Abstract

This paper uses panel data from the 2014–2020 China Family Panel Studies (CFPS) to study the impact of digital inclusive finance (DIF) on the cultural consumption of urban and rural residents using two-way fixed effects. The results show that DIF can promote the growth of cultural consumption of urban and rural residents, and the promotion effect is greater for rural residents. Mechanism analysis shows that DIF increases the cultural consumption of urban and rural residents mainly through easing liquidity constraints, reducing precautionary savings, and increasing payment convenience. Moreover, reducing precautionary savings has a greater impact on the cultural consumption of urban residents, while the other two mechanisms have a greater impact on rural residents. In the heterogeneity analysis, credit business and some indicators reflecting the convenience of payment have a greater impact on rural residents. The insurance business has a greater impact on urban residents. This paper provides policy references for the development of DIF and the enhancement of residents’ cultural consumption.

1. Introduction

Cultural consumption is an essential measure of a country or region’s residents’ quality of life [1]. It directly reflects the richness of their spiritual life and the quality of their lives. Raising residents’ cultural consumption supports sustainable lifestyles [2,3], promotes upgrading the consumption structure [4], and enhances people’s well-being [5]. In addition, it also reduces social exclusion while increasing the people’s sense of social belonging [4,6].

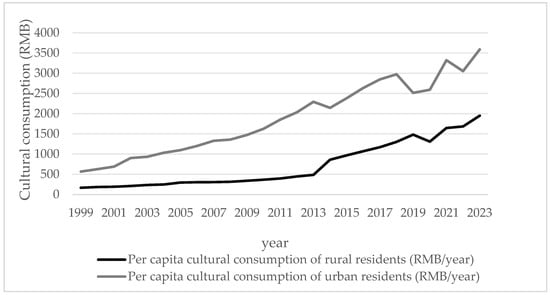

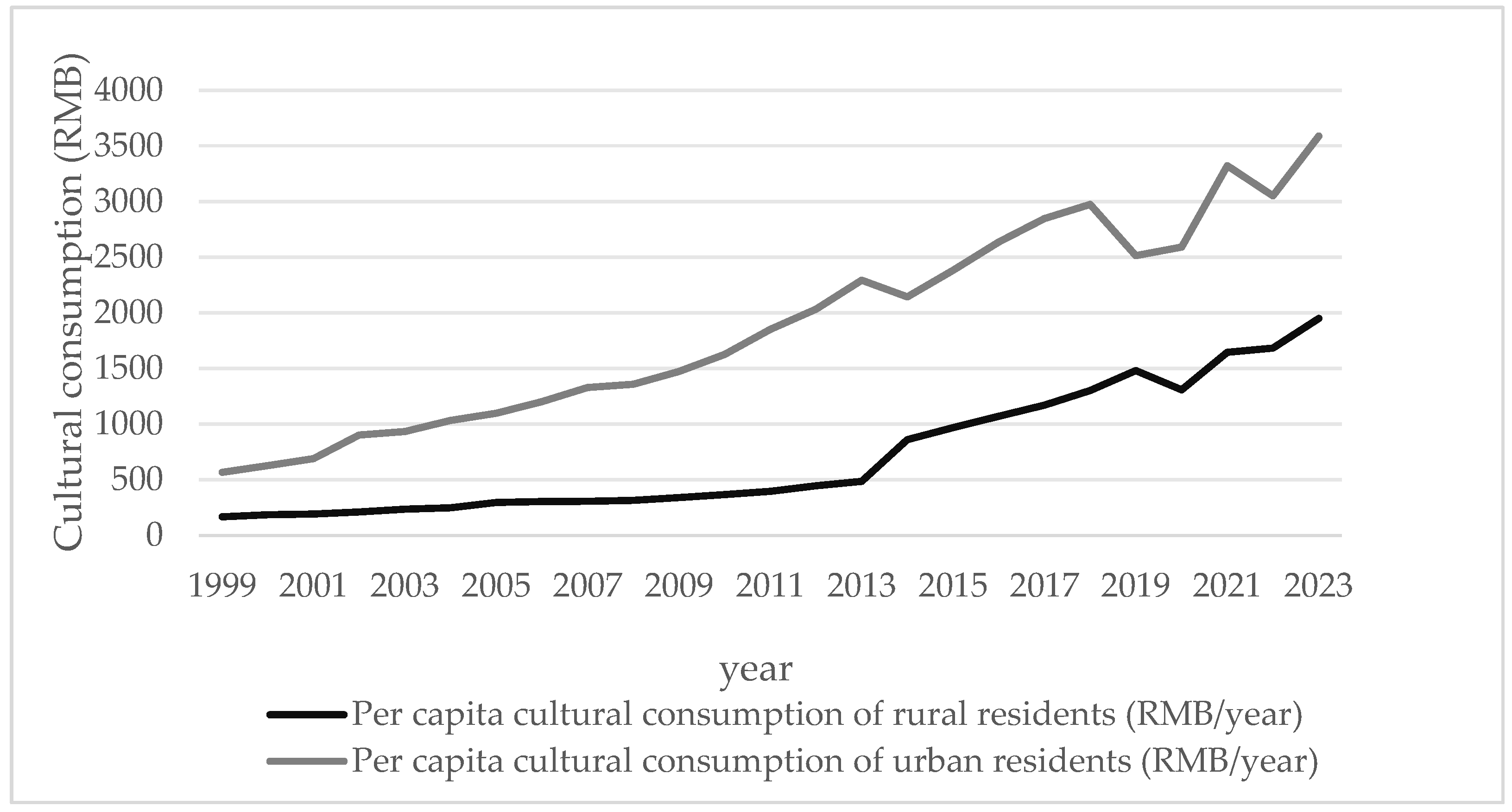

For a long time, China’s economy has been defined by a clear urban-rural dual structure, in which rural areas face the double dilemma of insufficient material wealth accumulation and a scarcity of cultural product supply [7]. Rural residents’ spiritual and cultural lives are largely barren, and their total quality of life is inferior to that of urban residents [8]. To better understand the current state of cultural consumption among urban and rural people, this article employs data from China’s National Bureau of Statistics to create a per capita cultural consumption curve among urban and rural inhabitants, as shown