Abstract

Improving the cultural consumption level of rural residents is of great practical significance to help revitalize rural culture and achieve common prosperity. Based on this, this study empirically examines the role and impact mechanism of digital inclusive finance on enhancing the cultural consumption of rural residents using panel data of 30 provinces across China from 2011 to 2020. The results show that: (1) Digital inclusive finance can significantly improve the cultural consumption level of rural residents. After a robustness test and endogenous analysis, this conclusion is still stable. (2) Digital inclusive finance significantly improves the cultural consumption level of rural residents through three paths: raising the income level of farmers, promoting the level of urbanization, and improving the level of financial development. (3) Heterogeneity analysis shows that the breadth of digital inclusive financial coverage can significantly improve the cultural consumption level of rural residents, but the depth of digital inclusive financial use and the degree of digitization do not show an enhancing effect; the development of digital inclusive finance in the eastern area has a significant role in promoting the cultural consumption level of rural residents, but the role is not significant in the central and western areas.

1. Introduction

Rural civilization is the guarantee of rural revitalization. Prospering rural culture, activating the rural cultural market, and constantly improving rural social civilization are the key to realizing rural cultural revitalization. Cultural consumption experience itself has its unique attraction and value [1], and the implementation of cultural revitalization in rural areas can release the potential of residents’ cultural consumption and meet their needs for a better life [2]. General Secretary Xi Jinping pointed out that “to revive the nation, the countryside must be revitalized”, and rural revitalization requires not only “shaping” but also “casting the soul”, while rural cultural revitalization is the soul-casting project of rural revitalization. Without a high degree of confidence in rural culture and the prosperous development of rural culture, it is difficult to realize the great mission of rural revitalization. The report of the 20th National Congress of the Communist Party of China clearly puts forward insisting on giving priority to the development of agriculture and rural areas, adhering to the integration of urban and rural development, smoothing the flow of urban and rural elements, and solidly promoting the revitalization of rural industries, talents, culture, ecology, and organizations. Strengthening rural cultural construction and realizing rural cultural revitalization is a powerful way to realize the effective connection between the achievements of poverty eradication and rural revitalization, and to promote common prosperity in rural areas. Cultural consumption is a booster to promote rural cultural revitalization.

With the rapid development of China’s economy, residents’ demand for cultural consumption has been further enhanced, and the cultural consumption economy has shown an increasing trend. In 2012, the per capita consumption expenditure of urban residents on education, culture, and entertainment reached 2000 yuan, and in 2019 it broke through to 3000 yuan. However, affected by the COVID-19 pandemic, it fell back to 2592 yuan in 2020. In the past ten years, the per capita consumption expenditure of urban residents on education, culture, and entertainment grew at an average annual rate of 4.5%. Compared with the rapid growth of urban residents’ cultural consumption level, rural residents’ cultural consumption situation was struggling until 2016 when per capita consumption expenditure of education, culture, and entertainment of rural residents broke through the 1000 yuan mark and has not exceeded 2000 yuan so far. From the perspective of growth rate, during the period of 2010–2020, the average annual growth rate of cultural consumption in rural areas reached 16.0%, which is about four times the average annual growth rate of urban residents. It is obvious that although the per capita consumption expenditure of education, culture, and entertainment of rural residents is growing faster, the concepts of cultural consumption and consumption awareness of rural residents are not strong, and their willingness to consume culture is not high, so there is still a large gap between urban and rural cultural consumption, and there is a more obvious cultural consumption “gap”. Cultural consumption is an important consumption activity and an indispensable part of residents’ daily life [3]. As China’s social contradictions change, rural residents’ demand for cultural consumption is getting higher and higher. Rural cultural consumption is not only an important breakthrough to balance rural material and spiritual consumption and promote the revitalization of cultural industry, but also a key focus point to narrow the “cultural gap” and coordinate urban and rural development [4]. How to stimulate rural residents’ cultural consumption demand, promote the improvement of rural residents’ cultural consumption level, and bridge and cross the “gap” of cultural consumption has become the focus of this study.

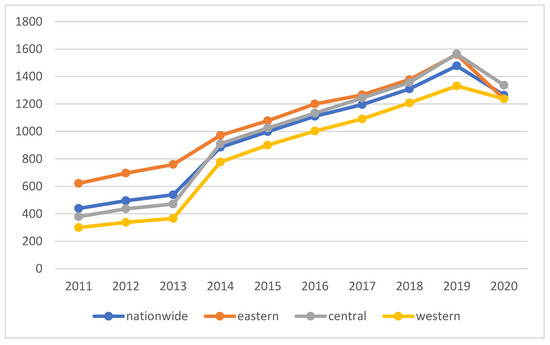

This study maps the development trend of the average value of cultural consumption of rural residents in China from 2011 to 2020, and divides the Chinese region into three regions: eastern, central, and western according to the different statuses of socioeconomic development (the eastern region includes 11 provinces in Beijing, Tianjin, Hebei, Liaoning, Shandong, Jiangsu, Shanghai, Zhejiang, Fujian, Guangdong, and Hainan; the central region includes 8 provinces in Shanxi, Jilin, Heilongjiang, Anhui, Jiangxi, Henan, Hubei, and Hunan; and the western region includes 11 provinces in Guangxi, Yunnan, Chongqing, Sichuan, Guizhou, Shaanxi, Gansu, Inner Mongolia, Ningxia, Qinghai, and Xinjiang), and draws the development trend of the average cultural consumption of rural residents in these three regions. According to Figure 1, it can be found that, as a whole, the level of cultural consumption of rural residents in China has been in the rising stage during 2011–2019, while a turning point of decline occurred in 2020, which may be due to the impact of the COVID-19 pandemic, which has affected the economy more and residents have reduced their cultural consumption expenditure. In terms of regional heterogeneity, the cultural consumption level of rural residents in the eastern region is at the forefront of the three regions, the cultural consumption level of rural residents in the central region also performs relatively well and gradually maintains a balance with the cultural consumption level of rural residents in the eastern region, and the cultural consumption level of rural residents in the western region is at the bottom of the three regions and still has more room for improvement.

Figure 1.

Trend of cultural consumption level of rural residents in China 2011–2020.

In order to investigate the regional differences in the cultural consumption levels of rural residents in China in depth, this study refers to the method of calculating the Theil index by Zhu and Chen [5], and uses the Theil index to measure the degree of regional differences in the cultural consumption levels of rural residents, and further decomposes the overall differences in the cultural consumption levels of rural residents into intra- and inter-regional differences among the three major regions of East, Central, and West to study the degree of regional differences in the cultural consumption levels of rural residents in China and their related contribution rates, and the results are shown in Table 1. From the overall differences, the Theil index of Chinese rural residents’ cultural consumption level dropped from 0.1158 in 2011 to 0.1015 in 2013, then dropped sharply to 0.0122 in 2018, and rebounded slightly to 0.0135 in 2019, which may be due to the impact caused by the epidemic, but it dropped to 0.0122 after 2020, so it should be more concerned about the future trend of cultural consumption of rural residents in China. On the whole, the overall differences in the cultural consumption level of rural residents in China show a narrowing trend. From the decomposition results, the contribution rates of inter-regional differences are all less than 50% from 2011 to 2020, and the contribution rates of intra-regional differences are all greater than 50%, that is, the contribution rates of intra-regional differences are greater than those of inter-regional differences, indicating that the overall differences of cultural consumption of rural residents in China mainly come from intra-regional differences, and the eastern region has the highest contribution rate.

