease in firms’ performance. Ref. [28] investigate the corporate governance with financial preference and sustainability practices in five European countries, Germany, France, the UK, Italy, and Spain. Results suggest that board size enhances financial performance and CSR sustainable practices. According to [29] investigate the effect of good governance and financial performance and corporate financial responsibility disclosures in the telecommunication industry in Indonesia. Results indicate that good governance within the telecommunication industry in the form of board size causes a financial performance indicator. Board size consists of members with diverse industries experience. The opinions of every board member have an effect on the decision making of company policy, so due to board size, different people come together to make rational decisions. On the basis of the above discussion, the hypothesis is developed.

Hypothesis 1 (H1).

Board size is positively associated with firm performance.

2.2. Board Independence and Firm Performance

Board independence relates to the decisions taken by the board of how much their decisions are interrelated. According to [24], board independence is insignificantly impacting the productivity of firms of India on all levels of the profitability ratio. They argued that board decisions taken by consent of all members can increase firm performance. Research presented by [30] showed that if board members worked independently, it caused declining profitability related to return on assets in listed companies of Pakistan. They found that Pakistani firms are usually family oriented so the conflict of interest arises if they work independently. The results of adverse relationships between board independence and firm performance are also shown in firms based in Kuwait [31]. In the studies concerning the impact of board independence on firm performance, it is shown that the relationships among both are significantly observed when demand for some specific products drop [32]. According to [33], studies were conducted in banks. These studies entailed the role of corporate governance with financial performance as well as the direct and indirect role of board independence. Results showed that board independent had a positive influence on banks performance, which was confirmed by using Pannal data analysis. The study suggests that the type of firms has a significant impact on the corporate governance indicators and financial performance. According to [34] investigate the relationship between corporate governance and financial performance in the energy sector. Results suggest that board independence enhances the financial performance in the energy context. As investigation carried by [35] conducted an investigation in the Indian context. The purpose of the study is to find out the relationship between the board characteristics and textile sector performance. The finding shows that board independence has no effect on the textile sector performance in the Indian context.

Hypothesis 2 (H2).

Board independence is positively associated with firm performance.

2.3. Audit Committee Size and Firm Performance

The study related to [36] showed that an audit committee influenced firm profitability in positive manners in Jordanian companies. They considered dependency theory and showed similar expression that an audit committee performs more efficiently if its size increases and has a positive impact on the profit of the firm. The researcher [37] tried to determine whether an audit committee makes a great contribution in improving the performance of firms in Pakistan and they argued that a powerful CEO forces the audit committee to find unfavorable financing activities happening in firms. If the audit committee strictly control fraud, firm profit automatically enhances. According to the [38] showed from his research that an audit committee has a positive effect on a firm’s performance according to the academic community, while firm age weakens the effect of the audit committee on the performance of firms. They argued that longevity of firms affect inversely upon the audit committee control and that fraudulent activities badly affect firm profit.

Hypothesis 3 (H3).

Audit committee size is positively associated with firm performance.

2.4. Female Directorship and Financial Performance

Many companies focus on the company’s characteristics while computing profitability, although managerial characteristics are usually ignored. Some literature shows the results of no relationship between female directorship and the firm’s performance [39]. On the other hand, female presence is considered mandatory for corporate governance and presents a positive association between female directorship and the performance of firms [28]. Over the past decade, studies on gender within boards have justified women in higher executive positions show higher related outcomes of performance [27]. Another research [40] conducted an investigation on female presence in corporate governance and firm performance of the mediating role of family ownership. Results clarifies that female director on the board having positive influence on performance, but family ownership does not mediate the relationship. They suggest that there is a balance on the board of the firm and that gender diversity has positively enhanced the performed of firms. Another research [41] studied females on boards of Portuguese listed companies and investigated i: does gender diversity affect firm performance. Results show that a 20% presence of females on boards has a positive relationship with performance in Portuguese firms. According to [42] investigate the impact of corporate governance and intellectual capital on firm performance. Studies show that female director ratio has a positive impact on financial performance.

Hypothesis 4 (H4).

There is a positive effect of female directorship on firm performance.

2.5. CEO Duality and Firm Performance

Another research [43] investigated CEO duality and firm performance on the different stages of venture and proved that CEO duality enhances firms’ performance in the starting age of venture while, in the long run, it affected firm profit due to the personal interests of the CEO, which accelerated expenses. An empirical analysis performed by [30] between CEO duality and profitability of Chinese business firms showed that both were insignificantly associated. They also argued that firm’s size moderates the effect of CEO duality and a firm’s performance positively in larger firms. A researcher investigated the effect of agency theory and steward theory on CEO duality and firm productivity with findings that dual leadership structure negatively affects firm matters and should be eliminated for higher performance in Portuguese firms. Another research [44] found from their research that CEO duality has a positive significant relation with ROA while it has an inverse relationship with market capitalization.

Hypothesis 5 (H5).

CEO duality is negatively associated with firm performance.

2.6. Board Size and Capital Structure

According to [45], there is strong association between board and firm size with capital structure in the listed firms of Chinese real estate. They argued that better governed firms by the efficient board size must have a better capital structure of real estates. Another research [46] investigation presented that board size strongly influenced the decision making of the capital structure of Kenya’s commercial banks. They argued in their study that to increase the profitability of firms, debt and equity levels should be managed rationally. In contrast, previous research by [47] presented that the association between board size and capital structure was negative in listed Thai companies. They also argued that if corporate governance was managed in a better way than external funding could be assured which showed a good position of company. A study presented by [48] analyzed the firms of three countries with distinct corporate governance (Japanese, French, and German) and showed that board size is negatively associated with debt financing.

Hypothesis 6 (H6).

Board size is negatively associated with financial leverage.

