1. Introduction

The dynamics of the financial market have changed over the last several decades in response to several major economic events, such as the global financial crisis of 2007–2008 (GFC), the world’s great pandemic (COVID-19), regional divisions like Brexit in 2020, and several other regional conflicts, such as the US–China strategic trade war and the Russia–Ukraine conflict, have increased economic uncertainty and raised some serious concerns in the financial market all over the for the entire world [

1,

2,

3,

4]. Financial analysts, individual investors, and financial policy regulators are uncertain about the impact of such changes, which continuously increase global uncertainty and affect the domestic financial market of individual countries. The world leading financial markets, mainly the G5 markets, are supposed to dominate the financial market worldwide [

5]. Similarly, the adaptation of certain economic policies of world-leading countries has the potential to affect the entire financial market around the world for example: the United States’ (USA) decision about imports and increases in tariff on exporting partners, particularly in China. In response to this policy global uncertainty in financial market was triggered where external investors and trading partners with the USA faced massive losses due to changes in economic policy [

3]. Such transaction shows an incredible volume of potential volatility in financial markets. In line with this, the financial markets of developing countries are found to be rapidly responsive to global uncertainty [

6]. Similarly, global uncertainty affect domestic financial market in developing countries, particularly small open economies such as Pakistan [

7]. The interconnectedness spillover of the Pakistan stock market (PSX) in dealing loans with international financial institutions like the IMF. Considering all the above economic uncertainties and crises, it is necessary to examine the real-time impact of global economic uncertainty on the stock market. In this study, we empirically examine the volatility spillovers transmitted from global uncertainty indices and their impact on PSX’s major sectoral indices, i.e., the energy index, the financial index, and the material composite index. Furthermore, by applying the quantile connectedness estimation, the study examines the impact of a great economic outbreak, such as the global financial crisis (GFC) of 2007–2008 and the pandemic of COVID-19.

Financial institutions like the World Bank and IMF have warned about the expected financial crisis that may arise with connectedness and led-lag relations between global uncertainty and the domestic financial market. This type of issue has attracted the attention of research scholars recently. Several studies reported that EPU originating from the market could potentially increase the uncertainty of the domestic stock market and the stock market of closed trading partners [

8,

9]. Several studies found that the significant impact of EPU from developed economies has the potential to carry significant causes with respect to volatility and return spillovers over developing stock markets. Ref. [

10] found that EPU from the US tends to affect the uncertainty level for BRICS. Similarly, Ref. [

11] found that the EUP from the US is considered a source of major co-movements in several regional and domestic stock markets. Ref. [

12] showed that developing economies are more affected by global uncertainty transmitted from large economies. Ref. [

13] revealed more evidence of global uncertainty connectedness spillover from developed economies and international markets on the small open economy.

Consequently, the domestic stock market of a smaller open economy with capital openness and higher degree of trade that has stable monetary policy regimes are supposed to be more protected from external shocks in comparison with a local arena to a foreign landscape. Several research studies indicated that foreign and local uncertainty is likely to spot a significant volatility spillover effect over the uncertainty of the domestic market [

14]. In addition, empirical research studies cited the presence of uncertainty spillover connectedness among the international and domestic stock markets worldwide [

15,

16]. However, several questions remain unaddressed and need serious attention, and these queries motivate us to formulate this study with an effective empirical solution. First, global uncertainty spillovers have been thoroughly studied for several regional and country-specific markets. However, such studies have been conducted for the international market at an aggregate level, disregarding the strong possibility that various indices (main and sectoral indices) may respond heterogeneously to the EPU of the dominant economy [

17,

18].

In line with this, the sectoral indices could be tremendously heterogeneous in their exposure to foreign EPU [

19]. Second, most of the previous literature has mainly studied the spillovers of US EPU on US stock markets or at the regional level, for European economies [

10]. Thus, little attention is paid to small size open economies such as Pakistan. Third, most studies examined the impact of EPU arising in the international landscape on main stock and ignored the sectoral indices.

In this current study, we examine the response of risk and return volatility spillovers from global uncertainty indices and their impact on domestic sectoral indices of the Pakistan stock market. We consider the sectoral indices, which almost translate the macro portion of the main indices registered with PSX. We selected three major sectoral indices: the energy index, the financial index, and the material composite index of PSX. To measure the possible impact of global economic policy uncertainty, we use the West Texas Intermediate (WTI) crude oil index and the European economic policy uncertainty composite index (EPU), based on the current literature used by major research studies [

10,

20]. The study measures the impact of EPU with variation at a different degree in response to any event where the changes in leading global stock markets become a reason for economic uncertainty for small open economies like Pakistan. Kamber et al. (2016) [

21] studied that uncertainty in the USA and the New Zealand stock market assets process, and return dropped immediately.

The current study is much broader in scope in several dimensions; first, we measure the volatility and return spillovers among foreign and domestic stock markets; second, we examine the time-varying change in domestic sectoral indices; and lastly, we examine the change which is received due to global uncertainty indices. Our methodology explains the overall connectedness among indices. We employed the quantile connectedness-based methodological estimations proposed by [

22,

23]. Pakistan is a small, developing, open-traded economy with several unique features such as an unstable political situation, controlled financial openness, low GDP growth, unstable monetary policy regimes, and a higher degree of foreign debt. Due to all these characteristics, we expect that the economy, particularly in the stock market indices, is different in response to global uncertainty indices and shocks compared to other developing economies’ stock markets.

