1. Introduction

Given the pressing urgency of the escalating crisis of global warming and the increasingly detrimental impact of human activity on the environment, effective policies aimed at reducing emissions and conserving energy have been discussed by the international community. These efforts should aim not only to curtail emissions but also to necessitate efficient resource allocation among nations [

1]. Consequently, discussions about the allocation of carbon emissions rights have been a topic of global interest. The Kyoto Protocol officially began on 16 February 2005, and the European Union’s Emission Trading Scheme (EU ETS) launched in 2005, giving shape to the global carbon market, which aims to effectively allocate carbon emissions rights by trading carbon allowances [

2]. As a unique environmental regulatory tool, the carbon emissions trading market exhibits distinct market characteristics [

3,

4,

5]. The primary objective of this initiative is to harness market mechanisms, such as price discovery, to maximize the efficiency of carbon reduction efforts throughout society [

3]. The allocation of carbon allowances occurs through government-issued allowances, fixed-price sales, or competitive auctions [

6,

7,

8]. Expanding on this foundation, the carbon emissions trading market is implemented to monitor the emissions rights pricing, creating a secondary market [

6]. This strategy effectively internalizes environmental pollution externalities into corporate responsibilities through market-based pricing mechanisms, ultimately achieving the goal of reducing the total carbon emissions produced by businesses [

8,

9]. The frame of the carbon emissions trading system, which utilizes carbon emissions allowances, is presented in

Figure 1.

From 2001, when China joined the World Trade Organization, until around 2011, its carbon emissions grew rapidly, increasing from 14.86% to 28.57% of the world’s total [

11]. Between 2012 and 2021, China’s carbon emissions growth rate slowed down due to a slowdown in GDP growth, a decline in the energy intensity of GDP, and faster decarbonization [

12,

13]. However, China remains the largest emitter of CO

2, with the highest GDP carbon intensity among major economies worldwide [

14]. According to the IEA’s report, global CO

2 emissions related to energy and industrial emissions are projected to reach 36.8 billion tons in 2022, with China accounting for about one-third of total global carbon emissions, emitting 12.1 billion tons [

14].

To address climate change, since 2011, the Chinese government has taken a pioneering step by launching a pilot carbon emissions trading scheme (CETS) in eight provinces and municipalities. Then, on 16 July 2021, the Chinese government officially announced the establishment of the national carbon emissions trading market (NCETM). As of 17 October 2023, the NCETM had a cumulative turnover of 324.8 million tons and a total turnover of RMB 16.64 billion [

15]. This market has now become the major carbon emissions trading platform in the world.

