The Nexus between Climate Change and Geopolitical Risk Index in Saudi Arabia Based on the Fourier-Domain Transfer Entropy Spectrum Method

Abstract

:1. Introduction

2. Literature Review

3. Fourier-Domain Transfer Entropy Spectrum

4. Data and Empirical Results

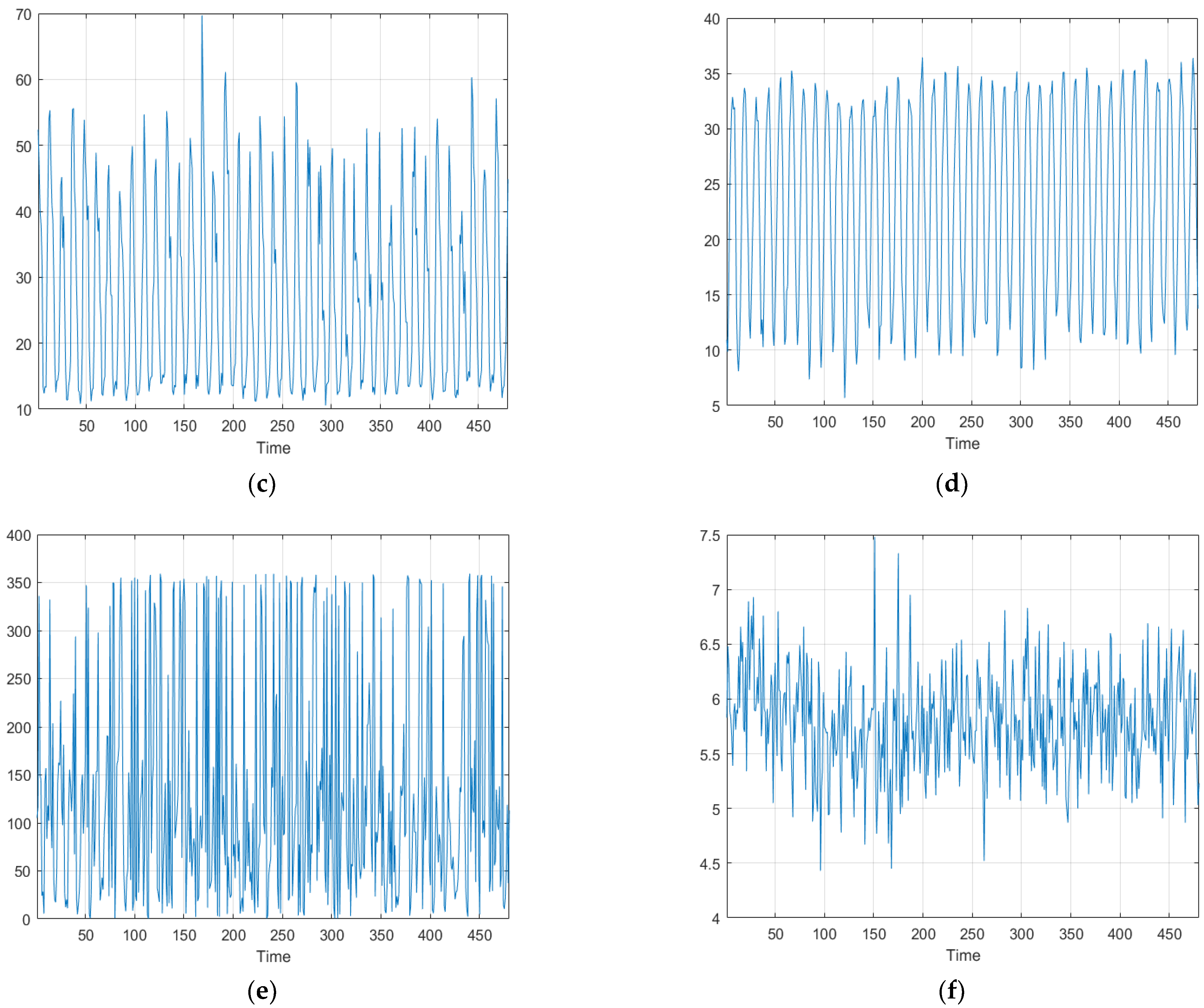

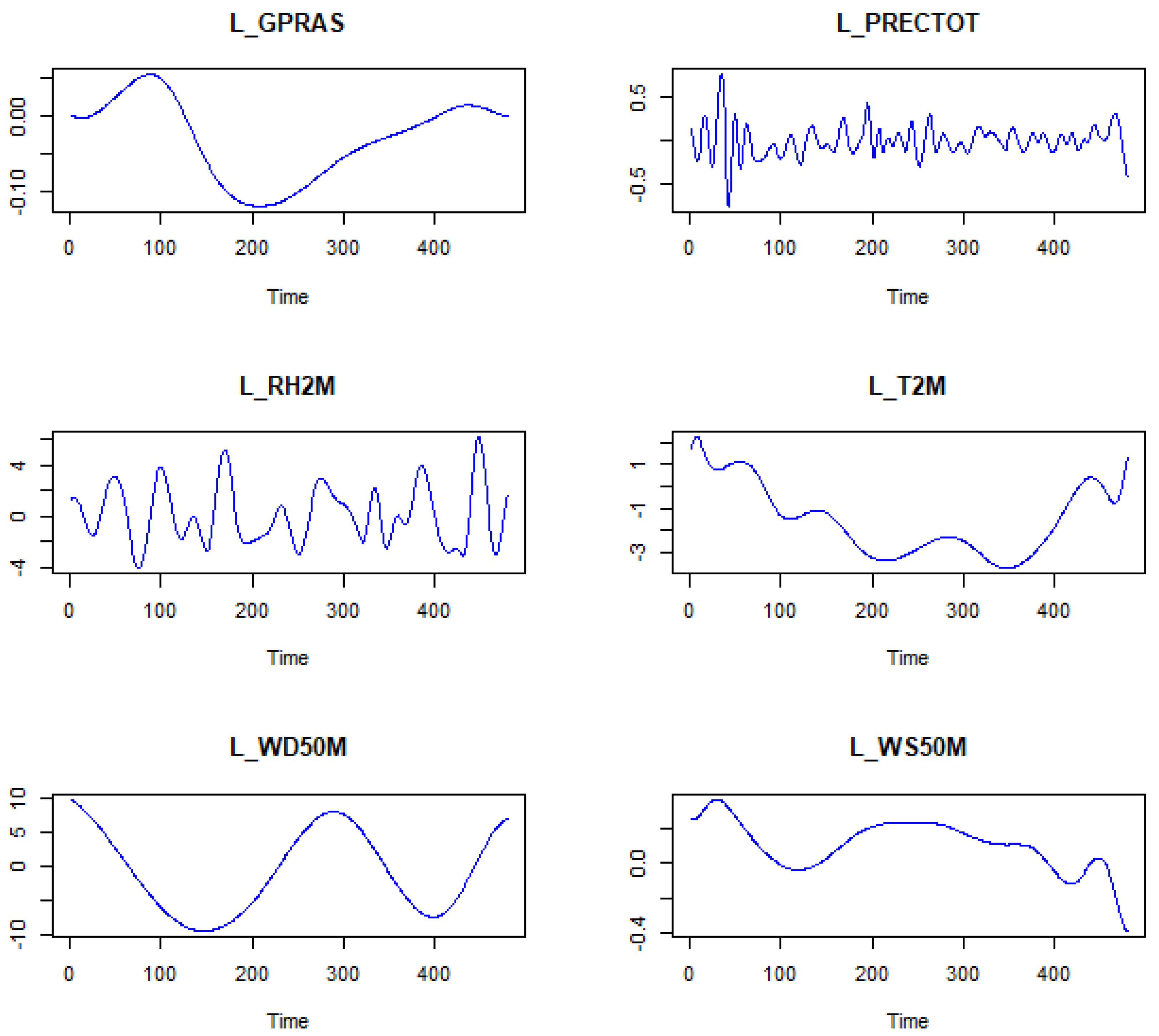

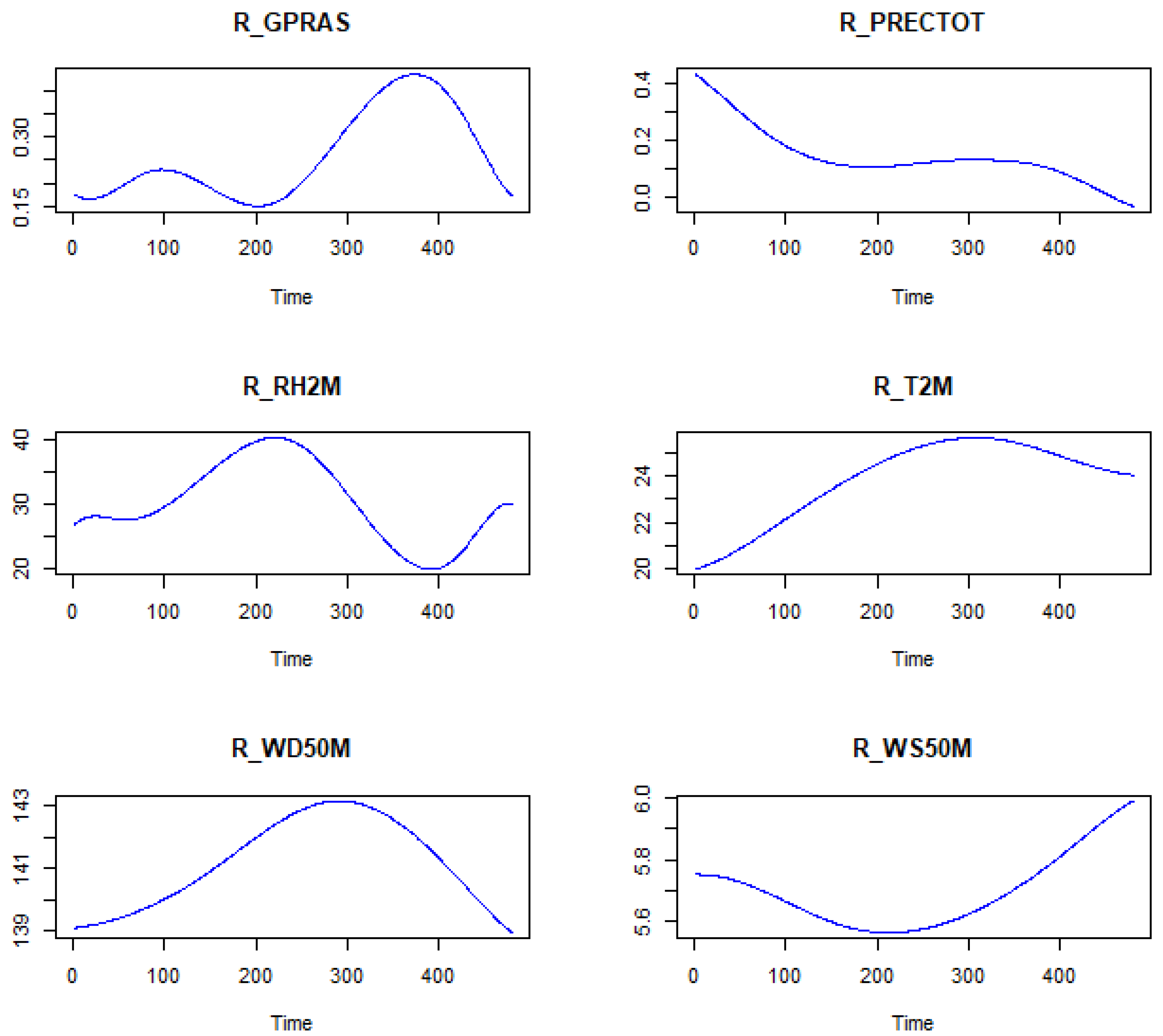

4.1. Data

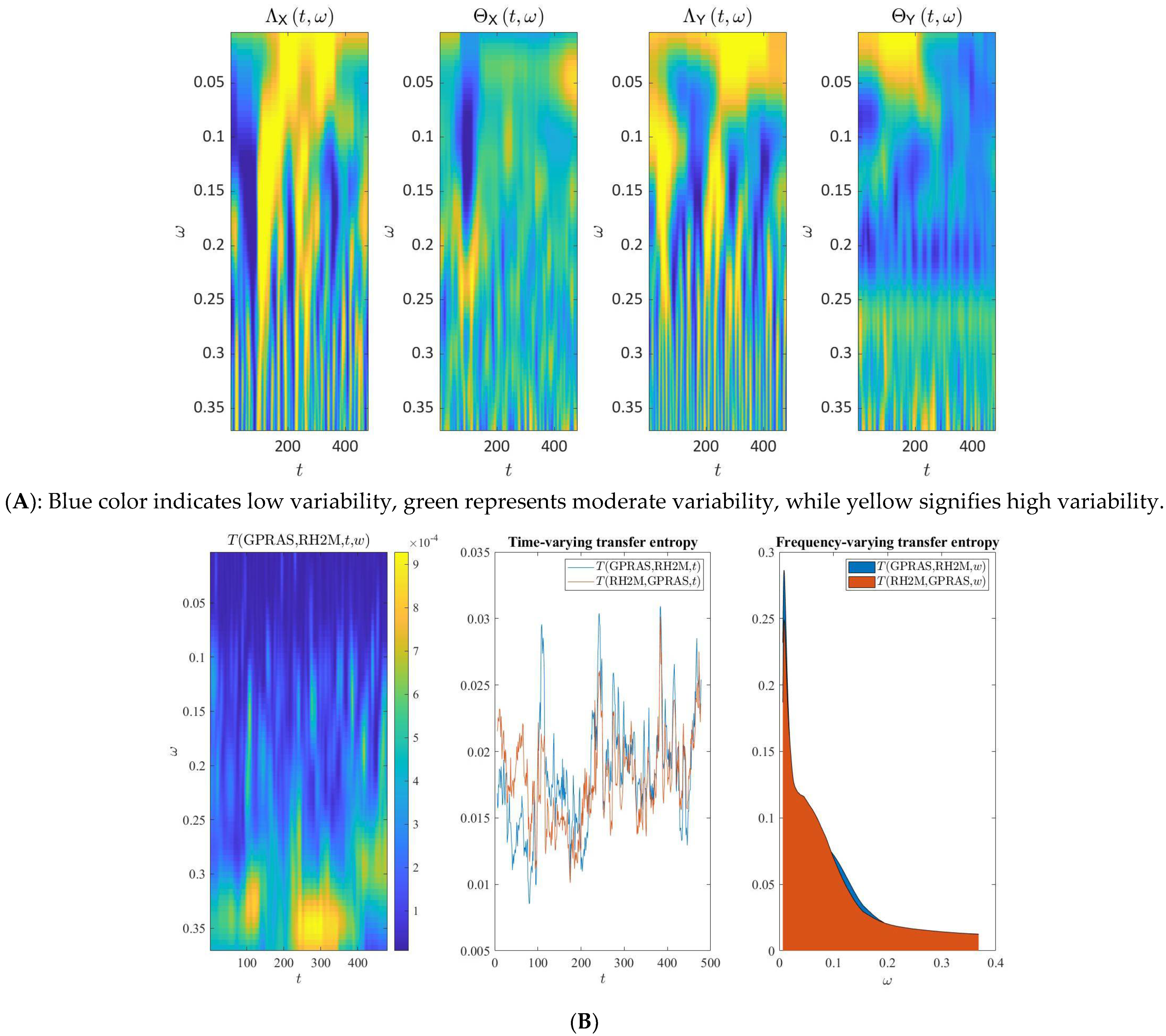

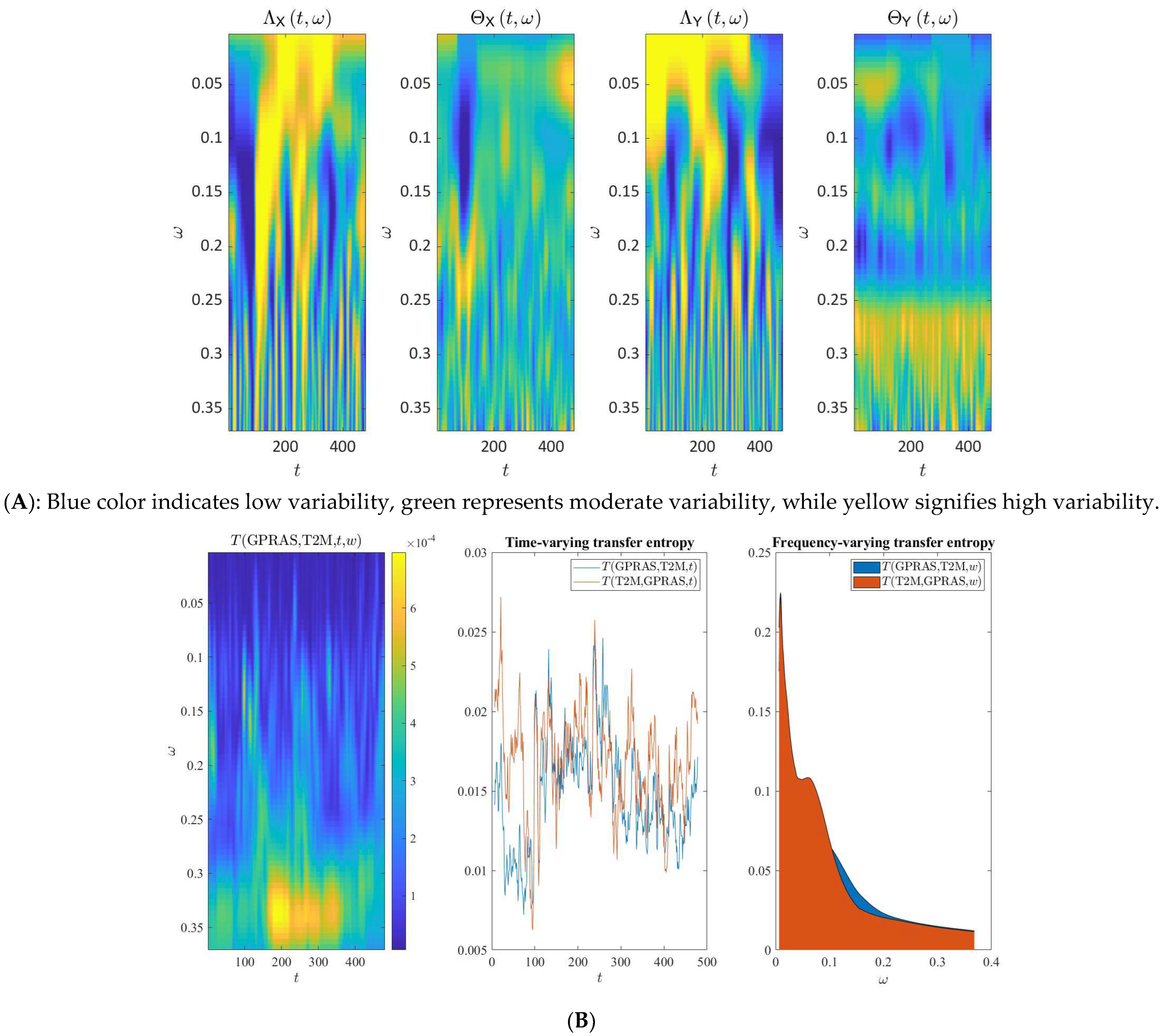

4.2. Empirical Results

5. Robustness Check

6. Discussion

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- World Bank. World Development Indicators. 2010. Available online: https://data.worldbank.org (accessed on 1 June 2023).

