1. Introduction

Climate warming has a profound influence on the continued survival of human beings and has thus become a priority in the global community. At present, China is already the world’s largest carbon dioxide (CO

2) emitter. As an accountable country, China has committed to reducing carbon emissions as outlined at the Copenhagen Conference, as well as to the dual carbon emission goals (i.e., achieving carbon peak by 2030 and carbon neutrality by 2060) at the General Assembly of the United Nations. China is therefore under tremendous pressure to reduce its CO

2 emissions. China has emerged as the world’s second-largest economy and has enjoyed moderate to high economic growth since the country’s reform and opening up over the last 40 years. However, China’s past economic growth was the result of industrial production that required excessive energy consumption and created excessive pollution and emissions, which urgently requires the transformation to high-quality economic development. Lowering CO

2 emissions is fundamental for China’s sustainable development, but the government should also continue to develop the economy and raise living conditions [

1]. It has therefore become an urgent issue for both scholars and policymakers to achieve the dual carbon goals while maintaining steady economic development. For the developing countries that are represented by China, enhancing carbon emission efficiency (CEE) is an advantageous way to meet this demand [

2], while coordinating CO

2 emissions with economic activity [

3].

Energy is the backbone of manufacturing and people’s living standards and thus drives socioeconomic improvement [

4]. However, traditional fossil fuels create welfare while producing a massive amount of CO

2 emissions [

5,

6]. Given the concern for global warming, most scholars view clean energy as a vital alternative to fossil energy [

7,

8,

9]. It is therefore beneficial to explore the relationship between clean energy development and CEE to support decision making for promoting sustainable economic growth and limiting CO

2 emissions [

10]. Meanwhile, a stable financial system also has a crucial role to play in economic and environmental terms. From the perspective of structural transformation, different stages of economic growth will face various environmental issues; then there are also structural differences in the financial system’s response to environmental problems. Some studies have shown that the market-oriented financial structure has an important impact on economic development and carbon emission reduction [

11,

12]. Theoretically, the change of financial structure also plays a crucial role in CEE. As China’s structural supply-side financial reforms continue to deepen, it may facilitate the flow of capital to clean industries and mitigate environmental pollution [

13]. However, bank credit tends to be less good at financing clean energy, while capital market is more conducive to clean energy development [

14]. As such, whether the integration of clean energy development and financial structure transformation can become a key way to enhance CEE, so as to achieve carbon emission reduction targets and long-term economic development, is of critical value to both China and the world.

At present, the research on CEE is focused on the following two aspects: On the one hand, it is about the definition and calculation of CEE. The early definition of CEE involved single-factor indicators, and its ease of use has received significant interest from academics. Other scholars have adopted other indicators to define carbon emission performance [

15,

16]. Despite this, the one-factor approach can only capture a small portion of carbon efficiency and fails to reveal the importance of other factors that affect CEE (such as labor force, capital accumulation, and energy inputs) [

17]. It is for this reason that total factor indicators, which include more than one input and output involved in the production process, have attracted a great deal of attention [

17]. Generally, total factor performance indicators have been calculated using the frontier approach, which measures performance as the distance between the inputs and outputs and the production frontier. There are two methods to measure performance: stochastic frontier analysis (SFA) and data envelopment analysis (DEA). SFA is a parametric method that requires a predetermined production function and is exceedingly subjective, which may lead to deviations in the calculating results [

18]. However, DEA is a nonparametric method that does not need to assume a function form or random component distribution, and is suitable for evaluating performance through multi-input/output indicators. Accordingly, some researchers incorporate CO

2 into the undesirable output and obtain CEE through slack-based measure (SBM), directional distance function (DDF), and nonradial directional distance function (NDDF) [

19,

20,

21,

22]. It should be noted that the technological heterogeneity among regions [

20] and the inconsistency between desirable and undesirable outputs [

23] are not considered in the efficiency calculation, which will lead to some deviations and errors in the results.

On the other hand, enhancing CEE has also been explored. Some researchers have produced promising results in terms of industrial structure [

24], green technology [

22], urbanization, and foreign direct investment [

25]. However, as an effective way to limit CO

2 emissions and achieve the sustainable development goals [

26], the influence of clean energy on CEE has been broadly ignored. Previous studies have focused more on the impact of clean (or renewable) energy on economic growth and CO

2 emissions, but have not yet reached a consensus [

27,

28,

29]. Meanwhile, as China’s financial system continues to improve, it has shifted from a single banking system to a multilevel financial market system. Whether structural financial reforms should contribute to economic growth and promote energy conservation and emission reduction cannot be ignored. Some researchers have also begun to examine the role of financial structure in reducing carbon emissions [

11,

12]. In addition, compared with the bank-led financial structure, the capital market is more conducive to promoting clean energy development [

30,

31]. However, there is little literature that provides in-depth analysis of clean energy and financial structure as an effective way to enhance CEE.

Considering that China is a large country with regional heterogeneity, regional differences are apparent in CEE due to its economic development, industrial distribution, energy endowment, environmental pollution, and other factors [

21,

22]. Clean energy development is inconsistent across regions [

32], and there is also variability in the extent to which market-oriented financial structures affect each region [

33]. Therefore, clean energy development and financial structure transformation may have different impacts and extents across different regions when it comes to carbon efficiency. The aim of this article is therefore to further elaborate on our discussion by applying a spatial econometric model.

