Insurance as an Alternative for Sustainable Economic Recovery after Natural Disasters: A Systematic Literature Review

1

Doctoral Program of Mathematics, Faculty of Mathematics and Natural Sciences, Universitas Padjadjaran, Sumedang 45363, Indonesia

2

Department of Mathematics, Faculty of Mathematics and Natural Sciences, Universitas Padjadjaran, Sumedang 45363, Indonesia

3

Faculty of Informatics and Computing, Universiti Sultan Zainal Abidin, Kuala Terengganu 21300, Malaysia

*

Author to whom correspondence should be addressed.

Sustainability 2022, 14(7), 4349; https://doi.org/10.3390/su14074349

Submission received: 5 February 2022

/

Revised: 14 March 2022

/

Accepted: 24 March 2022

/

Published: 6 April 2022

Abstract

:The risk of natural disasters has increased over the last few decades, leading to significant economic losses across the globe. In response, research related to the risk of economic loss due to natural disasters has continued to develop. At present, insurance remains the best solution for funding such losses. The purpose of this study is to analyse the development of insurance as an alternative for sustainable economic recovery after natural disasters. The data used are articles obtained from several sources indexed by Scopus and Google Scholar. The search resulted in a final database of 266 articles, culled from a total of 813 articles before the final selection was made. The articles used are publications from 2000–2021 (including 21 database periods), to which we applied a systematic literature review method. Identification and evaluation of the articles was carried out through visualization of their content, development of disaster risk insurance, and availability of disaster risk insurance by country and type. The identification results show that the relationship between the word “insurance”, according to visualization using the VOSviewer software, has a relationship with other clusters including the words “disaster”, “disaster insurance”, “risk”, “natural disaster”, “study”, “recovery”, and “disaster risk financing”. The 266 articles studied show that there was an annual increase in the number of published scientific papers over the period 2000–2021. The types of disaster risk insurance, based on a review of the articles, include agricultural insurance, flood insurance, property insurance, earthquake insurance, crop insurance, and natural disaster insurance. In addition, of the six types of disaster risk insurance, three have been discussed the most in the last five years, namely, agricultural, flood, and property insurance. The increase in the number of scientific publications discussing these three types of disaster risk insurance has been influenced by climate change. Climate change causes a significant increase in the potential for disasters and is accompanied by an increased risk of loss. This review is expected to provide information and motivation for researchers related to the development and importance of disaster risk insurance research. Research in the risk sector for disaster losses due to climate change should be continued in the future in order to help fund economic recovery, especially throughout the insurance sector. With continuous research on disaster risk insurance, it is hoped that the resulting information can be more effective in determining insurance risk and in helping local economies and communities recover after the advent of a disaster. With the availability of funds for post-disaster recovery, the regional economy affected by the disaster can be immediately restored and recovered from adversity.

1. Introduction

A disaster is a dangerous event; it is not known exactly when it will occur, and it may be caused by nature or by humans [1]. Disasters can pose a risk of economic loss in the form of the loss of livelihoods and/or damage to infrastructure. In addition to economic losses, natural disasters cause social impacts in the form of injuries, deaths, and psychological effects. The type of natural disaster differs by region in the world. In continental Europe, flooding occurs nearly every year [2,3]. Flood disasters have caused economic losses in many countries on the European continent due to the damage caused and the costs associated with disaster management [4,5,6]. In America, common disasters are floods [7,8,9], earthquakes [10,11,12,13], tornadoes [14,15,16], and landslides [17,18]. The United States is a country that often experiences tornadoes, one of the most dangerous and frightening types of disaster, which can cause casualties, damage to settlements, and economic losses. Meanwhile, on the Asian continent, the disasters that often occur are flash floods [19,20], landslides [21,22], earthquakes, and tsunamis [23,24]. Flash floods, earthquakes, and landslides are the types of disasters that lead to the highest material and economic losses.

The number of disasters that has occurred significantly increased up to 2021. In particular, flooding is a type of disaster that has experienced a rapid increase in prevalence worldwide [25]. This increase in flood disasters has been influenced by the occurrence of global warming, causing climate change. Climate change has an impact on rainfall intensity, which greatly increases the potential for flooding in various countries [26]. Based on data obtained from the International Disaster Database, from 2000 to 2019, most disasters were caused by extreme climate change. In terms of the spread of natural disasters, most (42%) occurred in Asia; of those in other continents, 24% occurred in the Americas, 18% in Europe, and the lowest (16%) number occurred on the African continent [27]. These results demonstrate that climate change has increased the frequency and distribution of disasters due to an increase in the number of extreme weather events. In particular, increased numbers of flash floods and landslides have been observed [28,29].

The risk of loss cannot be avoided when a natural disaster occurs, and there exists a close relationship between the two. When the potential for natural disasters increases, it is naturally followed by an increase in the number of losses, which may be in the form of damage to infrastructure or socio-economic losses. The relationships between natural disasters and the risk of economic loss have been researched. Among other things, such research has investigated the relationship between the risk posed by natural disasters and the resulting losses [30], the level of damage caused [31], and sustainable community economic recovery after the disaster [32]. Looking at the impact of disaster risk, research focused on disaster management has also been carried out. This includes the use of social media for the collection and dissemination of disaster-related information data [33] and the use of artificial intelligence in detecting disasters [34]. All of this is done to minimize the impact of disasters. According to [35], the threat of disasters cannot be eliminated, but their destructive power can be reduced, such that the impact of disasters can be reduced. Therefore, disaster risk management efforts need to be carried out in the form of preventative activities to reduce the threat of disasters, as well as mitigation in the form of physical development activities and capacity-building, preparedness, and public awareness to face disaster threats [36,37]. Disaster risk management is needed as, in the future, it is estimated that the level of disaster risk will increase, as triggered by climate change and mass development in various countries.

Disaster management is needed in the form of activities carried out during the pre-and post-disaster periods, as well as during the emergency response. Pre-disaster activities can be in the form of risk management [38] while, during an emergency response, they can be in the form of a series of activities carried out during a disaster to deal with the adverse impacts caused [39]. The activities carried out may include rescue and evacuation of victims, fulfilment of basic needs, protection, management of refugees, and provision of infrastructure and facilities. Post-disaster activities that can be carried out include rehabilitation, reconstruction, and community economic recovery [40,41]. Overcoming the problem of economic losses and damage to infrastructure and community settlements may occur through protection by having disaster insurance products. Disaster insurance is a mitigation program against the potential risk of loss that may arise due to natural disasters. Disaster insurance can provide alternative funding for management in the event of a disaster or during the post-disaster period. The selection of insurance products for loss and protection serves as a solution for overcoming the losses and damage due to disasters. Insurance can also provide a solution for the economic recovery of affected communities and post-disaster areas [42].

Disaster insurance is a suitable method for transferring risk to insurance companies [43]. The development of disaster insurance has resulted in various types of insurance, according to the risks faced. For example, floods can cause crop losses for farmers; to overcome the risk of crop losses, agricultural insurance is used. Agricultural insurance is a means for farmers to be compensated for the risks of farming, especially those associated with food crops, horticulture, and plantations due to flooding [44]. Compensation is given to farmers from the premium payments that have been made during the insurance program. Research has revealed several approaches for addressing the problem of the risk of loss, including earthquake insurance, which provides guarantees for properties against the risk of damage or loss caused by earthquakes [45,46], and property insurance, which covers the risk of property damage (e.g., for cars, electronic equipment, or houses) [47].

Research has suggested that disaster risk insurance may follow various different systematic approaches, according to the disaster, the condition of the area, and the condition of the community. A systematic literature review related to disaster risk insurance is quite interesting. The development of the types of risks insured in post-disaster recovery was the initial motivation for this research, and we wished to learn how far research into disaster risk insurance has developed each year, and what types of disaster insurance have been widely studied. With this knowledge, it is possible to know which types of disaster risk insurance are interesting for research and development in the future. This study was carried out based on articles that discuss insurance as a form of disaster risk management. Identification and evaluation were carried out by considering the level of development of disaster insurance each year, the types of disaster insurance, the development of disaster insurance in each country, and the types of disaster risk insurance, which have been quite widely discussed. The identification and evaluation considered the opportunities for the development of disaster insurance and the level of future needs in overcoming the risk of losses that occur. In addition, research related to how disaster risk insurance can be an effective means of economic recovery for communities affected by disasters was also considered.

Research discussing disaster insurance in general tends to focus on how the various types of disaster insurance have developed. In contrast, in this study, we consider which conditions lead to disaster-based insurance coverage and impact-based insurance coverage. This general research is very useful for regulators (i.e., governments), in terms of planning the provision of funds for post-disaster management, including infrastructure improvement and recovery of economic activities in disaster-affected areas. Thus, government policies for economic recovery can be realized more quickly. Meanwhile, specific research is usually more useful for investors and insurance companies in order to design schema for insurance products.

