Abstract

Corporate social responsibility (CSR) research is diversified and yet fragmented sustainable development literature. CSR literature is growing at a fast pace in the era of globalization. This article presents a bibliometric analysis of CSR in growing finance and economics literature between 2000 and 2021 using Scopus database extraction of 1134 articles out of 50,435 total articles through lemmatizing, stemming, and clustering. This study used bibliometric coupling to part the research front of CSR and then studied each theme’s conceptual structure and influential aspects separately. The analysis divided the literature into four main themes: (1) CSR performance theme (CSPR), (2) CSR and responsible investment theme (CSRI), (3) CSR market settings theme (CSMS), and (4) CSR and corporate strategy theme (CSCS). This research proposed a future research agenda for the advancement of each theme of CSR in finance and economics. Using meta-literature, 41 future research questions are proposed along with subjective propositions by the authors.

1. Introduction

Research on corporate social responsibility (CSR) has decades of history, but in the field of finance, it gained much importance after 1990. The first article on the subject was published by Filene [1] who wrote about the importance of CSR in all areas of businesses to stay financially and morally sound. Carroll defined CSR as a four-dimensional concept, with economic, social, ethical, and discretionary dimensions till 1999 [2]. The economic dimension involves firms’ financial stability to address their sustainable existence [2,3,4]. It is emphasized that the importance of the economic dimension of CSR cannot be ignored while making firms accountable to society and other stakeholders for sustainability [3].

Though, the CSR phenomenon is well established in business studies and is embedded broadly in the management literature [5]. However, in a recent study, the researchers found a dearth of research in the context of individual subjects such as CSR in management, finance, marketing, etc. [6]. Particularly, in the last few years, CSR has been researched widely from various economic and financial perspectives [7,8].

Sustainability has become an utmost concern, and businesses seek ways and means to justify their CSR initiatives regarding sustainable finance and economic performance [9]. From regulator to customer, the expectation of firms performing well in their CSR activities improves investor confidence and ensures better financial opportunities for firms and, ultimately, economic and environmental sustainability [9]. Researchers found that firms’ financial performance, risk management, stakeholder value, ethical standing, and financial value are connected with the firm’s CSR strategy [10]. There is a need to comprehend such diverse literature to understand the width and depth of the impact of CSR on different economic and financial perspectives. The substantial amount of research on CSR made it difficult for researchers to stay updated on the newest research. In addition, the bounty of papers using empirical methods make it important to comprehend the findings and to locate the gaps in research [11].

Therefore, to move forward, it is pertinent to understand the earlier research and the gaps in CSR literature in finance and economics. This research focuses on this pertinent view and explores the CSR literature in finance and economics using the science mapping approach of bibliometric analysis. The use of science mapping techniques based on quantitative bibliometric research methods is popular among researchers to comprehend the literature in themes [11,12,13]. This study uses bibliometric analysis and additionally presents a systematic review to propose future research questions based on qualitative content analysis in CSR research. The study design in this research is focused on finding the knowledge base and examining the conceptual and influential aspects of the CSR research in finance and economics.

This research is based on two decades (2000–2021) of literature extracted from the Scopus database. The superiority of the Scopus database is augmented by researchers over other databases in various fields [14,15,16]. A study compared the two famous databases (i.e., WoS and Scopus) and found that Scopus has superiority to WoS due to its data extraction convenience, data coverage, and availability of individual author profiles [16]. This research also selected Scopus to extract data due to its wide coverage of data and journals. The study uses the bibliometric coupling, thematic analysis and conceptual structure using an R package (Biblioshiny). Bibliometric coupling is used to determine the closeness of research articles based on their similar citations [17]. R package Biblioshiny is used as it provides extensive options in defining clusters within the literature based on coupling analysis and thematic structure [11,18].

After defining the clusters using coupling analysis, conceptual structure and influential aspects of each theme are explored. Furthermore, this research suggests future research questions using a twofold method. First, future recommendations are provided based on subjective judgments and theme specific conceptual structure. Second, future research agenda is defined based on the future recommendations by the recent studies on CSR in finance and economics. More specifically, this study aims to answer the following research questions using bibliometric analysis:

- What are the major themes of CSR in finance and economics literature based on bibliometric coupling analysis?

- What are the influential aspects and conceptual structure of major themes of the literature on CSR in finance and economics?

- What are the theme specific research gaps in CSR literature?

- What future research directions are provided in the recent CSR literature?

The contributions to this research are manifold and can be categorized as theoretical, methodological, and practical contributions. Theoretically the study contributes a bibliometric and narrative review of CSR literature in finance and economics. In a recent study, the researchers found that there is a dearth of bibliometric research in the context of individual subjects such as CSR in management, finance, marketing, etc. [6]. Few review studies on CSR focus on comprehending the CSR literature with specific research field. Therefore, providing a detailed review of the literature on CSR within a specific subject matter such as finance and economics will have a significant theoretical contribution.

Methodologically this research contributes in three ways. Firstly, the research uses a systematic procedure for query formulation to extract the relevant literature on CSR. The keywords used in the query formulation are extracted through expert opinion and previously published reviews to find accurate results. Most of the earlier review studies of CSR did not follow some systematic procedure to formulate the search query or missed some of the important keywords developed overtime. We updated the keyword list from prior literature to ensure that all the relevant studies are part of the analysis to provide more robust conclusions. Secondly, an important contribution of the study is that it provides cluster-wise bibliometric analysis, whereas most bibliometric analyses reveal overall results on one topic and do not relate to sub-topics or themes. This contribution will allow the reader to understand theme specific conceptual structure and influential aspects.

Third, a list of keywords is generated after combining and cleaning the author keywords, keyword index, and title using R Package (AKA). The newly generated keywords are used in the analysis of conceptual structure. The processing of the keywords is a unique contribution of the study since earlier bibliometric analyses used author keywords or keyword index without cleaning. As a practical implication, the research proposed cluster-wise implications and proposed future research questions that would be helpful for academicians in their future research endeavors.

The paper is structured as follows: the Section 2 explains the methodology and step by step process for bibliometric analysis and meta-literature review, the Section 3 summarizes findings and results, and the Section 4 presents the conclusion and future research of CSR in finance and economics literature.

2. Materials and Methods

This research used a mixed approach of quantitative and qualitative research. The quantitative methods include the famous framework of science mapping often used for visualization, and interpretation of the thematic structure of a research field [13,19,20]. The traditional literature review depicts profound knowledge of the field, while science mapping depends on extensive literature. This analysis can grip a large number of published research articles and also offers a graphical representation of the inter-connected bibliographic parameters such as authors, journals, institutes, and countries [14]. The bibliometric research method is observed as the most methodical, transparent, and easily reproduced for science mapping analysis [21,22].

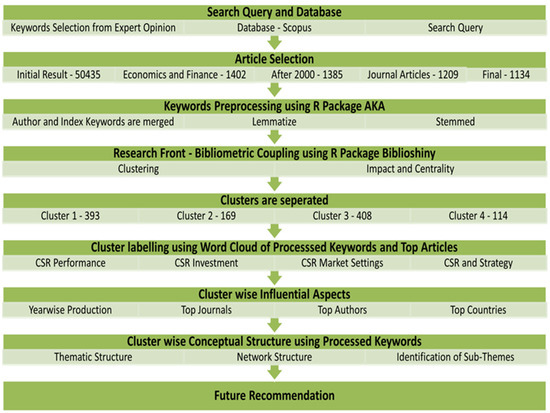

We followed a nine-step research process as provided in Figure 1. The foremost step is the selection of the database and search query formulation. This research used Scopus database (www.scopus.com, accessed on 20 December 2021) to retrieve the targeted literature. The superiority of Scopus is augmented by researchers due to its coverage [14,15,16]. Conversely, the search query is finalized after consulting three domain experts and the latest review studies on CSR. We identified 226 keywords related to CSR to make sure that all aspects of CSR are covered. These keywords are also searched in the title, author keyword, and keyword index to find the 50,435 studies at initial stage.

Figure 1.

Research Process.

The second step is to select only relevant articles from the initial set of articles. Since the focus of the current review is finance and economics, we filtered our query for the subject category of Finance and Economics in Scopus. Further, the query is limited to the journal articles, English language and timespan from 2000 to 2021 to finalize the sample of 1134 research articles. The complete query is provided in Appendix A.

The third step includes keyword pre-processing (for conceptual analysis) using R package AKC (Automatic Knowledge Classification). We generated a list of keywords extracted from the title, author keywords, and keyword index after lemmatizing, stemming, and removing duplicates. The fourth step included bibliometric coupling for clustering the targeted literature based on similar citations. This step will answer the first research question of this study. For instance, our analysis showed that the literature on CSR in finance and economics can be segregated into four sub-domains.

As a fifth step, these clusters are separated and divided into Cluster-I comprising 393 articles, Cluster II including 169 articles, Cluster III including 408 articles, and Cluster IV including 114 articles. The sixth step is labelling each theme using content analysis of word clouds. The word clouds are prepared using processed keywords and four themes emerged: the CSR Performance theme (CSPR), CSR Responsible investment theme (CSRI), CSR market settings theme (CSMS), and CSR corporate strategy theme (CSCS).

