1. Introduction

As society progresses and develops, social contradictions are constantly changing, but world poverty has always been a major issue. To improve the lives of people, the government and scholars began to pay attention to the role of financial development in poverty alleviation. Studies have found that financial development can promote economic development, so people began to study the relationship between financial development and poverty. As China’s economy shifts from high-speed development to high-quality development, the impact of green finance on poverty should be considered from the perspective of sustainable economic development. Despite not having developed a green finance index system from the national level, many developing countries have prioritized green finance development as a core strategy of national development. For example, the fourteenth five-year period is the critical period and window period for carbon peak. The Central Committee of the Communist Party of China and the State Council have entrusted the financial system with the glorious mission and important task of supporting green, low-carbon, and high-quality development in the financial sector in the new period and new stage. The financial sector should focus on carbon peak and carbon neutrality, plan of green finance, and give priority to the three supporting functions of finance (Zhao, 2022) [

1].

As the largest developing country, poverty and relative poverty have always been an important problem restricting China’s development. In order to better solve the problem of poverty and relative poverty, we must deeply understand the causes of poverty and relative poverty. Since China’s reform and opening up, the Chinese economy has experienced rapid development, but there has been a wider income gap for urban people and rural people, due to the dual economic structure of urban and rural areas. This phenomenon is mainly driven by urban and rural development patterns; the developmental pattern mainly makes the rural develop by small-scale peasant economy, unable to realize the rapid development of economy. In conclusion, the gap between urban and rural income continues to widen. Starting from the urban-rural dual economic structure, using green finance to alleviate rural poverty, urban poverty, and relative poverty between cities, and rural areas from various aspects through a spatial econometric model, is discussed in this paper.

White (1996) first put forward the concept of environmental finance. By analyzing the role of corporate finance, he concluded that investment and financial institutions in solving environmental threats and environmental protection must be developed in a coordinated manner, and it is important to promote green finance, which is the embryonic form of green financing [

2]. Scholten (2006) deeply studied the internal relationship between sustainable development and finance and proposed that green finance is to seek the optimal solution of environmental protection through a variety of financial tools [

3]. Soundarrajan and Vivek (2016) studied the effectiveness of green finance in India’s industrial development. They found that green finance can be effectively applied to India’s industrial system, reduce environmental risks, and improve ecological integrity [

4]. The study by Ngan (2018) identified and assessed the risk factors for slow growth in green economies in developing countries. As a result, financing risk is the main concern of the industry, followed by technology risk and supply chain risk [

5]. Taghizadeh-Hesary and Yoshino (2020) found that investors can benefit from the spillover effect of green finance, using the relevant investment theory model by the use of related investment theoretical models, so as to expand the development level of green finance, reduce the risk of green finance, and improve the return rate of green energy [

6]. Green finance policies are discussed by Yu et al. (2021) in relation to how they resolve financing constraints of firms for green innovation. Despite green finance policies’ ability to alleviate financing restraints on green innovation, generally, private enterprises are less likely to have access to green credits. In spite of this, these enterprises with severe financing constraints are relatively innovative [

7].

The World Bank points out that the poor population’s average income is less than $100 by linking the poor with the gross national product. The main cause of poverty has been found to be urban and rural dual structures in a number of studies. The urban-rural dual structure is generally considered to be an economic structure in which urban economy and small-scale peasant production coexist. Urban economy is dominated by modern industry, while rural economy is dominated by small-scale peasantry, which leads to the transfer of the rural labor force to central cities and towns. This development model makes urban people richer and rural people poorer. The existence of the urban-rural dual structure requires that we should separate the rural and urban areas for discussion and put forward a more reasonable poverty reduction plan. This paper divides poverty into urban poverty and rural poverty, and this study examines how green finance can alleviate two types of poverty.

At present, there is little research on the effect of green finance on poverty alleviation, but there is more research on the effect of financial development. Financial development’s impact on scholars and poverty reduction are mainly divided into several representative views.

