1. Introduction

The COVID-19 pandemic has had profound impacts on the global economy. The governments’ decision worldwide to impose mobility restrictions to curb virus transmission has led to sluggish economic activities, where the global GDP shrunk by 3.41% in 2020. It remarks the biggest fall in the worldwide GDP in more than four decades. In addition to global GDP, several indicators show the COVID-19 crisis brought a magnitude of damage like never before. International trade dropped by −7.36% [

1], while industrial production fell by 6.8% [

2]. COVID-19 also reversed the decades of progress in poverty reduction. It is estimated that COVID-19 could increase the poverty level to that of 30 years ago. It will pose a severe challenge to end poverty by 2030 as stipulated in Sustainable Development Goals (SDGs) [

3].

Although COVID-19 has devastating effects on the global economy, there are opportunities for a greener world. Many governments and scholars have pushed for a green recovery. “Build back better” has been a buzzword for the past years. Despite all the publicity about the prospects for the green recovery, it is crucial to perform an empirical ‘reality check’ to see whether countries are living up to these expectations or missing this one-time opportunity. Hence, the objective of this study was to investigate to what extent the COVID-19 pandemic has shaped the green recovery trajectory in emerging economies. This study selected two countries as the cases, namely Indonesia and Vietnam. These two countries make good case studies for two reasons. Both countries represent emerging economies. It is essential to focus on emerging economies considering the wide variation in green recovery spending size between advanced and emerging economies. The Global Recovery Observatory documented that around USD 760 billion of global recovery spending (21.7% of total recovery spending) is considered green spending [

4].

On the contrary, many emerging economies budgeted a small share of their recovery spending for green targets. This is unsurprising given the limited budget faced by these countries. At the same time, the pandemic exacerbated the economic problems in developing countries, including debt distress [

5]. With a limited budget, the governments in many developing countries have to shift their focus from green spending to other primary priorities, such as increasing the health capacity to deal with the pandemic [

6]. Given the differences in a country’s economic and fiscal conditions between advanced and emerging economies, it is crucial to conduct an in-depth analysis of emerging countries. It will enable us to draw lessons learned from other countries because other emerging economies would inherit similar economic conditions.

The overall structure of this paper takes the form of seven sections. After the Introduction, the methodology used in this paper is explained. Then, this paper discusses the green recovery trajectory at the global level and the regional level. The following sections will discuss situations in Indonesia and Vietnam, respectively. It starts with a discussion of Indonesia and Vietnam’s recent economic growth and energy demand (

Section 4). This will provide background information before moving to a more in-depth discussion of Indonesia (

Section 5) and Vietnam (

Section 6). Specifically, we will focus on examining three aspects. Firstly, the current condition of the energy sector. Secondly, the energy transition target of the respective countries. And lastly, the alignment between the green recovery plan after the COVID-19 pandemic and the energy transition target. This paper concludes by discussing findings and lessons learned for other countries, especially how a country can reach the double goal of economic recovery and clean energy targets.

2. Methodology

As mentioned earlier, this paper attempts to investigate to what extent the COVID-19 pandemic has shaped the green recovery trajectory. Specifically, this paper explores the stimulus plans launched by emerging countries and whether the stimulus plans align with a country’s sustainable energy and climate targets. To this end, this study uses country case studies to identify similarities and differences between cases and to construct a causal mechanism for the phenomena. Furthermore, it also allows us to capture the details of each case. Lastly, it can help us gain a nuanced understanding of the respective country’s green recovery plans and trajectories.

As

Figure 1 shows, this study conducted a two-stage approach. The first step in the process was a desk study where we analyzed documents related to the COVID-19 fiscal stimulus at the global and national levels. The objective was to identify to what extent the fiscal stimulus plan launched by a government is directed toward green recovery. Documents used in the first stage are government documents and regulations, reports published by international organizations, and other credible sources. The result from the first stage was used to design the second stage, namely semi-structured interviews and focus group discussions (FGDs). This study interviewed key government figures, private sectors, and research institutes. Furthermore, the study also used data gathered from FGDs, where a number of officials from emerging economies were invited to discuss the stimulus plans launched by the respective governments.

3. Green Recovery Trajectory at the Global Level

The COVID-19 pandemic has presented a window of opportunity for a greener world. The connection between green transition prospects and the COVID-19 pandemic relates to two recent developments. The first is from the total primary energy supply (TPES). Unlike fossil fuel sectors, renewable energy (RE) appeared resilient throughout the pandemic. Globally, electricity generated from RE sources increased by 13%. It contributed to the growing share of renewable in total electricity generation from 27% in 2019 to 29% in the following year [

7]. At the regional level, the growing share of renewables was particularly vivid in Asia and Oceania. Renewable generation increased by 15% in the former and 18.5% in the latter [

8]. ASEAN Centre for Energy (ACE) reported that the Southeast Asia region added to the renewables capacity by 23.7%—making them the most dynamic region in renewables deployment. At the country level, 2020 also remarks on the expansion of RE in many advanced economies. The percentage of RE in the total electricity generation of the USA increased to 11.8%. Similarly, in Europe, the share of renewables in electricity demand increased from 21% to 23.7% [

7]. The completion of new wind and solar photovoltaic (PV) projects has driven the increasing contribution of renewable sources to total electricity generation over the past year. This is not only because renewables have low marginal operation costs and are generally dispatched before other sources of electricity [

9].