2. Materials and Methods

2.1. Scientific Article Data

In this study, we selected and identified the literature that focuses on insurance as disaster risk management for review. These materials have focused on various types of natural disasters, in the form of floods, earthquakes, storms, droughts, climate change, and other natural disasters. The data used were articles obtained from several sources indexed by Scopus and Google Scholar. The articles considered as literature material were published from 2000–2021 and, so, 21 database periods were used. The articles considered in the literature took the form of journal articles, proceedings, and the results of published doctoral theses. Furthermore, they were written in English and discussed insurance as disaster risk management. The search was carried out using the Publish or Perish software, selecting data sources in the form of Scopus and Google Scholar. In the selection of Scopus and Google Scholar data sources, the keywords entered were the same, in the form of “insurance” and “disaster.” The maximum number of results selected was 1,000, and the publishing year ranged from 2000 to 2021.

2.2. Selection of Literature Database

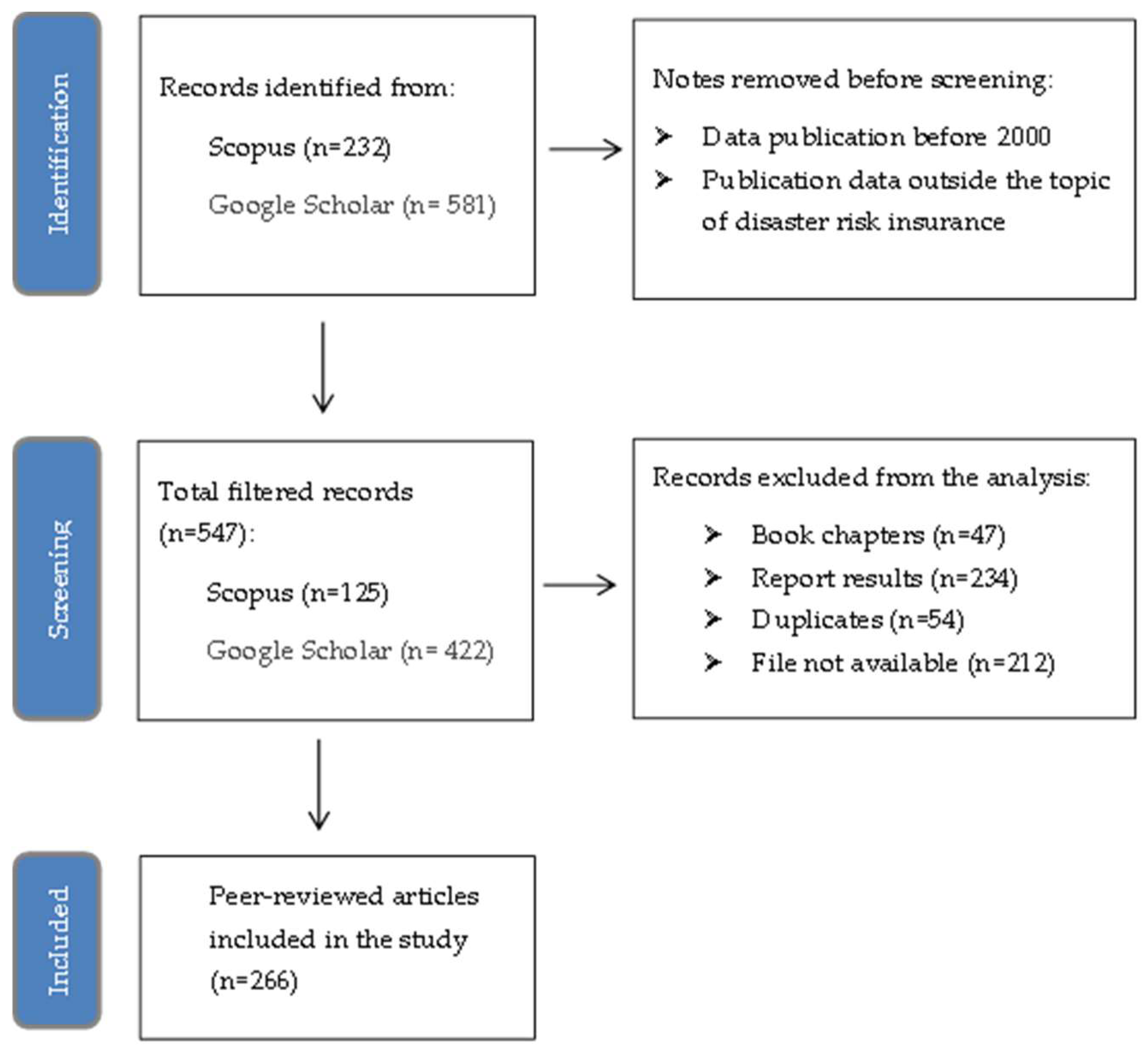

Literature data obtained from the Publish or Perish software were selected by removing literature in the form of books or topics that were considered irrelevant to the research conducted. This selection was carried out in order to obtain literature that was in accordance with our research objectives, in the form of articles discussing insurance as disaster risk management. Each result was checked, one by one, in order to obtain an appropriate database, in the form of journal articles, proceedings, and the results of published doctoral theses, written in English. After carrying out the selection, the identification of articles was also carried out by comparing the duplicate databases of Scopus and Google Scholar. If a duplicate was found, the data from Google Scholar were deleted, leaving one version of the title in the Scopus database. The total literature data obtained from the search results comprised 813 results; after checking and sorting, 266 articles were obtained, which were entered into the analysis detailed in this study. The literature review was carried out by mapping the article data obtained, including the development of insurance research as disaster risk management from 2000–2021, types of insurance as disaster risk management, and the development of disaster insurance in several countries, based on the literature used. The search process and strategy for obtaining relevant and quality articles is given in the form of a flowchart in Figure 1.

2.3. Methods and Systematic Data Analysis

We considered a systematic literature review method based on published articles. The articles obtained were assessed, identified, and interpreted based on the findings obtained after reading each article, in accordance with the research topic (i.e., insurance as an alternative to disaster management). However, in the systematic literature review process, a systematic evaluation stage is also needed when conducting research, such that there are no similarities to previous research. In this study, systematic analysis of article data was conducted in the following stages: (1) Visualizing the article database, relative to the relationships between the article data and the most-discussed topics. Visualization was carried out using the VOSviewer software in order to obtain the most widely used word quotes, the relationships between word quotes, and the level of attachment between word quotes; (2) mapping the number of articles each year (from 2000 to 2021), presented in the form of a bar chart, and providing general information related to research topics that are frequently cited; and (3) mapping the type of insurance in each country and the number of articles that have discussed it. This mapping was carried out by checking the articles one by one, in order to determine the countries and types of insurance discussed, including agricultural, flood, earthquake, property, crop, and natural disaster insurance.

3. Results

The following section describes the results of the data analysis focused on 266 articles, including visualization of article data, development of disaster risk insurance, and types of disaster insurance. Based on the database used, the majority of scientific papers were published with a Google Scholar index (60%), while 40% of scientific papers were published with a Scopus index. Therefore, the scientific papers in this field are mostly published on the Google Scholar index; the reason for this is that the majority of research results in the form of doctoral theses are published using the Google Scholar index. Meanwhile, only scientific works in the form of papers and journal articles are published on the Scopus index. In addition, the publication of scientific papers in journals with the Scopus index has its own complexity, where the review process is quite long and detailed, such that the quality of the scientific papers produced is higher.

3.1. Article Data Visualization

In this section, we provide a description of the visualization of article data obtained using the VOSviewer software. Visualization was carried out to determine the relationships between the data in the considered articles. The cluster size in the visualization shown in Figure 2 reflects how many articles discuss the keywords in the research topic. If the cluster in the visualization is large, it indicates that the word (quote) was present in in most articles in the database. In contrast, if a keyword is not widely discussed in the articles, then its cluster size is small among all words (quotations) related to the research topic. A line connecting two clusters indicates that a relationship exists between the two clusters in the form of quotes; furthermore, the distance between two clusters shows the strength of the relationship between the two clusters. For clusters that have a tendency to be highly bound (in the form of quotes), the distance between the two clusters is not far; however, if the distance between the two clusters is large, the two quotations have a weaker attachment [48,49].