First, poverty alleviation is believed to be a result of financial development. Beck et al. (2007) investigated the relationship between finance, inequality, and poverty through empirical research [

8]. Poor people’s income levels were improved by financial development and reduced the inequality of income to a certain extent. South Africa’s financial development, economic growth, and poverty reduction are examined by Odhiambo (2009) [

9]. According to the study’s empirical findings, both financial development and economic growth are both responsible for poverty reduction in South Africa. AnneWelle–Strand (2010) compared several poverty eradication tools and found that microfinance can alleviate poverty more than social integration or institutional construction [

10]. Inoue and Hamori (2011) investigated the impact of financial deepening on poverty reduction in India. In controlling international openness, the inflation rate, and economic growth, empirical results demonstrated that financial deepening significantly reduces poverty [

11]. Abosedraet (2015) used data from 1975 to 2011 to analyze the relationship between Egyptian financial development and poverty reduction. He found that, if domestic credit to the private sector was used to indicate financial development, financial development could reduce poverty [

12]. Park (2015) selected data from 37 Asian economies to test the impact of inclusive financial development on poverty and income inequality [

13]. According to the results, inclusive financial development reduced poverty and narrowed the income gap. Li and Wang (2017) found that there are some limitations in the practice of financial poverty alleviation, but with the help of internet finance there can still be benefits from financial markets [

14]. Raberto et al. (2016) found that there was a significant negative correlation between financial development and poverty through empirical research [

15]. Meghana et al. (2020) found that the poverty rate has decreased due to financial deepening and that financial deepening will make rural areas migrate to the tertiary industry in urban areas, thus reducing the poverty level in rural areas [

16]. David and Varaidzo (2020) found that financial inclusion is helpful to achieve seven of seventeen sustainable development items. Using simple linear regression, they found that the reduction of small-scale agricultural production is strongly influenced by financial inclusion. Therefore, the government of Zimbabwe must implement the financial inclusion policy in an all-round way to ensure the realization of the poverty reduction and poverty alleviation task [

17]. Xiong (2022) investigated the relationship between digital inclusive finance and poverty reduction, using regional economic development as an intermediary variable. The study revealed a threshold effect of digital finance on poverty alleviation, where an increase in the threshold led to a gradual increase in the poverty reduction effect of digital inclusive finance [

18]. Li (2022) focused on rural areas and explored the impact of inclusive finance on poverty reduction, using rural income as an intermediary variable. The study found that inclusive finance can promote people’s income in Xinjiang, reduce poverty at a deeper level, and increase farmers’ income [

19]. Zhao (2022) and Yu (2021) analyzed the impact of digital inclusive finance on narrowing the urban-rural income gap using the intermediary effect model and the primary distribution theory. They found that digital inclusive finance has significant regional heterogeneity, but overall, it can effectively narrow the urban-rural income gap [

20,

21]. Finally, Song (2023) investigated the impact of digital finance on agricultural income from multiple perspectives using multiple intermediary effect models. The study revealed that digital finance can improve investment and land circulation to increase agricultural income but can also reduce labor force [

22].

Second, financial development has a negative effect on poverty alleviation. Ravallion (1997, 2001) found that finance can alleviate poverty to some extent, but the inequality caused by finance also makes the poverty level deeper [

23]. According to Maurer and Ha (2007), financial development can contribute to economic growth, but economic development often flows to high-income groups, and low-income people cannot get more funds, which will eventually widen the income gap and deepen the poverty level [

24].

Third, it is unclear how financial development affects poverty alleviation. Greenwood and Jovanovic (1990) proposed that, when poor people have a low income at the beginning of their lives, they will not be able to obtain the financial services they want, so poverty cannot be effectively solved; when the initial income of poor people is very high, it will be easy for people to obtain financial services, and the poverty level will be reduced. Financial development has a complex impact on poverty alleviation, which is shown in the Kuznets curve, namely, the influence of financial development on income reduction shows a downward U-shaped trend [

25]. Financial development and poverty in developing countries were examined by Perez-Moreno (2011). No Granger causality between poverty and financial development was demonstrated by the analysis [

26].

Green finance has the potential to promote sustainable development and innovation in enterprises, leading to economic growth and poverty reduction. Recent studies by Ji (2020), Yang (2022), and Li (2022) indicated that enterprises with strong green social responsibility enjoy lower financing costs and are encouraged to undertake more social responsibilities, thereby promoting the common development of both enterprises and society [

27,

28,

29]. Cao’s (2021) analysis of corporate credit policy revealed that green credit can increase long-term bank credit and reduce the risk of polluting corporate risk mismatch [

30]. Dong (2022) suggested that listed companies should promote green innovation and enterprise transformation, as green finance can reduce long-term debt ratios and foster high-quality development [

31]. Xiang (2022) and Li (2022) found that external financing favors green innovation, and government subsidies can increase corporate development subsidies to a certain extent, while green finance promotes green innovation through debt financing and equity financing [

32,

33]. Meanwhile, Chai (2022) and Peng (2022) discovered that green credit plays an important role in corporate financing for heavily polluting enterprises, helping them obtain more funds to support their upgrading and transformation [

34,

35]. Lai’s (2022) study on the impact of green credit on new energy companies found that it not only reduces financing costs, but also directly increases corporate value, with a long-term sustainability effect [

36]. As a result, more scholars have begun to explore the impact of green credit on financing efficiency, revealing that, while the overall financing efficiency of Chinese enterprises has been restricted, the improvement of the green financial environment has led to significant enhancements (Yu, 2022; Li, 2022; Ming, 2022) [

37,

38,

39].