In view of the gap in the existing literature, this paper aims to analyze the influence of clean energy and financial restructuring on provincial CEE in China. Specifically, the principal contributions of this study are as follows: First, this study applies the improved NDDF to calculate the CEE at the provincial level in China. We find that there is a sizeable spatial imbalance, which provides a basis for policy makers to recognize the current status of CEE and take robust measures. Second, unlike previous studies, we put clean energy, financial structure, and CEE into a single framework. Third, we systematically explore the influence of clean energy and a market-oriented financial structure on CEE and include the spillover effects. Meanwhile, we classify Chinese provinces into groups according to their CEE level to explore the variability in the influence of regional clean energy under different financing channels. This method provides a theoretical foundation for enhancing CEE in each region in China and formulating financial support mechanisms for clean energy in a localized manner.

Following is a description of the rest of this study. Review of the literature is provided in

Section 2. The hypotheses of the study are presented in

Section 3. The data and methods of research are described in

Section 4. An analysis and presentation of the empirical results are provided in

Section 5. A discussion of policy implications concludes

Section 6.

3. Research Hypothesis

Carbon emission efficiency is an important evaluation indicator of low carbon economy, that is, an effective basis for reconciling economic growth with carbon emission reduction [

10]. Theoretically, the factor and substitution effects of clean energy can effectively promote economic development and reduce CO

2 emissions, which implies that clean energy has great potential to enhance CEE. However, this potential has been greatly diminished by the lack of mature technologies and the large capital requirements needed in the early developmental stages. With the gradual removal of government subsidies further constraining clean energy development, external financing has become an inevitable choice for companies. Unlike the risk-averse nature of the banking industry, the stock market favors high-risk, high-return projects such as clean energy [

30], and is therefore willing to provide direct financing opportunities for concepts such as clean energy [

14]. Additionally, the capital market can mitigate the adverse selection and moral hazard issues to a large extent. Clean energy companies have increased in valuation because of investor demand for social responsibility and more informative disclosure requirements [

49], which has provided reliable sources of financing for the clean energy industry. As capital funds gradually flow to the green sector, it will alleviate the difficulty of financing the clean energy industry, thus unleashing the potential of clean energy in enhancing CEE. Therefore, we propose our first hypothesis.

H1. The integration of clean energy and stock market can improve CEE.

Currently, the banking industry remains the most important component of China’s financial system. Functionally, banks are more sophisticated than capital markets in terms of capital reserves, information management, and risk control, so they can play a more important role in promoting economic growth [

14]. Despite China undergoing a period of economic transition, there is significant credit discrimination in financial institutions, particularly in state-owned commercial banks [

50]. As a result of this, commercial banks are more likely to provide credit to state-owned or listed companies, which limits access to financial services and loans for green firms. In addition, the banking industry is risk-averse, and its loan review processes are not only very strict but also time-consuming [

11]. For example, Nasir et al. [

51], in studying ASEAN economies, found that the banking industry provides more credit channels for energy-intensive sectors, while green industries obtain very little. In turn, this phenomenon is causing the clean energy industry and its related technology R&D projects to have difficulty obtaining sufficient funding from commercial banks, which may adversely affect CEE. On the basis of the above analysis, we propose the second hypothesis.

H2. The combination of clean energy and the banking industry may reduce CEE.

Existing studies have shown that if one region produces and consumes energy, it is likely to affect the production and consumption of energy in adjoining regions and vice versa [

52]. Clean energy is mainly supplied and consumed in the form of electricity, and the impact between regions is particularly evident [

9]. Chica-Olmo et al. [

53], for example, found that stimulated renewable energy consumption promoted both domestic economic growth and the economic growth of neighboring countries, thus showing the spatial spillover effects of renewable energy use. Compared with banking institutions, which are restricted by business premises, financial markets have stronger liquidity and wider distribution characteristics and can therefore improve the cross-regional allocation of financial resources, reduce transaction costs and mitigate information asymmetries, and provide a favorable financing environment for clean energy enterprises in neighboring regions. As clean energy is incorporated more widely in neighboring regions, economic growth is promoted, and carbon emissions are reduced, which improves the quality of the environment. Therefore, we propose our third hypotheses.

H3: The neighboring CEE can be enhanced through a spatial spillover effect, which combines clean energy with a market-oriented financial structure.