in Figure 1. It has been discovered that the cultural consumption of urban and rural residents has shown an overall upward trend over the last two decades, and the gap between urban and rural areas is evident. For example, in 2023, the per capita cultural consumption of China’s rural and urban residents will be CNY 1951 and CNY 3589, respectively, and the ratio of per capita cultural consumption of rural and urban residents will be 1:1.84. As a result, research on increasing cultural consumption among urban and rural residents, particularly among the latter, is critical for improving quality of life and closing the urban-rural divide.

Figure 1.

The curves of cultural consumption of urban and rural residents.

This paper examines the effect of digital inclusive finance (DIF) on promoting cultural consumption in urban and rural residents. DIF is the combination of digital technology and inclusive finance. Digital technology, which can break through the limitations of time and space, is conducive to expanding the social boundaries of residents and changing their original preferences, values, and lifestyles, which in turn changes cultural consumption patterns [9]. Inclusive finance can also increase the availability of financial services to disadvantaged groups and enhance the ability to consume culturally.

DIF is widely used to explain the phenomenon of residential consumption growth and upgrading the consumption structure that has emerged in China. It is widely recognized in the academic community that the development of digital inclusive finance has promoted the growth of urban residents’ consumption and the upgrading of their consumption structure [10]. In addition, the role of the Internet in cultural consumption has also been confirmed [11]. Some scholars believe developing the Internet can effectively increase residents’ cultural consumption [12,13]. The propensity for cultural and recreational consumption increases significantly in rural households that have mastered Internet skills. Some scholars also suggest that the popularization of the Internet significantly reduces the cultural consumption gap between urban and rural residents [14]. However, there needs to be more literature studying the impact of DIF on the cultural consumption of urban and rural residents.