2.7. Board Independence and Capital Structure

According to a research investigation by [43], if gender diversity prevails as high, than board independence shows a positive relationship with a firm’s leverage of non- financial listed firms in Palestine. They presented the logic behind this result that agency theory entrenched logic of effecting corporate governance on capital structure, but gender diversity should be a concern. Another research [49] suggested that board size significantly influences the firm’s value of firms based in Vietnam. They also depicted that the characteristics of the board of directors have a great contribution in making the capital structure of firms. A study by [47] found that if there was more independence given to the board of directors of listed companies of Thailand, than lower debt financing was required in capital structure. They also mentioned that if more independent board of directors is in firms, they can strictly control management for debt financing. The outcomes revealed that board independence has an affirmative relationship with capital structure of firms based in UK, France, and Germany [50]. They elaborated in studies that more board independence shows that shareholders’ interest is protected. In contrast, Another research [12] showed weak results that the board independence had no influence on the capital structure, but it had an association with firms’ performance of cement companies listed in Pakistan.

Hypothesis 7 (H7).

There is a positive effect of board independence on financial leverage.

2.8. Audit Committee Size and Capital Structure

Audit committee decisions are considered very important in the policy making of firms regarding the capital structure of firms. According to [51], studies presented that the large size of an audit committee gives high audit quality and is very important in making capital structure decisions in wealth creator companies of Indonesia. They also suggested that firms increase their audit committee size to reduce agency cost. According to the research by [52], firms that have a large audit committee size have more debt financing ratio in capital structure. The researcher also argued that high composition of audit committee shows high credible results to stakeholders. Another research [30] discusses audit committee effectiveness, internal audit function, firm-specific attributes, and internet financial reporting: a managerial perception-based evidence. Results show that audit committee is highly credible for capital structure. Audit committee enhances debt ratio so that external monitoring from banks and financial regulation is enhanced. This may lead to reduced the work of audit [53]. The impact of corporate governace on firm performance on famiy owned firs with mediation of finacial levergae.According to findings, the audit committee is partially mediated by capital structure ratio, while they have a positive effect on the financial performace of firms [54]. In regard to the mediating effect of audit committees on the board dynamic, capital structure, and creative accounting in Nigerian firms, results suggest that the audit committee has a postive effect on capital structure.

Hypothesis 8 (H8).

Audit committee is positively associated with financial leverage.

2.9. CEO Duality and Capital Structure

CEO duality means the chief executive officer of the firm holds as much power as the chief of board (COB). According to previous literature, CEO duality increases agency cost, and a research investigation by [47] presents that there is no significant relationship between CEO duality and capital structure of listed companies of Thailand, with the argument that companies that have management with clear roles and responsibilities work efficiently. Responsiveness of capital structure helps to make a better financial mix which can enhance the firm market share, but CEO duality in firms of Vietnam cause a decrease in capital structure speed [11]. Elements of BOD are highly relevant to capital structure, but CEO duality impacts insignificantly on it as women having CEO duality in European firms, cannot handle financial distress [55]. In contrast, Another research [56] carried out research to find how CEO duality impacts capital structure among Egyptian listed companies and showed positive results that if a CEO performs the duty as COB, there is more concern about equity financing.

Hypothesis 9 (H9).

CEO duality is negatively associated with financial leverage.

2.10. Female Directorship and Capital Structure

Directors are considered topmost level managers who have a major influence on the decision making of any organization’s capital structure. Female directors are considered calm natured and found to have less debt financing ratio in the financing mix [57]. The structure of board of directors and structure of debts and equity are examined to study impact on performance of firms and extracted that female BOD accelerates performance if equity financing in enhanced [58]. Meanwhile, past research investigations show female directors and non-executive directors are inversely relates to financial leverage and firms’ performance of financial industry of Pakistan [36]. In the banking industry, when capital adequacy ratio is higher for considering performance than females, CEOs are considered as inconsistent to outcomes [58].

Hypothesis 10 (H10).

There is a positive effect of female directorship on financial leverage.

2.11. Financial Leverage and Financial Performance

Savings and credit co-operative societies in Tanzania were investigated for the relationship of financial leverage and firms’ performance; it was found that both are negatively and significantly associated [59]. The same outcomes are shown by Nigerian goods firms too, which revealed firm performance by cash value added of quoted industrial good firms and presented a negative relationship with long term debt ratio while having positive links with short term debt ratio [50]. A research study about oil firms of Nigeria showed a negative link between financial leverage and performance which was measured by ROE and suggested to enhance debt financing to secure shareholders’ position in firms [60]. Pengaruh Financial Leverage, Capital Structure, Liquidity, Dan Sales Growth Terhadap Financial Performance [61]. Findings suggest that financial leverage positvely effects financial performance and growth. [62] The Mediating Role Of Capital Structure In Corporate Governance On Firm Performance Of Family Companies. According to findings, the capital structure enhances the financial performance of family-owned firms. Family-owned firms with a lack of resources experience a decline in opportunities to invest but due to debts more opportunities has been available. [63] Financial Leverage and Financial Performanceof Savings and Credit Co-operative Societiesin Tanzania. Credit cooperative society performance was effected by financial leverage. (Appendix A)

Hypothesis 11 (H11).

Financial leverage negatively associated with firm performance.

2.12. Financial Leverage Mediation between Corporate Governance and Financial Performance

Another research [64] examined that corporate governance and a firm’s performance relationship is negatively correlated but significant and mediating by financial leverage. According to [65], financial leverage significantly reduces performance in time of economic downturn but it can be controlled by improving corporate governance quality. Another research [66] stated in his research that increased debt financing can decrease opportunistic behavior of managers and minimize effect on corporate governance. Thus, extent financial leverage and debt contracts can increase performance of firms. Role of financial leverage is examined as a mediator among firm size and performance of sugar firms in western Kenya and stated that it negatively mediates the relationship [67].

Hypothesis 12 (H12).

Financial leverage mediates the effect of board independence on firm performance.

Hypothesis 13 (H13).

Financial leverage mediates the effect of audit committee size on firm performance.

Hypothesis 14 (H14).

