Abstract

This paper focuses on the study of the “greenium”, i.e., the premium on Green Bonds (GBs) vs. Traditional Bonds (TBs) whereby investors accept lower yields of GBs vs. TBs, which is caused by the important difference between them with reference to their contribution to the green transition, specifically paying attention to the influence of the COVID-19 pandemic on it. The conjecture of this paper is that the negative shock of rates due to the pandemic crisis has increased the greenium, as it has also increased the interest in projects of the green transition. In addition, a hypothesis is made that the risk of breaking the green promises might be higher for corporations than for governments and, hence, that the greenium would be lower for corporate GBs than for government GBs. Finally, the possibility that the post-pandemic changes of the greenium might vary depending on individual GBs’ liquidity is considered. The empirical analyses provide support for the first two hypotheses but not for the third one.

1. Introduction

The literature on Green Bonds (GBs) shows that investors can accept lower yields on GBs vs. Traditional Bonds (TBs) provided that the former (latter) bonds will give a contribution to (will not be engaged in) the green transition. In this paper, the extent to which the lower yields (called the “premium” or the “greenium”) can be accepted is analyzed. Specifically, the paper looks at whether and how the greenium changed with the COVID-19 pandemic.

The focus is on the following issues:

- The literature on GBs and brief analysis on standards, disclosure and projects;

- The determinants of the greenium;

- The influence of variables such as the issued amount, the rating, the currency and the issuer type;

- The greenium growing trend as the investor confidence in the quality of GBs grows (this can be assessed from issuance information and issuer status) as well as its extent in both government bonds and private issuers.

Based on the literature on the subject, we identify and verify three significant research hypotheses:

H1.

The negative shock could increase the greenium because the pandemic crisis also increases the interest in projects of green transition;

H2.

Since the risk of breaking the green transition promises—engaging in greenwashing—was higher for corporations than for governments, the post-pandemic drop in the greenium was lower for corporate GBs than for government GBs;

H3.

Because of the financial turmoil induced by COVID-19, the post-pandemic changes of the greenium might vary depending on individual GBs’ liquidity.

The remaining part of the paper is organized as follows. Section 2 summarizes the relevant literature and recaps the GBs’ standards. In Section 3, the major benefits of issuing GBs are outlined to support the green transition in the agricultural sector. Section 4 presents the methodology and the dataset construction, while Section 5 casts the GB premium analysis. In Section 6, an analysis of the greenium over time, both pre- and post-pandemic, is performed. In Section 7, the main results are discussed. Finally, in Section 8, the main findings are summarized and conclusions are drawn.

2. Literature Review and GBs Standards

The international literature on the topic of GBs focuses on two main lines: the first is related to the growth of the market for this type of bond [1,2]; the second concerns the effective presence of a yield differential between GBs and traditional bonds and the determinants of this difference [3].

On the second topic, in [3], Zerbib tries to explain the greenium using an econometric model starting from the awareness that the phenomenon can be calculated both as a negative and as a positive yield differential with respect to the price that characterizes two types of bonds, one green and one brown. The author uses three methods to analyze data: the matching method (to link yields and prices of those bonds, one to the other), a panel regression analysis (to determine the greenium) and a cross-section analysis (to understand which bond characteristic is most decisive in creating the GB premium).

Zerbib’s study is part of a branch of the literature that leads to different results about the existence and entity of greenium [4]: the deviations between the results could be caused by the methodologies used, by the year of publication and by the GBs market evolution. In this literature, in 2016, the study of Climate Bond Initiative [5] uses a matching method on the bonds traded on the primary market, showing that there is not a negative premium on the yield. On the contrary, the study of Barclays [6], through an OLS regression on the bonds traded on the secondary market, finds a greenium of −17 bps. This result is much greater than that found two years later in [3].

In the same period, the study of Ehlers [7] shows a greenium of −18 bps, both in the primary market and in the secondary, using an initial matching method and subsequent analysis of the yield curve of the green and brown bond pairs. In 2018, the Baker analysis [8] used a large sample composed of 2083 GBs in a period between 2010 and 2016 and, through a regression on bond yields, came to an interesting result of −5.7 bps in the primary market, and a similar result in the secondary. Lastly, Fatica, Panzica and Rancan [9], with a dataset containing 1397 GBs and the same methodology used by Baker in the previous year, achieved non-homogeneous results. For this reason, the authors conclude that greenium does not appear to be present for all issuers’ categories and explain that in non-financial corporations, the proceeds of the bond are more transparent about the greenness of projects than in financial institutions. Since investors are interested in buying and investing in green products, asymmetric information on the sustainability of the underlying projects is very important to influence market prices. In this line, Bour [10] reproduced the same model as Zerbib using, as a dependent variable, the number of documents in support of the project that the companies would have realized through the GBs’ issuance. His results are statistically significant and show that companies and governments that provided complete documentation regarding the destination of the funds raised by the GBs’ issuance showed a higher value of the greenium.