Table 1.

Theil index of cultural consumption of rural residents in china and its contribution rate.

With the combination and development of big data, cloud computing, blockchain, artificial intelligence, and other advanced technologies in the financial field, digital inclusive finance has emerged as a potential means to stimulate the cultural consumption vitality and promote the cultural consumption of rural residents. As an extension and innovation of the traditional financial field, digital inclusive finance breaks through the temporal and spatial limitations of inclusive financial development; has extensive connections between different regions; breaks through the geographical and spatial barriers with its advantages of low cost, wide coverage, and deep services; effectively alleviates the financial exclusion phenomenon prevailing in the traditional financial market [6]; and provides disadvantaged groups and groups in remote areas with convenient digital inclusive finance that may be an effective digital path to stimulate rural residents’ willingness to consume culture, improve the level of cultural consumption, and bridge the cultural consumption “divide”.

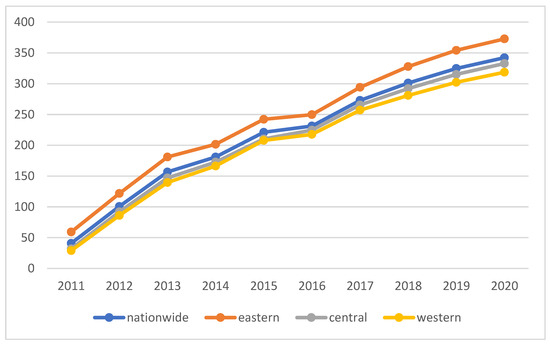

This study draws the development trend of China’s digital inclusive financing total index average from 2011 to 2020 and draws the development trend chart of the digital inclusive financing total index average in these three regions. According to Figure 2, it can be found that, on the whole, China’s digital inclusive finance continued to develop from 2011 to 2020 and can be subdivided into two rapid development stages: 2011–2013 and 2016–2018. In terms of regional heterogeneity, the development of digital inclusive finance in the eastern region has always outperformed the national level of digital inclusive finance development and is at the forefront of the three regions; the development of digital inclusive finance in the central region is on par with the national level of digital inclusive finance occurrence, while the development of digital inclusive finance in the western region lags behind the national level of digital inclusive finance development and is at the bottom of the three regions. It can be seen that, for the development of digital inclusive finance in various regions of China, the government should do a good job of top-level design, actively promote the organic and synergistic development of digital inclusive finance in the western region, balance the resource allocation pattern of digital inclusive finance development, and reduce the problem of the widening consumption gap caused by the unbalanced development of digital inclusive finance.

Figure 2.

Trend of the digital inclusive finance index in China, 2011–2020.

Therefore, it is of great practical significance to explore whether digital inclusive finance can improve the cultural consumption level of rural residents, in order to help revitalize rural culture and promote the common prosperity of rural farmers. Based on this, this study attempts to establish a theoretical analysis framework between digital inclusive finance and rural residents’ cultural consumption and uses panel data of 30 provinces from 2011 to 2020 to test the impact of digital inclusive finance on rural residents’ cultural consumption level and its mechanism. The results of the study will provide a feasible digital solution to improve the cultural consumption level of rural residents, bridge the cultural “gap”, help revitalize rural culture, and realize the common prosperity of farmers and rural areas.

2. Literature Review, Theoretical Analysis, and Research Hypothesis

2.1. Literature Review

In the national fintech strategic deployment, digital inclusive finance is a key development task [7]. In studies related to digital inclusive finance, scholars at home and abroad have focused on the role it plays. A large number of studies have shown that digital inclusive finance has an important role in promoting economic growth, raising residents’ income, alleviating poverty, and narrowing the income gap between urban and rural areas. First, regarding the role of digital inclusive finance in promoting economic growth, Greenwood and Jovanovic proposed that there is an inextricable relationship between financial development and economic growth, and that financial development can promote economic growth, and verified this promotional relationship through models [8]. Digital inclusive finance has a positive contribution to economic growth by alleviating financial exclusion, reducing the cost of services, improving the efficiency of financing, achieving the complementary effect of financing, and promoting entrepreneurship among rural residents [9]. Further, Ding argues that the development of digital inclusive finance injects new vitality into economic growth, and innovatively suggests that digital inclusive finance and environmental regulation have significant synergistic effects on regional economic growth [10]. Second, regarding the poverty reduction role of digital inclusive finance, in order to verify whether financial development can alleviate poverty, Dollar and Kraay conducted an empirical study on economic variables in several countries, and the results showed that financial development can achieve the goal of poverty reduction among the poor and improve their living standards [11]. As finance evolves and deepens, the income of the poor group will be increased, which in turn will reduce the share of the poor [12]. Specifically, first, the development of digital inclusive finance has led to a significant increase in the possibility and ease of access to credit support for the poor groups, thereby alleviating their liquidity constraints and achieving goals such as poverty reduction and elimination [13]. Second, the development of inclusive finance can enable farmers to obtain an increase in productivity equipment and thus production income, thereby reducing their poverty levels and alleviating hunger and undernutrition [14]. Third, digital inclusive finance can play an important role in poverty reduction by making it easier for people to access and obtain financial resources through innovations in savings, loans, and payments, thus gaining access to a wide range of financial services [15]. Digital inclusive finance can alleviate poverty and have a poverty reduction effect in three dimensions: health care poverty, income poverty, and education poverty [16]. Third, in terms of the role of digital inclusive finance in narrowing the urban-rural income gap, Yu and Wang suggest that digital inclusive finance can narrow the urban-rural income gap and has a non-equilibrium effect between regions [17]. Digital inclusive finance has a significant effect of narrowing the urban-rural income gap, which is more significant in the eastern and central regions and weaker in the western region [18]. Ji et al. proposed that digital inclusive finance alleviates the income gap between urban and rural areas through the transmission mechanism of promoting resident entrepreneurship [19], and further, Zhao et al. argue that digital inclusive finance can narrow the urban-rural income gap and can reduce the income differences between urban and rural residents in both the primary and redistribution [20]. While, there are some scholars who believe that financial development brings negative effects. Li proposed the view that with the rapid development of the financial industry, the income gap between urban and rural residents is growing, and the widening of the urban-rural income gap has caused a large number of unfavorable phenomena in the process of economic development [21]. Yue et al. pointed out that while digital finance is financially inclusive, it also increases the risk of households falling into financial distress, which has an impact on household consumption [22].

Li et al. investigate the impact of digital inclusive finance on household consumption using Chinese household finance survey data, and the results show that digital inclusive finance can increase the level of Chinese household consumption, and the mediating effect model test shows that online shopping, digital payment, access to online credit, purchasing financing products and commercial insurance online can effectively promote digital inclusive finance to increase the level of Chinese household consumption [23]. In addition, some scholars say that the current consumption problem of Chinese residents is largely manifested as the consumption problem of rural residents [24]. The existing research on rural residents’ consumption mainly focuses on the promotion of the use of the Internet. Zhou and Yang point out that the rapid popularization of the Internet has greatly changed the consumption environment of rural residents and has positively promoted the consumption behavior of rural residents [25], and the development of network infrastructure has significantly promoted the overall consumption number of rural residents in China [26], and further, Sun et al. argue that the application of the Internet not only promotes the consumption of rural residents, but also plays an important role in the process of upgrading the consumption of rural residents [27]. In addition, a few studies have argued that fiscal support expenditure on agriculture has an impact on rural residents’ consumption [28].

