4.1. The Position of Developing Countries in World Agricultural Trade

The value of world food exports during the 26-year period under review, i.e., 1995–2020, more than tripled (averaging about 13.2% per year), while the increase in the value of food exports from developing countries reached almost five times its initial value, growing by less than 18%. Thus, the share of food exports from developing countries in world trade increased (

Figure 2) [

76].

The share of developing countries in world food exports has been on a steady upward trend. In the second half of the 1990s it oscillated around 32%, while after 2010 it reached almost 40%. The average annual share of food exports from developing countries was 36.2% between 1995 and 2020, of which until 2008 the share was below the average level, and since 2009 the value of the share of food exports from developing countries has exceeded the average values. In 2017, developing countries accounted for the largest share of global food exports at 41.2%.

The increase in the share of developing countries in world food exports between 1995 and 2020 was 9%. The largest part of exported food (average share in the period under review was 19.2% per year) came from the Asian continent together with Oceania, and this group also saw the largest increase in the share of food exports supplied to foreign markets. Latin and South American food exporters also held a significant share at an average annual rate of 13.7%, increasing their share of global food exports by over 3%. On the other hand, the share of food export from African countries remained stable (

Table 1).

In world agricultural commodity exports, the share of developing countries was in the range of 28–41% between 1995 and 2020, reaching an annual average value of 34%. From 2001 to 2011, the share of agricultural commodity exports from developing countries described an upward trend, which then collapsed. In 2013, the share declined by 2.5% over the 1-year period and by a further 1.3% over the following year. A return to an upward trend has occurred since 2017, but has not reached the 2011–2012 peaks (

Figure 3).

In the case of trade in agricultural commodities, the Asian continent with Oceania had the largest share in world exports, averaging 23.6% per year between 1990 and 2020. The highest increase (reaching almost 4%) in the share of exported agricultural raw materials belonged to exporters from Latin and South America, while African exporters kept their share in the export of agricultural raw materials constant, averaging about 4.3% per year (

Table 2).