Financial leverage mediates the effect of female directorship on firm performance.

Hypothesis 15 (H15).

Financial leverage mediates the effect of CEO duality on firm performance.

Hypothesis 16 (H16).

Financial leverage mediates the effect of Board size on firm performance.

3. Methodology

3.1. Population of Study

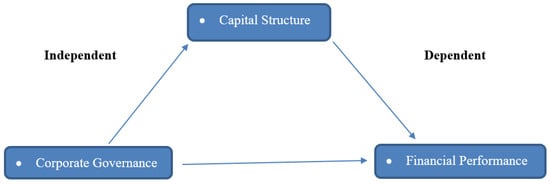

The purpose of this study was to find out the effect of corporate governance on financial performance and mediation role capital structure firm listed on the PSX. This study used secondary panel data that was collected from the financial statements of the firms and from the SECP. The population of the study is the non-financial sector of Pakistan. The total population of the registered companies on the Pakistan Stock Exchange was 375 of which 150 non-financial firms were selected for this study. Companies’ data was collected from year 2011 to 2021. In order to address the research question of how financial leverage mediates the relationship between corporate governance and firm performance, OLS panel regression was used. This research study used one lagged right hand for all models to avoid endogeneity and causality problems. This was the reason for using qualitative data collection. So as to address the research question of the impact of corporate governance and firm performance, this research used series panel OLS regression for corporate governance and financial performance with some control variables. Firm fixed effect and time fixed effect was used to control the unobserved time-invariant firm characteristic and cover omitted time-variant effect that may cause problems for firms and samples or both. For capital structure and firm performance, we used one left side lagged of one period in order to avoid the endogeneity and causality problem. So here this research was used to regress one lagged corporate governance and one lagged control variable on capital structure. (Figure 1)

Figure 1.

Research Modal.

3.1.1. Model 1

To test effect of the corporate governance on the capital structure, we estimate a series of Equation (1) using panel OLS regressions as follows:

where financial leverage (FLEV) is the dependent variable and CG represents (board size, board independence, audit committee size, CEO duality, and female directorship) while is the firm level control variable, is the firm fixed effect, and is the time fix effect. Firm fixed effect and time fixed effect was used to control the unobserved time-invariant firm characteristic and cover omitted time-variant effect that may cause problem for firms and sample or both.

3.1.2. Model 2

Equation (2) used a test that predicts the effect of the corporate governance on the firm’s performance.

where Return on Equity (ROE) is the dependent variable CG represents (board size, board independence, audit committee size, CEO duality, and female directorship) while is the firm level control variable, is the firm fixed effect, and is the time fix effect. Firm fixed effect and time fixed effect was used to control the unobserved time-invariant firm characteristic and cover omitted time-variant effect that may cause problems for firms and samples or both.

3.1.3. Model 3

Equation (3) used a test that predicts the effect of financial leverage on the firm’s performance

In Model 3, return on assets (ROA) is the dependent variable and independent variables, financial leverage (FLEV) while is the firm level control variable, is the firm fixed effect and is the time fix effect. Firm fixed effect and time fixed effect was used to control the unobserved time-invariant firm characteristic and cover omitted time-variant effect that may cause problems for firms and samples or both.

3.1.4. Model 4

Equation (4) used a test that predicts the effect of the corporate governance and financial leverage on the firm’s performance.

In Model 4, return on assets (ROA) is the dependent variable and CG represents (board size, board independence, audit committee size, CEO duality, and female directorship) financial leverage (FLEV) while is the firm level control variable, is the firm fixed effect and is the time fix effect. Firm fixed effect and time fixed effect was used to control the unobserved time-invariant firm characteristic and cover omitted time-variant effect that may cause problems for firms and samples or both.

4. Empirical Results

4.1. Descriptive Statistics

Table 1 shows the descriptive statistics f corporate governance financial leverage financial performance. The financial leverage mean is (0.24) and median (0.33) which mean that Pakistan firms are not overloaded with external debts whether using equity financing in ordinary operations of business. Board size mean value (9.00) shows that on average, all firms in Pakistan have (9.00) board members to fulfill the corporate governance code as amended 2017 rules. Board independence value shows (1.44) on average, one independent director is present which ranges from two to five independence directors. Audit committee size minimum mean value (3.06) three independent members are present. WD mean value (0.99) every company must have one female director in the board in order to maintain gender diversity in the board.

Table 1.

Descriptive statistics on keys variables.

4.2. Regression Results Corporate Governance and Financial Leverage

This study attempts to answer the question, What impact does corporate governance have on financial leverage? Here this research presents the empirical results. Table 2 represents the penal regression results; financial leverage regresses on all the control variables relevant to industry and firm level and corporate governance variables. This research study used firm fixed and time fixed effect in all the models. Model 1 shows regress dependent variable financial leverage with firm and industry level control variables. INDR industry return, F.SIZE firm size, F.AGE firm age, EXPCAP capital investment, C.R current ratio, MKT market to book value, are positively associated with financial leverage, NCF cash flow to total assets, FXR fixed assets ratio, ROA profitability return on assets are negatively associated with financial leverage. Model 2 runs in order to find out the straight forward impact of corporate governance on financial leverage. FLEV financial leverages regresses with corporate governance variables board size, BI board independence, ACS audit committee size, WD woman director in the board, CE. D CEO chair main duality. In Model 2, INDR industry return, F. SIZE firm size, F.AGE firm age, EXPCAP capital investment, C.R current ratio, MKT market to book value are positively and significantly linked to financial leverage, NCF cash flow to total assets, FXR fixed assets ratio, ROA profitability return on assets negatively associated with financial leverage. The board size p < 0.005 and positive impact on financial leverage [48]. The board independent p < 0.000 has positive and significant impact on financial leverage [49]. Audit committee size p < 0.10 has a significant impact on financial leverage [51]. The female directorship p< 0.003 has a significant and positive impact on financial leverage [48]. CEO duality p < 0.20 does not have an impact on financial leverage. This finding provides empirical support to H6–H10 except H9. Wen et al. (2002) find no relationship between board size and financial leverage for listed firms in China.