In the latest research on cultural consumption, Qin and Zhang pointed out that digital cultural consumption has great development potential, the types of digital cultural consumption products are becoming more and more abundant, the digital cultural consumption market is expanding, and the residents’ cultural consumption tendency is steadily increasing [29]. Huang et al. proposed promoting digital cultural consumption, digitally boosting the creative transformation and innovative development of outstanding Chinese traditional culture, and contributing to building a strong cultural nation [30]; in the new development pattern, in the field of consumption, focusing on the development of the digital economy to release the consumption potential, further enhancing the domestic cultural consumption demand to lay a solid foundation.

As can be seen from the above, most of the existing studies on the impact on residential consumption discuss the use of the Internet to promote it, and a few studies have paid attention to the influence of digital inclusive finance on residential consumption. Yi and Zhou propose that the development of digital inclusive finance significantly promotes residential consumption [31]; Zou and Wang propose that digital inclusive finance can significantly promote the level of residential consumption, and the promotion effect is more significant for the eastern and western regions [32]; Long et al. propose that the level of digital inclusive finance development promotes residents’ consumption, and the years of education and household income have an impact on this effect [33]. Further studies found that the impact of digital inclusive finance on residents’ consumption mainly focused on how to enhance urban residents’ consumption, and fewer studies addressed the issue of how to apply digital inclusive finance to enhance rural residents’ consumption. Among the few studies, Guo et al. proposed that the development of digital inclusive finance can significantly promote rural residents’ consumption [34]. All of the above research perspectives belong to the broad consumption field research, while there is a lack of research on the impact of digital inclusive finance and rural residents’ cultural consumption. Based on the above analysis, this study, based on the field of rural residents’ cultural consumption, uses panel data of 30 provinces across China from 2011 to 2020 to explore in depth the impact of digital inclusive finance on rural residents’ cultural consumption and its mechanism of action, with a view to providing feasible digital paths for achieving comprehensive rural revitalization and solidly promoting farmers’ common prosperity in rural areas.

2.2. Theoretical Analysis

Liquidity Constraint Theory. The theoretical origin of the influence of finance on consumption can be traced back to the liquidity constraint theory [35]. ”Liquidity constraint”, also known as “credit constraint”, is a constraint on the ability of residents to obtain loans from financial and non-financial institutions to meet their consumption activities. Liquidity constraints can be divided into current liquidity constraints and expected liquidity constraints, both of which have an impact on consumer spending. The current liquidity constraint makes residents’ consumption demand much lower than their desired consumption demand, and they have to maintain or even reduce their consumption level due to the unavailability of funds. The expected liquidity constraint creates a “fear of danger” mentality among residents, who will reduce their current consumption level when they expect to be constrained by credit in the future. There are three reasons for liquidity constraints: first, consumers lack wealth, have no realizable assets, or cannot obtain credit through a mortgage; second, the development of the credit market is not perfect, and there are problems of information asymmetry, which are prone to adverse selection and moral hazard; third, the scale of the consumer credit market is not large enough, and there are not enough kinds of products, which leads to the poor matching between consumer demand and products provided by the market.

Long Tail Theory. The concept of “long tail” was first proposed by American economist Chris Anderson at the beginning of this century. When he depicted the market, the horizontal axis represented the entire market of consumers, and the vertical axis represented the product demand, which depicted the curve with an obvious trailing phenomenon. In comparing the traditional retail market with the online retail market, Chris Anderson found that the Internet retail market gains in serving the long tail market. The long tail market is a concept relative to the mainstream market, which is a mass market belonging to the front end, occupying twenty percent of the products but having eighty percent of the profits, while the long tail market is a cold market belonging to the back end, occupying eighty percent of the market of heterogeneous products, which brings significant profits if the consumers’ needs of the back end group are valued and met. The long tail theory emphasizes focusing on the tail of the population, focusing on market segments, and creating personalized and differentiated strategies, and there is huge market potential in this group. The era of rapid development of internet information technology, digital inclusive finance, with its digitalization, high efficiency, and low threshold serves the “long tail” customers who are excluded from traditional finance, and these groups can enjoy more comprehensive and lower-cost financial services, effectively solving the problem of financing constraints and improving the overall efficiency of financial institutions. The overall efficiency of financial institutions has also improved.

Income Determination Theory. Income determination theory is divided into absolute income theory and relative income theory. As for the absolute income theory, Keynes pointed out that the primary factor determining consumption is income, and there is a positive relationship between income and consumption, that is, consumption will increase with the increase of income, but the part used for consumption per unit of increased income will gradually decrease, that is, there is a law of diminishing marginal consumption. Keynes proposed that the law of diminishing marginal consumption exists because of the basic psychological laws of man. Overall, consumption depends on the absolute level of income and decreases as a proportion of incremental consumption per unit of incremental income. However, this hypothesis only considers the relationship between current income and current consumption and does not take into account the impact of intertemporal income and other social factors on current consumption, so it has some limitations. As for the relative income theory, the theory was put forward by Duesenberry. It is a revision of Keynes’s absolute income hypothesis on the basis of introducing consumer behavior. He believes that consumers’ current consumption depends not only on their current income but also on their consumption behavior habits and the consumption behavior of surrounding consumers. From this perspective, residents’ consumption behavior depends not only on their own income level, but also on the income level of surrounding consumers. From the perspective of social psychology, Duesenberry analyzed the existence of the “ratchet effect” and “demonstration effect” in consumers’ behavior. The so-called “ratchet effect” means that consumers’ consumption expenditure will increase with the increase in income level; when consumption reaches a certain level, even when the future income level drops, their consumption expenditure will not drop to the previous level. After the formation of consumers’ consumption habits, it is irreversible and difficult to adjust downward. The ”demonstration effect” means that consumers have the psychology of imitation and comparison, and their consumption behavior will change according to the consumption behavior of neighboring people. For example, when they see the higher consumption level of neighboring people, they will also increase their own consumption expenditure and follow the example of neighboring people to improve their own consumption level.

2.3. Research Hypothesis

In the context of the Internet, the development of digital inclusive finance has improved the convenience of payment. Zhang et al. proposed that the convenience of payment can promote residents’ consumption, and with the promotion and popularity of mobile payments such as Alipay and WeChat, residents can complete shopping and other consumption behaviors with just one cell phone, which not only improves the convenience of payment but also greatly shortens the transaction time [36]. The development of digital inclusive finance includes the improvement and development of the financial environment, and the widespread application of digital inclusive financial services such as payment, credit, insurance, investment, and finance in the vast rural areas has promoted offline commerce online, which can provide farmers with a shopping and consumption experience similar to that of urban residents, thus effectively releasing the cultural consumption demand in rural areas and providing rural residents with deferred payment. With the help of online channels, micro-credit services can promote cultural consumption in rural areas. When there is uncertainty about consumers’ future income, consumers will increase precautionary savings and reduce current consumption. Rural digital inclusive finance can provide farmers with financial services such as digital insurance and wealth management to reduce the uncertainty faced by rural residents’ individuals and families, making rural residents more willing to spend psychologically and helping to raise their spending levels on cultural consumption. In addition, the cultural consumption needs of rural residents are subject to “financial exclusion” due to factors such as geographical remoteness and lack of qualifications [37], while the development of digital inclusive finance can alleviate the problem of financial exclusion and liquidity constraints to a certain extent, and rural residents can borrow relatively freely to satisfy their current consumption desires when they are free from liquidity constraints, which is conducive to increasing total rural cultural consumption and raising consumption levels. This leads to hypothesis 1.

