Reaction to Idiosyncratic Economic Shocks—Economic Resilience of Small- and Medium-Sized Enterprises

Abstract

:1. Introduction

2. Overview of the Related Literature

2.1. Prior Approaches to Address Economic Resilience

2.2. Prospects of Predicting SME Resilience

3. Methodological Approach

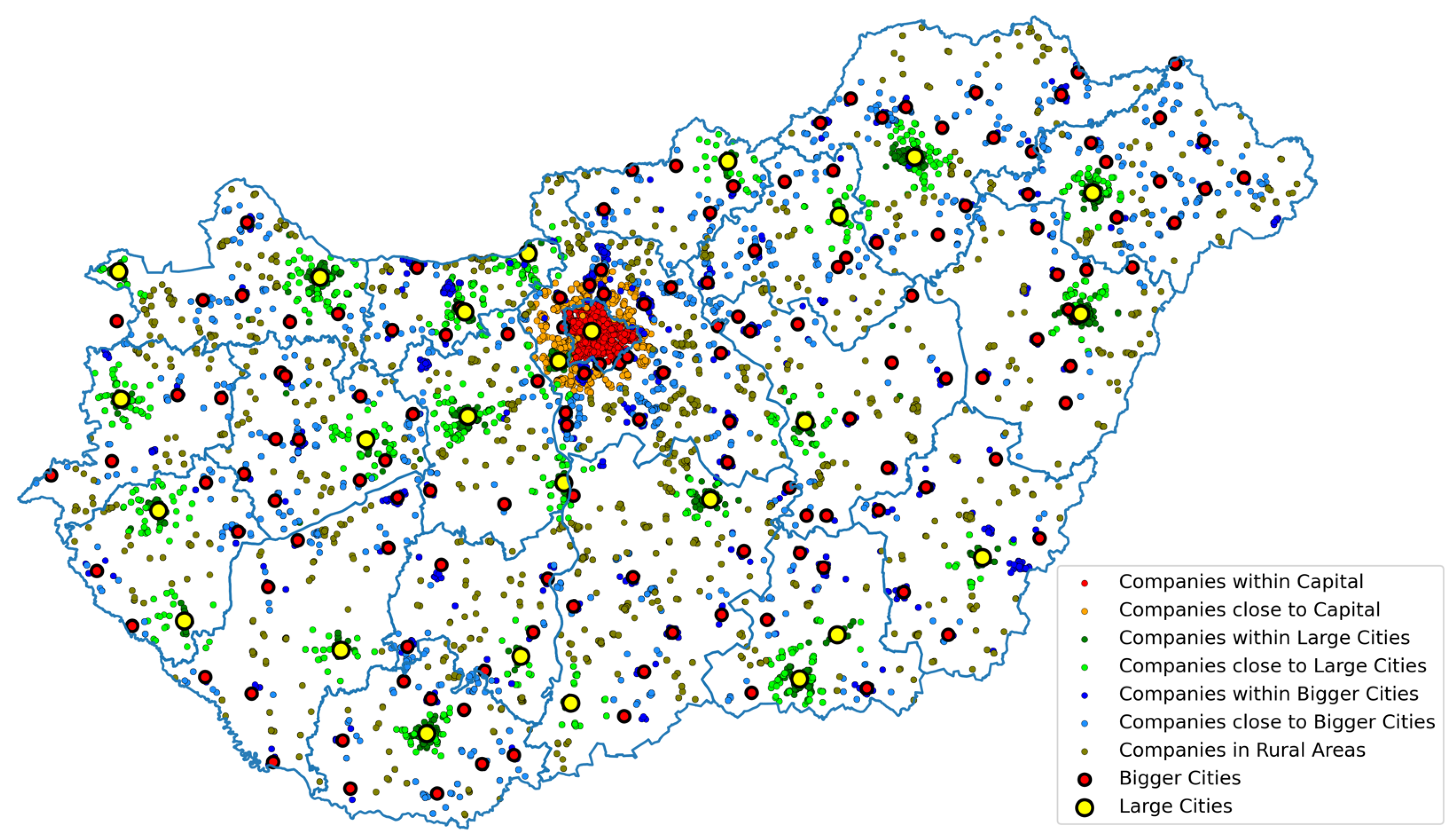

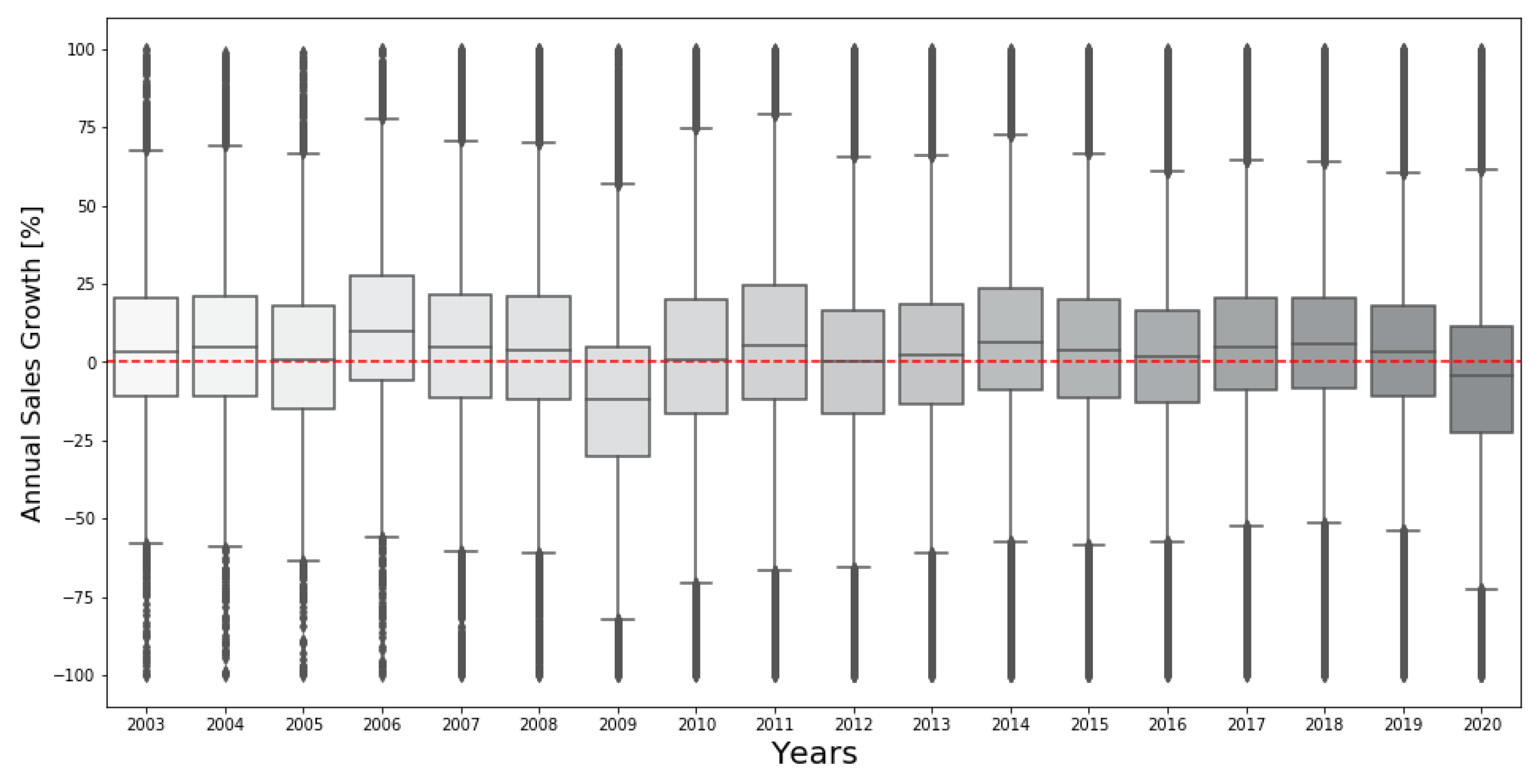

