Abstract

Knowledge management (KM) practice is increasingly less considered as a supportive activity, as knowledge management processes (KMP) are inseparable from critical business processes (BP). Even though some scientific studies underlined that KM integration into BP are expensive and slow due to many organizational barriers, their sustainable value to organizations is undeniable. Although KMPs’ interactions have been studied in the scientific literature, there is still a lack of comprehensive studies related to knowledge-intensive organizations’ practices on the impact of the whole KM cycle—consisting of knowledge creation, sharing, storage, and application—on BP, such as development, production, and sales, for creating value-added (VA) and sustainability. In order to identify interconnections between individual KMP and BP, this study aimed to evaluate the influence of KMP on BP to support the continuous improvement of BP and the creation of VA in knowledge-intensive organizations. A research model was developed to analyze the impact of KMP on BP and VA perspectives. An empirical study was performed in Lithuanian project management companies that used BP in their operations and involved 144 managers from 72 IT organizations. Survey (structured questionnaire) and statistical analysis methods (one-way analysis of variance (ANOVA); Pearson’s correlation analysis; multiple regression analysis and mediation analysis; cluster analysis and chi-square analysis) were applied in this study. The research results confirmed that every KMP positively affected individual BP, where knowledge creation had the most significant impact. The hypothesis that every KMP positively affected the VA created in an organization was partially confirmed since knowledge sharing and creation had a strong influence. The study demonstrated that KMP as a whole had a positive effect on the central BP, change (improvement) of BP increased VA created in organizations, and BP acted as a mediator of the positive correlation between KMP and the VA. The effectiveness of individual KMP depended on the size of the organization. As a result, the study confirmed that KMP in organizations could not be performed separately and had to be integrated into BP to maximize the VA. The significance of the research model lay not only in its ability to identify the influence of KMP on the VA created in organizations but also in evaluating each KMP individually.

1. Introduction

Knowledge-intensive organizations facing sustainability and social responsibility challenges should consider economic, social, and environmental goals [1] and perceive value creation more holistically [2]. The focus of socially responsible business and behavior is not only to maximize profits but also to create valuable contributions to the environment [3] and the welfare of society that positively affect the community by integrating these social policies and values into the business operations of knowledge-intensive organizations [4,5]. In this case, effective and efficient knowledge potential management and integration into daily business processes (BP) are powerful ways to increase knowledge-intensive organizations’ sustainable performance, leading to a sustainable environment and community welfare [6,7].

A knowledge-intensive organization’s essential strategic resources are highly qualified staff and organizational knowledge with the most critical inputs by using knowledge management (KM) practices and knowledge management processes (KMP) for sustainable development and innovation creation [8]. Knowledge management (KM) in the context of sustainability has been increasingly crucial over the years for organizations aimed at achieving uniqueness and leadership [9,10,11]. Sustainability is critical to creating long-term value in business and requires system thinking to maximize the total value captured [12]. KM has an integrated impact on sustainability perspectives: economic, environmental, and social [13]. Knowledge is often identified as one of the most highly valued commodities in the knowledge economy [14] and as a strategic asset associated with sustainable organizational performance [15]. Knowledge strategy reflects the integration of KM practices such as KMP and aims to create new value by considering knowledge as a strategic resource in decision making and achieving uniqueness [16]. The knowledge-based view of the organization emphasizes that successful change to a sustainable business model requires the implementation of sustainability principles and institutionalizing them throughout organizational activities and business processes (BP) [8,17,18].

The importance of KM practices for overall business management has increased to the point that the management of KMP can be characterized as a vital instrument for improving organizational effectiveness, efficiency, and sustainable performance [8,9,19,20], as scientific studies [21,22,23,24,25] have revealed a positive correlation between KMP and organizational performance (OP). For example, Kun’s analysis showed that the organizations’ success or failure depended on their knowledge, where KMP was a crucial determinant of frugal innovation and affected sustainable corporate performance [26]. Cegarra-Navarro et al. developed a research model that explored the relationships among KM structures, organizational agility, and OP. The results of this modeling exercise supported the effectiveness of a specific set and sequence of KMP. They confirmed the direct effect of knowledge application on OP and the mediating impact of organizational agility in this relationship [22]. Khanal and Paudyal’s research presented that KMP (obtaining, organizing, and applying) were positively correlated with the OP measured in financial and market results, organizational effectiveness, and employee and customer satisfaction [24]. Tajpour et al. examined the effect of KM components on the sustainability of technology-driven businesses mediated by social media in emerging markets. The result showed that knowledge management components must be applied to technology-driven firms in all parts of the company to be in a sustainable environment [27]. Hossain et al. developed a model in which KMP affected corporate sustainability via corporate structure, culture, and leadership style [28].

Although the influence of KM on OP is more comprehensively researched, there is still a lack of scientific studies addressing problematic areas of the appliance of the whole KM cycle impact on BP leading to value-added (VA) evaluation aspects. Most of the studies were based primarily on the influence of KM on various organizational variables. In addition, there is a lack of studies evaluating the whole KM cycle [9,20], consisting of significant KMP impacting BP. Often, scientists focused on one or a set of variables influencing several KMP. For instance, Irani et al. analyzed only the impact of knowledge sharing on BP and organizational activities, as one of the essential KMP, even highlighting that knowledge sharing affects overall business performance. It is noted that knowledge sharing should be incorporated into BP to maintain a business and OP at a sustainable level [29]. As a result, research on assessing the benefits of the whole KM cycle on BP for creating organizational VA is rather incomplete.

Analysis of previous research suggested that the attempts to address these research issues and to answer the question of to what extent different KMP affect specific BP in creating VA were not sufficiently grounded in analyzed scientific studies. This study aimed to evaluate the influence of KMP on BP to support the continuous improvement of BP and the creation of VA in knowledge-intensive organizations. The main research objectives of this study were to determine the influence of KMP on the critical BP; identify relationships between KMP and dimensions of BP (quality, time, costs, etc.); calculate the effect size of KMP on the change in VA created in knowledge-intensive organizations; measure and justify empirically the overall VA created by KMP in knowledge-intensive organizations.

This research was based on the contingency theory of BP management that builds on available research on context-sensitive process management, identifies the main factors critical for process management, and provides milestones for process evaluation and optimization [30].

Based on the influence of the KM cycle on BP through process-oriented and VA perspectives, a research model was proposed, which allows for assessing the creation of the VA through KM practice by estimating the change in OP. In order to examine this research model, an empirical study was performed in Lithuanian information technology (IT) project management companies that used BP in their operations. These companies were chosen because they operated in a knowledge-intensive industry by developing project innovations with a clear structure of BP, planning, and control, using information and communication technologies (ICT), and by applying decision support systems. This study involved 144 managers from 72 IT organizations. Survey (structured questionnaire) and statistical analysis methods (one-way analysis of variance (ANOVA); Pearson’s correlation analysis; multiple regression analysis and mediation analysis; cluster analysis and chi-square analysis) were applied in this study. Survey analysis was based on statistical methods, and data analysis was performed with IBM SPSS software.

2. Literature Review

2.1. Measurement Aspects of KMP

Factors of the globalized world have created new challenges, requirements, and opportunities for building management models for knowledge-intensive organizations that include sustainability aspects. One of the fundamental questions arises regarding assessing the added value created by sustainability because, in business, the financial value is usually assessed [31,32]. In order to combine economic, social, and environmental goals, business organizations have to perceive value creation holistically, taking into account the role of knowledge in the economy and seeking an answer to the question of how KM can contribute to the creation of sustainable value [2]. Complex knowledge potential assessment and efficient management create preconditions for satisfying changing customer needs and creating value and uniqueness in the marketplace [33]. KMP is an essential instrument of cooperation and guarantees of employees in knowledge-intensive organizations in all business units to increase sustainable development [34]. KMP help ensure the sustainability of the flow of knowledge in knowledge-intensive organizations [7]. KM cycle has become equivalent to other main business processes as their application, analysis, optimization, evaluation, and management become necessary for an innovative, leadership-seeking, and sustainable organization. Scientists and business practitioners interpreted the importance of KMP in different ways [9,20]. Classification of KM according to researchers [35], as well as systematization of KMP according to importance [9,20] were used to distinguish the main KMP. From various analyzed combinations of KMP, reflected in KM studies conducted in IT organizations and based on Lithuanian IT organizations’ administration discussion results, four main ones could be singled out as the most critical: knowledge creation, sharing, storage, and application.