5. Empirical Results and Analysis

5.1. Spatial Characteristics of CEE

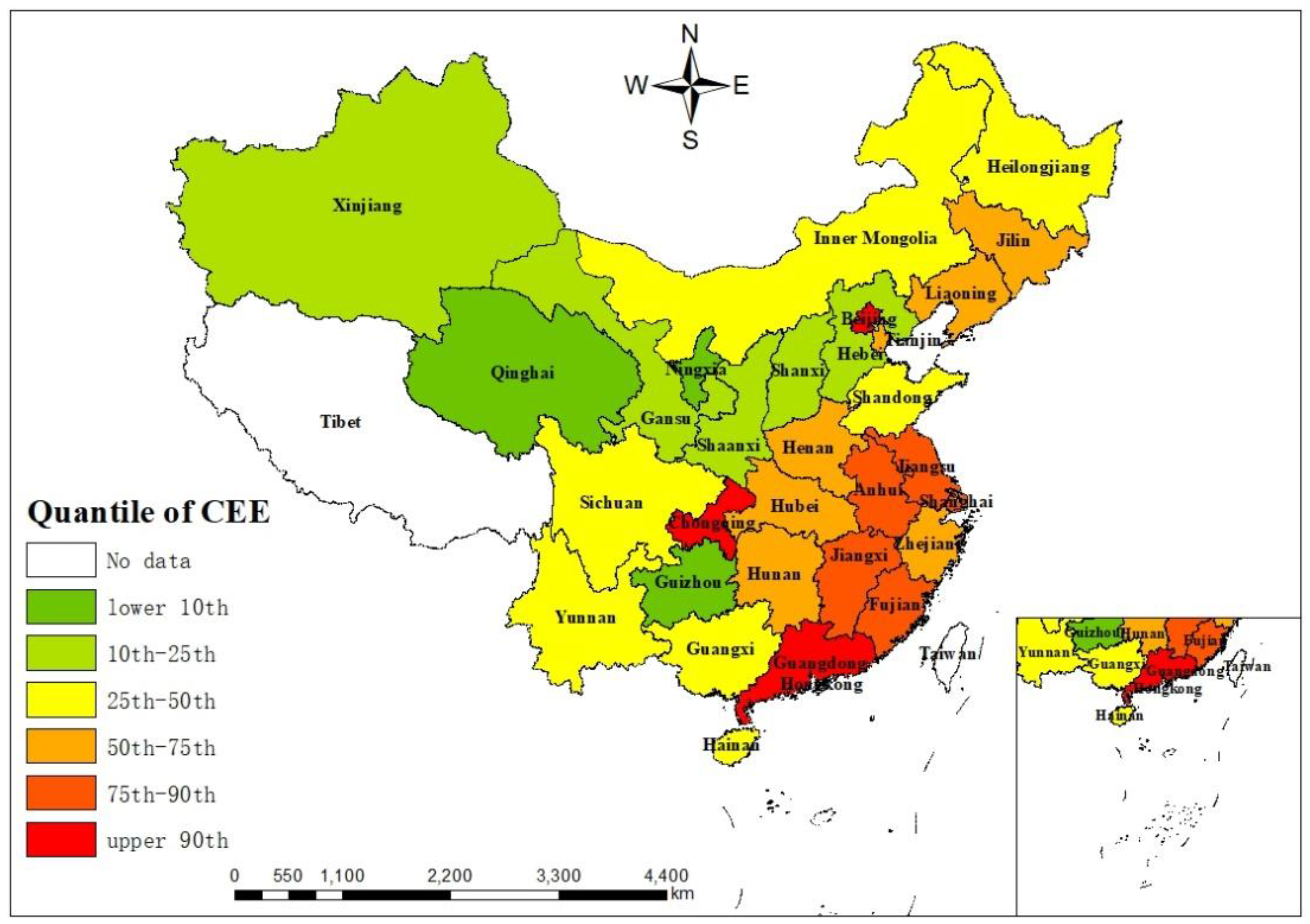

Based on Equation (6), this paper obtains the CEEs of 30 provinces in China from 2000 to 2019. The average value is only 0.172, thus indicating that the overall level of CEE is still low. Furthermore, according to the average of CEE, we choose five representative quantiles of 10%, 25%, 50%, 75%, and 90% and divide the 30 provinces into six groups (see

Figure 1 and

Table A2). It can be seen that roughly half of the provinces are below average, most of which are in the western region, and only Beijing, Guangdong, and Chongqing have efficiency values above the 90th quantile. From the perspective of regional distribution, provinces with higher efficiency are generally concentrated in eastern China, especially in the southeast region, and their efficiency values are significantly higher than those in the northwest region. In contrast, most northern provinces have low efficiency, especially those in the northwest, which demonstrates that there is an obvious imbalance in CEE across provinces and the spatial characteristics are very obvious.

5.2. Spatial Econometric Test

5.2.1. Spatial Autocorrelation Test

There is no doubt that CEE exhibits the spatial characteristics shown above. We further explore the spatial autocorrelation of CEE by estimating the Moran index (Moran’s I). The value of Moran’s I is typically from −1 to 1. If Moran’s I exceeds 0, then an observation has positive spatial correlation, whereas if it is less than 0, then it has negative spatial correlation. The specific formulation is as follows:

In Equations (18) and (19), n is the total number of regions and Xi and Xj are CEEs of regions i and j, respectively. is the average value of all sample regions, S2 is the sample variance, is the spatial weight matrix, and is the total of all spatial weights.

As shown in

Table 2, Moran’s Is for CEE from 2000 to 2019 are all positive and significant, suggesting that CEE distribution has an apparent spatial autocorrelation.

5.2.2. Spatial Econometric Model Tests

For the analysis of the spatial econometric model, a set of estimations and statistical tests must be performed on the nonspatial panel regression model first. This indicates that the fixed effects model is more effective than the random effects model based on Hausman’s test, which rejects null hypothesis in all models (see

Table A3). The two types of likelihood ratio (LR) individual and temporal effect tests pass the significance test at the 1% level, thus demonstrating that it is more appropriate that the individual and time double fixed effect model. As shown by the Lagrange multiplier test results, LMerror, R-LMerror, LMlag, and R-LMlag all pass the significance test at the 1% level, confirming Moran’s I results of the aforementioned CEE. An economic model should therefore include spatial factors as a component.