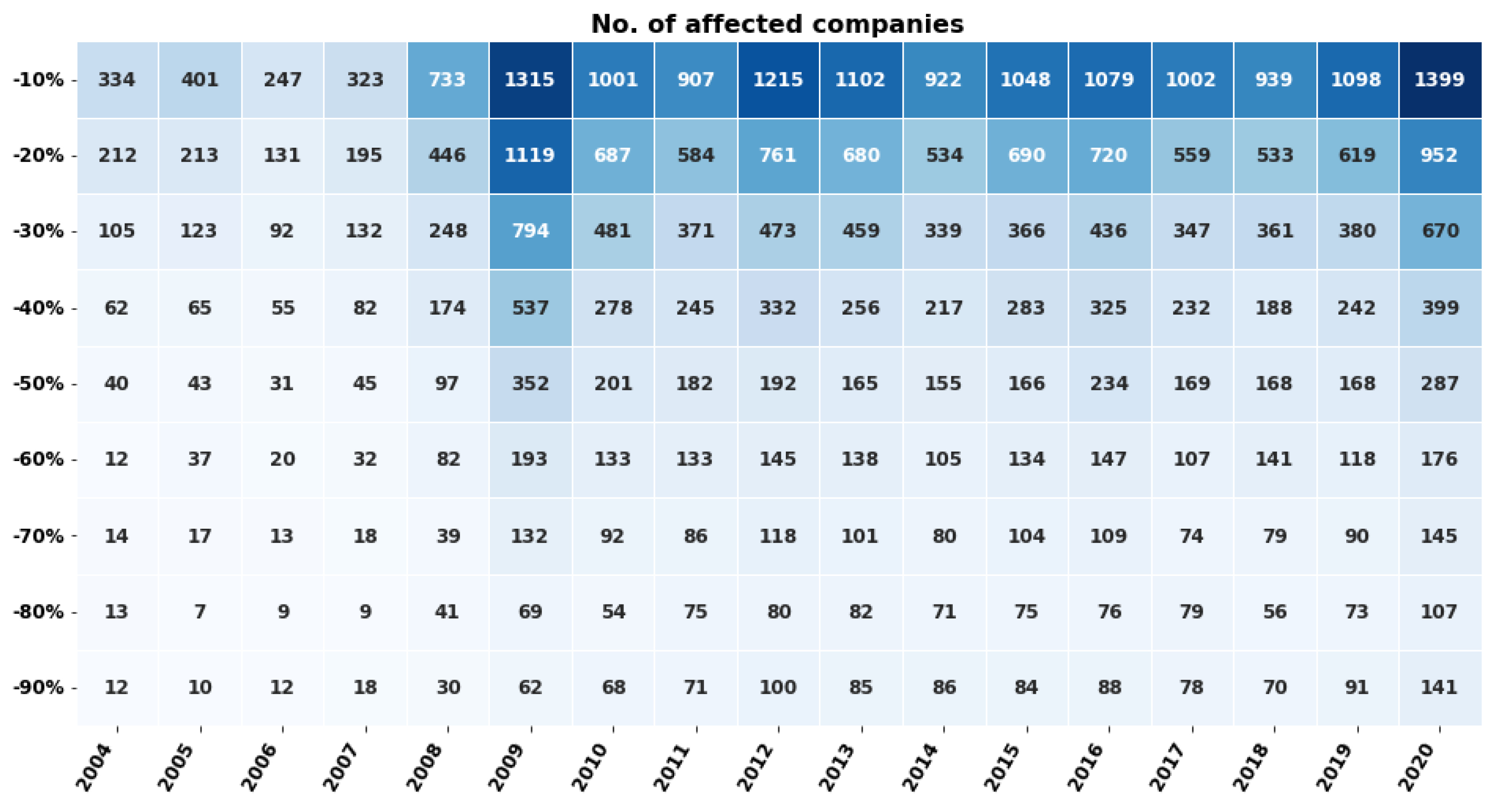

3.1. Data Description

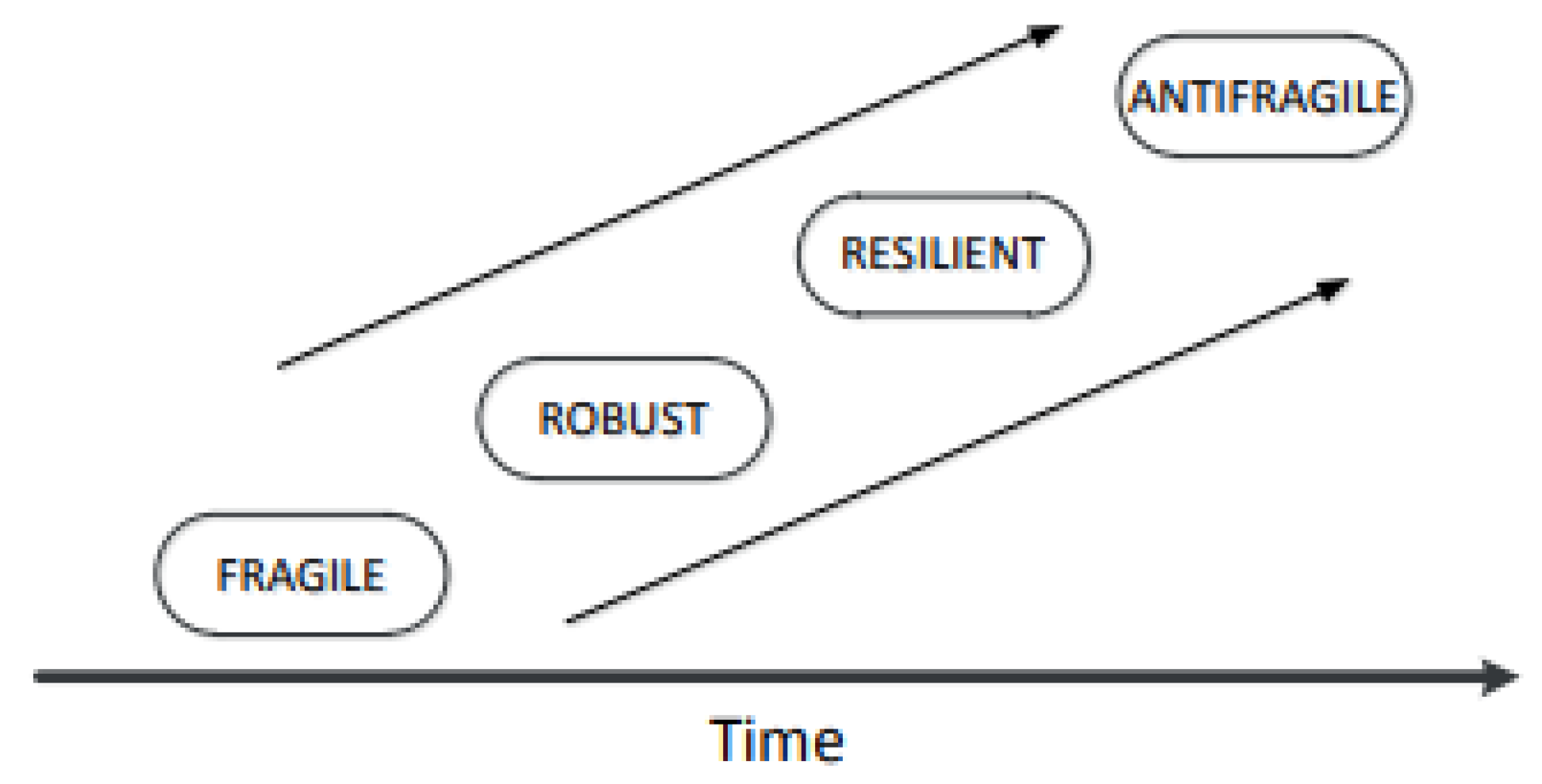

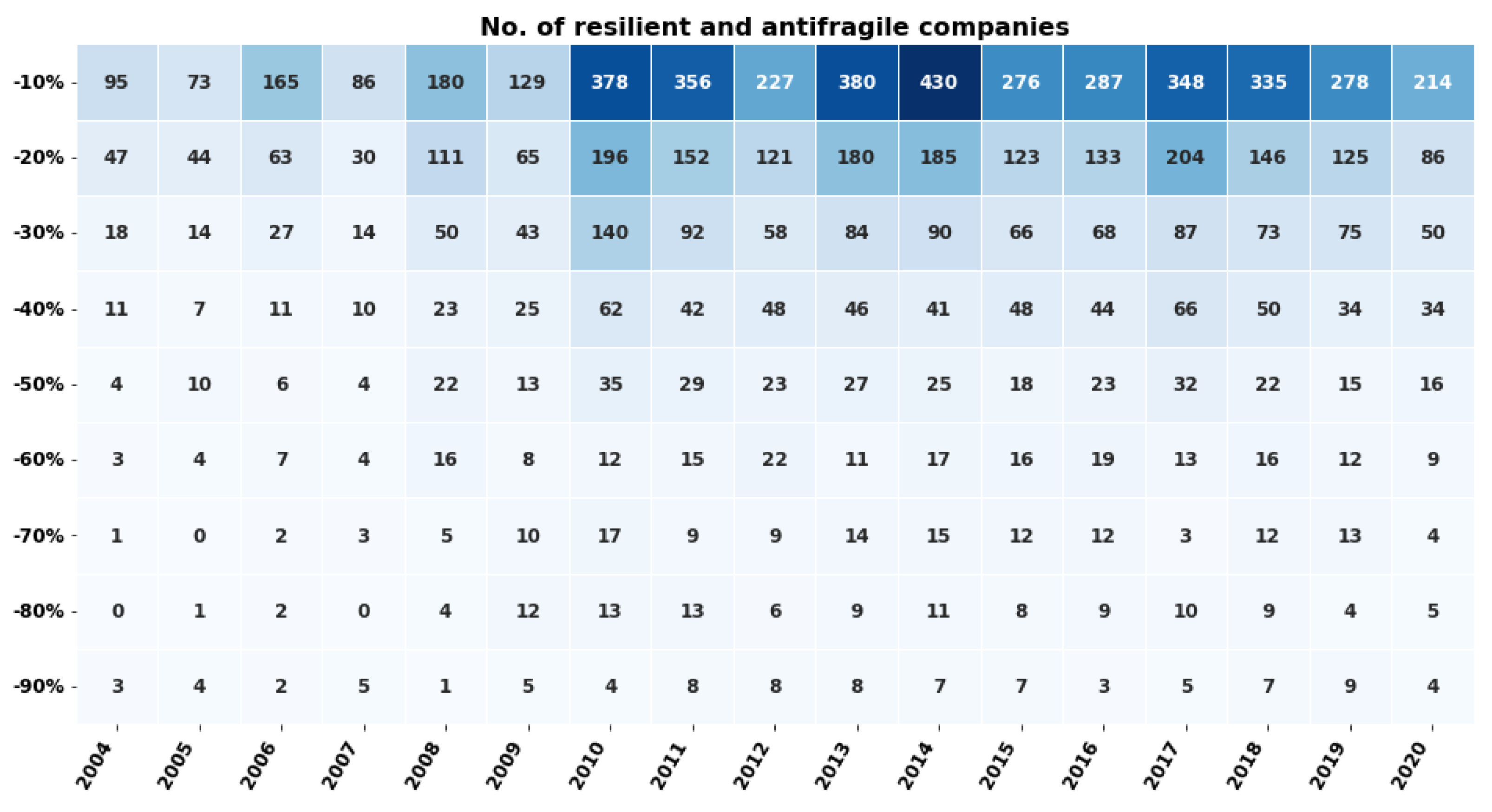

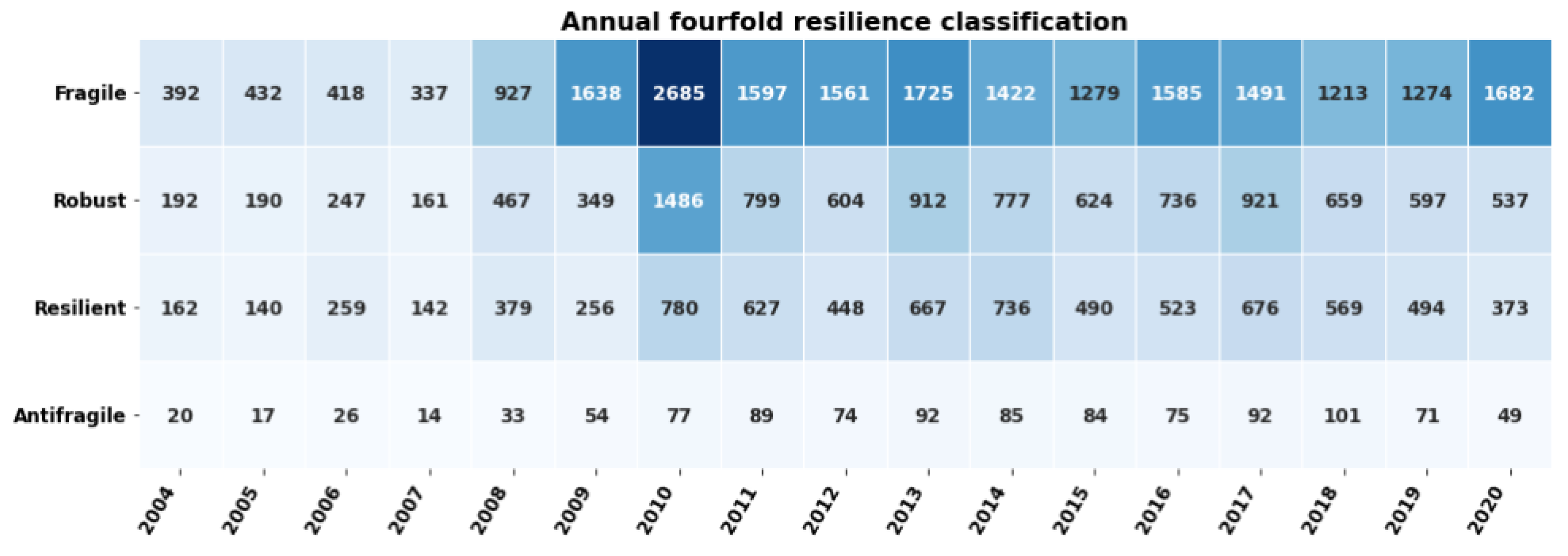

3.2. Proposed Resilience Index

- Fragile: R() < R() orSG() > SG() > −100%;

- Robust: R() < R() < R() or0% > SG() > SG();

- Resilient: R() < R() < R() or100% > SG() > 0%;

- Antifragile: 2· R() < R() orSG() > 100%.