4.2. The Importance of Foreign Value Added in the Gross Exports of Agricultural Commodities of Developing Countries

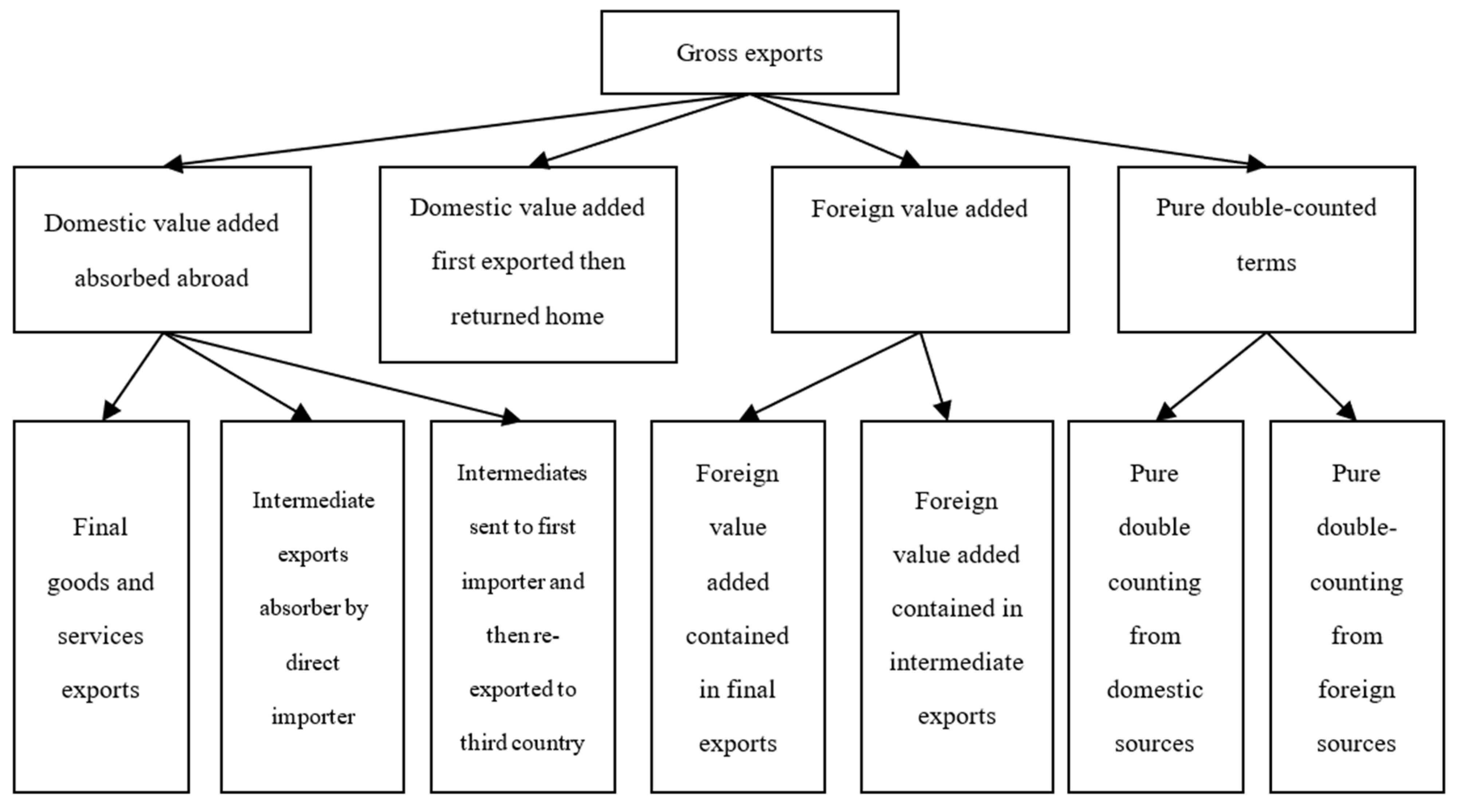

The standard method of assessing the degree of a country’s participation in global value-added chains is to estimate the share of foreign value added in gross exports. Using the data contained in the OECD–WTO database, we can determine the share of foreign value added in gross exports of agriculture, hunting, forestry, fishing, food products, beverages and tobacco of 28 developing countries in 1995–2018 (

Table 3).

Based on the data contained in the

Table 3, we can draw some conclusions. First, the share of foreign value added in agriculture, hunting, forestry and fishing exports varied widely between countries. The highest share of FVA in 2018 was that of Vietnam (35.61%), Hungary (27.63%), Bulgaria (27.31%), Poland (25.23%), and Croatia (21.42%). In other countries, the share of foreign value added in gross exports did not exceed 20%. Particularly weak links within global value chains, in which the share of FVA did not exceed 10% of gross exports, occurred in several Asian economies (Cambodia, China, India, Indonesia, Lao, Myanmar, Philippines) and South and Central America (Argentina, Colombia and Peru).

Secondly, when analyzing the changes in the strength of production links in agriculture, hunting, forestry and fishing after 1995, several trends can be identified. First of all, there are clear differences between the continents. In the case of Europe and Latin America, we can observe an increase in the share of foreign expenditure in exports, especially rapid in Europe in the years 1995–2010. After 2010, the growth dynamics weakened, which may be related to the phenomenon of defragmentation of production chains after the economic and financial crisis of 2008–2009. More complex changes took place in the countries of Asia and Oceania. Only in the case of Turkey and Vietnam has there been a steady increase in the strength of production links.

In Turkey, the share of foreign value added in gross exports increased by 14%, and in Vietnam by 19%, which was one of the best results in the studied group of developing countries. In other Asian countries, the trends in the share of FVA were variable. In Cambodia and India, the share of FVA grew until 2010, in China, Indonesia and Thailand until 2005, in Kazakhstan, Malaysia and Myanmar until 2000. In the following years, there was an extension to 2015 (Indonesia, Myanmar) or even 2018 (China, India, Kazakhstan, Malaysia), the weakening of production ties. The Philippines was characterized by the greatest volatility of the trends, but downward trends prevailed there. In Africa, the share of foreign value added in gross exports of agriculture, hunting, forestry and fishing increased in the years 1995–2010 (in the case of South Africa until 2015), and in the following years the production links weakened.

