Empowering Women through Digital Financial Inclusion: Comparative Study before and after COVID-19

Abstract

:1. Introduction

2. Literature Review and Hypothesis Development

2.1. Digital Financial Inclusion before and after the Pandemic

2.2. Digital Financial Inclusion and Women’s Economic Empowerment

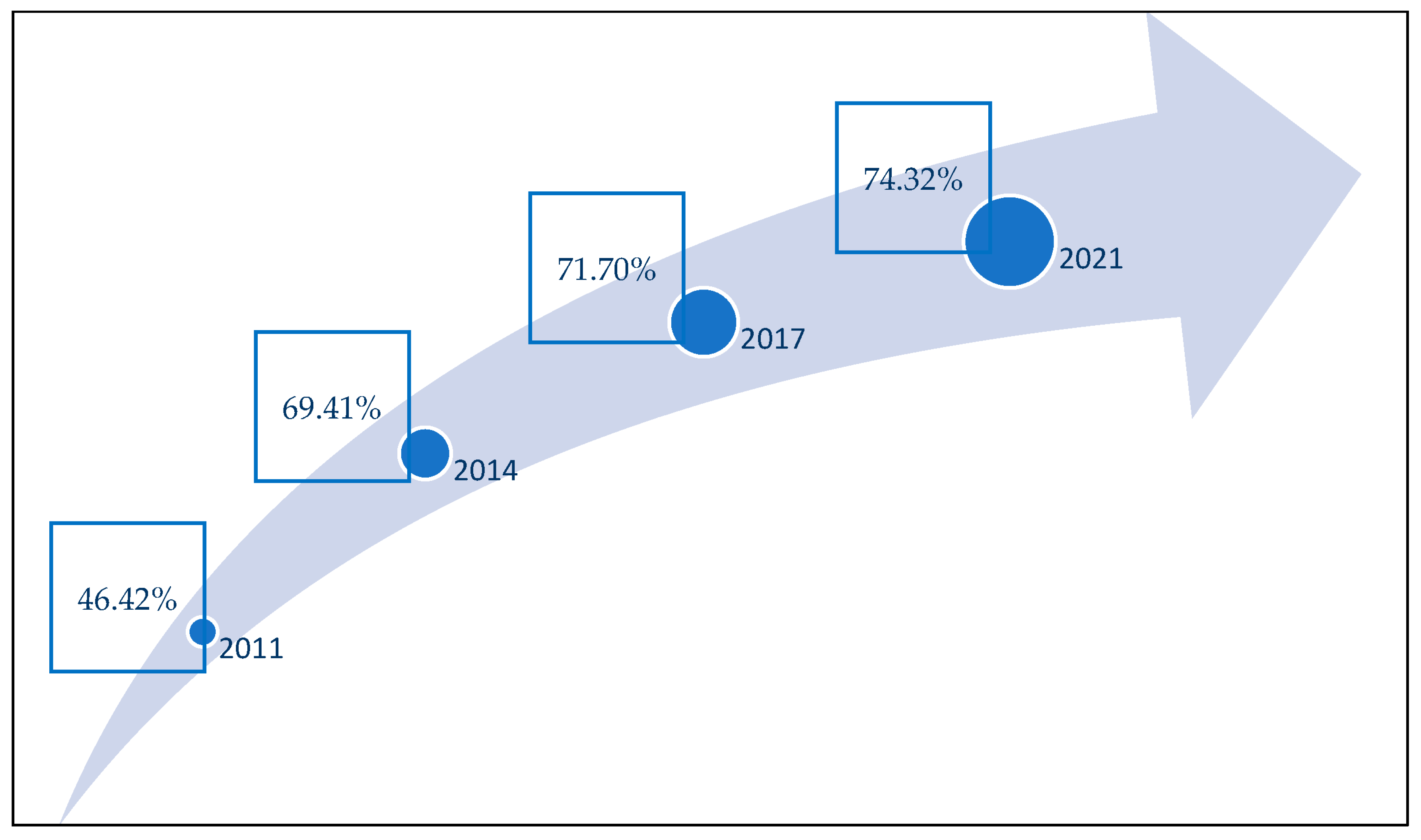

3. Stylized Facts

4. Data and Methodology

- Furthermore, j = 1…3

- where, i = 1…5

5. Results and Discussion

6. Conclusions, Study Implications, and Recommendations for Further Research

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Income Quintile Poorest 20% | Income Quintile Second 20% | Income Quintile Middle 20% | Income Quintile Fourth 20% | Income Quintile Richest 20% | |