- UN-Habitat. Annual Report 2010; United Nations: New York, NY, USA, 2010; ISBN 978-92-1-132336-8. Available online: https://unhabitat.org/annual-report-2021 (accessed on 1 June 2023).

- Michel, D.; Klimes, M.; Eriksson, M. Climate Change and (In)Security in Transboundary River Basins. In Handbook of Security and the Environment; Edward Elgar: Northampton, MA, USA, 2021; pp. 62–75. [Google Scholar]

- Alrashed, F.; Asif, M. Climatic Classifications of Saudi Arabia for Building Energy Modelling. Energy Procedia 2015, 75, 1425–1430. [Google Scholar] [CrossRef]

- Al-Maamary, H.M.S.; Kazem, H.A.; Chaichan, M.T. Climate Change: The Game Changer in the Gulf Cooperation Council Region. Renew. Sustain. Energy Rev. 2017, 76, 555–576. [Google Scholar] [CrossRef]

- Tolba, M.K.; Saab, N.W. Arab environment: Climate change. In 2009 Report of The Arab Forum for Environment and Development; Tolba, M.K., Saab, N.W., Eds.; AFED: Beirut, Lebanon, 2009; Available online: http://www.afedonline.org/afedreport09/Full%20English%20Report.pdf (accessed on 7 April 2019).

- Azamathulla, H.; Rathnayake, U.; Shatnawi, A. Gene Expression Programming and Artificial Neural Network to Estimate Atmospheric Temperature in Tabuk, Saudi Arabia. Appl. Water Sci. 2018, 8, 184. [Google Scholar] [CrossRef]

- Nassar, M.; Bakr, R.; Abdeldayem, M.; El-Barky, N.; Kotb, T. Seasonal Abundance of Mosquitoes in Jizan Province. Egypt. Acad. J. Biol. Sci. Entomol. 2016, 9, 1–13. [Google Scholar] [CrossRef]

- Lee, C.-C.; Olasehinde-Williams, G.; Akadiri, S.S. Geopolitical Risk and Tourism: Evidence from Dynamic Heterogeneous Panel Models. Int. J. Tour. Res. 2021, 23, 26–38. [Google Scholar] [CrossRef]

- Caldara, D.; Iacoviello, M. Measuring Geopolitical Risk. Am. Econ. Rev. 2022, 112, 1194–1225. [Google Scholar] [CrossRef]

- Olasehinde-Williams, G.O.; Balcilar, M. The Effect of Geopolitical Risks on Insurance Premiums. J. Public Aff. 2022, 22, e2387. [Google Scholar] [CrossRef]

- Li, B.; Chang, C.-P.; Chu, Y.; Sui, B. Oil Prices and Geopolitical Risks: What Implications are Offered via Multi-Domain Investigations? Energy Environ. 2020, 31, 492–516. [Google Scholar] [CrossRef]

- Dhifaoui, Z.; Khalfaoui, R.; Abedin, M.Z.; Shi, B. Quantifying Information Transfer Among Clean Energy, Carbon, Oil, and Precious Metals: A Novel Transfer Entropy-Based Approach. Financ. Res. Lett. 2022, 49, 103138. [Google Scholar] [CrossRef]

- Dhifaoui, Z.; Khalfaoui, R.; Jabeur, S.B.; Abedin, M.Z. Exploring the Effect of Climate Risk on Agricultural and Food Stock Prices: Fresh Evidence from EMD-Based Variable-Lag Transfer Entropy Analysis. J. Environ. Manag. 2023, 326, 116789. [Google Scholar] [CrossRef]

- Dibiasi, A.; Abberger, K.; Siegenthaler, M.; Sturm, J.-E. The Effects of Policy Uncertainty on Investment: Evidence from the Unexpected Acceptance of a Far-Reaching Referendum in Switzerland. Eur. Econ. Rev. 2018, 104, 38–67. [Google Scholar] [CrossRef]

- Xue, C.; Shahbaz, M.; Ahmed, Z.; Ahmad, M.; Sinha, A. Clean Energy Consumption, Economic Growth, and Environmental Sustainability: What is the Role of Economic Policy Uncertainty? Renew. Energy 2022, 184, 899–907. [Google Scholar] [CrossRef]

- Yu, M.; Wang, N. The Influence of Geopolitical Risk on International Direct Investment and Its Counter-Measures. Sustainability 2023, 15, 2522. [Google Scholar] [CrossRef]

- Eksi, O.; Tas, B.K.O. Time-Varying Effect of Uncertainty Shocks on Unemployment. Econ. Model. 2022, 110, 105810. [Google Scholar] [CrossRef]

- Azad, N.F.; Serletis, A. Spillovers of U.S. Monetary Policy Uncertainty on Inflation-Targeting Emerging Economies. Emerg. Mark. Rev. 2021, 51, 100875. [Google Scholar] [CrossRef]

- Haque, Q.; Magnusson, L.M. Uncertainty Shocks and Inflation Dynamics in the U.S. Econ. Lett. 2021, 202, 109825. [Google Scholar] [CrossRef]

- Chiang, T.C. The Effects of Economic Uncertainty, Geopolitical Risk, and Pandemic Upheaval on Gold Prices. Resour. Policy 2022, 76, 102546. [Google Scholar] [CrossRef]

- Jiao, Y.; Xiao, X.; Bao, X. Economic Policy Uncertainty, Geopolitical Risks, Energy Output, and Ecological Footprint: Empirical Evidence from China. Energy Rep. 2022, 8, 324–334. [Google Scholar] [CrossRef]

- Gupta, R.; Gozgor, G.; Kaya, H.; Demir, E. Effects of Geopolitical Risks on Trade Flows: Evidence from the Gravity Model. Eurasian Econ. Rev. 2019, 9, 515–530. [Google Scholar] [CrossRef]