Then, as a seventh step, the influential aspects of each theme are analyzed by presenting graphical visualization of the theme’s top journals, top authors, annual production over time, and top authors’ countries. Hitherto, Bibliometric reviews mostly present influential aspects of the overall literature; however, this research presents the theme specific influential aspects. It is found that presenting the influential aspects of each theme will present more specific information to the reader. For instance, the top authors and top journals could be different for themes of a research topic. Therefore, this research aimed to supply theme-specific influential aspects.

The eighth step includes conceptual structure analysis using newly generated keywords. The conceptual structures are useful to explore the content of a theme. The conceptual structure analysis in Biblioshiny provides a thematic structure and network diagram having four quadrants plotted on centrality (x-axis) and density (y-axis) values: Motor themes (Quadrant 1, Q1) with high centrality and density; Basic and transversal themes (Quadrant 2, Q2) with strong centrality, but low density; Emerging or declining themes (Quadrant 3, Q3) showing emerging or declining theme; and Niche themes (Quadrant 4, Q4), which are clusters with high density and low centrality [19,23]. A co-occurrence network of keywords is presented in addition to the thematic structure to show the strength of connection and relative frequency of occurrence. These analyses will help to identify the content of each theme. In this way, step five to eight will answer the second research question of this study.

As a last step of the methodology, a narrative review using qualitative (content analysis) is prepared to propose a future research agenda. The suggestions for future research questions through content analysis are divided into two parts. The first part uses all papers published in 2021 and draws 41 research questions from a total of 221 articles. The future research agendas of all these articles were explored and articles with no research agenda, already explored topics, context-based, and limited scope were refined and limited to 41 questions. Based on the author’s judgment and the recent publications, further research areas are highlighted to move CSR research forward in finance and economics. The development of such a future agenda is consistent with the research questions.

3. Results and Discussion

This section is divided into three parts to address the first two research questions of the current study. This section starts with bibliometric coupling analysis and divides the CSR literature into heterogeneous clusters based on similar citations. The second part labels each theme using content analysis of word clouds of newly generated keywords, as defined in the methodology. Identifying the major themes and labelling them is consistent with the first research question. Finally, to address the second research question, the influential aspects and conceptual structure of each theme are presented.

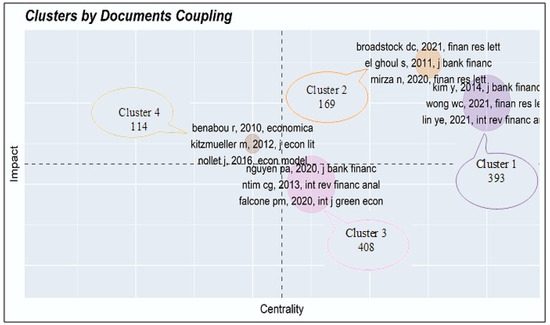

Figure 2 presents the document coupling structure, constructed using the coupling of references, where the impact is measured through global citation scores. In this method, two documents are considered similar if both cite identical references. The analysis is done in Biblioshiny (an R package). Traditionally, coupling analysis is presented with the network structure of the documents to segregate the articles into heterogeneous clusters. However, this research presents the bibliometric coupling structure (Figure 2) that segregates the literature into clusters with their level of impact and centrality. The recent version of Biblioshiny allows us to create such a coupling structure.

Figure 2.

Coupling Analysis.

Figure 2 shows that CSR literature can be segregated into four themes. The size depicts the number of documents in each theme. For instance, cluster 3 has the highest number of articles (408). Similarly, 393 articles are associated with cluster 1. Each theme also corresponds with the top three most cited articles. Theme-I and Theme-II show high centrality and high impact and are placed in the 1st Quadrant (Q1). Here, the impact refers to the overall citations by the documents in a cluster. Similarly, centrality is the level of citations of other member articles in a cluster. Theme-III is close to the origin in the 2nd Quadrant (Q2), depicting average centrality and above-average impact. Lastly, Theme-IV lies in the 4th Quadrant (Q4) with low centrality and above-average impact. It is also notable that Theme-I and Theme-III consist of high numbers of articles.

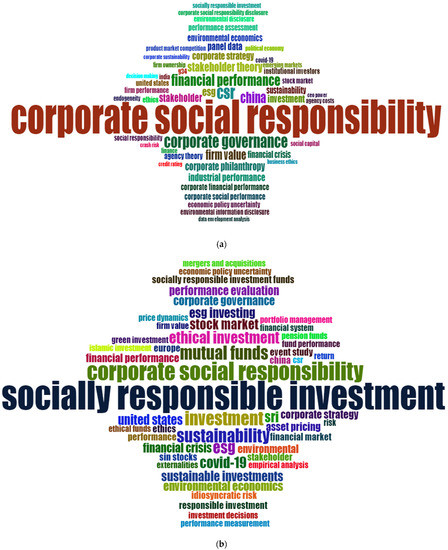

To find the content studied in each theme, word clouds of newly formed keywords are constructed, as shown in Figure 3. Each word cloud shows the top 50 keywords from each theme, respectively. For instance, Figure 3a shows the top 50 keywords for Theme-I. It shows that CSR-related keywords (e.g., corporate social responsibility), performance-related keywords (e.g., firm value, financial performance, corporate financial performance, industrial performance, social performance, and firm performance, ESG), and corporate governance-related keywords (e.g., corporate governance, agency theory, corporate philanthropy, and CEO) are frequently used keywords in the articles from Theme-I. Based on these keywords, it is inferred that the Theme-I is about CSR performances while considering corporate governance (CG) and named CSR and Performance (CSPR). For instance, a recent article from Theme-I studies the CSR, CG and financial performance [24].

Figure 3.

CSR cluster-wise word cloud. (a) CSPR; (b) CSRI; (c) CSMS; (d) CSCS.

The Figure 3b represents the word cloud of top keywords for Theme-II. It shows that keywords related to socially responsible investment (e.g., socially responsible investment, sustainable investments, ethical investment, stocks, mutual funds investment, green investments, ethical funds, ESG investment, social investments, socially responsible investment funds) are main keywords. Similarly, CSR related keywords (e.g., corporate social responsibility, CSR, sustainable development, sustainability, and ESG disclosure) crisis-related keywords (e.g., COVID-19, financial crisis, and economic funds) and risk-related keywords (e.g., risk, idiosyncratic risk, economic policy uncertainty, and externalities) are among frequently used keywords. The combination of such keywords shows that Theme-II is about CSR investments, particularly from a risk perspective (CSRI).

The third theme explored CSR in different market settings as main keywords (see Figure 3c) are market-related, e.g., duopoly, mixed oligopoly, bilateral monopoly, Cournot duopoly, mixed market, competitiveness, privatization policies, cross-ownership, partial privatization, etc. There are also keywords related to stakeholder and strategy, e.g., corporate strategy, stakeholders, stakeholder theory, consumer behavior, strategic CSR, social welfare, labor union, etc. Some of the keywords are performance-related in such settings such as industrial performance, sustainable development, reputation, etc. This shows that this theme is focusing market settings, their outcomes, and how the responsible firms can attain competitive advantages. Therefore, Theme-III is named CSR in Market Settings (CSMS).

Figure 3d shows the word cloud of Theme-IV. The commonly used keywords are corporate governance-related keywords (e.g., corporate governance, business ethics, stakeholder theory, sustainability, sustainable development, triple bottom line, social responsibility, ethics, social investment, sustainability reporting, socially responsible investments, etc.) and strategy-related keywords such as decision making, corporate strategy, and business development. These keywords are also found along with keywords related to economic growth (e.g., economic growth, economic development, financial market, small and medium-sized enterprises, environmental economics, etc.) and entrepreneurship-related keywords (e.g., entrepreneurship, social entrepreneurship, social enterprise, sustainable investments, innovation, etc.). Considering these keywords, this theme is named CSR and Corporate Strategy (CSCS).

Hence, the coupling analysis concludes that the CSR literature on business and economics can be segregated into four major themes of CSR and Performance (CSPR), CSR Investment (CSRI), CSR and Market Settings (CSMS), and CSR and Corporate Strategy (CSCS). These results answered out first research question. To answer the second research question, influential aspects and conceptual structure of each theme are studied in the following sections.

3.1. CSR and Performance (CSPR)

This theme, as discussed above, revolves around CSR and performance. The current study explains the CSPR from two perspectives. First, the influential aspects in terms of annual production, top journals, top authors, and corresponding author’s country are explored. These influential aspects will help to understand the overall structure of the articles published in CSPR theme. Second, conceptual structure is explored using keyword thematic analysis and keyword co-occurrence analysis to explain the sub-themes of the CSPR. These results are presented in the following sections.

3.1.1. Influential Aspects of CSPR Theme

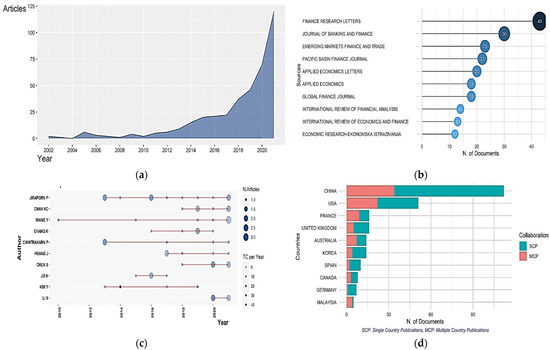

Figure 4a presents the annual production of articles in the CSPR theme, which shows an evolution of CSPR since the year 2000. It shows an upward trend since the financial crisis of 2008 and to date researchers are writing on the theme. The literature of CSPR has been published in many journals. To explicate journal impacts, Figure 4b shows the 10 most relevant journals based on the number of publications. The Finance Research Letters Journal is at the top, with 43 publications, whereas the Journal of Banking and Finance showed 30 publications. Emerging Markets, Finance and Trade and Pacific Basin Finance are placed at third and fourth position, respectively, with sizeable contributions.