In a dynamic business environment, knowledge-intensive organizations emphasize the need for KM practice by specifying implementation peculiarities, analyzing interconnections between processes, and searching for more effective and efficient measurement tools to assess the impact on organizational outcomes and sustainability. KM practice has a significant relationship with a sustainable environment, environmental awareness, and green technological use [36]. Applying KMP creates value and sustainable competitive advantage in a dynamic environment. For instance, knowledge acquisition through social media optimizes learning. It encourages idea generation, and for technology-driven companies that lack resources, this acquisition enables development and sustainability in a dynamic environment [27]. Comprehensive assessment of KMP has become an inherent part of a challenging business environment; the need to evaluate the results of the KM cycle in BP to identify the VA of this practice to organizations has become inevitable [22].

In economics, value is defined as the result of a product, service, or process that brings benefits. The main models for determining value are based on the relationship between economic value and OP.

Economic value is commonly measured in both financial and non-financial terms. Some of the most popular models for measuring economic VA are the Economic Value Added (EVA) and Value-Added Intellectual Coefficient (VAIC) models. While the EVA model is based on an organization’s net profit (NOPAT) and weighted average cost of capital (WACC) and invested capital, the VAIC focuses on VA, not only structural capital but also human capital.

The difference between economic value and AV is that AV is created through change, optimization, and improvement of business models, processes, and activities to replace existing economic value by increasing productivity [37].

In a market economy, the VA of a business is often determined using financial and non-financial indicators. Financial indexes such as Return on Investment (ROI), Return On Equity (ROE), Return On Net Assets (RONA), Return On Assets (ROA), Cash Flow Return On Investment (CFROI), Cash flow (CF), Profit Before Interest, Taxes, Depreciation and Amortization (EBITDA), Market Value Added (MVA), Debt to Equity ratio (D/E), Capital Expenses (CapEx), Operating Expenses (OpEx), Company Value (EV), etc., describe the organization’s retrospective or results already achieved, and non-financial indicators, which are measured by the following indicators: order evaluation (number of orders delivered on time), satisfaction (number of satisfied customers), number of defects (number of defective products or percentage), delivery (time, lost in product delivery), returned goods (number of returned goods due to poor quality), complaints (number of unsatisfied customer complaints), innovation (number of new commercial products in the market), skills (staff skills in developing and producing new products), resource gap planned and actually used resources), time (time to use automated systems), etc., and which reflect the internal picture of the organization and point out the perspectives. To determine the value of the organization and the AV it creates, it is necessary to measure financial and non-financial indicators.

A review of both financial and non-financial measures of VA shows that VA could not be calculated on just one side. Financial indicators may be more objective and provide more accurate figures. Still, they do not reflect the internal picture of the organization, staffing problems, skills available, distinctiveness, level of opportunities for quality innovation, etc. Suppose plans to increase financial performance and AV are universal regarding cost reduction, revenue, and profit growth. In that case, it is not easy to create non-financial VA.

Organizational AV is the added economic value created through changes in the BP [38] that KM and KMP positively influence. Such a principle allows for refining the AV created by the organization, which is based not only on financial capital but also on human resources. In this way, a deeper approach to VA creation and measurement principles is affirmed, not limited to financial ratios and gross capitalization.

As a result, scientific studies started exploring every KMP’s outcomes and benefits to knowledge-intensive organizations, such as IT project management companies. However, assessing the relationship between the KM cycle and organizational BP has become an issue, as this research objective is still underdeveloped [39]. Furthermore, knowledge-intensive industry organizations aim to create a knowledge-based organization that can establish links between KMP, BP, and OP [40].

Analyzed research models have proven the benefits of KM for organizations, as they mainly focus on two main aspects: quality and performance. However, these research models [21,22,24,25,39,41,42] do not allow for comprehensive evaluation of the outcomes of the KM cycle into BP. For instance, Lee et al. provided a new metric, the KM performance index, to assess a firm’s KM performance at a point in time. Research results showed that when knowledge circulation process efficiency increases, the KM performance index will also expand, enabling firms to become knowledge intensive [41]. Chang and Lin explored that if firms could manage their knowledge resources effectively, a wide range of benefits could be reaped, such as improved corporate effectiveness, efficiency, innovation, and customer service [42]. Handzic and Durmic proposed a conceptual model that merges KM, intellectual capital, and project management aspects. The model was developed to analyze how combining KM, intellectual capital, and project management can enhance project success [25]. Foote and Halawi proposed a conceptual framework that included the project KM model, which helped identify knowledge sharing in IT software projects [39]. Zaim et al. explored the relationship between KMP and the impact of KMP performance using a variance-based theoretical approach instead of a process-based theoretical approach [21].

Another group of scientific studies was focused on research that addressed the assessment of KM based on KMP-oriented perspective to introduce evaluation criteria and even precise metrics of assessment [38,43,44,45,46,47,48,49]. For example, Al-Qarioti researched how variables such as knowledge accumulation, utilization, sharing practices and ownership identification, IT in knowledge capturing and usage of information systems, and knowledge organization (people, organizational climate, and processes) were related to OP [43]. Alrubaiee et al. explored the mediating effect of organizational innovation on the relationship between KMP and OP [44]. Mousavizadeh et al. showed that KMP implementation, top management support, and organizational culture positively affect KM business value [38]. Heisig et al. researched how KM can increase employees’ job satisfaction [45]. Novak proposed a research model concerning relations between KMP (creation, storage, transfer, and application) and OP and connections between knowledge infrastructure elements (technology, organizational culture, and structure) and OP, which defined OP with various performance indicators, from financial to strictly non-financial performance measures, and as a combination of several different performance indicators [46]. Abdi et al. studied the direct and indirect effects of organizational culture, KM, and organizational learning on innovation [47]. Abuaddous et al.’s study showed that KM, including knowledge process and infrastructure capabilities, positively affected all aspects of OP directly or indirectly [48]. Oufkir and Kassou proposed a model for measuring the performance of KM projects. The results supported the model designed for KM activities and related interactions [49].

To measure the effectiveness and efficiency of the KMP, it is crucial to consider the organization’s type, size, business sector, and other aspects [41,50,51,52]. For instance, Arora emphasized a balanced scorecard for strategy deployment that can effectively implement KM by developing and deploying a KM index [50]. Lee et al. proposed a KM performance index where the knowledge circulation process could affect the efficiency of work processes and the performance of management activities. Based on the argument regarding the knowledge circulation process characteristics, it was claimed that the KM performance index could measure organizational knowledge quality and was related to management performance [41]. Shannak presented direct KM performance and another way of evaluating KM performance based on the inclusion of KM strategy. It proposed a categorization matrix that classifies the performance indicators for potential use in KM performance measurements [51]. Kuah et al. proposed a Monte Carlo data envelopment analysis model to measure the stochastic performance of KM. A genetic algorithm was used to determine the appropriate data collection budget allocation for stochastic variables [52]. The proposed model is better than a deterministic approach in evaluating the efficiency of KM.

Based on analyzed studies, assessment of KMPs combined qualitative and quantitative approaches and specific measurement aspects. There is still a lack of comprehensive measurement resulting from KM practice influence on BP leading to AV perspective. Qualitative research is suitable for specifying assumptions laid down in previous research. The advantages of qualitative research are that it is better suited to evaluate intangible factors and the relationship of KM with human management aspects, such as culture, structure, behavior, competencies, etc. Furthermore, qualitative methods are effective when organizations need to identify the best practices. Quantitative approaches mostly use statistical techniques, hypotheses, and theory testing. They produce statistical results for identifying causal relationships. Quantitative research facilitates overcoming shortcomings related to the researcher’s subjectivity and is mainly used to measure specific KMP and their effects on BP [53]. Quantitative research in KM often uses metrics as input and/or output indicators directly related to KMP. The application of various metrics and specific indicators within the metrics allows for one to evaluate the effectiveness, efficiency, and quality of KMP and monitor their implementation. Metrics enable the evaluation of the results both in financial and non-financial terms.