Concerning the link between transparency of documentation and greenium, other works analyze the relationship between financial rating and greenium. In this context, using a sample of 60 pairs of green bonds and traditional bonds, in [11], Hinsche highlights that the bonds with a higher rating have a higher (negative) greenium than the others. Supporting this result on the higher rating score and disclosure for a higher greenium, in [12], Bachelet also shows that the GBs of institutional issuers have higher liquidity than their corresponding brown bonds, negative premiums and lower volatility. Green bonds of private issuers have much less favorable characteristics in terms of liquidity and volatility but have positive premiums compared to their brown correspondents unless the private issuer undertakes to certify the “greenness” of the bond. Then, in [13], Christian Koziol et al. carried out an experiment on the greenium through sentiment analysis, thus including in the panel regression model three variables representing Google searches for the terms ESG, Green Bonds and Sustainability. The results show an increase in greenium in the periods when interest and searches are the highest.

Given the importance of transparency for the dissemination of GBs and the study of greenium, both at the European and international levels, attention is paid to the definition of information standards. About standards and disclosure, this type of financial instrument is issued with the specific purpose to contribute to the ecological transition in order to facilitate the transformation of our economic system into a low-carbon economy, resilient to climate change and resource-efficient (European Central Bank, in [14]). With their issuance, it is possible to create a “win-win” situation in which both the issuer and the investor contribute, with mutual advantage, to the pursuit of a sustainable future (Eurosif, [15]). Therefore, GBs are sustainable finance instruments, useful to achieve the Sustainable Development Goals (SDGs) of the UN 2030 Agenda, in particular environmental goals, and aimed at pursuing the actions identified in the EU’s Action Plan on Sustainable Finance, where a European GBs issuance standard has recently been implemented.

The provision of adequate and transparent information tools is a key element in increasing investor attention, reducing the risk of greenwashing and making the GBs market efficient, to the benefit of the environmental objectives that these issuances intend to pursue. In this line, in [16], Akerlof emphasizes that investors attach greater importance to the green aspect of the bond and are more determined to invest in GB when documentation minimizes the risk of information asymmetry about the use of the proceeds. Government GBs, by nature, have precise documentation on the use of finance [17], and Fatica et al. in [9] and [18] (in 2019 and 2021 works, respectively) highlight that an increase in security in the use of money leads to a growth of greenium. Recognizing the importance of GBs’ disclosure, on January 2020, the European Commission issued the “EU Green Bond Standard” (GBS), a standardized GB model which issuers can voluntarily join with the aim of standardizing the information provided by GBs’ issuers to investors and achieving a higher level of effectiveness and transparency. Although no obligation exists in the drafting of the information to the public, except for the government GBs, most issuers comply with the GBS Framework (GBF) that, according to the Usability Guide of the EU Technical Expert Group in Sustainable Finance (European Commission, Technical expert group on sustainable finance, TEG, [19]), must have the following template:

- Section 1—Strategy and rationale that outlines the ONU Sustainable Development Goals (SDG) pursued by issuing GBs;

- Section 2—Process for selection of Green Projects, which is required to indicate the procedures for each project to comply with Taxonomy (i.e., the forecasting of committees, the Technical Screening Criteria (TSC) and the criteria for the exclusion of projects);

- Section 3—Green Projects, in which there is the description of the green projects;

- Section 4—Management of Use-of-Proceeds about the specification of funds raised and the modalities for their administration;

- Section 5—Reporting, in which the issuer indicates the frequency and way the reports on results are published.

The last two sections can be further explored in the Allocation Report and the Impact Report, documents that are not mandatory but can provide high qualitative and quantitative information content. The first aims to inform the market in a clear way about the areas of investment in which the issuer intends to use the collected financial resources; the second, on the other hand, highlights the methods and Key Performance Indicators (KPI) useful for verifying the compliance of the results with the ex ante indications. The above-mentioned European GB model conforms to the international standard called Green Bond Principles of the International Capital Market Association, which contains non-binding procedural guidelines and key components for the issuing of GBs, assisting investors by promoting access to the information useful for assessing the positive impact of their investments in GBs [20] (ICMA in 2018).

The key components are:

- Use of Proceeds;

- Process for Project Evaluation and Selection;

- Management of Proceeds;

- Reporting with External Review.

As we will see, the disclosure of the GBs represents a key element in triggering a process of increasing investor confidence, which leads to the underwriting of bonds in the awareness that the risk of greenwashing can be minimized through adequate transparency and accountability tools.