In addition to TPES, another indicator that shows the connection between the green energy transition and the pandemic is positive investment trends in RE projects. In 2020, investment in renewable power increased from USD 336 billion in the previous year to USD 359 billion. The momentum continued in 2021 as the figure rose to USD 367 billion [

10]. Several factors contribute to this phenomenon. These include improvements in the cost-competitiveness of RE [

11,

12]. Another factor is the increasing uncertainty in fossil fuels in recent years that forced some companies in fossil fuels to shift their investment in the energy sector from investing in fossil fuels to investing in RE [

13].

The drop in carbon emissions and the increasing demand for RE have raised optimism for green recovery post-COVID-19 pandemic. Many international organizations, such as the United Nations (UN), the World Bank, and International Monetary Fund (IMF), call for green recovery and ‘build back’. In April 2020, a green recovery alliance was established with the chair of the Environment Committee of the European Parliament aims to work together to ensure the recovery trajectory from the COVID-19 pandemic aligned with the climate target. The European Parliament also emphasizes the importance of incorporating the European Green Deal into the COVID-19 recovery plan [

14]. Public organizations and many private sector leaders advocate for a ‘green recovery’. The World Economic Forum (WEF), for instance, launched the Great Reset initiative, where one of the critical components is to ensure a greener world after the COVID-19 pandemic [

15]. The importance of green recovery is also increasingly relevant in the context of the 26th Conference of the Parties (COP 26) of the United Nations Framework Convention on Climate Change (UNFCCC), where many scholars also emphasize the importance of aligning the COVID-19 recovery plan with the climate target [

16,

17,

18,

19]. In addition, the green recovery plan is supported by the public. A survey conducted by UNDP with 1.2 million total respondents shows that most respondents agree that the climate target should be an integral part of a government’s recovery plan [

20]. The importance of green recovery is not only urged at the global level. At the regional level, many institutions and scholars call for green recovery in Southeast Asia. The Asian Development Bank (ADB) emphasized the importance of green recovery for Southeast Asia [

21]. This is not only to reduce the risk of the future pandemic but also to mitigate and adapt to any negative impact of climate change while increasing competitiveness and meeting Sustainable Development Goals (SDGs).

The importance of green recovery spending was also observed during the 2008 financial crisis. After the crisis, some advanced economies budgeted a substantial share of their recovery spending for green recovery [

22]. This includes spending to generate RE-related jobs, including construction, installation, and manufacturing. Several studies have shown the positive impacts of green fiscal expenditure [

23,

24]. It was found that every USD 1 million spent under the green American Recovery and Reinvestment Act created five new jobs [

25].

At the same time, the optimism for green recovery is also driven by the massive spending budgeted by governments around the world. In just two months since the pandemic, the size of economic packages launched by the governments was already ten times larger than the 2008 global financial crisis [

26]. Hence, it is unsurprising that the UN Secretary-General considers this a ‘rare and short window of opportunity to ensure a green recovery from the COVID-19 pandemic [

27]. It was also reported that by Q2 2021, the world’s 50 largest economies had allocated USD 380 billion to energy-related sustainable recovery policies, constituting 16% of all economic recovery packages and 2.3% of total fiscal support provided during the pandemic [

28]. Using a Green Recovery Database, OECD reported that green spending constitutes 17% of the total recovery spending in 43 countries [

29]. Using a database with more countries, the Global Recovery Observatory noted that around USD 970 billion of global recovery spending (31.2% of total recovery spending) is considered green spending [

4]. However, as previously mentioned, there is a wide variation in the size of green recovery spending between advanced and emerging economies. Using the case of Indonesia and Vietnam, the following two sections will explore these aspects.

4. COVID-19 and Energy Sector Development in Indonesia and Vietnam

The COVID-19 pandemic has stunned Indonesia’s economy. With the restrictions imposed on people’s mobility during the pandemic’s peak (mid-2020), Indonesia’s GDP fell by more than 5% in Q2 2020 and shrunk by −3.49% and −2.19% in the next two quarters (i.e., Q3 and Q4) of 2020. As Indonesia’s GDP contracted in two consecutive quarters, Indonesia was officially in an economic recession for the first time since the 1997 Asian Financial Crisis. However, with the reopening of economic activity in 2021, the economy started a gradual recovery. As a result, Indonesia has had positive GDP growth since Q2 2021.