Table A4 presents the results of the Wald and LR tests, which both pass the significance test at the 1% level, demonstrating that the null hypothesis was rejected and SDM was not reduced to SLM and SEM. Hence, we adopt a double fixed effect SDM for subsequent empirical analysis.

5.3. Empirical Results and Discussion

The spatial lag term

is estimated using the maximum likelihood estimation of SDM, along with the explanatory variables. The specific results are shown in

Table 3. This indicates that the local CEE is affected by a positive spatial spillover effect and that the distribution of the CEE among regions is not random, as the coefficients of

are positive and pass the 1% significance test. The spatial distribution of regional CEE is not random.

From the empirical results shown in column (1), the coefficient of lnCE is positive but not significant, while the coefficient of W×lnCE is positive and significant, thus indicating that the positive effect of clean energy on local CEE is not obvious, but neighboring clean energy development promotes local CEE. The coefficients of FS and W×FS are both positive and nonsignificant, thus indicating that the positive effect of financial structure on CEE in local and surrounding areas is not obvious. After including lnCE×FS in column (4), the original sign and significance of lnCE and FS do not change, and the interactive coefficient is positive and passes the significance test at the 10% level, thus indicating that the combination of clean energy and the financial structure can be effective in enhancing local CEE. W×lnCE×FS is also positive and significant, thus indicating that the synergistic effect of neighboring regions can enhance local CEE.

Table 3 also shows the impact of clean energy on CEE through financial markets and bank credit. In column (5), the coefficient of lnCE×STOCK is positive and passes the significance test at the 5% level, thus illustrating that clean energy can effectively promote local CEE through the stock market, which confirms H1. W×lnCE×STOCK is also positive and significant, which indicates that neighboring clean energy generation has a positive spillover effect on local CEE through financial markets. In column (6), the coefficient of lnCE×BANK is negative and nonsignificant, thus indicating that clean energy cannot enhance local CEE through bank credit, which confirms H2. Moreover, W×lnCE×BANK is negative and significant, which reveals that neighboring clean energy generation inhibits local CEE through bank credit. The spatial spillover effect of the cointegration of clean energy and financial structure on CEE is the focus of this paper. To confirm H3, we will conduct a more in-depth empirical test.

LeSage and Pace [

68] argued that the regression coefficient of SDM did not directly reflect the marginal effect of independent variables given the existence of spatial lag terms. Therefore, they decomposed the spatial effects of cross-sectional data using the partial derivative method. Then, this decomposition method was extended to spatial panel data [

63]. The specific formulation of decomposition is as follows:

where Equation (20) is obtained by deriving explanatory variables from Equations (11)–(13). Calculating the partial derivative of the kth explanatory variable, n regions are considered, and a partial derivative matrix is generated, as shown in Equation (21):

There are two effects in the right-hand matrix: the mean value of the main diagonal elements is direct effect, which indicates that the explanatory variable has an influence on local CEE; indirect effect occurs when the explanatory variable impacts neighboring CEEs through the mean value of nondiagonal elements. The indirect, direct, and total effects are further decomposed by using a partial derivative matrix to determine the spatial influence of independent variables on CEE. It can be seen from

Table 4 that the spatial effect has been decomposed to produce the results shown here.

A study has demonstrated that the direct effects of lnCE are not significant, while its indirect effects are positive and significant at the 1% level, indicating that clean energy does not have a clear impact on local CEE, while it can significantly enhance neighboring CEE via the spatial spillover effect. It is argued that clean energy is mainly reflected in power generation and has obvious spillover effects through the “west-to-east” power transmission policy formulated by the Chinese government.

FS has both direct and indirect effects that are positive but not statistically significant, which indicates that the financial structure does not impact local and neighboring CEEs. The direct and indirect effects of STOCK are 0.0109 and 0.0223, respectively, and both pass the significance at the 5% level, which demonstrates that the stock market promotes local CEE while having obvious spillover effects on neighboring regions. The direct and indirect effects of BANK are negative, which indicates that bank credit inhibits CEE in both local and neighboring areas.

The direct and indirect effects of lnCE×FS are 0.0032 and 0.0076, respectively, and both pass the significance test at the 5% level. This shows that a 1% increase in the integration of clean energy and a market-oriented financial structure leads to a 0.0032% increase in the local CEE and a 0.0076% increase in neighboring regions’ CEE through the spatial spillover effect, which confirms H3. The direct and indirect effects of lnCE×STOCK are 0.0032 and 0.0076, respectively, and both pass the significance test, which indicates that clean energy can effectively promote local and neighboring CEEs through the stock market. The direct effect of lnCE×BANK is negative but nonsignificant, while its indirect effect is negative and significant, which demonstrates not only that clean energy inhibits the local CEE through bank credit, but also that the inhibitory effect on neighboring regions is more significant. This is explained by the fact that banking institutions emphasize risk control, and clean energy is often accompanied by its own inherent uncertainties, which makes it difficult for the banking industry to provide adequate financial support for it. As for the stock market, clean energy enterprises can directly obtain social funding through the capital market, which effectively alleviates financing difficulties and enables the long-term development of clean energy to drive local economic growth and achieve carbon emission reduction. The spillover effect of clean energy and the liquidity of the financial market also encourage the surrounding areas to increase their R&D and applications of clean energy through imitation and learning to optimize their energy structure and improve their CEE.