3.3. Hypothesis Testing Regarding Resilient Shock Reactions

- Within each pair, members were from the same main industrial sector.

- Within each pair, members were of the same size regarding employment grouping.

- Within each pair, members’ annual net revenue did not differ by more than 10% in the year following the shock, when corresponding shock reactions manifested.

- Within each pair, members were selected so that neither had any “shock experience” before the investigated one (no previous sales growth drop greater than −10% in their time-series).

- The formation of treatment and controlled group pairs was conducted on a random basis to minimise selection bias.

3.4. Predictive Model for Resilience

4. Results, Discussion

4.1. Conclusions

4.2. Limitations, Future Work

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Bhamra, R.; Dani, S.; Burnard, K. Resilience: The concept, a literature review and future directions. Int. J. Prod. Res. 2011, 49, 5375–5393. [Google Scholar] [CrossRef]

- Holling, C. Resilience and stability of ecological systems. Annu. Rev. Ecol. Syst. 1973, 4, 1–23. [Google Scholar] [CrossRef]

- Aleksić, A.; Stefanović, M.; Arsovski, S.; Tadić, D. An assessment of organizational resilience potential in SMEs of the process industry, a fuzzy approach. J. Loss Prev. Process Ind. 2013, 26, 1238–1245. [Google Scholar] [CrossRef]

- Karácsony, P. Analyzing the Relationship between Leadership Style and Corporate Social Responsibility in Hungarian Small and Medium-sized Enterprises. Acta Polytech. Hung. 2020, 17, 183–198. [Google Scholar] [CrossRef]

- Aldea, A.; Vaicekauskaité, E.; Daneva, M.; Piest, J.P.S. Assessing Resilience in Enterprise Architecture: A Systematic Review. In Proceedings of the 2020 IEEE 24th International Enterprise Distributed Object Computing Conference (EDOC), Eindhoven, The Netherlands, 5–8 October 2020. [Google Scholar] [CrossRef]

- Varga, J. Defining the Economic Role and Benefits of Micro, Small and Medium-sized Enterprises in the 21st Century with a Systematic Review of the Literature. ACTA Polytech. Hung. 2021, 28, 209–228. [Google Scholar] [CrossRef]

- Kennon, D.; Schutte, C.S.; Lutters, E. An alternative view to assessing antifragility in an organisation: A case study in a manufacturing SME. CIRP Ann.-Manuf. Technol. 2015, 64, 177–180. [Google Scholar] [CrossRef]

- Masood, T.; Sonntag, P. Industry 4.0: Adoption challenges and benefits for SMEs. Comput. Ind. 2020, 121, 103261. [Google Scholar] [CrossRef]

- Némethné Gál, A. Competitiveness of Small and Medium-Sized Enterprises (In Hungarian). Ph.D. Thesis, István Széchenyi University, Doctoral School of Regional- and Business Administration, Győr, Hungary, 2009. Available online: https://rgdi.sze.hu/files/Ertekezesek,%20tezisek/Magyar%20Tezis%20NGA.pdf (accessed on 1 June 2023).

- Ruiz-Martina, C.; López-Paredes, A.; Wainer, G. What we know and do not know about organizational resilience. Int. J. Prod. Manag. Eng. 2018, 6, 11–28. [Google Scholar] [CrossRef]

- Eckardt, O. Company Maturity Matrix. Emerg. Mark. J. 2008, 8, 28–30. [Google Scholar] [CrossRef]

- Man, T.K. Measuring and Analysing Resilience of Enterprise Architectures. In Proceedings of the 31th Twente Student Conference on IT, University of Twente, Enschede, The Netherlands, 5 July 2019. [Google Scholar]

- Ramezani, J.; Camarinha-Matos, L.M. Approaches for resilience and antifragility in collaborative business ecosystems. Technol. Forecast. Soc. Change 2020, 151, 119846. [Google Scholar] [CrossRef]

- Taleb, N.N.; Douady, R. Mathematical Definition, Mapping, and Detection of (Anti)Fragility. Quant. Financ. 2013, 13, 1677–1689. [Google Scholar] [CrossRef]

- Graça, P.; Camarinha-Matos, L.M. Performance indicators for collaborative business ecosystems—Literature review and trends. Technol. Forecast. Soc. Change 2017, 116, 237–255. [Google Scholar] [CrossRef]

- Somers, S. Measuring Resilience Potential: An Adaptive Strategy for Organizational Crisis Planning. J. Contingencies Crisis Manag. 2009, 17, 12–23. [Google Scholar] [CrossRef]

- Jung, H.; Hwang, J.; Kim, B.K. Does R&D investment increase SME survival during a recession? Technol. Forecast. Soc. Change 2018, 137, 190–198. [Google Scholar] [CrossRef]

- Sauser, B.; Baldwin, C.; Pourreza, S.; Randall, W.; Nowicki, D. Resilience of small- and medium-sized enterprises as a correlation to community impact: An agent-based modeling approach. Nat. Hazards 2018, 90, 79–99. [Google Scholar] [CrossRef]

- Erol, O.; Henry, D.; Sauser, B.; Mansouri, M. Perspectives on Measuring Enterprise Resilience. In Proceedings of the 2010 IEEE International Systems Conference, San Diego, CA, USA, 5–8 April 2010; pp. 587–592. [Google Scholar] [CrossRef]

- saad, M.H.; Hagelaar, G.; van der Velde, G.; Omta, S.W.F. Conceptualization of SMEs’ business resilience: A systematic literature review. Cogent Bus. Manag. 2021, 8, 1938347. [Google Scholar] [CrossRef]