Hypothesis 1:

Digital inclusive finance is conducive to raising the cultural consumption level of rural residents.

Mediating role of rural residents’ income. From the theory of income determination, it is known that income is the key factor of consumption. If the cultural consumption of rural residents is to be enhanced, then raising the income of rural residents is the fundamental way. In the context of the Internet, rural residents’ income levels have been raised (Zhou X. et al.) [38]. Digital inclusive finance reduces the cost of service provision of financial institutions and the cost of use of farmers, and in terms of service provision cost, the service outlets of financial institutions no longer rely only on traditional operating outlets but can operate remotely through the Internet and mobile terminals to provide various financial services to farmers, which can reduce the cost of fixed operating institutions and bring more of a “long-tail group” of customers (Fang and Cai) [39]. In terms of the cost of use by farmers, farmers can access the services they need, such as mortgage loans and investment finance, through mobile terminals without leaving their homes, saving time and travel costs. Coupled with the competitive pattern that exists among financial institutions, the interest rates on loans offered by each institution have generally become favorable, the procedures have become relatively simple, the threshold has become increasingly low, and the quality of services has continued to improve. In addition, digital inclusive finance can alleviate the problem of information asymmetry. In the consumer credit market, the existence of information asymmetry makes it difficult for rural residents to reach financial services due to their lack of understanding of financial services and products, and digital inclusive finance has broadened the channels for residents in rural areas to understand financial-related knowledge, and residents can learn to be familiar with more information about financial products through relevant websites and cell phone APPs. Information is open and transparent, and information asymmetry is greatly reduced. Under a variety of favorable conditions, farmers’ willingness to use digital inclusive finance is also getting stronger. Farmers enjoy financial services and ease financing constraints, which can promote income increase and help stimulate their consumption, thus enhancing their cultural consumption. This leads to hypothesis 2.

Hypothesis 2:

Digital inclusion enhances the cultural consumption of rural residents by increasing their income.

Mediating role of urbanization level. The role mechanism of urbanization boosting. Urbanization aims to promote the mutual interaction of new rural construction, community construction, and town construction, and enhance the coordinated development of urban and rural areas. It should be deployed around the construction of rural digital inclusive finance and new urbanization, and focus on building a modern development pattern of urban-rural integration and common prosperity. Digital inclusive finance promotes the development of urban-rural integration and urbanization level by serving the rural household groups. The availability of financial services for urban residents is already relatively high, and the poverty reduction effect played by digital inclusive finance is better in areas with developed transportation and high urbanization levels. In areas with higher urbanization levels, residents have more opportunities and expenditures for cultural consumption and more funds in hand for cultural consumption, which in turn improves the level of cultural consumption. Secondly, digital inclusive finance, while promoting the level of urbanization, can also give rise to more new businesses and expand more production and service models, which is conducive to improving the production and consumption structure in rural areas, creating more impetus for agricultural production and rural development, and helping to stimulate rural residents’ demand for cultural consumption and raise the level of cultural consumption of rural residents. This leads to hypothesis 3.

Hypothesis 3:

Digital inclusive finance enhances the cultural consumption of rural residents by promoting the level of urbanization.

Mediating the role of the financial development level. In addition to the two mechanisms of action mentioned above, digital inclusive finance can also influence the cultural consumption of rural residents by improving the level of financial development. With the development of internet information technology, the degree of information asymmetry in the credit market has been reduced, which in turn improves the accessibility of corporate bank loans, and companies have broken through geographical restrictions through diversified service means, making financial services available in cyberspace, and groups in remote areas can also access financial services, coupled with the reduction of transaction costs, making the price of financial services lower. With the lowering of the threshold, rural residents can afford the price of financial products, which greatly reduces the phenomenon of financial exclusion, expands the audience of financial services, helps to increase the scale of bank loans and reduce the cost of loans, and improves the level of financial development. The level of cultural consumption of rural residents can be improved. This leads to hypothesis 4.

Hypothesis 4:

Digital inclusive finance enhances the cultural consumption of rural residents by improving financial development.

3. Study Design

3.1. Baseline Regression Model

To verify the impact of digital inclusive finance on rural residents’ cultural consumption, a two-way fixed effects model is constructed. To eliminate the effect of heteroskedasticity, all variables are taken in their logarithmic form in the construction of the model. The model settings are shown as follows:

In Equation (1), represents the level of cultural consumption of rural residents in province i in year t; represents the level of digital inclusive finance development in province i in year t; represents the remaining variables affecting the level of cultural consumption of rural residents, including the level of economic development, industrial structure upgrading, the level of openness to the outside world, the Engel coefficient, and the level of human capital; is the regional fixed effects; is year fixed effects; and is a random disturbance term. is the core coefficient of interest for this study, and the sign is expected to be positive.

3.2. Mediation Effect Model

The starting point for analyzing the causal channels of action is that the causal relationship between phenomena may contain multiple logical links, and the cause does not act directly on the outcome; therefore, it is necessary to examine through which intermediate variables in the causal chain the cause affects the outcome, and such an analysis is often referred to as a mediating effect analysis [40]. Drawing on the studies of Baron and Kenny [41] and Shi and Li [42], a mediating effect model is constructed and the model is set as follows:

Equation (2) is the total effect model, Equation (3) is the effect model of digital inclusive finance on the mediating variables, where lnMit is the mediating variables, including the level of farmers’ income (lnINCOME), the level of urbanization (lnURBAN) and the level of financial development (lnLFD), and Equation (4) represents the estimated model considering both digital inclusive finance and the mediating variables.α1 represents the total effect of digital inclusive finance on the cultural consumption level of rural residents, β1 represents the effect of digital inclusion on the mediating variable, γ1 is the direct effect of digital inclusion on the cultural consumption level of rural residents after controlling for the mediating variable, and γ2 is the effect of the mediating variable on the cultural consumption level of rural residents after controlling for the digital inclusion variable. The criteria for judging the existence of intermediary effects are: if α1 is significant, the coefficients β1 and γ2 are tested in turn; if β1 and γ2 are significant, the coefficient γ1 is further tested; if γ1 is not significant, it means that the direct effect is not significant and there is a full intermediary effect; if γ1 is significant, it means that the direct effect is significant, and if β1 *γ2 has the same sign as γ1, it means that there is a partial intermediary effect and the amount of intermediary effect is β1 − γ2/α1.

3.3. Variable Selection

The explanatory variable is the level of cultural consumption of rural residents (lnCONSUME). Drawing on the study of Wang et al. [43], the cultural consumption ratio of rural residents is used to characterize the level of cultural consumption of rural residents, which is expressed using the proportion of per capita education, culture, and entertainment consumption expenditure of rural residents to per capita consumption expenditure of rural residents.

