1. Introduction

This study investigates the association between creative accounting determinants and financial reporting quality and addresses the debate on the implications for sustainable business strategies. Stakeholders’ pressures and information demands have changed significantly in recent years, and companies are required to respond [

1]. Sustainability reporting is an important communication tool for demonstrating transparency and effective governance and is specifically addressed to stakeholders [

2]. The need to provide transparency to stakeholders is a driver of enhanced reporting quality [

3]. In addition, a few studies have focused on sustainability information disclosure to capture disclosure information standardization levels based on international indicators [

4].

Financial reporting features agreements with providing reliable, accurate, and timely financial data required by stakeholders for making decisions concerning banks’ operations [

5]. The objective of financial reporting is to present financial data to users in order to facilitate informed and objective decisions. Nevertheless, the present accounting policy provides some choice concerning accounting techniques and the use of objective judgement to define measurement policies, recognition criteria, and, in some cases, the characterization of the accounting body. The ability to choose several aspects of accounting allows for deliberate information manipulation or concealment. Such manipulations increase businesses’ apparent attractiveness that can project better profitability and financial stability instead of the actual position [

6]. Thus, the financial reports of banks can provide a direction of reliance to users towards objective decision making [

7]. Essentially, the reports used for financial decision making must be understandable, comparable, relevant, and realistic.

The body of knowledge concerning creative accounting does not explicitly specify if the auditor is obliged to unmask aspects of creative accounting that are permitted and legal. Hence, the intention is to assess the use of creative accounting in Iraq and its effects on the banking sector and its financial reporting quality. It should be noted that auditing standards require that auditors formulate processes that can ascertain if the accounting practice followed by a business entity can record financial information correctly. The auditors are only obliged to ensure that a business’s financial information presents an accurate and fair state of the company’s financial position [

8,

9]. There is no explicit obligation for assessing and discovering fraud. The significance of specific research on corporate social responsibility and its association with creative accounting and all its manifestations concerns the overall trend that inadequate governance provides or sustains an impetus to manipulative activities [

10]. Poor corporate social responsibility has a higher correlation with accounting manipulation [

11,

12,

13].

This study aimed to understand both empirical and theoretical viewpoints in this domain by formulating a structure that provides hands-on support for regulators and investors related to the banking industry. This study provides a fresh perspective concerning creative accounting and contributes significantly to the related literature because creative accounting in Iraq has not been studied extensively. The endeavor is to enrich the literature concerning creative accounting. There are three aspects: Firstly, we intended to assess the primary determinants of creative accounting such as ethical issues, internal control, disclosure quality, and ownership structure. Secondly, this study evaluated the effectiveness of strong corporate social responsibility concerning eradicating creative accounting by the banking sector in Iraq. Thirdly, we intended to use information concerning commercial banks in Iraq to determine the degree to which creative accounting is entrenched in Iraq’s banking system. Lastly, the present research assessed financial reporting quality as a practice in commercial banks in Iraq from the perspective of regulatory agencies, corporate social responsibility, and other aspects. However, there is limited evidence on how the impact of determinants of creative accounting on financial reporting quality is affected by corporate social responsibility in the banking sector of Iraq. This study aimed to examine the joint influence of determinants of creative accounting and corporate social responsibility on financial reporting quality in Iraq. It concentrated on two questions:

What are the effects of creative accounting determinants on financial reporting quality in the banking sector?

To what extent does corporate social responsibility moderate the relationship between creative accounting and financial reporting quality?

Finally, the findings of this study will be useful to policymakers, researchers, and managers. In particular, they provide current knowledge of the effect of corporate social responsibility, creative accounting, and financial reporting quality, contributing to the literature on performance and the firm-based view. Thus, the present research was designed to attain the following objectives that contribute to limiting the practice of creative accounting and increasing the quality of financial reports in the banking sector:

To identify the effects of creative accounting determinants on financial reporting quality in the banking sector;

To examine the moderating effects of corporate social responsibility on the relationship between creative accounting determinants and financial reporting quality.