2.2. Evaluation Aspects of Organizational BP

The output of one process transforms into the output of another process as a result; thus, the disruption of any process affects the activity of other processes and, accordingly, the results. The process combines material, financial and human resources into a chain of activities, allowing for achievement, management, and predicting the result. Many authors classify BP based on various characteristics. Rose distinguished between business administration and product-specific processes [54]. Moen and Norman paid more attention to process cyclicity [55]. Scientists try to classify the processes by dividing them into different classes according to the nature of the processes, whether they are primary or secondary [56,57,58]. Classification by BP can identify the organization’s activities and pay enough attention to each stage of the activity process. APQC (American Productivity and Quality Center) proposes to classify processes based on their nature and consistency in each organization by dividing them into two main branches: operating processes and management and support services. APQC emphasizes its interrelationship and connections rather than consistency [59]. It helps any process-based business organization identify the most important BP and easily link them to nearby processes. This study will analyze the main BP that enables the organization’s creation of value. It will be based on the authors’ classification of basic BP using the three most essential for IT services developing organizations: product development processes, product creation processes, and product sales processes [58].

The methodology of process-oriented perspective evaluation can be widely applied to measure various processes by measuring their effectiveness and efficiency. Therefore, the most often used factors and indicators are related to effectiveness, efficiency, and other performance criteria, determined by the peculiarities of the process itself and the intended result. Items of the same type used only once in an indicator of a specific process stage can be included in the overall indicator of the whole process. This enables measuring the duration and costs of the separate stages and the whole process. The obtained results can be compared with the respective earlier results of the same organization, with the planned results, with the results of the local, regional, or global competitors, as well as the best companies operating in the market; thus, they can be evaluated in respect of time, planning, and territorial dimension.

Often, the evaluation of process results is linked with the end product or service [56] presented to the consumer, its real and perceived value, i.e., objective and subjective value. Aa customer is not interested in the management structure of the organization, its strategic plans, or its financial structure; they are interested in the outcome, i.e., the value created for the organization [60]. In the stage of process result, the most often used indicator is the number of the items produced or services provided, compliance with the standards set for that product, and in the case of services, fulfillment of the client’s expectations.

Since process effectiveness and efficiency are most often directly associated with OP, the following criteria are often used in their measurement: KPI (Key Performance Index) measures process effectiveness; KSF (Key Success Factors) measures alignment of the process with the objective, strategy, and goals of the company; KPF (Key Performance Factor) defines the impact of the process on organizational success through operations; CSF (Critical Success Factors) reflects the factor of success; KII (Key Improvement Index) defines the results of the process in terms of quality. PPIs (Process Performance Indicators) are different from other quantitative indicators; these indicators define dichotomous (yes/no) variables of a specific process part or even a task.

Every BP is associated with different dimensions, metrics, and ways of implementing the measurement. Based on a scientific literature review [61,62,63], every metric consists of a set of criteria. For example, costs include such criteria as costs of operation and process costs, and production comprises costs per item; time: process cycle time, order processing time, production time per time unit, etc.; financial metrics: cash flow, return on equity, return on investment, margin, profit, etc. Ittner et al. examined the factors influencing the relative weights placed on CEO bonus contracts’ financial and non-financial performance measures [63]. The study revealed that the use of non-financial measures increased with the level of regulation, the extent to which the firm followed an innovation-oriented strategy, the adoption of strategic quality initiatives, and the noise in financial measures. Findings showed no evidence that the choice of performance measures in bonus contracts was associated with the level of financial distress or the value of CEO equity holdings relative to salary and bonus. Results also provided no support for the hypothesis that CEOs with greater influence over the board of directors were more likely to be compensated based on non-financial measures. Laitamäki and Kordupleski’s study aimed to expand business leaders’ knowledge of the critical drivers of customer satisfaction and BP excellence and strengthen their skills in developing profitable growth strategies based on customer VA [61]. Gaiardelli et al. proposed an integrated framework for after-sales performance measurement consisting of four levels (business, process, activity and development, and innovation). They provided an empirical application of the framework to four case studies that showed a link (explicit or, more often, implicit) between corporate strategic objectives, after-sales strategies, and after-sales performance measures [62]. Therefore, the proposed framework could be applied as a tool to base the definition of a company’s after-sales performance measurement system.

As a result, there are no unified measurement systems and sets of criteria and indicators that could be used to measure BP. However, scientists identified the main measurement metrics, and their applicability for every business sector has to be tested individually. Appropriately chosen criteria and indicators facilitate the preservation of the direction toward process improvement, which can measure the process at any stage and obtain both intermediate and final results.

2.3. Synergy between KM and BP

The relationship between KM and BP became the focus of scientists’ and business practitioners’ attention in the last decade, where many studies addressed the relationship between KM and OP.

KM and overall effectiveness comprise strategies and practices applied in an organization. It is a set of knowledge creation, sharing, and application processes to improve O.P. Both individual case studies and broader-scale research [19,64,65,66,67,68] show a direct relationship between KM and OP. For instance, Ahmed et al. identified the impact of KM practices, e.g., knowledge acquisition, conversion, application, and protection, on OP. The study results revealed that KMP resulted in quality customer service, high customer satisfaction, efficiency in resource utilization, profits, and overall improved OP [64]. Vidovi investigated the link between the quality of KM and the financial performance of an organization [68]. Zack et al. researched the relationship between KM practices and performance outcomes [19]. KM practices showed a direct relationship with intermediate OP measures, and OP showed a significant and direct connection to financial performance. There was no critical relationship found between KM practices and financial performance. Khanal and Paudyal’s survey of financial institutions showed that all BP were related to KM and helped organizations become innovative [24]; it was directly related to financial and non-financial OP.

KM relates to financial and non-financial aspects, such as product quality control and management, innovation, and performance. Zack and Barr proved that KM was related to organizational functioning (operational competence, customer loyalty, and production management) and positively affected financial results [69]. They claimed that financial results demonstrated that companies had to introduce more intermediate measures and evaluate the overall performance alongside applying the discipline of value management (operational competence, product leadership, and customer loyalty).

Knowledge and BP are integral elements of organizational success in the dynamic business environment. Starns and Odom also emphasized that improved OP requires integrating KM into the company’s management structure and business strategy [70]. BP can be regarded as a framework of organizational functioning used to attain competitive advantage. Wu and Chen claim that BP capabilities describe distinctive BP that uniquely contribute to organizational competence and, as a result, increase the company’s market value [71]. Rehman et al. showed that KM performs a vital role in analyzing and restructuring BP [72]. KM comprises the identification and integration of knowledge content relevant to every BP. Considering BP’ capabilities, KM has to be integrated into developing a business strategy to improve internal and external processes [73].

Research that links these two areas of practice is mainly based on a systematic approach to an organization or treats the whole organization as a system of processes. However, to perform a comprehensive analysis of the effect of KM, it was proposed to evaluate the impact of KMP on specific BP separately. This would determine which KMP has the most significant impact on each BP and which organizational VA they create.

2.4. A Research Model Evaluating the Influence of KMP on BP

The analysis of KM practice in a dynamic business environment highlighted the importance of IT for KM activities [8,19], particularly for KMP, and showed that the measurement of KM lacks a holistic approach. Still, many organizations treat KM as a supportive activity because they do not assess its actual benefits. In addition, there are very few conceptual models for researching the influence of KM on BP that could be used as a basis for empirical research.

The presented analysis of BP in contemporary organizations concludes that modern organizations tend to adopt a procedural approach to critical BP. Classification of BP remains complicated due to many different processes and their distinctiveness. The analysis also showed research gaps in the BP measurement field. This study’s approach to process measurement allows for a comprehensive and accurate analysis of organizational activities, classified into many processes. If the measurement comprises the value created by all critical BP, its average value reflects the value created by all organizations as a system of processes. At the same time, the measurement enables the analysis of different organizational activities in a step-by-step manner.

One of the main aspects of researching the influence of KM, emphasized in this study, is its positive impact on organizational VA. Many studies reported a positive correlation between KMP and OP, efficiency, intellectual capital, financial indicators, etc. However, it was rarely analyzed to what extent each KMP impacts specific BP from regarding VA perspective [24].