- Li, Y.; Huang, J.; Chen, J. Dynamic Spillovers of Geopolitical Risks and Gold Prices: New Evidence from 18 Emerging Economies. Resour. Policy 2021, 70, 101938. [Google Scholar] [CrossRef]

- Li, Y.; Huang, J.; Gao, W.; Zhang, H. Analyzing the Time-Frequency Connectedness Among Oil, Gold Prices, and BRICS Geopolitical Risks. Resour. Policy 2021, 73, 102134. [Google Scholar] [CrossRef]

- Su, C.-W.; Khan, K.; Tao, R.; Nicoleta-Claudia, M. Does Geopolitical Risk Strengthen or Depress Oil Prices and Financial Liquidity? Evidence from Saudi Arabia. Energy 2019, 187, 116003. [Google Scholar] [CrossRef]

- Kannadhasan, M.; Das, D. Do Asian Emerging Stock Markets React to International Economic Policy Uncertainty and Geopolitical Risk Alike? A Quantile Regression Approach. Financ. Res. Lett. 2020, 34, 101276. [Google Scholar] [CrossRef]

- Hoque, M.E.; Zaidi, M.A.S. Global and Country-Specific Geopolitical Risk Uncertainty and Stock Return of Fragile Emerging Economies. Borsa Istanb. Rev. 2020, 20, 197–213. [Google Scholar] [CrossRef]

- Yang, K.; Wei, Y.; Li, S.; He, J. Geopolitical Risk and Renewable Energy Stock Markets: An Insight from Multiscale Dynamic Risk Spillover. J. Clean. Prod. 2021, 279, 123429. [Google Scholar] [CrossRef]

- Smales, L.A. Geopolitical Risk and Volatility Spillovers in Oil and Stock Markets. Q. Rev. Econ. Financ. 2021, 80, 358–366. [Google Scholar] [CrossRef]

- Sohag, K.; Hammoudeh, S.; Elsayed, A.H.; Mariev, O.; Safonova, Y. Do Geopolitical Events Transmit Opportunity or Threat to Green Markets? Decomposed Measures of Geopolitical Risks. Energy Econ. 2022, 111, 106068. [Google Scholar] [CrossRef]

- Flouros, F.; Pistikou, V.; Plakandaras, V. Geopolitical Risk as a Determinant of Renewable Energy Investments. Energies 2022, 15, 1498. [Google Scholar] [CrossRef]

- Li, S.; Tu, D.; Zeng, Y.; Gong, C.; Yuan, D. Does Geopolitical Risk Matter in Crude Oil and Stock Markets? Evidence from Disaggregated Data. Energy Econ. 2022, 113, 106191. [Google Scholar] [CrossRef]

- Gong, X.; Xu, J. Geopolitical Risk and Dynamic Connectedness Between Commodity Markets. Energy Econ. 2022, 110, 106028. [Google Scholar] [CrossRef]

- Umar, M.; Riaz, Y.; Yousaf, I. Impact of Russian-Ukraine War on Clean Energy, Conventional Energy, and Metal Markets: Evidence from Event Study Approach. Resour. Policy 2022, 79, 102966. [Google Scholar] [CrossRef]

- Steffen, B.; Patt, A. A Historical Turning Point? Early Evidence on How the Russia-Ukraine War Changes Public Support for Clean Energy Policies. Energy Res. Soc. Sci. 2022, 91, 102758. [Google Scholar] [CrossRef]

- Oloko, T.; Olaniran, A.; Lasisi, L. Hedging Global and Country-Specific Geopolitical Risks with South Korean Stocks: A Predictability Approach. Asian Econ. Lett. 2021, 2, 24418. [Google Scholar] [CrossRef]

- Bilgin, M.H.; Gozgor, G.; Karabulut, G. How Do Geopolitical Risks Affect Government Investment? An Empirical Investigation. Def. Peace Econ. 2020, 31, 550–564. [Google Scholar] [CrossRef]

- Zhang, Z.; He, M.; Zhang, Y.; Wang, Y. Geopolitical Risk Trends and Crude Oil Price Predictability. Energy 2022, 258, 124824. [Google Scholar] [CrossRef]

- Cai, Y.; Wu, Y. Time-Varying Interactions between Geopolitical Risks and Renewable Energy Consumption. In ADBI Working Paper; Asian Development Bank Institute: Tokyo, Japan, 2020; p. 1089. Available online: https://www.adb.org/publications/time-varyinginteractionsbetween-geopolitical-risks-renewable-energy-consumption (accessed on 1 June 2023).

- Sweidan, O.D. The Geopolitical Risk Effect on US Renewable Energy Deployment. J. Clean. Prod. 2021, 293, 126189. [Google Scholar] [CrossRef]

- Demiralay, S.; Kilincarslan, E. The Impact of Geopolitical Risks on Travel and Leisure Stocks. Tour. Manag. 2019, 75, 460–476. [Google Scholar] [CrossRef]

- Cheng, C.H.J.; Chiu, C.-W.J. How Important Are Global Geopolitical Risks to Emerging Countries? Int. Econ. 2018, 156, 305–325. [Google Scholar] [CrossRef]

- Zhao, W.; Zhong, R.; Sohail, S.; Majeed, M.; Ullah, S. Geopolitical Risks, Energy Consumption, and CO2 Emissions in BRICS: An Asymmetric Analysis. Environ. Sci. Pollut. Res. 2021, 28, 39668–39679. [Google Scholar] [CrossRef]

- Anasori, E.; Kucukergin, K.G.; Soliman, M.; Tulucu, F.; Altinay, L. How Can the Subjective Well-being of Nurses Be Predicted? Understanding the Mediating Effect of Psychological Distress, Psychological Resilience, and Emotional Exhaustion. J. Serv. Theory Pract. 2022, 32, 762–780. [Google Scholar] [CrossRef]

- Goes, C.; Bekkers, E. The Impact of Geopolitical Conflicts on Trade, Growth, and Innovation: An Illustrative Simulation Study. Available online: https://cepr.org/voxeu/columns/impact-geopolitical-conflicts-trade-growth-and-innovation-illustrative-simulation (accessed on 1 June 2023).