Table 2.

Corporate governance and financial leverage.

4.3. Corporate Governance, Financial Leverage Impact on Firm Performance

To answer the question, impact of corporate governance and financial leverage on firm performance? here this research presents the empirical results. Model 1 firm performance was regress on all the control variable relevant to industry and firm level. This research study used firm fixed and time fixed effect in all the models, INDR industry return, F. SIZE, F.AGE, EXPCAP capital investment, C.R current ratio, MKT market to book value, ROA profitability return on assets having positively associated with financial leverage NCF cash flow to total assets, FXR fixed assets ratio and F. SIZE having negatively associated with firm performance. Important to note the negative effect of firm size on firm performance is inconsistent with prior studies (Elsayed, 2007). Model 2 test the relationship corporate governance on firm performance, all dimension of corporate governance regress with firm performance. BS board size having p < 0.004 significant positive impact on firm performance [24]. BI board independence having p < 0.002 significant and positive impact on firm performance [25]. ACS audit committee size having p < 0.005 significant and positive impact on firm performance [36]. WD woman director in the board having p < 0.003 significant and positive impact on firm performance [63].CE. D CEO chair main duality having p < 0.005 significant and positive impact on firm performance [56]. This finding provides empirical support to H1–H5. Model 3 was for financial leverage and firm performance. ROA profitability return on assets p < 0.03, INDR industry return p < 0.09, F. SIZE firm size p < 0.07, F.AGE firm age p < 0.03, EXPCAP capital investment p < 0.06, C.R current ratio p < 0.03, MKT market to book value p < 0.06, are positively associated with financial leverage NCF cash flow to total assets p < 0.03, FXR fixed assets ratio p < 0.07 negatively associated with firm performance. Financial leverage coefficient and p < 0.06 negatively associated with firm performance [59]. This finding supports our hypothesis that there is positive relationship between financial leverage and firm performance. Model 4 full estimate the result of control variable, corporate governance, financial leverage. Financial leverage p < 0.09 represents that more financial leverage more firm performance in Pakistani nonfinancial sector case [60]. Bord size p < 0.00 having significant and positive impact on firm performance [9] here results suggest that more bord size with firm leverage leads to more firm performance. Board independent and female director in the board leads to firm performance so concluded that mere independent director with more gender diversity with firm leverage led to firm performance [30]. CEO duality p < 97 des not significant impact on firm performance. these findings are consistent with several prior studies [59]. Elsayed (2007) finds that CEO duality has no impact on corporate performance, measured as ROA and Tobin’s Q, for a sample of publicly listed firms in Egypt from 2000 to 2004.

4.4. Mediation of Financial Leverage between Corporate Governance Firm Performance

Baron and Kenny (1986) methods used to test the mediation effect of financial leverage with corporate governance and firm performance. If the relationship between the corporate governance and firm performance becomes insignificant in Equation (3) after entering the financial leverage said to be the full mediation. Financial leverage partially mediates the relationship between the corporate governance and firm performance when Equation (3) weaker than Equation (2). Table 3 results describes that the board independent having positive correlation with return on equity p < 0.034 and with financial leverage positive correlation p < 0.0244. after entering the financial leverage, the p < 0.05 which represent that there is partially mediation with board independent and firm performance. Female director relationship with financial leverage positive and significant < 0.043 and firm performance < 0.025 which become insignificant p < 0.983. financial leverage full mediation with female directorship and firm performance. Audit committee size relationship with financial leverage significant and positive with p < 0.003 and significant and positive with firm performance p < 0.10 but become insignificant when financial leverage added. So financial leverage fully mediated the audit committee board size having positive and significant impact on firm performance < 0.067 after mediation that there is difference in p < 0.015 which mean financial leverage partially mediate the relationship between board size and firm performance. These finding provides empirical evidence for hypothesis H12–H16 except H15.

Table 3.

Corporate governance financial leverage and firm performance.

4.5. Firm Division in Small and Large on Basis of Firm Size

Impact of corporate governance on financial leverage and firm performance was tested above. Here some extra modification was carried out in data and test robustness of main dependent variable with independent variable. This investigation confirms that either results were consistent with previous finding. The method was to divide the firms into two groups based on firm size. Two groups have been made: one represents the small businesses and the other represents the larger firms. The sub group of date based on firm size cross section mean value of total asset. We used zero if cross sectional means value of total assets higher then firm size. A firm size (HTA) dummy variable takes a value of one for an observation with LNTA larger than the cross-sectional mean of LNTA, and zero otherwise. This study sought to find out the relationship between corporate governance with financial leverage both with sub samples for large and small firms. Model 2 tested the relationship corporate governance on financial leverage for small subsample. BS board size had β = −0.053 p < 0.00 a negative impact and financial leverage, BI board independence had β = 0.042 p < 0.00 a significant and positive impact and financial leverage, ACS audit committee size had β = 0.031 p < 0.00 a significant and positive impact and firm financial leverage, WD woman director in the board had β = 0.054 p < 0.00 a significant and positive impact on financial leverage, CE. D CEO chair main duality had an insignificant but positive impact and financial leverage. This finding provides empirical support to H5–H9. Model 4 test the relationship corporate governance on financial leverage, for large sub sample. BS board size had β = −0.0567 p < 0.00 a significant and negative impact and financial leverage, BI board independence had β = −0.0184 p < 0.00 a significant and positive impact and firm performance, ACS audit committee size had β = 0.315 p < 0.00 a significant and positive impact and financial leverage, WD woman director in the board had β = 0.096 p < 0.00 a significant and positive impact on financial leverage, CE. D CEO chair main duality had an insignificant but positive impact and firm performance (Table 4).

Table 4.

Corporate governance and financial leverage subsample small and large firms.

