1. Introduction

As the extent to which corporates benefit or harm social welfare, Corporate Social Responsibility (CSR) refers broadly to conducting social or environmental behaviors beyond compliance with the law and beyond economic profitability maximization [

1]. Given its various potential benefits on corporate value [

2], innovation [

3], reputational risks [

4] and other business activities, an increasing number of enterprises/institutional investors have gradually incorporated CSR into their mainstream business strategy and investment decisions [

5], and how to effectively strengthen the willingness or impetus of firms to engage in CSR has aroused heated debate among scholars, business ethicists and regulators [

6].

Prior literature has discussed the various factors affecting CSR from the perspectives of both internal and external drivers. The internal driver perspective focuses on variables pertaining to enterprise digitization [

7,

8], organizational efficiency [

9], and corporate governance [

10]. While keeping in mind their shared objective of fostering CSR and sustainable development as complementary to traditional hard-law regulations [

11], many governments, particularly in Europe, have enacted CSR laws and regulations to shape CSR as a new societal governance [

6,

12], resulting in a reactive approach to CSR instead of a proactive approach [

13], thus external driving forces, such as government initiative [

6], social media [

14,

15] and mandatory disclosure [

16] have also become crucial determinants of CSR.

Reviewing the related research of CSR so far however, there is a scant amount of literature paying attention to the impact of the digital economy on CSR performance. As a new economic paradigm grounded in digital technology and information networks, the digital economy fundamentally changes the traditional economic environment and activities [

17,

18], leading to profound restructuring of corporate business models, organizational structures, and market competition patterns. Especially for CSR strategy decisions, a multi-dimensional enterprise behavior containing shareholders, employees, suppliers, consumers, environment, community and so on, will be deeply involved in the internal and external environment changes created by the deep application of digital technologies. As a result, CSR may become an increasingly important issue for firms operating in the digital economy, and it would be of great interest to investigate whether the development of the digital economy could affect the CSR performance for local firms; and what is the mechanism that brings them to this point.

The digital economy could bring about significant changes in the way businesses operate and interact with their stakeholders. From the corporate governance point of view, the digital economy accelerates the speed of information acquisition, storage, and processing, providing firms with adequate opportunities for digital transformation [

19], which enables firms to quickly capture and respond to the CSR proposition of various stakeholders based on digital technologies. On the other hand, the information disclosure system of firms to stakeholders would be comprehensively reshaped in the digital context [

20], improving the transparency of accounting information [

21,

22] and decreasing the agency in organizations with strong socially responsible commitment [

23], thereby contributing to the suppression of CSR “Greenwashing” behavior and other opportunist tendencies.

Additionally, in view of stakeholder identification, the digital economy has enabled stakeholders to have greater access to information and communication channels with the rise of digital media and industries such as online chats, short videos and livestreaming platforms. Thus, the CSR engagement will be more easily perceived by stakeholders, which can amplify the financial return from a more effective signaling [

24], further enhancing the economic motive for firms to invest in CSR. For example, in the “7·20” heavy rainstorm disaster in Zhengzhou, Henan Province of China in 2021, Hongxing Erke Company (ERKE), as a large sportswear firm, donated 50 million Yuan in goods and materials for post-disaster reconstruction, which was quickly fermented in the online media such as TikTok and Internet We-Media, eventually inducing a huge product publicity effect. According to the report released by

JD.com, the sales of ERKE increased 52 times year-on-year on 23 July 2021.

On the basis of the above practical observation and theoretical analysis, this paper attempts to fill the gap in the literature and explore the nexus between the local digital economy and CSR. China, as the largest emerging economy, has become increasingly reliant on the digital economy development model but at the same time is characterized by overall-low CSR performance [

