1. Introduction

In the post-epidemic era, the world will face a series of severe challenges such as rapid economic decline, industrial chain restructuring, and intensified financial risks, and technological innovation has increasingly become a breakthrough for countries to cope with the impact of public health events and achieve economic growth [

1]. Based on China’s major strategic achievements in epidemic prevention and control, how to accelerate digital transformation and drive high-quality economic development with scientific and technological innovation has become an urgent problem to be solved. As the backbone of building an innovative country, small and medium-sized enterprises (SMEs) should seize opportunities and cope with challenges in the context of complex changes in the macro environment and continuous adjustment of industrial structure [

2]. However, the technical route for the development of China’s SMEs has not yet been finalized, and the profit model has not yet stabilized. The traditional financial model led by banks cannot achieve the dual performance goals of economic and social benefits of SMEs due to risk uncertainty, adverse selection, credit discrimination, and other phenomena [

3]. The funds required for enterprise innovation are difficult to meet the needs of high-quality R&D and innovation by relying only on endogenous financing, and financing constraints have become the “stumbling block” for enterprises to carry out innovation activities.

The mature experience of the international market tells us that the support of capital is particularly important, and scientific and technological innovation is inseparable from the optimal allocation of resources guided by the market and the government and the improvement of the incentive and constraint mechanism. Developed countries such as the United Kingdom and the United States attach great importance to the development of digital inclusive finance. The digital inclusive financial business in the United States includes not only traditional financial business but also new financial services such as robot consulting and big data wealth management, building a complete digital inclusive financial chain [

4]. The UK has also been focusing on nurturing the fintech sector. In 2010, the UK established the Digital Technology Cluster Science and Technology City in London. The UK’s Financial Supervisory Authority launched the Financial Regulatory Sandbox in 2016 to provide a safe “test zone” for fintech development [

5]. Digital inclusive finance, Internet finance, and financial technology are a series of digital technology and financial services innovations with a combined genealogical concept [

6]. Digital inclusive finance was first proposed at the 2016 Hangzhou G20 Summit, and generally refers to all formal financial service actions that promote inclusive finance through the use of digital financial services [

7], has better data processing advantages than inclusive finance, higher low-risk than Internet finance, and more accurate inclusiveness than digital finance [

8].

Can digital inclusive finance truly alleviate the financing problems of SMEs and improve their technological innovation capabilities? Is the effect of digital inclusive finances on the innovation incentives of SMEs in different regions and industries heterogeneous? Is its influence process and its transmission mechanism regulated by external factors? This series of problems needs to be excavated and condensed. Therefore, objectively and accurately evaluating the stimulating effect of digitally inclusive financial business on the innovation of SMEs can not only provide new ideas for supporting the technological innovation of SMEs but also have important theoretical significance and practical value for the development and improvement of digitally inclusive finance in the future. Based on the above background, this paper intends to discuss the relationship between digital inclusive financial and technological innovation of SMEs. The significance and contribution of this paper are reflected in the following three aspects. First, taking the listed companies on the New Third Board (2011–2020) as the research object, the inclusive characteristics of digital inclusive finance are analyzed from a more micro level, which not only expands the research perspective of the micro effect of digital inclusive finance but also enriches the relevant research results on the driving factors of technological innovation of SMEs. Second, it further clarifies the role mechanism of digital inclusive finance in promoting technological innovation of SMEs and provides a new basis for empowering technological innovation of SMEs. Third, from the perspective of financial supervision and government subsidies, it provides policy suggestions for narrowing the digital divide and better realizing the “government-enterprise-financial institution” multi-party linkage mechanism under macro-control.

The rest of the structure of this paper is as follows: the second part is a literature review; the third part is the theoretical analysis and research hypotheses; the fourth part is the study design, including the selection of data, the measurement of variables and the construction of models; the fifth part is empirical testing; the six parts are endogenous analysis and robustness analysis; the seventh part is the conclusions and revelations and limitations of the study.