The core explanatory variable is digital inclusive finance (lnDFI). Drawing on the study of Guo et al. [44], the digital inclusive finance index at the provincial level from 2011 to 2020 compiled by the Digital Finance Research Center of Peking University is used to measure. Further, this study conducted heterogeneity analysis using three dimensions of digital inclusive finance coverage breadth (lnBRE), depth of use (lnDEP), and degree of digitization (lnDIG) to explore the impact of different dimensions of digital inclusive finance on rural residents’ cultural consumption.

The mediating variables include the level of rural residents’ income (lnINCOME), the level of urbanization (lnURBAN), and the level of financial development (lnLFD). The per capita disposable income of rural residents measures the level of farmers’ income; the share of urban resident population in the total resident population measures the level of urbanization; the ratio of deposit and loan balance of financial institutions to GDP measures the level of financial development.

Control variables. (1) The level of economic development (lnPGDP): GDP per capita is adopted to measure the level of economic development. (2) Industrial structure upgrading (lnISU): Referring to the study of Xu and Jiang, the industrial structure level coefficient is adopted to portray the industrial structure upgrading of each province, and the calculation formula is: ISU = q1 × 1 + q2 × 2 + q3 × 3, where q1, q2, and q3 denote the proportion of primary industry, the proportion of secondary industry, and the proportion of tertiary industry, respectively [45]. (3) The level of foreign openness (lnFDI): The increase of foreign openness can promote the integration of urban and rural industries into the process of economic globalization, which in turn promotes the development and exchange of cultural industries, releases the cultural consumption potential of rural residents, and thus enhances the cultural consumption level of rural residents. The proportion of the level of foreign direct investment to the regional GDP is used to measure the level of opening up to the outside world. (4) Rural Engel’s coefficient (lnENGEL): Rural Engel’s coefficient may affect cultural consumption; if the higher Engel’s coefficient indicates a greater proportion of food expenditure, the proportion of cultural consumption will decrease. (5) Human capital level (lnEDU): the level of human capital is measured using the number of years of education per rural resident. The formula of years of education per rural resident is: EDU = (number of people educated in elementary school × 6 + number of people educated in junior high school × 9 + number of people educated in senior high school × 12 + number of people educated in college and above × 16)/total population aged 6 and above.

3.4. Data Sources and Descriptive Statistics of Variables

This study conducts empirical analysis based on panel data of 30 provinces nationwide from 2011–2020. The research data are mainly obtained from the China Statistical Yearbook, the China Rural Statistical Yearbook, provincial statistical yearbooks, and the EPS database for the calendar years 2012–2021, and the data on digital inclusive finance comes from the Digital Inclusion Index constructed by the Digital Finance Research Center of Peking University. The results of descriptive statistics for each variable are shown in Table 2.

Table 2.

Results of descriptive statistics of variables.

4. Analysis of Empirical Results

4.1. Baseline Regression Results and Analysis

Prior to the baseline regression analysis, it is necessary to determine whether there is a multicollinearity problem among the variables. Generally, if the variance inflation factor (VIF) is less than 10, it indicates that there is no multicollinearity problem. the VIF test results show that the VIF values of each variable are less than 10, and the average VIF value is 2.030, which is much smaller than the empirical value, indicating that there is no multicollinearity problem among the variables. Table 3 reflects the results of the benchmark regression of the impact of digital inclusive finance on the cultural consumption of rural residents. As can be seen from column (1), when no control variables are included and regional fixed effects are considered, digital inclusive finance significantly raises the cultural consumption level of rural residents at the 1% level; as can be seen from column (2), when no control variables are included and regional and time-fixed effects are considered, digital inclusive finance still significantly raises the cultural consumption level of rural residents at the 1% level. The coefficient at this point is 0.016, indicating that for every 1% increase in the level of development of digital inclusive finance, the level of cultural consumption of rural residents increases by 1.6%, which initially verifies the validity of hypothesis H1. From column (4), it can be seen that when the control variables are added and the dual fixed effects of region and time are considered, digital inclusive finance still significantly promotes the cultural consumption level of rural residents at the level of 1%, at which time the coefficient is 0.046, indicating that for every 1% increase in the development level of digital inclusive finance, the cultural consumption level of rural residents increases by 4.6%, and hypothesis H1 is again verified. With its unique advantages of inclusiveness, low cost, and high efficiency, digital inclusive finance effectively alleviates the financing and credit constraints of rural residents and improves their credit availability, and rural residents can conduct online cultural consumption as well as offline cultural experiences through the platform provided by digital inclusive finance, which is important for the improvement of cultural consumption level of rural residents.

Table 3.

Baseline regression result.

From the control variables in column (4), the regression coefficients of the level of economic development and the level of openness to the outside world are 0.033 and 0.120, respectively, and both are significant at the 10% level. It shows that for every 1% increase in the level of economic development, the level of cultural consumption of rural residents increases by 3.3%, and for every 1% increase in the level of openness to the outside world, the level of cultural consumption of rural residents increases by 12%. The regression coefficient of the rural Engel coefficient is −0.218, and it is significant at the level of 1%, which indicates that the rural Engel coefficient has a negative influence on rural residents’ cultural consumption level, that is to say, the lower the Engel coefficient, the more obvious the promotion effect on rural residents’ cultural consumption, and for every 1% decrease in the Engel coefficient, the rural residents’ cultural consumption level increases by 21.8%; thus, it can be seen that the Engel coefficient has an important influence on the level of cultural consumption of rural residents. The effects of industrial structure upgrading and human capital level on the level of cultural consumption of rural residents are not significant.

4.2. Robustness Test

To test the robustness of the baseline regression results, this study uses the variable substitution method and the panel Tobit model for robustness testing, and the results are shown in Table 4. First, the regression is conducted using the level of urban residents’ cultural consumption (lnCITYC) instead of the explanatory variable. The cultural consumption level of urban residents is expressed using the proportion of urban residents’ education, culture, and entertainment consumption expenditure to urban residents’ per capita consumption expenditure, and the results are shown in column (5). Second, the first-order lagged term (lag1_lnDFI) and second-order lagged term (lag2_lnDFI) of digital inclusive finance are used to replace the core explanatory variables for the regressions, and the results are shown in columns (6) and (7). Third, the regression analysis is conducted using a panel Tobit model. Since the value of the cultural consumption level of rural residents is taken between 0 and 1, which has an obvious truncated nature, this study uses the panel Tobit model for robustness testing, and the results are shown in column (8). After the robustness test using the variable substitution method and the panel Tobit model, the effect of digital inclusive finance on the level of cultural consumption of rural residents is still significant, indicating that the baseline regression results are more robust.

Table 4.

Robustness tests.