- Sowby, R.B.; Capener, A. The Influence of Precipitation on the Energy Footprint of Denver’s Water Supply: A 20-year Analysis and Implications for Climate Change. Energy Nexus 2023, 9, 100166. [Google Scholar] [CrossRef]

- Jin, Y.; Zhao, H.; Bu, L.; Zhang, D. Geopolitical Risk, Climate Risk, and Energy Markets: A Dynamic Spillover Analysis. Int. Rev. Financ. Anal. 2023, 87, 102597. [Google Scholar] [CrossRef]

- Shen, L.; Hong, Y. Can Geopolitical Risks Excite Germany Economic Policy Uncertainty: Rethinking in the Context of the Russia-Ukraine Conflict. Financ. Res. Lett. 2023, 51, 103420. [Google Scholar] [CrossRef]

- Soltani, H.; Triki, M.; Ghandri, M.; Abderzag, F. Does Geopolitical Risk and Financial Development Matter for Economic Growth in MENA Countries? J. Int. Stud. 2021, 14, 103–116. [Google Scholar] [CrossRef]

- Le, A.-T.; Tran, T.P. Does Geopolitical Risk Matter for Corporate Investment? Evidence from Emerging Countries in Asia. J. Multinatl. Financ. Manag. 2021, 62, 100703. [Google Scholar] [CrossRef]

- Hailemariam, A.; Ivanovski, K. The Impact of Geopolitical Risk on Tourism. Curr. Issues Tour. 2021, 24, 3134–3140. [Google Scholar] [CrossRef]

- Alsagr, N.; Almazor, S.F.V.H. Oil Rent, Geopolitical Risk, and Banking Sector Performance. Int. J. Energy Econ. Policy 2020, 10, 305–314. [Google Scholar] [CrossRef]

- Olanipekun, I.O.; Alola, A.A. Crude Oil Production in the Persian Gulf amidst Geopolitical Risk, Cost of Damage, and Resources Rents: Is There Asymmetric Inference? Resour. Policy 2020, 69, 101873. [Google Scholar] [CrossRef]

- Akadiri, S.S.; Eluwole, K.K.; Akadiri, A.C.; Avci, T. Does Causality between Geopolitical Risk, Tourism, and Economic Growth Matter? Evidence from Turkey. J. Hosp. Tour. Manag. 2020, 43, 273–277. [Google Scholar] [CrossRef]

- Anser, M.K.; Syed, Q.R.; Apergis, N. Does Geopolitical Risk Escalate CO2 Emissions? Evidence from the BRICS Countries. Environ. Sci. Pollut. Res. 2021, 28, 48011–48021. [Google Scholar] [CrossRef]

- Anser, M.K.; Syed, Q.R.; Lean, H.H.; Alola, A.A.; Ahmad, M. Do Economic Policy Uncertainty and Geopolitical Risk Lead to Environmental Degradation? Evidence from Emerging Economies. Sustainability 2021, 13, 5866. [Google Scholar] [CrossRef]

- Adams, S.; Adedoyin, F.; Olaniran, E.; Bekun, F.V. Energy Consumption, Economic Policy Uncertainty, and Carbon Emissions: Causality Evidence from Resource-rich Economies. Econ. Anal. Policy 2020, 68, 179–190. [Google Scholar] [CrossRef]

- Alsagr, N.; Hemmen, S. The Impact of Financial Development and Geopolitical Risk on Renewable Energy Consumption: Evidence from Emerging Markets. Environ. Sci. Pollut. Res. 2021, 28, 25906–25919. [Google Scholar] [CrossRef] [PubMed]

- Mohsin Hashmi, S.; Bhowmik, R.; Inglesi-Lotz, R.; Syed, Q. Investigating the Environmental Kuznets Curve Hypothesis amidst Geopolitical Risk: Global Evidence using Bootstrap ARDL Approach. Environ. Sci. Pollut. Res. 2021, 29, 24049–24062. [Google Scholar] [CrossRef]

- Tian, Y.; Wang, Y.; Zhang, Z.; Sun, P. Fourier-Domain Transfer Entropy Spectrum. Phys. Rev. Res. 2021, 3, L042040. [Google Scholar] [CrossRef]

- James, R.G.; Barnett, N.; Crutchfield, J.P. Information Flows? A Critique of Transfer Entropies. Phys. Rev. Lett. 2016, 116, 1–6. [Google Scholar] [CrossRef]

- Wyner, A.D. A Definition of Conditional Mutual Information for Arbitrary Ensembles. Inf. Control. 1978, 38, 51–59. [Google Scholar] [CrossRef]

- Bandt, C.; Pompe, B. Permutation Entropy: A Natural Complexity Measure for Time Series. Phys. Rev. Lett. 2002, 88, 174102. [Google Scholar] [CrossRef]

- Jafari-Mamaghani, M.; Tyrcha, J. Transfer Entropy Expressions for a Class of Non-Gaussian Distributions. Entropy 2014, 16, 1743–1755. [Google Scholar] [CrossRef]

- Liu, A.; Chen, J.; Yang, S.Y.; Hawkes, A.G. The Flow of Information in Trading: An Entropy Approach to Market Regimes. Entropy 2020, 22, 1064. [Google Scholar] [CrossRef]

- Papana, A.; Kyrtsou, C.; Kugiumtzis, D.; Diks, C. Detecting Causality in Non-Stationary Time Series Using Partial Symbolic Transfer Entropy: Evidence in Financial Data. Comput. Econ. 2016, 47, 341–365. [Google Scholar] [CrossRef]

- Acheampong, A.O.; Opoku, E.E.O.; Aluko, O.A. The Roadmap to Net-zero Emission: Do Geopolitical Risk and Energy Transition Matter? J. Public Aff. 2023, e2882. [Google Scholar] [CrossRef]

- Shabir, M.; Jiang, P.; Shahab, Y.; Wang, P. Geopolitical, Economic Uncertainty and Bank Risk: Do CEO Power and Board Strength Matter? Int. Rev. Financ. Anal. 2023, 87, 102603. [Google Scholar] [CrossRef]

- Sharif, A.; Aloui, C.; Yarovaya, L. COVID-19 Pandemic, Oil Prices, Stock Market, Geopolitical Risk and Policy Uncertainty Nexus in the US Economy: Fresh Evidence from the Wavelet-based Approach. Int. Rev. Financ. Anal. 2020, 70, 101496. [Google Scholar] [CrossRef]

- Long, S.; Lucey, B.; Kumar, S.; Zhang, D.; Zhang, Z. Climate Finance: What We Know and What We Should Know? J. Clim. Financ. 2022, 1, 100005. [Google Scholar] [CrossRef]

- Simionescu, M.; Radulescu, M.; Balsalobre-Lorente, D.; Cifuentes-Faura, J. Pollution, Political Instabilities and Electricity Price in the CEE Countries During the War Time. J. Environ. Manag. 2023, 343, 118206. [Google Scholar] [CrossRef]