3. Green Project Hypothesis for GBs’ Issuance

The agricultural field can certainly be included among sectors to be supported through the issuance of GBs and can be seen here as an example of how information about “green” issues that have to be provided to issuers to gain their favorable interest. The analysis of the development trends in this sector highlights some main problems to be addressed in the immediate as well as in the distant future to make the sector environmentally and socially sustainable. Having healthy foodstuffs sufficient to meet the needs of an enormously growing world population cannot ignore those for the conservation of acceptable environmental conditions. To this purpose, some critical elements have to be highlighted that must necessarily be taken into consideration when adopting solutions in the agricultural production processes and when issuing GBs:

- The constant demographic increase requires:

- The possible spread of epidemics of new viruses and bacteria to be controlled;

- The yields of agricultural land to be multiplied by a significant factor;

- The crops for subsequent distribution to be guaranteed.

- The great demand for food brings with it that of an equally important quantity of water, especially in places where water resources are scarce;

- The globalization of markets and the ease of transport of goods over long and very long distances greatly increases the probability of a contamination of viruses, bacteria, insects and animal species between distant territories;

- The trend toward climate change exposes crops to increasingly real risks and requires protection from atmospheric agents;

- The increasing sensitivity to environmental aspects in developed countries and to people’s health favors organic crops, and for this reason, almost zero use of pesticides is required;

- New trends in high-tech agriculture integrated with innovative approaches to the control of crops and the means to ensure them require knowledge of the interactions between plants, systems and components of agricultural activity.

Those who implement policies should be fully aware of the trends described above when involved in building up financial resource-raising activities to develop relevant businesses. The issuance of GBs by private issuing companies can undoubtedly contribute to the achievement of important sustainability objectives.

For example, environmental friendly solutions providing protection to cultivation like agro-textile investments should be boosted as they can be purposely adapted to the need of each crop and to the characteristics of the environment in which they will be located, whether it is made up of greenhouses and artificially confined areas or open fields.

The aim must be at providing crops with the most favorable microclimate for growth with minimal use of chemical treatments, resulting in healthy and safe foods with almost no negative impact. At the same time, it will be necessary to guarantee high durability and resistance to agro-textiles together with their complete recyclability to reach full sustainability.

To this purpose, research and development activities constitute a fundamental element to improve the knowledge, characteristics and performance of the agro-textiles, and the projects to be financed may have the objective of realizing:

- (a)

- Research laboratory equipped with advanced instruments purposely designed to carry out tests there and in the open field and tailored to the needs of its production;

- (b)

- Make a group of researchers grow internally by developing knowledge and expertise in the reference sectors;

- (c)

- Collaborations with universities and research institutes to develop (from the concept to the practical application in the field) innovative ideas that solve the problems related to the production and use of agro-textiles;

- (d)

- Research projects on topics that broaden the uses of products and specialize optimal solutions;

- (e)

- Experimental campaigns among operators in the sector to detect the actual operating conditions and measure the effectiveness of the adopted solutions.

4. Methodology and Dataset Construction

The quantitative analysis was carried out in four steps: The first one was aimed at determining the existence of a differential yield between GBs and traditional bonds. The second step, based on a panel analysis, was aimed at verifying if the greenium exists due to the nature of GBs. To do this, the liquidity factor was used as an independent variable of the model in [21]. A third step, characterized by a cross-section analysis, was aimed at verifying whether the components of the GBs, as (a) the currency, (b) the issued quantity, (c) the rating and (d) the type of issuer, are determinants for the greenium factor. Lastly, the evolution of the “greenium constant” over time was determined to draw conclusions. The data to perform the econometric analysis were collected from the database by Thomson Reuter Eikon, named Refinitiv Workspace, and selected by the “Green Bond Guide”, a database containing over 70,000 GBs issued by both government and corporations. The GBs used in the sample were approved by the Climate Bond Initiative. The yield and prices data are supplied by the database Refinitiv Workspace under license and so are not freely available (requests for access to these data should be made to prof. Mariantonietta Intonti (mariantonietta.intonti@uniba.it)).

The composition of the dataset was made through four main phases.

- (1)

- All GBs having the following characteristics have been identified:

- (i)

- Issue amount over USD 100 million;

- (ii)

- Higher rating than BBB, issued by Fitch.

- (2)

- Traditional bonds were selected with:

- (i)

- The same GBs issuer;

- (ii)

- The same maturity (with a gap of up to two years of difference between the GBs and the traditional);

- (iii)

- The same rating;

- (iv)

- A similar amount emitted (certainly more than 100 mln);

- (v)

- The same currency.

- (3)

- The final dataset, composed of 32 GBs and two Traditional Bonds for each green bond, is composed as follows, keeping the same proportions of the GBs’ universe issued in 2021 and censored by the database:

- (i)

- 13 government bonds;

- (ii)

- 14 corporate bonds;

- (iii)

- 5 bond agencies.