4. Discussion

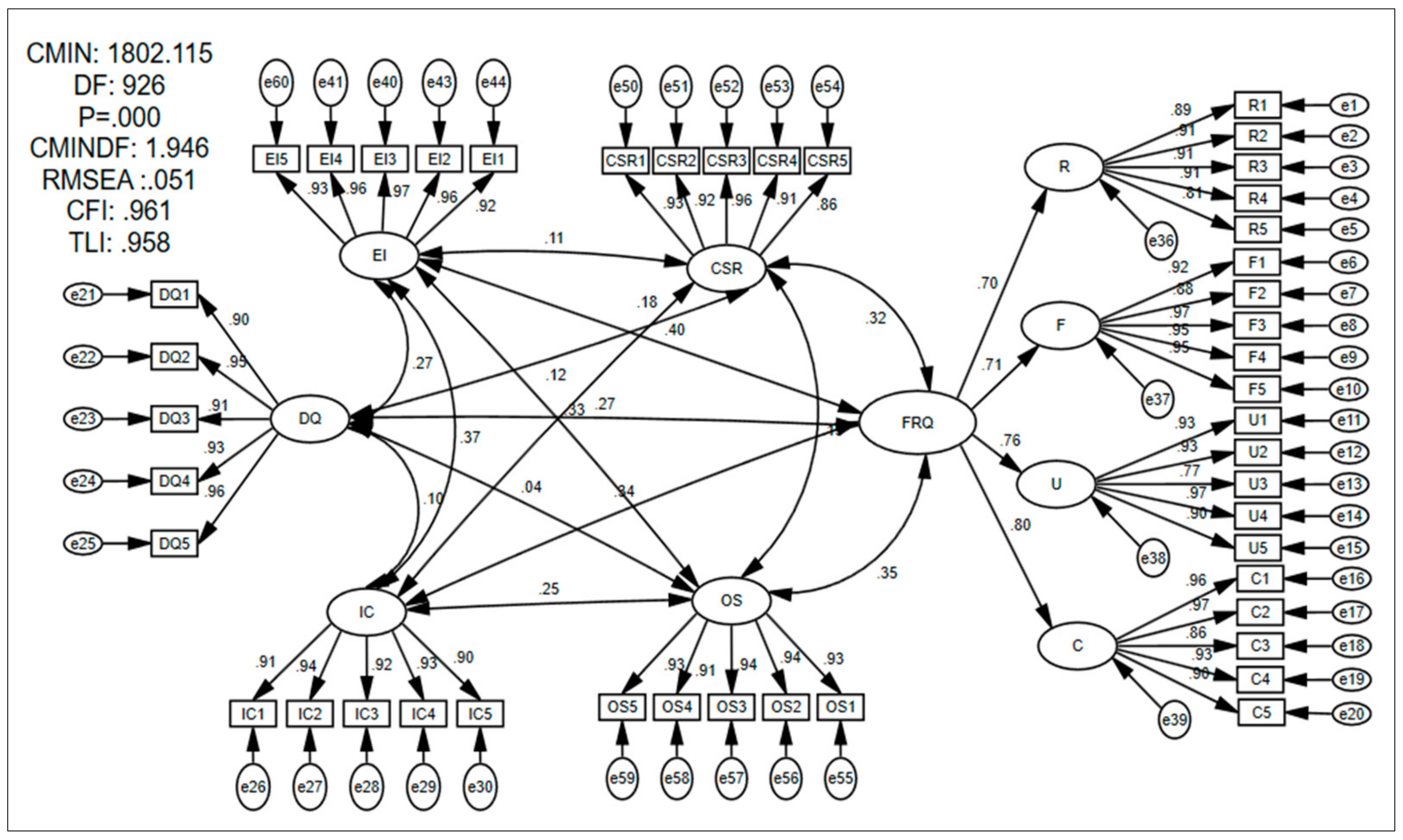

This part of the study discusses the findings related to the first research question on the direct relationship between the determinants of creative accounting and financial reporting quality. In this respect, the present research findings explain the positive implications of the determinants on identifying creative accounting practices as proposed in the hypotheses within the context of Iraqi commercial banks. Accordingly, the result for hypothesis H1a was (t = 3.328), which aligns with the assumptions provided by agency theory, where the hypothesis indicated significant impacts of maintaining ethical issues on the quality of financial reporting. Furthermore, the results reaffirm that ethical aspects lead to the establishment of a higher quality of financial reporting practices, as shown in the context of Iraqi commercial banks. Moreover, the results acknowledge the findings in previous studies presented by [

10,

47,

55,

62], which demonstrate limited consideration of ethical issues on creative accounting practices in the context of commercial banks.