For the control variables, the direct effects of GOV are negative but nonsignificant, while its indirect effects are positive and significant, which can be explained as follows: Local fiscal expenditure on environmental management is limited and fails to play a decisive role in the impact of local CEE, but it can play a demonstration effect for neighboring regions and help to improve the neighboring provinces’ CEE. The direct, indirect, and total effects of IS are not significant, thus indicating that upgrading the industrial structure does not have a significant impact on the local and neighboring CEEs. This is explained by the fact that tertiary industries have developed rapidly in various regions, but industrialization is still the main driving force of regional economic growth, which indicates that the transformation and upgrading of the industrial structure remains low and has not yet had a significant effect on CEE. The three effects of ES are negative, which can be explained as follows: The production processes of enterprises with high energy consumption, such as coal, will produce a large amount of carbon dioxide given China’s current energy structure. However, the downward pressure exerted by China’s slowing economy has further restrained CEE in recent years. The three effects of TO are negative and significant, thus indicating that trade openness has a significant inhibitory effect on the local and neighboring CEEs. Among the direct effects of lnER, there are significant and positive ones, demonstrating that environmental regulations play an important role in promoting local CEE. In this manner, the “innovation compensation effect” can be achieved, and local CEE can be improved by ensuring that enterprises optimize resource allocation and improve their technological levels.

5.4. Endogeneity Test

Qu and Lee [

69] argue that the spatial weight matrix does not satisfy the null hypothesis that it is strictly exogenous, which may lead to endogeneity problems. The spatial lag variables W

2X and W

3X are used as instrumental variables in this paper to avoid endogeneity, as suggested by Zhang and Liu [

60]. Among them,

W denotes the space weight matrix and

X indicates the explanatory variables. The specific results are shown in

Table 5.

There are no significant differences in the estimated coefficients of the explanatory variables (see

Table 5) compared with the estimated results depicted in

Table 3. Additionally, the coefficients of each variable’s spatial lag terms are similar, thereby suggesting that instrumental variables can still be used to address the endogeneity of spatial weights while maintaining consistent and robust estimation results.

5.5. Robustness Check

This paper further tests the robustness of the estimates by replacing the spatial weight matrix and changing the core explanatory variables. The results are shown in

Table 6.

According to Zhang and Liu [

60], this paper employs the spatial adjacent weight matrix W01 (i.e., when two regions have a common border, the weight is 1; otherwise, it is 0) as substitute matrix to investigate whether SDM will produce significantly different results due to changes in the spatial weight matrix. Compared with

Table 3, there is no significant difference in the symbols and significance of the estimated coefficients using the substitute matrix in column (1), further indicating that the combination of clean energy and the financial structure can effectively enhance CEE. In column (2), the results show that clean energy can still effectively improve local and neighboring CEEs through stock market. In column (3), the results show that the interaction between clean energy and bank credit has a dampening effect on local and neighboring CEEs.

Nuclear energy is controversial in its ability to promote economic development and reduce CO

2 emissions [

28] compared with other types of clean energy. Additionally, it may threaten living conditions due to safety issues that have arisen in recent years. Following Chen et al. [

9], we exclude nuclear power from the clean energy indicators used in this paper and construct a new proxy variable, lnCE2, to perform a robustness test. There is no significant difference between the estimates in

Table 3 and the findings in this study. For example, the coefficient of lnCE2×FS is 0.0030 (

p < 0.05), which indicates that it still contributes to CEE. The coefficients of lnCE2×STOCK and W×lnCE2×STOCK are positive and significant, thus indicating that they improve the local and neighboring CEEs, while lnCE2×BANK and W×lnCE2×BANK are negative and similar to the results shown in

Table 5. Therefore, the estimation results are strongly robust.

5.6. Spatial Quantile Regression Results

The average effect of combining clean energy and financial structures to affect CEE is mainly obtained through the abovementioned empirical studies. Under various provinces’ CEE, this paper seeks to identify the characteristics of clean energy interaction with a market-oriented financial structure by using SQR and the 10th, 25th, 50th, 75th, and 90th quantiles for analysis. As shown in

Table 7, the estimated results are presented.

The coefficients of lnCE×FS are positive at all five quartiles, and the coefficient of the 90th quantile is 0.0032 and passes the significance test at the 10% level, while the 10th quantile is the smallest at only 0.0010. This indicates that the interaction between clean energy and a market-oriented finance can enhance CEE in various regions, and this synergistic effect is more significant in areas with higher efficiency. Accordingly, it can be concluded that clean energy impacts CEE differently in different provinces with market-oriented financial structures. Additionally, with the increase in CEE, the coefficient of W×lnCE×FS is also increased, and the coefficient of the 90th quantile reaches its maximum and is significant, which demonstrates that the impact of clean energy through a market-oriented financial structure in neighboring areas increases with the continued growth of local CEE.