The proportion concerning the subdivision of the type of green bond that makes up the sample is taken from the Refinitiv Workspace database. The analysis period is from 28 April 2017 to 21 January 2022 (248 weeks).

- (4)

- Finally, a dataset panel has been created, containing:

- (i)

- Changes in yields over time;

- (ii)

- Changes in liquidity over time;

- (iii)

- The rating;

- (iv)

- The quantity emitted;

- (v)

- The type of issuer;

- (vi)

- The currency.

5. Green Bond Premium Analysis

The premium of green bonds (the greenium) is defined in the literature as “a negative difference between Green bonds yields, and Traditional Bond yields based on the difference in residual liquidity” [3]. Based on this definition, the greenium was calculated using the panel fixed-effects model, “to bring out the bond-specific time-invariant unobserved effect without imposing any distribution or using any information about other bonds“ [3]. Before estimating the model, a Hausman test was applied to verify that the fixed-effects model was the best model for the considered sample.

where:

is the yield differential over time between the ask yields of the GBs and the Traditional Bond yield calculated by interpolation;

g𝑖 is the greenium;

∆𝐿𝑖𝑞𝑢𝑖𝑑𝑖𝑡𝑦𝑖,𝑡 is the change in liquidity calculated as the difference between the GBs the TBs using the Bid-Ask spread as a proxy;

𝜖𝑖,t is the error term.

is the difference between the yield of the green bond and the one of the brown bonds created via the interpolation of the two brown bonds for each green bond. The interpolation, in this case, occurred by calculating the average between the yields of the TBs chosen from GBs with similar maturities.

The difference between the yields of the securities pairs is calculated as follows:

where:

is the GBi yield at time t;

is the TBi yield at time t, calculated via interpolation of the yields of the two traditional bonds at time t).

Table 1.

Descriptive Statistics .

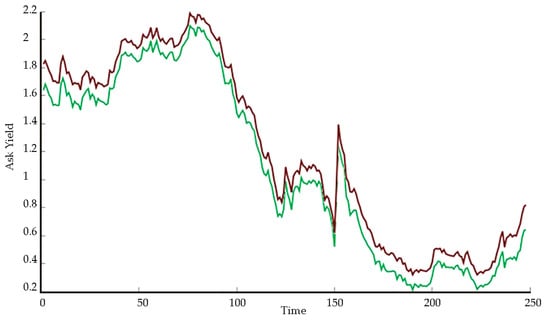

Figure 1.

The distribution of returns over time. Average values of the yields of green bonds (in green) and Traditional Bonds calculated by interpolation (in red), divided by type of issuer, versus time Traditional Bond. (Source: authors’ elaborations).

Figure 1 shows a difference between the distribution of GB yields (in green) and TB yields (in red) as a negative spread for GB. The average result of −10 bps cannot be defined as greenium because it could depend on factors extraneous to the GB and are, therefore, exogenous.

It was therefore deemed necessary to verify whether the spread of liquidity between these two types of bonds was impactful on the yield differential. With reference to their liquidity, the two types of bonds show an interesting difference in issuance. Table 2 shows the average of the issues of the different types of issuers. It also shows that the emissions of TB1 and TB2 are higher than those of the corresponding GB. Since the size of the emission could be a determinant of greenium, to understand its real impact, it was included as an independent variable in the cross-sectional analysis. Although the matching method captures part of the liquidity effects through matching based on maturities and issuance amounts, it does not capture its entirety, so the next step in analyzing the GBs premium is necessary to control the remaining liquidity.

Table 2.

The average of issuances (Values in M€).

The bid–ask spread [22,23,24], which is a widely recognized methodology, was applied to the residual liquidity calculation.

To this aim, the difference between bid and ask yields was used instead of bid and ask prices [3], and this choice was made on the basis of previous studies on the high or low frequency liquidity value approximation. Available data are neither low nor high frequency measurements (characterized by an intraday sampling) [25].

Liquidity is therefore calculated as follows:

where:

∆𝐿𝑖𝑞𝑢𝑖𝑑𝑖𝑡𝑦𝑖,𝑡 = 𝐿𝑖𝑞𝑢𝑖𝑑𝑖𝑡𝑦𝑖,𝑡GB − 𝐿𝑖𝑞𝑢𝑖𝑑𝑖𝑡𝑦𝑖,𝑡TB

Liq𝑢𝑖𝑑𝑖𝑡𝑦𝑖,𝑡GB is the measure of liquidity for GBs;

𝐿𝑖𝑞𝑢𝑖𝑑𝑖𝑡𝑦𝑖,𝑡TB is the measure of liquidity for TBs.