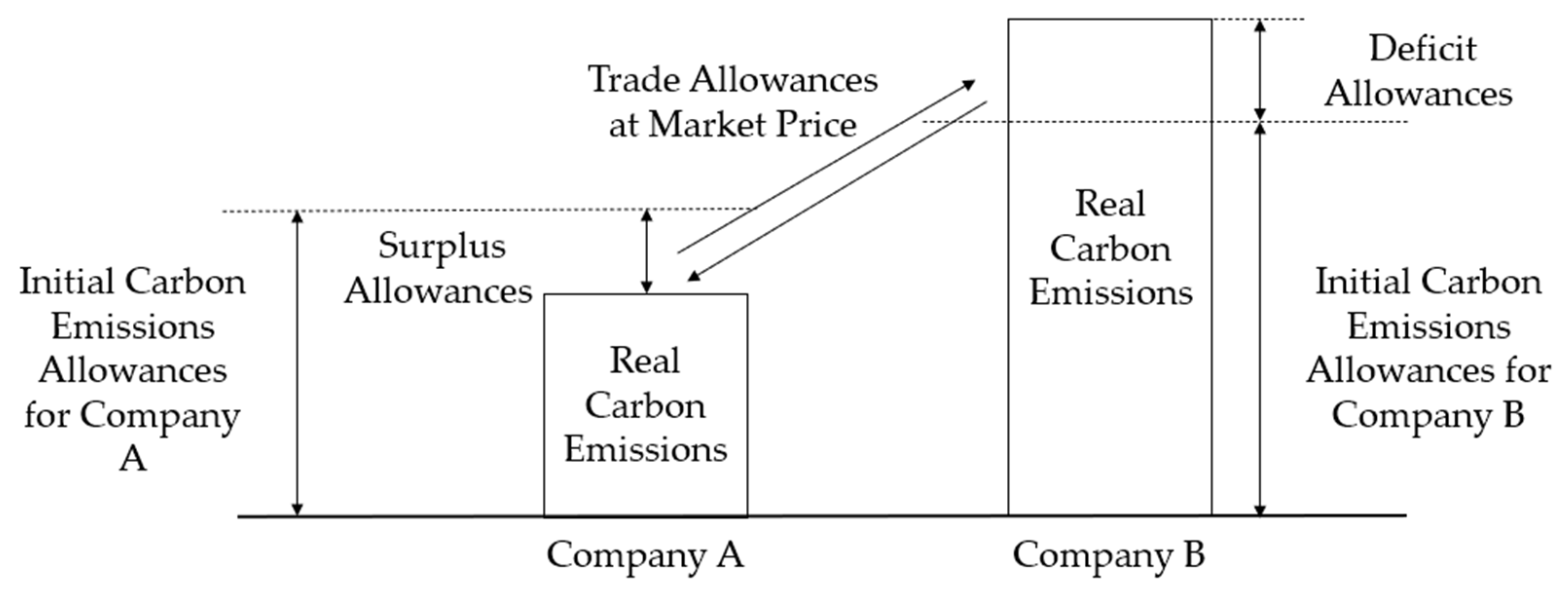

Similar to the stock market, the carbon emissions trading market can be divided into a primary market and a secondary market [

6]. The government mainly issues carbon emissions allowances to emissions control enterprises, which constitute the primary market. The issuance of corresponding carbon allowances is governed by a policy cap on total annual emissions. The secondary market primarily serves as a platform for trading surplus carbon allowances, involving participants such as emissions control enterprises and professional investment institutions. A simple visual representation of this trading model is shown in

Figure 2.

As significant NCETM participants, enterprises hold considerable sway over carbon emissions resulting from production [

16]. The externalities of the eco-environment and the lack of balance between environmental protection and environmental pollution pose a challenge for enterprises in implementing robust environmental governance [

17]. In the context of government regulatory instruments, enterprises adopt a stance focused on maximizing economic efficiency [

18]. Their decisions are shaped by a careful evaluation of the advantages and disadvantages of proactive environmental investments and the procurement of necessary environmental equipment to meet pollution emissions standards [

18]. This results in a scenario characterized by passive environmental governance. Environmental regulations, through exerting pressure, could push companies to engage in environmental stewardship and increase corporate environmental protection investment (EPI) [

19], ultimately helping to achieve sustainable development goals. Nevertheless, an overabundance of regulatory pressure can potentially produce adverse effects [

20]. When environmental regulations impose external pressure on firms lacking internal motivations, their investment in environmental protection may become a pragmatic compromise between benefits and costs [

18]. Corporate investment in environmental protection is often marked by long cycles and a diminished return on investment, deviating from the corporate aim of profit maximization [

21]. This leads many enterprises to show reluctance in allocating resources toward programs contributing to environmental protection. As a result, their environmental protection conduct is mainly reactive, mostly motivated by the pursuit of compliance [

22].

Therefore, governments need to design innovative policy tools to provide adequate incentives for enterprises to increase their EPI, to achieve green development. The implementation of a carbon emissions trading market has spurred a noteworthy shift, motivating companies to actively pursue innovation in technology and manufacturing processes, resulting in a reduction in carbon emissions [

23]. Such proactive engagement generates social benefits and simultaneously strengthens economic gains derived from market mechanisms [

16].

The literature lacks a consensus on whether government-mandated environmental regulations are effective in encouraging stronger investments in environmental protection. The pollution paradise hypothesis posits that strict environmental policy requires firms to invest more in the protection and conservation of eco-environment [

24]. This can lead to higher costs of production and lower profits [

24]. Conversely, Porter’s hypothesis argues that proper environmental regulations could stimulate business investments and encourage innovation in the technology [

17]. Such regulations can prompt a transition away from traditional production methods and product structures, ultimately increasing dedication to environmental investments [

17]. Moreover, the factor endowment hypothesis suggests that enterprises base their decisions regarding EPI on a calculation that compares the costs incurred by the enterprise to the benefits gained from adhering to environmental regulations [

18].