|---|---|---|---|---|---|

| Model 1 Year 2017 | |||||

| Gender | 0.0128 | 0.0071 | 0.0014 | −0.0054 | −0.0159 |

| Age | 0.0173 | 0.0097 | 0.0021 | −0.0073 | −0.0219 |

| Age2 | −0.0002 | −0.0001 | 0.0000 | 0.0001 | 0.0003 |

| Education Secondary | −0.1473 | −0.0750 | 0.0128 | 0.0606 | 0.1745 |

| Education Tertiary or more | −0.2282 | −0.1410 | −0.0524 | 0.0675 | 0.3541 |

| Employment | 0.0538 | 0.0335 | 0.0100 | −0.0209 | −0.0764 |

| Has an account | −0.1281 | −0.0560 | −0.0024 | 0.0560 | 0.1304 |

| Saved | −0.0475 | −0.0265 | −0.0057 | 0.0198 | 0.0599 |

| Borrowed | 0.0393 | 0.0224 | 0.0052 | −0.0162 | −0.0507 |

| Digital payments | −0.0339 | −0.0195 | −0.0046 | 0.0139 | 0.0441 |

| Model 2 Year 2017 | |||||

| Gender × Digital payments | 0.0541 | 0.0257 | 0.0023 | −0.0239 | −0.0582 |

| Gender | −0.0020 | −0.0012 | −0.0002 | 0.0009 | 0.0026 |

| Age | 0.0175 | 0.0098 | 0.0021 | −0.0074 | −0.0221 |

| Age2 | −0.0002 | −0.0001 | 0.0000 | 0.0001 | 0.0003 |

| Education Secondary | −0.1442 | −0.0739 | −0.0127 | 0.0596 | 0.1712 |

| Education Tertiary or more | −0.2272 | −0.1409 | −0.0523 | 0.0676 | 0.3527 |

| Employment | 0.0512 | 0.0318 | 0.0093 | −0.0200 | −0.0723 |

| Has an account | −0.1271 | −0.0559 | −0.0024 | 0.0557 | 0.1296 |

| Saved | −0.0480 | −0.0268 | −0.0057 | 0.0201 | 0.0605 |

| Borrowed | 0.0394 | 0.0226 | 0.0052 | −0.0163 | −0.0509 |

| Digital payments | −0.0468 | −0.0273 | −0.0067 | 0.0191 | 0.0617 |

| Model 3 Year 2017 | |||||

| Gender × Digital payments | 0.0514 | 0.0023 | 0.0023 | −0.0226 | −0.0556 |

| Gender × Employment | 0.0575 | 0.0282 | 0.0034 | −0.0251 | −0.0251 |

| Gender | −0.0468 | −0.0273 | −0.0068 | 0.0190 | 0.0620 |

| Age | 0.0192 | 0.0107 | 0.0023 | −0.0080 | −0.0241 |

| Age2 | −0.0002 | −0.0001 | 0.0000 | 0.0001 | 0.0003 |

| Education Secondary | −0.1390 | −0.0713 | −0.0124 | 0.0574 | 0.1653 |

| Education Tertiary or more | −0.2243 | −0.1387 | 0.0512 | 0.0671 | 0.3471 |

| Has a n account | −0.1249 | −0.0550 | −0.0025 | 0.0546 | 0.1278 |

| Saved | −0.0469 | −0.0261 | −0.0056 | 0.0195 | 0.0590 |

| Borrowed | 0.0414 | 0.0237 | 0.0055 | −0.0170 | −0.0535 |

| Digital payments | −0.0458 | −0.0266 | −0.0066 | 0.0186 | 0.0603 |

| Model 1 Year 2021 | |||||

|---|---|---|---|---|---|

| Gender | −0.0583 | −0.0418 | −0.0171 | 0.0187 | 0.0986 |

| Age | −0.0060 | −0.0043 | −0.0017 | 0.0020 | 0.0101 |

| Age2 | 0.0001 | 0.0001 | 0.0000 | 0.0000 | −0.0002 |

| Education Secondary | −0.1291 | −0.0889 | −0.0357 | 0.0400 | 0.2138 |

| Education Tertiary or more | −0.2146 | −0.1366 | −0.0534 | 0.0609 | 0.3438 |

| Employment | −0.0502 | −0.0320 | −0.0103 | 0.0186 | 0.0739 |