4.3. Endogeneity Analysis

The baseline regression has demonstrated that digital inclusive finance can significantly increase the cultural consumption level of rural residents, but it may also generate endogeneity problems due to the omission of key variables and reverse causality, resulting in biased regression results. On the one hand, among the factors affecting the cultural consumption level of rural residents, there may be unidentifiable factors or factors that are difficult to be measured, and the omission of these factors may cause endogeneity problems; on the other hand, the increase in the cultural consumption level of rural residents may prompt farmers to use digital inclusive finance to obtain more financial support or to use digital platforms to carry out cultural consumption activities conveniently and efficiently, instead promoting the digital further development of inclusive finance, which may lead to endogeneity problems due to reverse causation. This study uses two strategies to identify the endogeneity problem: first, the first-order lagged term and second-order lagged term of digital inclusive finance are selected as instrumental variables for endogeneity testing, and the results are shown in columns (9) and (10) of Table 5. Second, the endogeneity test is conducted using instrumental variables of digital inclusive finance, and the selection of instrumental variables needs to satisfy the requirements of exogeneity and correlation. The number of landline phones per 100 people (lnPHONE) in 1984 in each province is selected as an instrumental variable for endogeneity testing and regressed using two-stage least squares, and the results are shown in column (11) of Table 5. On the one hand, the use of landline telephones changed the way of communication between people, broke through the physical space barrier, represented the in-depth development of mobile communication technology, and had an important impact on the development of advanced digital technologies such as the Internet, satisfying the instrumental variable relevance requirement; on the other hand, the use of landline telephones in history does not affect the current use of digital inclusive finance among residents, satisfying the instrumental variable exogeneity requirement. As can be seen from Table 5, after using the first-order lag and second-order lag terms of digital inclusive finance and the number of fixed telephones per 100 people in 1984 as instrumental variables, the role of digital inclusive finance in enhancing the cultural consumption level of rural residents remains significant, further verifying the robustness of the regression results.

Table 5.

Endogeneity test.

5. Further Discussion: Heterogeneity Analysis and Mediating Effect Test

5.1. Heterogeneity Analysis

5.1.1. The Impact of Different Dimensions of Digital Inclusive Finance on Rural Residents’ Cultural Consumption

The results of the benchmark regression indicate that digital inclusive finance can significantly increase the level of cultural consumption of rural residents. Then, how will the three different dimensions of digital inclusive finance affect the level of cultural consumption of rural residents? Therefore, this study further analyzes the effects of the breadth of digital inclusive finance coverage, depth of use, and digitization on rural residents’ cultural consumption levels, and the results are shown in columns (12) to (14) of Table 6. The results show that there are differences in the effects of different dimensions of digital inclusive finance on the cultural consumption level of rural residents; the breadth of digital inclusive finance coverage can significantly improve the cultural consumption level of rural residents, and for every 1% increase in the breadth of digital inclusive financial coverage, the cultural consumption level of rural residents increases by 1.6%, while the depth of digital inclusive finance usage and the degree of digitization do not reflect the promotion effect on the cultural consumption level of rural residents. The increase in the breadth of digital inclusive financial coverage enhances the availability of financial services for rural residents, and rural residents can better satisfy their own demand for cultural consumption after obtaining financial services and stimulating their willingness to consume culture, thus improving the level of cultural consumption. However, at the present stage, the use level of digital inclusive finance in rural areas is low and the degree of digitization is not high, which may limit the further enhancement of digital inclusive finance to the cultural consumption level of rural residents. Therefore, in the process of financial service rural revitalization, it is not only necessary to improve the coverage of digital inclusive finance so that every resident can reach financial products and services, but also to improve the usage level of digital inclusive finance so that it can be most effective, thus further enhancing the cultural consumption level of rural residents.

Table 6.

Heterogeneity of different dimensions of digital inclusive finance, regional heterogeneity results.

5.1.2. The Impact of Digital Inclusive Finance on Rural Residents’ Cultural Consumption in Different Regions

China’s rural areas have a vast territory, and there are differences in resource endowments and development stages. There are great differences in economic development levels, regional consumption policies, and total consumption of residents, which leads to possible differences in the impact of digital inclusive finance development on residents’ consumption. Therefore, this study makes a regional heterogeneity analysis; the results are shown in columns (15) to (17) of Table 6. The results of the study find that the eastern region has the most significant effect of digital inclusive finance on the cultural consumption level of rural residents; at this point the correlation coefficient is 0.076, which means that for every 1% increase in digital inclusive finance, the cultural consumption level of rural residents increases by 7.6%, while the impact of digital inclusive finance on the cultural consumption level of rural residents in the central and western regions is not significant. The main reason is that the eastern region has a higher level of economic development and digital inclusive finance development, and rural residents are more willing to use digital inclusive finance to meet their cultural consumption needs, thus helping to raise the cultural consumption level of rural residents; while the central and western regions have a lower level of economic development and the development of digital inclusive finance is relatively backward, which is not easy to meet the cultural consumption needs of residents.

5.2. Mediating Effect Test

From the theoretical analysis, it can be seen that digital inclusive finance can enhance the cultural consumption of rural residents through three paths: increasing the income level of farmers, promoting the level of urbanization, and improving the level of financial development. To test the existence of the three paths, this study uses the mediating effect model for empirical testing, and the test results are shown in Table 7. When the income level of rural residents is used as an intermediary variable, the coefficients of the main variables are significantly positive. It shows that there is a mechanism for digital inclusive finance to improve the cultural consumption level of rural residents by improving their income level. At this time, the mediating effect is 0.0105 (obtained by multiplying the coefficient of lnDFI in column (18) of Table 7 with the coefficient of lnINCOME in column (19)), accounting for about 22.83% of the total effect of digital inclusive finance on rural residents’ cultural consumption level (obtained by dividing the above mediating effect by the coefficient of lnDFI in column (4) of Table 3). This mechanism can explain the total impact of rural residents’ income level on rural residents’ cultural consumption level. When the urbanization level is used as an intermediary variable, the coefficients of the main variables are significantly positive. It shows that there is a mechanism for digital inclusive finance to improve rural residents’ cultural consumption level by improving the urbanization level. At this time, the intermediary effect is 0.0109, accounting for 23.70% of the total effect of digital inclusive finance on rural residents’ cultural consumption level. This mechanism can explain 23.70% of the total impact of urbanization level on rural residents’ cultural consumption level. Similarly, when the level of financial development is used as an intermediary variable, the coefficients of the main variables are significantly positive. It shows that there is a mechanism for digital inclusive finance to improve rural residents’ cultural consumption level by improving the financial development level. At this time, the intermediary effect is 0.0050, accounting for 10.87% of the total effect of digital inclusive finance on rural residents’ cultural consumption level. This mechanism can explain 23.70% of the total impact of the financial development level on rural residents’ cultural consumption level.

Table 7.

Results of intermediate effect test.

6. Research Conclusions and Policy Recommendations

Based on the panel data of 30 provinces in China from 2011 to 2020, this study analyzes the influence and mechanism of digital inclusive finance and rural residents’ cultural consumption level from theoretical and empirical perspectives. The results are as follows: First, digital inclusive finance can significantly improve the cultural consumption level of rural residents, and the conclusion is still robust after using the variable substitution method, the panel Tobit model for the robustness test, and instrumental variables for the endogenous test. For a long time, the remote and backward geographical location and other factors have brought about a great limitation in the consumption demand of rural society. In the context of the Internet, digital inclusive finance has started to focus more on the tail group, as there is huge market potential in this segment. With powerful technology, digital inclusive finance caters to national strategies to serve remote rural areas, alleviate their liquidity constraints, and meet their consumption needs. Second, from the perspective of different dimensions of digital inclusive finance, the breadth of digital inclusive finance coverage can significantly enhance the cultural consumption level of rural residents, but the depth of digital inclusive finance use and digitalization fail to show the effect of enhancing the cultural consumption level of rural residents. Third, from the perspective of different regions, digital inclusive finance in the eastern region can significantly improve the cultural consumption level of rural residents, while this effect is not significant in the central and western regions. Fourth, the intermediary mechanism test shows that digital inclusive finance can effectively raise the cultural consumption level of rural residents through three paths: raising the income level of rural residents, promoting the level of urbanization, and improving the level of financial development. Continuously improve the income level of rural residents, urbanization level, and financial development level, and drive digital inclusive finance to enhance the cultural consumption level of rural residents, so that the huge consumption demand and development vitality of rural society can be further released and the volume of the rural economy can be continuously increased.