Looking at Figure 2a, the cluster associated with the quote “insurance” has the largest size, compared to the others. This indicates that the word “insurance” is the most-discussed in the database. This is followed by clusters with the words “disaster” and “disaster insurance”, occupying the second and third ranks. This demonstrates that insurance has a great relationship with disaster risk management, as insurance can reduce the risk of losses due to disasters. Next, to further determine the relationships between clusters (in this case, quote words), we simply hover over the word quote that we want to see the relationships with. We demonstrate this through the relationships of the word “insurance” with others, as shown in Figure 2b. In the figure, it can be seen that relationships exist between this cluster and others, including “disaster”, “disaster insurance”, “risk”, “natural disaster”, “study”, “recovery”, “disaster risk financing”, and others. This indicates that, in the existing articles, there are relationships between concepts associated with disaster risk management using insurance. In addition, several countries have implemented insurance for disaster risk management. This is indicated by the quote of the word “insurance” having relationships with “Indonesia”, “New Zealand”, “Japan”, and “China”. Thus, these four countries are the most-discussed, based on the existing database of articles, when compared to other countries. However, this does not mean that countries other than the aforementioned four do not have disaster insurance options—it just has not been as widely discussed in other countries when compared to these four countries.

3.2. Development of Disaster Risk Insurance

Insurance as a form of disaster risk management has developed continually throughout the world. Disaster insurance has also received good responses from communities and governments, as indicated by the demand for disaster insurance both by the community (individuals) and by governments in the form of national disaster insurance. Disaster insurance can provide an efficient solution for addressing the problem of losses that occur both among the closest communities and on a large scale, namely, the state. Insurance is considered sufficient to help communities in the event of a natural disaster. For example, if a flood disaster occurs, the agricultural sector will experience a significant loss in the form of damage to the crops of farmers. The existence of agricultural insurance can cover the risk of loss to farmers due to the occurrence of a flood disaster [50]; however, it should be noted that, in insurance, policyholders need to pay an agreed-upon premium as a form of conversion or compensation for losses experienced by farmers when a disaster occurs. In this case, the party who will convert or provide compensation is the insurance company [51]. Research related to disaster risk insurance has attracted a lot of attention among researchers. Research conducted on disaster risk insurance has been widely published in both Scopus and Google Scholar. The research that has been published in this area has tended to increase over the period from 2000 to 2021, as evidenced in Figure 3. Research published in the form of proceedings, journal articles, and doctoral theses was collected in a literature database. The development of disaster risk insurance research each year, from the collected database of articles, is shown in Figure 3.

Based on Figure 3, the most publications related to insurance as disaster risk management occurred in 2018, with as many as 24 scientific articles being published. Meanwhile, the fewest number of publications occurred in 2001 and 2005, with only two articles in each of these years. Research in the disaster risk insurance sector has increased significantly leading up to 2021. This has been influenced by the risk of loss and the frequency of natural disasters that occur increasingly each year. Climate change leads to an increase in the frequency of disasters, especially those dependent on weather factors, such as droughts, floods, landslides, and storms. Indirectly, research related to disaster risk insurance is expected to continue to be a concern for researchers, even if it does not mean that the possibility will continue to increase.

Based on a database of 266 published articles, we classified the top 10 articles with the most citations. The citation count indicates how interesting the information provided in an article is, such that it can be used as a reference in other research articles. The more an article is cited, the more interesting the information it provides, and the more references are made in other articles in the following period. Figure 4 shows the citation information of the collected articles, with reference to the search results on Google Scholar.

The number of citations is not affected by how long ago the article was published. For example, looking at the number of citations in Figure 4, an article published in 2000 was in sixth place, while an article published in 2006 was in the first position. In addition, an article published in 2017 was in the fifth position and, when considering positions six to ten, most articles were published in the earlier part of the considered period; namely in 2000, 2002, 2003, 2007, and 2008. The number of citations of the article in the first position, that by Kunreuther in 2006, was a total of 339 citations in books, proceedings, journal articles, and other forms of articles. The ease of obtaining the article files, the quality of the article, and the information’s level all serve to attract the attention of researchers in making references in their research and determining whether the article may continue to be a reference for researchers in the future. A detailed explanation regarding the research topics discussed in the top 10 articles with the most citations is given in Table 1. Knowing the research topics from the top 10 most-cited articles provides material for evaluating the development of disaster risk insurance, both at present and in the future.

In the top 10 articles, the majority discussed hurricanes and floods. In the case of climate change, disasters that have shown increasing frequency of occurrence are hurricanes and floods, which are influenced by extreme weather. Based on Table 1, three articles focused on hurricane disasters, namely, [52,56,61]. Meanwhile, four articles focused on disasters caused by weather and floods [53,55,58,59]. Thus, it can be estimated that, in the future, research topics related to hurricanes, extreme weather, and floods will still be a concern for researchers conducting research into disaster risk management efforts, one of which is insurance. In Table 1, it can be seen that, in the top 10 cited articles, there were 7 articles discussing risk insurance associated with weather factors, demonstrating that the topic of risk insurance due to extreme weather is still actively being researched. An article with a certain topic and many citations indicates that the research topic is considered to be quite interesting to discuss and has a major contribution for later researchers.

3.3. Types of Disaster Insurance

Natural disasters that occur have different types, and the risks caused by disasters vary. For example, the risk of loss from an earthquake comes typically in the form of damage to buildings while, in a drought disaster, the risk of loss is most felt in the agricultural sector, namely, due to the death of community agricultural crops. Therefore, with the development of research, the types of insurance are progressing. Disaster insurance has become able to focus more on dealing with the specific risk of losses incurred. Disaster risk insurance can be mainly divided into six types: agricultural insurance, flood insurance, property insurance, earthquake insurance, crop insurance, and natural disaster insurance. Based on the database of articles collected, these types of disaster insurance have been widely used in various countries across the world. The purchasing of disaster insurance is adjusted according to the disasters that occur and the risks posed to the country. However, not all countries implement disaster insurance when tackling the risk of losses that occur. In such cases, disaster management still uses assistance from the government, in terms of funding the risk of losses that occur. The availability of disaster insurance by type in each country is detailed in Table 2.

Disaster insurance has undergone various developments to overcome the risk of losses that occur. Risk management is no longer general in nature, but has become more specific, based on the risks posed; this can be seen by the availability of various types of insurance. The availability of disaster insurance based on the type varies for each country, which is adjusted to the level of need and the impact of the risks that arise, such that the availability of insurance types in each country also differs. There are countries that have various types of disaster insurance available, as these countries are located in areas prone to natural disasters. However, there are also countries where only one type of disaster insurance is available, and even countries which have not implemented disaster insurance. For example, in China, the availability of disaster insurance has been well-developed. The availabilities of various types of disaster insurance are provided in Table 2. There are many types of disaster insurance, in the form of agricultural insurance, flood insurance, property insurance, earthquake insurance, crop insurance, and natural disaster insurance. Based on the collected database of published scientific papers, eight articles have discussed agricultural insurance, three articles have discussed flood insurance, one article has discussed property insurance, five articles have discussed earthquake insurance, six articles have discussed natural disaster insurance, and one article has discussed crop insurance. Based on Table 2, flood insurance is the most widely available type when compared to other types of insurance; that is, it was found to be available in 14 countries. Furthermore, in second place is natural disaster insurance (available in 13 countries), followed by crop insurance (which is available in at least 3 countries).

3.4. Methodology Used in Disaster Risk Insurance Studies

Based on the collected database of scientific publications, five main methods are used to determine the type of disaster risk insurance. Based on the results of the analysis, the most frequently used method is the characterization approach, which is present in as much as 40% of the article database. The next method is statistical approaches (in 18% of the article database), followed by inventory approaches (16% of the article database), heuristic approaches (15% of the article database), and deterministic approaches (12% of the article database). Methods using a characterization approach are the most widely used in determining the type of disaster risk insurance, as such an approach is based on the characteristics of the disasters that have occurred in the area being observed. Determination of disaster characteristics based on published articles is carried out by looking at geographic and topographical information in the observed area. Thus, the type of insurance offered is considered acceptable among the public and the government. Thus, in determining the type of disaster insurance by adapting to the characteristics of the disasters in a given area, effective risk management can be provided. Statistical approaches are mostly used to analyse the factors influencing the purchase of certain types of insurance and the number of premiums that are paid by the public. This approach can provide insurance companies with an overview of the type of insurance and the number of premiums paid by the public. Thus, the insurance offered to the public is deemed both acceptable and desirable.