- Gunasekaran, A.; Rai, B.K.; Griffn, M. Resilience and competitiveness of small and medium size enterprises: An empirical research. Int. J. Prod. Res. 2011, 49, 5489–5509. [Google Scholar] [CrossRef]

- Jabeur, S.B. Bankruptcy prediction using Partial Least Squares Logistic Regression. J. Retail. Comput. Serv. 2017, 36, 197–202. [Google Scholar] [CrossRef]

- Zizi, Y.; Oudgou, M.; Moudden, A.E. Determinants and Predictors of SMEs’ Financial Failure: A Logistic Regression Approach. Risks 2020, 8, 107. [Google Scholar] [CrossRef]

- Kristóf, T.; Virág, M. A Comprehensive Review of Corporate Bankruptcy Prediction in Hungary. J. Risk Financ. Manag. 2020, 13, 35. [Google Scholar] [CrossRef]

- Tinoco, M.H.; Wilson, N. Financial distress and bankruptcy prediction among listed companies using accounting, market and macroeconomic variables. Int. Rev. Financ. Anal. 2013, 30, 391–419. [Google Scholar] [CrossRef]

- Johnson, J.; Gheorghe, A.V. Antifragility Analysis and Measurement Framework for Systems of Systems. Int. J. Disaster Risk Sci. 2013, 4, 159–168. [Google Scholar] [CrossRef]

- Hungarian Central Statistical Office, Distribution of the Hungarian Gross Domestic Product among Industries. Available online: https://www.ksh.hu/stadat_files/gdp/hu/gdp0006.html (accessed on 10 June 2024). (In Hungarian).

- Virág, M.; Kristóf, T.; Fiáth, A.; Varsányi, J. Financial Analysis, Bankruptcy Prediction, Crisis Management; Kossuth Kiadó: Budapest, Hungary, 2013; ISBN 978 963 09 7724 1. (In Hungarian) [Google Scholar]

- Jordahl, K. GeoPandas: Python Tools for Geographic Data. 2014. Available online: https://github.com/geopandas/geopandas (accessed on 15 June 2023).

- de Wet, J.; du Toit, E. Return on equity: A popular, but flawed measure of corporate financial performance. S. Afr. J. Bus. Manag. 2007, 38, 59–69. [Google Scholar] [CrossRef]

- Murphy, G.B.; Trailer, J.W.; Hill, R.C. Measuring performance in entrepreneurship research. J. Bus. Res. 1996, 36, 15–23. [Google Scholar] [CrossRef]

- Brambor, T.; Clark, W.R.; Golder, M. Understanding Interaction Models: Improving Empirical Analyses. Political Anal. 2006, 14, 63–82. [Google Scholar] [CrossRef]

- Curran-Everett, D. Explorations in statistics: The analysis of ratios and normalized data. Adv. Physiol. Educ. 2013, 37, 213–219. [Google Scholar] [CrossRef]

- Kim, J.H. Spurious Correlation between Ratios with a Common Divisor. Stat. Probab. Lett. 1999, 44, 383–386. [Google Scholar] [CrossRef]

- Barnes, P. The Analysis and Use of Financial Ratios: A Review Article. J. Bus. Financ. Account. 1987, 14, 3311–3323. [Google Scholar] [CrossRef]

- Lev, B.; Sunder, S. Methodological Issues in the Use of Financial Ratios. J. Account. Econ. 1979, 1, 187–210. [Google Scholar] [CrossRef]

- Tognazzo, A.; Gubitta, P.; Favaron, S.D. Does slack always affect resilience? A study of quasi-medium-sized Italian firms. Entrep. Reg. Dev. 2016, 28, 768–790. [Google Scholar] [CrossRef]

- de Mandojana, N.O.; Bansal, P. The Long-term Benefits of Organizational Resilience Through Sustainable Business Practices. Strateg. Manag. J. 2015, 37, 1615–1631. [Google Scholar] [CrossRef]

- Pálovics, R.; Dolenc, P.; Leskovec, J. Companies under stress: The impact of shocks on the production network. EPJ Data Sci. 2021, 10, 57. [Google Scholar] [CrossRef] [PubMed]

- Markman, G.M.; Venzin, M. Resilience: Lessons from banks that have braved the economic crisis—And from those that have not. Int. Bus. Rev. 2014, 23, 1096–1107. [Google Scholar] [CrossRef]

- Pal, R.; Torstensson, H.; Mattila, H. Antecedents of Organizational Resilience in Economic Crises—an Empirical Study of Swedish Textile and Clothing SMEs. Int. J. Prod. Econ. 2014, 147, 410–428. [Google Scholar] [CrossRef]

- Rose, A.; Krausmann, E. An economic framework for the development of a resilience index for business recovery. Int. J. Disaster Risk Reduct. 2013, 5, 73–83. [Google Scholar] [CrossRef]

- Henry, D.; Ramirez-Marquez, J.E. A Generic Quantitative Approach to Resilience: A Proposal. INCOSE Int. Symp. 2010, 20, 291–301. [Google Scholar] [CrossRef]

- Nyikos, G.; Soha, B.; Béres, A. Entrepreneurial resilience and firm performance during the COVID-19 crisis–Evidence from Hungary. Reg. Stat. 2021, 11, 29–59. [Google Scholar] [CrossRef]

- Tolner, F.; Pálovics, R.; Barta, B.; Eigner, G. Long-term Development Perspectives of Resilient Companies. In Proceedings of the 2023 IEEE 21th Jubilee World Symposium on Applied Machine Intelligence and Informatics (SAMI), Herl’any, Slovakia, 19–21 January 2023; IEEE: Piscataway, NJ, USA, 2023. [Google Scholar] [CrossRef]