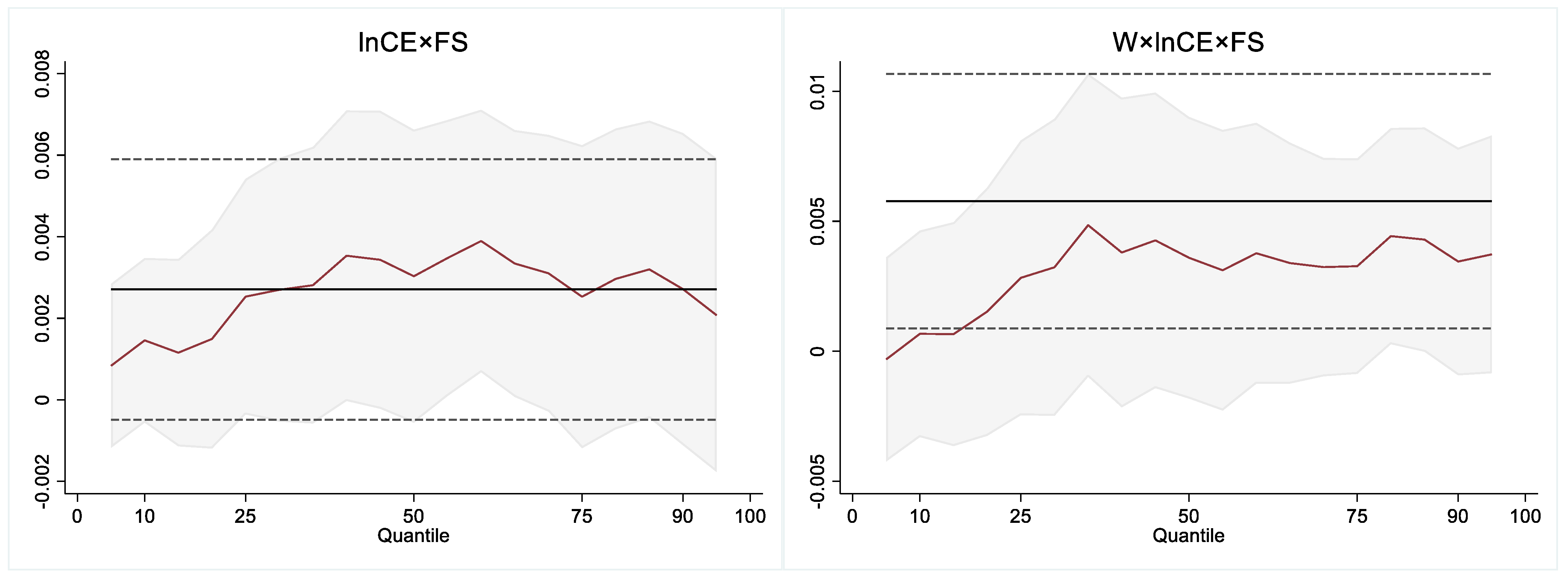

This paper plots the regression coefficients of lnCE×FS and W×lnCE×FS at all quartiles, which allows for a more intuitive description of the dynamic trajectory of the joint impacts of clean energy and the financial structures on CEE (see

Figure 2). It can be seen that the change in the coefficient of lnCE×FS is similar to an “inverted U-shaped” pattern, and its interactive coefficient represents a fluctuating upward trend in the 10th–50th quantiles, while it shows a downward trend to some extent from the 50th to the 90th quantiles. The coefficient of W×lnCE×FS shows an upward trend. Among them, the coefficient of the 5th quantile is the lowest and less than 0, and the coefficients above the 25th quantile are all greater than 0 and increasing. This indicates that the neighboring provinces’ clean energy production inhibits local CEE through market-oriented finance in regions with low efficiency (e.g., Guizhou, Qinghai, and Ningxia), while the positive role of neighboring regions will gradually increase in areas with higher efficiency. This is consistent with the estimates shown in

Table 7, where clean energy enhances local CEE through a market-oriented financial structure and the effect varies. With the increase in CEE, the stimulating effect, by which clean energy is supported by a market-oriented financial structure in neighboring areas, is gradually enhanced.