Studies using the characterization method are carried out by analysing the geographical and topographic maps of an area to determine the types of disasters that may occur. The software used by the researchers may include ArcGIS (geographical information system) and HidroSIG Java (for visualization and analysis of hydro-climatological data tools). Among the studies applying a statistical approach, there are several statistical analyses that are commonly used, such as regression analysis, the Black–Scholes method, and Structural Equation Modelling (SEM). Among the studies following a statistical approach, researchers generally use software, such as SPSS (for interactive statistical analysis) in the statistical data analysis process, and MATLAB (for numerical computational programming) in the process of determining insurance premiums. Researchers using an inventory approach collect data in the form of the types of disasters and risks that occur in the area studied. These researchers use software such as AutoCAD Map to carry out data processing and the analysis of Geographic Information Systems. In the heuristic approach, the researchers apply a search strategy based on existing supporting data, in the form of disaster risk, to determine the best insurance policy. Finally, the researchers using a deterministic approach seek to estimate the parameters of the insurance model under study. These five approaches used by researchers are generally applied to determine the type of insurance, premiums, influencing factors, or the level of willingness to purchase the insurance on offer.

Based on the approach used in determining the type of insurance, the type of disaster due to extreme weather was the most discussed, in as much as 39% of the articles in the database. This was followed by natural disasters in general (as much as 32% of the articles), flood disasters (19%), and earthquake disasters (10%). Of the several researchers who discussed extreme weather disasters, they conducted research on disasters in the form of droughts, storms, floods, and forest fires. The number of researchers discussing extreme weather disasters has been influenced by a significant increase in the potential for disasters that have impacts on various sectors. Several sectors may be affected by extreme weather disasters; for example, an increase in high rainfall causes an increase in the potential for floods and landslides, which have impacts on the risk of loss for community settlements, agricultural land, and livestock. In addition, the research revealed that the mainland of the African continent has experienced the worst droughts. This is due to extreme weather disasters on the mainland of the African continent, causing minimal rainfall and increasing high temperatures, leading to drought on community agricultural land and causing crop failures for agricultural products. According to the research results, several types of insurance related to extreme weather disasters are offered, namely, crop, agricultural, flood, and property insurance.

4. Discussion

4.1. Trends in Disaster Risk Insurance Studies

Research on disaster risk management through insurance has developed quite significantly. Based on the results shown in Figure 3, research in the form of articles has increased over the last 21 years (2000–2021), considering the number of publications in the related literature. The published articles serve to evaluate the quality of solutions offered for disaster risk insurance. In the development of research in the future, the risk of loss caused by extreme weather is expected to be a prominent topic. The occurrence of climate change increases the potential natural disasters in the form of floods, droughts, and landslides [62,63]. The trend of research development, according to the articles that have been published, involves discussing the risk of extreme weather disasters caused by climate change. The evaluation of existing insurance continues to be carried out, including the level of gaps that occur and the adjustment of insurance premiums [64,65]. Premium adjustments are made due to the increased potential for disasters. The occurrence of climate change causes an increase in the potential for disasters due to increased extreme weather in all regions.

Research related to insurance as disaster risk management has attracted the attention of researchers in various countries. The potential risk of loss due to the occurrence of natural disasters has sparked the attention of researchers in both institutions and universities. This research has been carried out in the form of evaluation and appropriate policy solutions for dealing with natural disaster risks. One of the solutions offered to overcome this risk of loss is the purchasing of insurance. The natural disasters that occur in each region vary, leading to different types of insurance being chosen. Based on the results shown in Table 2, six types of insurance were observed in the database, namely, agricultural, flood, earthquake, property, crop, and natural disaster insurance. Based on the type, disaster insurance has different uses in funding the risk of loss. Agricultural insurance provides a guarantee of compensation for all risks of loss caused by natural disasters in farming, fishing, and animal husbandry. Crop insurance is part of agricultural insurance, which provides compensation for risks that occur due to disasters in the plant sector only. Flood insurance provides property insurance against the various risks that occur due to flooding. Property insurance provides insurance coverage for valuable assets that need to be protected—including houses, apartments, and shophouses—against the risk of disasters that may occur. Earthquake insurance provides coverage for property against damages or losses caused by an earthquake. Natural disaster insurance is usually taken out at the national scale, where this insurance becomes a disaster mitigation program against potential losses that may arise due to natural disasters, such as tsunamis, floods, earthquakes, and other natural disasters.

In continental Europe, flooding is a serious problem that has been affected by climate change. In overcoming the risk of unwanted losses, disaster insurance is one of the solutions offered to the public [64,66]. In addition, crop insurance is also in demand by farmers, as the disasters that occur can have an impact on the agricultural sector in Europe, influenced by the occurrence of extreme weather. Extreme weather causes high rainfall, leading to floods in plantation areas [67]. In the Americas, based on Table 2, flooding is a problem that often occurs [68,69]. Flooding disasters may cause losses in the agricultural crop sector. However, farmers often feel unable to buy flood insurance, as the premiums are generally quite high. To reduce the burden of such large premiums, farmers can purchase crop insurance [70], which typically provides lower premiums when compared to flood insurance because flood insurance bears a wide range of risk types in the form of property, vehicles, and crops; therefore, the premium offered is generally high. However, the premiums for crop insurance may be lower, as the risk borne is in the form of plant damage only. Tornadoes also often occur in several areas of the Americas, and they pose a threat with a large risk of loss [71]. However, tornado insurance does not yet exist in the Americas. To overcome these problems, we look at the risk of losses caused by tornadoes, namely, the damage to vehicles, houses, and other property. The solution to overcoming these losses is that the public can buy a type of insurance that covers the risk of loss from any disaster that occurs; for example, they can buy property insurance, which covers the risk of loss from a tornado.

Due to climate change, the African region has been experiencing extreme weather, resulting in drought and causing the agricultural sector to experience crop failure. Agricultural insurance can provide a solution for overcoming crop failures in agricultural production [72,73]. In addition, in the Asian region, the availability of insurance types varies widely, causing several countries in the Asian region to have a high disaster risk. As shown in Table 2, based on the database of articles that have been collected, China, Indonesia, Korea, and Japan have experienced developments in the availability of types of disaster risk insurance.

4.2. Sustainable Disaster Risk Insurance

The climate change that is occurring is of widespread concern among researchers. The impacts of climate change are causing warmer temperatures, rising sea levels, and erratic rain patterns, as well as other extreme weather conditions. The disasters that may occur can lead to losses in the socio-economic sector. These risks cannot be avoided, especially if they are exacerbated by the occurrence of climate change. Disaster insurance plays an important role in funding in the event of a disaster, or as a means of economic recovery [74]. The existence of disaster insurance guarantees the availability of funds for economic recovery. In the agricultural sector, agricultural insurance is sufficient to help farmers overcome the losses they experience such that, in the future, they will have the capital and supplies to procure the seeds and fertilizers they require [75,76]. Meanwhile, on a large scale, national disaster insurance can assist recovery, both during and after disasters. In the event of a disaster, such insurance can provide the capital for needs during an emergency response, in the form of tents, basic necessities, and medicines. Meanwhile, after the disaster, the government has the available funds to recover the economy affected by natural disasters. Activities that can be carried out take the form of infrastructure development, offices, and community economic centres. Thus, with insurance, the large-scale, planned, timely, and targeted sustainable financing needs can be met, which are managed transparently to protect state finances.

4.3. Types of Disaster Insurance Based on Geographical Conditions

Based on the results shown in Table 2, considering the type of insurance, the available insurance in a given country differs, as adjusted to the geographical conditions of the country. For example, earthquake insurance is quite popular in Japan, Indonesia, China, and New Zealand. Earthquake insurance is quite attractive to these four countries as large-scale earthquakes often occur. Earthquakes often occur in Japan due to its geographic location, above four large plates of the earth’s crust (called tectonic plates) [77]. Meanwhile, China is quite attractive for earthquake insurance as it is influenced by its geographic location in mountainous areas, which cover 73.4% of the land area and which have an impact on the frequent occurrence of earthquake disasters [78]. In addition, earthquake insurance is quite popular in New Zealand, due to the fact that earthquakes with high intensity frequently occur in the country, causing considerable economic loss to its communities [79,80].

Property insurance is generally preferred in geographical areas where floods, volcanic eruptions, and earthquakes often occur. Property insurance is purchased to obtain compensation for damage to property owned by the community [81]. Meanwhile, agricultural, flood, and crop insurance are generally in demand in geographic areas that have extreme weather. These three types of insurance have experienced an increase in demand in the last five years, as influenced by climate change. For example, in China, which features mountainous areas, the extreme climate has caused some areas to be submerged by floods recently. As such, flood insurance is quite attractive to the public in order to minimize the risk of losses they experience [82]. In addition, agricultural and crop insurance are of interest to people in several regions of China. The purchasing of agricultural insurance is carried out in order to reduce the losses experienced by the community in the farming, livestock, and fisheries sectors caused by extreme weather in the form of floods and hurricanes [83,84]. However, farmers may also be interested in buying crop insurance, which is adjusted to the risk of loss in the crop sector caused by disasters. Crop insurance is in demand by farmers in China, as the premiums provided are more affordable [85]. Furthermore, flood insurance is quite attractive on the European continent, as floods occur often in several European countries. Flood disasters in Europe have experienced a steep increase and are predicted to occur more often due to global warming [64,66].