2. Literature Review

COVID-19 has hit global economic activity multiple times from both the supply and demand sides. A study analyzing 739 publicly traded companies in 12 countries in the Middle East and North Africa from 2011 to 2020 found that the COVID-19 crisis harmed company performance in most industries and increased overall corporate risk [

9]. At the same time, fintech uses emerging cutting-edge technologies such as big data, cloud computing, and artificial intelligence to transform and innovate traditional financial services or businesses, resulting in emerging financial products, financial services, or financial models that provide important support for economic recovery in the post-epidemic era. However, using data from 37 commercial banks in Vietnam between 2010 and 2020, foreign scholars found that the development of fintech has hurt financial stability [

10]. Therefore, strengthening financial supervision and promoting a virtuous cycle of “science and technology-industry-finance” is an important measure to achieve self-reliance and self-improvement in science and technology.

With the integration of digital inclusive finance and various industries and the increasing status of SMEs in innovation, the research on digital inclusive finance and SME innovation has gradually been enriched. Scholars focused on the direct impact of digital inclusive finance on the innovation of SMEs and found that digital inclusive finance plays an important role in promoting SME innovation. Yang et al. used data from 2011 to 2017 listed companies on China’s SME Board and ChiNext Board and found that digital inclusive finance can have a long-term and “structural” role in driving innovation for SMEs, that is, with the improvement of enterprise innovation level, it shows a trend of first strengthening and then weakening [

11]. In addition, after breaking down the innovation indicators, it is found that digital inclusive finance promotes innovation input more than innovation output [

12]. Cao et al. used the data from China’s A-share SME Board from 2011 to 2020 to construct a panel threshold model, revealing the single-threshold effect of digital inclusive finance coverage breadth and the double-threshold effect of enterprise market position [

13].

This innovation-driven effect of digital inclusive finance on SMEs is heterogeneous in terms of firm size, nature of ownership, level of internal control, region, and life cycle. Yang et al. divided enterprises with more than 100 employees, 20~100 employees, and less than 20 employees into medium-sized enterprises, small enterprises, and microenterprises, respectively, and found that technological innovation of small enterprises and microenterprises is more dependent on the support of digital inclusive finance [

12]. Digital inclusive finance should not cause “financing discrimination” to private enterprises and state-owned enterprises based on its inclusive characteristic but should have a skewed “supporting role” [

14]. Yu and Dou grouped enterprises according to whether the two powers were separated and the shareholding ratio of management, which verified that digital inclusive finance has a more prominent impact on the innovation of SMEs with poor internal governance quality with efficient information processing platforms [

15]. Liu et al. established a research framework of “digital inclusive finance-enterprise life cycle-enterprise technology innovation”, and empirical studies show that digital inclusive finance has the greatest impact on the technological innovation of enterprises in the growth stage, followed by mature enterprises, which has the least impact on enterprises in the recession period [

16]. Zhang et al. used city-level panel data for empirical analysis and found that digital inclusive finance improved the financing environment for SMEs and individual practitioners, effectively supplemented traditional finance, and promoted the improvement of urban innovation [

17]. Therefore, in regions where the development of traditional finance lags, the incentive effect of digital inclusive finance on the technological innovation of SMEs is more significant [

11,

18].

In recent years, most of the discussions among scholars have focused on the path and mechanism of digital inclusive finance to affect the innovation of SMEs. Digital inclusive finance stimulates innovation in SMEs by alleviating financing constraints and reducing the intermediary effect of financing costs [