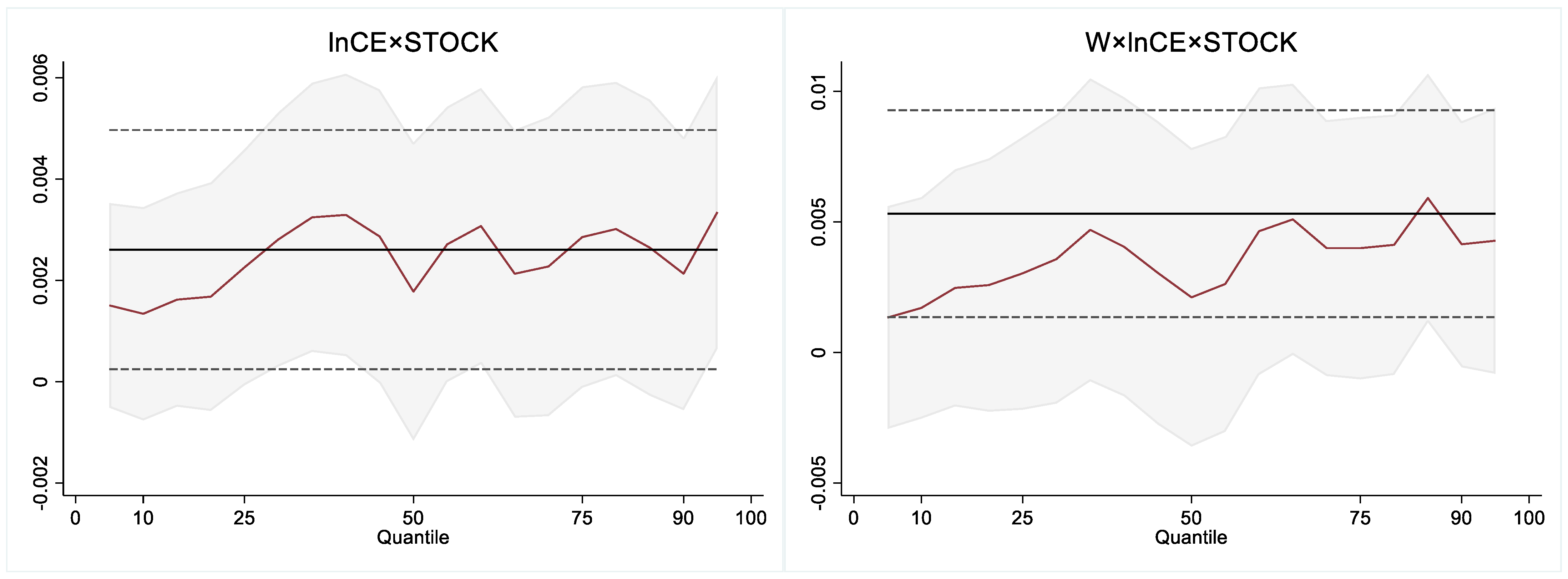

Furthermore, this paper plots the trend of the coefficients of lnCE×STOCK and W×lnCE×STOCK at all quantiles (see

Figure 3). As a whole, the coefficient of lnCE×STOCK is positive, which indicates that clean energy can enhance CEE through the stock market in all regions. The coefficients are relatively small before the 25th quantile, thus indicating that clean energy does not significantly improve CEE through the stock market in low-efficiency areas, such as Hebei, Xinjiang, Shanxi, Guizhou, Qinghai, and Ningxia. This is explained by the fact that these provinces are concentrated in the western district, where fewer clean energy companies are located and are not supported by the financial market. Meanwhile, they are rich in fossil energy resources, and the substitution effect of clean energy is not fully reflected in the local economy, which is not effective in promoting CEE. When CEE increases, there is evident volatility between the 25th and 90th quantiles, indicating that clean energy and the stock market interact differently. It is explained by the fact that different regions possess substantially different resources and financial markets. Some western provinces with high economic development, such as Sichuan, are not only relatively rich in natural resources, but also have a number of listed energy companies to support clean energy development through capital markets to improve the local economy and reduce CO

2 emissions. For regions with higher economic development, the financial market is relatively mature, but the huge demand for energy and the relative lack of natural resources increase the competition for clean energy among regions, which leads to the impact of clean energy through direct financing being unsatisfactory.

The coefficient of W×lnCE×STOCK shows a fluctuating upward trend. From the 10th to the 25th quantiles, the coefficients are relatively small, while their coefficients show higher volatility from the 25th to the 90th quantiles. This indicates that the interactive effect between clean energy and the stock market on local CEE is not obvious in the low-efficiency regions, while the neighboring provinces’ clean energy has significant spillover effects through the stock market in the higher-efficiency regions, although the differences between them are large. A possible explanation for this finding is that the cross-regional liquidity of the stock market provides financial support for clean energy development in the surrounding regions and thus improves the neighboring provinces’ CEE. As CEE rises, local governments work to develop clean energy but lack planning and coordination, which aggravates competition among provinces. Therefore, the interaction between the two is highly volatile.