- Vakulchuk, R.; Overland, I.; Scholten, D. Renewable Energy and Geopolitics: A Review. Renew. Sustain. Energy Rev. 2020, 122, 109547. [Google Scholar] [CrossRef]

- Li, H.; Liu, Y.; Xu, B. Does Target Country’s Climate Risk Matter in Cross-border M&A? The Evidence in the Presence of Geopolitical Risk. J. Environ. Manag. 2023, 344, 118439. [Google Scholar]

- Omar, M.E.D.M.; Moussa, A.M.A.; Hinkelmann, R. Impacts of Climate Change on Water Quantity, Water Salinity, Food Security, and Socioeconomy in Egypt. Water Sci. Eng. 2021, 14, 17–27. [Google Scholar] [CrossRef]

- Ahmed, B. Who Takes Responsibility for the Climate Refugees? Int. J. Clim. Change Strateg. Manag. 2017, in press. [Google Scholar] [CrossRef]

- Balsari, C.; Dresser, S.; Leaning, J. Climate Change, Migration, and Civil Strife. Curr. Environ. Health Rep. 2020, 7, 404–414. [Google Scholar] [CrossRef] [PubMed]

- Methmann, C.; Oels, A. From “fearing” to “empowering” climate refugees: Governing climate-induced migration in the name of resilience. Secur. Dialogue 2015, 46, 51–68. [Google Scholar] [CrossRef]

- Tiwari, A.K.; Abakah, E.J.A.; Le, T.-L.; la Hiz, D.I.L. Markov-Switching Dependence Between Artificial Intelligence and Carbon Price: The Role of Policy Uncertainty in the Era of the 4th Industrial Revolution and the Effect of COVID-19 Pandemic. Technol. Forecast. Soc. Change 2021, 163, 120434. [Google Scholar] [CrossRef]

- Dhifaoui, Z. Robust to Noise and Outliers Estimator of Correlation Dimension. Chaos Solitons Fractals 2016, 93, 169–174. [Google Scholar] [CrossRef]

- Dhifaoui, Z. Statistical Moments of Gaussian Kernel Correlation Sum and Weighted Least Square Estimator of Correlation Dimension and Noise Level. J. Stat. Plann. Inference 2018, 193, 55–69. [Google Scholar] [CrossRef]

- Barunik, J.; Kley, T. Quantile Coherency: A General Measure for Dependence Between Cyclical Economic Variables. Econom. J. 2019, 22, 131–152. [Google Scholar] [CrossRef]

- Antonakakis, N.; Chatziantoniou, I.; Gabauer, D. Refined Measures of Dynamic Connectedness Based on TVP-VAR. MPRA 2017, 78282, 1–15. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Author | Country/ Period | Studies/Variables | Methods | Finding |

|---|---|---|---|---|

| [38] | 1985–2015/18 countries | Public investment (GI), geopolitical risk (GPR), gross domestic product per individual, inhabitants, traffic accessibility, aging reliance, urban population, capital accumulation, FDI, cumulative debt, and deficits in the budget | Fixed-effects, Least squares dummy variable-corrected (LSDVC) method | GPR incentivizes GI |

| [44] | 1985–2019/ BRIC | Energy use (EC), government stability (GS), geopolitical risk index (GPR), and the gross domestic product for each person (GDP) are some of the metrics used to measure environmental impact. | NARDL | In Russia as well as South Africa, GPR rises cause CO2 levels to soar, in India, China, and South Africa, GPR drops cause CO2 levels to go up. |

| [45] | 2005M1/ 2017M12 16 selected countries | Demand for travel (Q), average income per person (Y), relative prices (P), international travel (IT), exchange rate (EX), and geopolitical risk (GPR) | AMG and common correlated effects mean group (CCEMG) | GDP impedes Q |

| [47] | US (Denver) 1995/2014 | The influence of precipitation on the energy footprint of Denver’s water supply: A 20-year analysis and implications for climate change | Regression model | 1 cm decrease in annual precipitation equates to 275,000 kWh of additional energy use |

| [48] | 13 countries 2002/2022 | Geopolitical risk, climate risk, and energy markets: A dynamic spillover analysis | BEKK-GARCH model | Significant static spillovers between energy, climate risk, and geopolitical risk |

| [49] | Germany 2023 | Uncertainty in Germany’s economic policy due to geopolitical risks: Reevaluating in light of the war between Russia and Ukraine | Time-varying Granger-causality tests | Confusion about Germany’s economic strategy may be exacerbated by rising geopolitical risks. |

| [50] | 1995–2020 15 MENA countries | Foreign direct investment, financial development, inflation, trade openness, and the geopolitical risk index contribute to a nation’s economic output per person (GDP). | Panel vector auto-regression | GPR has a negative impact on GDP, but financial development has a positive impact in certain nations. |

| [51] | 1995–2018 9 Asian countries | Capital spending (CAPX/ASSET), power of legislation, investing liberty, expansion of GDP, and inflation all go into the geopolitical risk index (GPR). | Generalized method of moments + two-stage least-squares method | GPR has a significant impact on corporate expenditure in China as well as Russia, but not as much in India or Turkey. |

| [52] | January 1999–August 2020/U.S. | Worldwide manufacturing capacity, purchasing power, and net spending on touristic exports and imports (TNX) + geopolitical risk. | Structural vector auto regression (SVAR) | GPR negatively affects TNX |

| [53] | 1998–2017/ Emerging Nations | Fuel rents, gross domestic product (GDP), geopolitical risk index (GPR), and exchange value-defaulted loans and monetary deposits | Fixed effect | GPR plunges banking sector performance |

| [54] | 1975–2018/ Persian Gulf | Petroleum prices, rents related to natural resources (RENT), average damage cost (ACOD), and oil generation | Nonlinear autoregressive distributed lag (NARDL) | PROD is adversely affected by beneficial shocks to GPR and ACOD, while negative shocks adversely impact PROD and PRICE. |

| [55] | 1985Q12017Q4/ Turkey | The real gross domestic product, the number of tourists entering the country, and the geopolitical risk index (GPR) | Toda and Yamamoto causality test (1995) | GPR adversely influences the real gross domestic product and TOUR; there is an a single-direction relationship. |

| [56] | 1985–2015/ BRIC | The world’s inhabitants (POP), non-renewable energy (ENE), renewable energy (REN), carbon dioxide gases (CO2), gross domestic product for each person (GDP), and geopolitical risk index (GPR) | AMG | GPR, GDP, POP, and ENE increase CO2 while REN impedes CO2 |