Based on the above analysis, this paper empirically analyzes the impact of DIF on the cultural consumption of urban and rural households using data from the China Family Panel Studies (CFPS) from 2014 to 2020. This paper adopts the provincial DIF index published by Peking University to measure the regional level of DIF development. In the empirical study, a double fixed effects model is used to examine the relationship between DIF and the cultural consumption of urban and rural residents.

The empirical results of this paper show that every unit increase in DIF increases the cultural consumption expenditure of urban and rural residents by 1.2% and 4.6%, respectively. To show the robustness of the estimation results, we reduce the number of years in the resident sample, delete part of the sample, and replace the dependent variables, obtaining results similar to those of the benchmark regression.

It is indisputable that the reverse causation problem may impact our estimation results. The increase in residents’ cultural consumption expenditures may reduce the cost of Internet use, thereby promoting the development of DIF. Therefore, this paper adopts the instrumental variable test method. The spherical distance from the provincial capital city where the respondent lives to Hangzhou City multiplied by the mean value of DIF index in all provinces (except for the province where the respondent is located) is chosen as the instrumental variable. The test results are consistent with the baseline regression.

The research also investigates the mechanism and heterogeneity of DIF on the cultural consumption of urban and rural residents. The mechanism variables are liquidity constraints, precautionary savings, and payment convenience. Moreover, decreasing precautionary savings more strongly impacts the cultural consumption of urban residents, whereas the other two variables show a greater impact on rural residents. In the heterogeneity analysis, the credit business and some indices of payment convenience exert a stronger influence on rural residents, whereas the insurance business exerts a greater influence on urban residents.

This paper contributes to the current literature in two ways. First, this paper differs from previous studies. When discussing the effect of DIF on residents’ cultural consumption, the existing literature usually assumes that DIF development promotes economic growth, thereby increasing residents’ cultural consumption [15,16]. However, by building a mathematical model, this paper finds that in addition to promoting economic growth, DIF development promotes cultural consumption by changing residents’ consumption patterns. This is manifested in the fact that residents buy more cultural products and services in the market while reducing family cultural activities such as emotional communication and leisure. This is why DIF has a greater impact on rural residents’ cultural consumption, but it has yet to be mentioned in the literature.

Second, this paper contributes to the literature on DIF and the upgrading of the consumption structure. In the digital era, many studies have emphasized the impact of DIF. Urban and rural residents’ consumption level or structure improvement is the research object emphasized at the micro level. Much of the literature argues that the digital divide has led to an insignificant effect of the DIF on the consumption growth and upgrading of the consumption structure of rural residents [17,18]. However, this paper finds that the impact of DIF on rural residents’ cultural consumption is greater because digital technology significantly changes cultural consumption patterns, while inclusive finance improves the ability of rural residents to smooth out their cultural consumption. This paper enriches the existing literature.

The rest of the paper is organized as follows. Section 2 delineates a theoretical framework and analyzes the mechanisms. Section 3 defines the variables and states the empirical methods. Section 4 discusses specific empirical results. Section 5 presents an analysis of heterogeneity. Section 6 delineates specific conclusions, policy implications, and limitations.

2. Theoretical Framework

2.1. A Theoretical Model

Examine an economy characterized by a stable population, presuming the existence of numerous homogeneous families and its permanence. Each household has a fixed amount of time each period, and there is no elasticity in the labor supply. Households generate income from their working hours, which can be spent on non-cultural and cultural items or invested in production as physical capital. Households also benefit from leisure time for emotional interaction, recreation, and other purposes, so a household’s overall utility function over its lifetime is as follows:

In Equation (1), is the discount rate; are the household non-cultural and cultural consumption at time point , respectively; represents labor time; represents leisure time. Households maximize lifetime utility and save by making the optimal decision for non-cultural and cultural consumption. Considering the utility of cultural consumption of activities such as emotional communication, leisure, and recreation carried out by family members in their leisure time, they can be considered a part of family cultural activities. Such family cultural activities are different from cultural goods on the market. The instantaneous utility function of the household is expressed in logarithmic form as follows:

In Equation (2), the coefficient represents the cultural consumer goods produced and consumed by households in their leisure time and is a function of DIF. The first-order derivative of to DIF is less than zero. This result is because the development of DIF based on digital technology helps individuals or households break through time and space constraints and greatly expands their social boundaries. Digital technology has also enabled people with shared preferences and values to form quasi-communities in the real world or the online world. This digital technology has changed the old way of life by reducing cultural activities within the family in favor of cultural products from the market. As a result of the rise of DIF, there has been a slight decline in the demand for and relative value of family cultural activities.