Figure 4.

CSR and Performance CSPR theme. (a) Annual Scientific Production; (b) Top Journals; (c) Top Authors Production overtime; (d) Top Countries Production.

Similarly, productivity and impact are the pertinent aspects considered for the relevance of a particular field [25]. Top author production is measured by the total number of articles published by the author in a specific time and the impact is measured by total citations [25]. These important aspects are depicted in Figure 4c, which supplies an overview of the top ten authors’ work over 20 years. The author with the most publications and impact is Mr. Jiraporn P, who published 11 articles with 224 total citations. However, the second most productive and impactful author is Chan KC, with 11 articles and 68 total citations score. Although the research’s main contributors evolved as Jiraporn, Chan, and Wang, young contributors to the theme cannot be ignored. Despite the small number of publications, their influence is much higher; for example, author Kim Y has only four publications since 2015 but the total citation for these publications is 361, which is the highest among all.

Similarly, Figure 4d shows the corresponding author’s affiliation to the country, and their collaborations from multiple countries. China is ranked as the number one contributor to the theme with more collaborations from other countries, followed by the USA, France, and the UK.

3.1.2. Conceptual Aspects of CSR and Performance (CSPR) Theme

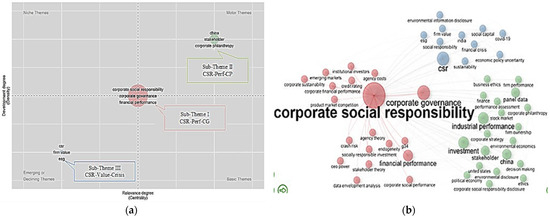

Figure 5a,b presents the keyword thematic structure and keyword network structure, respectively. Here keywords used are the list generated from author keywords, keyword index, and title after the cleaning, as explained in Materials and Methods. Thematic structure formulates clusters based on the keyword co-occurrence and presents them based on centrality and density. Results show that the CSPR can be segregated into three subthemes. For instance, subtheme-I has average centrality and density and is placed in the middle of the Figure 5a. Here, centrality refers to the degree of keyword co-occurrence within a theme, while density shows the use of keywords in other themes as well.

Figure 5.

Conceptual Aspects of CSPR Theme. (a) Thematic Structure of CSR and Performance. (b) Network Structure of CSR and Performance.

To explain it further, Figure 5b provides the network structure of keywords of each subtheme. The important points to note are the size of the node and thickness of the lines depicting keyword frequency and strength of connection, respectively. For instance, Figure 5b shows that keywords in subtheme-I (red colour) are related to CSR, performances, and corporate governance. This indicates that subtheme-I explored CSR performances with respect to corporate governance. Here performance has been explored from multiple perspectives, such as financial performance, CSR performance, or stock market performance. For instance, a study investigated the impact of ESG disclosure and actions on financial performances [26]. Next, researchers studied the moderating role of CSR between board gender diversity and financial performances [27]. Conversely, some papers explored the impact of corporate governance on CSR performances while considering block shareholders [7,28]. This subtheme is labelled as ‘CSR Performances and Corporate Governance (CSR-Perf-CG)’.

The subtheme-II is motor theme, as placed in the Q1 of the thematic structure (Figure 5a). The Figure 5b of keyword structure further shows that subtheme-II (green colour) investigated the industrial and firm performances in the context of corporate philanthropy. “China” is also among the frequently used keywords, indicating more research for Chinese listed firms. For instance, researchers studied the stock performances of Chinese listed firms that announced donations in response to the Wenchuan earthquake in China in 2008 [29]. J. Another group also explored the relationship between corporate philanthropy and investment efficiencies in China [30]. Recently, researchers studied the impact of institutional cross-ownership on philanthropy behavior [31]. This sub-theme is named ‘CSR Performances and Corporate Philanthropy (CSR-Perf-CP)’.

The subtheme-III is placed in the Q3 in Figure 5a, with low centrality and density. Such themes are either declining or emerging themes. Figure 5b shows that the main keywords of this theme include CSR-related and crisis-related keywords (such as COVID, financial crisis, and uncertainty). This indicates that subtheme-III is about the CSR performances during the crisis. For instance, a recent article shows the impact of CSR performances on stock returns during COVID-19 in China [32]. Similarly, Takahashi and Yamada (2021) investigated the impact of ESG measures and corporate governance on the stock market performances of Japanese firms. Researchers also explored CSR benefits during the financial crisis [33]. In conclusion, articles in Theme-I studied the CSR performances in the context of corporate governance (subtheme-I), corporate philanthropy (subtheme-II), and crisis (subtheme-III).

3.2. CSR and Investments (CSRI)

This theme, as shown in word cloud Figure 3b, discusses CSR and investment-related topics and is named as CSR and Investment theme (CSRI). To understand the theme in detail, the influential and conceptual aspects of CSRI theme are presented in following sub-sections.

3.2.1. Influential Aspects of CSRI

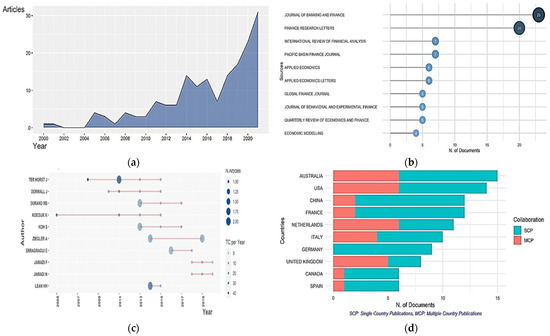

Figure 6 provides the influential aspects of CSRI theme, focusing on CSR and investments. Results show that this theme gained more publications since 2014, although the articles on the theme started in the year 2004. To explicate journal impacts, Figure 6b shows the ten most relevant journals. The Journal of Banking and Finance is at the top with 23 publications. Finance Research Letters also published 20 articles to become second in the list. Author number of publications and citations are also provided in Figure 6c. The author with the most publications and impact is Mr. Ter Horst J., who published five articles but with 992 total citations. This shows his strong influence on the theme. However, the second most productive and impactful author is Mr. Derwall J., with five articles and 349 total citations score, showing that the publication number is small, but their influence is much higher.

Figure 6.

Influential aspects of CSRI Theme. (a) Annual Scientific Production; (b) Most Relevant Sources; (c) Top Authors Production overtime; (d) Top Countries Production.

Figure 6d shows the corresponding author’s affiliation to a country and the degree of collaboration with other countries. Australia is ranked as the number one contributor to the CSRI theme with the USA in second place. Both the countries also have high collaborative work with authors from other countries. However, authors from China and France are producing literature with less collaboration from other countries.

3.2.2. Conceptual Aspects of CSRI Theme

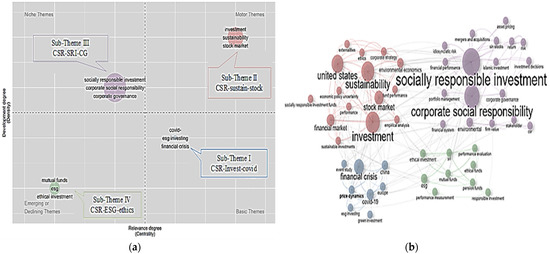

The thematic structure and network structure of Theme-II are shown in Figure 7. Results reveal that CSRI theme is divided into four dimensions based on conceptual structure. In Figure 7a, the important points to note are the size of the node and thickness of the lines depicting keyword frequency and strength of connection, respectively. This indicates that subtheme-I explored CSR performances with respect to corporate governance. subtheme-I in the Q2 of thematic structure shows a basic theme and COVID, ESG investing, and financial crises as frequently used keywords. These keywords are used jointly in ten articles published during 2020 and 2021. For instance, Yoo and Managi (2021) investigated whether the influence of ESG has more impact on profits. A recent study compared the Islamic and socially responsible investments to the conventional stocks and analyzed the impact on the risks attached to both stocks [34]. Another article showed the value of CSR in a financial crisis in China and found that CSR may not yield desirable outcomes during a crisis situation in developing economies [33]. Some studies also explored SRI or ESG investments’ outcomes during the COVID-19 pandemic [35,36]. This subtheme is labelled as CSR investments in crisis (CSR-invest-crisis). The subtheme-II lying in the first quadrant Q1 shows a motor theme related to keywords investment, sustainability, and stock market, and is named as CSR-sustain-stock.

Figure 7.

Conceptual Aspects of CSRI Theme. (a) Thematic Structure of CSRI Theme; (b) Network Structure of CSRI Theme.

The articles that form subtheme-III of CSRI mostly revolve around socially responsible investment and corporate governance. Lying in Q4 is a niche subtheme named as CSR-SRI-CG. The main contribution related to weaker governance performance may influence the ESG performance and firms’ investment returns [37,38,39]. The keywords that appear mostly in the CSRI subtheme-IV are mutual funds, ESG, and ethical investment and portfolio funds and risks associated with them play an important role in the investment decisions [40,41,42,43,44,45,46]. The subtheme is named as CSR-ESG-ethics.