| Has an account | −0.0935 | −0.0544 | −0.0142 | 0.0364 | 0.1257 |

| Saved | −0.0271 | −0.0187 | −0.0070 | 0.0094 | 0.0434 |

| Borrowed | 0.0109 | 0.0078 | 0.0032 | −0.0036 | −0.0183 |

| Digital payments | −0.0299 | −0.0208 | −0.0079 | 0.0102 | 0.0484 |

| Model 2 Year 2021 | |||||

| Female × Digital payments | 0.0791 | 0.0475 | 0.0131 | −0.0308 | −0.1089 |

| Gender | −0.0994 | −0.0714 | −0.0297 | 0.0310 | 0.1695 |

| Age | −0.0056 | −0.0040 | −0.0016 | 0.0019 | 0.0093 |

| Age2 | 0.0001 | 0.0001 | 0.0000 | 0.0000 | −0.0002 |

| Education Secondary | −0.1197 | −0.0836 | −0.0335 | 0.0378 | 0.1990 |

| Education Tertiary or more | −0.2037 | −0.1321 | −0.0517 | 0.0592 | 0.3282 |

| Employment | −0.0517 | −0.0332 | −0.0105 | 0.0194 | 0.0760 |

| Has an account | −0.0912 | −0.0538 | −0.0141 | 0.0358 | 0.1233 |

| Saved | −0.0280 | −0.0194 | −0.0072 | 0.0098 | 0.0448 |

| Borrowed | 0.0109 | 0.0079 | 0.0032 | −0.0036 | −0.0184 |

| Digital payments | −0.0692 | −0.0467 | −0.0168 | 0.0244 | 0.1083 |

| Model 3 Year 2021 | |||||

| Gender × Digital payments | 0.0841 | 0.0501 | 0.0135 | −0.0330 | −0.1147 |

| Gender × Employment | −0.0553 | −0.0431 | −0.0199 | 0.0158 | 0.1024 |

| Female | −0.0523 | −0.0380 | −0.0155 | 0.0171 | 0.0887 |

| Age | −0.0063 | −0.0045 | −0.0018 | 0.0021 | 0.0105 |

| Age2 | 0.0001 | 0.0001 | 0.0000 | 0.0000 | −0.0002 |

| Education Secondary | −0.1189 | −0.0832 | −0.0335 | 0.0376 | 0.1980 |

| Education Tertiary or more | −0.2043 | −0.1327 | −0.0521 | 0.0594 | 0.3296 |

| Has an account | −0.0920 | −0.0542 | −0.0142 | 0.0361 | 0.1243 |

| Saved | −0.0280 | −0.0194 | −0.0073 | 0.0098 | 0.0448 |

| Borrowed | 0.0091 | 0.0066 | 0.0027 | −0.0030 | −0.0154 |

| Digital payments | −0.0715 | −0.0483 | −0.0173 | 0.0253 | 0.1118 |

References

- Popescu, C.R.G. Fostering creativity in business: Empowering strong transformational leaders. In Handbook of Research on Changing Dynamics in Responsible and Sustainable Business in the Post-COVID-19 Era; IGI Global: Hershey, PA, USA, 2022; pp. 349–381. [Google Scholar]

- Hendriks, S. The role of financial inclusion in driving women’s economic empowerment. Dev. Pract. 2019, 29, 1029–1038. [Google Scholar] [CrossRef] [Green Version]

- Ibrahim, S.S.; Aliero, H.M. Testing the impact of financial inclusion on income convergence: Empirical evidence from Nigeria. Afr. Dev. Rev. 2020, 32, 42–54. [Google Scholar] [CrossRef]

- Allen, F.; Demirguc-Kunt, A.; Klapper, L.; Peria, M.S.M. The foundations of financial inclusion: Understanding ownership and use of formal accounts. J. Financ. Intermed. 2016, 27, 1–30. [Google Scholar] [CrossRef] [Green Version]