Overall, the findings suggest that sectoral indices of PSX receive pronounced volatility spillover effects from the global uncertainly index compared to the domestic sectoral counterpart. However, the return volatility spillovers from the global uncertainly index are observed with limited variation sectors-wise, such as energy, financial, and material composite indices. Finally, we contribute to the existing body of literature in several ways. First, we examine the volatility and return spillover of PSX sectoral-wise with some new insights. We examined the energy, financial, and material composite indices of PSX, which are considered major stockholding sectors in PSX. Second, we measure the global uncertainty indices’ effect on the sectoral indices of PSX. Lastly, in line with this, we found significant insights from domestic indices in response to global uncertainty indices. For policy implications, our results are helpful to all investors, such as foreign, domestic, and corporate investors, in setting portfolio classification and asset management.

The originality and gap of this study are that we are examining the volatility spillovers disseminated from global economics uncertainty indices on domestic sectoral indices of PSX. We consider three major sectoral indices:the energy index, the financial index, and the material composite index of PSX. We examine the time-varying change in domestic sectoral indices.Lastly, we measure the impact of global uncertainty indices on the domestic stock market of Pakistan. We employed the quantile connectedness-based methodological estimations regarding Pakistan’s economy, which is notable for its unstable political situation, controlled financial openness, low GDP growth, unstable monetary policy regimes, and a higher degree of foreign debt.

The rest of the article is as follows.

Section 2 describes historical insights with cross-classical thoughts, whereas

Section 3 explains the historical financial data with empirical estimation and econometric methodology.

Section 4 reports empirical estimation, analysis, and findings, and finally,

Section 5 concludes the overall work.

2. Literature Review

Owing to the intricate nature of financial choices, market regulators often seek to explore and understand the complicated mechanisms of financial markets. Especially since the 2008 global financial crisis (GFC), a lot has been discussed and evaluated in the literature concerning the nexus between global uncertainties (including economic policy uncertainty) and foreign and domestic financial markets, such as [

10,

24,

25,

26,

27,

28,

29,

30]. Researchers have defined economic policy uncertainty (EPU) in several ways, but in a broad context, it refers to economic fluctuations caused by unpredictable regulatory, fiscal, monetary, and political policies. In other words, it reflects unanticipated changes in global policies that have enormous implications for the country’s economy. This policy uncertainty leads to delays in financial and economic decisions, causing a decline in the country’s general productivity and overall growth. For instance, one of the main implications of COVID-19 was on the general decisionmaking of corporations and countries as they intentionally delayed their decisions due to the unpredictable nature of this pandemic. Similarly, a failed coup in Turkey and the uncertainty caused by it have forced Moody’s investors to downgrade the credit rating of Turkey [

31] (Davis, 2016).

Moreover, several studies have explored the influence of uncertainties on financial markets and found huge implications, especially on stock markets. Global risk factors such as uncertain economic policies, geopolitical risks, and oil price fluctuations are the main determinants, with enormous implications for aggregate stock markets [

28,

32]). In the context of the US, China, Europe, and GCC, Arouri et al. (2014) [

26] found a negative association between stock returns and policy uncertainty in respective countries. Similarly, Ref. [

27] emphasize the significant implications of uncertain US policies and the DOW Jones Sustainability Index of North America and the Asia Pacific regions during financial turbulence. However, he found inconsistent relationship patterns among stock returns and EPU throughout seven OECD countries. The study’s findings indicate a neutral relation among intended variables across Germany, Canada, and France. Likewise, Ref. [

33] found a positive association between market volatility and policy uncertainty and a negative impact on stock returns in Indian and US markets. As per the study by [

34] Tsai (2017), the Chinese stock market is highly affected by uncertain economic policies, and the effects of this can be found in regional markets (except in Europe). However, the implications of EPU are lower in the United States than in China.

Notably, uncertain policies can distort and determine the level of each economic indicator, including consumption and investment trends, output growth, GDP level, financing cost, asset growth, prices, etc. Thus, the study by [

35] found a significant effect between economic uncertainty and a country’s output gap. Furthermore, Ref. [

36] found a higher level of uncertainty in global stock markets than in global bond markets. Similarly, the negative impact of global economic uncertainty can be found in Malaysia [

37] and the United States [

33]. This suggests that regardless of the level of stability in markets, the implications of uncertain policies are the same for both developed (the US) and emerging markets (Malaysia). Apart from the stock markets, the uncertainty impacts other asset classes, such as the gold bar (2100 ounces) and WTI crude oil in the context of the United States [

38].