3.3. CSR and Market Settings (CSMS) Theme

This theme as shown in word cloud Figure 3c, discusses CSR and market settings related topics, and is named as CSR and Market Settings theme (CSMS). To understand the theme in detail and understand its sub-themes, the influential and conceptual aspects of CSMS theme are presented in the following sub-sections.

3.3.1. Influential Aspects of CSMS Theme

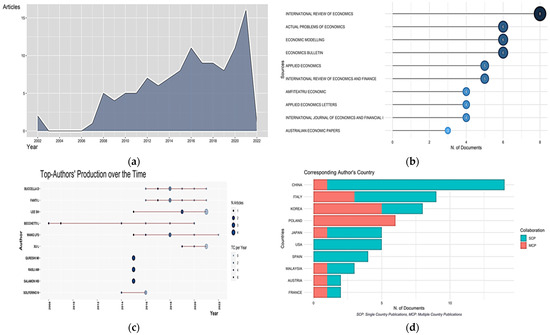

Figure 8a shows an upward trend since the financial crisis of 2008 for the publications on CSMS theme. To explicate journal impacts, Figure 8b shows the ten most relevant journals. The International Review of Economics is at the top with eight publications, whereas the Actual Problems of Economics and Economic Modelling journals had six publications each. The theme is rooted in mostly economics journals.

Figure 8.

Influential aspects of CSMS Theme. (a) Annual Scientific Production; (b) Most Relevant Sources; (c) Top Authors Production Overtime; (d) Top Countries Production.

The author with the most publications and impact is Fanti Bucella D., Fanti L., and Lee SH., who published seven articles each, followed by Becchetti L, Wnag LFS with six publications each, shown in Figure 8c. The impact was more by young researchers such as Benabou R., with only one publication and 575 total citations. However, the second most productive and impactful author is Wang LFS, with six articles and 575 total citations score. Although the research’s main contributors emerged as Becchetti L, Bucella D., Fanti L., and Lee SH., young contributors to the theme cannot be ignored. Although their publication number is small, their influence is much higher.

Figure 8d shows the corresponding author’s affiliation to the country and the degree of collaboration with other countries. China is ranked as the number one contributor to this theme where the single and multiple author contributions are highest with total publications of 13 single country productions and one multiple countries contribution, followed by Italy and Korea. Poland is the country with all multiple country contributions.

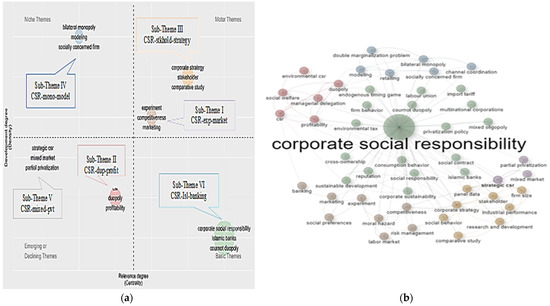

3.3.2. Conceptual Aspects of CSMS Theme

The thematic structure and network structure of CSMS theme is shown in Figure 9a,b, respectively. Both figures indicate that CSMS theme is divided into six subthemes based on conceptual structure. Figure 9b clearly indicates six different colors to depict inter-related but differentiated subthemes and node sizes indicate most frequently used keyword. Figure 9a explains further density and centrality of the subthemes with placement of each theme in four quadrants. Subtheme-I is in the Q1 of thematic structure, and shows CSR and market competitiveness, experiment, and marketing as frequently used keywords, named as CSR-exp-market. Researchers investigated the impact of green consumers and responsible firms on market equilibrium, concluding that the conscious consumers and firms play a positive role in increasing the environmental quality provision by firms but reduces social welfare initiatives in marketing [47]. For example, a recent study explored the social responsibility representation and their individual relationship to distributive fairness using an ultimatum game experiment [48].

Figure 9.

Conceptual Aspects of CSMS Theme. (a) Thematic Structure of CSMS Theme. (b) Network Structure of CSMS Theme.

The subtheme-II lying in the Q3 showed keywords CSR, duopoly, and profitability as frequently used, and is named as CSR-dup-profit. For instance, an artical examined duopoly setting for a conventional profit maximizing firm and socially responsible firm [49]. The subtheme-III stays in the Q1 depicting frequently used words as corporate strategy, stakeholder, and comparative, named as CSR-stkhold-strategy.

The subtheme-IV lying in the Q4, showing unique impact theme, used keywords such as bilateral monopoly, modelling, and socially responsible firms, and is named as CSR-mono-model. There are four articles that relate to bilateral monopoly. One of the top papers of the overall papers, discussed bilateral monopoly situation where firms can either be socially concerned or profit maximizing [50]. Similarly, in a study shows the effects on market and welfare initiatives by the mutual option of CSR [51].

The subtheme-V lying in the Q3 showed frequent keywords as strategic CSR, marketing mix, and partial privatization, and is named as CSR-mixed-pvt. Subtheme-VI found in Q2 used keywords such as CSR, Islamic banks and Cournot duopoly, and frequently is named as CSR-Isl-Banking. For instance, some researchers studied the impact of firms’ engagement in consumer-friendly CSR on profit and welfare in a duopoly network setting [52]. In another study, researchers found that the customers have lesser complaints towards the charity driven sellers [53].

3.4. CSR and Strategy (CSCS) Theme

This theme, as shown in word cloud Figure 3d, discusses CSR and corporate strategy-related topics and is named as CSR and Strategy theme (CSCS). To understand the theme and its sub-themes in detail, the influential and conceptual aspects of CSCS theme are presented in the next two sub-sections.

3.4.1. Influential Aspects of CSCS Theme

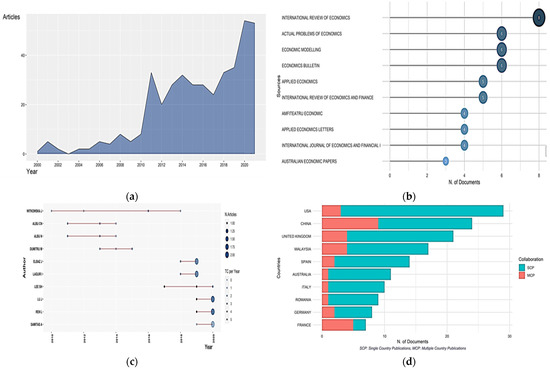

Figure 10 shows the influential aspects of the CSR and strategy theme (CSCS). Research on CSR has decades of history but in the field of corporate strategy, investment, and ethics it gained much importance after 2000. Figure 10a shows an evolution of literature since the year 2002. It shows an upward trend after the financial crisis. The theme showed the highest growth rate in the scientific production over the years among all themes.

Figure 10.

Influential aspects of CSCS Theme. (a) Annual Scientific Production; (b) Most Relevant Sources; (c) Top Authors Production overtime; (d) Top Countries Production.

Figure 10b shows the ten most relevant journals. The Amfiteatru Economic Journal is at the top, with 47 publications, whereas Economic Research-Ekonomska Istrazivanja Journal showed 21 publications each, and in third is the Actual Problems of Economics. The theme is rooted in mostly economics and some in finance journal such as International Journal of Financial studies.

Figure 10c shows the top ten authors work over 20 years of time. The author with the most publications and impact is Witkowska J., who published four articles since 2010, followed by Albu CN, with three publications. The impact was more by young researchers such as [54] with only one publication and 155 total citations. However, the second most productive and impactful authors are [55], with one article and 139 total citations score.

Figure 10d shows the corresponding authors’ affiliation to the country and their contributions to multiple countries. USA is ranked at number one contributor to this theme with 29 publications single country, and number 3 with collaboration. China ranked second with most multiple country contributions.

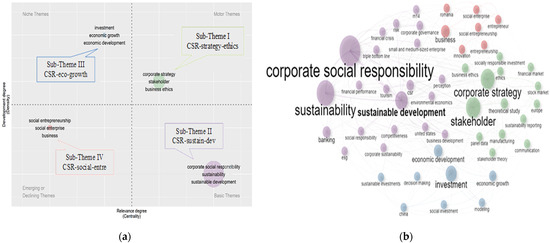

3.4.2. Conceptual Aspects of CSCS Theme

Figure 11 shows thematic and network map of newly formed keywords for CSCS Theme-IV. The strategic diagram in Figure 11a shows that, based on keywords, Theme-IV can be segregated into four subthemes. This strategic diagram comprises four quadrants showing that subtheme-I has high centrality and density and placed it in the upper Quadrant-1 (Q1) of Figure 11a. Figure 11b further provides the network structure of keywords of each subtheme. The important points to note are the size of the node and thickness of the lines depicting keyword frequency and strength of connection, respectively. For instance, subtheme-I shows bigger nodes related to strategy, ethics, and stakeholders. These nodes are also connected to other sub-themes.

Figure 11.

Conceptual Aspects of CSCS Theme. (a) Thematic Structure of CSCS Theme; (b) Network Structure of CSCS Theme.

The subtheme-II is located in the Quadrant-II (Q2), the subtheme-III is a niche theme that lies in the Quadrant-IV (Q4), and the fourth theme in the Quadrant-III (Q3) depicts the emerging theme or declining theme.