| [57] | 1995–2015/ Brazil, Mexico, Russia, Colombia, and China | The economic policy ambiguity index (EPU), geopolitical risk index (GPR), non-renewable energy (EN), renewable energy (REN), footprint on the environment (EF), and the gross domestic product for every person (GDP) | Co-integration, FMOLS, DOLS, AMG | Whenever GPR and GDP reduce EF, EPU and EN increase it. |

| [58] | 1996–2017/ Resource-rich countries | CO2 emissions (CO2), Geopolitical risk index (GPR), uncertainty in economic policy (EPU), consumption of energy (ENC), real gross domestic product for each person (RGDP) | Kao cointegration, PMG-ARDL causality test | ENC and RGDP increase CO2; a bidirectional causality CO2 ↔ ENC, RGD ↔PEPU, RGDP ↔ CO2; a unidirectional causality CO2 → GPR |

| [59] | 1996–2015/ Developing countries | GDP per capita (GDPPC), private credit (PCD), bank credit (BCB), domestic credit (DCP), stock market turnover rates (TOR), geopolitical risk index, and consumer price index (CPI) | Two-step system GMM | GPR and expansion of finances lead to a boost in REC. |

| [60] | 1970–2015/ Global Level | World carbon dioxide emissions (CO2), geopolitical risk index (GPR), world GDP (GGDP), world energy consumption (GEN) | Bootstrap ARDL | EKC is valid; GPR negatively affects CO2 in the short run but positively affects it in the long run |

| Index | Symbol | Description |

|---|---|---|

| Geopolitical risk index | GPRAS | Reflects automated text-search results of the electronic archives of The New York Times, Chicago Tribune, and The Washington Post newspapers. |

| Total precipitation | PRECTOT | The total precipitation in mm per day. |

| The relative humidity | RH2M | The relative humidity measured at two meters is given in percentage. |

| The temperature | T2M | The temperature was measured at two meters. |

| The wind direction | WD50M | The wind direction was measured at 50 m in degree. |

| The wind speed | WS50M | The wind speed is measured at 50 m in meters per second. |

| GPRAS | PRECTOT | RH2M | T2M | WD50M | WS50M | |

|---|---|---|---|---|---|---|

| Mean | 0.224 | 0.110 | 27.218 | 23.261 | 130.328 | 5.789 |

| Median | 0.150 | 0.000 | 23.815 | 24.455 | 88.940 | 5.800 |

| Min | 0.010 | 0.000 | 10.560 | 5.690 | 0.250 | 4.430 |

| Max | 3.420 | 3.040 | 69.690 | 36.440 | 359.250 | 7.480 |

| Std.Dev. | 0.306 | 0.253 | 13.796 | 8.603 | 117.318 | 0.459 |

| Skewness | 52.134 | 43.783 | 2.172 | 1.581 | 2.395 | 3.275 |

| Kurtosis | 6.099 | 5.006 | 0.604 | −0.190 | 0.893 | 0.069 |

| JB test | 5.126 × 104 (0.000) | 3.527 × 104 (0.000) | 42.952 (0.001) | 43.160 (0.001) | 71.148 (0.001) | 1.911 (0.355) |

| ADF test | −7.515 (0.001) | −16.856 (0.001) | −3.426 (0.001) | −2.070 (0.037) | −11.086 (0.001) | −1.120 (0.241) |

| Time Series | Variance as a Percentage of Original Time Series | Main Scales | ||

|---|---|---|---|---|

| H | L | R | ||

| GPRAS | 89.306 | 2.585 | 8.107 | Short-term; long-term |

| PRECTOT | 61.210 | 29.520 | 9.269 | Short-term; medium-term; long-term |

| RH2M | 1.858 | 83.956 | 14.184 | Medium-term; long-term |

| T2M | 3.314 | 92.95 | 3.735 | Medium-term |

| WD50M | 99.729 | 0.255 | 0.014 | Short-term |

| WS50M | 85.282 | 8.838 | 5.878 | Short-term; medium-term; long-term |

| Percentage of Information Flows | |||

|---|---|---|---|

| Pairs of Time Series | Short-Term Scale | Medium-Term Scale | Long-Term Scale |

| GPRAS → PRECTOT | 0.222 | 0.346 | 0.029 |

| PRECTOT → GPRAS | 0.556 | 0.376 | 0.033 |

| GPRAS → RH2M | 5.268 | 0.087 | 2.378 |

| RH2M → GPRAS | 4.502 | 0.436 | 0.657 |

| GPRAS → T2M | 0.382 | 0.042 | 0.014 |

| T2M → GPRAS | 0.542 | 0.028 | 0.028 |

| GPRAS → WD50M | 4.121 | 0.066 | 0.028 |

| WD50M → GPRAS | 5.009 | 0.066 | 0.028 |

| GPRAS → WS50M | 0.454 | 0.065 | 1.214 |

| WS50M → GPRAS | 0.454 | 0.063 | 0.339 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dhifaoui, Z.; Ncibi, K.; Gasmi, F.; Alqarni, A.A. The Nexus between Climate Change and Geopolitical Risk Index in Saudi Arabia Based on the Fourier-Domain Transfer Entropy Spectrum Method. Sustainability 2023, 15, 13579. https://doi.org/10.3390/su151813579

Dhifaoui Z, Ncibi K, Gasmi F, Alqarni AA. The Nexus between Climate Change and Geopolitical Risk Index in Saudi Arabia Based on the Fourier-Domain Transfer Entropy Spectrum Method. Sustainability. 2023; 15(18):13579. https://doi.org/10.3390/su151813579

Chicago/Turabian StyleDhifaoui, Zouhaier, Kaies Ncibi, Faicel Gasmi, and Abulmajeed Abdallah Alqarni. 2023. "The Nexus between Climate Change and Geopolitical Risk Index in Saudi Arabia Based on the Fourier-Domain Transfer Entropy Spectrum Method" Sustainability 15, no. 18: 13579. https://doi.org/10.3390/su151813579

APA StyleDhifaoui, Z., Ncibi, K., Gasmi, F., & Alqarni, A. A. (2023). The Nexus between Climate Change and Geopolitical Risk Index in Saudi Arabia Based on the Fourier-Domain Transfer Entropy Spectrum Method. Sustainability, 15(18), 13579. https://doi.org/10.3390/su151813579