- Arner, D.W.; Buckley, R.P.; Zetzsche, D.A.; Veidt, R. Sustainability, FinTech and financial inclusion. Eur. Bus. Organ. Law Rev. 2020, 21, 7–35. [Google Scholar] [CrossRef]

- Guiso, L.; Sapienza, P.; Zingales, L. Does Local Financial Development Matter? Springer: Berlin/Heidelberg, Germany, 2009. [Google Scholar]

- Brown, J.R.; Cookson, J.A.; Heimer, R.Z. Growing up without finance. J. Financ. Econ. 2019, 134, 591–616. [Google Scholar] [CrossRef]

- Célerier, C.; Matray, A. Bank-branch supply, financial inclusion, and wealth accumulation. Rev. Financ. Stud. 2019, 32, 4767–4809. [Google Scholar] [CrossRef]

- Demirgüç-Kunt, A.; Singer, D. Financial Inclusion and Inclusive Growth: A Review of Recent Empirical Evidence; World Bank Policy Research Working Paper; World Bank Publications: Washington, DC, USA, 2017. [Google Scholar]

- Ke, D. Who wears the pants? Gender identity norms and intrahousehold financial decision-making. J. Financ. 2021, 76, 1389–1425. [Google Scholar] [CrossRef]

- Demirguc-Kunt, A.; Klapper, L.; Singer, D.; Ansar, S. The Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution; World Bank Publications: Washington, DC, USA, 2018. [Google Scholar]

- Breza, E.; Kanz, M.; Klapper, L.F. Learning to Navigate a New Financial Technology: Evidence from Payroll Accounts; National Bureau of Economic Research: Cambridge, MA, USA, 2020. [Google Scholar]

- Philippon, T. On Fintech and Financial Inclusion; National Bureau of Economic Research: Cambridge, MA, USA, 2019. [Google Scholar]

- Boot, A.W.; Hoffmann, P.; Laeven, L.; Ratnovski, L. Financial Intermediation and Technology: What’s Old, What’s New? IMF: Washington, DC, USA, 2020. [Google Scholar]

- Thakor, A.V. Fintech and banking: What do we know? J. Financ. Intermed. 2020, 41, 100833. [Google Scholar] [CrossRef]

- Suri, T.; Jack, W. The long-run poverty and gender impacts of mobile money. Science 2016, 354, 1288–1292. [Google Scholar] [CrossRef]

- Ouma, S.A.; Odongo, T.M.; Were, M. Mobile financial services and financial inclusion: Is it a boon for savings mobilization? Rev. Dev. Financ. 2017, 7, 29–35. [Google Scholar] [CrossRef]

- Lee, J.N.; Morduch, J.; Ravindran, S.; Shonchoy, A.; Zaman, H. Poverty and migration in the digital age: Experimental evidence on mobile banking in Bangladesh. Am. Econ. J. Appl. Econ. 2021, 13, 38–71. [Google Scholar] [CrossRef]

- Bachas, P.; Gertler, P.; Higgins, S.; Seira, E. How debit cards enable the poor to save more. J. Financ. 2021, 76, 1913–1957. [Google Scholar] [CrossRef]

- Aker, J.C.; Boumnijel, R.; McClelland, A.; Tierney, N. Payment mechanisms and antipoverty programs: Evidence from a mobile money cash transfer experiment in Niger. Econ. Dev. Cult. Chang. 2016, 65, 1–37. [Google Scholar] [CrossRef] [Green Version]

- Ashraf, N.; Aycinena, D.; Martínez, A.C.; Yang, D. Savings in transnational households: A field experiment among migrants from El Salvador. Rev. Econ. Stat. 2015, 97, 332–351. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. Financial Literacy and Planning: Implications for Retirement Wellbeing; National Bureau of Economic Research: Cambridge, MA, USA, 2011. [Google Scholar]

- Hasler, A.; Lusardi, A. The Gender Gap in Financial Literacy: A Global Perspective; Global Financial Literacy Excellence Center, The George Washington University School of Business: Washington, DC, USA, 2017. [Google Scholar]

- Gonçalves, V.N.; Ponchio, M.C.; Basílio, R.G. Women’s financial well-being: A systematic literature review and directions for future research. Int. J. Consum. Stud. 2021, 45, 824–843. [Google Scholar] [CrossRef]