In addition, the result of H1b (t = 3.427) indicates a significant relationship between the constructs with limited operation of disclosure procedures in the context of commercial banks. This determination designated the higher implications of creative accounting practices to the quality of financial reporting in the banking sector, which was found to be consistent with the previous literature [

9,

44,

63]. The implementation of new institutional theory contributed to explaining the underlying preposition that limited disclosure practice in the commercial bank context was due to the pressure exerted by the institutional setup related to ownership structure. These results are in good agreement with numerous studies in the literature which display the significance of the linkage between these determinants and accounting practice [

19,

36,

64]. However, the present research findings are contradicted by other studies that proposed a limited controlling role of disclosure quality in creative accounting practice [

28,

65,

66]. In brief, disclosure quality has been found to be one of the essential determinants of institutional transparency that increase the trust of the public in the financial reporting quality of banks. This finding is supported with high consistency in previous claims cited in [

67] on maintaining ethical concerns through disclosure quality.

The results of the last two hypotheses related to the first research question are H1c (t = 3.640) and H1d (t = 3.912). As mentioned earlier, the present research findings show a significant inter-correlated relationship between the determinants of creative accounting, i.e., each of the determinants has an effect on the others. The origin of this relationship is clearly identified in the previous literature, and it is verified in the present research findings. Thus, limited consideration of ethical issues and disclosure quality results in limited implementation of internal control. These procedures enable the practice of creative accounting to take place in the commercial banking sector at various levels according to the ownership structure of the bank. Thus, the present findings are consistent with previous studies that indicated poor internal control may lead to higher errors and inaccurate financial disclosure of the financial reporting quality of banks [

46,

68,

69].

Therefore, the ownership structure theory sufficiently explains the findings concerning the last two hypotheses through identifying the manipulation practices adopted in the banks to avoid a poor performance of the share value and loss of control in the business. Therefore, the relationship between ownership structure and financial reporting quality can be reflected as fewer agency problems and information asymmetry in family organizations, in contrast to non-familial organizations [

49,

70]. These descriptions verify previous results in the literature which proposed high impacts of ownership structure on providing a faithful representation in the reports presented by commercial banks [

71,

72]. Yet, again, the present findings are found to be consistent with those in [

34,

73], which asserted that complying with a high level of internal control can reduce the risk of mitigation policies to increase reporting quality through the determinants of creative accounting.

It is worth declaring that the outcomes of this research support the current literature concerning the correlation between the determinants of creative accounting to detect fraudulent practices, but these determinants fail to control these practices at safe levels [

22,

74,

75]. These findings apply to the context of Iraqi commercial banks, although dedicated efforts are constantly made to retain and establish healthy relations with outside shareholders as one of the major resources; however, additional enhancement is required to reduce fraudulent practices within creative accounting to present a high quality of financial reports. This, in turn, implies that the internal banking system would sustain ethical issues, disclose honest information to the public, and implement qualified internal control for faithful representations of the financial reporting practice in Iraqi commercial banks.

The present study findings reveal a statistically significant impact of employees’ opinion on CSR on the relation between employees’ opinion on creative accounting determinants and employees’ opinion on financial reporting quality. Thus, the results provide a feasible answer for the second research question and help to examine the proposed hypotheses. The significance of corporate social responsibility for the commercial banks’ financial reporting quality indeed validated most of the proposed hypotheses, wherein H2a (t = 5.892), H2c (t = 4.936), and H2d (t = 5.626). These values are found to agree with those of previous studies of [

21,

76], who considered banks as entities that operate in society and are obliged to ensure fair and consistent benefits to all stakeholders and safeguarding to uphold social justice responsibility. Moreover, the findings are consistent with a previous study presented by [

77], who reported that corporate social responsibility plays a prominent role in attaining sustainable financial practice, especially for the commercial banking sector.