There are diverse views concerning the impact of global economic uncertainty. For instance, according to [

8,

39], contrary to the general notion, their study found positive implications of global policy uncertainty on the Chinese stock market. Similarly, in the Thailand stock market, the impact of EPU was minimal after 2010 [

40]. Moreover, the impacts of EPU vary per the sectors, regimes, and the type of effects (positive or negative). However, the negative outcomes usually outnumber the positive impacts. For instance, Ref. [

29] conclude that, in an unstable environment, the influence of uncertainty on stock returns is much more significant than in a stable environment. Thus, their findings indicate the presence of a state-dependent, asymmetric, nonlinear correlation between Malaysian sectoral stock returns and global EPU. Ref. [

41] performed a thorough analysis of Chinese stock markets to understand the sectoral differences concerning the influence of uncertainty. Their study found a positive impact of uncertainty on consumer discretion and financial businesses, but telecommunication services, energy, information technology, and material sectors were all negatively affected by this policy uncertainty. Furthermore, the long-run correlations among industries and sectors are positively influenced by global uncertainties.

Moreover, given the level of integration among global markets, numerous empirical research studies imply the presence of uncertainty spillover connectedness among the international and domestic stock markets worldwide [

16]. Especially in the context of developed countries, i.e., the US stock market, various studies pointed out the possibility that uncertainty in the US economic policy has direct implications on the volatility/uncertainty of its domestic stock market, as well as the stock market of his trading partners [

8]. Therefore, the developed market’s uncertainties (i.e., the US) tend to influence the domestic and global markets, like Asian stock markets, regarding their returns and volatilities. In their study, Ref. [

11] conclude that EPU in the US causes significant co-movements across regional and domestic stock markets. Similarly, Ref. [

10] concluded that the uncertainty level of BRICS markets is impacted by uncertain US economic policy. However, the spillover level varies across the market based on the size and state of the economy. Ref. [

12] found that developing markets are more prone to the uncertainty transmitted from developed economies. In contributing to the same idea, Ref. [

13] also demonstrated significant evidence of global uncertainty spillover from developed international markets to small open economies.

There is a vast literature on evaluating the global uncertainty spillover in several markets, the focus of these studies is on an aggregate level. Thus, their findings disregard the sectoral differences; for example, how these sectors vary in their response to those global EPU [

17]. Because these sectors are composed of different kinds of stocks, some deal with luxury items, and some with cyclical, non-cyclical, or necessity items. Hence, it is understandable to have varying levels of response to those uncertainties from unanticipated domestic and international scenarios. For example, stocks belonging to importing/exporting companies or consisting of financial entities tend to be more connected to those global uncertainties, as they are more exposed to foreign affairs [

19]. Moreover, the prior literature is highly centered on analyzing the US EPU spillovers to domestic or regional markets, i.e., European markets [

10], with no regard for small open economies like the Pakistan stock market. Therefore, this study is the first to provide a developing country’s perspective regarding sectoral differences in the implications of global uncertainty on the stock market. Thus, this study addresses the following hypothesis:

Ho: Is there any response of Pakistan sectoral indices to global uncertainty factors?