Based on the above findings, this study puts forward the following policy recommendations: first, promote the further development of digital inclusive finance, give full play to the advantages of digital inclusive finance in terms of convenience and efficiency, improve the availability of credit for rural residents, and reduce the cost of financial credit services. Focus on improving the level of economic development, the level of openness to the outside world, efforts to reduce the Engel coefficient in rural areas, and multiple channels to improve the level of cultural consumption of rural residents. In addition, it is necessary to enhance the convenience of mass cultural consumption, to enrich the supply of cultural products and services through integrated development online and offline, to continuously provide cultural consumption products and services with price advantages, and to improve the sustainability and satisfaction of cultural consumption of rural residents. Second, play the role of financial services for rural revitalization, promote the deep integration of rural finance and rural residents, improve the coverage of digital inclusive finance so that every resident can obtain convenient and efficient digital inclusive financial products and services, and also improve the level of use of digital inclusive finance in rural areas. Third, it should strike a balance between efficiency and equity, deeply explore the potential of digital inclusive finance in regions with lower levels of economic development, promote the reform and upgrading of financial structures in central and western regions, and facilitate the development of digital inclusive finance in central and western regions. Avoid further widening of the cultural consumption gap due to the uneven development of the digital economy. In addition, focus on the spatial spillover effect of the development of digital inclusive finance, expand the radius of consumption spillover, stimulate the cultural consumption potential in rural areas, and further improve the consumption experience and effectiveness of rural residents. Fourth, further promote the sinking of digital inclusive financial services into the process of rural construction, and continuously play the role of digital inclusive finance in raising the income level of rural residents, promoting the level of urbanization and improving the level of financial development, especially focusing on raising the income level of rural residents and increasing the income channels. Income is a decisive factor in cultural consumption, which directly affects the level of cultural consumption of the population. This can be done by enriching financial management tools and products, increasing investment income from financial products through multiple channels, making up for the shortcomings of rural residents’ consumption, and helping to release the potential of cultural consumption. Make digital inclusive finance more convenient and efficient to popularize and promote in rural areas, to better serve the revitalization of rural culture, so as to enhance the cultural consumption level of rural residents, and ultimately help farmers and rural areas to common prosperity and enhance people’s well-being

Looking ahead, some scholars have suggested that fintech has the potential to disrupt the entire financial system, and in recent years it has played a significant role in the rapid digital transformation and production, delivery, and consumption of financial products and services, with billions of consumers around the world benefiting from these changes [46]. Although digital inclusive finance can improve credit services and enhance economic transformation with many advantages, there are also certain risks, such as cybersecurity, default risk, and data leakage, which may occur from time to time. In addition, products brought by new technologies may cause financial difficulties if not properly regulated [22]. Therefore, while focusing on the innovation and advantages brought by emerging fintech services, such as digital inclusive finance, it is also important to focus on its possible problems and actively explore and take effective measures to prevent risks, minimize risks, and increase social and economic benefits.

Author Contributions

Conceptualization, Y.S.; methodology, Y.S. and Q.C.; software, Y.S.; validation, Q.C.; formal analysis, Y.W.; investigation, Y.S. and Q.L.; data curation, Y.S. and Q.C.; writing—original draft preparation, A.X., Q.Z. and Y.S.; writing—review and editing, A.X. and Q.Z.; funding acquisition, Q.Z. All authors have read and agreed to the published version of the manuscript.

Funding

Projects were supported by the Major Project of Social Science Fund of Fujian Province in 2022 “Research on The Strategy of Fujian Province Adhering to Expanding Domestic Demand” (FJ2022Z006).

Data Availability Statement

All data are available via email from the corresponding author.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Benzecry, C.; Collins, R. The High of Cultural Experience. Sociol. Theory 2014, 32, 307–326. [Google Scholar] [CrossRef]

- Gu, J. The Achievements, Experience and Prospects of China’s Cultural Industry Development Since the 18th National Congress of the Communist Party of China. J. Manag. World 2022, 38, 49–60. [Google Scholar] [CrossRef]

- Kántor, S. Culture-Based Urban Development: The Relationship between Culture Consumption, Residence Preferences, and Quality of Life in Győr, Debrecen, and Veszprém. 2021. Available online: https://xs2.studiodahu.com/scholar?cluster=129826857145513286&hl=zh-CN&as_sdt=0,5 (accessed on 1 August 2022).

- Lin, L. Present Situation, Problems and Countermeasures of Rural Cultural Consumption in the New Era. Chin. J. Agric. Resour. Reg. Plan. 2022, 43, 188–200. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?FileName=ZGNZ202208033&DbName=CJFQ2022 (accessed on 18 January 2023).

- Zhu, H.; Chen, H. Level Measurement, Spatial-temporal Evolution and Promotion Path of Digital Village Development in China. Issues Agric. Econ. 2022, 1–14. [Google Scholar] [CrossRef]

- Liu, X.; Zhu, J.; Guo, J.; Cui, C. Spatial Association and Explanation of China’s Digital Financial Inclusion Development Based on the Network Analysis Method. Complexity 2021, 2021, 6649894. [Google Scholar] [CrossRef]

- Zhong, T.; Huang, Y.; Sun, F. Digital Inclusive Finance and Green Technology Innovation: Dividend or Gap. Financ. Econ. Res. 2022, 37, 131–145. [Google Scholar]

- Greenwood, J.; Jovanovic, B. Financial Development Growth and the Distribution of Income. J. Political Econ. 1990, 98, 1076–1107. [Google Scholar] [CrossRef]

- Xie, W.; Wang, T.; Zhao, X. Does Digital Inclusive Finance Promote Coastal Rural Entrepreneurship? J. Coast. Res. 2020, 103, 240–245. [Google Scholar] [CrossRef]

- Ding, R.; Shi, F.; Hao, S. Digital Inclusive Finance, Environmental Regulation, and Regional Economic Growth: An Empirical Study Based on Spatial Spillover Effect and Panel Threshold Effect. Sustainability 2022, 14, 4340. [Google Scholar] [CrossRef]

- Dollar, D.; Kraay, A. Growth is Good for the Poor. J. Econ. Growth 2002, 7, 195–225. [Google Scholar] [CrossRef]

- Honohan, P. Financial Development, Growth and Poverty: How Close Are the Links? World Bank Policy Research Working Paper; Working Paper No. 3203; World Bank Website: Washington, DC, USA, 2004. [Google Scholar] [CrossRef]

- Shoji, M.; Aoyagi, K.; Kasahara, R.; Sawada, Y.; Ueyama, M. Social Capital Formation and Credit Access: Evidence from Sri Lanka. World Dev. 2012, 40, 2522–2536. [Google Scholar] [CrossRef]

- Claessens, S.; Feijen, E. Finance and Hunger: Empirical Evidence of the Agricultural Productivity Channel; Social Science Electronic Publishing: New York, NY, USA, 2007; pp. 1–48. [Google Scholar] [CrossRef]

