1. Introduction

The aggravation of global environmental problems make relevant the issue of preserving the natural environment and reducing harmful anthropogenic impacts. This leads to the constant diversification and improvement of environmental policy instruments at the national and international levels. Nowadays, the environmental context accompanies the making of political decisions in any sphere and should be considered in the process of strategic planning for state and interstate development [

1].

Modern contexts of scientific research testify that the issue of sustainable development is closely related to energy security and renewable energy [

2]. At the same time, ensuring energy efficiency becomes important, which leads not only to economic but also to environmental benefits [

3]. Energy efficiency is a complex process that is characterized not only by the features of energy production but also by the volume and structure of its consumption [

4]. The implementation of high tech in the infrastructure network also makes an important contribution to increasing resource efficiency [

5]. Thus, the integration of smart networks into economic activity has a positive effect on economic results, creates additional comfort benefits and reduces the irrational use of resources [

6]. Recent events in the world have proven that energy security is among the most important guarantees of economic security. That is why the formation of a national policy in the field of energy and environmental protection should consider the priorities of energy security [

7].

In modern conditions, ensuring sustainable development is carried out not only by producers but also by consumers. Thus, the development of a circular and sharing economy determines a reduction in the volume of product consumption, the generation of waste and a reduction in ecological footprints [

8]. At the same time, the change in the level of consumers’ environmental consciousness is correspondingly reflected in the structure of production and the implementation of environmentally safe technologies, the production of environmentally safe products, etc. At the same time, the role of civil society organizations and the unification of the initiatives of various groups of economic agents are growing. It has been proven that collective actions can ensure the maximum progress of sustainable development [

9].

The psychology of the behaviour of economic agents is characterized by the influence of many factors that collectively determine changes and the peculiarities of decision-making [

10]. It was determined that social interaction is an important factor in the development and implementation of business strategies [

11]. This determines the need to find the most effective regulatory initiatives that will stimulate economic entities to increase environmental responsibility. Particularly, one of the modern manifestations of the implementation of the concept of corporate social responsibility is reducing the level of environmental pollution [

12]. In this case, the additional benefit of the company is the formation of brand value, as well as gaining the trust of consumers with a high level of environmental awareness.

Studies of national and supranational policies to ensure the progress of sustainable development show that at the current stage, their effectiveness remains heterogeneous. So even in the countries of the European Union, there are quite significant gaps in the progress of implementing a circular economy [

13]. This indicates the importance of finding the most effective regulatory initiatives that can become the basis for their comprehensive implementation. At the same time, the initial historical and cultural features of the country’s development require the development of measures that factor in national specifics; only in this way will they be most effective [

14].

Analysing promising ways to ensure the progress of sustainable development, we note that at the moment, it is important to take into account not only the complexity of the achieved effects but also their positive synergy. This requires a study of the interrelationships between the various components of sustainable development to determine the key points of ensuring synergistic effects. Thus, the close connection between energy consumption and economic growth [

15], which cannot be ignored in the process of energy efficiency policy planning, has been repeatedly confirmed. At the same time, ecological and economic relations are usually reversed, such as trade in quotas for environmental pollution [

16,

17].

On the other hand, modern tools for ensuring economic development are increasingly becoming ecologically oriented. So green investments, which are becoming more and more popular, have positive consequences for both ecology and energy [

18]. At the same time, innovative development provides not only economic competitiveness but also energy efficiency for industrial enterprises [

19]. The energy-efficient transformation of the economy in the long run ensures not only economic but also social progress. Thus, reducing the level of environmental pollution in the process of energy production and consumption and reducing the number of human-caused disasters ultimately have positive effects on the health of populations [

20,

21].

Even though the priority of sustainable development tasks is certainly recognized by the international community, one of the main obstacles to their achievement is the potential reduction of economic benefits. Thus, the shortage of economic resources and their high cost restrain the development of renewable energy [

22,

23]. At the same time, it has been proven that the strategic technical re-equipment of enterprises with resource-saving technologies provides long-term economic benefits [

24,

25,

26].