Natural disaster insurance is generally in demand in countries with a high level of potential for natural disasters. The country purchases natural disaster insurance, which is generally used for the availability of funds in disaster management on a national scale. The funds are used to mitigate post-disaster losses, in the form of infrastructure development and long-term economic recovery. Several studies that discuss natural disaster insurance have considered the countries of Japan, Indonesia, and China. Considering Indonesia’s geographical location, which is between two continents and two oceans, it is naturally prone to disasters. In addition, Indonesia is located between the Eurasian, Indo-Australian, and Pacific plates. The movement of these plates will eventually cause various natural disasters, such as volcanic eruptions, earthquakes, and tsunamis. In 2018, the Indonesian government formed a policy to conduct research on natural disaster mitigation schemes by purchasing insurance [86,87]. Meanwhile, research related to natural disaster insurance in China has been influenced by geographic locations in mountainous areas and its harsh climate, causing disasters to occur frequently and posing a fairly large risk of loss. Due to its topography and natural conditions, China is one of the countries with the highest disaster risks in the world. Disasters that often occur include hurricanes, floods, landslides, and earthquakes, leading to many studies which have examined the effect of natural disaster insurance in post-disaster management [88,89,90,91].

5. Conclusions

The provision of an overview of the development of insurance research as a response to the risk of disaster losses can increase the interest of researchers in developing this topic. Research related to disaster risk insurance needs to be developed and continually carried out, as natural disasters continue to occur, and their frequency has been increasing due to climate change. Research related to disaster insurance has continued to increase over the last 21 years (2000–2021). Annual risk management continues to progress and has been effective in overcoming the losses that occur; however, the risk of disasters occurring has also continued to increase with time. Research conducted on an ongoing basis can minimize the risks that occur. The systematic literature review method can be used to facilitate future research findings related to research topics that are currently experiencing development. Some tools that can be used to determine developments and research that have not been well-developed are Publish or Perish software and VOSviewer; that is, Publish or Perish software can help to find articles related to the research topics to be developed, while the VOSviewer software can map research topics that have been carried out, such that research topics that have not been considered which should be developed by researchers can be determined. The involvement of institutions and universities in disaster risk insurance research can improve academic products. The improvement of academic products related to research findings also needs to be carried out through the publication of scientific works at the international level. Thus, the availability of information on the development of actuarial science research, especially regarding disaster risk insurance, may be increased, leading to increases in knowledge for other researchers. In addition, the availability of information also increases innovation, creativity, and further disaster management.

Based on our findings, we found that research related to disaster risk insurance continues to increase annually. Various types of disaster risk insurance have been developed, based on the level of need and the risk that is to be insured against, including six key types of insurance: agricultural, flood, earthquake, property, crop, and natural disaster insurance. The type of insurance purchased is affected by the local prevalence of disasters, which often occur on a large scale and cause considerable losses. The disasters that occur are generally influenced by the geographic conditions of a disaster-prone area. Research on extreme weather loss insurance has been conducted more extensively over the past five years, and it is an interesting field of research, both at present and for the future. This is influenced by climate change around the world, causing disasters due to extreme weather to continue to increase.

The main limitation of our systematic literature review research related to the databases used, considering the topic of disaster insurance in general, which considers floods, earthquakes, hurricanes, droughts, climate change, and other natural disasters. We constructed a database of articles obtained from Scopus and Google Scholar, which were written in English. The articles used as representations of the literature were in the form of journal articles, proceedings, and published thesis/dissertation results. Based on this limitation, further research will be carried out considering topics that are more specific to certain types of natural disaster risks, such as earthquake disaster insurance, extreme weather disaster insurance, and so on, which is still relatively undeveloped. As such, the source of the article data used can be expanded not only to Scopus- and Google Scholar-indexed articles, but we may add articles from Crossref, Web of Science, and Microsoft Academic. In this way, the findings and analyses may be more specific. In addition, we will also consider articles written in other international languages—for example using French, Spanish, Russian, Mandarin, and Arabic—in order to expand the article data as a basis for obtaining more comprehensive research findings.

Author Contributions

Conceptualization, K.; methodology, S. and S.S.; formal analysis, M.M. and K.; investigation, S. and M.M.; resources, S.S. and M.M.; writing—original, K. and S.; writing—revision and editing, K.; writing—review and editing, S.; supervision, K. All authors have read and agreed to the published version of the manuscript.

Funding

The APC was funded by Universitas Padjadjaran.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

The authors would like to thank the Directorate of Research and Community Service (DRPM) of Universitas Padjadjaran.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Wiegmann, M.; Kersten, J.; Senaratne, H.; Potthast, M.; Klan, F.; Stein, B. Opportunities and risks of disaster data from social media: A systematic review of incident information. Nat. Hazards Earth Syst. Sci. 2021, 21, 1431–1444. [Google Scholar] [CrossRef]

- Kron, W.; Eichner, J.; Kundzewicz, Z.W. Reduction of flood risk in Europe–Reflections from a reinsurance perspective. J. Hydrol. 2019, 576, 197–209. [Google Scholar] [CrossRef]

- Petrucci, O.; Aceto, L.; Bianchi, C.; Bigot, V.; Brázdil, R.; Pereira, S.; Kahraman, A.; Kılıç, Ö.; Kotroni, V.; Llasat, M.C.; et al. Flood Fatalities in Europe, 1980–2018: Variability, Features, and Lessons to Learn. Water 2019, 11, 1682. [Google Scholar] [CrossRef] [Green Version]

- Alfieri, L.; Feyen, L.; Salamon, P.; Thielen, J.; Bianchi, A.; Dottori, F.; Burek, P. Modelling the socio-economic impact of river floods in Europe. Nat. Hazards Earth Syst. Sci. 2016, 16, 1401–1411. [Google Scholar] [CrossRef] [Green Version]

- Paprotny, D.; Sebastian, A.; Morales-Nápoles, O.; Jonkman, S.N. Trends in flood losses in Europe over the past 150 years. Nat. Commun. 2018, 9, 1985. [Google Scholar] [CrossRef]

- Zanardo, S.; Nicotina, L.; Hilberts, A.G.J.; Jewson, S.P. Modulation of Economic Losses From European Floods by the North Atlantic Oscillation. Geophys. Res. Lett. 2019, 46, 2563–2572. [Google Scholar] [CrossRef]

- Li, Z.; Chen, M.; Gao, S.; Gourley, J.J.; Yang, T.; Shen, X.; Kolar, R.; Hong, Y. A multi-source 120-year US flood database with a unified common format and public access. Earth Syst. Sci. Data 2021, 13, 3755–3766. [Google Scholar] [CrossRef]

- Zúñiga, E.; Magaña, V.; Piña, V. Effect of Urban Development in Risk of Floods in Veracruz, Mexico. Geosciences 2020, 10, 402. [Google Scholar] [CrossRef]

- Young, A.F.; Papini, J.A.J. How can scenarios on flood disaster risk support urban response? A case study in Campinas Metropolitan Area (São Paulo, Brazil). Sustain. Cities Soc. 2020, 61, 102253. [Google Scholar] [CrossRef]

- Baxter, P.; Bettucci, L.S.; Costa, C.H. Assessing the earthquake hazard around the Río de la Plata estuary (Argentina and Uruguay): Implications for risk assessment. J. S. Am. Earth Sci. 2021, 112, 103509. [Google Scholar] [CrossRef]

- Perez-Oregon, J.; Varotsos, P.K.; Skordas, E.S.; Sarlis, N.V. Estimating the Epicenter of a Future Strong Earthquake in Southern California, Mexico, and Central America by Means of Natural Time Analysis and Earthquake Nowcasting. Entropy 2021, 23, 1658. [Google Scholar] [CrossRef] [PubMed]

- Assumpção, M.; Veloso, A.V. The 1885 M 6.9 Earthquake in the French Guiana–Brazil Border: The Largest Midplate Event in the Nineteenth Century in South America. Seism. Res. Lett. 2020, 91, 2497–2510. [Google Scholar] [CrossRef]