- Thomas, A.; Gupta, V. Social capital theory, social exchange theory, social cognitive theory, financial literacy, and the role of knowledge sharing as a moderator in enhancing financial well-being: From bibliometric analysis to a conceptual framework model. Front. Psychol. 2021, 12, 664638. [Google Scholar] [CrossRef] [PubMed]

- King, R.G.; Levine, R. Finance and growth: Schumpeter might be right. Q. J. Econ. 1993, 108, 717–737. [Google Scholar] [CrossRef]

- Levine, R. Finance and growth: Theory and evidence. In Handbook of Economic Growth; Elsevier: Amsterdam, The Netherlands, 2005; Volume 1, pp. 865–934. [Google Scholar]

- Banerjee, A.V.; Newman, A.F. Occupational choice and the process of development. J. Political Econ. 1993, 101, 274–298. [Google Scholar] [CrossRef] [Green Version]

- Clarke, G.R.; Xu, L.C.; Zou, H.F. Finance and income inequality: What do the data tell us? South. Econ. J. 2006, 72, 578–596. [Google Scholar]

- Davis, F.D. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Q. 1989, 13, 319–340. [Google Scholar] [CrossRef] [Green Version]

- Ajzen, I. Action control: From cognition to behavior. In From Intetions to Actions: A Theory of Planned Behavior; Springer: Berlin/Heidelberg, Germany, 1985. [Google Scholar]

- Rogers, E.M. Diffusion of Innovations; Simon and Schuster: New York, NY, USA, 2010. [Google Scholar]

- Were, M.; Odongo, M.; Israel, C. Gender Disparities in Financial Inclusion in Tanzania; Report No.: 9292670379; WIDER Working Paper; World Institute for Development Economics Research: Helsinki, Finland, 2021. [Google Scholar]

- Mndolwa, F.D.; Alhassan, A.L. Gender disparities in financial inclusion: Insights from Tanzania. Afr. Dev. Rev. 2020, 32, 578–590. [Google Scholar] [CrossRef]

- Songwe, V.; The Role of Digitalization in the Decade of Action for Africa. Retrieved from Tralac Org. 2020. Available online: https://www.tralac.org/news/article/14900-the-role-of-digitalization-in-the-decade-of-action-for-africa.html (accessed on 28 February 2023).

- United Nations Economic Commission for Africa. COVID-19 in Africa: Protecting Lives and Economies; Economic Commission for Africa: Addis Ababa, Ethiopia, 2020. [Google Scholar]

- Bousrih, J.; Elhaj, M.; Hassan, F. The labor market in the digital era: What matters for the Gulf Cooperation Council countries? Front. Sociol. 2022, 7, 959091. [Google Scholar] [CrossRef] [PubMed]

- Ozili, P. COVID-19 in Africa: Socio-economic impact, policy response and opportunities. Int. J. Sociol. Soc. Policy 2020, 42, 177–200. [Google Scholar] [CrossRef]

- Vasile, V.; Panait, M.; Apostu, S.-A. Financial inclusion paradigm shift in the postpandemic period. digital-divide and gender gap. Int. J. Environ. Res. Public Health 2021, 18, 10938. [Google Scholar] [CrossRef]

- Shafeeq, M.; Beg, S. A study to assess the impact of COVID-19 pandemic on digital financial services and digital financial inclusion in India. Afr. J. Account. Audit. Financ. 2021, 7, 326–345. [Google Scholar] [CrossRef]

- Alarifi, A.A.; Husain, K.S. The influence of Internet banking services quality on e-customers’ satisfaction of Saudi banks: Comparison study before and during COVID-19. Int. J. Qual. Reliab. Manag. 2023, 40, 496–516. [Google Scholar] [CrossRef]

- Abu Daqar, M.; Constantinovits, M.; Arqawi, S.; Daragmeh, A. The role of Fintech in predicting the spread of COVID-19. Banks Bank Syst. 2021, 16, 1–16. [Google Scholar] [CrossRef]

- Al Shehab, N.; Hamdan, A. Artificial intelligence and women empowerment in Bahrain. In Applications of Artificial Intelligence in Business, Education and Healthcare; Springer: Cham, Switzerland, 2021; pp. 101–121. [Google Scholar]