All this proves that modern regulatory tools can simultaneously provide an impact on reducing environmental pollution, on increasing energy efficiency and safety and on increasing long-term economic growth. In this context, the significance of environmental taxes is growing, which, on the one hand, have regulatory effectiveness and, on the other hand, ensure the redistribution of financial resources. At the same time, as practice shows, environmental taxes are not as important for generating budget revenues as, for example, labour is or corporate income taxes are. That is why the assessment of the effectiveness of environmental taxes should be based on their regulatory function. Thus, environmental taxes can be aimed at reducing the level of environmental pollution and at increasing the level of rational use of natural resources. These taxes also play an important role in the energy sector, creating incentives for both the production and use of green energy. In the direction of economic development, environmental taxes create additional incentives for transforming the structure of production. The generalization of the main directions of influence on environmental taxes allowed for integrating them into a single vector for ensuring national security, which is measured by three components: environmental, economic and energy security.

The results of previous studies [

27,

28] have proved that the total income from environmental taxes as a parameter of the intensity of their use has a stable effect on ensuring national security. However, the indicator of revenues from environmental taxes does not fully reflect their regulatory effectiveness, given that the definition of the tax base for environmental taxes affects the decisions of the payers of these taxes to abandon environmentally harmful or energy-inefficient activities or to change the materials, technological processes or entities that are the reason for paying environmental taxes. That is why it is of great interest to determine the most effective modifications for environmental taxes that increase the intensity of their impact on the specified goals.

Transport taxes were chosen as the object of the study because the practice of their establishment proves that the combination of different criteria affect various aspects of environmental, economic and energy security. In particular, measuring the impact of cars on the environment uses such parameters as the level of emissions, engine volume and age of the car. The practice of establishing transport tax differentiation by the type of fuel aimed at the increase of their impact on energy security, as it determines the propensity to purchase cars that use green fuel. The use of transport taxes based on the principle of a car’s value is a classic example of fiscal environmental taxes.

The main purpose of the study is to determine the optimal criteria for setting transport taxes, not in the context of achieving some specific goals of the state (obtaining additional revenues for the budget, reducing the circulation of old cars, encouraging the purchase of transport taxes, etc.) but rather comprehensively in the frame of maximizing the transport tax contribution to the provision of environmental, economic and energy security. The research is built in the following sequence: the identification of common approaches for setting transport taxes, the formalization of research data summarizing common parameters to setting transport taxes, the justification of mathematical tools for evaluating the impact of the design of transport taxes on their effectiveness in ensuring national security, an assessment and interpreting the results.

The proposed study has no analogues in the scientific literature. Existing publications either have a theoretical conceptual nature [

29,

30], are related to the comparative assessment of different types of taxes affecting the use of transport [

31,

32] or are based on the study of the experience of one country [

33].

2. Materials and Methods

Environmental taxation has a wide range of regulatory influence directions. Thus, taxes on the emissions of polluting substances have a direct restrictive and compensatory effect, to a greater extent. At the same time, energy, transport taxes, packaging taxes, etc. can provide incentives for the transformation of the economy in the direction of increasing its environmental and energy efficiency while maintaining the pace of economic development. Summarizing the directions of the regulatory influence of environmental taxes allowed for singling out three target blocks, reflecting the results of their functioning. This forms a background of the hypothesis that the result of establishing environmental taxes is the national security for the country (

Figure 1).

The system of environmental taxation has significant differences across the world, which does not always make it possible to compare the specifics of the same environmental taxes. In the structure of environmental taxes, it is transport taxes that have wide variability in their applications in different countries. Vehicle registration taxes, road taxes, car import duties, vehicle sales taxes, etc. successfully function in different countries. Previous research has shown that the most diverse in terms of the installation of functional elements are taxes for the registration and use of vehicles. Therefore, this group of taxes was chosen for the simulation.