- Soroka, A.; Bristow, G.; Naim, M.; Purvis, L. Measuring regional business resilience. Reg. Stud. 2019, 54, 838–850. [Google Scholar] [CrossRef]

- Tolner, F.; Barta, B.; Eigner, G. Economic Resilience and Antifragility: Classification of SME’s Shock Reactions based on Balance Sheet and Income Statement Data. In Proceedings of the 2023 IEEE 17th International Symposium on Applied Computational Intelligence and Informatics (SACI), Timisoara, Romania, 23–26 May 2023; IEEE: Piscataway, NJ, USA, 2022. [Google Scholar] [CrossRef]

- Pejić, A.; Molcer, P.S. Predictive Machine Learning Approach for Complex Problem Solving Process Data Mining. ACTA Polytech. Hung. 2021, 18, 45–63. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| NACE Code | Cardinality | Industrial Sector |

|---|---|---|

| 25 | 4981 | Manufacture of fabricated metal products |

| 10 | 3284 | Food production |

| 28 | 1827 | Manufacture of machinery and equipment n. e. c. |

| 22 | 1555 | Manufacture of rubber and plastic products |

| 46 | 1347 | Wholesale trade, except of motor vehicles and motorcycles |

| 16 | 1330 | Manufacture of wood and of products of wood and cork, except furniture |

| 33 | 1215 | Repair and installation of industrial machinery, equipment and tools |

| 23 | 987 | Manufacture of non-metallic mineral products |

| 31 | 920 | Furniture production |

| 26 | 709 | Manufacture of computer, electronic and optical products |

| 29 | 629 | Manufacture of road vehicles |

| 47 | 591 | Retail trade, except of motor vehicles and motorcycles |

| 27 | 548 | Manufacture of electrical equipment |

| 32 | 468 | Other manufacturing |

| 15 | 417 | Manufacture of leather and related products, footwear |

| 1 | 380 | Crop and animal production, hunting and related service activities |

| 18 | 339 | Printing and other reproduction activities |

| 43 | 336 | Special construction |

| 36 | 321 | Water production, treatment and supply |

| 24 | 290 | Manufacture of basic metals |

| 45 | 258 | Trade and repair of motor vehicles and motorcycles |

| 20 | 232 | Manufacture of chemicals and chemical products |

| 51 | 203 | Air Transport |

| 41 | 182 | Construction of buildings |

| 30 | 179 | Manufacture of other transport equipment |

| 56 | 154 | Hospitality |

| 13 | 150 | Manufacture of textiles |

| 17 | 132 | Manufacture of paper and paper products |

| 52 | 106 | Warehousing and support activities for transportation |

| 49 | 96 | Land transport by pipeline |

| 42 | 90 | Construction of other civil engineering projects |

| 21 | 78 | Manufacture of pharmaceuticals |

| 19 | 69 | Coke production, petroleum refining |

| 11 | 47 | Manufacture of beverages |

| 35 | 34 | Electricity, gas, steam and air conditioning supply |

| 14 | 31 | Manufacture of wearing apparel |

| 38 | 28 | Waste management |

| 50 | 24 | Water transportation |

| 55 | 23 | Accommodation service |

| 2 | 22 | Forestry |

| 53 | 6 | Postal and courier activities |

| 3 | 3 | Fishing, fish farming |

| 39 | 3 | Decontamination and other waste treatment |

| 37 | 2 | Sewage collection and treatment |

| 5 | 1 | Coal mining |

| Hypothesis | N | Group Means (Resilient/Control) | Group Medians (Resilient/Control) | t-Values | W-Values | Odds Ratio | (Df = 1) | Decision |

|---|---|---|---|---|---|---|---|---|

| H1 | 1349 | 5.8/5.9 (years) | 6.0/6.0 (years) | −0.597 (0.275) | 12,559 (0.036) | N.A. | N.A. | Rejected |

| H2 (t = 2) | 1161 | 320.1/395.2 (M HUF) | 129.5/179.3 (M HUF) | −2.823 (0.002) | 184,387 (0.000) | N.A. | N.A. | Rejected |

| H2 (t = 5) | 766 | 331.5/550.9 (M HUF) | 125.1/246.5 (M HUF) | −5.564 (0.000) | 51,920 (0.000) | Rejected | ||

| H2 (t = 7) | 530 | 482.1/721.5 (M HUF) | 134.6/314.3 (M HUF) | −5.892 (0.000) | 24,692 (0.000) | Rejected | ||

| H2 (t = 10) | 225 | 490.3/1008.5 (M HUF) | 187.5/415.9 (M HUF) | −4.788 (0.000) | 4170 (0.000) | Rejected | ||

| H3 (t = 2) | 1164 | 18.2/20.8 | 7.0/14.5 | −1.121 (0.131) | 64,034 (0.000) | N.A. | N.A. | Rejected |

| H3 (t = 5) | 769 | 17.4/25.4 | 7.0/14.5 | −4.212 (0.000) | 28,920 (0.000) | Rejected | ||

| H3 (t = 7) | 531 | 20.4/30.8 | 7.0/14.5 | −2.906 (0.002) | 11,839 (0.000) | Rejected | ||

| H3 (t = 10) | 228 | 27.8/42.2 | 14.5/34.5 | −1.841 (0.033) | 2351.5 (0.000) | Rejected | ||

| H4 | 104 | N.A. | N.A. | N.A. | N.A. | 0.095 (0.758) | 1.153 (0.759) | Rejected |

| H5 | 345 | N.A. | N.A. | N.A. | N.A. | 0.120 (0.729) | 1.198 (0.729) | Rejected |