4.6. Corporate Governance Financial Leverage and Firm Performance Small and Large Firm

Model 1 tested the relationship corporate governance on firm performance in sub sample of small firms. BS board size had β = 0.032 p < 0.00 a positive effect on the firm performance and a < 0.004 significant and positive impact and financial leverage, BI board independence had β = 0.315 p < 0.00 a significant and positive impact and firm performance, ACS audit committee size had β = 0.021 p < 0.00 a significant and positive impact on firm performance, WD woman director in the board had β = 0.044 p < 0.00 a significant and positive impact on firm performance, CEO chairman duality had an insignificant but significant and positive impact and financial leverage. This finding provides empirical support to H1–H5. Model 2 was for financial leverage and firm performance. Financial leverage coefficient and β = 0.039 p < 0.06. This finding supports our hypothesis that there is positive relationship between financial leverage and firm performance. Model 3 tested the relationship corporate governance on financial leverage, for large sub sample. BS board size had β = −0.247 p < 0.004 a significant and negative impact and firm performance, BI board independence had β = −0.043 p < 0.00 a significant and positive impact and firm performance, ACS audit committee size had β = 0.042 p < 0.00 a significant and positive impact and firm performance, WD woman director in the board had β = 0.051 p < 0.00 a significant and positive impact and firm performance, CE. D CEO chair main duality had an insignificant but significant and positive impact and firm performance. Model 4 tested for financial leverage and firm performance. Financial leverage coefficient and β = 0.045 p < 0.06. This finding supports our hypothesis that there is a positive relationship between financial leverage and firm performance (Table 5).

Table 5.

Corporate governance financial leverage and firm performance small and large firms.

5. Conclusions, Recommendation, and Limitation

5.1. Conclusions

The purpose of the present study is to investigate the impact of corporate governance on firm performance. The present study also investigated the mediating role of financial leverage between corporate governance on firm performance. The present study was conducted in the non-financial sector of Pakistan and data was collected from financial statements. This research tracked record non-financial sector of Pakistan throughout the period of 2010–2021, which shed light on of the associations between corporate governance and financial leverage with firm performance. This investigation reports the following primary discoveries. Board size has a positive relationship with firm performance; as board size increased, the performance of the firm also increased. Board independence is positively and significantly associated with firm performance; independent director opinions matter a lot because they have experienced diversity which is beneficial for the firm. Audit committee size also is positively associated with firm performance. Having female directors on the board is also associated with positive firm performance. Board independence, board size, audit committee, and female directorship, are positively associated with financial leverage. Corporate governance protects the interests of shareholders and transfers risk from shareholders to debt holders. Results of the study shows that corporate governance enhances the financial distress cost by enhancing the debt ratio in the financial leverage. Financial leverage partially mediates the board size and board independence with firm performance while audit committee size and female directorship relationship with firm performance fully mediated.

5.2. Recommendation and Limitation

This research study used only non-financial firms listed in the SECP. Financial firm must be included in order to know comprehensive knowledge about the mediation of financial leverage. Only local corporation is taken for researcher investigation, foreign corporations are also included. Due to globalization, data is available so comparisons must be made with developed and developing country stock exchanges. Only one measure for firm performance ROE was used in this investigation. Other measure also used ROA operating performance tobin Q. Some expect of corporate governance used other aspect of corporate governance was also used. Corporate governance index is created and the relationship is determined. CSR variable was included and difference dimension of CSR impact was explored. The political uncertainty, government debts, financial deficit, policy uncertainty, and market condition also have effects, so these variables can also be considered to find out the relationship between corporate governance and firm performance.

5.3. Policy Implication

If the manger implements corporate governance codes, the fairness of financial statement enhances. Implementation of corporate governance codes positively enhance financial performance. Higher management must have internal control systems which enable induced corporate governance codes. The higher management should consider the financial leverage also. Financial leverage provides the benefit of a tax shield, but the more financial leverage causes financial distress cost. Managers should also consider macro level variables by implanting policies with regard to corporate governance, financial performance, and financial leverage.

Author Contributions

Data curation, P.S. and W.A.W.; Formal analysis, M.E.H., P.S. and W.A.W.; Funding acquisition, P.S. and W.A.W.; Investigation, M.E.H., P.S. and W.A.W.; Methodology, Q.L.H., M.E.H., P.S. and W.A.W.; Project administration, W.A.W.; Resources, W.A.W.; Software, W.A.W.; Supervision, P.S. and W.A.W.; Validation, W.A.W.; Visualization, W.A.W.; Writing—original draft, W.A.W. and M.A.; Writing—review & editing, W.A.W. and M.A. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

| Variable Code | Variable Name | Variable Description |

| Dependent variable firm performance | ||

| ROE | Return on equity | The ratio of earnings before interest and taxes to equity. |

| Independent variable corporate governance | ||

| BS | Board size | A number of board directors, including a chairperson and independent directors. |

| BI | Board independence | The ratio of the number of independent directors to the number of all directors. |

| ACS | Audit committee size | A number of audit committee on the board. |

| WD | Female directorship | The ratio of number of female directors to the total number of directors. |

| CEOD | CEO duality | CEO duality is a dummy variable which take a value of one if the CEO is also the chairperson of the Board of directors, and zero otherwise. |

| Mediating variable | ||

| LEV | Financial leverage | The ratio of total debt to total assets. |

| Control variables | ||

| ROA | Industry return | The first difference of the natural logarithm of the price. |

| F.SIZE | Firm size | The natural logarithm of total assets. |

| F.AGE | Firm age | The natural logarithm of the number of years since the firm was listed. |

| EXPCAP | Capital investment | The ratio of capital expenditure to one-period lagged total assets. |

| C.R | Current ratio | The ratio of current assets to current liabilities. |

| MKT | The market-to-book ratio | The ratio of the market value of common equity to the book value of common equity. |

| NCF | The cash flow to total assets ratio | The ratio of net cash flow from operating to total assets. |

| FXR | The fixed assets ratio | The ratio of net property, plant, and equipment to total assets. |

| ROA | Return on assets | The ratio of earnings before interest and taxes to total assets. |