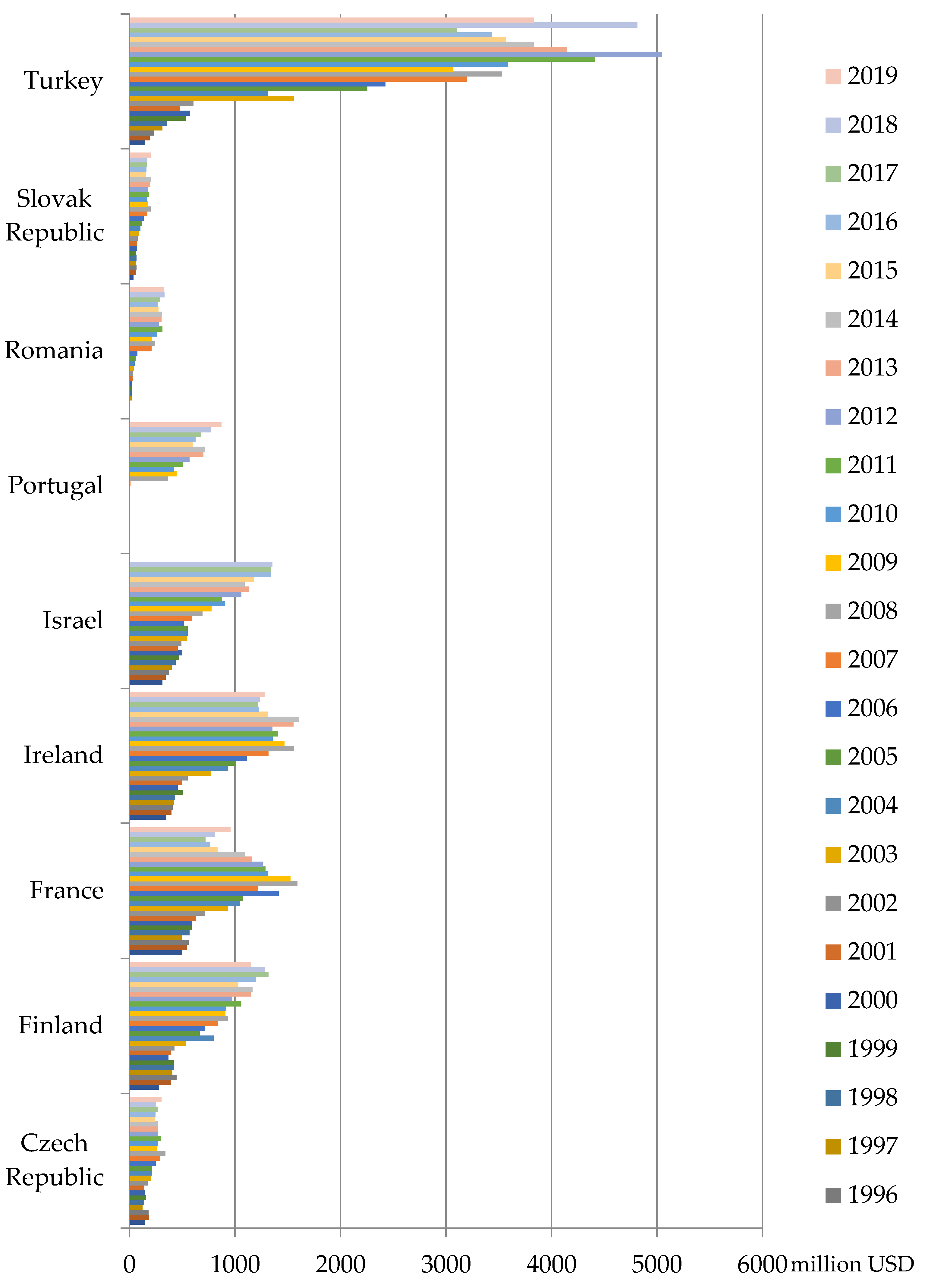

To form the research sample, it is necessary to provide a description of the main features of the functioning of these taxes in different countries. An analysis of environmental taxation systems and direct transport taxes made it possible to form a research sample from nine countries (i.e., the Czech Republic, Finland, France, Ireland, Israel, Portugal, Romania, Slovakia and Turkey). The conducted analysis of the design of transport taxes in different countries of the world proved that in these countries, different criteria for the taxation of transport taxes are used, and there are also common features of transport taxation. This makes it possible to build an economic-mathematical model that will consider the specifics of taxation in several countries at the same time and, consequently, to obtain broader conclusions about the effectiveness of transport taxes in ensuring national security. A general description of these taxes is presented in

Table 1.