25,

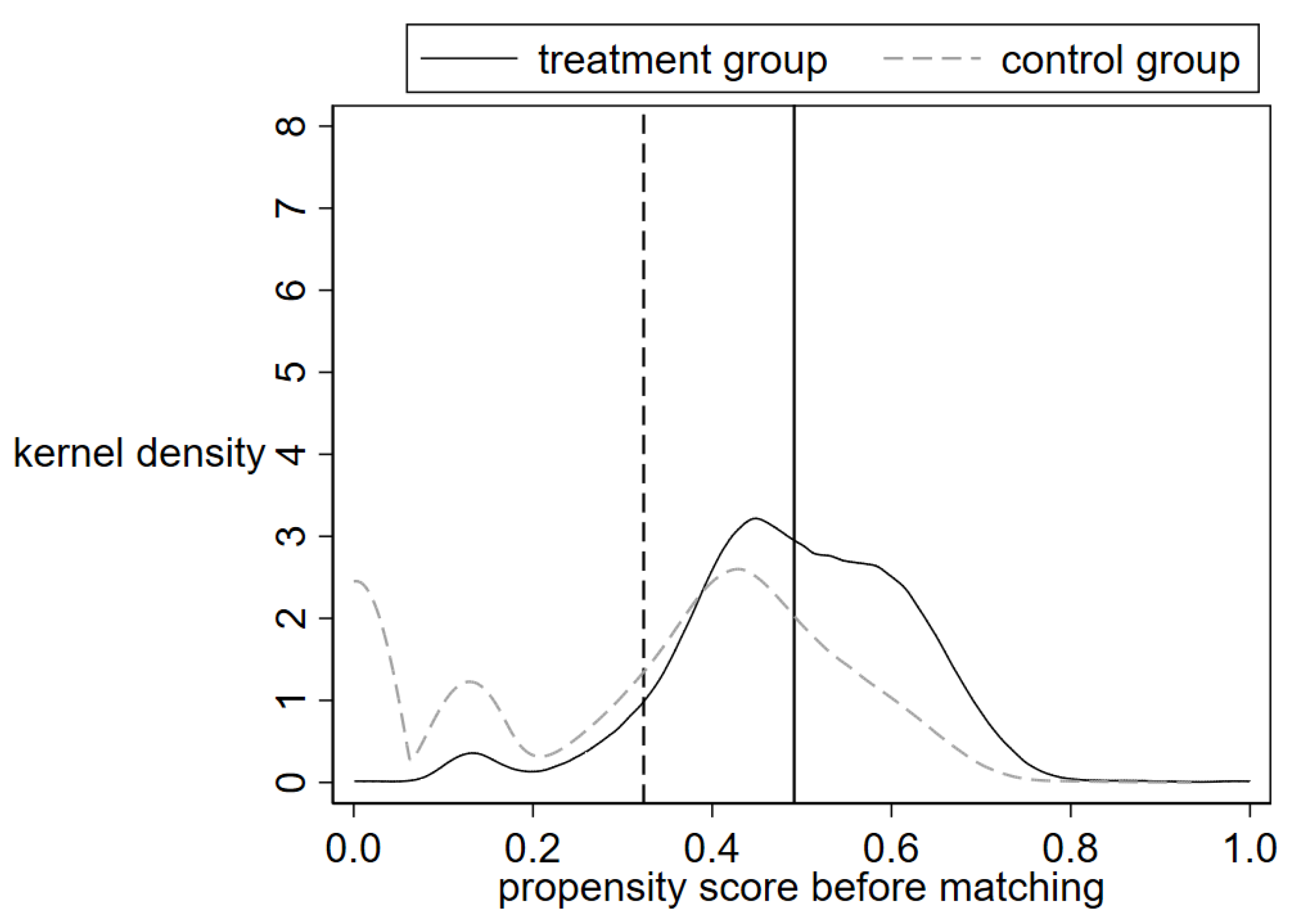

26], offering a suitable sample to examine empirical evidence on this important yet underexplored issue. Hence, using the data of Chinese A-shared listed companies from 2011 to 2020, we find that the development of digital economy significantly promotes local firms’ CSR performance. Our results are robust on a variety of endogenous and robustness levels, such as alternative measures of core variables, propensity score matching estimation, and instrumental variable estimation. Mechanism tests demonstrate that the digital economy can drive enterprise digital transformation, enhance agency efficiency and increase online media attention, thereby encouraging CSR of local firms. We also find that the impact of the local digital economy on different dimensions of CSR is different, and it is more pronounced among state-owned enterprises, firms in secondary industries, large-scale and non-digital enterprises.

This paper makes the following possible contributions. First, while numerous studies have explored the influencing factors of CSR [

6,

8,

10,

27], there is limited research on these in the digital economy context, so we expanded CSR research to new economic scenarios; and particularly based on signaling theory, we demonstrate the prevailing digital/online media in the era of digital economy could be used as an important transmission channel for firms to signal their ethical nature, providing a supplement to the relevant literature that mainly concerns traditional media communication [

15,

28].