References

- Pintea, M.O.; Pop, A.M.; Gavriletea, M.D.; Sechel, I.C. Corporate governance and financial performance: Evidence from Romania. J. Econ. Stud. 2020, 48, 1573–1590. [Google Scholar] [CrossRef]

- Khoa, B.T.; Thai, D.T. Capital Structure and Trade-Off Theory: Evidence from Vietnam. J. Asian Financ. Econ. Bus. 2021, 8, 45–52. [Google Scholar] [CrossRef]

- Elok, F.H.; Astari, D. Analysis of Capital Structure on Multinational Corporation: Trade off Theory and Pecking Theory Perspective. Adv. Soc. Sci. Educ. Humanit. Res. 2021, 536, 70–77. Available online: http://repository.unibi.ac.id/38/ (accessed on 15 September 2022).

- Haron, R.; Nomran, N.M.; Othman, A.H.A.; Husin, M.; Sharofiddin, A. The influence of firm, industry and concentrated ownership on dynamic capital structure decision in emerging market. J. Asia Bus. Stud. 2021, 15, 689–709. [Google Scholar] [CrossRef]

- Kyere, M.; Ausloos, M. Corporate governance and firms financial performance in the United Kingdom. Int. J. Financ. Econ. 2021, 26, 1871–1885. [Google Scholar] [CrossRef]

- Iqbal, M.; Javed, F. The moderating role of corporate governance on the relationship between capital structure and financial performance: Evidence from manufacturing sector of Pakistan. Int. J. Res. Bus. Soc. Sci. 2017, 6, 2147–4478. [Google Scholar] [CrossRef]

- Rizwan, M.; Asrar, H.; Siddiqui, N.; Usmani, W. The Impact of Corporate Governance on Financial Performance: An Empirical. Int. J. Manag. Sci. Bus. Res. 2016, 5. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2850312 (accessed on 15 September 2022).

- Iqbal, K. The impact of corporate governance on financial performance of the pharmaceutical industry in Pakistan. Abasyn Univ. J. Soc. Sci. 2016, 9, 166–175. Available online: http://ajss.abasyn.edu.pk/admineditor/papers/V9I1-11.pdf (accessed on 15 September 2022).

- Georgakopoulos, G.; Toudas, K.; Poutos, E.I.; Kounadeas, T.; Tsavalias, S. Capital Structure, Corporate Governance, Equity Ownership and Their Impact on Firms’ Profitability and Effectiveness in the Energy Sector. Energies 2022, 15, 3625. [Google Scholar] [CrossRef]

- Khan, S.; Kamal, Y.; Hussain, S.; Abbas, M. Corporate governance looking back to look forward in Pakistan: A review, synthesis and future research agenda. Future Bus. J. 2022, 8, 24. Available online: https://link.springer.com/article/10.1186/s43093-022-00137-5 (accessed on 15 September 2022). [CrossRef]

- Nguyen, T.; Bai, M.; Hou, Y.; Vu, M.-C. Corporate governance and dynamics capital structure: Evidence from Vietnam. Glob. Financ. J. 2021, 48, 100554. [Google Scholar] [CrossRef]

- Ullah, M.; Afgan, N.; Afridi, S.A. Effects of corporate governance on capital structure and financial performance: Empirical evidence from listed cement corporations in Pakistan. Glob. Soc. Sci. Rev. 2019, 4, 273–283. [Google Scholar] [CrossRef]

- Khatib, S.F.A.; Nour, A.-N.I. The impact of corporate governance on firm performance during the COVID-19 pandemic: Evidence from Malaysia. J. Asian Financ. Econ. Bus. 2021, 8, 943–952. [Google Scholar]

- Muhammad, A. Do Pakistani Corporate Governance reforms restore the relationship of trust on banking sector through good governance and disclosure practices. Int. J. Discl. Gov. 2022, 19, 176–203. [Google Scholar] [CrossRef]

- Khan, M. Corporate Governance and Cost of Capital: Evidence from Pakistani Listed Firms. 2016. Available online: https://theses.gla.ac.uk/7722/ (accessed on 15 September 2022).

- Muhammad, R.; Mangawing, M.A.; Salsabilla, S. The influence of intellectual capital and corporate governance on financial performance of Islamic banks. J. Ekon. Dan Keuang. Islam 2021, 7, 77–91. Available online: https://journal.uii.ac.id/JEKI/article/view/15970 (accessed on 15 September 2022). [CrossRef]

- Awan, A.W.; Jamali, J.A. Impact of corporate governance on financial performance: Karachi stock exchange, Pakistan. Bus. Econ. Res. 2016, 6, 401–411. [Google Scholar] [CrossRef]

- Goel, P. Implications of corporate governance on financial performance: An analytical review of governance and social reporting reforms in India. Asian J. Sustain. Soc. Responsib. 2018, 3, 4. [Google Scholar] [CrossRef]

- Patel, M.A. Corporate Governance and Financial Performance in an Emerging Economy Context: Evidence from Pakistan’s Food, Personal Care and Cement Sectors. South Asian J. Manag. 2018, 25, 7–22. Available online: https://search.ebscohost.com/login.aspx?direct=true&profile=ehost&scope=site&authtype=crawler&jrnl=09715428&AN=133083981&h=FLcKYhEDMNf%2BfKW43hrne1UBNCb9gej99WvkfEvMr2zSuoSXzDgSX5LD9mEbvkqD5UVeEUcKfHoH43LdlXq%2FvA%3D%3D&crl=c (accessed on 15 September 2022).