| H6 (t = 1) | 1059 | 6.0/20.5 (%) | −1.9/11.6 (%) | −6.468 (0.000) | 177,337 (0.000) | N.A. | N.A. | Rejected |

| H6 (t = 2) | 1048 | 12.8/19.3 (%) | 3.3/13.1 (%) | −2.761 (0.003) | 203,523 (0.000) | Rejected | ||

| H6 (t = 3) | 1012 | 10.9/18.4 (%) | 2.9/11.3 (%) | −3.431 (0.000) | 188,676 (0.000) | Rejected | ||

| H6 (t = 5) | 767 | 10.0/16.8 (%) | 5.1/10.5 (%) | −2.880 (0.002) | 111,607 (0.000) | Rejected | ||

| H6 (t = 7) | 530 | 14.2/12.6 (%) | 4.7/8.9 (%) | 0.471 (0.681) | 60,264 (0.002) | Rejected | ||

| H6 (t = 10) | 228 | 4.7/4.0 (%) | −0.6/4.8 (%) | 0.186 (0.574) | 11,559 (0.067) | Failed to reject | ||

| H7 (t = 2) | 1095 | 0.6/0.5 | 0.6/0.5 | 4.201 (0.000) | 345,400 (0.000) | N.A. | N.A. | Rejected |

| H7 (t = 5) | 730 | 0.6/0.6 | 0.6/0.6 | 3.975 (0.000) | 157,209 (0.000) | Rejected | ||

| H7 (t = 7) | 506 | 0.6/0.6 | 0.6/0.6 | 4.415 (0.000) | 78,097 (0.000) | Rejected | ||

| H7 (t = 10) | 220 | 0.7/0.6 | 0.7/0.6 | 3.979 (0.000) | 15,914 (0.000) | Rejected |

| Classification Results for Resilient + Antifragile Observations | |||||||||||||||

| Data Info | Random Forest | Logistic Regression | |||||||||||||

| No. of Samples | No. of Variable | No. of Missing Data | No. of True Labels | No. of False Labels | AUC | F1 Score | Recall | Precision | Accuracy | AUC | F1 Score | Recall | Precision | Accuracy | |

| Data_1 | 40,695 | 60 | 36,728 | 8774 | 31,921 | 0.75 ± 0.02 | 0.48 ± 0.02 | 0.55 ± 0.04 | 0.42 ± 0.01 | 0.74 ± 0.01 | 0.64 ± 0.01 | 0.36 ± 0.02 | 0.43 ± 0.03 | 0.31 ± 0.01 | 0.67 ± 0.01 |

| Data_2 | 40,695 | 132 | 115,660 | 8774 | 31,921 | 0.67 ± 0.01 | 0.39 ± 0.01 | 0.44 ± 0.02 | 0.34 ± 0.01 | 0.70 ± 0.01 | 0.48 ± 0.02 | 0.28 ± 0.02 | 0.45 ± 0.09 | 0.20 ± 0.01 | 0.50 ± 0.05 |

| Data_3 | 40,695 | 48 | 74,950 | 8774 | 31,921 | 0.74 ± 0.01 | 0.46 ± 0.02 | 0.49 ± 0.03 | 0.43 ± 0.02 | 0.75 ± 0.01 | 0.57 ± 0.01 | 0.34 ± 0.01 | 0.50 ± 0.06 | 0.26 ± 0.01 | 0.58 ± 0.04 |

| Classification Results for Antifragile Observations | |||||||||||||||

| Data Info | Random Forest | Logistic Regression | |||||||||||||

| No. of Samples | No. of Variable | No. of Missing Data | No. of True Labels | No. of False Labels | AUC | F1 Score | Recall | Precision | Accuracy | AUC | F1 Score | Recall | Precision | Accuracy | |

| Data_1 | 40,695 | 60 | 36,728 | 1053 | 39,642 | 0.88 ± 0.02 | 0.30 ± 0.05 | 0.41 ± 0.09 | 0.25 ± 0.05 | 0.95 ± 0.01 | 0.78 ± 0.04 | 0.14 ± 0.03 | 0.36 ± 0.05 | 0.08 ± 0.02 | 0.88 ± 0.02 |

| Data_2 | 40,695 | 132 | 115,660 | 1053 | 39,642 | 0.83 ± 0.02 | 0.21 ± 0.04 | 0.28 ± 0.05 | 0.17 ± 0.04 | 0.94 ± 0.01 | 0.53 ± 0.03 | 0.05 ± 0.01 | 0.35 ± 0.08 | 0.03 ± 0.00 | 0.67 ± 0.05 |

| Data_3 | 40,695 | 48 | 74,950 | 1053 | 39,642 | 0.84 ± 0.01 | 0.20 ± 0.06 | 0.21 ± 0.08 | 0.22 ± 0.09 | 0.96 ± 0.01 | 0.61 ± 0.04 | 0.06 ± 0.00 | 0.63 ± 0.09 | 0.03 ± 0.00 | 0.53 ± 0.07 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tolner, F.; Barta, B.; Eigner, G. Reaction to Idiosyncratic Economic Shocks—Economic Resilience of Small- and Medium-Sized Enterprises. Sustainability 2024, 16, 5470. https://doi.org/10.3390/su16135470

Tolner F, Barta B, Eigner G. Reaction to Idiosyncratic Economic Shocks—Economic Resilience of Small- and Medium-Sized Enterprises. Sustainability. 2024; 16(13):5470. https://doi.org/10.3390/su16135470

Chicago/Turabian StyleTolner, Ferenc, Balázs Barta, and György Eigner. 2024. "Reaction to Idiosyncratic Economic Shocks—Economic Resilience of Small- and Medium-Sized Enterprises" Sustainability 16, no. 13: 5470. https://doi.org/10.3390/su16135470