4. Result and Discussion

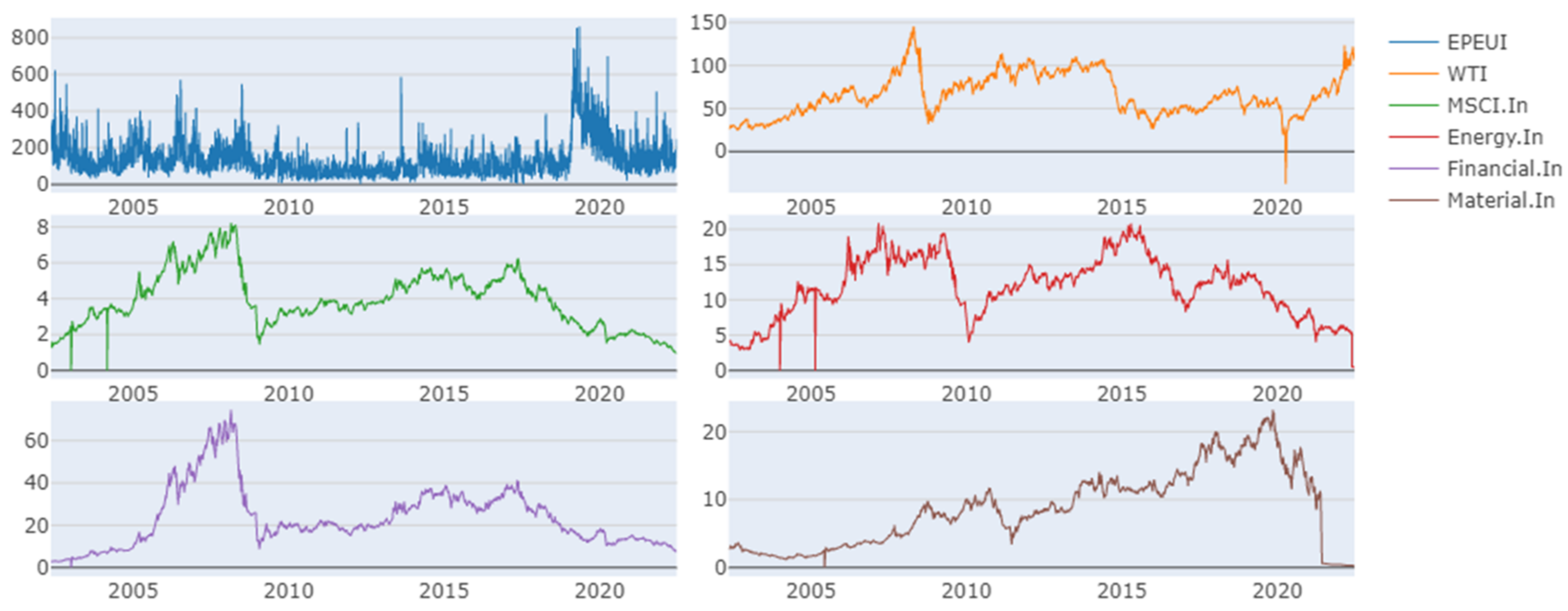

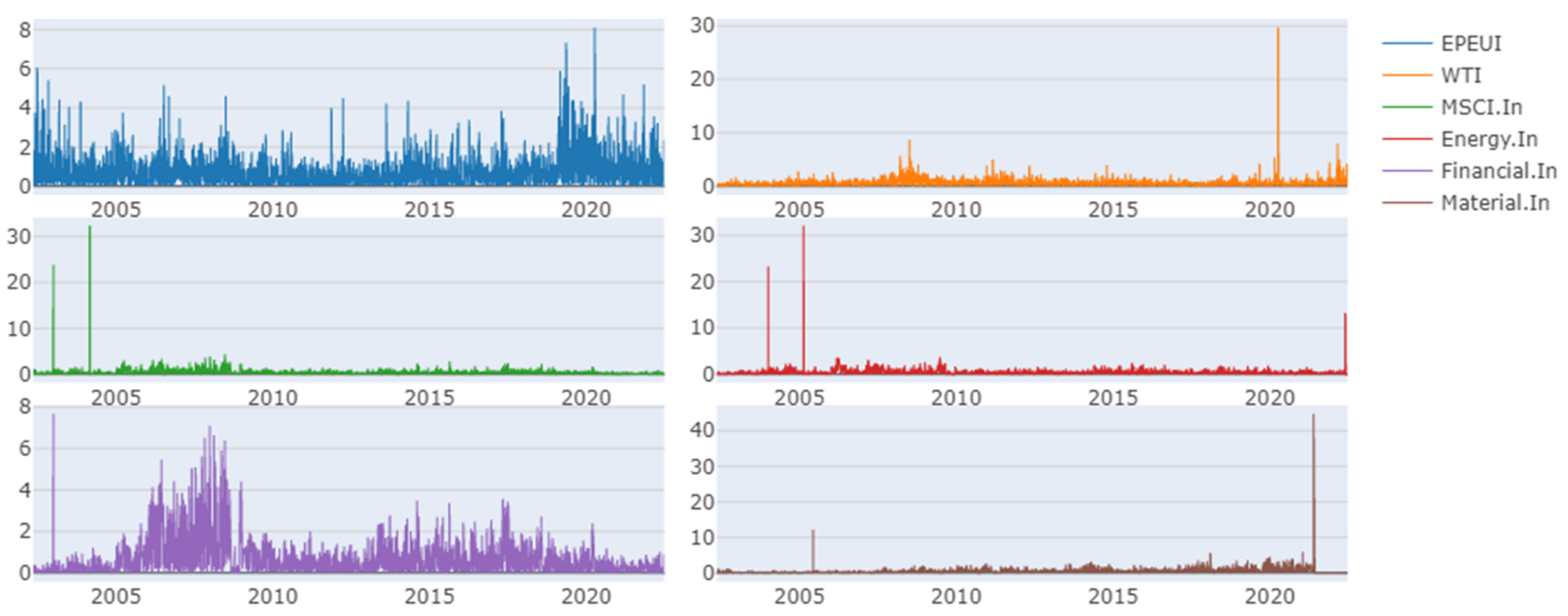

In both

Figure 1 as well as in

Figure 2, the impact of 2007–2008 financial crisis and COVID-19 are visible where global factors as well as local market display downward trends. In other words, both i.e., financial crisis and health crisis contribute negatively to stock market of Pakistan.