The second product groups analyzed were beverages and tobacco (

Table 4). Since the degree of processing of these goods is higher than that of unprocessed food and agricultural raw materials, the share of foreign value added in gross exports is also higher. The strongest manufacturing linkages characterize Vietnam (FVA’s share of gross exports was 40.71% in 2018), Hungary (38.18%), Bulgaria (35.70%), Malaysia (31.93%), and Tunisia (30.41%). In contrast, the lowest share of FVA was characteristic for some economies in Asia (China, India, Indonesia, Myanmar) and South America (Argentina, Brazil). As in the previously analyzed group of unprocessed agricultural products, and in the case of processed foods, there were large differences in the strength of production linkages within global value chains between continents during 1995–2018. In Europe, the share of foreign intermediate goods in gross exports was the highest, in addition to showing an upward trend, except for Croatia and Russia, where the share of FVA remained relatively stable. In South and Central America, linkages within global value-added chains developed until the first half of the 2000s. They weakened between 2005 and 2010 and especially 2009 and 2010, and since 2015 the share of FVA has stabilized. In Asian countries, production linkages in food products, beverages and tobacco expanded in Turkey and Vietnam throughout the period under review (1995–2018), and remained stable and strong in the Philippines. In the other economies, FVA’s share of gross exports grew until the crisis period of 2008–2009 and then fell by a few percent and, in the case of Cambodia, 12 percent. In Africa, stable production links were characteristic of Morocco (the share of FVA in gross exports oscillated around 20% in the period under review). South Africa and Tunisia have generally followed an upward trend in the share of FVA in gross exports.

4.3. The Comparative Advantage in International Trade of Agricultural Commodities

The standard method of assessing comparative advantage in international trade is based on the classical indexes of revealed comparative advantage (RCA). Based on data in terms of gross and domestic value added, we can determine the impact of integration within global value-added chains on competitive advantage in trade. In

Table 5, the results of the RCA indices in agriculture, hunting, forestry and fishing are included. In the traditional approach to gross exports (GE), Colombia (14.04), Myanmar (12.35), Costa Rica (9.75), Argentina (6.85), and Lao (6.19) had the highest comparative advantage in 1995. In the remaining analyzed economies RCA indices did not exceed 5, and Poland and the Russian Federation showed a gap. By 2018, there were significant changes in the evolution of revealed comparative advantage. RCA rates increased in 5 Asian countries (Cambodia, Indonesia, Kazakhstan, Lao and Vietnam), 3 in Europe (Bulgaria, Romania and Russia), 2 in South and Central America (Brazil and Mexico) and in Tunisia. In the remaining countries analyzed, the comparative advantage declined or a gap emerged (China, India, Malaysia, Thailand). In 2018, Myanmar (10.67), Brazil (9.14), Lao (7.58), Costa Rica (6.33) and Argentina (5.76) showed the highest comparative advantage.

Evaluation of the assessment of comparative advantage on RCA indices calculated on the basis of the gross value of exports may distort the actual specialization of individual economies. Only clearing gross exports of foreign value added and calculating the RCA indices taking into account only the domestic value added, allows the obtainment of objective results showing the real comparative advantage of the assessed countries. In 1995, countries such as Colombia (14.70), Myanmar (14.48), Costa Rica (10.92), Argentina (6.92) and Lao (6.66) had the highest comparative advantage calculated on the basis of domestic value added to gross exports. In other countries, RCA indices did not exceed 5, and only in the cases of Poland and the Russian Federation were they lower than 1, which means a comparative gap in this sector. As with the RCA indices calculated on the basis of gross export (GE), after the additional application of the alternative calculation method, until 2018, there were some changes in the evolution of the comparative advantage of the assessed countries. RCA indices increased in 2 countries of South and Central America (Brazil and Mexico), 4 Asian countries (Cambodia, Indonesia, Lao and Vietnam), 2 European countries (Bulgaria, Romania and Russia) and 2 African countries (Morocco and Tunisia). In 2018, Myanmar (11.86), Brazil (9.12), Lao (8.31), Costa Rica (6.09) and Argentina (5.88) had the highest comparative advantage calculated on the basis of domestic value added to gross exports.