Enterprises’ decisions regarding investments in environmental protection are influenced by numerous factors. Although environmental regulation is a compulsory tool, its effectiveness depends on the specific circumstances. China, a primary emitter of carbon and a prototypical representation of a developing economy, faces unique challenges arising from its distinct political and economic institutional context in setting up and operating a carbon emissions trading market [

25,

26]. Additionally, the status quo of China’s carbon emissions trading market displays a budding stage with significant dynamism, indicating that maturity and operational efficiency remain distant [

27]. The NCETM in China is at a nascent stage, characterized by ongoing testing and evaluation. The trajectory of its development is yet to be fully formed.

Therefore, the effectiveness of the NCETM in China to motivate companies to increase their investment in environmental protection remains uncertain. Previous research on the micro-level impact of the carbon emissions trading market on firms has primarily focused on the market’s influences on aspects, such as firms’ green transformation, capital allocation efficiency, and corporate financing [

28,

29,

30]. However, only a few studies have delved into the area of corporate EPI. While Lv et al. investigated carbon emissions trading and its impact on corporate environmental investment in pilot regions [

31], there is still a relative dearth of research from the NCETM perspective. As opposed to the examination of pilot data, a study that encompasses national policy can provide a more comprehensive interpretation of the overall state of policy implementation and allow for a deeper analysis of the long-term impact and sustainability of the policy. As such, this paper will focus on addressing the following research questions: (1) Does the establishment of the NCETM have an effect on firms’ EPI? (2) What mechanisms underlie the impact of the NCETM on corporate EPI? (3) Furthermore, do these effects vary according to the region in which firms are located?

To address these questions, this study conducts a theoretical analysis of how the NCETM affects corporate EPI and its underlying mechanisms. The study’s empirical aspect tests these hypotheses by examining financial data from publicly traded companies in China from 2018 to 2022. The difference-in-differences (DID) model is employed to explore the impact of the NCETM. Further analyses explore the impact’s mechanisms and potential heterogeneity in effects. Our study reveals some significant results. We determine that the implementation of the NCETM positively impacts the EPI of businesses. Our findings specifically indicate that Research and Development (R&D) investment serves as the intermediary role in mediating this effect. Moreover, the impact of the NCETM on enterprises is not consistent across diverse regions. Notably, the NCETM displays a significant influence on the EPI of firms in non-pilot regions, but no such effect is observed in pilot regions, showcasing regional variations.

Thus, this study contributes to the existing literature by empirically validating the positive effect of the NCETM on corporate EPI, while at the same time elucidating the underlying mechanisms. These findings have implications for both academic and practical perspectives on large-scale carbon emissions trading markets and corporate environmental performance. The implications of our study extend to policy considerations, as the study underscores the need for governments to consider the differential impacts of carbon markets on regulated firms across regions. Such insights are critical to improving the performance of national carbon markets. Additionally, our study adds to the literature the factors influencing firm EPI and provides valuable empirical insights for facilitating social green development.

The remaining sections of this paper are organized as follows.

Section 2 conducts a comprehensive literature review, delving into prior research and existing literature on both the carbon emissions trading market and the firm’s EPI.

Section 3 provides a theoretical analysis along with the formulated research hypotheses.

Section 4 delineates the research design, encompassing details on data sources, sample selection, and the chosen methodology.

Section 5 offers the empirical results.

Section 6 summarizes key findings, engaging in a discussion about the results.

Section 7 presents theoretical implications and policy recommendations, as well as limitations and future directions.

6. Discussion

This study investigates the relationship between the NCETM and corporate EPI and the intermediate role of R&D investment. The results support both Hypotheses 1 and 2. This research has shown that (1) the NCETM is positively associated with corporate EPI. (2) The effect of the NCETM on corporate EPI is intermediated by R&D investment. (3) The effectiveness of the impact of the NCETM on corporate EPI differs by the region in which the firm is located. The three findings are discussed below.