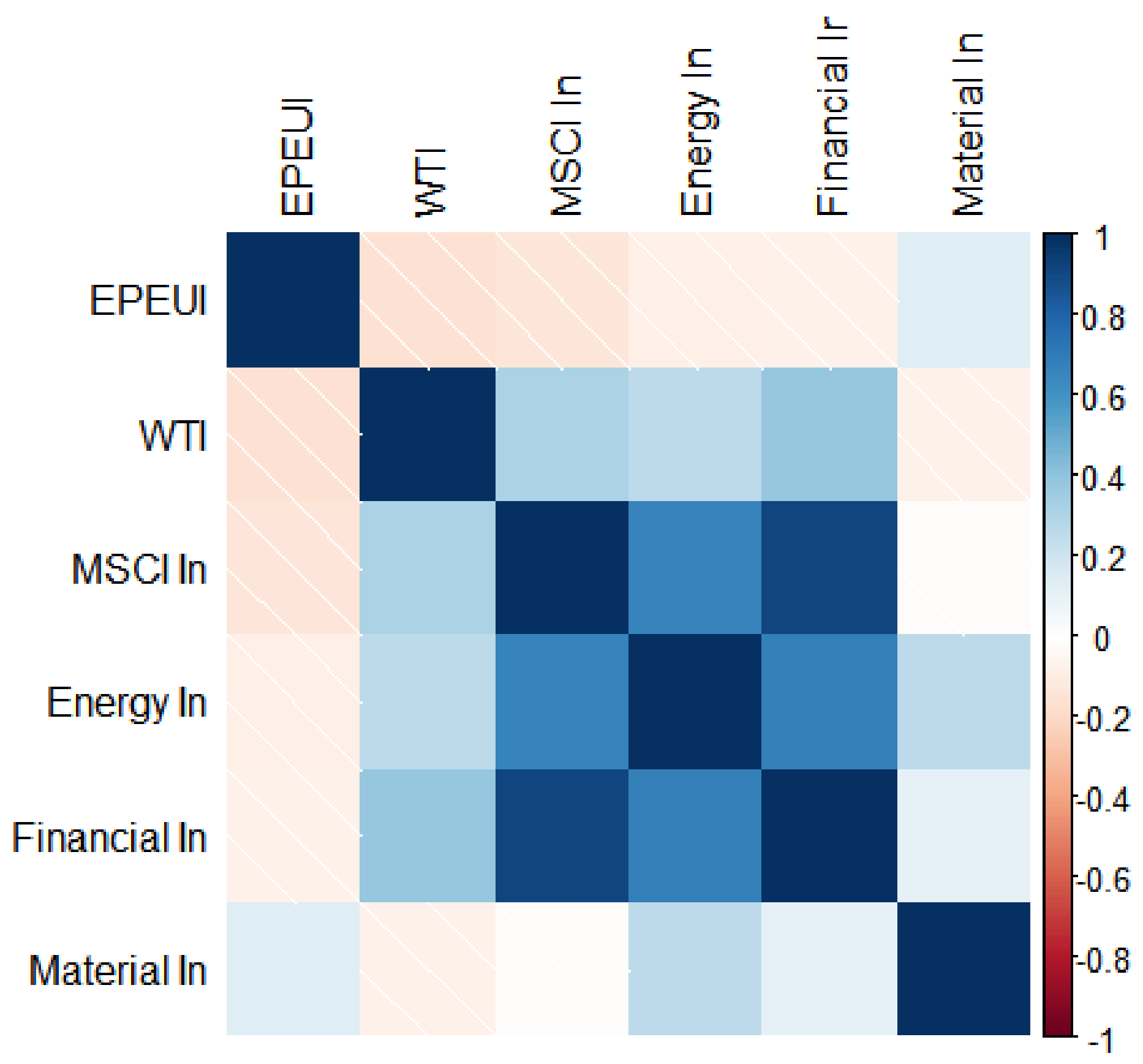

Figure 3 demonstrates the unconditional Pearson correlation coefficient matrix of the Pakistan sectoral indices and global factors. We can see that all these markets keep positive correlations with each other, indicating the robustly cooperative movements in these markets. In addition, it is no surprise that the highest degree of correlation is observed between the sectoral markets of Pakistan, namely the financial and MSCI Index, respectively. After that, we can take the name of energy markets with the MSCI index. Both are the largest correlation coefficients in the system, coming to 0.8.

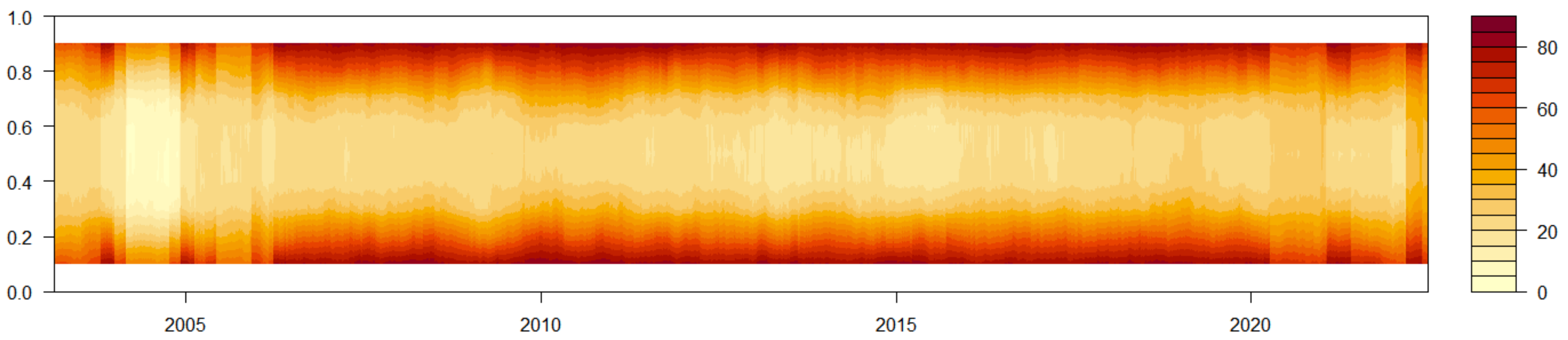

Figure 4 shows total dynamic connectedness in a picturized type of graph where the

warmer shaded area indicates higher levels of connectedness in the plot. Connectedness is strong enough in case of highly positive changes (above the 20% quantile) and highly negative changes (below the 80% quantile) for the local sectoral market indices. In other words, the impact on the local market is balanced. 50% quantile corresponds to the total average connectedness of the entire data period demonstrating a recurring pattern of connectedness. Thus, it indicates that Pakistan stock markets are not much impacted by financial crisis. One of the possible reasons is that the Pakistan market is close enough and very connected to the world economy. According to [

5,

19], the Pakistan stock market performed neutrally during financial crisis.