Lili Jiang et al. (2020) assessed poverty alleviation through green finance and found that green finance is helpful for poverty alleviation, but there is room for improvement. Firstly, the method of year-by-year construction is adopted in the construction of the green finance index. As a result, green finance development index comparisons cannot be done in time. Secondly, in the empirical study, poverty is measured by per capita consumption expenditure, but it is not intuitive to use this index as the proxy variable of poverty. Thirdly, the spatial effect of poverty is not considered in this paper. Fourthly, the article does not consider the urban-rural dual structure of poverty in China [

40].

Compared with the existing research, improvements are made in the following areas in this paper: (1) the linear and nonlinear relationship between green finance and relative and absolute poverty is studied from multiple perspectives; (2) using the number of urban and rural poor people in China as the proxy variable of poverty, which can more directly reflect the poverty level in China and can also further analyze the impact of green finance on poverty alleviation under the dual structure of urban and rural areas; (3) previous studies have primarily focused on linear studies, but this paper aims to expand the analysis by introducing a semi-parametric spatial lag model to study the dynamic change process of green finance poverty reduction from a nonlinear perspective. This approach provides a foundation for more nuanced and quantitative studies of the impact of green finance on poverty reduction; (4) in addition, this paper also introduces scientific and technological progress as an intermediary variable to further clarify the impact mechanism of green finance on poverty reduction. This allows for a deeper exploration of the complex relationship between green finance, technological progress, and poverty reduction, and provides theoretical support for subsequent analysis.