Firstly, the main focus of this paper is to analyze how the NCETM affects enterprise EPI. The study found that the NCETM acts as a catalyst for environmental investment, which is consistent with the findings of previous studies about the pilot scheme [

31]. This trend can be traced back to the market mechanisms embedded in the NCETM, which incentivize companies to increase their environmental protection investment [

16]. As one of the world’s largest carbon emitters, China is facing significant pressure to reduce its carbon emissions [

14]. Therefore, the Chinese government is prioritizing environmental protection and taking action to combat climate change [

10]. At the same time, China presents a vast market with ample business opportunities for carbon reduction [

14]. The NCETM provides guidance and incentives for companies to participate in environmental protection investments due to increasingly stringent regulations [

16]. Companies will be more proactive in doing so to avoid fines and sanctions [

21]. The NCETM could lead to a convergence of cost reduction, alleviated regulatory constraints, and increased economic benefits [

21]. The implementation of the NCETM provides financial incentives for firms to proactively reduce emissions, which contrasts with past passive approaches of avoiding fines [

9]. This policy encourages firms to participate more actively in environmental investments by increasing the rate of return on firms’ environmental investments as well as providing companies with an extra source of funding to support their environmental investment activities [

63]. It extends the existing literature by using the NCETM, a national-wide policy, as a quasi-natural experiment, to explore the effect of the carbon emissions trading market on corporate EPI.

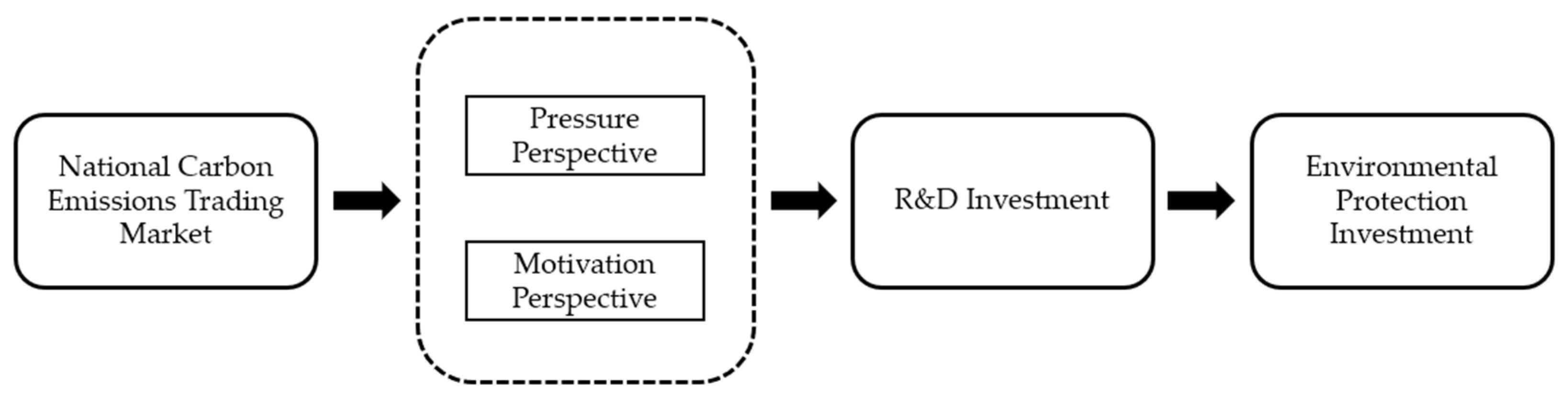

Secondly, this study demonstrates that R&D expenditures serve as a crucial intermediary mechanism in the impact of the NCETM on corporate EPI. On the one hand, China is currently undergoing a critical period of economic transformation and upgrading [

74]. Promoting technological innovation and industrial upgrading is crucial for achieving sustainable development [

74]. The implementation of the NCETM motivates firms to engage in technological innovation to cope with increasing market and investor concerns about environmental protection and gain market competition advantages [

66]. Companies can increase their profit margins by developing and implementing energy-saving and emission-reduction technologies [

33]. On the other hand, investment in R&D can increase a firm’s intangible assets to potentially enhance the return on environmental investment [

69,

71]. Along with the increasing awareness of environmental protection and social responsibility among Chinese companies, it may lead to an increase in firms’ participation in environmental investments [

69]. Therefore, the NCETM could promote corporate EPI through increasing R&D investment, which is little discussed in prior literature. For the first time, this study introduces R&D investment as an intermediate variable in the effect of carbon emissions trading market on corporate EPI.

Thirdly, as shown in

Table 8, the implementation of NCETM has no significant effect on corporate EPI for firms in the pilot area. Carbon emissions trading market construction in China started with local pilots due to significant differences between China and developed countries and regions in Europe and the United States in terms of their stage of economic development, international carbon emissions reduction responsibilities, distribution of carbon-emitting industries, and degree of electricity marketization [

8]. Due to these circumstances, China was unable to fully utilize international experience and therefore had to accumulate experience in carbon emissions trading market construction through pilot experience. This result may be due to the fact that the companies from the pilot region may have already executed a significant volume of EPI or successfully accomplished their green transformation earlier. This might lead to a less notable influence of NCETM on the enterprises’ EPI. Furthermore, the limited sample size and relatively short data window may have contributed to these results. This result demonstrates the effectiveness of the CETS from a different perspective compared to previous studies.