The Czech Republic has established a road tax, the purpose of which is to tax the registration or use of vehicles. Tax rates are set in Czech crowns per year per vehicle and are differentiated according to two criteria: for passenger vehicles, the tax rate depends on the volume of the engine cylinders, and for other vehicles, it depends on the number of axles and the total weight of the vehicle. A similar practice of establishing a transport tax is observed in Slovakia. In Ireland, the transport tax is set in fixed amounts calculated per year, and its amount depends on such criteria as the type of vehicle, its weight and the volume of carbon dioxide emissions generated during the operation of the vehicle. In addition, Ireland has also established a tax for the first registration of a vehicle, the rates of which are set at a percentage of the market value of the vehicle, differentiated by the categories of cars. It is important that the minimum amount of this tax is also determined for each category.

Portugal also has fixed vehicle tax rates that vary by car type. The criteria for setting tax rates are the category of the vehicle, the type of fuel used and the volume of the engine cylinders.

On the other hand, the tax for the first registration of vehicles operating in Finland is also set differently for the two categories of vehicles. For motorcycles and buses, the rate is set as a percentage of the value of the vehicle, whereas for minibuses and cars, it depend on the generated emissions of harmful substances. In addition to this, Finland also uses a transport tax, which is charged per 100 kg of vehicle weight for each day of use of such a vehicle. Moreover, the rates that will be charged to vehicles are differentiated depending on the type of vehicle and on the type of fuel used by the vehicle.

The practice of applying a transport tax in France is quite interesting. The annual amount of the tax is calculated differently depending on the total volume of carbon dioxide emissions generated by the car. At the same time, for each category of car, the tax consists of two parts: a basic fixed amount and an amount calculated by multiplying the rate by 1 g of carbon dioxide emissions per 1 km (for example, for cars generating CO2 emissions in the amount of 141–160 g per kilometre, the basic amount is 290 euros, and the settlement amount is 11.5 euros per 1 g of CO2). Moreover, it is important that vehicles that generate less than 50 g of carbon dioxide emissions per kilometre not be taxed.

The practice of applying the transport tax in Israel also attracts attention. Fixed rates are set in national currency per year and are differentiated according to two criteria, namely the cost of a new car and its age, while tax rates are progressive relative to the value of the car and regressive relative to its age. In Turkey, the basis for the application of fixed tax rates is also the type and age of the vehicle, as well as, for certain categories, the volume of the engine cylinders.

In Romania, the annual vehicle tax differs for the three categories of vehicles: buses and minibuses, cars with an engine cylinder volume of up to 2000 cm3, and cars with an engine cylinder volume of more than 2000 cm3. Moreover, the tax amount is calculated by multiplying the established rate for every 500 cm3.

Thus, it was found that 6 (the Czech Republic, Finland, Portugal, Romania, Slovakia and Turkey) out of the 9 studied countries establish tax on vehicles according to the vehicle’s type. At the same time, the Czech Republic, Slovakia and Finland consider the weight of vehicles when setting transport taxes. Among the studied countries, only Finland, France and Israel do not differentiate transport taxes depending on the power of the vehicle’s engine. It is important that in Portugal the criterion for establishing transport taxes is the type of fuel, and in Finland, France and Ireland it is the level of CO2 emitted into the atmosphere. Turkey and Israel tax vehicles based on their age, and the value of the vehicle was a criterion found only in Israel. It was found that different criteria (both the cost and physical characteristics of the car) are used for taxation. For example, in France, differentiated transport tax rates depending on the amount of CO2 emissions show that the criterion of stimulating the environmental safety of cars is also important for the government. On the other hand, the establishment of different taxes rates depending on the volume of the engine cylinder, as well as on its age, not only can have a fiscal purpose (collecting additional revenues from the more expensive cars) but also can regulate the use of the most environmentally harmful cars. In addition, it is also interesting to investigate whether transport taxes that are established according to the principle of the value of the car perform any regulatory function.

For further calculations, it is important to form the most homogeneous sample of transport environmental taxes. That is why, in the further study of the two taxes operating in Finland, we will choose only the transport tax, leaving out the tax for the first registration of vehicles, and we will also not consider the tax for the first registration of a vehicle while studying environmental taxation in Ireland.