- Abor, J.Y.; Amidu, M.; Issahaku, H. Mobile Telephony, Financial Inclusion and Inclusive Growth. J. Afr. Bus. 2018, 19, 430–453. [Google Scholar] [CrossRef]

- Zhou, L.; Wang, H. An Approach to Study the Poverty Reduction Effect of Digital Inclusive Finance from a Multidimensional Perspective Based on Clustering Algorithms. Sci. Program. 2021, 2021, 4645596. [Google Scholar] [CrossRef]

- Yu, N.; Wang, Y. Can Digital Inclusive Finance Narrow the Chinese Urban–Rural Income Gap? The Perspective of the Regional Urban–Rural Income Structure. Sustainability 2021, 13, 6427. [Google Scholar] [CrossRef]

- Song, K.; Liu, J.; Li, Z. Does the Development of Digital Financial Inclusion Narrows the Urban-rural Income Gap?—Concurrently Discuss the Synergistic Effect between Digital Financial Inclusion and Traditional Finance in Rural Area. China Soft Sci. 2022, 13, 133–145. [Google Scholar] [CrossRef]

- Ji, X.; Wang, K.; Xu, H.; Li, M. Has Digital Financial Inclusion Narrowed the Urban-Rural Income Gap: The Role of Entrepreneurship in China. Sustainability 2021, 13, 8292. [Google Scholar] [CrossRef]

- Zhao, H.; Zheng, X.; Yang, L. Does Digital Inclusive Finance Narrow the Urban-Rural Income Gap through Primary Distribution and Redistribution? Sustainability 2022, 14, 2120. [Google Scholar] [CrossRef]

- Li, Y. Empirical analysis of the impact of financial development on the income gap between urban and rural residents in the context of large data using fuzzy Kmeans clustering algorithm. Int. J. Electr. Eng. Educ. 2020, 002072092093683. [Google Scholar] [CrossRef]

- Yue, P.; Korkmaz, A.G.; Yin, Z.; Zhou, H. The rise of digital finance: Financial inclusion or debt trap? Financ. Res. Lett. 2022, 47, 102604. [Google Scholar] [CrossRef]

- Li, J.; Wu, Y.; Xiao, J.J. The impact of digital finance on household consumption: Evidence from China. Econ. Model. 2020, 86, 317–326. [Google Scholar] [CrossRef]

- Guo, S. Rural residents’ consumption behavior, influencing factors and development suggestions. Issues Agric. Econ. 2022, 509, 2. [Google Scholar] [CrossRef]

- Zhou, Y.; Yang, Z. Does Internet Use Promote Rural Residents’ Consumption: Based on the Survey of 739 Farmers in Jiangxi Province. Econ. Geogr. 2021, 41, 224–232. [Google Scholar] [CrossRef]

- He, D.; Gu, J. The Impact of the Internet on the Consumption Level and Structure of Rural Residents: An Empirical Study of PSM Based on CFPS Data. Rural. Econ. 2018, 10, 51–57. [Google Scholar]

- Sun, Z.; Dong, J.; Li, D. Consumption Upgrading of Rural Residents: Is Internet Literacy Important? Econ. Issues 2022, 2, 103–111. [Google Scholar] [CrossRef]

- Ma, A.; Shang, Z.; Hefan, X.; Jiafeng, Y. Research on regional differences in the impact of fiscal support expenditure on farmers’ consumption. Stat. Decis. 2020, 36, 75–78. [Google Scholar] [CrossRef]

- Qin, K.; Zhang, C. The connotation, potential and development path of digital cultural consumption in the new development pattern. Dongyue Trib. 2022, 43, 17–26. [Google Scholar] [CrossRef]

- Huang, Y.; Song, J.; Shishan, Z.; Yuanping, X. Commentaries:Multidimensional Observation and Prospect of Cultural Digitization. J. Cent. China Norm. Univ. 2023, 62, 52–69. [Google Scholar] [CrossRef]

- Yi, X.; Zhou, L. Does Digital Financial Inclusion Significantly Influence Household Consumption? Evidence from Household Survey Data in China. J. Financ. Res. 2018, 461, 47–67. [Google Scholar]

- Zhou, X.; Wang, W. The Impact of Digital Financial Inclusion on Household Consumption: An Empirical Analysis Based on a Spatial Econometric Model. Financ. Econ. Res. 2020, 35, 133–145. [Google Scholar]

- Long, H.; Li, Y.; Wu, D. The Impact of Digital Financial Inclusion on Household Consumption: “Digital Divide” or “Digital Dividend”? Stud. Int. Financ. 2022, 3–12. [Google Scholar] [CrossRef]

- Guo, H.; Zhang, Y.; Yanling, P.; Zhongwei, H. Research on Regional Differences in the Impact of Digital Financial Development on Rural Residents’ Consumption. J. Agrotech. Econ. 2020, 12, 66–80. [Google Scholar] [CrossRef]

- Deaton, A. Understanding Consumption; Oxford University Press: Oxford, UK, 1992; pp. 214–221. [Google Scholar] [CrossRef]

- Zhang, X.; Yang, T.; Chen, W.; Guanhua, W. Digital Finance and Household Consumption: Theory and Evidence from China. J. Manag. World 2020, 36, 48–63. [Google Scholar] [CrossRef]

- Leyshon, A.; Thrift, N. The restructuring of the UK financial services industry in the 1990s: A reversal of fortune? J. Rural Stud. 1993, 9, 223–241. [Google Scholar] [CrossRef]

- Zhou, X.; Cui, Y.; Zhang, S. Internet use and rural residents’ income growth. China Agric. Econ. Rev. 2020, 12, 315–327. [Google Scholar] [CrossRef]

- Fang, G.; Cai, L. How Digital Financial Inclusion Affects Agricultural Output: Facts, Mechanism and Policy Implications. Agric. Econ. Issues 2022, 10, 97–112. [Google Scholar] [CrossRef]

- Jiang, T. Mediating Effects and Moderating Effects in Causal Inference. China Ind. Econ. 2022, 5, 100–120. [Google Scholar] [CrossRef]

- Baron, R.M.; Kenny, D.A. The Moderator-Mediator Variable Distinction in Social Psychological Research: Conceptual, Strategic and Statistical Considerations. J. Personal. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef]

- Shi, B.; Li, J. Does the lnternet Promote Division of Labor? Evidences from Chinese Manufacturing Enterprises. J. Manag. World 2020, 36, 130–149. [Google Scholar] [CrossRef]

- Wang, W.; Liu, B.; Li, X. How does digital financial inclusion affect the urban-rural cultural consumption gap? Rural Econ. 2021, 468, 90–98. [Google Scholar]

- Guo, F.; Wang, J.; Wang, F.; Kong, T.; Zhang, X.; Cheng, Z. Measuring China’s Digital Financial Inclusion: Index Compilation and Spatial Characteristics. China Econ. Q. 2020, 19, 1401–1418. [Google Scholar] [CrossRef]

- Xu, M.; Jiang, Y. Can the China’s Industrial Structure Upgrading Narrowthe Gap between Urban and Rural Consumption? J. Quant. Technol. Econ. 2015, 32, 3–21. [Google Scholar] [CrossRef]

- Allen, F.; Gu, X.; Jagtiani, J. A Survey of Fintech Research and Policy Discussion. Rev. Corp. Financ. 2021, 1, 259–339. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).