Similar to Indonesia, Vietnam’s economy also suffered from the COVID-19 pandemic, especially in the early stage. Vietnam’s GDP growth dropped to 0.39% in Q2 2020. This growth was the lowest in more than 20 years. The country saw a rise in GDP growth in the subsequent quarters, reaching 2.69% and 4.48% in Q3 and Q4 2020, respectively. However, the delta variant that swept the country in 2021 had a devastating effect on Vietnam’s economy. For the first time in decades, the GDP contracted by 6.02% in Q3 2021. However, as the country managed to suppress virus transmission and opened the economy in mid-2021, Vietnam’s economy started to pick up. The GDP growth reached 5.22% in Q3 2021 and 5.05% in the subsequent quarter.

The COVID-19 pandemic has changed the growth path of these two countries. To understand differences in the growth path, this study compares the GDP using projections made before and after the pandemic.

Figure 2A,B reveal the actual GDP growth and two projections of GDP growth of Indonesia and Vietnam, respectively. As both subfigures show, the actual GDP was lower than the projection made before the pandemic. However, as the economy started to recover, the gap between forecasts before and after the pandemic narrowed. This is especially true for Indonesia, where the difference in projected CAGR for the economic growth made before and after the pandemic is marginal (see

Table 1).

Based on the post-COVID-19 growth paths explained above, one can forecast energy demand in both countries. For this study, the energy demand projection is modelled under the baseline scenario. In this case, it assumes that several factors that may affect energy demand are kept constant at the level of historical data. For example, the scenario assumes no policy interventions such as renewable energy and energy intensity/efficiency policy. This scenario also installed capacities from the Power Development Plan (PDP). As such, in this scenario, socio-economic parameters (e.g., population and economic growth) are the main factor that drives the country’s energy demand. This corresponds to the fact that energy demand in the region has been driven by strong economic growth [

33].