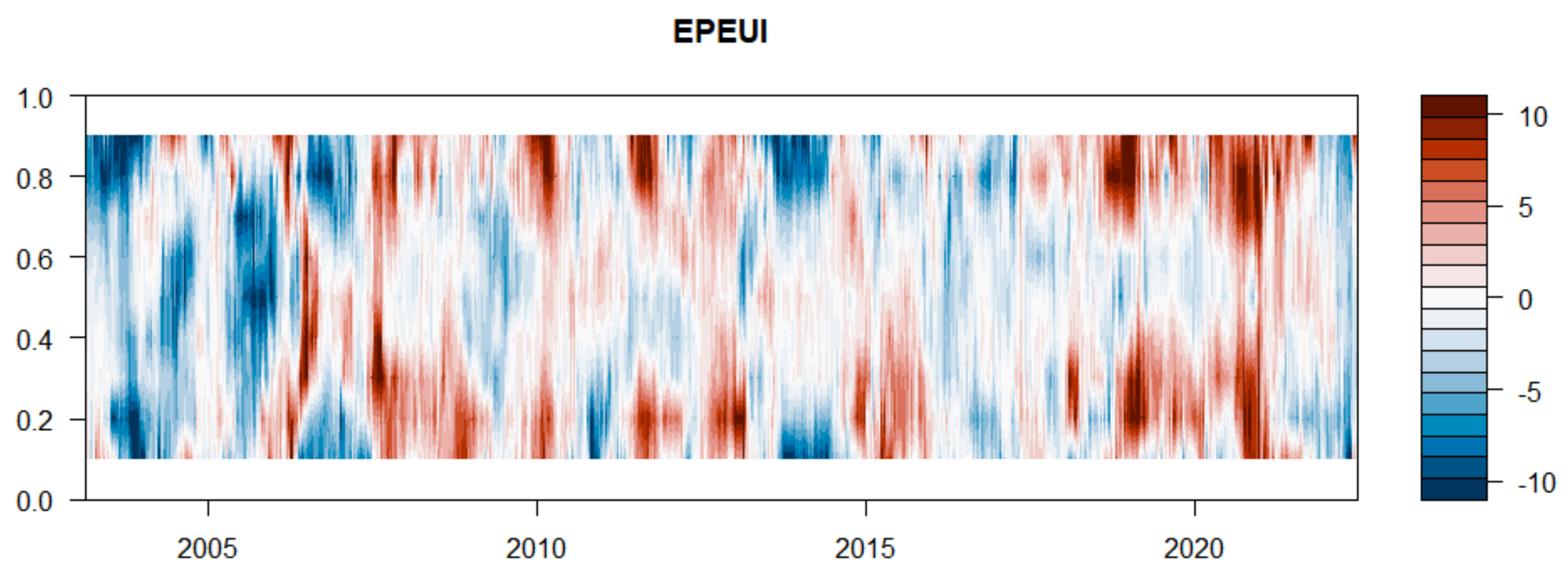

On the other hand, net directional connectedness of European economic policy uncertainty is represented in

Figure 5, where the

warmer shades on the plot indicate a nettransmitting impact of the European economic policy uncertainty on sectoral indices of Pakistan. As we see in

Figure 5, at the specific time period after 2005, the net transmitting effect of EPU became dominant; especially during the 2009 financial crisis, 2012 (the end of resurging credit spreads in major economies), 2013/14, 2015, and during COVID-19, the impact became significantly strong.