The subtheme-I named as CSR-strategy-ethics used keywords related to strategy, stakeholders, and business ethics. For example, a study explored the corporate sustainability and proposed usage of algorithms for sustainable human resource management for help of businesspeople on the basis of stakeholder theory [56]. In an empirical study in Slovenia focused on the firms’ main purpose and the firms’ response to their responsibility towards stakeholders using stakeholder model [57].

The subtheme-II shown in purple color used keywords related to CSR, sustainability, and sustainable development, and is named as CSR-sustain-dev. For instance, researchers explored the contribution of CSR to strong sustainability of businesses [58]. The subtheme-III has found itself rooted towards economic growth and development. A recent study on financialization in the climate change era emphasized the relevance of economic growth in the financial sector [59]. Another article contrasted the value maximization and stakeholder theory to bring a viable solution to the better economic and firms’ growth; it is concluded that the stock prices are significantly related to the economic growth of the nation [60].

The subtheme-IV mostly used keywords related to social entrepreneurship, social enterprise, and CSR, and is named as CSR-social-entre. For instance, researchers explored the social entrepreneurship through the known factors that impact the decision of such businesses in Romania [61]. In his study focused on the model of open social innovation and critically reviewed the literature to propose the model.

Thus, it can be concluded that financial perspectives of CSR can be divided into four major themes: performance, investment, market settings, and CSR strategy. Our analysis showed that the firm financial and market performances are significantly connected with different aspects of CST strategies. Similarly, the investment perspective explored corporate CSR investments and the investors’ behavior towards such initiatives. The third literature perspective discussed CSR initiatives within different market settings such as competition and duopoly. Finally, the fourth theme investigated CSR strategy and ethical decisions in financial decisions and social entrepreneurship. These themes portray the well-defined width and depth of CSR decisions from various economic and financial perspectives to answer the first two research questions of current research.

The two other research aims were to explore the future research agenda. Our analyses also showed the emerging CSR trends in finance and economics literature that can be viewed as future research agendas. It is a matter of concern that the niche subthemes may indicate new and emerging topics for future research, yet the results are based on 21 years of data and may not indicate only recent research topics. Therefore, we also focus on additional qualitative content analysis to highlight the future research agenda [16]. We defined a two-way method to propose recommendations and research questions for future studies, as presented in the next section.

4. Future Research Agenda

This section presents a future research agenda based on qualitative research using content analysis. A two-fold method is used in this regard; firstly, articles published in 2021 were explored to propose future research questions using a content analysis approach [60]. Overall, 221 articles published in 2021 were studied and their proposed future research questions are summarized in Table 1. This process accumulated 41 future research questions related to all four themes identified in bibliometric coupling analysis. The second method proposition of research topics was based on subjective judgement of authors after completing the review process [5]. Based on subjective judgement, the authors proposed some important future research directions regarding each theme.

Table 1.

Future Research Questions.

For instance, a total of 12 research questions were identified regarding Theme-I proposed in recent literature of 2021. These research questions focus on institutional settings, regulatory changes, socialism, climate change, ESG scores, ESG levels, CSR importance in time of crisis, better policies, and strategies similar to recent research as [7,62,63]. The societal demand and the changing environment calls for such diverse questions in the subject area. It is concluded that the literature of CSR performance has been saturated, whereas mostly recent studies are focusing on confirming or disapproving of the already established relationships. Among 221 selected studies, 120 were related to CSR performance theme. However, there is a lack of innovation in the CSR and performance (CSPR) theme and future proposed topics. Only twelve articles out of 120 proposed a theoretical future agenda, whereas most of the others discussed contextual or methodological differences. As per authors’ subjective judgement, the investigation of macro level, firm specific, and governance-related indicators influencing window dressed reporting of CSR performances could be an interesting area of research and some papers have recently been published related to these areas [64,65]. Similarly, contextual investigation of CSR performances considering industry difference such as halal products, behavioral differences of ethnic groups and economic differences such as developed vs. developing can provide insight of the subject matter. Communication strategies to market the CSR activities to increase firm performances can be another interesting area of research [66].

Table 1 explored eight future research questions (Sr. 13–20) using recent literature of Theme-II. As per authors’ subjective judgement, it will be interesting to note pre–post analysis of COVID-19 and responsible investment in a global scenario. The topics related to corporate governance and responsible investment still show potential for exploration in the future; for example, it would be interesting to investigate the relationship of fraud management [67] by firms and their CSR performance in a global context. ESG is an emerging scenario in CSR research, and it would be worth finding ESG levels and firms’ response to governance-related issues such as financial frauds.

Using recent literature of Theme-III (CSMS), Table 1 also explored 17 future research questions (Sr. 17–33). The CSMS theme showed only seventeen articles published during 2021 and out of these only thirteen showed a theoretical future agenda, whereas most of the others discussed contextual or methodological differences. This is still a developing theme and, as per author suggestion, a comparative cross-country study of different market settings in terms of CSR reporting will be an interesting area to explore in the future, for example [99].

From the recent literature, Table 1 also explored eight future research questions (Sr. 34–41) of Theme-IV (CSCS). As per authors’ suggestion, this theme may include CSR decoupling practices and their impact-related topics. Only one article was found out of a sample of 1134 that relates CSR to financial frauds theoretically; it would be interesting to find firms’ decoupling practices and financial frauds commitments. Sustainability concerns and relationship to CSR disclosure is explored in few studies; how sustainability is ensured in social entrepreneurial business may be interesting to note. There are some studies that found effective CSR reporting levels [100], but levels of CSR reporting and their relationship to financial frauds have not been investigated, to the best of our knowledge, and would be interesting to explore further.

Along with above contributions, this study has some limitations. Firstly, it is limited to the data from 2000 to 2021, and does not include any research papers that are impactful but are published before or after the said period; future studies may use extensive data to explore the phenomenon. The study is based on Scopus database and does not include data from other sources such as Web of Science (WoS) journals. The scope of this research is confined to CSR in finance and economics literature, whereas other areas such as marketing are beyond its scope.

Author Contributions

Conceptualization and methodology, A.S. and S.H.; validation, U.F.; formal analysis, S.H. and A.S.; software and visualization, U.F.; investigation, A.S.; resources, A.S.; data curation and writing—original draft preparation, S.H.; writing—review and editing, S.H. and U.F.; supervision and project administration, A.S.; revision and resubmission, A.S., F.A. and S.H; proof reading and improvement of connectivity, F.A. All authors have read and agreed to the published version of the manuscript.

Funding

The research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable due to the third-party data.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A. Scopus Query