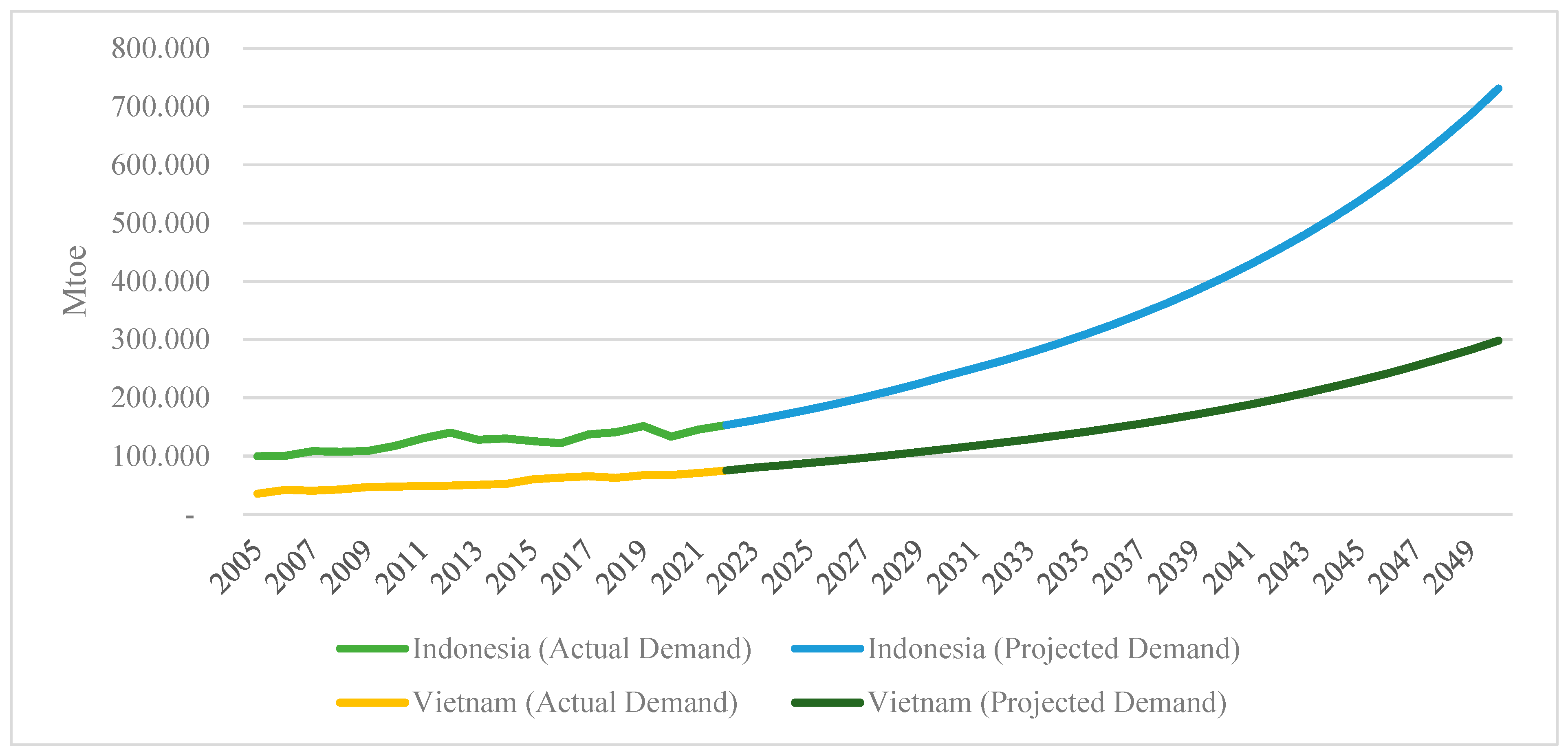

For economic growth, this study uses the post-COVID-19 growth projections. Meanwhile, for population growth, this study assumes that between 2020 and 2050, the CAGR for the population of Indonesia and Vietnam will be 0.6% and 0.4%, respectively. Based on these assumptions,

Figure 3 shows the projected energy demand of Indonesia and Vietnam. It is projected that Indonesia’s energy demand is projected to increase from 133.343 Mtoe in 2020 to 179.626 Mtoe, or approximately 34.7%. Driven by population and economic growth, the country’s energy demand is forecasted to increase more than fivefold to reach 731.058 Mtoe in 2050. Meanwhile, Vietnam’s energy demand is projected to grow by 30.4% between 2020 and 2025—from 67.435 Mtoe to 87.918 Mtoe. By 2050, the energy demand is projected to reach 298.091 Mtoe, or more than four times higher than in 2020.

In addition to the demand side, it is essential to discuss the supply side of the energy sector of Indonesia and Vietnam. Under the ‘baseline scenario’, the energy supply will follow the business as usual (BAU) assumption. In this case, traditional energy (oil, gas, and coal) is expected to account for more than 70% of a country’s energy supply (In 2020, fossil fuels accounted for 73% and 85% of the Total Energy Supply of Indonesia and Vietnam, respectively [

33].) However, as both countries have outlined the target for low-carbon energy transition, it is expected that the supply of fossil fuels will drop. Conversely, the supply of renewable energy is projected to increase to reach the growing energy demand. Both countries need to boost investment in RE projects to meet the energy demand while keeping climate targets (Both countries have outlined a target to increase the RE share in TPES. Indonesia set targets to increase the RE share to 23% in primary energy supply by 2025 and 31% by 2050, while Vietnam targets to increase the share to 15-20% in 2030 and 25-30% in 2050 [

33]). The following section will discuss each country’s efforts to accelerate the deployment of renewable energy and to what extent the stimulus plans align with a country’s sustainable energy and climate targets.

5. Case Study 1: Indonesia

Indonesia has many RE potentials, but its potential is largely untapped. Compared to other neighbouring countries, the RE progress in Indonesia is relatively slower. Data from ASEAN Centre for Energy (ACE) shows that the average annual growth of installed capacity from renewable sources over the last ten years is only 6.4%. Meanwhile, ASEAN’s average yearly growth of installed capacity from renewable sources reached 10.8%. The pandemic has worsened the progress of RE development. Despite the increase in the installed capacity from RE, the realization in 2020 was below the initial target. In 2020, the total installed capacity only achieved 10.467 MW, which was below the 10.843 MW target set. The COVID-19 pandemic contributed to this as it disrupted the implementation of many projects in RE. Initially, the government expected ten projects with more than 140 MW capacity to be completed in 2020. Nevertheless, only two projects entered the Commercial Operations Date phase, namely PLTA Hasang (hydroelectric power station) and PLTM Batu Bedil (Micro-Hydropower), with a total capacity of 14.7 MW [

34]. The disruption is not only triggered by the supply side problem, such as the mobility of people and materials but also caused by lower electricity demand throughout the pandemic.