- Ramírez-Rojas, A.; Flores-Márquez, E.L.; Sarlis, N.V.; Varotsos, P.A. The complexity measures associated with the fluctuations of the entropy in natural time before the deadly México M8. 2 earthquake on 7 September 2017. Entropy 2018, 20, 477. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Durage, S.W.; Wirasinghe, S.C.; Ruwanpura, J. Comparison of the Canadian and US tornado detection and warning systems. Nat. Hazards 2013, 66, 117–137. [Google Scholar] [CrossRef]

- Raker, E.J. Natural Hazards, Disasters, and Demographic Change: The Case of Severe Tornadoes in the United States, 1980–2010. Demography 2020, 57, 653–674. [Google Scholar] [CrossRef] [PubMed]

- Strader, S.M.; Roueche, D.B.; Davis, B.M. Unpacking Tornado Disasters: Illustrating Southeastern US Tornado Mobile and Manufactured Housing Problem Using March 3, 2019 Beauregard-Smith Station, Alabama, Tornado Event. Nat. Hazards Rev. 2021, 22, 04020060. [Google Scholar] [CrossRef]

- Mirus, B.B.; Jones, E.S.; Baum, R.L.; Godt, J.W.; Slaughter, S.; Crawford, M.M.; Lancaster, J.; Stanley, T.; Kirschbaum, D.B.; Burns, W.J.; et al. Landslides across the USA: Occurrence, susceptibility, and data limitations. Landslides 2020, 17, 2271–2285. [Google Scholar] [CrossRef]

- Carrera, A.C.V.; Mendoza, M.E.; Allende, T.C.; Macías, J.L. A review of recent studies on landslide hazard in Latin America. Phys. Geogr. 2021, 1–44. [Google Scholar] [CrossRef]

- Yulihastin, E.; Nuryanto, D.E.; Trismidianto; Muharsyah, R. Improvement of Heavy Rainfall Simulated with SST Adjustment Associated with Mesoscale Convective Complexes Related to Severe Flash Flood in Luwu, Sulawesi, Indonesia. Atmosphere 2021, 12, 1445. [Google Scholar] [CrossRef]

- Wang, X.; Xia, J.; Dong, B.; Zhou, M.; Deng, S. Spatiotemporal distribution of flood disasters in Asia and influencing factors in 1980–2019. Nat. Hazards 2021, 108, 2721–2738. [Google Scholar] [CrossRef]

- Jamalullail, S.N.R.; Sahari, S.; Shah, A.A.; Batmanathan, N. Preliminary analysis of landslide hazard in Brunei Darussalam, SE Asia. Environ. Earth Sci. 2021, 80, 512. [Google Scholar] [CrossRef]

- Pasang, S.; Kubíček, P. Landslide susceptibility mapping using statistical methods along the Asian Highway, Bhutan. Geosciences 2020, 10, 430. [Google Scholar] [CrossRef]

- Kurniasari, Z.; Nieamah, K.F.; Arum, W.F. Live Recovery After Post Earthquake and Tsunami: Economic Review Case Studies of Earthquake and Tsunami in Japan and Indonesia. In IOP Conference Series: Earth and Environmental Science; IOP Publishing: Bristol, UK, 2021; Volume 704, p. 012005. [Google Scholar] [CrossRef]

- Parwanto, N.B.; Oyama, T. A statistical analysis and comparison of historical earthquake and tsunami disasters in Japan and Indonesia. Int. J. Disaster Risk Reduct. 2014, 7, 122–141. [Google Scholar] [CrossRef]

- Soden, R.; Lallemant, D.; Hamel, P.; Barns, K. Becoming Interdisciplinary: Fostering Critical Engagement With Disaster Data. Proc. ACM Hum.-Comput. Interact. 2021, 5, 168. [Google Scholar] [CrossRef]

- Hirabayashi, Y.; Mahendran, R.; Koirala, S.; Konoshima, L.; Yamazaki, D.; Watanabe, S.; Kim, H.; Kanae, S. Global flood risk under climate change. Nat. Clim. Change 2013, 3, 816–821. [Google Scholar] [CrossRef]

- CRED (Centre for Research on the Epidemiology of Disasters); UNDRR (United Nations Office for Disaster Risk Reduction). Human Cost of Disasters. An Overview of the Last 20 Years 2000–2019; United Nations: New York, NY, USA, 2020; Available online: https://www.emdat.be/publications (accessed on 13 December 2021).

- Banholzer, S.; Kossin, J.P.; Donner, S.D. The Impact of Climate Change on Natural Disasters. In Reducing Disaster: Early Warning Systems For Climate Change; Springer: Dordrecht, The Netherlands, 2014; pp. 21–49. [Google Scholar]

- Frame, D.J.; Rosier, S.M.; Noy, I.; Harrington, L.J.; Carey-Smith, T.; Sparrow, S.N.; Stone, D.A.; Dean, S.M. Climate change attribution and the economic costs of extreme weather events: A study on damages from extreme rainfall and drought. Clim. Change 2020, 162, 781–797. [Google Scholar] [CrossRef]

- Chen, Y.; Li, J.; Chen, A. Does high risk mean high loss: Evidence from flood disaster in southern China. Sci. Total Environ. 2021, 785, 147127. [Google Scholar] [CrossRef]

- Luu, C.; von Meding, J.; Mojtahedi, M. Analyzing Vietnam’s national disaster loss database for flood risk assessment using multiple linear regression-TOPSIS. Int. J. Disaster Risk Reduct. 2019, 40, 101153. [Google Scholar] [CrossRef]

- Daly, P.; Mahdi, S.; McCaughey, J.; Mundzir, I.; Halim, A.; Nizamuddin; Ardiansyah; Srimulyani, E. Rethinking relief, reconstruction and development: Evaluating the effectiveness and sustainability of post-disaster livelihood aid. Int. J. Disaster Risk Reduct. 2020, 49, 101650. [Google Scholar] [CrossRef]

- Malawani, A.D.; Nurmandi, A.; Purnomo, E.P.; Rahman, T. Social media in aid of post disaster management. Transform. Gov. People Process Policy 2020, 14, 237–260. [Google Scholar] [CrossRef]

- Fan, C.; Zhang, C.; Yahja, A.; Mostafavi, A. Disaster City Digital Twin: A vision for integrating artificial and human intelligence for disaster management. Int. J. Inf. Manag. 2021, 56, 102049. [Google Scholar] [CrossRef]

- Ravankhah, M. Earthquake Disaster Risk Assessment for Cultural World Heritage Sites: The Case of “Bam and Its Cultural Landscape” in Iran. Ph.D. Thesis, BTU Cottbus-Senftenberg, Cottbus, Germany, 2019. [Google Scholar]

- Etinay, N.; Egbu, C.; Murray, V. Building Urban Resilience for Disaster Risk Management and Disaster Risk Reduction. Procedia Eng. 2018, 212, 575–582. [Google Scholar] [CrossRef]

- Cuthbertson, J.; Rodriguez-Llanes, J.M.; Robertson, A.; Archer, F. Current and Emerging Disaster Risks Perceptions in Oceania: Key Stakeholders Recommendations for Disaster Management and Resilience Building. Int. J. Environ. Res. Public Health 2019, 16, 460. [Google Scholar] [CrossRef] [Green Version]

- Behera, J.K. Role of Social Capital In Disaster Risk Management: A Theoretical Review. Int. J. Manag. (IJM) 2021, 12, 221–233. [Google Scholar]

- Astuti, V.W.; Rimawati, R. Kelud Community Activities in Disaster Management. J. Qual. Public Health 2021, 5, 339–343. [Google Scholar] [CrossRef]

- Dube, E.; Wedawatta, G.; Ginige, K. Building-Back-Better in Post-Disaster Recovery: Lessons Learnt from Cyclone Idai-Induced Floods in Zimbabwe. Int. J. Disaster Risk Sci. 2021, 12, 700–712. [Google Scholar] [CrossRef]

- Zhang, Y.-Y.; Ju, G.-W.; Zhan, J.-T. Farmers using insurance and cooperatives to manage agricultural risks: A case study of the swine industry in China. J. Integr. Agric. 2019, 18, 2910–2918. [Google Scholar] [CrossRef]

- Kousky, C. The Role of Natural Disaster Insurance in Recovery and Risk Reduction. Annu. Rev. Resour. Econ. 2019, 11, 399–418. [Google Scholar] [CrossRef]

- Bao, X.; Zhang, F.; Deng, X.; Xu, D. Can Trust Motivate Farmers to Purchase Natural Disaster Insurance? Evidence from Earthquake-Stricken Areas of Sichuan, China. Agriculture 2021, 11, 783. [Google Scholar] [CrossRef]