TITLE-ABS-KEY (“corporate social responsibility” OR “enterprise social responsibility” OR “business social responsibility” OR “socially responsible business” OR “socially responsible corporation” OR “socially responsible enterprise” OR “corporate social commitment” OR “enterprise social commitment” OR “business social commitment” OR “socially committed business” OR “socially committed corporation” OR “socially committed enterprise” OR “corporate social Management” OR “enterprise social Management” OR “business social Management” OR “socially Managed business” OR “socially Managed corporation” OR “socially Managed enterprise” OR “corporate social policy” OR “enterprise social policy” OR “business social policy” OR “social policy of business” OR “social policy of corporation” OR “social policy of enterprise” OR “corporate social performance” OR “enterprise social performance” OR “business social performance” OR “social performance of business” OR “social performance of corporation” OR “social performance of enterprise” OR “corporate social strategy” OR “enterprise social strategy” OR “business social strategy” OR “social strategy of business” OR “social strategy of corporation” OR “social strategy of enterprise” OR “corporate social advocacy” OR “enterprise social advocacy” OR “business social advocacy” OR “social advocacy of business” OR “social advocacy of corporation” OR “social advocacy of enterprise” OR “corporate social action” OR “enterprise social action” OR “business social action” OR “corporate social activities” OR “enterprise social activities” OR “business social activities” OR “social activities of business” OR “social activities of corporation” OR “social activities of enterprise” OR “corporate social behavior” OR “enterprise social behavior” OR “business social behavior” OR “social behavior of business” OR “social behavior of corporation” OR “social behavior of enterprise” OR “corporate social behaviour” OR “enterprise social behaviour” OR “business social behaviour” OR “social behaviour of business” OR “social behaviour of corporation” OR “social behaviour of enterprise” OR “corporate social engagement” OR “enterprise social engagement” OR “business social engagement” OR “social engagement of business” OR “social engagement of corporation” OR “social engagement of enterprise” OR “corporate social involvement” OR “enterprise social involvement “ OR “business social involvement” OR “social involvement of business” OR “social involvement of corporation” OR “social involvement of enterprise” OR “corporate social initiatives” OR “enterprise social initiatives” OR “business social initiatives” OR “corporate environmental responsibility” OR “enterprise environmental responsibility” OR “business environmental responsibility” OR “environmentally responsible business” OR “environmentally responsible corporation” OR “environmentally responsible enterprise “ OR “corporate environmental commitment” OR “enterprise environmental commitment” OR “business environmental commitment” OR “environmentally committed business” OR “environmentally committed corporation” OR “environmentally committed enterprise” OR “corporate environmental Management” OR “enterprise environmental Management” OR “business environmental Management” OR “environmentally Managed business” OR “environmentally Managed corporation” OR “environmentally Managed enterprise” OR “corporate environmental policy” OR “enterprise environmental policy” OR “business environmental policy” OR “environmental policy of business” OR “environmental policy of corporation” OR “environmental policy of enterprise” OR “corporate environmental performance” OR “enterprise environmental performance” OR “business environmental performance” OR “environmental performance of business” OR “environmental performance of corporation” OR “environmental performance of enterprise” OR “corporate environmental strategy” OR “enterprise environmental strategy” OR “business environmental strategy” OR “environmental strategy of business” OR “environmental strategy of corporation” OR “environmental strategy of enterprise” OR “corporate environmental advocacy” OR “enterprise environmental advocacy” OR “business environmental advocacy” OR “environmental advocacy of business” OR “environmental advocacy of corporation” OR “environmental advocacy of enterprise” OR “corporate environmental action” OR “enterprise environmental action” OR “business environmental action” OR “corporate environmental activities” OR “enterprise environmental activities” OR “business environmental activities” OR “environmental activities of business” OR “environmental activities of corporation” OR “environmental activities of enterprise” OR “corporate environmental behavior” OR “enterprise environmental behavior” OR “business environmental behavior” OR “environmental behavior of business” OR “environmental behavior of corporation” OR “environmental behavior of enterprise” OR “corporate environmental behaviour” OR “enterprise environmental behaviour” OR “business environmental behaviour” OR “environmental behaviour of business” OR “environmental behaviour of corporation” OR “environmental behaviour of enterprise” OR “corporate environmental initiatives” OR “enterprise environmental initiatives” OR “business environmental initiatives” OR “corporate citizenship” OR “enterprise citizenship” OR “business citizenship” OR “corporate philanthropy” OR “enterprise philanthropy” OR “business philanthropy” OR “social philanthropy of business” OR “social philanthropy of corporation” OR “social philanthropy of enterprise” OR “corporate sustainability” OR “enterprise sustainability” OR “business sustainability” OR “sustainable business” OR “sustainable corporation” OR “sustainable enterprise” OR “corporate ethics” OR “enterprise ethics” OR “business ethics” OR “ethical business” OR “ethical corporation” OR “ethical enterprise” OR “social entrepreneurship” OR “Triple bottom line” OR “stakeholder theory” OR “creating shared value” OR ((“social accounting” OR “environmental accounting” OR “social reporting” OR “environmental reporting” OR “social disclosure” OR “environmental disclosure” OR “Social Audit” OR “environmental audit” OR “social accountability” OR “environmental accountability” OR “environmental transparency” OR “environmental transparency”) AND (corporate OR enterprise OR firm)) OR “Principles for Responsible investing” OR “responsible investment” OR “responsible investing” OR “Social investment” OR “environmental investment” OR “Ethical investment” OR “ethical investing” OR “sustainable investment” OR “sustainable investing” OR “green investment” OR “green investing” OR “green business” OR “green corporation” OR “green enterprise” OR “environmental, social and governance” OR “ESG score” OR “ESG risk score” OR “ESG rating” OR “Environment Risk Score” OR “Social Risk Score” OR “Governance Risk Score” OR “corporate social capital” OR “enterprise social capital” OR “business social capital” OR “social capital of business” OR “social capital of corporation” OR “social capital of enterprise”) AND (LIMIT-TO (SRCTYPE, “j”)) AND (LIMIT-TO (SUBJAREA, “ECON”) OR EXCLUDE (SUBJAREA, “BUSI”) OR EXCLUDE (SUBJAREA, “SOCI”) OR EXCLUDE (SUBJAREA, “ARTS”) OR EXCLUDE (SUBJAREA, “ENVI”) OR EXCLUDE (SUBJAREA, “DECI”) OR EXCLUDE (SUBJAREA, “ENGI”) OR EXCLUDE ( SUBJAREA, “ENER”) OR EXCLUDE (SUBJAREA, “AGRI”) OR EXCLUDE (SUBJAREA, “COMP”) OR EXCLUDE (SUBJAREA, “PSYC”) OR EXCLUDE (SUBJAREA, “MATH”) OR EXCLUDE (SUBJAREA, “MEDI”) OR EXCLUDE (SUBJAREA, “EART”) OR EXCLUDE (SUBJAREA, “BIOC”)) AND (LIMIT-TO (LANGUAGE, “English”)) AND (EXCLUDE (PUBYEAR, 1999) OR EXCLUDE (PUBYEAR, 1998) OR EXCLUDE ( PUBYEAR, 1996) OR EXCLUDE (PUBYEAR, 1995) OR EXCLUDE (PUBYEAR, 1994) OR EXCLUDE (PUBYEAR, 1993) OR EXCLUDE (PUBYEAR, 1992) OR EXCLUDE ( PUBYEAR, 1981) OR EXCLUDE (PUBYEAR, 1977) OR EXCLUDE (PUBYEAR, 1974) OR EXCLUDE (PUBYEAR, 1969) OR EXCLUDE (PUBYEAR, 1960)).

References

- Filene, E.A. A Simple Code of Business Ethics. Ann. Am. Acad. Political Soc. Sci. 1922, 101, 223–228. [Google Scholar] [CrossRef]

- Carroll, A.B.; Brown, J.A. Corporate Social Responsibility: A Review of Current Concepts, Research, and Issues. Corp. Soc. Responsib. 2018, 2, 39–69. [Google Scholar] [CrossRef]

- Carroll, A.B. Corporate social responsibility (CSR) and the COVID-19 pandemic: Organizational and managerial implications. J. Strategy Manag. 2021, 14, 315–330. [Google Scholar] [CrossRef]

- Nurunnabi, M.; Alfakhri, Y.; Alfakhri, D.H. CSR in Saudi Arabia and Carroll’s Pyramid: What is ‘known’ and ‘unknown’? J. Mark. Commun. 2020, 26, 874–895. [Google Scholar] [CrossRef]

- Frynas, J.G.; Yamahaki, C. Corporate social responsibility: Review and roadmap of theoretical perspectives. Bus. Ethics 2016, 25, 258–285. [Google Scholar] [CrossRef]

- Ji, Y.G.; Tao, W.; Rim, H. Theoretical Insights of CSR Research in Communication from 1980 to 2018: A Bibliometric Network Analysis. J. Bus. Ethics 2021, 177, 327–349. [Google Scholar] [CrossRef]

- Barauskaite, G.; Streimikiene, D. Corporate social responsibility and financial performance of companies: The puzzle of concepts, definitions and assessment methods. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 278–287. [Google Scholar] [CrossRef]

- Fernández-Gago, R.; Cabeza-García, L.; Godos-Díez, J.L. How significant is corporate social responsibility to business research? Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1809–1817. [Google Scholar] [CrossRef]

- Vărzaru, A.A.; Bocean, C.G.; Nicolescu, M.M. Rethinking corporate responsibility and sustainability in light of economic performance. Sustainability 2021, 13, 1–21. [Google Scholar] [CrossRef]

- Arora, S.; Sur, J.K.; Chauhan, Y. Does corporate social responsibility affect shareholder value? Evidence from the COVID-19 crisis. Int. Rev. Financ. 2021, 22, 325–334. [Google Scholar] [CrossRef]

- Aria, M.; Cuccurullo, C. bibliometrix: An R-tool for comprehensive science mapping analysis. J. Informetr. 2017, 11, 959–975. [Google Scholar] [CrossRef]

- Liu, Y.; Rafols, I.; Rousseau, R. A framework for knowledge integration and diffusion. J. Doc. 2012, 68, 31–44. [Google Scholar] [CrossRef]

- Zupic, I.; Čater, T. Bibliometric Methods in Management and Organization. Organ. Res. Methods 2015, 18, 429–472. [Google Scholar] [CrossRef]

- Gu, Z.; Meng, F.; Farrukh, M. Mapping the Research on Knowledge Transfer: A Scientometrics Approach. IEEE Access 2021, 9, 34647–34659. [Google Scholar] [CrossRef]

- Lithin, B.M.; Chakraborty, S.; Kumar Ghosh, B.; Shenoy, U.R. Overview of bond mutual funds: A systematic and bibliometric review. Cogent Bus. Manag. 2021, 8, 1979386. [Google Scholar] [CrossRef]

- Pranckutė, R. Web of science (Wos) and scopus: The titans of bibliographic information in today’s academic world. Publications 2021, 9, 12. [Google Scholar] [CrossRef]

- Vladutz, G.; Cook, J. Bibliographic coupling and subject relatedness. Proc. Am. Soc. Inf. Sci. 1984, 21, 204–207. [Google Scholar]

- Moral-muñoz, J.A.; Herrera-viedma, E.; Santisteban-espejo, A.; Cobo, M.J.; Herrera-viedma, E.; Santisteban-espejo, A.; Cobo, M.J. Software tools for conducting bibliometric analysis in science: An upto-date review. Prof. Inf. 2020, 29, 1–20. [Google Scholar] [CrossRef]

- Cobo, M.J.; López-Herrera, A.G.; Herrera-Viedma; Herrera, F.E. Science Mapping Software Tools: Review, Analysis, and Cooperative Study Among Tools. J. Am. Soc. Inf. Sci. Technol. 2011, 7, 1382–1402. [Google Scholar] [CrossRef]

- Stemler, S. An overview of content analysis. Pract. Assess. Res. Eval. 2001, 7, 2000–2001. [Google Scholar] [CrossRef]

- Broadus, R.N. Toward a definition of “bibliometrics”. Scientometrics 1987, 12, 373–379. [Google Scholar] [CrossRef]

- Diodato, V. Dictionary of Bibliometrics; Routledge: Oxfordshire, UK, 1994. Available online: https://eric.ed.gov/?id=ED386214 (accessed on 3 February 2022).