Many proposed research models were linked to the relationship between KM and VA. However, these models were not oriented to identify the influence of KMP on BP, their optimization and re-engineering, and the VA created in the organization. Brunswicker and Vanhaverbeke’s study explored enterprises engaged in external knowledge sourcing, a form of open inbound innovation. The study indicated that external knowledge sourcing is sensible for enterprises. It offers performance benefits and can improve innovation performance in two dimensions: the success of launching innovation and the appropriation of financial value from new products and services [74].

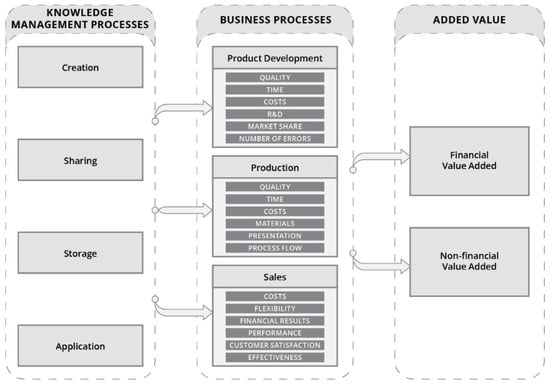

Salunke et al. showed how B2B service firms manage knowledge to deliver new VA solutions and, in turn, competitive advantage, addressing calls for research into this important yet neglected area [75]. Iqbal et al. revealed that KM enablers significantly impact KMP. The results also indicate that KMP influences OP directly and indirectly through innovation and IC by adding value to the organization [76]. Al Ahbabi et al. underlined that KMP, knowledge creation, capture and storage, sharing, application, and use positively impacted operational, quality, and innovation performance in the public sector in the UAE [77]. Khanal and Paudyal’s stated that KMP correlated with OP through financial and market results, organizational effectiveness, employee satisfaction, and customer satisfaction [24]. Paschen et al. showed how the B2B process creates AV with AI support [78]. Scientists represent that the premise of AI is to turn vast amounts of data into information for superiors’ knowledge creation and KM in B2B sales. A research model was developed based on previous scientific research analysis to measure KMP’s influence on BP leading to VA creation (Figure 1). The model allows for measuring the impact of every KMP on crucial BP that contribute to the VA in organizations and the influence of KMP as a whole.

Figure 1.

The research model of the influence of KMP on BP (created by the authors).

It is advisable to evaluate the influence of KMP over a certain period and relate the evaluation to organizational change, improvement of the situation, and increased effectiveness. KMP affects individual BP through specific dimensions. Most often, the effectiveness of BP and its change is measured by the change in quality, production time, costs, R&D, market share, number of errors, the effectiveness of the process flow, amount of raw materials, customer satisfaction, and other indicators.

Improvement of these indicators defines the effectiveness of the BP themselves, which, according to the research model (Figure 1), results from the increasing positive influence of KMP.

Different perspectives and different measurements and metrics are used to evaluate organizational processes. For each metric, the authors present different criteria, for example, costs—criteria for financial metrics such as activity, costs, process costs, cost of producing one part or creating a service unit; time—process cycle time, order time, production time per unit of time, etc. criteria; other financial metrics—cash flow, return on equity (ROE), return on investment (ROI), return on sales (ROS), margins, profit, etc.

After analyzing the commonly used methodologies, criteria, and indicators, the value of any BP is based on the measurement of both quantitative and qualitative indicators. Qualitative indicators are usually associated with emotions: satisfaction of employees and other members of the organization, motivation, and suitable environment, etc. Quantitative indicators are associated with the organization’s performance indicators, which always turn into a financial expression and directly impact performance indicators, such as sales revenue, long-term and short-term assets, gross and net profit, liabilities, etc.

Research results show that no unified criteria can be used to measure organizational processes, just as there is no consensus on what methodology or tools to use. However, key metrics have been identified, and their suitability for each organization should be checked individually. A correctly selected indicator helps to maintain the direction of process improvement, allows it to be measured at any step, and measures intermediate and final results. VA created by BP is analyzed through two dimensions: financial value and non-financial value. It is advisable to measure the VA not directly but through changes in BP, specifically, the change of each indicator associated with the process, including its metrics. In this way, the conceptual model evaluates BP as a mediator between KMP and financial/non-financial VA. The model can be used to measure VA in many process-based organizations. However, it should be adapted for each organization type. The specific process dimensions and metrics depend on the type of business activity and organization, size, nature of product or service, and other aspects.

3. Materials and Methods

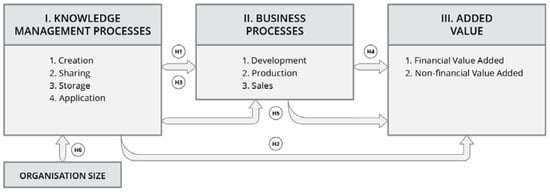

The object of the research is the influence of KMP on the creation of VA by BP in organizations. The research aims to determine KM’s direct and indirect influence on BP regarding VA. Objectives of the research are to determine the influence of KMP on the key BP; identify relationships between KMP and dimensions of BP (quality, time, costs, etc.); calculate the effect size of KMP on the change in VA created in organizations; empirically measure and justify the overall VA created by KMP in organizations. Empirical research is aimed at testing the following hypotheses:

Hypotheses (H1):

Every KMP separately has a positive effect on individual BP.

Hypotheses (H2):

Every KMP has a positive effect on the VA created in the organization.

Hypotheses (H3):

KMP as a whole has a positive effect on the essential BP.

Hypotheses (H4):

Change (improvement) of BP increases the VA created in the organization.

Hypotheses (H5):

BP acts as a mediator of the positive correlation between KMP and VA.

Hypotheses (H6):

Effectiveness of individual KMP depends on organization size.

Following the above-presented conceptual model, we developed a model for empirical analysis (Figure 2).

Figure 2.

Model for empirical analysis (created by the authors).

In the first part of the study, respondents were asked to evaluate the changes in KMP on the -point Likert scale. Mathematical methods were used to calculate the results. In this part, generalized indicators are used to measure the BP.

Factor analysis was used to determine the loading of every factor and the relationships between the factors. Correlations were calculated to determine relationships between variables; multiple linear regression was used to measure the potential positive influence. Multiple regression is a statistical technique that can be used to analyze the relationship between a single dependent variable and several independent variables. The objective of multiple regression analysis is to use the independent variables whose values are known to predict the value of the single dependent value. Each predictor value is weighed, with the weights denoting their relative contribution to the overall prediction. The multiple linear regression formula is presented below [79]:

Y = a + b1X1 + b2X3 + … + bnXn

Here, Y is the dependent variable, and X1, ...., Xn are the n independent variables. In calculating the weights, a, bl, ...., bn, regression analysis ensures maximal prediction of the dependent variable from the set of independent variables. This is usually performed by least squares estimation. This approach can be applied to analyze multivariate time series data when one of the variables is dependent on a set of other variables. It is possible to model the dependent variable Y on the set of independent variables. At any time, given the independent variables’ values, it is possible to predict the value of Y from Equation (1).

Mediation analysis was used to test hypothesis H5, which states that KMP have a larger positive influence indirectly through a mediator (BP). K means cluster analysis was used to determine if the effectiveness of KMP can be dependent on organization size (H6).

In the second part of the study, BP’s owners evaluated BP changes on the same Likert scale. To evaluate quantitative changes, metrics and indicators characteristic of those organizations were used. Change of indicators over a set period (Δt = 3 years) was used to assess the change in BP. Change in VA was also calculated on the basis of two dimensions drawn from scientific studies, evaluated by overall indicators and other financial and non-financial indicators.

The research data analysis included an overall evaluation of the collected data and scale reliability and validity analysis. Change in KMP in the respondent organizations was assessed.

Calculations were based on correlation and regression analysis. The first step was to calculate correlation coefficients. They show relationships between change in individual KMP and BP, change in individual KMP and VA, and change in individual BP and VA.

Afterward, the statistically significantly interrelated variables were subjected to regression analysis, which was used to evaluate the influence of individual KMP on BP and VA.