Moreover, the obtained results and analysis suggest that decision makers are affected by motives and business values; relatively, the choice of actions in the business influences corporate social responsibility activities. The moderating mechanism of CSR is presented sufficiently within the perspective of neo-institutional theory, which displays a significant interaction between CSR and the maintenance of ethical issues. However, some researchers such as [

9,

12] indicated that corporate social responsibility contributes to concealing questionable activities and creative accounting, but the adoption of highly independent internal control contributes to overcoming this complication. These indications contribute to clearing up the inconsistency of previous studies [

9,

19] on the mechanism of CSR in controlling creative accounting practices. In addition, the findings show a positive relationship between the variables of the study and CSR that impacts the power of non-executive members in the banks to design and develop business strategic plans for sustainable competitive development. These findings are found to be in good agreement with previous findings addressed in the studies of [

58,

78].

In addition, the findings show that the independence of audit committees is linked to a higher level of financial reporting, which is consistent with both the techniques used in CSR, and the integrated correlation between the determinants of creative accounting. Thus, the present research findings support previous findings in [

21] that the effect of CSR on auditing financial practices in various ownership structures is a standardized representation of financial reports of the financial status of banks. On this basis, the fourth hypothesis (H2d) was supported. Moreover, the results on the positive relationship between disclosure quality and internal control can also be related to the norms of interaction between the agency and neo-institutional theories, which state that autonomous independent audits, who have the freedom to make decisions and carry out error detection, can easily facilitate effective work and provide an unbiased judgment.

Contrary to the expectations, this study did not find a significant relationship in hypothesis H2b (t = 1.536), which indicated the absence of any statistical significance between corporate social responsibility and the determinant of disclosure quality. These findings further support the idea of [

9,

79] that CSR does not significantly impact the level of disclosure in the business to maintain a faithful presentation and understandability of the financial reporting. Thus, the current findings confirm the conventional foundations of CSR that can contribute to identifying customer needs, tracking new market trends, analyzing competitors’ actions, observing technological developments, and involving customers or suppliers in the product development process, thus playing a decisive role in preparing accurate financial reports. In brief, the results of H2b validate the suggestions made by [

9,

43,

66] concerning the limited impacts of CSR on disclosure quality, which found a dominant controlling role of business managers in preparing financial reports for stakeholders and the public.

In addition, this combination of findings for H2b provides some support for [

9] and the conceptual premise of neo-institutional theory that banks disclose information due to the pressure exerted by the institutional setup. Moreover, agency theory suggests that banks emphasize comprehensive aspects of accountability concerning numerous stakeholders. Thus, CSR does not add significant value to the willingness of banks to disclose any financial information. These findings corroborate the findings of [

80], who suggested that the scope of CSR is restricted to achieving significant disclosure of the business, especially in financial reporting. Therefore, the directors of commercial banks must determine the suitability of their actions for the public, bringing stability, harmony, and strength to society.

5. Conclusions

The present study was set up to reconceptualize and reform the current situation in the financial sector, especially in banks of developing nations. The present study focused on commercial banks, which are considered as the backbone of the national economy of any nation. Thus, it was vital to investigate this sector for identifying its strengths and weaknesses, which the present study highlighted regarding creative accounting and financial reporting practices. Previous studies showed the capability to hide some fraudulent practices within creative accounting, which directly impacts the quality of financial reporting [

12,

55,

81]. However, the literature review showed that the determinants of creative accounting could contribute to identifying any fraudulent practices which resulted in a high quality of financial reporting [

82,

83,

84]. However, it has been reported in previous studies that the financial banking sector performs many creative accounting practices which result in a low quality of financial reporting [

46,

56,

85].

Therefore, a theoretical investigation was conducted through a systematic literature review of previous relevant studies. The intensive review of the literature contributed to identifying the essential determinants of creative accounting, elements of financial reporting, and active aspects of corporate governance in the research context, which impact reporting practice in the commercial banking sector. Moreover, the review contributed to designing the present research questions and hypotheses on the relevant phenomena of interest, while the practical application of the present study framework resolved various shortcomings identified in previous studies through the moderating role of some corporate governance aspects. As a result, the framework contributed to attaining the present research objectives. Subsequently, this study makes several contributions to assessing and enhancing reporting practice in the financial sector, which is especially authenticated to be a valid model in the commercial banking sector.