The product market is assumed to be competitive, with firms renting capital from households and employing labor to produce. Assuming constant returns to scale, the firm’s production function, expressed using the Cobb–Douglas production function, is as follows:

In Equation (3), and represent labor and capital, respectively; represents the level of integrated technology. will be affected by the development of DIF. In other words, DIF affects firms’ output by affecting their combined technology and thus their output.

Households can maximize lifetime utility by choosing the optimal decision between non-cultural and cultural consumption and can save. The mathematical formulation of this economic problem is as follows:

In Equation (5), is the discount rate. Construct the Lagrange multiplier form and obtain the four first-order conditions as shown in Equations (6)–(9):

Transforming from Equation (6) and substituting into the constraint Equation (5) yields , then . Both sides divided by provide:

The two results under equilibrium conditions are obtained from Equations (7)–(9) and substituting into Equation (10) and further collation can be obtained:

As illustrated by Equation (11), the development of DIF is associated with an increase of and a decline of . The value in the middle bracket denotes a constant, increasing . This indicates that the expansion of residents’ cultural consumption is due to the advancement of DIF, which promotes economic development. Furthermore, the growth of DIF reduces family cultural activities, causing residents to purchase cultural commodities from the market as an alternative to family cultural activities.

Rural locations have a more limited geographical and social context and fewer resources than urban ones. This increases rural residents’ opportunities for emotional engagement, leisure, and enjoyment with family members. As the digital technology underlying DIF continues to evolve and expand, it presents new avenues for social interaction and engagement among rural residents. First, mobile phones and computers enable rural residents to access information and resources vastly beyond their immediate location, effectively transcending geographical boundaries. Second, many digital technology application platforms allow rural residents to express themselves and their ideas by sharing their everyday agricultural experiences via short video platforms. The advent of digitization has resulted in the creation of novel cultural items that integrate entertainment, learning, and education. These include e-books and online theaters, expanding the range and depth of cultural experiences available to rural residents while addressing contemporary cultural needs. Therefore, compared to urban households, DIF has facilitated a more rapid transition in rural residents’ cultural consumption patterns, shifting from household production to external purchases. This suggests that DIF is more important in promoting cultural consumption among rural and urban residents. This paper puts forth the initial hypothesis based on the preceding findings.

According to the above, DIF can increase the cultural consumption of urban and rural residents and has a greater impact on the cultural consumption of rural residents.

2.2. Mechanisms Analysis

2.2.1. Liquidity Constraints

The concept of liquidity constraints posits that as households encounter more significant liquidity constraints, their consumption levels decline. Conversely, when households have access to financial services, their liquidity constraints are reduced, leading to increased consumption [19]. DIF serves to reduce the financing threshold for residents. It increases the availability of financial services for all social classes, including those with deficient and middle incomes. This helps alleviate household liquidity constraints, and includes services such as the installment loan service for mobile phone payments, which frequently provide for high-value cultural products. As a result, consumer acceptance and tolerance of total consumption are improved [20].

It is worth noting that there needs to be more financial service institutions in rural China than in urban areas. Rural residents often need help dealing with emergencies or large expenditures in these areas due to a need for appropriate financial instruments to regulate consumption and savings [21]. These liquidity constraints hinder rural residents’ consumption patterns, forcing them to take a more conservative approach to responding to demand. DIF can provide rural communities with convenient, efficient, and inclusive financial services through an online platform [22]. DIF also allows rural residents to complete various financial transactions, including loan applications, savings deposits, payments, and settlements [11]. This improves the accessibility and convenience of financial services while reducing rural residents’ liquidity constraints regarding cultural consumption.