- Abrar ul Haq, M.; Victor, S.; Akram, F. Exploring the motives and success factors behind female entrepreneurs in India. Qual. Quant. 2021, 55, 1105–1132. [Google Scholar] [CrossRef]

- Abrar ul Haq, M.; Akram, F.; Ashiq, U.; Raza, S. The employment paradox to improve women’s empowerment in Pakistan. Cogent Soc. Sci. 2019, 5, 1707005. [Google Scholar] [CrossRef]

- Kulkarni, L.; Ghosh, A. Gender disparity in the digitalization of financial services: Challenges and promises for women’s financial inclusion in India. Gend. Technol. Dev. 2021, 25, 233–250. [Google Scholar] [CrossRef]

- Elzahi Saaid Ali, A. Empowering Women Through Islamic Financial Inclusion in Comoros. In Empowering the Poor through Financial and Social Inclusion in Africa: An Islamic Perspective; Springer: Berlin/Heidelberg, Germany, 2022; pp. 49–72. [Google Scholar]

- Ojo, T.A. Digital Financial Inclusion for Women in the Fourth Industrial Revolution: A Key towards Achieving Sustainable Development Goal 5. Afr. Rev. 2022, 14, 98–123. [Google Scholar] [CrossRef]

- Kim, K. Assessing the impact of mobile money on improving the financial inclusion of Nairobi women. J. Gend. Stud. 2022, 31, 306–322. [Google Scholar] [CrossRef]

- Corrêa, M.F. Fintechs as promoters of women’s financial inclusion: A comparative case study between Brazil, China and Kenya. Ph.D. Thesis, Escola de Administração de Empresas de São Paulo, São Paulo, Brazil, 2022. [Google Scholar]

- Cabeza-García, L.; Del Brio, E.B.; Oscanoa-Victorio, M.L. (Eds.) Female financial inclusion and its impacts on inclusive economic development. In Women’s Studies International Forum; Elsevier: Amsterdam, The Netherlands, 2019. [Google Scholar]

- Mabrouk, F.; Halid, N. Inclusive Finance and Income Inequality: An Evidence from Saudi Arabia. In Financial Inclusion in Emerging Markets; Palgrave Macmillan: Singapore, 2021; pp. 311–327. [Google Scholar]

- Jedi, F.F. The Relationship between Financial Inclusion and Women’s Empowerment: Evidence from Iraq. J. Bus. Manag. Stud. 2022, 4, 104–120. [Google Scholar] [CrossRef]

- Jahangir Rony, R.; Shabnam Khan, S.; Sinha, A.; Saha, A.; Ahmed, N. (Eds.) “COVID has made Everyone Digital and Digitally Independent”: Understanding Working Women’s DFS and Technology Adoption during COVID Pandemic in Bangladesh. In Proceedings of the Asian CHI Symposium 2021, Online, 16–17 October 2021; Association for Computing Machinery: New York, NY, USA, 2021. [Google Scholar]

- Demirgüç-Kunt, A.; Klapper, L.; Singer, D.; Ansar, S. The Global Findex Database 2021: Financial Inclusion, Digital Payments, and Resilience in the Age of COVID-19; World Bank Publications: Washington, DC, USA, 2022. [Google Scholar]

- Saudi Central Bank, 57th report. 2021. Available online: https://www.sama.gov.sa/en-US/EconomicReports/AnnualReport/ANNUAL_Report_57th_2021.pdf (accessed on 28 February 2023).

- Charmes, J.; Wieringa, S. Measuring women’s empowerment: An assessment of the gender-related development index and the gender empowerment measure. J. Hum. Dev. 2003, 4, 419–435. [Google Scholar] [CrossRef]

- Pal, M.; Gupta, H.; Joshi, Y.C. Social and economic empowerment of women through financial inclusion: Empirical evidence from India. Equal. Divers. Incl. Int. J. 2022, 41, 294–305. [Google Scholar] [CrossRef]

- Grilli, L.; Rampichini, C. Ordered logit model. In Encyclopedia of Quality of Life and Well-Being Research; Springer: Dordrecht, The Netherlands, 2014. [Google Scholar]

- Ferrant, G.; Thim, A. Measuring Women’s Economic Empowerment: Time Use Data and Gender Inequality; OECD Development Policy Papers, No. 16; OECD Publishing: Paris, France, 2019. [Google Scholar]