- Afroz, R.; Akhtar, R.; Farhana, P. Willingness to pay for crop insurance to adapt flood risk by Malaysian farmers: An empirical investigation of Kedah. Int. J. Econ. Financ. Issues 2017, 7, 1–9. [Google Scholar]

- Yucemen, M.S. Probabilistic Assessment of Earthquake Insurance Rates for Turkey. Nat. Hazards 2005, 35, 291–313. [Google Scholar] [CrossRef]

- Athavale, M.; Avila, S.M. An Analysis of the Demand for Earthquake Insurance. Risk Manag. Insur. Rev. 2011, 14, 233–246. [Google Scholar] [CrossRef]

- Thistlethwaite, J.; Henstra, D.; Brown, C.; Scott, D. Barriers to Insurance as a Flood Risk Management Tool: Evidence from a Survey of Property Owners. Int. J. Disaster Risk Sci. 2020, 11, 263–273. [Google Scholar] [CrossRef]

- Van Eck, N.J.; Waltman, L. Citation-based clustering of publications using CitNetExplorer and VOSviewer. Scientometrics 2017, 111, 1053–1070. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Meng, L.; Wen, K.-H.; Brewin, R.; Wu, Q. Knowledge Atlas on the Relationship between Urban Street Space and Residents’ Health—A Bibliometric Analysis Based on VOSviewer and CiteSpace. Sustainability 2020, 12, 2384. [Google Scholar] [CrossRef] [Green Version]

- Arshad, M.; Amjath-Babu, T.; Kächele, H.; Mueller, K. What drives the willingness to pay for crop insurance against extreme weather events (flood and drought) in Pakistan? A hypothetical market approach. Clim. Dev. 2016, 8, 234–244. [Google Scholar] [CrossRef]

- Mutaqin, D.J.; Usami, K. Smallholder Farmers’ Willingness to Pay for Agricultural Production Cost Insurance in Rural West Java, Indonesia: A Contingent Valuation Method (CVM) Approach. Risks 2019, 7, 69. [Google Scholar] [CrossRef] [Green Version]

- Kunreuther, H. Disaster Mitigation and Insurance: Learning from Katrina. Ann. Am. Acad. Politi-Soc. Sci. 2006, 604, 208–227. [Google Scholar] [CrossRef] [Green Version]

- Raschky, P.; Weck-Hannemann, H. Charity hazard—A real hazard to natural disaster insurance? Environ. Hazards 2007, 7, 321–329. [Google Scholar] [CrossRef] [Green Version]

- Lodree, E.J., Jr.; Taskin, S. An insurance risk management framework for disaster relief and supply chain disruption inventory planning. J. Oper. Res. Soc. 2008, 59, 674–684. [Google Scholar] [CrossRef]

- Miranda, M.; Vedenov, D.V. Innovations in Agricultural and Natural Disaster Insurance. Am. J. Agric. Econ. 2001, 83, 650–655. [Google Scholar] [CrossRef]

- Deryugina, T. The Fiscal Cost of Hurricanes: Disaster Aid versus Social Insurance. Am. Econ. J. Econ. Policy 2017, 9, 168–198. [Google Scholar] [CrossRef] [Green Version]

- Ganderton, P.T.; Brookshire, D.S.; McKee, M.; Stewart, S.; Thurston, H. Buying Insurance for Disaster-Type Risks: Experimental Evidence. J. Risk Uncertain. 2000, 20, 271–289. [Google Scholar] [CrossRef]

- Glauber, J.W.; Collins, K.J.; Barry, P.J. Crop insurance, disaster assistance, and the role of the federal government in providing catastrophic risk protection. Agric. Financ. Rev. 2002, 62, 81–101. [Google Scholar] [CrossRef] [Green Version]

- Schwarze, R.; Wagner, G.G. The political economy of natural disaster insurance: Lessons from the failure of a proposed compulsory insurance scheme in Germany. Eur. Environ. 2007, 17, 403–415. [Google Scholar] [CrossRef] [Green Version]

- Picard, P. Natural Disaster Insurance and the Equity-Efficiency Trade-Off. J. Risk Insur. 2008, 75, 17–38. [Google Scholar] [CrossRef]

- Clarke, G.; Wallsten, S. Do remittances act like insurance? Evidence from a natural disaster in Jamaica. Evid. A Nat. Disaster Jam. Available SSRN 2003, 1–27. [Google Scholar] [CrossRef] [Green Version]

- Lee, C.H.; Lin, S.H.; Kao, C.L.; Hong, M.Y.; Mr, P.C.H.; Shih, C.L.; Chuang, C.C. Impact of climate change on disaster events in metropolitan cities-trend of disasters reported by Taiwan national medical response and preparedness system. Environ. Res. 2020, 183, 109186. [Google Scholar] [CrossRef]

- Zandalinas, S.I.; Fritschi, F.B.; Mittler, R. Global Warming, Climate Change, and Environmental Pollution: Recipe for a Multifactorial Stress Combination Disaster. Trends Plant Sci. 2021, 26, 588–599. [Google Scholar] [CrossRef]

- Tesselaar, M.; Botzen, W.W.; Robinson, P.J.; Aerts, J.C.; Zhou, F. Charity hazard and the flood insurance protection gap: An EU scale assessment under climate change. Ecol. Econ. 2022, 193, 107289. [Google Scholar] [CrossRef]

- Ivčević, A.; Statzu, V.; Satta, A.; Bertoldo, R. The future protection from the climate change-related hazards and the willingness to pay for home insurance in the coastal wetlands of West Sardinia, Italy. Int. J. Disaster Risk Reduct. 2021, 52, 101956. [Google Scholar] [CrossRef]

- Hudson, P.; Botzen, W.W.; Aerts, J.C. Flood insurance arrangements in the European Union for future flood risk under climate and socioeconomic change. Glob. Environ. Change 2019, 58, 101966. [Google Scholar] [CrossRef] [Green Version]

- Doherty, E.; Mellett, S.; Norton, D.; McDermott, T.K.; Hora, D.O.; Ryan, M. A discrete choice experiment exploring farmer preferences for insurance against extreme weather events. J. Environ. Manag. 2021, 290, 112607. [Google Scholar] [CrossRef] [PubMed]

- Adeel, Z.; Alarcón, A.M.; Bakkensen, L.; Franco, E.; Garfin, G.M.; McPherson, R.A.; Méndez, K.; Roudaut, M.B.; Saffari, H.; Wen, X. Developing a comprehensive methodology for evaluating economic impacts of floods in Canada, Mexico and the United States. Int. J. Disaster Risk Reduct. 2020, 50, 101861. [Google Scholar] [CrossRef]

- Marcillo-Delgado, J.C.; Alvarez-Garcia, A.; García-Carrillo, A. Analysis of risk and disaster reduction strategies in South American countries. Int. J. Disaster Risk Reduct. 2021, 61, 102363. [Google Scholar] [CrossRef]

- Azzam, A.; Walters, C.; Kaus, T. Does subsidized crop insurance affect farm industry structure? Lessons from the U.S. J. Policy Model. 2021, 43, 1167–1180. [Google Scholar] [CrossRef]

- Molina, M.J.; Allen, J.T. Regionally-stratified tornadoes: Moisture source physical reasoning and climate trends. Weather Clim. Extremes 2020, 28, 100244. [Google Scholar] [CrossRef]

- Meze-Hausken, E.; Patt, A.; Fritz, S. Reducing climate risk for micro-insurance providers in Africa: A case study of Ethiopia. Glob. Environ. Change 2009, 19, 66–73. [Google Scholar] [CrossRef]

- Awondo, S.N. Efficiency of region-wide catastrophic weather risk pools: Implications for African Risk Capacity insurance program. J. Dev. Econ. 2019, 136, 111–118. [Google Scholar] [CrossRef]

- Kaushalya, H.; Karunasena, G.; Amarathunga, D. Role of Insurance in Post Disaster Recovery Planning in Business Community. Procedia Econ. Financ. 2014, 18, 626–634. [Google Scholar] [CrossRef] [Green Version]

- Alam, A.S.A.F.; Begum, H.; Masud, M.M.; Al-Amin, A.Q.; Filho, W.L. Agriculture insurance for disaster risk reduction: A case study of Malaysia. Int. J. Disaster Risk Reduct. 2020, 47, 101626. [Google Scholar] [CrossRef]

- Hasan, T. Prospects of Weather Index-Based Crop Insurance in Bangladesh. Int. J. Agric. Econ. 2019, 4, 32. [Google Scholar] [CrossRef] [Green Version]