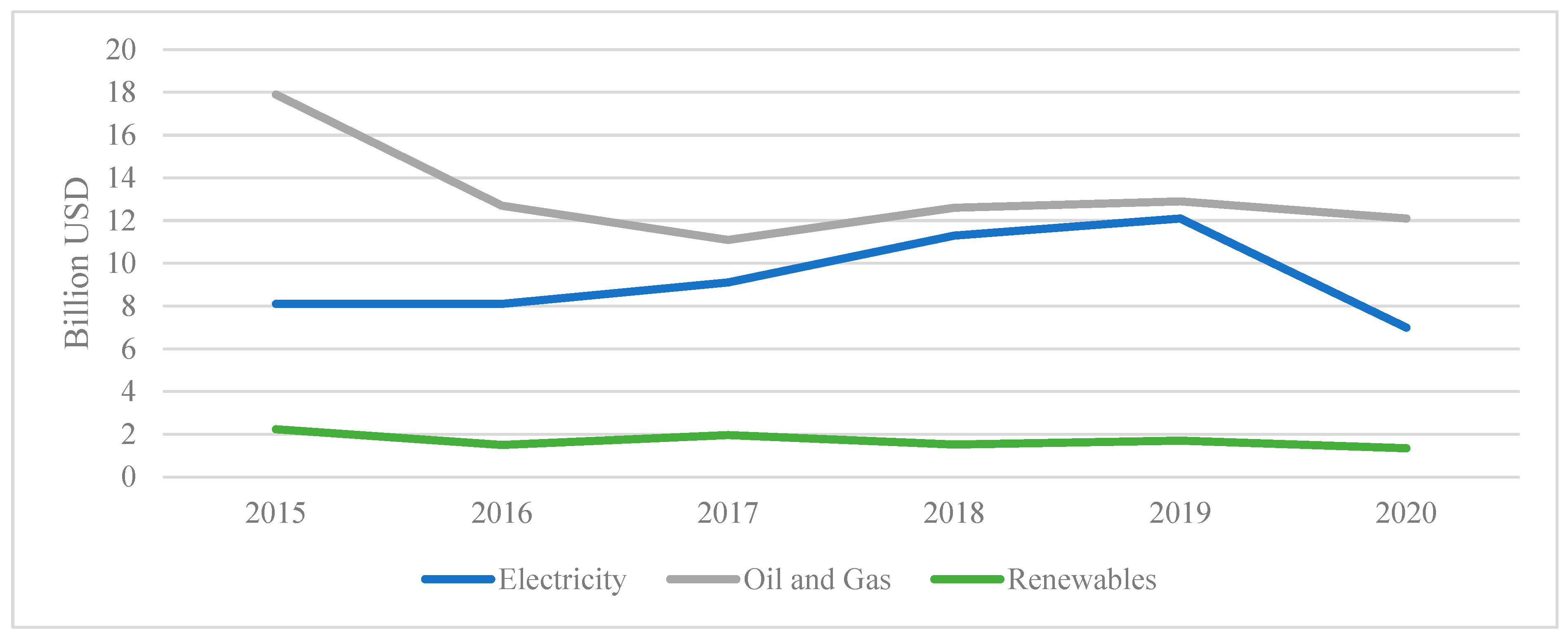

With regard to the investment in RE, the pandemic has brought uncertainty that forced the investors to hold the investment. As a result, investment in all types of energy in 2020 dropped, with the electricity sector experiencing the most significant drop in investment (see

Figure 4) [

34]. In addition to the lockdown policy that limits the mobility of people and goods to complete investment in electricity, the drop was caused by the cash flow problem faced by State Electricity Company / Perusahaan Listrik Negara (PLN) due to lower demand for electricity from nonsubsidized consumers, especially industry and commerce. As reported by PLN, their revenues in 2020 dropped to IDR 345 billion (USD 24.07 million) from IDR 359.6 billion (USD 25.09 million) in the previous year [

35]. The cash flow problem disrupts PLN’s capacity to invest in the electricity sector [

36]. Similar to the power sector, investment in RE experienced a drop in 2020 by 20.6%, from USD 1.7 billion in 2019 to USD 1.35 billion in 2020 [

36].

The COVID-19 pandemic also hurts the demand side as electricity consumption in 2020 dropped by 1.2% (from 245,518 GWh in 2019 to 242,598 in 2020) [

37]. The government’s decision to restrict people’s mobility changed the activity pattern. As a result, the consumption in all segments of electricity consumption dropped except for household customers. The consumption of this segment increased by 9% as people spent more time at home. The drop in the electricity demand further poses a problem in the electricity sector which has already experienced an excess supply problem over the past few years [

38].

As outlined in the Nationally Determined Contribution (NDC), Indonesia has set a target to increase the share of renewables to 23% in 2025 and 31% in 2030 [

39]. In line with this target, PLN (the state-run power company) recently published the Electricity Procurement Plan (RUPTL) for 2021–2030, where it sets a target that by 2030 RE will constitute more than 51.6% of the total additional installed capacity [

40]. However, the uncertainty about the duration of the pandemic could prevent Indonesia from achieving the energy transition target. As discussed in the preceding section, COVID-19 adversely affected the energy sector, including renewables. Despite the increasing share in installed capacity and the total primary energy mix, the realization in 2020 was still below the target outlined in the National Energy General Plan (RUEN). In 2020, the share of renewables in the total primary energy mix only reached 11.2%, which was lower than the RUEN target (23%) [

41]. While this is unsurprising given the devastating effects of the COVID-19 pandemic, there is a worry that Indonesia might miss the energy target without strong government support.