The liquidity for both green and Traditional Bonds is calculated as follows:

Following Zerbib’s model presented in 2019 and, therefore, having compared one green bond with two of its relevant traditional ones, the calculation of the liquidity of the former requires the following additional step.

with:

A premium for GBs is real if the regression panel with fixed effects shows a negative and statistically significant constant (gi) [3].

The results obtained by the regression “panel with fixed effects” (Table 3) clearly show the presence of a statistically significant greenium with a value of −13 bps, evident in the model constant. The independent variable of the residual liquidity appears to be close to 0 and not statistically significant. At the same time, the above data show a correct choice of bonds and an effective matching procedure for the sampled bonds, as in this case, data highlight that liquidity is not the determinant of the yield differential itself, and, therefore, of the greenium.

Table 3.

Determination of the greenium.

The Second Model

Further development is then focused on the buildup of a model that can allow understanding which qualitative variable, among those considered relevant in the literature, is more impactful on the greenium. Following Zerbib’s definition [3], greenium is the sum of time-invariant constants for each single triplet of regression.

The distribution of constants (greenium) was necessary to develop the model described above, and Table 4 shows the descriptive statistics for this distribution.

Table 4.

Descriptive statistics Greenium (gi).

In order to estimate which of the characteristics of GBs are most impactful on the greenium, some of the most important ones for a bond (issue amount, rating, currency, issue type) have been selected and transformed into dummy variables that have been inserted as independent cross-section ones with the time-invariant constant g𝑖 as a dependent variable. Their characteristics are summarized in Table 5.

Table 5.

The determinants of greenium (g𝑖).

The cross-sectional model has thus been configured as follows:

where

is the distribution of the constant coming from the regression panel fixed effect described in the first step model;

are the dummy variables vectors;

is the error term.

The analysis was carried out, split into two parts:

- The first is a complete analysis (column a in Table 6) aimed at encompassing all the possible greenium determinants: to this purpose, all the dummy variables in the model were included (excluding one per group to avoid problems related to the collinearity);

Table 6. OLS regression results. Greenium determinants.

- The second is composed of ten regressions (from (b) to (k) columns in Table 6) addressing different subsets of the specific GBs characteristics and using groups of different dummies as independent variables that represent qualitative variables related to the bonds (Table 6). For each test (a–k in Table 6), the Breuch–Pagan test has been run for non-heteroscedasticity. With regard to the dummy variables of amount issued, rating and type of issuer (Table 5), in the second part of the analysis, only one category per test was considered (e.g., in column (d) 1 for rating above AA and Government Bonds and 0 for all other categories).

6. The Greenium over Time Pre- and Post-Pandemic

With the aim of providing a complete overview of the greenium phenomenon, verifying its evolution and drawing some inferences, an analysis was carried out based on time.

The main goal was to understand whether the greenium has significantly changed in the preceding and subsequent periods of the pandemic, due to the shock of rates resulting from the sudden increase in economic instability [26]. In addition, the type of issuer (corporate and government) has been considered in the model setting. The first model is composed as follows:

where

is the yield differential between the GBs’ ask yields and the TBs’ yields calculated by interpolation of corporate bonds;

gcorp is the greenium for corporate bonds;

is the difference in liquidity (the difference between the liquidity of GBs and the liquidity of traditional corporate bonds using the bid–ask spread as a proxy).

is a dummy variable. Its value is 1 if the sample is estimated in post-pandemic time and 0 in the pre-pandemic time;

is the error term.

The second model is:

with the same meaning of (8) and reference to the government bonds.

The results of the four regressions are reported in Table 7. Results concern the calculation of the pre- and post-pandemic greenium on corporate and government bonds.

Table 7.

Determination of the greenium pre- and post-COVID-19.

The analyses show a greater amount of greenium for government bonds both in the period before the pandemic and in the following one (−0.1782 and −0.1803, respectively) as well as a lower liquidity impact (0.161). The coefficient of the dummy variable implies that for government bonds, greenium is stable. The results show values close to 0 and not significant for government bonds, unlike corporate bonds that are higher.

It was therefore necessary to graphically show the performance of the premium and liquidity of government and corporate bonds throughout the sample. To calculate the value of the differential in every single moment of time, therefore, 248 OLS have been estimated, one for every moment (t), in this case, the weeks between 28 April 2017 and 22 January 2022, and from the results, we drew the values of the constant for each estimate.

The estimated model is the following:

where

is the yield differential for every single moment of time between the ask yields of GBs and the TBs’ yields calculated by interpolation;

gt is the greenium (for every moment);

is the change in liquidity calculated as the difference between the liquidity of the GBs and the liquidity of the TBs, using the bid–ask spread as proxy;

is the error term.