The empirical study used a wide-scale survey of middle-level managers who are owners of every BP addressed by the study. In the survey, the representatives of organizations were asked to answer questions on the changes in KMP and BP in their organizations during a set period (3 years), according to criteria of organizational stability [80]. When a particular process was attributed to one managerial position, but most of the processes were managed by a person in another position (the actual process owner), the priority to answer the respective questions was given to the latter. The study was based on the main criteria of research, such as validity, reliability, objectivity, and representative sample. Validity was ensured by carefully choosing sampling criteria for organizations and respondents to be included in the study. Criteria of reliability were met by using ordinal data. Objectivity was attained by the selected research instrument (survey), where the researcher does not influence the process and results of the measurement. The representative sample size was calculated with the Paniotto formula, which gives probability-based calculations for the extrapolation of sample data to the general population. Analysis of empirical data was approached with the strategy of the sequential research design. Based on the conceptual model of KM’s influence on BP, the following aspects were identified: the key KM and BP, their components, evaluation indicators, and components of VA and its indicators. Theoretical analysis results were used to design the quantitative instrument—the survey questionnaire. The questionnaire aimed to identify the effect of each of the KMPs on BP through the defined metrics. Indicators for each metric were measured; then, all indicators were recalculated into the VA created in the organizations.

The sample of organizations was drawn from IT companies operating in Lithuania. According to the National Register Centre data for 2019, it received financial statements from 1940 companies whose activities, according to the Classification of Economic Activities (Lithuanian Statistics), were classified as IT activities. The National Register Centre divides the areas of activities, which are used to classify all IT companies operating in Lithuania into further 583 subareas. To represent the characteristics of IT companies, the research population did not include the following categories of companies:

- According to the area of activity, the research population did not include companies in which IT is only supportive, instead of direct, income-generating activity, such as audit, manufacturing, online retail trade, office and stationery supply, wholesale and retail sale of computer equipment and third-party software retail companies.

- According to the income size and number of employees, the population included small, medium, and large companies, constituting 98.3% of the Lithuanian IT market. Micro-enterprises were not included in the general population because of the assumption that these companies’ BP are little understood and are not being evaluated, while KMP is only supportive and not systematic.

By using these criteria, a list of 72 companies was compiled. Based on the assumption that in each company, owners of the three essential BP are at least two people in different positions, questionnaires were sent to 144 middle-level managers from the selected 72 IT companies. Thus, the general population of the research consisted of 144 managers (process owners) from 72 organizations.

To define the size of a representative sample, a minimum of 105 individuals were calculated, while the number of returned questionnaires was 108. The period of data collection was from January to July 2020.

4. Results

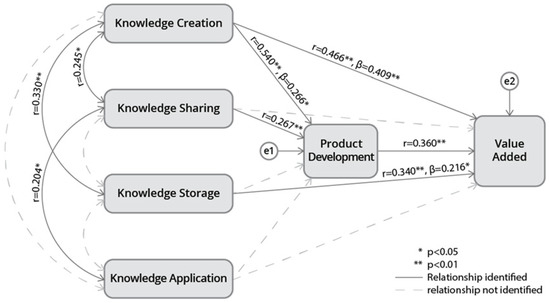

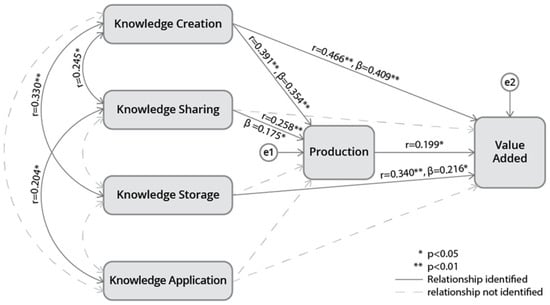

Calculation of correlation coefficients showed that relationships between the quality of the overall KMP and BP (Figure 3, Figure 4 and Figure 5)—processes of product development (r = 0.425; p < 0.001), production (r = 0.325; p = 0.001) and sales (r = 0.325; p = 0.001)—are statistically significant.

Figure 3.

Structural model: KMP, product development process, and VA (created by the authors).

Figure 4.

Structural model: KMP, production process, and VA (created by the authors).

Figure 5.

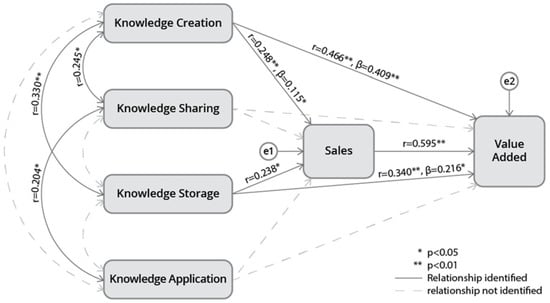

Structural model: KMP, product sales process, and VA (created by the authors).

The analysis also confirmed the statistical significance of positive correlations between individual KMP and BP. A higher evaluation of knowledge creation was related to a higher evaluation of product development (Figure 3), production, and sales (r = 0.540, p < 0.001; r = 0.391, p < 0.001; r = 0.248, p = 0.01). Knowledge sharing was related to product development (Figure 3) (r = 0.267; p < 0.01) and production (Figure 4) (r = 0.258, p < 0.01), from knowledge storage to sales (Figure 5) (r = 0.238; p < 0.05).

In the regression model, which was constructed to evaluate the influence of KMP on product development, the dependent variable is the score for product development; independent variables are the aspects of KMP, which were shown to be statistically significantly correlated with the dependent variable. Calculations with AMOS software helped to produce a regression equation, which includes only one statistically significant (p < 0.001) variable—the process of knowledge creation. Calculations with a non-standardized coefficient showed that an increase in the score for knowledge creation by one would increase the predicted product development score by 0.266 points (Figure 3). The obtained coefficient of determination R2 = 0.285. According to Cohen [81], an R2 value of 0.12 or lower indicates a small effect, a value between 0.13 and 0.25 is a medium size effect, while a value of 0.25 and higher is a strong effect.

In the regression model, designed to evaluate the effect of KMP on the process of production, the dependent variable is the score for the production process; independent variables are the aspects of KMP, which showed to be statistically significantly correlated with the dependent variable. The regression equation includes two statistically significant (p < 0.05) variables: knowledge creation and knowledge sharing processes. Calculations with a non-standardized coefficient showed that an increase in the score for knowledge creation by one would increase the predicted production score by 0.217 points (Figure 4) and the knowledge sharing score by 0.118 points. The obtained coefficient of determination R2 = 0.156, which means that taken together, the scores for knowledge creation and knowledge sharing explain about 15.6% of the distribution of scores for production. With standardized coefficients, the effect of knowledge creation is larger than that of knowledge sharing (β = 0.354 > β = 0.175).

In the regression model, designed to evaluate the effect of KMP on the process of sales, the dependent variable is the score for the sales; independent variables are the aspects of KMP, which showed to be statistically significantly correlated with the dependent variable. The regression equation includes one statistically significant (p < 0.05) variable—the knowledge creation process. Calculations with a non-standardized coefficient showed that an increase in the scale for knowledge creation by one would increase the predicted sales score by 0.115 points (Figure 5). The obtained coefficient of determination R2 = 0.098, meaning that the score for knowledge creation explains about 9.8% of the distribution of sales scores.

In the regression model, designed to evaluate the effect of KMP on the essential BP, the dependent variable is the score for the key BP; independent variables are the aspects of KMP. The regression equation includes one statistically significant (p < 0.05) variable—the knowledge creation process. Calculations with a non-standardized coefficient showed that increasing the scale for knowledge creation by one would increase the predicted score for BP by 0.208 points. The obtained coefficient of determination R2 = 0.267, which means that the forecast equation explains about 26.7 percent of the distribution of the critical BP.

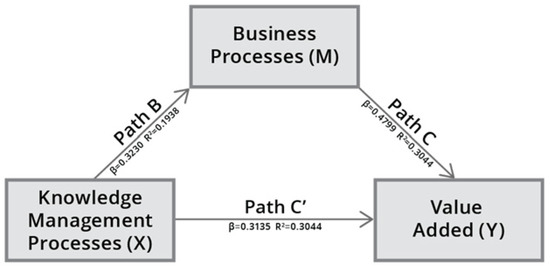

The Relationship between KMP and VA through a Mediating Variable—The Key BP

To establish if BP act as mediators between KMP and the VA indicators, PROCESS mediation analysis was used to construct three regression models. The first path (A, depicted in Figure 6) assesses the influence of KMP on the VA.

Figure 6.

A direct influence of KMP on the VA (created by the authors).