- Seko, M. Perceived preparedness and attitude of Japanese households toward risk mitigation activities following the great East Japan earthquake: Earthquake insurance purchase and seismic retrofitting. In Housing Markets and Household Behavior in Japan; Springer: Singapore, 2019; pp. 231–249. [Google Scholar]

- Xu, D.; Liu, E.; Wang, X.; Tang, H.; Liu, S. Rural Households’ Livelihood Capital, Risk Perception, and Willingness to Purchase Earthquake Disaster Insurance: Evidence from Southwestern China. Int. J. Environ. Res. Public Health 2018, 15, 1319. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Marquis, F.; Kim, J.J.; Elwood, K.J.; Chang, S.E. Understanding post-earthquake decisions on multi-storey concrete buildings in Christchurch, New Zealand. Bull. Earthq. Eng. 2017, 15, 731–758. [Google Scholar] [CrossRef]

- McAneney, J.; Timms, M.; Browning, S.; Somerville, P.; Crompton, R. Normalised New Zealand natural Disaster insurance losses: 1968–2019. Environ. Hazards 2021, 21, 58–76. [Google Scholar] [CrossRef]

- Ding, Y.; Wang, P.; Liu, X.; Zhang, X.; Hong, L.; Cao, Z. Risk assessment of highway structures in natural disaster for the property insurance. Nat. Hazards 2020, 104, 2663–2685. [Google Scholar] [CrossRef]

- Jiang, Y.; Luo, Y.; Xu, X. Flood insurance in China: Recommendations based on a comparative analysis of flood insurance in developed countries. Environ. Earth Sci. 2019, 78, 93. [Google Scholar] [CrossRef]

- Yanli, Z. An Introduction to the Development and Regulation of Agricultural Insurance in China. Geneva Pap. Risk Insur.-Issues Pract. 2009, 34, 78–84. [Google Scholar] [CrossRef] [Green Version]

- Zhang, H.; Dolan, C.; Jing, S.M.; Uyimleshi, J.; Dodd, P. Bounce Forward: Economic Recovery in Post-Disaster Fukushima. Sustainability 2019, 11, 6736. [Google Scholar] [CrossRef] [Green Version]

- Peng, R.; Zhao, Y.; Elahi, E.; Peng, B. Does disaster shocks affect farmers’ willingness for insurance? Mediating effect of risk perception and survey data from risk-prone areas in East China. Nat. Hazards 2021, 106, 2883–2899. [Google Scholar] [CrossRef]

- Aidi, Z.; Farida, H. Natural disaster insurance for Indonesia disaster management. Adv. Environ. Sci. 2020, 12, 137–145. [Google Scholar]

- Dubelmar, D.; Kartini, M.A.D.; Mareli, S.; Soedarno, M. Natural Disaster Insurance Policy in Indonesia: Proposing an Institutional Design. In Asia-Pacific Research in Social Sciences and Humanities Universitas Indonesia Conference (APRISH 2019); Atlantis Press: Amsterdam, The Netherlands, 2021; pp. 277–284. [Google Scholar]

- Shi, P.J.; Tang, D.; Liu, J.; Chen, B.; Zhou, M.Q. Natural disaster insurance: Issues and strategy of China. Asian Catastr. Insur. 2008, 79–93. [Google Scholar]

- Wang, F.; Yin, H. A new form of governance or the reunion of the government and business sector? A case analysis of the collaborative natural disaster insurance system in the Zhejiang Province of China. Int. Public Manag. J. 2012, 15, 429–453. [Google Scholar]

- Ma, S.; Jiang, J. Discrete dynamical Pareto optimization model in the risk portfolio for natural disaster insurance in China. Nat. Hazards 2018, 90, 445–460. [Google Scholar] [CrossRef]

- Shen, G.; Hwang, S.N. A spatial risk analysis of tornado-induced human injuries and fatalities in the USA. Nat. Hazards 2015, 77, 1223–1242. [Google Scholar] [CrossRef]

Figure 1.

Flowchart of the Search Strategy and Process.

Figure 2.

Article database visualization: (a) Clustered network graph from the article database; and (b) clustered network graph of keyword “insurance” with other keywords from the article database.

Figure 2.

Article database visualization: (a) Clustered network graph from the article database; and (b) clustered network graph of keyword “insurance” with other keywords from the article database.

Figure 3.

Data for publication of works from 2000 to2021.

Figure 4.

Top 10 article citations based on the collected database.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Research topics from the top 10 most-cited articles.

| Author | Indexed Database | Keywords | Citation | Focus |

|---|---|---|---|---|

| Kunreuther (2006) [52] | Scopus | Disaster insurance, building codes, homeowner motivation, community planning, disaster mitigation, risk assessment | 339 | Insurance, Hurricane Katrina, post-disaster economic recovery |

| Raschky and Weck-Hannemann (2007) [53] | Scopus | Natural hazard insurance, market failure, government assistance | 214 | Insurance, flood disaster, risk of economic loss |

| Lodree and Taskin (2008) [54] | Scopus | Inventory, news seller, emergency response, supply chain disruption | 190 | Risk management, insurance, insurance premium |

| Miranda and Vedenov (2001) [55] | Scopus | Agricultural insurance, natural disasters, weather, risk of loss | 178 | Extreme weather, agricultural risk, index-based insurance |

| Deryugina (2017) [56] | Scopus | Disaster relief, hurricane fiscal costs, social insurance | 168 | Hurricane, climate, risk of loss, insurance |

| Ganderton et al. (2000) [57] | Scopus | Disaster, risk, insurance | 166 | Natural disasters, risk of loss, insurance |

| Glauber et al. (2002) [58] | Scopus | Disaster risk protection, crop insurance, climate change, disaster relief | 159 | Extreme weather, crop loss, crop Insurance |

| Schwarze and Wagner (2007) [59] | Scopus | Political economy, natural hazards, flood insurance, Germany, EU | 114 | Flood disaster, insurance, economic loss |

| Picard (2008) [60] | Scopus | Equity–efficiency trade-off, natural disaster insurance | 111 | Natural disasters, risk of loss, insurance |

| Clarke and Wallsten (2003) [61] | Google Scholar | Insurance, Jamaica, altruism, natural disasters, migration | 100 | Hurricane, loss, insurance |

Table 2.

Number of articles in the database by type of insurance in each country.

| Country | Type of Insurance and Number of Articles in the Database | |||||||

|---|---|---|---|---|---|---|---|---|

| China | 8 | 3 | 1 | 5 | 6 | 1 | ||

| U.S.A. | 3 | 3 | 6 | 2 | 3 | |||

| Indonesia | 3 | 3 | 1 | 6 | ||||

| Korea | 3 | 2 | 3 | 6 | ||||

| Japan | 1 | 3 | 2 | |||||

| New Zealand | 7 | 1 | ||||||

| Australia | 1 | 1 | Description: | |||||

| England | 1 | 1 | ||||||

| Malaysia | 1 | 2 | Agricultural insurance | |||||

| France | 1 | 1 | ||||||

| Bangladesh | 2 | 1 | Flood insurance | |||||

| India | 1 | 2 | ||||||

| Ethiopia | 1 | Property insurance | ||||||

| Kenya | 1 | |||||||

| Hungary | 1 | Earthquake insurance | ||||||

| Georgia | 1 | |||||||

| Nigeria | 1 | Natural disaster insurance | ||||||

| Netherlands | 3 | |||||||

| Honduras | 1 | Plant insurance | ||||||

| Colombia | 1 | |||||||

| Mongolia | 2 | |||||||

| Caribbean | 1 | |||||||

| Mexico | 1 | |||||||

| Jamaica | 1 | |||||||

| Ghana | 1 | |||||||

| Poland | 1 | |||||||

| German | 1 | |||||||

| Egypt | 1 | |||||||

| Italy | 1 | |||||||

| Uganda | 1 | |||||||

| Georgia | 1 | |||||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Kalfin; Sukono; Supian, S.; Mamat, M. Insurance as an Alternative for Sustainable Economic Recovery after Natural Disasters: A Systematic Literature Review. Sustainability 2022, 14, 4349. https://doi.org/10.3390/su14074349

AMA Style

Kalfin, Sukono, Supian S, Mamat M. Insurance as an Alternative for Sustainable Economic Recovery after Natural Disasters: A Systematic Literature Review. Sustainability. 2022; 14(7):4349. https://doi.org/10.3390/su14074349

Chicago/Turabian StyleKalfin, Sukono, Sudradjat Supian, and Mustafa Mamat. 2022. "Insurance as an Alternative for Sustainable Economic Recovery after Natural Disasters: A Systematic Literature Review" Sustainability 14, no. 7: 4349. https://doi.org/10.3390/su14074349

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.