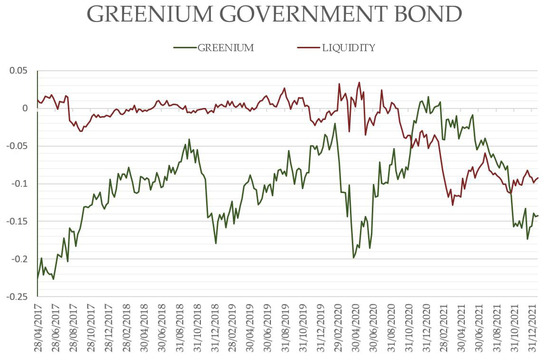

Figure 2 shows in green the evolution of the greenium over time and in red the independent variable of the liquidity calculated using the proxy of the bid-ask spread.

Figure 2.

Greenium and liquidity over time The evolution of the greenium (in green), and of the liquidity (in red) of bonds calculated through OLS regression (9) over time. (Source: authors’ elaborations).

The division of the phenomenon into two main phases can be observed. The first is a constant declining phase in the period between 2017 and the beginning of 2019; the second during the first months of 2020, after a period of stability, is a phase of sudden growth characterized by the pandemic and the first lockdown. The opposite effect, however, can be observed for liquidity. Actually, most government and non-government bonds suffered a sharp deterioration in liquidity during the most acute phase of the COVID-19 crisis, with a maximum around the third week of March 2020. Before estimating the evolution of greenium for the two different types of issuers, it is necessary to provide an overview of the phenomenon through two regressions carried out on the bonds belonging to the two types of issuers. The results (Table 8) show a much more important greenium for government issuers (−0.199), a result consistent with the previous OLS regression.

Table 8.

Greenium determination by issuer’s type.

Figure 3 explains the evolution of the greenium and the liquidity over time by type of issuer, using the same methodology applied for the determination of the differential in the most general case. Finally, in Figure 4 and Figure 5, the two differentials are compared over time, which is necessary to draw some conclusions.

Figure 3.

Greenium in corporate bond. The graph shows the evolution of the greenium (in green) and liquidity (in red) of corporate bonds calculated through OLS regression (9) for each moment. (Source: authors’ elaborations).

Figure 4.

Greenium in government bonds. The evolution of the greenium (in green) and liquidity (in red) of government bonds calculated through OLS regression (9) over time. (Source: authors’ elaborations).

Figure 5.

Greenium in government vs. corporate bonds. The evolution of the greenium for government bonds (in green), and for corporate bonds (in blue) taken from the previous analyses (Source: authors’ elaborations).

Lastly, a test was performed to estimate the presence of a structural break between the two-time intervals (pre- and post-pandemic). The test is characterized by a regression panel containing an independent variable calculated as an interaction between liquidity and the time dummy (Pre_Pandemic) as well as the dummy variable itself. To understand which one of the two types of issuers suffered the most from the lockdown and the interest rate crisis, two regressions were performed: the first for the corporate bonds and the second for the government ones. Results are summarized in Table 9.

Table 9.

Structural Break determination pre/post COVID-19.

The model for the corporate bonds is:

with

IteractionPrePandemiccorp,t, = ∆𝐿𝑖𝑞𝑢𝑖𝑑𝑖𝑡𝑦corp,𝑡 × PrePandemiccorp,t,

The model for the government bonds is:

with

IteractionPrePandemicgov,t, = ∆𝐿𝑖𝑞𝑢𝑖𝑑𝑖𝑡𝑦gov,𝑡 × PrePandemicgov,t,

7. Discussion of the Results

Considerations coming from the elaboration process can be grouped as follows:

- (1)

- In Table 6, unlike what Zerbib stated in 2019 in [3], the greenium determinant’s analysis allows us to conclude that the bonds with a lower S&P rating are not statistically significant (c). However, a positive influence of government bonds on the greenium can be highlighted in comparison with the other types (d) (f) (j) (k) of 0.67, 0.79, 0.91 and 0.92, respectively. This result seems to be due to their nature, typically safer and more transparent than corporate or agency bonds;

- (2)

- A second interesting result comes from the analysis concerning the rating. A higher financial rating has a negative influence on the greenium, even if they are linked to government bonds;

- (3)

- The currency does not significantly influence the greenium in any of the analyzed cases. The complete analysis (a) shows results similar to that variable. Government bonds correspond to the highest influence on the greenium compared to other types; in this case, 0.97 against 0.64 of the corporate bonds. The other included factors do not appear to be statistically significant, although a positive influence on bonds with an issue exceeding 1000 mln (0.27) and a negative influence on bonds with a rating above AA of 0.33 can be observed.