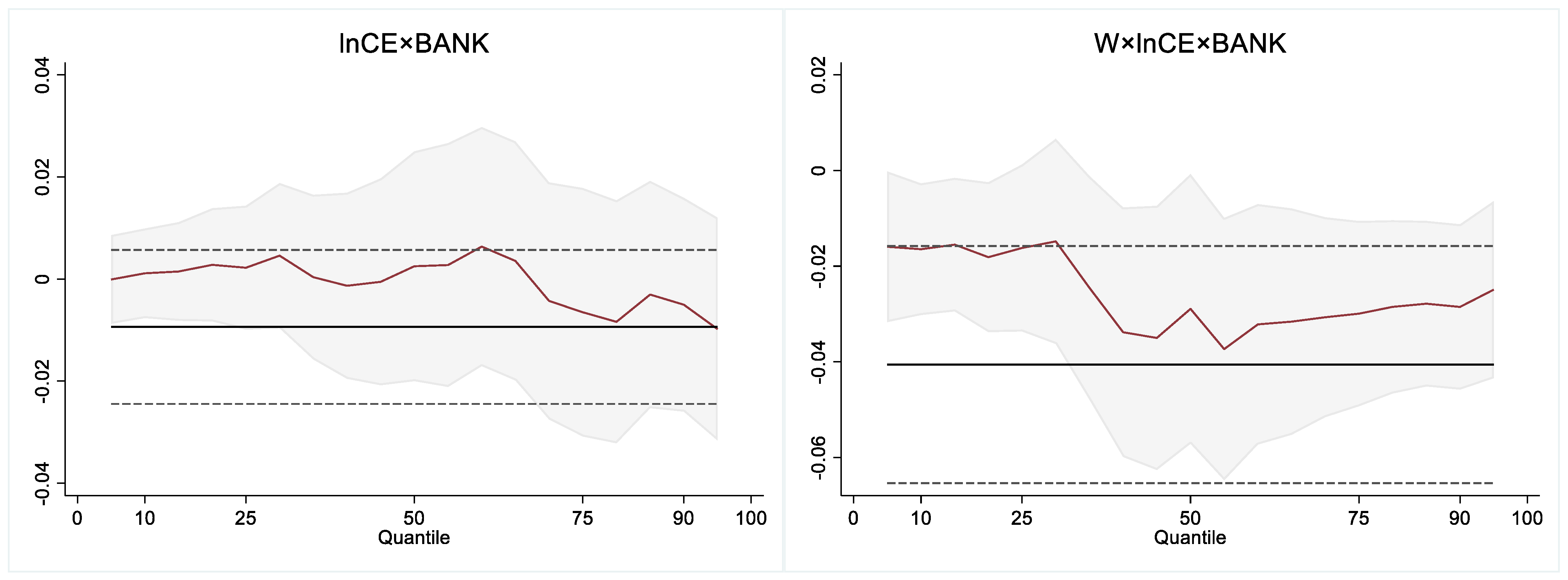

Figure 4 shows the trends in lnCE×BANK and W×lnCE×BANK. The coefficients of lnCE×BANK are less than 0 in most quantiles and obviously decrease from the 50th to the 90th quantiles, which indicates that clean energy has a mitigating effect on CEE via bank credit in most provinces, especially in high-efficiency areas. A possible explanation for this finding is that clean energy development is faced with problems such as small scales, high development costs, and longer payback periods. Meanwhile, considering the influence of natural endowments and immature clean energy technologies, banks and financial institutions are more willing to provide financing facilities for state-owned enterprises due to risk aversion in regions with high economic levels (e.g., Beijing, Guangdong, and Chongqing), while they are very cautious in providing financial support for clean energy enterprises.

As a whole, the coefficients of W×lnCE×BANK are less than 0. From the 10th to the 25th quantiles, they show a relatively steady trend, then decrease rapidly from the 25th to the 50th quantiles, and then remain low after the 50th quantile. This demonstrates that the neighboring regions’ clean energy generation suppresses the local CEE through bank credit. In the low-efficiency regions, the inhibitory effect of neighboring areas is lower, while it is more obvious in high-efficiency regions.

6. Conclusions and Policy Implications

This study analyzes the influencing mechanism of clean energy on CEE through market-oriented financial structures to fill the research gap in this area. Based on the panel data of 30 provinces in China from 2000 to 2019, this paper employs the improved NDDF to calculate the CEE of each province and applies SDM to empirically investigate the relationship between clean energy, financial structure, and CEE. Furthermore, we also apply SQR to conduct a heterogeneity analysis according to the regional division of CEE. We obtain several interesting conclusions.

6.1. Conclusions

(1) It is evident that the provincial CEE in China is spatially autocorrelative, and the local CEE is spatially positively correlated with neighboring regions. (2) A 1% increase in the integration of clean energy and market-oriented financial structure leads to a 0.0032% increase in the local CEE and a 0.0076% increase in neighboring regions’ CEE through the spatial spillover effect. The regression results of SDM are strongly robust through the endogeneity and robustness tests. Among those, clean energy impacts local CEEs positively through the stock market and significantly spatially through spillover effects to surrounding provinces, while inhibiting local and neighboring CEEs through bank credit. (3) Under the market-oriented financial structure, clean energy enhances the local CEE in all quantiles, and the impact of neighboring areas will increase gradually as the local CEE rises. From the 25th to the 90th quantiles, clean energy can greatly promote CEE through the capital market, and neighboring regions also show significant spillover effects. While the interactive effect between clean energy and bank credit suppresses the local CEE in most provinces, the inhibitory effect of neighboring regions is obvious.

6.2. Policy Implications

First, a long-term coordination mechanism should be established between regions to enhance CEE. Each provincial government should set up a coordination and leadership group to explore the balance between regional economic development and carbon emission reduction and to provide regional policy guarantee to achieve the dual goals of carbon peaking and carbon neutrality.

Second, clean energy development should be provided with more effective financial services in order to promote CEE. The central government should improve the upper-level design of the financial system, and local governments should formulate more detailed regulations to guide the flow of funds to the clean energy industry. All regions should give full play to the spatial spillover effect of clean energy and the cross-regional mobility of financial resources, and effectively integrate the two to enhance the overall CEE in China.

Third, policy makers should create support plans for clean energy that are individualized to the conditions of the local region in order to alleviate the imbalances in CEE across the country. Each local government should adopt differentiated policies and formulate targeted financial measures according to the CEE in different regions to improve the efficiency of regional clean energy capital allocation.

6.3. Discussion

Unlike the existing literature, this paper explores the spatial effects of clean energy and a financial structure on the efficiency of carbon emissions in Chinese provinces. Dong et al. [

10] argued that clean energy could be effective in enhancing CEE when financial development exceeds the threshold value. Unlike them, this study finds that the integration of clean energy with a market-oriented financial structure not only improves local CEE, but also has spillover effects on neighboring regions. In addition, Yu [

12] analyzed the heterogeneity of a financial structure affecting carbon emission intensity by dividing each region according to administrative regions. Based on the difference of CEE, this study applies the SQR model for heterogeneity analysis, avoiding the subjective factor of administrative region grouping.

At present, this paper uses provincial-level data, which can be followed by collecting firm panel data to explore the impact of the financing structure of clean energy firms on carbon efficiency from a more microscopic perspective. Additionally, this paper just only analyzes the average effect of a certain study sample by a spatial econometric model, and cannot obtain the heterogeneity influence of clean energy and financial structure on CEE in each region. The panel geographically and temporally weighted regression model can be used for further research.

{kind=link}

{kind=link}

{kind=link}

{kind=link}