7. Conclusions

7.1. Theoretical Implications and Policy Recommendations

The study provides new insights into the field of carbon emissions trading market and corporate EPI by systematically examining the effect of the nationwide carbon emissions trading market policy on corporate EPI. Firstly, this study introduces the nationwide carbon emissions trading market into the research framework for the first time. Secondly, this study innovatively includes R&D investment as a key mediating variable, to explore the mechanism underlying the effect of the NCETM on corporate EPI. The findings provide empirical support for the relationship between the carbon emissions trading market and corporate EPI. They also offer valuable references on how corporations can optimize their R&D investment in response to carbon emissions trading policies. These insights are useful for subsequent researchers and promote in-depth research in the field of carbon emissions trading market and corporate EPI.

Based on these findings, environmental protection regulation policymakers can benefit from the following insights:

Firstly, the government can expand the list of industries and enterprises involved in the carbon emissions trading market. This could incentivize more enterprises to increase their environmental protection investment. Consequently, it would improve the effectiveness of the country’s environmental governance mechanism. By expanding the reach of the carbon emissions trading market to include more industries and enterprises, the government can encourage greater participation in environmental protection efforts. This, in turn, will promote the overall process of environmental protection throughout the country.

Secondly, the government should explore the implementation of tailored environmental governance policies to enhance the efficacy of regulatory initiatives. Companies in different regions exhibit varying responses to the NCETM. An improved understanding of interregional enterprise variations would enable the government to develop more precise regulations and initiatives. Companies located in pilot regions may gain an edge in the NCETM compared to those in non-pilot regions. This advantage may stem from the fact that firms in pilot regions have already undergone their green transformation in the pilot phases and possess greater familiarity with the carbon emissions trading mechanism. Therefore, the government can compile an account of the pilot regions’ experiences and offer guidance to enterprises in non-pilot regions to improve their adaptation to the carbon emissions trading market.

Thirdly, the study offers a valuable policy reference for other countries seeking to promote environmental protection investments and building carbon trading emissions markets. The results highlight the potential benefits of implementing a carbon market as an effective policy tool to encourage firms to reduce carbon emissions and adopt more sustainable business practices. Other countries can learn from this study by combining carbon market policies with innovation and R&D policies to incentivize firms to adopt greener technologies and production methods. The early experience of pilot regions can also serve as a useful reference for accumulating experience on a limited scale and gradually expanding it to the whole country.

7.2. Future Directions

During the research and writing process, it was found that there were some limitations in this study and further exploration is necessary. Firstly, this study recognizes a limitation in its investigation of the long-term impacts of the NCETM as the policy has only recently been implemented. Future research could expand the study window, covering a more extended period, to comprehensively clarify the medium- and long-term implications of the NCETM.

Secondly, the present investigation examines the influence of the NCETM on corporate EPI predominantly from the standpoint of R&D investment. Nevertheless, the fundamental process might be complex and extend beyond this lone perspective. Future research could examine other moderating and intermediary factors that influence the NCETM’s effect on corporate EPI. For example, studying politically affiliated companies, which often receive increased government aid and protection, to analyze the effect of the NCETM could provide important findings. This research could contribute to the current literature regarding the connection between the NCETM and corporate EPI.

Thirdly, this study examines the impact of the NCETM on corporate EPI without considering the variations in this process across industries and firms. Different industries and firms may encounter distinct market environments and technological requirements, which can influence their response to the NCETM and their investment decisions. Future research could refine the analysis to explore the differentiated responses of different industries and firms when facing NCETM. For instance, comparing factors such as carbon intensity, technology level, and market competitiveness between industries can provide insights into the specific impacts of NCETM on each industry. Additionally, it is important to consider the impact of policy constraints, economic incentives, and social responsibility on these enterprises. This will enable us to provide more targeted recommendations to policymakers and enterprises to promote sustainable development and a green, low-carbon transition.

{kind=link}

{kind=link}

{kind=link}

{kind=link}