Thus, the conclusions are in line with [9] and [27] (Climate Bonds Initiative in 2017): “Greenium does not seem to be present for all categories of issuers”. One of the possible reasons is that the greenium may be linked to a different degree of transparency observed by the different issuers. In particular, states seem to be more attentive to the information dissemination at the time of issue and subsequent reporting in order to keep their reputation and rating high.

Finally, the evolution of the greenium over time was analyzed. The relevant regressions carried out have outlined a quite clear evolution: in the period between 2017 and 2020, greenium tends to have a higher value, which corresponds to a lower impact. As a consequence, during the pandemic, the differential dramatically decreased, thus corresponding to a higher greenium value. In general, estimates from regressions reported in Table 7 show that government bonds have a broader differential than corporate ones (in the sample, pre- to post-pandemic government bonds go from −0.1782 to −0.1803, against pre- to post-pandemic corporate bonds going from −0.11 to 0.006). It is therefore evident that the greenium was affected by the pandemic turnaround, being higher in government bonds, while lower in corporate ones.

In addition, in government bonds, the variation and the evolution of the differential has not been found to be dependent on changes in liquidity caused by the interest rate crisis. The liquidity ratio, actually, is very small and not significant for government bonds in the period before the pandemic; that was even lower than for corporations in the following period (a pre-pandemic value of 0.383 against a post-pandemic one of 0.310). The interaction coefficients and the pre- and post-pandemic dummies are statistically significant at a level of significance of 0.01, showing that, in the period after the pandemic crisis, the yield differential decreased for corporate bonds (−0.113) and remained stable for governmental ones (0.03). The significance of the coefficients shows the presence of a structural break between observations 150 and 151, corresponding to the dates of 6 March 2020 and 13 March 2020.

The results are confirmed by the tests on linear restrictions which, in each performed regression, have a value of the F statistic higher than the critical value, rejecting the null hypothesis (all coefficients have a null value).

8. Conclusions

Some interesting conclusions can be drawn from the multi-step analysis here proposed, with reference to the initial research hypotheses.

After a first step focused on measuring the greenium between Green Bonds and Traditional Bonds, a panel analysis was carried out aimed at verifying if the greenium exists due to the nature of GBs. To do this, the liquidity factor was used as an independent variable of the 2016 Abudy model in [22].

A cross-section analysis was provided as a third step in order to verify whether the components of the GBs, as (a) the currency, (b) the issued quantity, (c) the rating and (d) the type of issuer, were determinants for the greenium factor.

Lastly, the evolution of the greenium over time had to be determined.

Thus, the starting point was the study of the differential yield between Green Bonds and Traditional Bonds created by interpolation. A panel analysis was carried out and made it possible to state whether this greenium was due to the liquidity of the bonds, where the liquidity is calculated through a bid–ask spread. Then, it was possible to evaluate what characteristics of the bonds had a positive impact on the greenium performing a cross-section analysis.

Finally, an analysis was carried out to understand whether and how the greenium changed with the COVID-19 pandemic, considering its time frame (2017–2021).

Based on the three hypotheses initially formulated and of the analyses carried out, it can be stated that the negative COVID-19 shock increases the greenium, especially for government GBs more than for corporate ones, and that the post-pandemic changes of the greenium do not depend on GBs’ liquidity.

Therefore, the present empirical analyses succeeded in providing support to hypotheses H1 and H2 and not to H3.

Author Contributions

Although the paper is the result of a common effort, G.F. wrote Section 1 and Section 8, M.I. wrote Section 2 and Section 7, G.S. wrote Section 3, L.S. wrote Section 4, L.S. and M.D.L. wrote Section 5, M.D.L. wrote Section 6. Grateful to M.D.L. for data collection. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Access to these data needs a request to Mariantonietta Intonti (mariantonietta.intonti@uniba.it).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Wood, D.; Grace, K. A Brief Note on the Global Green Bond Market; The Houser Center, IRI working Paper; European Union: Brussels, Belgium, 2011. [Google Scholar]

- Elliott, T.; Zhuang, M. Transnational governance in China’s green bond market development. J. Environ. Policy Plan. 2014, 21, 391–406. [Google Scholar] [CrossRef]

- Zerbib, D. The effect of pro-environmental preferences on bond prices: Evidence from green bonds. J. Bank. Financ. 2019, 98, 39–60. [Google Scholar] [CrossRef]

- Bloomberg. Investors Are Willing to Pay a “Green” Premium; Bloomberg New Energy Finance Report; Bloomberg: Lexington, KY, USA, 2017. [Google Scholar]

- Climate Bonds Initiative. Green Bonds Highlights. 2016. Available online: https://www.climatebonds.net/files/files/2016%20GB%20Market%20Roundup.pdf (accessed on 15 December 2021).