11,

15,

18,

19,

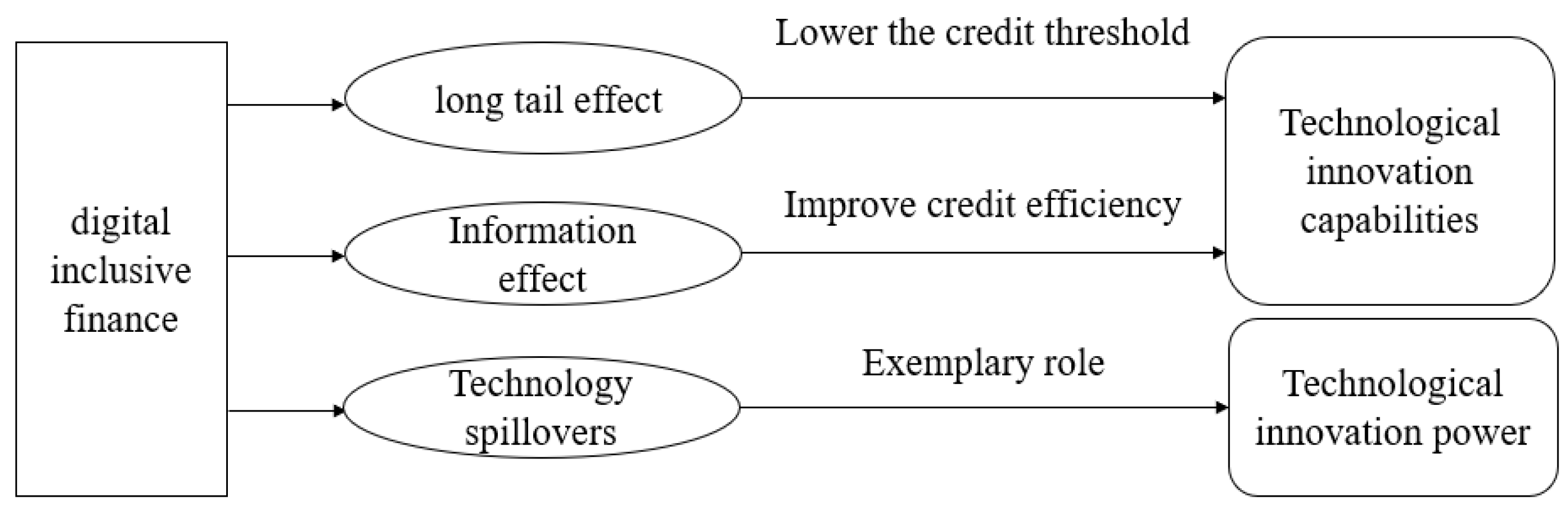

20]. First, the development of digital inclusive finance can lower the threshold of financial services, broaden the source of funds for SMEs, improve the availability of innovation funds, and ease the constraints of innovation financing. Secondly, digital inclusive finance has unique data collection and processing capabilities, which can better play the functions of information screening and risk screening, and reduce the innovative financing costs of SMEs. Finally, digital inclusive finance can help alleviate the problem of information asymmetry and improve the efficiency of innovation financing for SMEs. Moreover, entrepreneurship [

20] and corporate reputation [

13] play a positive moderating role in this influence path. When SMEs face financing problems in innovation activities, entrepreneurs with strong entrepreneurial spirit are more motivated to broaden their sources of funds, actively explore digital technology support and financial service model innovation, explore diversified financial support, and continue to promote enterprise innovation activities. A good reputation is an enterprise’s exclusive and strategic intangible capital, which will send a good signal to the market resource provider that the enterprise can trust, and further amplify this signal through digital inclusive finance.

The above literature provides a reference for the research of this paper. Sorting out the existing research, there are roughly the following characteristics and areas that need to be expanded: First, most of them take ChiNext and small and medium-sized board enterprises as the main research body, but these enterprises are relatively mature in development, and their financing channels are relatively diversified and lack representativeness. Secondly, in terms of the impact of heterogeneity, the existing literature mainly analyzes the differences in the characteristics of enterprises, and there are few studies on the differences in industries and geographical locations of enterprises. Third, some scholars have empirically tested the internal regulatory factors in the process of digital inclusive finance in promoting the innovation of SMEs, but there is a lack of research on the regulatory effect of government intervention (such as financial regulation and government subsidies).

Given this, this paper intends to select the panel data of enterprises listed on the New Third Board from 2011 to 2020, combined with the development indicators of digital inclusive finance, to discuss whether digital inclusive finance can provide the impetus for technological innovation of SMEs, as well as the heterogeneity of enterprises in different industries and regions. A further empirical test is whether financing constraints play an intermediary role under the framework of “digital inclusive finance-scientific and technological innovation of SMEs”, and whether financial supervision and government subsidies play a regulating role.

7. Conclusions and Discussion

7.1. Research Conclusions

The development of digital inclusive finance provides new opportunities for SMEs’ technological innovation in the context of the major strategy of “innovation-driven.” This paper firstly analyzes the theoretical mechanism of digital inclusive finance’s impact on SMEs’ technological innovation and then constructs a benchmark regression model and a mediating and moderating effect model with the help of 2011–2020 New Third Board listed companies’ data and provincial digital inclusive finance indices to empirically test the impact of digital inclusive finance on SMEs’ technological innovation. SMEs’ technological innovation and further verify the heterogeneous impact of digital inclusive finance on promoting SMEs’ technological innovation based on the industry nature and regional distribution of enterprises, and mainly obtain the following conclusions.