- Sott, M.K.; Bender, M.S.; Furstenau, L.B.; Machado, L.M.; Cobo, M.J.; Bragazzi, N.L. 100 Years of Scientific Evolution of Work and Organizational Psychology: A Bibliometric Network Analysis from 1919 to 2019. Front. Psychol. 2020, 11. [Google Scholar] [CrossRef] [PubMed]

- Rodríguez-Fernández, M.; Gaspar-González, A.I.; Sánchez-Teba, E.M. Sustainable social responsibility through stakeholders engagement. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 2425–2436. [Google Scholar] [CrossRef]

- Forliano, C.; De Bernardi, P.; Yahiaoui, D. Entrepreneurial universities: A bibliometric analysis within the business and management domains. Technol. Forecast. Soc. Change 2021, 165, 120522. [Google Scholar] [CrossRef]

- Yoo, S.; Managi, S. Disclosure or action: Evaluating ESG behavior towards financial performance. Financ. Res. Lett. 2021, 44, 102108. [Google Scholar] [CrossRef]

- Jiang, X.; Yang, J.; Yang, W.; Zhang, J. Do employees’ voices matter? Unionization and corporate environmental responsibility. Int. Rev. Econ. Financ. 2021, 76, 1265–1281. [Google Scholar] [CrossRef]

- Halkos, G.; Nomikos, S. Corporate social responsibility: Trends in global reporting initiative standards. Econ. Anal. Policy 2021, 69, 106–117. [Google Scholar] [CrossRef]

- Gao, F.; Faff, R.; Navissi, F. Corporate philanthropy: Insights from the 2008 Wenchuan Earthquake in China. Pac. Basin Financ. J. 2012, 20, 363–377. [Google Scholar] [CrossRef]

- Chen, J.; Dong, W.; Tong, J.Y.; Zhang, F.F. Corporate philanthropy and investment efficiency: Empirical evidence from China. Pac. Basin Financ. J. 2018, 51, 392–409. [Google Scholar] [CrossRef]

- Fu, Y.; Qin, Z. Institutional cross-ownership and corporate philanthropy. Financ. Res. Lett. 2021. [CrossRef]

- Yu, E.P.Y.; Luu, B.V. International variations in ESG disclosure–Do cross-listed companies care more? Int. Rev. Financ. Anal. 2021, 75, 101731. [Google Scholar] [CrossRef]

- Zhang, J.; Zi, S.; Shao, P.; Xiao, Y. The value of corporate social responsibility during the crisis: Chinese evidence. Pac. Basin Financ. J. 2020, 64, 101432. [Google Scholar] [CrossRef]

- Jawadi, F.; Jawadi, N.; Idi Cheffou, A. A statistical analysis of uncertainty for conventional and ethical stock indexes. Q. Rev. Econ. Financ. 2019, 74, 9–17. [Google Scholar] [CrossRef]

- Broadstock, D.C.; Chan, K.; Cheng, L.T.W.; Wang, X. The role of ESG performance during times of financial crisis: Evidence from COVID-19 in China. Financ. Res. Lett. 2021, 38, 101716. [Google Scholar] [CrossRef] [PubMed]

- Omura, A.; Roca, E.; Nakai, M. Does responsible investing pay during economic downturns: Evidence from the COVID-19 pandemic. Financ. Res. Lett. 2021, 42, 101914. [Google Scholar] [CrossRef]

- Erragraguy, E.; Revelli, C. Should Islamic investors consider SRI criteria in their investment strategies? Financ. Res. Lett. 2015, 14, 11–19. [Google Scholar] [CrossRef]

- Galema, R.; Plantinga, A.; Scholtens, B. The stocks at stake: Return and risk in socially responsible investment. J. Bank. Financ. 2008, 32, 2646–2654. [Google Scholar] [CrossRef]

- O’sullivan, M. The innovative enterprise and corporate governance. Camb. J. Econ. 2000, 24, 393–416. [Google Scholar] [CrossRef]

- Bauer, R.; Otten, R.; Rad, A.T. Ethical investing in Australia: Is there a financial penalty? Pac. Basin Financ. J. 2006, 14, 33–48. [Google Scholar] [CrossRef]

- Borgers, A.C.T.; Pownall, R.A.J. Attitudes towards socially and environmentally responsible investment. J. Behav. Exp. Financ. 2014, 1, 27–44. [Google Scholar] [CrossRef]

- Borgers, A.; Derwall, J.; Koedijk, K.; Ter Horst, J. Do social factors influence investment behavior and performance? Evidence from mutual fund holdings. J. Bank. Financ. 2015, 60, 112–126. [Google Scholar] [CrossRef]

- Geczy, C.C.; Stambaugh, R.F.; Levin, D. Investing in Socially Responsible Mutual Funds. Rev. Asset Pricing Stud. 2021, 11, 309–351. [Google Scholar] [CrossRef]

- Ielasi, F.; Rossolini, M.; Limberti, S. Sustainability-themed mutual funds: An empirical examination of risk and performance. J. Risk Financ. 2018, 19, 247–261. [Google Scholar] [CrossRef]

- Joliet, R.; Titova, Y. Equity SRI funds vacillate between ethics and money: An analysis of the funds’ stock holding decisions. J. Bank. Financ. 2018, 97, 70–86. [Google Scholar] [CrossRef]

- Renneboog, L.; Ter Horst, J.; Zhang, C. Socially responsible investments: Institutional aspects, performance, and investor behavior. J. Bank. Financ. 2008, 32, 1723–1742. [Google Scholar] [CrossRef]

- Doni, N.; Ricchiuti, G. Market equilibrium in the presence of green consumers and responsible firms: A comparative statics analysis. Resour. Energy Econ. 2013, 35, 380–395. [Google Scholar] [CrossRef]

- Kim, H.; Lee, J. Distributive fairness and the social responsibility of the representative of a group. Appl. Econ. 2021, 53, 1264–1279. [Google Scholar] [CrossRef]

- Kopel, M.; Brand, B. Socially responsible firms and endogenous choice of strategic incentives. Econ. Model. 2012, 29, 982–989. [Google Scholar] [CrossRef]

- Goering, G.E. Corporate social responsibility and marketing channel coordination. Res. Econ. 2012, 66, 142–148. [Google Scholar] [CrossRef]

- Ouchida, Y. Cooperative choice of corporate social responsibility in a bilateral monopoly model. Appl. Econ. Lett. 2019, 26, 799–806. [Google Scholar] [CrossRef]

- Fanti, L.; Buccella, D. Corporate social responsibility in unionised network industries. Int. Rev. Econ. 2021, 68, 235–262. [Google Scholar] [CrossRef]

- Elfenbein, D.W.; Fisman, R.; Mcmanus, B. Charity as a substitute for reputation: Evidence from an online marketplace. Rev. Econ. Stud. 2012, 79, 1441–1468. [Google Scholar] [CrossRef]

- Hoxby, C.M. All school finance equalizations are not created equal. Q. J. Econ. 2001, 116, 1189–1231. [Google Scholar] [CrossRef]

- Ntim, C.G.; Soobaroyen, T. Corporate governance and performance in socially responsible corporations in South Africa: New empirical insights from a multi-theoretical perspective. Corp. Gov. Int. Rev. 2013, 21, 468–484. [Google Scholar] [CrossRef]

- Gil Lafuente, A.M.; Barcellos Paula, L. Algorithms applied in the sustainable management of human resources. Fuzzy Econ. Rev. 2010, 15, 39–51. [Google Scholar] [CrossRef]

- Stubelj, I.; Dolenc, P.; Biloslavo, R.; Nahtigal, M.; Laporšek, S. Corporate purpose in a small post-transitional economy: The case of Slovenia. Econ. Res. Ekon. Istraz. 2017, 30, 818–835. [Google Scholar] [CrossRef]

- Málovics, G.; Csigéné, N.N.; Kraus, S. The role of corporate social responsibility in strong sustainability. J. Socio Econ. 2008, 37, 907–918. [Google Scholar] [CrossRef]

- Sawyer, M. Financialisation, industrial strategy and the challenges of climate change and environmental degradation. Int. Rev. Appl. Econ. 2021, 35, 338–354. [Google Scholar] [CrossRef]

- Khan, K.; Amin, I.U.; Ahmed, S. Management Decisions, Stock Prices and the Economy. Int. Res. J. Financ. Econ. 2011, 75, 7–13. Available online: https://www.scopus.com/inward/record.uri?eid=2-s2.0–80054745401&partnerID=40&md5=78256cd0abd2854dcc86f9a7a173e3ec. (accessed on 15 March 2022).