- Barclays. The Cost of Being Green. Credit Research. 2015. Available online: https://www.environmentalfinance.com/assets/files/US_Credit_Focus_The_Cost_of_Being_Green (accessed on 15 December 2021).

- Ehlers, T.; Packer, F. Green Bond Finance and Certification; BIS Quarterly Review September; BIS: Basel, Switzerland, 2017. [Google Scholar]

- Baker, M.; Bergstresser, D.; Serafeim, G.; Wurgler, J. Financing the Response to Climate Change: The Pricing and Ownership of U.S. Green Bonds; National Bureau of Economic Research, Inc.: Cambridge, MA, USA, 2018. [Google Scholar]

- Fatica, S.; Panzica, R.; Rancan, M. The Pricing of Green Bonds: Are Financial Institutions Special? Working Papers 2019 07; Joint Research Centre, European Commission: Brussels, Belgium, 2019. [Google Scholar]

- Bour, T. The Green Bond Premium and Non-Financial Disclosure: Financing the Future, or Merely Greenwashing? Master’s Thesis, Maastricht University, Maastricht, The Netherlands. Available online: https://finance-ideas.nl/wp-content/uploads/2019/02/msc.-thesis-tom-bour.pdf (accessed on 30 January 2022).

- Hinsche, C. A Greenium for the Next Generation EU Green Bonds Analysis of a Potential Green Bond Premium and Its Drivers; Analysis of a Potential Green Bond Premium and Its Drivers. CFS Working Papers Series n. 663; CFS: Mount Barker, Australia, 2021. [Google Scholar]

- Bachelet, M.; Becchetti, L.; Manfredonia, S. The Green Bonds Premium Puzzle: The Role of Issuer Characteristics and Third-Party Verification. Sustainability 2018, 11, 1098. [Google Scholar] [CrossRef]

- Koziol, C.; Proelss, J.; Roßmann, P.; Schweize, D. The Price of Being Green; Finance Research Letters, Forthcoming; Elsevier: Amsterdam, The Netherlands, 2022. [Google Scholar]

- European Central Bank. Implications of the Transition to a Low-Carbon Economy for the Euro Area Financial System; European Central Bank: Frankfurt, Germany, 2019. [Google Scholar]

- Eurosif. European Study SRI; Eurosif: Gewest, Belgium, 2018. [Google Scholar]

- Akerlof, G.A. The market for “lemons”: Asymmetrical information and market behavior. Q. J. Econ. 1970, 83, 488–500. [Google Scholar] [CrossRef]

- Doronzo, R.; Siracusa, V.; Antonelli, S. Green Bonds: The Sovereign Issuers’ Perspective; Mercati, Infrastrutture e Sistemi di Pagamento, n. 3; Banca d’Italia: Rome, Italy, 2021. [Google Scholar]

- Fatica, S.; Panzica, R.; Rancan, M. The pricing of green bonds: Are financial institutions special? J. Financ. Stab. 2021, 54, 100873. [Google Scholar] [CrossRef]

- European Commission. Technical Expert Group on Sustainable Finance (TEG); European Union: Brussels, Belgium, 2019. [Google Scholar]

- ICMA. Green Bond Principles; ICMA: Zürich, Switzerland, 2018. [Google Scholar]

- Abudy, M.A.R. How Much Can Illiquidity Affect Corporate Debt Yield Spread? J. Financ. Stab. 2016, 25, 58–69. [Google Scholar] [CrossRef]

- Beber, A.; Brandt, M.W.; Kavajecz, K.A. Flight-to-Quality or Flight-to-Liquidity? Evidence from the Euro-Area Bond Market. Rev. Financ. Stud. 2009, 22, 925–937. [Google Scholar] [CrossRef]

- Dick-Nielsen, J.; Feldhütter, P.; Lando, D. Corporate bond liquidity before and after the onset of the subprime crisis. J. Financ. Econ. 2012, 103, 471–492. [Google Scholar] [CrossRef]

- Chen, L.; Lesmond, D.; Wei, J.A. Corporate Yield Spreads and Bond Liquidity. J. Financ. 2007, 62, 119–149. [Google Scholar] [CrossRef]

- Fong KY, L.; Holden, C.W.; Trzcinka, C.A. What Are the Best Liquidity Proxies for Global Research? Rev. Financ. 2017, 21, 1355–1401. [Google Scholar] [CrossRef]

- Fatica, S.; Panzica, R. Sustainable Investing in Times of Crisis: Evidence from Bond Holdings and the COVID-19 Pandemic; JRC Working Papers in Economics and Finance; JRC: Brussels, Belgium, 2021. [Google Scholar]

- Climate Bonds Initiative. Green Bonds Highlights; Climate Bonds Initiative: London, UK, 2017. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).