- Bank, W. Women, Business and the Law 2020; The World Bank: Washington, DC, USA, 2020. [Google Scholar]

- Alshebami, A.S.; Rengarajan, V.; Pahlevi, R.W.; Said, J.; Sari, W.R. Challenges and Risk of Microfinance Sustainability Amid COVID-19 Pandemic Crisis. Acad. Strateg. Manag. J. 2021, 20, 1–5. [Google Scholar]

| 2014 | 2017 | 2021 | |||

|---|---|---|---|---|---|

| High-Income Economies | Developing Economies | High-Income Economies | Developing Economies | High-Income Economies | Developing Economies |

| 88% | 35% | 90% | 44% | 95% | 57% |

| Year 2017 Valid and Total Responses: 1009 | Year 2021 Valid and Total Responses: 1019 | ||

|---|---|---|---|

| Female 2017 | Male 2017 | Female 2021 | Male 2021 |

| 363 (36%) | 646 (64%) | 472 (46.3%) | 547 (53.7%) |

| Gender | Respondent is Female |

|---|---|

| Age | Respondent age |

| Education Secondary | Respondent’s education level is secondary |

| Education Tertiary or more | Respondent’s education level is completed tertiary or more |

| Employment | Respondent’s is in the workforce |

| Has an account | Respondent has an account at a financial institution |

| Saved | Respondent saved in the past year at a financial institution |

| Borrowed | Respondent borrowed in the past year at a financial institution |

| Digital payments | Respondent made bill payments online using the Internet |

| Gender × Digital payments | Female respondents made bill payments online using the Internet |

| Gender × Employment | Female respondent is in the workforce |

| Year 2017 | Year 2021 | |||

|---|---|---|---|---|

| All Sample (100%) | Only Women (36%) | All Sample (100%) | Only Women (46.3%) | |