4. Conclusions and Policy Analysis

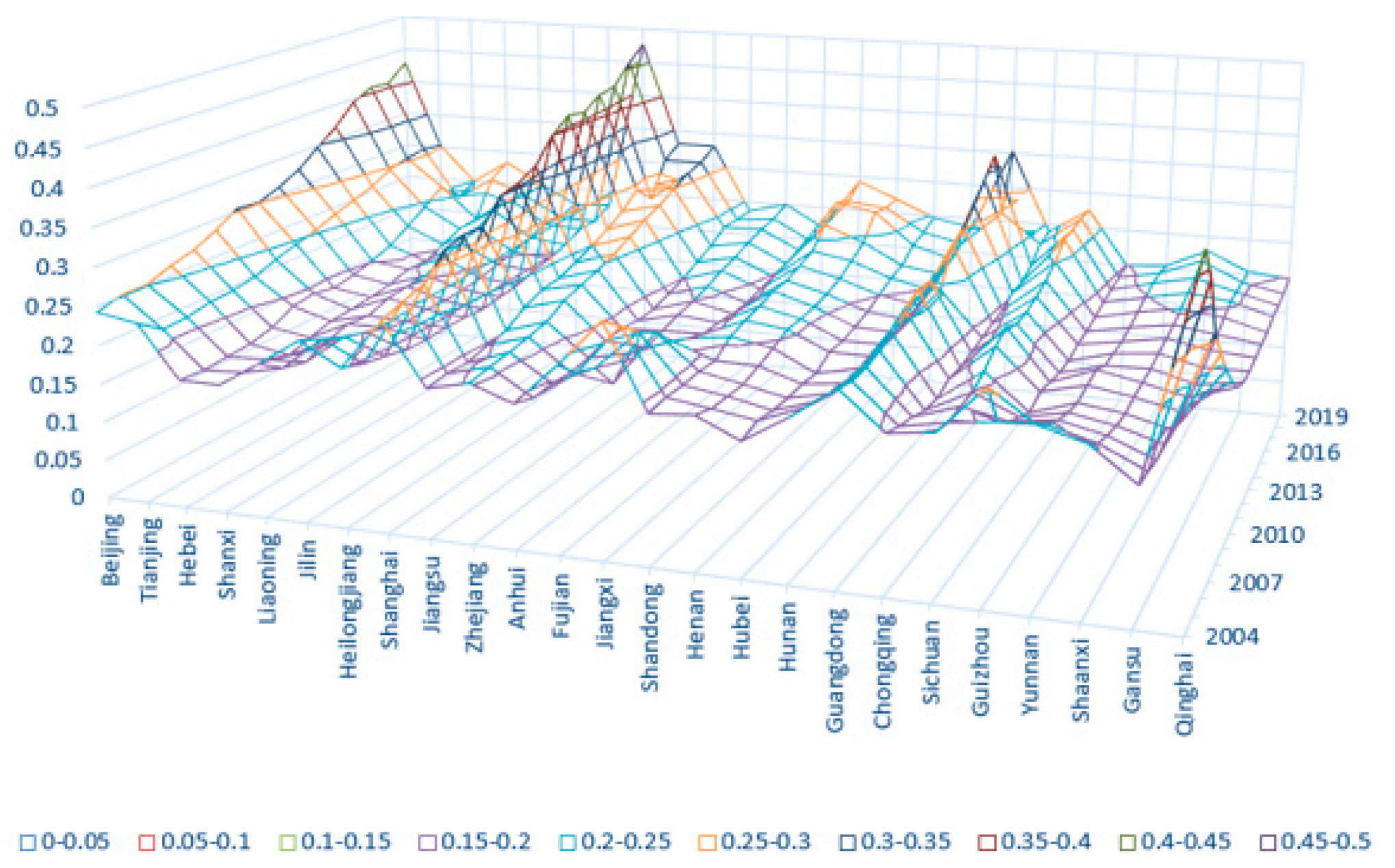

The improved entropy weight method is used in this paper to calculate green finance development levels in Chinese provinces and finds that China’s green finance development level by province is generally showing an upward trend. Through the spatial econometric model, the paper discusses whether there are positive and negative spatial spillovers among provinces. At the same time, the semi parametric spatial lag model is used to describe the partial derivative of green finance to poverty and the path map of green finance to poverty change. From the results of spatial measurement, rural and urban poverty are negatively impacted by the development of green finance, and the effect of green finance on the poverty alleviation of urban areas is better than that of rural ones. Meanwhile, at the beginning of the development of green finance, green finance will aggravate the relative poverty of urban and rural areas, but with the continuous increase of green finance, green finance will alleviate the relative poverty of urban and rural areas to a certain extent. In conclusion, this study revealed that scientific and technological progress plays an intermediary role in the relationship between green finance and poverty reduction. Compared to previous research, this study takes a more comprehensive approach to poverty reduction by examining multiple poverty indices, including absolute poverty (both urban and rural) and relative poverty, to analyze the impact of green finance on poverty from various angles. Additionally, this study takes into account regional linkages and employs a spatial measurement model to more accurately measure the relationship between green finance and poverty. The non-linear results provide valuable insights into the dynamic changes of green finance and poverty. Moreover, this study extends the existing literature by introducing scientific and technological progress as an intermediary variable, aiming to uncover the underlying mechanism linking green finance and poverty reduction. Overall, these methodological and conceptual contributions enhance our understanding of the complex relationship between green finance and poverty reduction.

This study has significant policy implications for poverty alleviation. Policymakers need to expand their vision when developing poverty reduction policies, consider the sustainable development goals, and encourage the development of green finance by creating a supportive regulatory environment. The government should implement policies to ensure adequate financing for enterprises, improve financing efficiency, and promote technological innovation. It is also important to strengthen international cooperation to ensure sufficient green financial funds and to promote economic development to increase people’s income. To achieve the goal of poverty reduction, policymakers should prioritize improving the access of low-income families, small enterprises, and marginalized communities to green finance, broaden the scope of green finance, and achieve a common reduction of relative and absolute poverty. Additionally, policymakers should focus on investing in green industries to create more job opportunities and income for residents in low-income regions, which would promote high-speed and sustainable economic development. These policy recommendations can effectively use green finance to reduce poverty levels and promote sustainable development. Decision-makers should take these suggestions into account when developing policies to ensure that green finance is utilized to its fullest potential in poverty alleviation efforts.

This article provides valuable insights into the relationship between green finance and poverty. However, it is important to acknowledge some of the limitations of this study. Firstly, the construction of green finance indicators used in this study is not yet comprehensive enough due to data limitations. Although indicators from three dimensions were used, there is still room for improvement. Therefore, future research should aim to improve the accuracy of China’s green finance index by incorporating more comprehensive and reliable indicators. Secondly, the mechanism by which green finance affects poverty reduction should be further explored. Although the study finds that technological progress is one pathway through which green finance can reduce poverty, there are other complex pathways that need to be further examined. Therefore, future research should explore additional impact pathways to better understand the relationship between green finance and poverty. To address these limitations, future research should aim to improve the accuracy and comprehensiveness of green finance indicators and explore additional pathways through which green finance can reduce poverty. By doing so, we can gain a deeper understanding of the relationship between green finance and poverty reduction and develop more effective policies to promote sustainable development and poverty reduction.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}