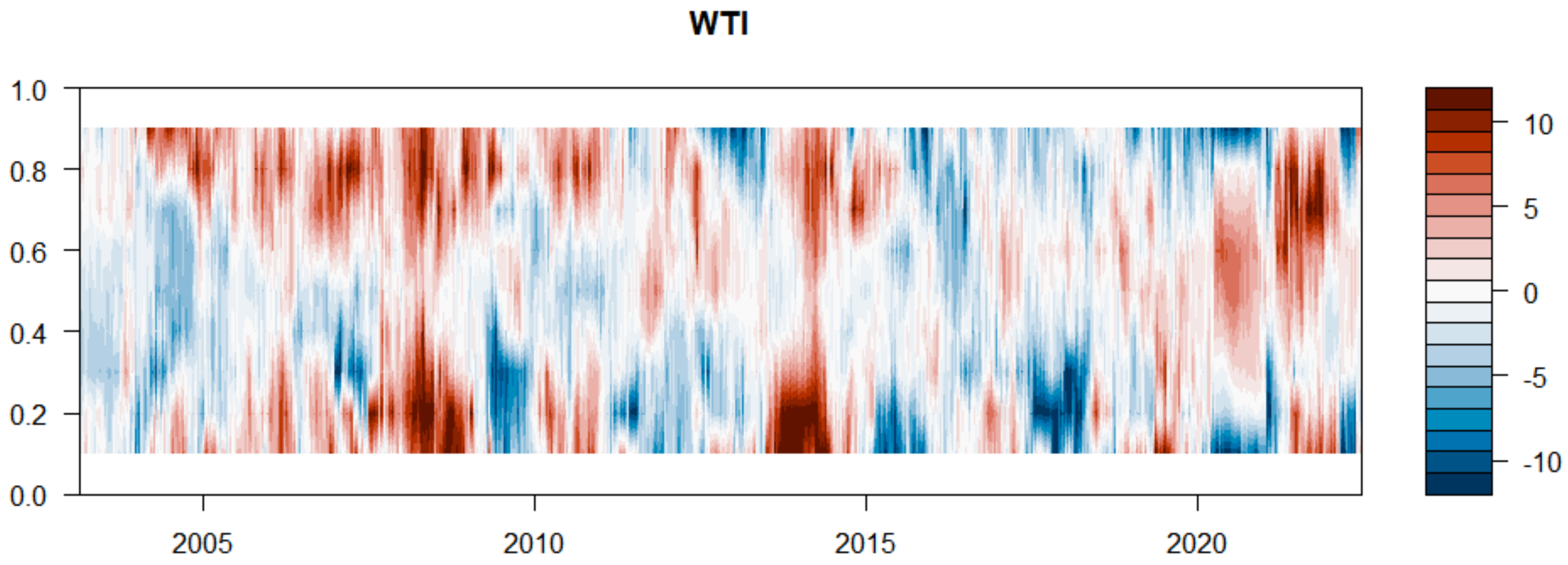

When it comes to the WTI in

Figure 6, the transmitting impact became dominant during the financial crisis 2007–2008. One of the possible reasons is that Pakistan is an oil-importing country where the uncertainty of global oil prices directly transmitted to local markets in the form of more volatility. Similarly, the crisis of 2015–2016 also hit the local economy. Interestingly, during the COVID-19 pandemic, the oil prices drastically decreased, which had very limited impact on Pakistan’s economy. One of the possible reasons is that whenever there is an increase in oil price in the international market, local prices also increase, but conversely, local prices hardly decrease when oil prices decrease globally.

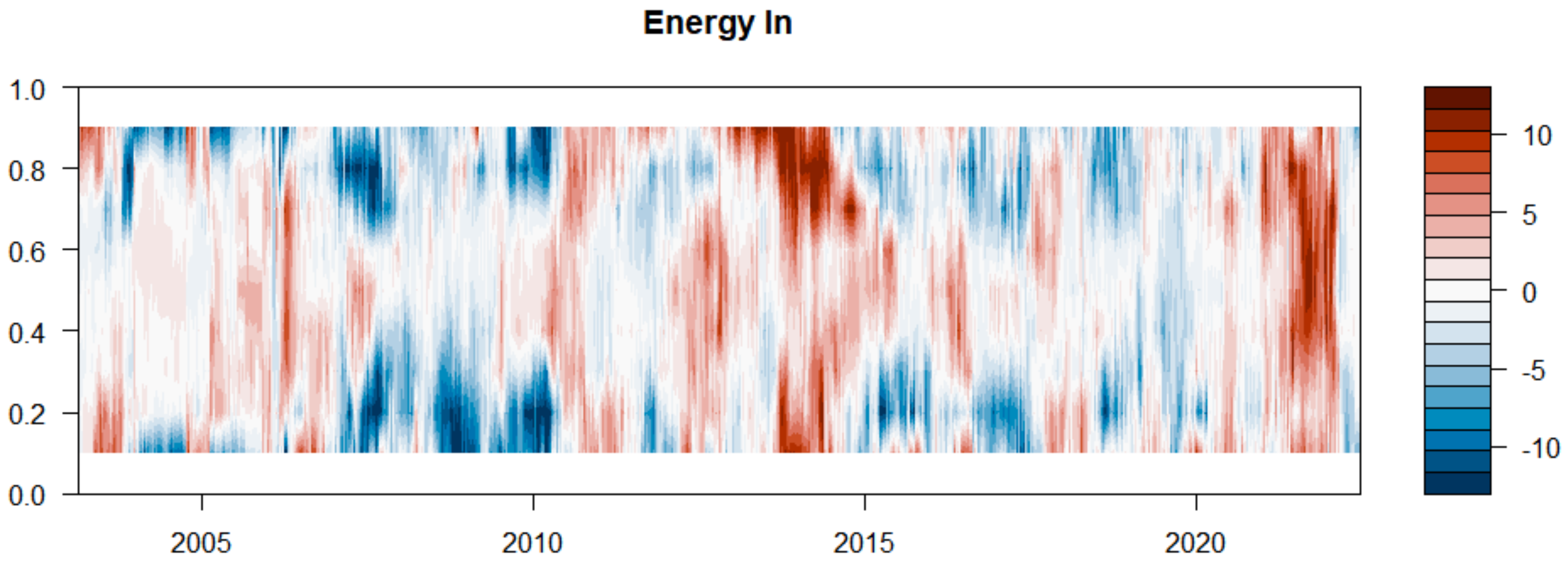

As the MSCI index is concerned, as seen in

Figure 7, it remains affected by the spillover during the study period, and the transmitting effect becomes dominant during the financial crisis and during COVID-19. Moreover, the materials sector remained the least impacted, as depicted by

Figure 8. The energy sector is affected more compared to material during the financial crisis and during the shocks after 2020, as shown in

Figure 9. In

Figure 10, we see that financial sector is a transmitter of the spillover during the entire study period, and the spillover is more significant during the financial crisis and during COVID-19.