As discussed in the previous sections, the relationship between the determinants of creative accounting and financial reporting encountered some noticeable limitations. Thus, it is necessary to measure the implications of these determinants on financial reporting practice using a survey questionnaire which reviews the intentions and conceptualization of the main persons contributing to preparing financial policies in commercial banks. Relatively, the increasing attention towards creative accounting and higher academic demands on financial reporting in practice motivated this research aimed at addressing the main determinants in relation to the criteria of financial reporting. Taken together, the present research findings show that the degree of impact of creative accounting determinants is linked to the aspect of corporate governance. This, in turn, was found to directly impact the quality of financial reporting practice in commercial banks, whereas the balanced use of these aspects can maintain diagnostic and interactive knowledge.

Most of the earlier reports concluded that creative accounting determination generally depends on the framework, idiosyncrasy, and interconnectivity [

20,

46,

86]. It was indicated that a perfect solution is impossible for all the financial sectors wherein creative accounting might be inappropriate and dependent on the contexts. Therefore, the level of creative practice may vary appreciably from one sector to another [

87]. This fact inspired the present study to adopt a triangulated application of agency, neo-institutional, and ownership theories to explain the correlation between the variables of the study and the moderator, as shown in the designed conceptual framework. The results contribute to presenting concurrent evidence on the flexibility of creative accounting determinants with a higher degree of implication on corporate aspects and financial reporting quality. Additionally, the obtained findings strongly emphasize the significant impacts of the moderator in enhancing the determination of creative practice, as well as the strength of the quality of financial reporting within Iraqi commercial banks.

Furthermore, the results acquired from the present investigation extend our knowledge through offering valid answers for the research questions. These findings show the importance of corporate aspects of corporate social responsibility that moderate the relationships among the determinants and financial reporting quality in commercial banks of Iraq. Thus, entrepreneurial administration connected to the identification of new scopes and recognition of problems as well as trends in commercial banks is needed. This process enables the management to contribute to the adjustment and upgrading of daily schedules; largely, this is a tactical act for transforming the reporting practice of banks into a higher level of qualified reporting practice [

12,

88]. This identification is shown in the findings of this study, which support the required reform through the moderation of corporate aspects of financial reporting quality. In conclusion, the results of this study show harmony with the views demonstrated in most of the previous studies in the literature on the determination of creative practice that influences the preparation of financial reports through the moderation of corporate social responsibility of the banking sector in Iraq, such as [

89,

90].

The limitation of this research is that the focus on a single research context (Iraqi commercial banks) may mean the results are not generalizable to every financial sector, each with different issues. Thus, potential context limitations are acknowledged, particularly the distinctions amongst developing and developed countries affecting the views of creative accounting allocations and financial reporting for identifying the quality of business performance. It is important to note that various banking sectors in different contexts, imposing more limitations, are worth studying in the future. Additionally, nationalized differences in the culture can appreciably influence the perception of the research regarding some important issues of creative accounting practice and its impacts on the quality of financial reporting, thus offering more conclusive evidence.

Thus, the present research limitations open up new directions for further studies. Moreover, this study used a single source of data via a survey questionnaire from the Iraqi research context. Future studies could contribute to collecting data from multiple sources such as financial reports, surveys, and interviews that may facilitate making several modifications and estimates of the implications of business governance on creative accounting practices and the quality of financial reports. In addition, it is recommended that future longitudinal studies include the opinions of multiple sources of information from management, and other auditing levels, in order to confirm their impacts on developing the determination of creative accounting practices and the quality of financial reports. Briefly, this study focused on four determinants of creative accounting (ethical issues, disclosure quality, internal control, and ownership structure) and one aspect of corporate governance (corporate social responsibility). Future studies should determine the mechanism of other determinants and corporate aspects in enhancing the quality of financial reporting. All of these future developments may offer pioneering findings which could contribute to validating the present research findings and those of previous studies in the literature.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}