- Iancu, A.; Popescu, L.; Popescu, V. Factors influencing social entrepreneurship intentions in Romania. Econ. Res. -Ekon. Istraz. 2021, 34, 1190–1201. [Google Scholar] [CrossRef]

- Mah, S.K. Earth, wind, and fire: Pace plays a vital esg role. J. Struct. Financ. 2021, 26, 73–85. [Google Scholar] [CrossRef]

- Qoyum, A.; Al Hashfi, R.U.; Zusryn, A.S.; Kusuma, H.; Qizam, I. Does an Islamic-SRI portfolio really matter? Empirical application of valuation models in Indonesia. Borsa Istanb. Rev. 2021, 21, 105–124. [Google Scholar] [CrossRef]

- Landi, G.C.; Iandolo, F.; Renzi, A.; Rey, A. Embedding sustainability in risk management: The impact of environmental, social, and governance ratings on corporate financial risk. Corp. Soc. Responsib. Environ. Manag. 2022, 29, 1096–1107. [Google Scholar] [CrossRef]

- Radu, C.; Smaili, N. Alignment Versus Monitoring: An Examination of the Effect of the CSR Committee and CSR-Linked Executive Compensation on CSR Performance. J. Bus. Ethics 2021, 180, 145–163. [Google Scholar] [CrossRef]

- Yang, J.; Basile, K. Communicating Corporate Social Responsibility: External Stakeholder Involvement, Productivity and Firm Performance. J. Bus. Ethics 2022, 178, 501–517. [Google Scholar] [CrossRef]

- Liao, L.; Chen, G.; Zheng, D. Corporate social responsibility and financial fraud: Evidence from China. Account. Financ. 2019, 59, 3133–3169. [Google Scholar] [CrossRef]

- Hunjra, A.I.; Boubaker, S.; Arunachalam, M.; Mehmood, A. How does CSR mediate the relationship between culture, religiosity and firm performance? Financ. Res. Lett. 2021, 39, 101587. [Google Scholar] [CrossRef]

- Beloskar, V.D.; Rao, S.V.D.N. Corporate Social Responsibility: Is Too Much Bad?—Evidence from India. In Asia-Pacific Financial Markets; Springer: Tokyo, Japan, 2021; Issue 0123456789. [Google Scholar] [CrossRef]

- Chahine, S.; Daher, M.; Saade, S. Doing good in periods of high uncertainty: Economic policy uncertainty, corporate social responsibility, and analyst forecast error. J. Financ. Stab. 2021, 56, 100919. [Google Scholar] [CrossRef]

- Zhao, T. Board network, investment efficiency, and the mediating role of CSR: Evidence from China. Int. Rev. Econ. Financ. 2021, 76, 897–919. [Google Scholar] [CrossRef]

- Kong, D.; Cheng, X.; Jiang, X. Effects of political promotion on local firms’ social responsibility in China. Econ. Model. 2021, 95, 418–429. [Google Scholar] [CrossRef]

- Wong, W.C.; Batten, J.A.; Ahmad, A.H.; Mohamed-Arshad, S.B.; Nordin, S.; Adzis, A.A. Does ESG certification add firm value? Financ. Res. Lett. 2021, 39, 101593. [Google Scholar] [CrossRef]

- Briscese, G.; Feltovich, N.; Slonim, R.L. Who benefits from corporate social responsibility? Reciprocity in the presence of social incentives and self-selection. Games Econ. Behav. 2021, 126, 288–304. [Google Scholar] [CrossRef]

- Lan, T.; Chen, Y.; Li, H.; Guo, L.; Huang, J. From driver to enabler: The moderating effect of corporate social responsibility on firm performance. Econ. Res. Ekon. Istraz. 2021, 34, 2240–2262. [Google Scholar] [CrossRef]

- Takahashi, H.; Yamada, K. When the Japanese stock market meets COVID-19: Impact of ownership, China and US exposure, and ESG channels. Int. Rev. Financ. Anal. 2021, 74, 101670. [Google Scholar] [CrossRef]

- Jost, S.; Erben, S.; Ottenstein, P.; Zülch, H. Does CSR impact mergers & acquisition premia? New international evidence. Financ. Res. Lett. 2021, 46, 102237. [Google Scholar] [CrossRef]

- Azmi, W.; Hassan, M.K.; Houston, R.; Karim, M.S. ESG activities and banking performance: International evidence from emerging economies. J. Int. Financ. Mark. Inst. Money 2021, 70, 101277. [Google Scholar] [CrossRef]

- Zhang, J.; Zi, S. Socially responsible investment and firm value: The role of institutions. Financ. Res. Lett. 2021, 41, 101806. [Google Scholar] [CrossRef]

- Cerqueti, R.; Ciciretti, R.; Dalò, A.; Nicolosi, M. ESG investing: A chance to reduce systemic risk. J. Financ. Stab. 2021, 54, 100887. [Google Scholar] [CrossRef]

- Díaz, V.; Ibrushi, D.; Zhao, J. Reconsidering systematic factors during the COVID-19 pandemic–The rising importance of ESG. Financ. Res. Lett. 2021, 38, 101870. [Google Scholar] [CrossRef]

- Bofinger, Y.; Heyden, K.J.; Rock, B.; Bannier, C.E. The sustainability trap: Active fund managers between ESG investing and fund overpricing. Financ. Res. Lett. 2021, 45, 102160. [Google Scholar] [CrossRef]

- Ferriani, F.; Natoli, F. ESG risks in times of COVID-19. Appl. Econ. Lett. 2021, 28, 1537–1541. [Google Scholar] [CrossRef]

- Janik, B.; Bartkowiak, M. Are sustainable investments profitable for investors in Central and Eastern European Countries (CEECs)? Financ. Res. Lett. 2021, 44, 102102. [Google Scholar] [CrossRef]

- Mehta, P.; Singh, M.; Mittal, M.; Singla, H. Is knowledge alone enough for socially responsible investing? A moderation of religiosity and serial mediation analysis. Qual. Res. Financ. Mark. 2021, 14, 413–432. [Google Scholar] [CrossRef]

- Umar, Z.; Gubareva, M. The relationship between the COVID-19 media coverage and the Environmental, Social and Governance leaders equity volatility: A time-frequency wavelet analysis. Appl. Econ. 2021, 53, 3193–3206. [Google Scholar] [CrossRef]

- Xu, L.; Lee, S.H. Corporate Profit Tax and Strategic Corporate Social Responsibility under Foreign Acquisition. B.E. J. Theor. Econ. 2021, 22, 123–151. [Google Scholar] [CrossRef]

- Breton, M.; Crettez, B.; Hayek, N. Corporate social responsibility, profits, and welfare in a duopolistic market. Appl. Econ. 2021, 53, 6897–6909. [Google Scholar] [CrossRef]

- Garcia, A.; Leal, M.; Lee, S.H. Competitive CSR in a strategic managerial delegation game with a multiproduct corporation. Int. Rev. Econ. 2021, 68, 301–330. [Google Scholar] [CrossRef]

- Fernández-Ruiz, J. Corporate social responsibility in a supply chain and competition from a vertically integrated firm. Int. Rev. Econ. 2021, 68, 209–233. [Google Scholar] [CrossRef]

- Leal, M.; García, A.; Lee, S.-H. Strategic CSR and merger decisions in multiproduct mixed markets with state-holding corporation. Int. Rev. Econ. Financ. 2021, 72, 319–333. [Google Scholar] [CrossRef]

- Xu, H.; Xu, X.; Yu, J. The Impact of Mandatory CSR Disclosure on the Cost of Debt Financing: Evidence from China. Emerg. Mark. Financ. Trade 2021, 57, 2191–2205. [Google Scholar] [CrossRef]

- Remišová, A.; Lašáková, A.; Stankovičová, I.; Stachová, P. Unethical practices in the slovak business environment. Ekon. Cas. 2021, 69, 59–87. [Google Scholar] [CrossRef]

- Alsahlawi, A.M.; Chebbi, K.; Ammer, M.A. The impact of environmental sustainability disclosure on stock return of saudi listed firms: The moderating role of financial constraints. Int. J. Financ. Stud. 2021, 9, 4. [Google Scholar] [CrossRef]

- Jakubik, P.; Uguz, S. Impact of green bond policies on insurers: Evidence from the European equity market. J. Econ. Financ. 2021, 45, 381–393. [Google Scholar] [CrossRef]

- Zhang, C.; Liu, Q.; Ge, G.; Hao, Y.; Hao, H. The impact of government intervention on corporate environmental performance: Evidence from China’s national civilized city award. Financ. Res. Lett. 2021, 39. [Google Scholar] [CrossRef]

- Novak, M. Social innovation and Austrian economics: Exploring the gains from intellectual trade. Rev. Austrian Econ. 2021, 34, 129–147. [Google Scholar] [CrossRef]

- Rey-Martí, A.; Díaz-Foncea, M.; Alguacil-Marí, P. The determinants of social sustainability in work integration social enterprises: The effect of entrepreneurship. Econ. Res. Ekon. Istraz. 2021, 34, 929–947. [Google Scholar] [CrossRef]

- Wang, C. Monopoly with corporate social responsibility, product differentiation, and environmental R&D: Implications for economic, environmental, and social sustainability. J. Clean. Prod. 2021, 287, 125433. [Google Scholar] [CrossRef]

- Ammar Ali, G.; Nazim, H.; Khan, S.A.; Khan, Z.; Saeed, A. Governing Corporate Social Responsibility Decoupling: The Effect of the Governance Committee on Corporate Social Responsibility Decoupling. J. Bus. Ethics 2022, 1–26. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).