- Bashir, U.; Fatima, U.; Sohail, S.; Rasul, F.; Mehboob, R. Internal corporate governance and financial performance nexus; a case of banks of Pakistan. J. Financ. Account. 2018, 6, 11–17. [Google Scholar] [CrossRef]

- Modigliani, F.; Miller, M.H.A. Corporate income taxes and the cost of capital: A correction. Am. Econ. Rev. 1963, 53, 433–443. Available online: https://www.jstor.org/stable/1809167 (accessed on 15 September 2022).

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. In Corporate Governance; Gower: Hampshire, UK, 2019; pp. 77–132. Available online: https://www.taylorfrancis.com/chapters/edit/10.4324/9781315191157-9/theory-firm-managerial-behavior-agency-costs-ownership-structure-michael-jensen-william-meckling (accessed on 15 September 2022).

- Hastutik, S.; Soetjipto, B.E.; Wadoyo, C.; Winarno, A. Trade-Off and Pecking Order Theory of Capital Structure in Indonesia: Systematic Literature Review. J. Posit. Sch. Psychol. 2022, 2022, 5585–5597. Available online: https://journalppw.com/index.php/jpsp/article/view/7624 (accessed on 15 September 2022).

- Pucheta-Martínez, M.C.; Gallego-Álvarez, I. Do board characteristics drive firm performance? An international perspective. Rev. Manag. Sci. 2020, 14, 1251–1297. [Google Scholar] [CrossRef]

- Puni, A.; Anlesinya, A. Corporate governance mechanisms and firm performance in a developing country. Int. J. Law Manag. 2020, 62, 147–169. [Google Scholar] [CrossRef]

- Goel, A.; Dhiman, R.; Rana, S.; Srivastava, V. Board composition and firm performance: Empirical evidence from Indian companies. Asia-Pac. J. Bus. Adm. 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Brahma, S.; Nwafor, C.; Boateng, A. Board gender diversity and firm performance: The UK evidence. Int. J. Financ. Econ. 2021, 26, 5704–5719. [Google Scholar] [CrossRef]

- Fiandrino, S.; Devalle, A.; Cantino, V. Corporate governance and financial performance for engaging socially and environmentally responsible practices. Soc. Responsib. J. 2018, 15, 171–185. [Google Scholar] [CrossRef]

- Abriyani, D.R.; Wiryono, S.K. The effect of good corporate governance and financial performance on the corporate social responsibility disclosure of telecommunication company in Indonesia. Indones. J. Bus. Adm. 2012, 1, 68447. [Google Scholar]

- Amin, A.; Ali, R.; Rehman, R.U.; Naseem, M.A.; Ahmad, M.I. Female presence in corporate governance, firm performance, and the moderating role of family ownership. Econ. Res.-Ekon. Istraživanja 2022, 35, 929–948. [Google Scholar] [CrossRef]

- Al-Saidi, M. Board independence and firm performance: Evidence from Kuwait. Int. J. Law Manag. 2020, 63, 251–262. [Google Scholar] [CrossRef]

- Pillai, R.; Al-Malkawi, H.-A.N.; Bhatti, M.I. Assessing Institutional Dynamics of Governance Compliance in Emerging Markets: The GCC Real Estate Sector. J. Risk Financ. Manag. 2021, 14, 501. [Google Scholar] [CrossRef]

- Handa, R. Role of Board Functions in Bank Performance: Direct and Indirect Effects of Board Independence. Manag. Labour Stud. 2022, 47, 0258042X221078486. [Google Scholar] [CrossRef]

- Kumar, A.; Gupta, J.; Das, N. Revisiting the influence of corporate sustainability practices on corporate financial performance: An evidence from the global energy sector. Bus. Strategy Environ. 2022, in press. [Google Scholar] [CrossRef]

- Nepal, M.; Deb, R. Board characteristics and firm performance: Indian textiles sector panorama. Manag. Labour Stud. 2022, 47, 74–96. [Google Scholar] [CrossRef]

- Dakhlallh, M.M.; Rashid, N.; Abdullah, W.A.W.; Al Shehab, H.J. Audit committee and Tobin’s Q as a measure of firm performance among Jordanian companies. J. Adv. Res. Dyn. Control Syst. 2020, 12, 28–41. [Google Scholar] [CrossRef]

- Ali, A.; Alim, W.; Ahmed, J.; Nisar, S. Yoke of corporate governance and firm performance: A study of listed firms in Pakistan. Indian J. Commer. Manag. Stud. 2022, 13, 8–17. [Google Scholar] [CrossRef]

- Muslih, M. The effect of internal audit and audit committee to firm performance moderated by firm age. South East Asia J. Contemp. Bus. Econ. Law 2021, 25, 233–241. [Google Scholar]

- Marpaung, A.P.; Koto, M.; Shareza Hafiz, M.; Hamdani, R. Female Directors and Firm Performance: Evidence of Family Firm in Indonesia. Asian J. Econ. Bus. Account. 2022, 22, 19–30. [Google Scholar] [CrossRef]

- Loi, R.; Zhang, L.; Lau, V.P.; Ngo, H.-Y. The interaction between leader–member exchange and perceived job security in predicting employee altruism and work performance. J. Occup. Organ. Psychol. 2011, 84, 669–685. [Google Scholar] [CrossRef]

- Margaritis, D.; Psillaki, M. Capital structure, equity ownership and firm performance. J. Bank Financ. 2010, 34, 621–632. [Google Scholar] [CrossRef]

- Javeed, S.; Ong, T.; Latief, R.; Muhamad, H.; Soh, W. Conceptualizing the Moderating Role of CEO Power and Ownership Concentration in the Relationship between Audit Committee and Firm Performance: Empirical Evidence from Pakistan. Sustainability 2021, 13, 6329. [Google Scholar] [CrossRef]

- Gan, D.; Erikson, T. Venture governance: CEO duality and new venture performance. J. Bus. Ventur. Insights 2022, 17, e00304. [Google Scholar] [CrossRef]