The second path (B) indicates the influence of KMP on BP, and the third path (C) is the influence of KMP and the key BP on the VA.

The calculated coefficients indicate that all relationships are statistically significant: between KMP and VA (p < 0.001), between KMP and the key BP (p < 0.001), and between KMP and the VA (p < 0.001). Determination coefficients R2 indicate that KMP explains about 20.9% of the distribution of the scores for VA Scores for KMP, together with the scores for BP, explaining about 30.4% of the distribution of the scores for VA (Figure 7). Thus, the VA model that includes the mediating variable is more informative. Results of the Sobel test show that the effect of the mediating variable (BP) is statistically significant (p < 0.001). KMP has both a direct and indirect effect (through the mediating variable) on the VA; therefore, we can conclude that it is a case of partial mediation.

Figure 7.

The influence of KMP on the VA through the mediating variable (BP) (created by the authors).

K means cluster analysis showed that, according to the KMP, the companies included in the survey could be divided into two groups. Here, we present two clusters since, in these cases, the obtained results are worthy of closer analysis. The first group represents companies with rather high average scores for knowledge creation, sharing, and storage but lower scores for knowledge application. On the contrary, knowledge application received higher scores in the companies of the second group, while the other three processes were evaluated with lower scores.

Analysis indicates statistically significant differences between the processes of product development and sales, the overall score for the BP, non-financial indicators of VA, and the overall VA. In all companies of the first group, these indicators are higher (p < 0.05). Companies with less than 205 employees are likelier to be in the second group.

Hypothesis testing

Hypothesis (H1):

Every KMP separately has a positive effect on individual BP: confirmed (knowledge creation was found to have the most significant impact).

Hypothesis (H2):

Every KMP has a positive effect on the VA created in an organization: confirmed, partially since knowledge sharing and knowledge creation have a strong influence. However, no statistically significant coefficients were used to prove the relationship between knowledge storage, knowledge application, and VA.

Hypothesis (H3):

KMP as a whole have a positive effect on the main BP: confirmed.

Hypothesis (H4):

Change (improvement) of BP increase VA created in organizations: confirmed.

Hypothesis (H5):

BP acts as a mediator of the positive correlation between KMP and the VA: confirmed.

Hypothesis (H6):

Effectiveness of individual KMP depend on the size of the organization: confirmed.

5. Discussion and Conclusions

The presented theoretical analysis showed that KMPs were related to almost all organizational activities and were significantly associated with many organizational processes. Therefore, a theoretical assumption was made that KMP should be evaluated concerning BP, while methods applicable for improving BP were also relevant to KMP.

In other scientific studies, there is a lack of systematic analysis and scientifically based answers to which KMP is the most important for effective and efficient organizational performance. The conceptual model facilitates the assessment of the impact of KMP on the critical BP individually or as the whole cycle for creating VA.

The authors’ systematic analysis of KMP made it possible to distinguish the four most crucial KMP: knowledge creation, sharing, storage, and application. The broad set of organizational processes, lack of a process-oriented approach, and various combinations of indicators did not allow the application of universal methodologies to evaluate, measure, and improve BP and their connections with KM practices. Using the comparative analysis of the iteration, the authors highlighted key BP characteristics of product development, production, and sales. Six essential dimensions were distinguished for evaluating each process: quality, time, costs, financial indicators, productivity, and efficiency.

An empirical study showed that the critical KMP functioned together as one system in IT organizations:

- Correlational analysis showed that KMP positively affected the essential BP; the knowledge creation process positively affected product development, production, and sales processes. Knowledge sharing had a weaker effect on product development and production processes.

- Multiple regression analysis showed that KMP as a whole KM cycle positively affected the VA created in knowledge-intensive organizations by the critical BP.

- Mediation analysis confirmed that KMP had a more substantial effect on the VA when they were integrated into other BP.

- VA was most strongly affected by two of the analyzed KMP: knowledge creation and knowledge sharing.

- Analysis of the effects of KMP on VA in IT organizations of different sizes and grouping them into clusters demonstrated that middle and small-sized organizations focused more on knowledge creation, sharing, and storage. In contrast, large organizations paid more attention to knowledge application.

The results of the empirical study confirmed the practical relevance of the conceptual model of the influence of KMP on BP. The model could be applied to improve separate KMP, improve the critical BP’s effectiveness, and thus increase the financial and non-financial VA created in knowledge-intensive organizations.

KMP had positive relationships with many organizational process dimensions. It had the most substantial relationship with the product development process’s quality, time, and cost dimensions. Product manufacturing dimensions such as quality, resources, and delivery had direct connections with KMP, and the most important relationships of the product sales process were determined for the dimensions of financial results and process efficiency.

The main study limitations were related to a specific set of KMP, and BP linked to knowledge-intensive industries in a particular geographical area and sector. The first limitation of this study was connected with one specific combination of KMP focused only on four KMP (knowledge creation, storage, sharing, and application) and BP (development, production, sales) to the knowledge-intensive industry where different business sectors and organizations can underline other necessary combinations of KMP and BP. The second limitation was related to the Lithuanian IT sector since the survey was conducted in the Lithuanian IT sector, limiting the generalization of the results. Future research directions could explore different business sectors with a common economic, social and cultural background in other geographical regions, for instance, Baltic countries. Another future research direction could be applying the research methodology in project-based organizations that use a process-based management approach and improving the measurement of KMP. It should be performed not only through indicators of organizational processes but also by applying other mediators. Expansion in this field of research could be achieved by measuring the impact not only on KMP but also on additional KM activities. Measurement of KM and organizational indicators should be based more on objective values, and the obtained values should be checked using the triangulation method.

Author Contributions

Conceptualization, Z.O.A., J.G. and J.R.; methodology, Z.O.A., J.G. and J.R.; software and validation, J.G.; formal analysis and investigation, J.G.; resources, J.G. and J.R.; data curation J.G.; writing—original draft preparation, Z.O.A., J.G. and J.R.; writing—review and editing Z.O.A., J.G. and J.R.; visualization, J.G.; supervision, J.R.; funding acquisition, J.R. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data of this study are available from the authors upon request.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Dima, A.; Bugheanu, A.-M.; Dinulescu, R.; Potcovaru, A.-M.; Stefanescu, C.A.; Marin, I. Exploring the research regarding frugal innovation and business sustainability through bibliometric analysis. Sustainability 2022, 14, 1326. [Google Scholar] [CrossRef]

- Kragulj, F. Knowledge Management and Sustainable Value Creation: Needs as a Strategic Focus for Organizations; Springer: Berlin/Heidelberg, Germany, 2022. [Google Scholar]

- Popescu, D.V.; Dima, A.; Radu, E.; Dobrota, E.M.; Dumitrache, V.M. Bibliometric analysis of the green deal policies in the food chain. Amfiteatru Econ. 2022, 24, 411. [Google Scholar] [CrossRef]

- Davidavičienė, V.; Raudeliūnienė, J. Corporate social entrepreneurship practice: Lithuanian case analysis. J. Syst. Manag. Sci. 2021, 11, 218–231. [Google Scholar] [CrossRef]

- Davidavičienė, V.; Raudeliūnienė, J. Corporate social entrepreneurship practice: Lithuanian case study in public and private organizations. J. Syst. Manag. Sci. 2022, 12, 548–569. [Google Scholar] [CrossRef]

- Kordab, M.; Raudeliūnienė, J.; Meidutė-Kavaliauskienė, I. Mediating role of knowledge management in the relationship between organizational learning and sustainable organizational performance. Sustainability 2020, 12, 10061. [Google Scholar] [CrossRef]

- Raudeliuniene, J.; Matar, I. Knowledge management practice for sustainable development in higher education institutions: Women managers’ perspective. Sustainability 2022, 14, 12311. [Google Scholar] [CrossRef]

- Raudeliuniene, J.; Albats, E.; Kordab, M. Impact of information technologies and social networks on knowledge management processes in Middle Eastern audit and consulting companies. J. Knowl. Manag. 2021, 25, 871–898. [Google Scholar] [CrossRef]

- Raudeliūnienė, J. Topicalities of the Organization’s Knowledge Potential Assessment; Technika: Vilnius, Lithuania, 2017; (In Lithuanian). [Google Scholar] [CrossRef]