The COVID-19 recovery plan plays an important role in accelerating RE deployment and achieving the energy transition target. Nevertheless, an assessment of the national economic recovery program (PEN) suggests that the portion of the stimulus for the energy sector, especially RE, is limited. There is only one program: “electricity discount”, directly related to the energy sector. The main objective is to provide subsidies to low-income households—a 50% subsidy for the 900 VA category and a 100% for the 450 VA category [

42]. The government spent IDR 11.45 trillion (USD 798 million) and IDR 8.12 trillion (USD 566 million) on electricity subsidies under the PEN program in 2020 and 2021, respectively [

43,

44]. The government’s policy to provide electricity discounts for the fiscal years 2020 and 2021 led to an increase in the electricity subsidy, from IDR 52.7 trillion (USD 3.68 billion) in 2019 to IDR 61.1 trillion (USD 4.26 billion) in 2020 [

45]. While the electricity subsidy decreased to IDR 56.1 trillion (USD 3.91 billion) in 2021, the figure was higher than in 2019 [

46]. The government also provided some fiscal stimulus for firms, such as tax relief. However, this measure is intended for all firms regardless of the sector [

4].

With the current design of the recovery spending, Indonesia might be missing the opportunity to achieve both green recovery and energy mix targets. It only supports the status quo of energy production as the substantial fraction of spending related to the energy sector was directed to sectors with large consumption of fossil fuels, such as the transportation sector. The government injected capital into two state-owned enterprises (SOEs) in the transport sector, namely Garuda Indonesia and Kereta Api Indonesia (KAI), IDR 8.5 trillion (USD 593 million) and IDR 3.5 trillion (USD 244 million), respectively [

43]. In the future, the prospect of green recovery spending is likely to be more difficult as the government has outlined a target for fiscal consolidation to control a widening of the government budget deficits and ensure the sustainability of the fiscal conditions in the long run. While the public debt ratio remains below the 60% threshold in the medium term, the government has revealed a plan to return to the budget deficit ceiling (3% of GDP) by 2023 [

47]. Without a recovery in the tax revenue, the government has no choice but to pursue expenditure consolidation that could further limit the fiscal space to fund development projects, including green transitions.

6. Case Study 2: Vietnam

Many observers consider Vietnam a good example of how a country can boost the deployment of RE [

48,

49,

50]. The share of RE in the total installed capacity has continued to increase over the last ten years. In 2005, renewables only made up 38% of the total country’s installed capacity. In 2019, the share of RE increased to reach 48%. This remarkable increase was driven by the capacity of hydropower plants, which grew more than 15.11% annually on average. The country kept the momentum for RE development during the pandemic as the share of RE in the total installed capacity increased dramatically from 48% to 56%. Over the last year, the expansion of RE was driven by solar PV installations, which recorded an almost 200 times increase from only 86 MW in 2019 to 16,566 MW in 2020. The country installed more than 100,000 rooftop solar PV systems between 2019 and 2020 [

48]. With this rate, Vietnam ranked 3rd globally for the additional RE installed capacity in 2020. Only China and the USA deployed more installed solar PV during that period [

51].

The expansion of RE in Vietnam was not only driven by the increasing competitiveness of solar and wind to compete with fossil fuels but also attributed to strong government support [

48,

52,

53]. The government considers energy security indispensable in achieving sustainable development [

54]. In this case, given the great potential of RE for the country, the government has outlined a bold commitment to supporting RE development. As a result, Vietnam has emerged as a leader in RE, not only at the regional level but also at the global level.

As reflected in a draft version of Power Development Plan 8 (PDP 8), the country’s latest national power development plan, the government maintains the commitment to boost the deployment of RE in the country in the long term. The plan sets the country’s power plan for the next ten years (2021 to 2030). As can be seen from

Table 2 below, the PDP VIII (revised draft, September 2021) targets an increase in the renewable capacity to 58 GW or a 26% increase from the current installed capacity. The newest draft also put renewable sources at the center of the country’s power plant as the share of these sources is expected to be higher than the previous plan (PDP VII). In PDP VII, the country’s target on the share was 37.84%. Meanwhile, the share in the recent draft increased to 44.74%. By 2045, as outlined in PDP VIII, the share of RE is expected to reach 53.67%.

While the draft shows the country’s ambitions to achieve the clean energy transition, challenges remain including institutional issues, high investment costs, and policy and regulatory uncertainty, especially concerning Feed-in-Tariff (FIT) mechanism and other technical problems [

53]. These challenges become more severe as the country deals with the COVID-19 pandemic. One crucial question is how the government maintains support for the development of RE amid the disruptions brought by the COVID-19 pandemic.