Given the wide spectrum of influence of environmental taxes on various aspects of ecological development, energy efficiency and environmental consequences, it is advisable to choose a single measure of the resulting parameters. Research in the field of national security proves that its measurement involves the construction of integral indicators that characterize individual aspects of national security depending on the goals of the analysis [

35].

To characterize the indicator of national security, we will use an integral indicator that summarizes the parameters of environmental, energy and economic security that are sensitive to the impact of environmental taxation. The method of calculating the defined integral indicator is presented in detail in [

27,

28].

Figure 2 presents the dynamics of the values of the calculated integral indicator for the studied sample of countries. As we can see, during the analysed period, the level of national security grew most dynamically in Finland, France, Portugal, Romania and Slovakia. The Czech Republic and Israel were characterized by moderate values of the indicator without sharp deviations during the year. On the other hand, it is important that the integral level of national security in Turkey has almost halved during the studied period. At the same time, it is important that during the studied period, the integral indicator of ecological, economic and energy security has a rather high level of volatility in almost all the studied countries. This indicates the fact that the latest trends in the development of national economies are characterized by significant transformations under the influence of political decisions, limited resources and the growth of public consciousness. However, given the heterogeneity of global development, it is of scientific interest to identify the reasons for such fluctuations in the levels of national security. This will allow for establishing vectors of the application of regulatory measures in countries across the world.

This paper proposes to study the influence of the specifics of the choice of functional elements of environmental transport taxes on the national security of a country with the help of regression modelling tools using dummy variables characterizing a certain feature of transport taxation. The choice of an approach to modelling with dummy variables is determined by the need to formalize the parameters of transport taxes in different countries in order to enter into the model notations regarding their application in the panel data sample. This approach allows for comparing the effectiveness of transport taxes applications in the countries that used a certain criterion for transport taxation with the countries that ignored such a criterion. The general appearance of the model is in Equation (1):

where

NSI is the resulting variable denoting the integral indicator of national security;

ETR is a factor variable denoting the amount of revenue from the payment of the investigated environmental tax in the country;

β1 is the coefficient that takes into account the influence of the factor variable amount of revenues from the environmental tax on the integral indicator of national security;

ETp is a dummy variable denoting the use in the country of a certain criterion for determining the tax base for an environmental transport tax, which takes the value 1 if the criterion is used and 0 if it is not used;

β2 is the coefficient that takes into account the effect of the dummy variable on the resulting characteristic; and

ε is the measurement and specification errors.

The main factor variable is the total annual amount of revenue from the investigated transport tax in each country. To ensure the proportionality of the statistical sample of data, the indicators of tax revenues are measured in millions USD.

Figure 3 shows the summary statistics of the revenues from the environmental tax for the registration/use of vehicles in the cross section of the studied countries.

The criteria for the formation of dummy variables characterizing the tax base with environmental taxes for the registration/use of vehicles in a country are the selected parameters of the specificity of taxation, revealed during the preliminary analysis.

Table 2 forms a matrix of dummy variables. The dummy variables measured as 1 characterize the application in the country of a certain criterion of environmental taxation, and those as 0 characterize its absence.

Therefore, this paper proposes to model the influence of the specificity of the establishment of the functional parameters of environmental taxes on national security by using the panel regression toolkit, which allows for the simultaneous assessment of the effects in terms of the general sample of countries. A model specification with panel-adjusted standard errors based on the use of the Durbin–Watson test was chosen for the calculations. The choice of the model specification was determined by the peculiarities in the input statistical data. At the beginning of the study, an OLS regression was built; however, the model-adequacy criteria turned out to be unsatisfactory. Given the selection of panel data for the evaluation, it was assumed that the input data would be characterized by the heteroscedasticity of the residuals, which would not allow the use of classical linear models. The conducted White’s test confirmed the heteroskedasticity in the input data. To eliminate this problem, the contemporaneous correlation model, namely the panel-adjusted standard errors, was chosen. The testing of various modifications of this model revealed that the most adequate was the model based on the Durbin–Watson criterion. The assessment involved the construction of separate models using dummy variables that characterized the application of each of the criteria for determining the tax base. Calculations were made for the period 1996–2019. The choice of research period was informed by the availability of a complete data set of transport tax revenues and by indicators of national security factored into the model.

,

,

{kind=link}

{kind=link}

{kind=link}