- Martins, V.W.B.; Rampasso, I.S.; Anholon, R.; Quelhas, O.L.G.; Leal Filho, W. Knowledge management in the context of sustainability: Literature review and opportunities for future research. J. Clean. Prod. 2019, 229, 489–500. [Google Scholar] [CrossRef]

- Raudeliūnienė, J.; Tvaronavičienė, M.; Blažytė, M. Knowledge management practice in general education schools as a tool for sustainable development. Sustainability 2020, 12, 4034. [Google Scholar] [CrossRef]

- Evans, S.; Fernando, L.; Yang, M. Sustainable value creation—from concept towards implementation. In Sustainable Manufacturing. Sustainable Production, Life Cycle Engineering and Management; Stark, R., Seliger, G., Bonvoisin, J., Eds.; Springer: Cham, Switzerland, 2017; pp. 203–220. [Google Scholar] [CrossRef]

- Centobelli, P.; Cerchione, R.; Esposito, E. Efficiency and effectiveness of knowledge management systems in SMEs. Prod. Plan. Control. 2019, 30, 779–791. [Google Scholar] [CrossRef]

- Hegazy, F.; Ghorab, K. The effect of knowledge management processes on organizational business processes’ and employees’ benefits in an academic institution’s portal environment. Commun. IBIMA 2015, 2015, 928262. [Google Scholar] [CrossRef]

- Knowledge management as a strategic asset for customer service delivery at a contact centre in South Africa. Knowl. Manag. E-Learn. Int. J. 2021, 13, 225–249. [CrossRef]

- Bolisani, E.; Bratianu, C. Knowledge strategy planning: An integrated approach to manage uncertainty, turbulence, and dynamics. J. Knowl. Manag. 2017, 21, 233–253. [Google Scholar] [CrossRef]

- Klingenberg, B.; Rothberg, H.N. The status quo of knowledge management and sustainability knowledge. Electron. J. Knowl. Manag. 2020, 18, 136–148. [Google Scholar] [CrossRef]

- Akram, M.S.; Goraya, M.A.S.; Malik, A.; Aljarallah, A.M. Organizational performance and sustainability: Exploring the roles of IT capabilities and knowledge management capabilities. Sustainability 2018, 10, 3816. [Google Scholar] [CrossRef]

- Zack, M.; McKeen, J.; Singh, S. Knowledge management and organizational performance: An exploratory analysis. J. Knowl. Manag. 2009, 13, 392–409. [Google Scholar] [CrossRef]

- Raudeliūnienė, J.; Davidavičienė, V.; Jakubavičius, A. Knowledge management process model. Entrep. Sustain. Issues 2018, 5, 542–554. [Google Scholar] [CrossRef]

- Zaim, H.; Muhammed, S.; Tarim, M. Relationship between knowledge management processes and performance: Critical role of knowledge utilization in organizations. Knowl. Manag. Res. Pract. 2019, 17, 24–38. [Google Scholar] [CrossRef]

- Cegarra-Navarro, J.-G.; Soto-Acosta, P.; Wensley, A.K. Structured knowledge processes and firm performance: The role of organizational agility. J. Bus. Res. 2016, 69, 1544–1549. [Google Scholar] [CrossRef]

- Soto-Acosta, P.; Cegarra-Navarro, J.-G. New ICTs for knowledge management in organizations. J. Knowl. Manag. 2016, 20, 417–422. [Google Scholar] [CrossRef]

- Khanal, L.; Paudyal, S.R. Effect of knowledge management practices on the performance of Nepalese financial institutions. J. Adv. Acad. Res. 2018, 4, 44–59. [Google Scholar] [CrossRef]

- Handzic, M.; Durmic, N. Knowledge management, intellectual capital and project management: Connecting the dots. Electron. J. Knowl. Manag. 2015, 13, 51–61. [Google Scholar]

- Kun, M. Linkages between knowledge management process and corporate sustainable performance of Chinese small and medium enterprises: Mediating role of frugal innovation. Front. Psychol. 2022, 13, 850820. [Google Scholar] [CrossRef] [PubMed]

- Tajpour, M.; Hosseini, E.; Mohammadi, M.; Bahman-Zangi, B. The effect of knowledge management on the sustainability of technology-driven businesses in emerging markets: The mediating role of social media. Sustainability 2022, 14, 8602. [Google Scholar] [CrossRef]

- Hossain, B.; Nassar, S.; Rahman, M.U.; Dunay, A.; Illés, C.B. Exploring the mediating role of knowledge management practices to corporate sustainability. J. Clean. Prod. 2022, 374, 133869. [Google Scholar] [CrossRef]

- Irani, M.A.; Ghazali, M.Z.M.; Osman, H.M. Incorporating knowledge sharing as a sustainable competitive advantage with business processes. GATR Glob. J. Bus. Soc. Sci. Rev. 2013, 3, 41–53. [Google Scholar] [CrossRef] [PubMed]

- Zelt, S.; Recker, J.; Schmiedel, T.; Brocke, J.V. A theory of contingent business process management. Bus. Process. Manag. J. 2018, 25, 1291–1316. [Google Scholar] [CrossRef]

- Kneipp, J.M.; Gomes, C.M.; Bichueti, R.S.; Frizzo, K.; Perlin, A.P. Sustainable innovation practices and their relationship with the performance of industrial companies. Rev. Gestão 2019, 26, 94–111. [Google Scholar] [CrossRef]

- Frizzo, K.; Kneipp, J.M.; Gomes, C.M.; Jardón, C.M.F.; Bichueti, R.S. The strategic management of sustainable innovation and its relation to business models and corporate performance. Int. J. Innov. Sustain. Dev. 2020, 14, 397. [Google Scholar] [CrossRef]

- Raudeliūnienė, J.; Szarucki, M. An integrated approach to assessing an organization’s knowledge potential. Eng. Econ. 2019, 30, 69–80. [Google Scholar] [CrossRef]

- Shahzad, M.; Qu, Y.; Zafar, A.U.; Appolloni, A. Does the interaction between the knowledge management process and sustainable development practices boost corporate green innovation? Bus. Strat. Environ. 2021, 30, 4206–4222. [Google Scholar] [CrossRef]

- Tubigi, M.; Alshawi, S. The impact of knowledge management processes on organisational performance: The case of the airline industry. J. Enterp. Inf. Manag. 2015, 28, 167–185. [Google Scholar] [CrossRef]

- Weina, A.; Yanling, Y. Role of knowledge management on the sustainable environment: Assessing the moderating effect of innovative culture. Front. Psychol. 2022, 13, 861813. [Google Scholar] [CrossRef] [PubMed]

- Iazzolino, G.; Laise, D.; Migliano, G. Measuring value creation: VAIC and EVA. Meas. Bus. Excel. 2014, 18, 8–21. [Google Scholar] [CrossRef]

- Mousavizadeh, M.; Ryan, S.; Harden, G.; Windsor, J. Knowledge management and the creation of business value. J. Comput. Inf. Syst. 2015, 55, 35–45. [Google Scholar] [CrossRef]

- Foote, A.; Halawi, L.A. Knowledge management models within information technology projects. J. Comput. Inf. Syst. 2018, 58, 89–97. [Google Scholar] [CrossRef]

- Martelo-Landroguez, S.; Martin-Ruiz, D. Managing knowledge to create customer service value. J. Serv. Theory Pract. 2016, 26, 471–496. [Google Scholar] [CrossRef]

- Lee, K.C.; Lee, S.; Kang, I.W. KMPI: Measuring knowledge management performance. Inf. Manag. 2005, 42, 469–482. [Google Scholar] [CrossRef]

- Chang, C.L.-H.; Lin, T.-C. The role of organizational culture in the knowledge management process. J. Knowl. Manag. 2015, 19, 433–455. [Google Scholar] [CrossRef]

- Al-Qarioti, M.Q.A. The impact of knowledge management on organizational performance: An empirical study of Kuwait University. Eurasian J. Bus. Manag. 2015, 3, 36–54. [Google Scholar] [CrossRef]

- Alrubaiee, L.; Alzubi, H.M.; Hanandeh, R.; Ali, R.A. Investigating the relationship between knowledge management processes and organizational performance the mediating effect of organizational innovation. Int. Rev. Manag. Bus. Res. 2015, 4, 989–1009. [Google Scholar]