It has been widely acknowledged that fiscal policy plays a crucial role in RE development, and green energy transition is fiscal policy. Nevertheless, similar to Indonesia, fiscal stimulus allocated towards the energy sector and RE is limited [

4] The government focuses on the most affected sectors and households, given the limited fiscal budget. Consequently, the majority of the economic relief package was spent on affected firms, including tax reliefs and land rentals deferrals (VND 65.9 trillion (USD 2.89 billion) or 52.02% of total fiscal spending in response to COVID-19) [

56]. The government also spent VND 12.7 trillion (USD 556.3 million) on cash transfer programs for vulnerable households [

56].

One notable program related to the energy sector is the government’s decision to cut the price of electricity to help vulnerable groups. While the main target of this policy is to support vulnerable groups, it has a positive implication for the electricity sector as it maintains the demand for electricity during the COVID-19 pandemic [

42]. It is reported that over the period of 2020, the government has spent VND 9.2 trillion (USD 403 million) on this policy [

55]. Nevertheless, this policy only supports the status quo of energy production without providing a new direction of recovery toward a greener energy production system. The authorities launched some policies to stimulate the RE sector, but the value is not quantifiable. These include the new FIT rates for solar projects and a new regulation that enables corporate power purchase agreements for rooftop solar projects [

57,

58,

59].

Despite the tremendous achievements of RE development in Vietnam over the last few years, there are no quantifiable fiscal measures for RE. The limited fiscal budget is one vital constraint that prevents the government from allocating more fiscal stimulus to the clean energy sector. Similar to other emerging economies, the COVID-19 pandemic caused disruptions in the country’s fiscal conditions. The economic slowdown at the national and global levels adversely affects revenue collection. Tax revenues as a share of GDP dropped from 18.6% to 16.9% [

60]. The World Bank reported a drop in the VAT on domestic and imported goods and services, especially in the hardest-hit sectors such as tourism [

60]. A shock in the global market also caused a lower tax revenue. Vietnam also saw a reduction in taxes on oil producers by 38.5% due to the shock in the global oil market [

60]. In addition to slower economic activity, the decrease in revenue was also attributed to tax reliefs (reductions and waivers) associated with the authority’s monetary support packages in response to COVID-19. It is projected that the revenue for 2021 and 2022 will remain low due to uncertainty brought about by the COVID-19 pandemic. At the same time, the government’s expenditure increased dramatically, driven by the economic relief packages launched by the authority since the start of the pandemic.

The revenue and expenditure growth imbalance led to a widening fiscal deficit from 3.36% of the GDP in 2019 to 3.39% in 2020. Consequently, over the same period, the government’s debt as a percentage of the GDP increased from 43% of the GDP to 46.6% [

56]. In the medium term, the government has outlined the plan to resume fiscal consolidation that was put on hold during the pandemic [

61]. Before the pandemic, fiscal consolidation successfully controlled public debt [

62]. It includes limiting fiscal expenditure while mobilizing additional tax revenues. As the size of expenditure will be increasingly limited, it is vital to improving expenditure quality, primarily using public investment programs. While the shape of the future public investment programs is yet to be announced, the government’s priority is reflected in the 2019/20 public investment composition. Apart from the transport sector, the public investment focused on the Ministry of Security and the Ministry of Agriculture and Rural Development (MARD) [

60].

7. Way Forward

Despite the ambitious climate target set by both Indonesia and Vietnam, the stimulus for the green energy transition is relatively limited. Both countries focused on helping the most vulnerable households and most affected firms. Hence, only electricity discount programs that have related to the energy sector. Limited green fiscal measure in both countries is unsurprising given the limited fiscal space posed by these two countries. In fact, the COVID-19 pandemic has exacerbated public fiscal budgets that may further limit the fiscal capacity to fund green projects required for achieving green energy transition targets in the future. Amidst the uncertainty and challenges brought by the pandemic, it is essential to balance between promoting economic recovery and achieving sustainable energy and climate targets. To this end, the authors suggest several policy recommendations as follows:

7.1. Green Fiscal Consolidation

Many developing countries have indicated a plan for fiscal consolidation. However, as the climate clock is ticking, balancing a government’s plans to maintain fiscal sustainability while keeping progress toward the climate targets intact is essential. In doing so, the government may consider incorporating a green perspective with fiscal consolidation efforts. Firstly, governments can mobilize additional revenues from the fossil fuels sector using a carbon tax policy. In the short term, this policy can generate fiscal space to improve fiscal conditions post the pandemic. This policy also offers incentives for households and firms to make cleaner choices, which could reduce carbon emissions in the long run. Several studies also show that this policy can increase investment and production of RE [

63]. Furthermore, additional fiscal revenues could be used to fund green public investment. This includes green energy, green transport, energy efficiency, and green R&D. These policy options are considered to have the possible benefit of stimulating the economy and facilitating energy transition [

17]. Recycling the additional revenues toward green investment can provide double dividends: reducing carbon emissions and creating fiscal spaces [

64]. As this policy has been implemented in more than 40 countries with various rates and mechanisms [

65], the importance of this policy is becoming more critical than ever in the post-pandemic world.