- (1)

(The development of digital inclusive finance can empower technological innovation in SMEs and can effectively enhance the R&D intensity of SMEs, especially the degree of digitization of digital inclusive finance plays a central role. The core findings still hold after robustness tests using a higher-order fixed effects model and the use of the instrumental variables approach to address the endogeneity issue.

- (2)

(Digital inclusive finance can alleviate SMEs’ financing constraints, stimulating technological innovation. Digital inclusive finance alleviates the phenomenon of financial exclusion in the traditional financial market, lowers the entry threshold for SME credit, fosters a favorable financial environment, and can better match the financing needs of SMEs’ technological innovation projects.

- (3)

Effective financial regulation and appropriate government subsidies can enhance the driving effect of digital inclusion, and the degree of financial regulation and government subsidies show a positive moderating effect in the relationship of “digital inclusion–SME technology innovation”.

- (4)

In comparison to non-high-tech industries and the central and western regions, digital inclusive finance has the potential to significantly boost technological innovation among SMEs in high-tech industries and the eastern region. Although digital inclusive finance can help to address the industry mismatch of credit resources in the traditional financial system, there are still some regional differences in development.

7.2. Theoretical Contribution

The marginal contribution of this paper, in theory, is reflected in the following three points: (1) This paper constructs the mechanism analysis model of digital inclusive finance on the technological innovation of SMEs, deepens the understanding of “long-tail theory”, “information asymmetry theory”, “technology spillover theory” and “government intervention theory”, and improves the relevant research on the technological innovation behavior of micro-enterprises in the development of digital inclusive finance. (2) From the perspectives of financing constraints, financial supervision, and government subsidies, the impact of digital inclusive finance on the technological innovation of SMEs was deeply discussed and analyzed, and the impact of financial supervision and government subsidies on the innovation driving effect of digital inclusive finance was quantified, which provided a theoretical basis for the healthy development of digital inclusive finance and related policy formulation in China. (3) Based on the different industries and spatial distribution, the heterogeneity analysis of the innovation driving-effect of digital inclusive finance further reveals the inclusive characteristics of digital inclusive finance that can reduce the misallocation of financial resources and make up for the shortcomings of traditional finance.

7.3. Practical Enlightenment

Through the theoretical analysis and empirical test of digital inclusive finance enabling SMEs’ technological innovation, the following enlightenment is obtained: First, financial technology can indeed play a positive role in promoting the real economy. We should vigorously develop digital inclusive finance, encourage traditional financial institutions to carry out digital transformation, create a multi-level financial service network, optimize the financial supply structure, and achieve the precise connection between digital inclusive finance and SMEs. Second, as 5G, blockchain, big data platforms, and cloud computing realize the deep integration of data elements and capital circulation process, the efficient flow of data among governments, enterprises, and individuals has been realized, and the financing needs of small and micro enterprises have been met to the greatest extent. Third, the popularity and penetration of digital inclusive finance need to be further expanded, the development of digital inclusive finance in central and western regions should be strengthened, and regional differences in digital inclusive finance should be continuously narrowed. Fourth, to avoid the digital divide and overlapping risks, we must uphold the regulatory and legal bottom line and strengthen the construction of the prudential regulatory framework in the field of digital inclusive finance from the perspective of business norms and technical security. Innovate regulatory technology, realize the complementary development of credit reporting institutions and digital inclusive finance, maintain the fairness of the capital lending market, and protect the financing rights and interests of SMEs’ innovative projects.

7.4. Research Limitations and Prospects

There are still some limitations of this study: (1) In this paper, a panel data model is constructed for empirical testing, and the threshold model and nonlinear smooth transformation model can also be considered for verification in the future. (2) The theoretical model of the impact of digital inclusive finance on the technological innovation of SMEs needs to be further deepened, and it is expected that the existing model can be expanded in the future, and the different impact mechanisms of digital inclusive finance on the technological innovation of SMEs are analyzed from other perspectives. (3) This paper uses the Peking University Digital Inclusive Finance Index to measure digital inclusive finance and new measurement methods can be explored in the future to enhance the robustness of the research results.

{kind=link}

{kind=link}