The comparison of RCA indices calculated on the basis of the gross value of exports and domestic value added allowed the identification of those countries for which integration within global production networks had a significant impact on their comparative advantage. In 1995, the positive impact of foreign value added on the formation of a comparative advantage could be demonstrated only in three countries (Chile, Russia and Kazakhstan). In 2018, FVA positively influenced the comparative advantage of 7 economies (Chile, Costa Rica, Brazil, Croatia, Kazakhstan, Russia and South Africa). Nevertheless, only in two cases (Brazil and Russia) did the foreign value added increase the RCA indices, and thus the improvement of their comparative advantage relative to 1995. In other economies, the FVA only slowed down the process of losing comparative advantage.

The second product group analyzed is food products, beverages and tobacco. When assessing the formation of the revealed comparative advantage in the analyzed group of economies, we can indicate several regularities. For the RCA indices calculated on the gross value of exports in 1995, 18 out of 28 analyzed countries had a comparative advantage, and by 2018 the number had increased to 23. The value of RCA indices was in most countries lower than in the previously analyzed group of unprocessed agricultural products. In 1995, South and Central American countries had the highest comparative advantage: Costa Rica (6.36), Argentina (4.57), Brazil (4.44) and Peru (3.82). Whereas in 2018 we can again consider South and Central American countries as the most competitive in the export of the studied group of products: Argentina (6.20), Costa Rica (3.82), Chile (3.29) and Brazil (3.25), joined by Asian countries: Indonesia (3.92) and Myanmar (3.88). In the years 1995–2018, RCA indices increased in 19 out of 28 analyzed economies (

Table 6), and in 5 countries the increases were significant enough to allow for a comparative advantage (RCA > 1). Despite the reduction of the comparative gap in 4 economies (Mexico, Kazakhstan, Romania and Russia), it was not possible to achieve an advantage.

After the use of an alternative calculation method based on domestic value added, the group of countries with the highest comparative advantage in 1995 included Costa Rica (6.55), Argentina (4.62), Brazil (4.51), Peru (3.64) and Myanmar (3.66). In 2018, apart from the countries of South and Central America: Argentina (6.35), Costa Rica (3.62), Brazil (3.28) and Chile (3.21), Asian countries had the largest comparative advantage: Myanmar (4.35), Indonesia (4.10), Vietnam (3.25) and Thailand (3.14). The improvement in comparative advantage between 1995 and 2018 occurred in 19 out of 28 economies, with Indonesia and Colombia having the greatest increase in the RCA index. The improvement in the RCA indices in Colombia, Cambodia, Lao and South Africa was so significant that they moved from a group of countries which in the mid-1990s had a comparative gap, to a group of countries with an advantage. Despite the increase in the RCA indexes, Mexico, Kazakhstan, Romania and Russia still have a comparative gap in the export of food products, beverages and tobacco.

Assessing the role of foreign value added in the creation of comparative advantage, we indicate 6 countries for which the impact was positive. In Chile and Colombia competitiveness has improved, in Russia and Kazakhstan the comparative gap has narrowed. In Croatia, FVA has slowed the loss of competitiveness. In Peru, on the other hand, the large decline in the FVA share between 1995 and 2018 resulted in a significant deterioration in export competitiveness.

Usually, the importance of FVA in creating a country’s comparative advantage in global exports increases as the degree of product processing, level of technological advancement and capital intensity increases. This partly explains the relatively low impact of foreign value added on agricultural trade competitiveness. This is due to the low possibility of fragmentation of the production process of agricultural raw materials and processed food, much less than, for example, in the automotive or electronics industries. The following factors also played an important role in the limited impact of integration within global chains on the competitiveness of the analyzed group of countries in world agricultural exports:

- (1)

ongoing structural transformations consisting of a decrease in the share of the agricultural sector in generating GDP and employment for the benefit of the processing industry and/or services.