- Heisig, P.; Suraj, O.A.; Kianto, A.; Kemboi, C.; Arrau, G.P.; Easa, N.F. Knowledge management and business performance: Global experts’ views on future research needs. J. Knowl. Manag. 2016, 20, 1169–1198. [Google Scholar] [CrossRef]

- Novak, A. Knowledge management and organizational performance—Literature review. Management Challenges in a Network Economy. In Proceedings of the MakeLearn and TIIM International Conference 2017, Lublin, Poland, 17–19 May 2017; pp. 433–440. [Google Scholar]

- Abdi, K.; Mardani, A.; Senin, A.A.; Tupenaite, L.; Naimaviciene, J.; Kanapeckiene, L.; Kutut, V. The effect of knowledge management, organizational culture and organizational learning on innovation in automotive industry. J. Bus. Econ. Manag. 2018, 19, 1–19. [Google Scholar] [CrossRef]

- Abuaddous, H.Y.; al Sokkar, A.A.M.; Abualodous, B.I. The impact of knowledge management on organizational performance. Int. J. Adv. Comput. Sci. Appl. 2018, 9, 204–208. [Google Scholar] [CrossRef]

- Oufkir, L.; Kassou, I. Performance measurement for knowledge management project: Model development and empirical validation. J. Knowl. Manag. 2019, 23, 1403–1428. [Google Scholar] [CrossRef]

- Arora, R. Implementing KM—A balanced score card approach. J. Knowl. Manag. 2002, 6, 240–249. [Google Scholar] [CrossRef]

- Shannak, R.O. Measuring knowledge management performance. Eur. J. Sci. Res. 2009, 35, 242–253. [Google Scholar]

- Kuah, C.T.; Wong, K.Y.; Wong, W.P. Monte Carlo data envelopment analysis with genetic algorithm for knowledge management performance measurement. Expert Syst. Appl. 2012, 39, 9348–9358. [Google Scholar] [CrossRef]

- Chen, M.-Y.; Chen, A.-P. Integrating option model and knowledge management performance measures: An empirical study. J. Inf. Sci. 2005, 31, 381–393. [Google Scholar] [CrossRef]

- Rose, T.J. Sustained Growth in Small Enterprises: A Process Management Approach. Ph.D. Thesis, Cranfield University, Cranfield, UK, 2003. [Google Scholar]

- Moen, R.; Norman, C. Evolution of the PDCA Cycle. In Proceedings of the 7th ANQ Congress, Tokyo, Japan, 17 September 2009; pp. 1–11. [Google Scholar]

- Sobotkiewicz, D. Processes in multiple economic entities. Management 2015, 19, 19–32. [Google Scholar] [CrossRef]

- Moldagulova, A.; Satybaldiyeva, R.; Uskenbayeva, R.; Kassymova, A.; Kalpeyeva, Z. Architecture development for certain classes of university business processes. In Proceedings of the 2020 IEEE 22nd Conference on Business Informatics, CBI 2020, Antwerp, Belgium, 22–24 June 2020; Volume 2, pp. 91–95. [Google Scholar] [CrossRef]

- Strazdas, R.; Černevičiūtė, J.; Jančoras, Ž. Kūrybinio verslo valdymas: Procesų tobulinimas; VU Tarptautinio Verslo Mokykla: Vilnius, Lithuania, 2014. [Google Scholar]

- APQC (American Productivity & Quality Center). 3.0 Market and Sell Products and Services Definitions and Key Measures PCF Version 6.0.0. Available online: https://www.apqc.org/resource-library/resource-listing/30-market-and-sell-products-and-services-definitions-and-key (accessed on 13 December 2022).

- van Rensburg, A. A Framework for business process management. Comput. Ind. Eng. 1998, 35, 217–220. [Google Scholar] [CrossRef]

- Laitamäki, J.; Kordupleski, R. Building and deploying profitable growth strategies based on the waterfall of customer value added. Eur. Manag. J. 1997, 15, 158–166. [Google Scholar] [CrossRef]

- Gaiardelli, P.; Saccani, N.; Songini, L. Performance measurement systems in after-sales service: An integrated framework. Int. J. Bus. Perform. Manag. 2007, 9, 145. [Google Scholar] [CrossRef]

- Ittner, C.D.; Larcker, D.F.; Rajan, M.V. The choice of performance measures in annual bonus contracts. Account. Rev. 1997, 72, 231–255. [Google Scholar]

- Ahmed, S.; Fiaz, M.; Shoaib, M. Impact of knowledge management practices on organizational performance: An empirical study of banking sector in Pakistan. FWU J. Soc. Sci. 2015, 9, 147–167. [Google Scholar]

- Liao, S.-H.; Wu, C.-C. The Relationship among knowledge management, organizational learning, and organizational performance. Int. J. Bus. Manag. 2009, 4, 64. [Google Scholar] [CrossRef]

- Tanriverdi, H. Information technology relatedness, knowledge management capability, and performance of multibusiness firms. MIS Q. 2005, 29, 311. [Google Scholar] [CrossRef]

- Vaccaro, A.; Parente, R.; Veloso, F.M. Knowledge management tools, inter-organizational relationships, innovation and firm performance. Technol. Forecast. Soc. Chang. 2010, 77, 1076–1089. [Google Scholar] [CrossRef]

- Vidovi, M. The link between the quality of knowledge management and financial performance—The case of Croatia. Probl. Perspect. Manag. 2010, 8, 159–169. [Google Scholar]

- Zack, E.; Barr, R. The role of interactional quality in learning from touch screens during infancy: Context matters. Front. Psychol. 2016, 7, 1264. [Google Scholar] [CrossRef]

- Starns, J.; Odom, C. Using knowledge management principles to solve organizational performance problems. VINE 2006, 36, 186–198. [Google Scholar] [CrossRef]

- Wu, I.-L.; Chen, J.-L. Knowledge management driven firm performance: The roles of business process capabilities and organizational learning. J. Knowl. Manag. 2014, 18, 1141–1164. [Google Scholar] [CrossRef]

- Rehman, W.U.; Asghar, N.; Ahmad, K. Impact of KM practices on firms’ performance: A mediating role of business process capability and organizational learning. Pak. Econ. Soc. Rev. 2015, 53, 47–80. [Google Scholar]

- Easterby-Smith, M.; Prieto, I.M. Dynamic capabilities and knowledge management: An integrative role for learning? Br. J. Manag. 2008, 19, 235–249. [Google Scholar] [CrossRef]

- Brunswicker, S.; Vanhaverbeke, W. Open innovation in small and medium-sized enterprises (SMEs): External knowledge sourcing strategies and internal organizational facilitators. J. Small Bus. Manag. 2015, 53, 1241–1263. [Google Scholar] [CrossRef]

- Salunke, S.; Weerawardena, J.; McColl-Kennedy, J.R. The central role of knowledge integration capability in service innovation-based competitive strategy. Ind. Mark. Manag. 2019, 76, 144–156. [Google Scholar] [CrossRef]

- Iqbal, A.; Latif, F.; Marimon, F.; Sahibzada, U.F.; Hussain, S. From knowledge management to organizational performance. J. Enterp. Inf. Manag. 2019, 32, 36–59. [Google Scholar] [CrossRef]

- Al Ahbabi, S.A.; Singh, S.K.; Balasubramanian, S.; Gaur, S.S. Employee perception of impact of knowledge management processes on public sector performance. J. Knowl. Manag. 2019, 23, 351–373. [Google Scholar] [CrossRef]

- Paschen, J.; Wilson, M.; Ferreira, J.J. Collaborative intelligence: How human and artificial intelligence create value along the B2B sales funnel. Bus. Horiz. 2020, 63, 403–414. [Google Scholar] [CrossRef]

- Teo, T. Handbook of Quantitative Methods for Educational Research; Springer: Berlin/Heidelberg, Germany, 2013; pp. 1–404. [Google Scholar] [CrossRef]

- Langley, A.; Smallman, C.; Tsoukas, H.; Van de Ven, A.H. Process studies of change in organization and management: Unveiling temporality, activity, and flow. Acad. Manag. J. 2017, 56, 1–13. [Google Scholar] [CrossRef]

- Cohen, J. Statistical power analysis. Curr. Dir. Psychol. Sci. 1992, 1, 98–101. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).