- Debnath, P.; Das, P.; Laskar, N.; Khan, S.B.; Dhand, S.; Kaushal, K. CEO duality and firm performance: An empirical study on listed companies from an emerging market. Corp. Gov. Organ. Behav. Rev. 2021, 5, 194–202. [Google Scholar] [CrossRef]

- Feng, Y.; Hassan, A.; Elamer, A.A. Corporate governance, ownership structure and capital structure: Evidence from Chinese real estate listed companies. Int. J. Account. Inf. Manag. 2020, 28, 759–783. [Google Scholar] [CrossRef]

- Gyimah, D.; Kwansa, N.A.; Kyiu, A.K.; Sikochi, A.S. Multinationality and capital structure dynamics: A corporate governance explanation. Int. Rev. Financ. Anal. 2021, 76, 101758. [Google Scholar] [CrossRef]

- Thakolwiroj, C.; Sithipolvanichgul, J. Board characteristics and capital structure: Evidence from Thai listed companies. J. Asian Financ. Econ. Bus. 2021, 8, 861–872. [Google Scholar]

- Ezeani, E.; Kwabi, F.; Salem, R.; Usman, M.; Alqatamin, R.M.H.; Kostov, P. Corporate board and dynamics of capital structure: Evidence from UK, France and Germany. Int. J. Financ. Econ. 2022, in press. [Google Scholar] [CrossRef]

- Khanh, V.; Hung, D.; Van, V.; Huyen, H. A study on the effect of corporate governance and capital structure on firm value in Vietnam. Accounting 2020, 6, 221–230. [Google Scholar] [CrossRef]

- Ofulue, I.; Ezeagba, C.E.; Amahalu, N.N.; Obi, J.C. Financial leverage and financial performance of quoted industrial goods firms in nigeria. Int. J. Manag. Stud. Soc. Sci. Res. 2022, 4, 172–181. [Google Scholar]

- Lidyah, R.; Mismiwat, T.H.; Akbar, D.A.; Africano, F.; Anggreni, M. The effect of audit committee, independent commissioners board and firm size on audit delay through capital structure as an intervening variable in sharia bank. PalArch’s J. Archaeol. Egypt/Egyptol. 2020, 17, 11313–11325. [Google Scholar]

- Thiruvadi, S. Male versus Female Audit Committee Chair Characteristics and Capital Structure Shiyaamsundar Thiruvadi. J. Account. Financ. 2018, 18, 144–153. [Google Scholar]

- Carmo, C.; Alves, S.; Quaresma, B. Women on Boards in Portuguese Listed Companies: Does Gender Diversity Influence Financial Performance? Sustainability 2022, 14, 6186. [Google Scholar] [CrossRef]

- Nawaz, T.; Ohlrogge, O. Clarifying the impact of corporate governance and intellectual capital on financial performance: A longitudinal study of Deutsche Bank (1957–2019). Int. J. Financ. Econ. 2022, in press. [Google Scholar] [CrossRef]

- García, C.J.; Herrero, B. Female directors, capital structure, and financial distress. J. Bus. Res. 2021, 136, 592–601. [Google Scholar] [CrossRef]

- Abd-Elmageed, M.H.; Abdel Megeid, N.S. Impact of CEO Duality, Board Independence, Board Size and Financial Performance on Capital Structure using Corporate Tax Aggressiveness as a Moderator. Account. Thought 2020, 24, 724–759. [Google Scholar] [CrossRef]

- Bawazir, H.; Khayati, A.; AbdulMajeed, F. Corporate governance and the performance of non-financial firms: The case of Oman. Entrep. Sustain. Issues 2021, 8, 595. [Google Scholar] [CrossRef]

- PeiZhi, W.; Ramzan, M. Do corporate governance structure and capital structure matter for the performance of the firms? An empirical testing with the contemplation of outliers. PLoS ONE 2020, 15, e0229157. [Google Scholar] [CrossRef]

- Towo, N.N. Financial Leverage and Financial Performanceof Savings and Credit Co-operative Societiesin Tanzania. Int. J. Rural. Manag. 2022, 12, 09730052221077846. [Google Scholar] [CrossRef]

- Abubakar, A. Financial Leverage and Financial Performance of Oil and Gas Companies in Nigeria. Open J. Manag. Sci. 2020, 1, 28–44. [Google Scholar] [CrossRef]

- Bananuka, J.; Nkundabanyanga, S.K. Audit committee effectiveness, internal audit function, firm-specific attributes and internet financial reporting: A managerial perception-based evidence. J. Financ. Report. Account. 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Itan, I.; Chelencia, V. The Mediating Role of Capital Structure in Corporate Governance on Firm Performance of Family Companies. J. Ecodemica J. Ekon. Manaj. Dan Bisnis 2022, 6, 306–318. [Google Scholar] [CrossRef]

- Usman, A.; Usman, H.S. Mediating effect of audit committee on board dynamic and creative accounting in Nigerian firms. Gusau J. Account. Financ. 2022, 3, 29. [Google Scholar]

- Sarwar, A.; Al-Faryan, M.A.S.; Saeed, S. The Impact of Corporate Governance and Financial Leverage on the Performance of Local Thai Banks Using Corporate Social Responsibility as a Mediator. Theor. Econ. Lett. 2022, 12, 19–51. [Google Scholar] [CrossRef]

- Zhou, M.; Li, K.; Chen, Z. Corporate governance quality and financial leverage: Evidence from China. Int. Rev. Financ. Anal. 2021, 73, 101652. [Google Scholar] [CrossRef]

- Varnamkhasti, J.H. Studying the impact of corporate governance on earning management with the mediating role of financial leverage: Case study companies listed on the Tehran stock exchange. Int. J. Health Sci. 2022, 6, 4094–4111. [Google Scholar] [CrossRef]

- Chijoke-Mgbame, A.M.; Mgbame, C.O.; Akintoye, S.; Ohalehi, P. The role of corporate governance on CSR disclosure and firm performance in a voluntary environment. Corp. Gov. Int. J. Bus. Soc. 2020, 20, 294–306. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).