| Age | ||||

| 15–25 | 268 | 141 | 334 | 188 |

| 26.56% | 38.84% | 32.78% | 39.83% | |

| 26–35 | 435 | 139 | 476 | 193 |

| 43.11% | 38.29% | 46.71% | 40.89% | |

| 36–45 | 186 | 53 | 159 | 72 |

| 18.43% | 14.60% | 15.60% | 15.25% | |

| 46–65 And > 65 | 120 | 30 | 50 | 19 |

| 11.89% | 8.26% | 4.91% | 4.03% | |

| Education | ||||

| Primary or less | 77 | 29 | 16 | 8 |

| 7.63% | 7.99% | 1.57% | 1.69% | |

| Secondary | 557 | 201 | 498 | 236 |

| 55.20% | 55.37% | 48.87% | 50.00% | |

| Tertiary or more | 375 | 133 | 505 | 228 |

| 37.17% | 36.64% | 49.56% | 48.31% | |

| Workforce | ||||

| Out of workforce | 226 | 163 | 213 | 168 |

| 22.40% | 44.90% | 20.90% | 35.59% | |

| In workforce | 783 | 200 | 806 | 304 |

| 77.60% | 55.10% | 79.10% | 64.41% | |

| Income quintile | ||||

| Poorest 20% | 117 | 62 | 142 | 65 |

| 11.60% | 17.08% | 13.94% | 13.77% | |

| Second 20% | 184 | 70 | 165 | 72 |

| 18.24% | 19.28% | 16.19% | 15.25% | |

| Middle 20% | 184 | 76 | 184 | 72 |

| 18.24% | 20.94% | 18.06% | 15.25% | |

| Fourth 20% | 218 | 72 | 233 | 114 |

| 21.61% | 19.83% | 22.87% | 24.15% | |

| Richest 20% | 246 | 83 | 295 | 149 |

| 24.38% | 22.87% | 28.95% | 31.57% | |

| Has an account at a financial institution | 752 | 220 | 801 | 330 |

| 74.53% | 60.61% | 78.61% | 69.92% | |

| 2017 | 2021 | |||||

|---|---|---|---|---|---|---|

| Model 1 | Model 2 | Model 3 | Model 1 | Model 2 | Model 3 | |

| Gender × Digital payments | −0.2104 | −0.2002 | −0.3528 ** | −0.3734 ** | ||

| (0.1607) | (0.1623) | (0.1494) | (0.1499) | |||

| Gender × Employment | −0.2275 * | 0.2990 *** | ||||

| (0.1194) | (0.1074) | |||||

| Gender | −0.0539 | 0.0087 | 0.2041 * | 0.2955 *** | 0.5089 *** | 0.2663 * |

| (0.0810) | (0.0962) | (0.1069) | (0.0773) | (0.1244) | (0.1388) | |

| Age | −0.0734 *** | −0.0744 *** | −0.0811 *** | 0.0302 | 0.0280 | 0.0316 |

| (0.0184) | (0.0184) | (0.0183) | (0.0259) | (0.0257) | (0.0259) | |

| Age2 | 0.0009 *** | 0.0009 *** | 0.0010 *** | −0.0007 * | −0.0007 * | −0.0007 ** |

| (0.0002) | (0.0002) | (0.0002) | (0.0004) | (0.0004) | (0.0004) | |

| Education Secondary | 0.6043 *** | 0.5928 *** | 0.5713 *** | 0.6479 ** | 0.6033 * | 0.6001 * |

| (0.1444) | (0.1445) | (0.1428) | (0.3167) | (0.3190) | (0.3137) | |

| Education Tertiary or more | 1.1119 *** | 1.1083 *** | 1.0904 *** | 1.0632 *** | 1.0138 *** | 1.0183 *** |

| (0.1520) | (0.1516) | (0.1503) | (0.3161) | (0.3183) | (0.3134) | |

| Employment | −0.2446 *** | −0.2321 *** | 0.2325 *** | 0.2398 * | ||

| (0.0941) | (0.0945) | (0.0928) | (0.0929) | |||

| Has an account | 0.4844 *** | 0.4815 *** | 0.4734 *** | 0.4104 *** | 0.4027 *** | 0.4061 *** |

| (0.0893) | (0.0893) | (0.0892) | (0.1023) | (0.1028) | (0.1024) | |

| Saved | 0.2012 *** | 0.2037 *** | 0.1985 *** | 0.1325 * | 0.1370 * | 0.1371 * |

| (0.0699) | (0.0701) | (0.0701) | (0.0744) | (0.0745) | (0.0742) | |

| Borrowed | −0.1686 *** | −0.1693 *** | −0.1779 ** | −0.0547 | −0.0553 | −0.0462 |

| (0.0724) | (0.0725) | (0.0723) | (0.0763) | (0.0763) | (0.0762) | |

| Digital payments | 0.1463 ** | 0.2036 *** | 0.1990 ** | 0.1470 * | 0.3342 *** | 0.3453 *** |

| (0.0769) | (0.0894) | (0.0894) | (0.0803) | (0.1141) | (0.1143) | |

| Number of observations | 1009 | 1009 | 1009 | 1019 | 1019 | 1019 |

| Log pseudolikelihood | −1531.7143 | −1530.8759 | −1532.031 | −1531.4408 | −1528.5298 | −1527.9718 |

| Wald Chi2 | 161.11 [0.0000] | 162.70 [0.0000] | 159.56 [0.0000] | 123.11 [0.0000] | 129.25 [0.0000] | 132.70 [0.0000] |

| Pseudo R2 | 0.0519 | 0.0524 | 0.0517 | 0.0456 | 0.0475 | 0.0478 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mabrouk, F.; Bousrih, J.; Elhaj, M.; Binsuwadan, J.; Alofaysan, H. Empowering Women through Digital Financial Inclusion: Comparative Study before and after COVID-19. Sustainability 2023, 15, 9154. https://doi.org/10.3390/su15129154

Mabrouk F, Bousrih J, Elhaj M, Binsuwadan J, Alofaysan H. Empowering Women through Digital Financial Inclusion: Comparative Study before and after COVID-19. Sustainability. 2023; 15(12):9154. https://doi.org/10.3390/su15129154

Chicago/Turabian StyleMabrouk, Fatma, Jihen Bousrih, Manal Elhaj, Jawaher Binsuwadan, and Hind Alofaysan. 2023. "Empowering Women through Digital Financial Inclusion: Comparative Study before and after COVID-19" Sustainability 15, no. 12: 9154. https://doi.org/10.3390/su15129154