- (2)

high concentration of sales of agricultural products on the domestic market.

4.4. Discussion

The main conclusions of the study are confirmed by the published results of other authors. Regarding the increasing trend in exports of food and agricultural raw materials by developing countries, similar findings were obtained by Bojnec, Ferto and Fogaras (2014), whose study focused on Brazil and India [

77]. In contrast, Schwartz et al. (2015) noted that not only has trade in agri-food commodities expanded rapidly, but its structure has additionally changed significantly, with important implications, especially for developing economies [

78]. Szczepaniak (2018) pointed out the positive impact of integration processes on the development of foreign trade in food products [

79]. Moreover, Athukorala (2018) noted that operational linkages between cooperators generally intensified foreign trade processes [

80].

Another important finding of the study is that the share of foreign value added in the exports of agriculture, hunting, forestry and fishing varied strongly between countries. Bojnec and Ferto (2012) showed a positive effect of an increased number of varieties of agri-food products on export growth, but less on the diversification of higher value-added food products [

81]. It is even a frequent phenomenon that the share of products with higher added value decreases, despite the increase in exports, which is due to the increase in the share of basic agricultural raw materials with low added value [

82]. This research is supported by the results of Shafi, Muchie and Sedebo (2021) who showed that the growth in the value of real exports and imports of the agro-processing sub-sector of manufacturing industry tends to decline in each specified period [

83].

The linking of global value chains to the measurement of competitiveness was carried out in the research of Mashabela and Vink (2008). The authors proved that participation in global value chains increases the competitiveness of the participant in the international arena [

84]. Oro and Pritchard (2011) on the other hand, showed that the necessary restructuring in food resulted additionally from the desire to obtain a foreign competitive advantage [

85]. Intensifying global competition means that even in the local market and in retail, an increase in demanding customers creates the requirement of more attention focused to seeking and maintaining a sustainable competitive advantage [

86]. Further development of the discussed research can be found in the results of Gachukia and Muturi (2017). Competitive strategies play a role in the configuration of global value chains [

87]. However, as Ćejvanović and Potrebić (2018) note, agriculture and agri-food chains have a number of weaknesses that reduce their competitiveness in the international market [

88]. The main weaknesses are that the uncertainty and complexity of the environment is exacerbated in food supply chains, which is when approaches move from production with undifferentiated food commodities to products with differentiated value added [

89]. Not all countries participating in foreign trade have been able to integrate into global value chains with equal success. This is largely true of trade in food and other agribusiness industry commodities. As shown by Şerbănel’s (2014) research, African and Latin American countries are still seeking better access to global value chains by increasing the competitiveness of their industries and products [

90]. LDC countries face similar problems. Therefore, international organizations recommend the necessity to draw the attention of authorities to the improvement of public order and taxation systems in these countries in order to increase the competitiveness of these markets. This will then increase the willingness to use agricultural raw materials from these countries and, as a result, improve their share in global value chains [

91]. The exact indicators of the discussed values were observed by Fujita (2013), showing that in developed countries, the average imported value added in exports amounts to 31%, assuming much lower values in developing countries. However, this indicator does not exceed 14% for LDC countries [

92]. These conclusions are also confirmed by other authors, pointing to the need to support and promote domestic food producers by improving their competitiveness on the international market, which is also expressed in the increase in export value added [

59,

93,

94,

95,

96,

97,

98,

99,

100,

101,

102,

103]. Moreover, in this context, it is important that at the level of individual enterprises, who export their products on international agricultural markets, intensification of activities improves their long-term competitiveness. Felzensztein and Gimmon (2014) proved that management should improve value added through differentiation, diversification of offerings and implementation of innovative marketing strategies [

104]. It should also be remembered that the production and generation sectors were in the past considered to generate the highest added value. In a modern economy, research should also include R&D, the infrastructure of enterprises and their logistics, as well as marketing activities as a source of added value. Jun and Rowley (2019) argue that even a change in organizational structure affects the added value that interacts with the international competitiveness of the entity [

105].

{kind=link}

{kind=link}

{kind=link}