7.2. Green and Sustainability Bonds

Given the limited fiscal budget, it is crucial to consider using the capital market to finance green recovery. Over the past years, the world saw an increasing trend of raising funds from private investors using green bonds. Amidst the global pandemic, the Climate Bonds Initiative (CBI) records that green, social, and sustainability (GSS) bond issuance at the worldwide level stood at USD 700 billion. This remarks a 95% increase compared to the previous year, reaching USD 358 billion [

66]. While the trend is increasing, the potential is largely untapped, especially in emerging economies. In 2020, emerging economies only made up 16% of the total green bonds. This share is lower than the previous year, reaching 22% [

66]. In the medium term, considering the conducive environment for GSS bond issuance in emerging economies, the figure is projected to reach USD 100 billion by 2023 [

67]. Given the ample opportunities for this finance, a government must focus on addressing challenges that hinder the expansion of the green finance market in emerging economies.

7.3. Green Conditionality

Governments in emerging economies may also consider options for green conditionality. In this case, fiscal stimulus allocated to help those most affected by the pandemic is tied with sustainability objectives such as increasing the use of sustainable fuel or requirements and achieving net-zero emissions in specific periods or years. Green conditionality can be essential to attain double goals: helping the most affected sector while achieving climate targets. As in the case of Indonesia, the transport sector is among the sectors hit hardest by the COVID-19 pandemic. Hence, the government supports this sector, including providing capital injections to SOEs. While this policy is understandable given the devastating effects of the COVID-19 pandemic on the transport sector, it could only support the status quo energy production. Hence, it is crucial to integrate green perspectives into this policy by linking financial support with sustainability objectives. This policy may also present incentives for firms to foster sustainable business models.

7.4. Debt for Nature Swap Funds

The pandemic has put many developing countries in debt distress. As in the case of Indonesia and Vietnam, both countries experience an increasing debt as a percentage of GDP. The COVID-19 pandemic induces debt problems in developing countries. It is estimated that debt services will reach more than USD 3 trillion in developing countries in 2020 and 2021 because of the pandemic [

68]. Given the damages that can be caused, the debt crisis has been a significant concern for many international organizations [

69,

70,

71]. The looming debt crisis could hamper the recovery plan of developing countries, let alone the allocation for green recovery. Therefore, it is crucial to reconsider the debt-for-nature swap (DFNS) to achieve two targets: addressing the debt problems of developing countries and achieving climate targets. In this case, the debtors pay the remaining outstanding interest to finance energy transition projects instead of paying creditors. DFNS was originally implemented in the 1980s to reduce the pressure developing countries face to secure foreign currency. The proponent of this approach argues that the pressure of foreign debt repayment obligations in hard currency has forced many developing countries to export commodities to secure foreign exchange. It encourages over-exploitation, which harms the environment [

72]. Hence, a number of organizations call for a DFNS, which is considered a joint solution to protect the environment as the debtor country is no longer required to export commodities to secure foreign income. In fact, developing countries could receive additional funding to finance green programs. Hence, through DFNS, it is hoped that the debt pressure of developing countries can be reduced and eventually reduce extractive activities. Considering this notion, DFNS is worth reconsidering during the COVID-19 pandemic.

8. Conclusions

The main goal of the current study was to understand the stimulus plans launched by emerging economies and how it aligns with a country’s sustainable energy and climate targets. There has been growing optimism about the green recovery since the pandemic started especially considering the recovery plan launched by many major countries. Furthermore, the resilience of renewables during the pandemic fueled this optimism. Nevertheless, in the case of Indonesia and Vietnam, these two countries share similarities where fiscal measures directed to green recovery are limited. In sum, although these two countries have outlined ambitious targets toward clean energy targets, the pandemic would not accelerate the progress in achieving those targets. In fact, in the case of Indonesia, for instance, the country saw a drop in investment in the RE sector. The disruptions in the energy demand during the pandemic may be further complicated as Indonesia has already experienced an excess supply problem over the past few years. Similar to other emerging economies, this result may be explained by the fact that these two countries faced limited fiscal budgets that prevented them from focusing on the green recovery. In fact, the COVID-19 pandemic has exacerbated public fiscal budgets where both countries experience widening fiscal deficits and increasing public debt. To address this problem, both countries have outlined plans for fiscal consolidation that may further limit the fiscal capacity to fund green projects required for achieving the green energy transition target. At the same, both countries also specify ambitious climate targets. Hence, a key policy priority should be to plan for these targets while coping with the limited and constrained fiscal capacity. This paper suggests four courses of action: green fiscal consolidation, green and sustainability bonds, green conditionality, and debt for nature swap funds. Several questions remain to be answered, including enabling and disabling factors at the national level that affect the implementation of these policies.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}