Second, in contrast to previous studies that have focused on the digital economy from a specific perspective, such as artificial intelligence [

29], big data [

30] and the internet [

31], we attempt to construct the digital economy index of prefecture-level cities in China with an entropy approach, which is an objective weighting method aiming to scientifically reflect the contribution of various dimensions of evaluation [

30,

32].

Third, this paper contributes to literature on the impacts of the digital economy at the micro level. Different to the existing studies that mainly address the digital economy at the city or industry level, including the green economy [

17] and urban innovation [

33], the firm-level analysis in this study enables exploration of the mechanisms of the digital economy, which is useful for policymakers to build a micro foundation for sustainable economic development.

The remainder of the paper is structured as follows.

Section 2 introduces the theoretical hypotheses.

Section 3 outlines the construction of the sample and the regression models.

Section 4 presents the empirical results,

Section 5 discusses the findings, and

Section 6 concludes the paper.

5. Discussion of Findings

In the digital era, the application of digital technology in enterprises’ production and management has brought major changes to the development of enterprises. This study focuses on the relationship between local digital economy development and CSR. We find that the development of the local digital economy improves CSR performance by promoting the digital transformation of enterprises, improving agency efficiency, and increasing the attention of online media to enterprises. Moreover, the impact of the local digital economy on enterprises of different dimensions and the nature of CSR is significantly different.

Compared with previous research on the influencing factors of CSR, we explored how the digital development of the external or macro environment affected CSR from the perspective of the local digital economy. Based on signaling theory and “Greenwashing” behavior, we demonstrated the important role played by online media and agency efficiency in the performance of CSR, which provided theoretical guidance for policy formulation and sustainable development of enterprises.

Despite the achievements of this study, there are still shortcomings. On the one hand, as a developing country with rapid economic development and rapid rise of digital economy, the research conclusions may not be applicable to other countries with a rapid digital economy, which makes the research results limited. The follow-up research will focus on the impact on CSR of other countries with rapid digital economy development. On the other hand, during the COVID-19 pandemic, as the virus prevented people from working and consuming, online office and online shopping became mainstream, and these specific behaviors had a significant impact on the production and operations of enterprises [

52]. However, due to limited data availability, it is not possible to include the entire sample during the COVID-19 pandemic, and subsequent studies will focus on how the digital economy has impacted CSR during the COVID-19 pandemic.

6. Conclusions

The digital economy has brought about significant changes in the way businesses operate and interact with their stakeholders. As a result, CSR has become an increasingly important issue for companies operating in the digital economy. This paper regards Chinese A-share listed companies during 2011–2020 as a research sample, empirically examined the impact and mechanism of the digital economy on CSR performance. The empirical findings suggested that the digital economy can improve CSR performance through various channels including enterprise digital transformation, agency efficiency and online media attention. The heterogeneity analyses show that the impact of the digital economy on CSR varies according to stakeholder and firm characteristics, namely, the local digital economy would induce somewhat distinct impacts on different dimensions of CSR, and it is more pronounced among state-owned enterprises, firms in secondary industries, large-scale and non-digital firms.

To sum up, this research explores the modern link between local digital economy development and CSR. Due to the recent impact of the COVID-19 pandemic, firms are increasingly affected by the digital economy, online office and online sales enable corporate stakeholders to better supervise CSR behavior, and firms also improve their own value in undertaking CSR. Therefore, policymakers should encourage and support companies to undergo digital transformation by providing incentives, training programs, and financial support [

53,

54], enable companies to leverage digital technologies to adopt robust governance mechanisms to ensure compliance with CSR objectives and improve their CSR performance. Additionally, governments can collaborate with media organizations and digital platforms to highlight and promote companies that demonstrate exemplary CSR practices. This will encourage companies to prioritize CSR and engage in socially responsible activities, knowing that their efforts will be recognized and rewarded [

55]. In addition, investing in capacity building and education programs will enhance CSR knowledge and skills among digital economy professionals, promote the integration of CSR principles and practices into relevant academic curricula and professional development courses. This will contribute to a skilled workforce that understands the importance of CSR and can effectively drive its implementation in the digital economy, promoting CSR performance.

{kind=link}

{kind=link}