On the other hand, descriptive statistics and unit root tests for the sectoral indices of Pakistan and global factors are provided in

Table 1. If we see the nature of the data, we can assume that all the selected returns in the system have a positive average daily return. The EPEUI and the financial index have the highest returns, with average values of 0.692 and 0.607, respectively, while the MSCI and energy index have the lowest returns, with average values of 0.416 and 0.422, respectively.

The overall standard deviations of Pakistan’s sectoral markets are higher than the global factors, implying that sectoral indices are relatively more boorish moves compared to global factor markets. The Jarque–Bera (JB) normality test shows that the series is not normally distributed. The Elliot–Rothenberg–Stock unit root (ERS) test also illustrates statistical significance in the sample period.

Similarly,

Table 2 displays the averaged connectedness, as we see that EPU is the least impacted from others i.e., 8.66% while financial sector has strong impact on others i.e., 70.77%. Finally, the least connectedness sector is found to be material 1.58%.

Static Quantile Connectedness

In this section of the paper, we use the quantile-frequency connectedness method to analyze the static, normal, and extreme interactions among the sectoral and global factors markets. We define the extreme downside, normal, and extreme upside connectedness effects of sectoral and global markets in 0.05, 0.50, and 0.75 quantiles, respectively.

The selection of these extreme quantiles is based on the idea of getting diverse results. Thus, the tail connectedness measures are estimated at the extreme lower (Q = 0.05, Q = 0.50) and upper (Q = 0.75) quantiles and collected to distinguish between extreme positive and negative shocks. In our study, the (0.05, 0.50, and 0.75) limits show more diverse results considering these (0.05, 0.50, and 0.95) limits.

Table 3,

Table 4 and

Table 5 report the extreme downside, normal, and extreme upside directional connectedness measurements in the domain of 200 days’ time, respectively. Firstly, in general,

Table 3,

Table 4 and

Table 5 show that the total connectedness indices for extreme upside (left tail, quantile = 0.05), Normal (Quantile= 0.50), and extreme upside connectedness (right tail, quantile = 0.75) are 48.75%, 34.91%, and 53.93%, respectively.

Our results show that the interaction between these markets changes in extreme downside, normal, and extreme upside cases. This interaction is high in the extreme upside case and lower in the normal case. These results also show the existence of asymmetric tail connectedness in the system. Furthermore, regarding the net connectedness of these markets, the financial index keeps the role of the strong net transmitter in all extreme downside, normal, and extreme upside cases. In contrast, MSCI keeps the position of the strong net recipient in all three cases.

5. Conclusions

Investment analysis is one of the most complex tasks for financial analysis to provide authentic information by considering all dynamics of current and previous market conditions. In line with this, we provide a mechanism for investments. Our results are prudential for stock market investors. Employing quantile connectedness approaches, this study analyzes the effect of global economic uncertainty and the response of sectoral indices from PSX. In particular, we examined the energy, financial, and material composite indices using data from 10 May 2002 to 27 June 2022. We found significant insights from the domestic indices in response to global uncertainty indices. Connectedness is strong enough for the local market in case of highly positive changes (above the 20% quantile) and highly negative changes (below the 80% quantile). In other words, the impact on the local market is balanced. The 50% quantile corresponds to the total average connectedness of the entire data period demonstrating a recurring pattern of connectedness.

Regarding WTI, the transmitting impact became dominant during the financial crisis of 2007–2008. One possible reason is that Pakistan is an oil-dependent country, and global oil prices are directly transmitted to the local market. Similarly, the 2015 crisis also hit the local economy. Interestingly, during COVID-19, oil prices drastically decreased, which has had a very limited impact on Pakistan’s economy. One of the possible reasons is that whenever there is an increase in oil prices in the international market, local prices also increase, but conversely, local prices hardly decrease when oil prices decrease globally.

The MSCI index remained the recipient of the spillover during the study period, and the transmitting effect became dominant during the financial crisis and COVID-19. Moreover, the materials sector remained the least impacted. The energy sector was a recipient during the financial crisis and a term transmitter of the shocks after 2020. The financial sector was a transmitter of the spillovers during the entire study period, and the spillover was significant during the financial crisis and COVID-19.

The study recommends that investors consider the materials sector for investment, because it is the least connected, and invest their savings rationally in the financial sector, as it is a strong net transmitter of spillovers to other sectors.

Limitation and Future Direction

In this research study, we empirically examined the spillover transmission from global uncertainty indices and their impact on PSX’s major sectoral indices i.e., the energy, the financial, and the material composite indices, with a data period of only ten years. We only considers the domestic indices related to PSX, whereas we only examine the impact of global uncertainty indices. To resolve these limitations, future research should extend the data time frame of study and add more countries. This will help to examine the impact of global economic uncertainty on regional financial markets in the long term. Additionally, we only consider the GFC-2008 and COVID-19 outbreaks. In the future, research should include more global and regional crises, especially geopolitical crisis such as Russia-Ukraine War.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}