Based on the above evidence, this paper proposes that DIF increases cultural consumption among urban and rural residents by alleviating liquidity constraints, with a greater impact on rural residents.

2.2.2. Precautionary Savings

Insurance can mitigate the risk of household income loss due to unemployment, health issues, and other factors and reduce the household’s exposure to significant medical expenses. It can also help households cope with future uncertainty and contribute to their preventive savings [23]. DIF can provide fair services for people with insurance needs from all social strata, reducing the threshold for residents to participate in insurance services and the cost of insurance services by using e-commerce platforms and big data [24]. The use of big data allows for the provision of insurance products and services that are more diversified and even customized, which effectively increases the willingness of residents to participate in insurance [25,26].

Compared to their urban counterparts, those residing in rural areas tend to have lower income levels. Consequently, they are more likely to utilize their limited financial resources to address various risks encountered in their daily lives, including illnesses and accidents. Furthermore, the limited dissemination of insurance knowledge in rural areas has resulted in a need for more awareness and understanding of insurance products among many rural residents. This, in turn, has led to a lack of motivation and confidence in purchasing insurance [27]. This inclination to allocate funds toward savings rather than insurance purchases constrains rural residents’ discretionary spending.

In light of these findings, this paper proposes that DIF increases cultural consumption among urban and rural residents by reducing precautionary savings, with a greater impact on urban residents.

2.2.3. Payment Convenience

The advent of digital payments based on Internet technology has significantly transformed the traditional cash payment mode. The popularity of mobile payment platforms, particularly WeChat and Alipay, has facilitated daily consumption in urban and rural households while increasing the frequency and volume of payments made by residents [28,29]. Mobile payment reduces the cost of consumption and the time and effort spent searching for product information, thereby enhancing transaction efficiency [30]. Furthermore, customers regard random discounts, points, and coupons supplied by merchants or financial service platforms during digital payment as a form of gratuity and use them for hedonic experiences such as cultural products and services [31,32].

Rural residents face more significant financial constraints than their urban counterparts due to the scarcity and uneven distribution of financial institutions in rural areas. The convenience of DIF payments can alleviate rural residents’ cash constraints during the consumption process and significantly expand their consumption channels, enabling them to enjoy a convenient shopping experience comparable to that of urban residents [33].

Based on the preceding evidence, this paper proposes that DIF increases cultural consumption among urban and rural residents by improving payment convenience, with a greater impact on rural residents.

3. Data and Empirical Strategy

3.1. Construction of Variables

3.1.1. Cultural Consumption

The dependent variable is residents’ cultural consumption. Cultural consumption refers to consuming goods and services with aesthetic function and instrumental use, primarily linked with art, culture, and leisure. There are two definitions of cultural consumption. The first is generalized cultural consumption, defined as the sum of direct and indirect cultural consumption expenditure. The second is cultural consumption, defined as direct cultural consumption expenditure [1,34]. China’s National Bureau of Statistics and various survey and statistical databases define generalized cultural consumption in China. This paper also uses generalized cultural consumption. The CFPS database data related to generalized cultural consumption were summed to form a proxy variable for the cultural consumption of urban and rural residents. This proxy variable is logarithmic in this paper to mitigate the impact of the order-of-magnitude difference.

3.1.2. Digital Inclusive Finance

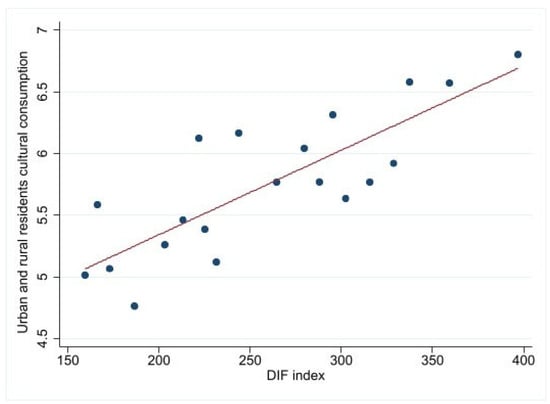

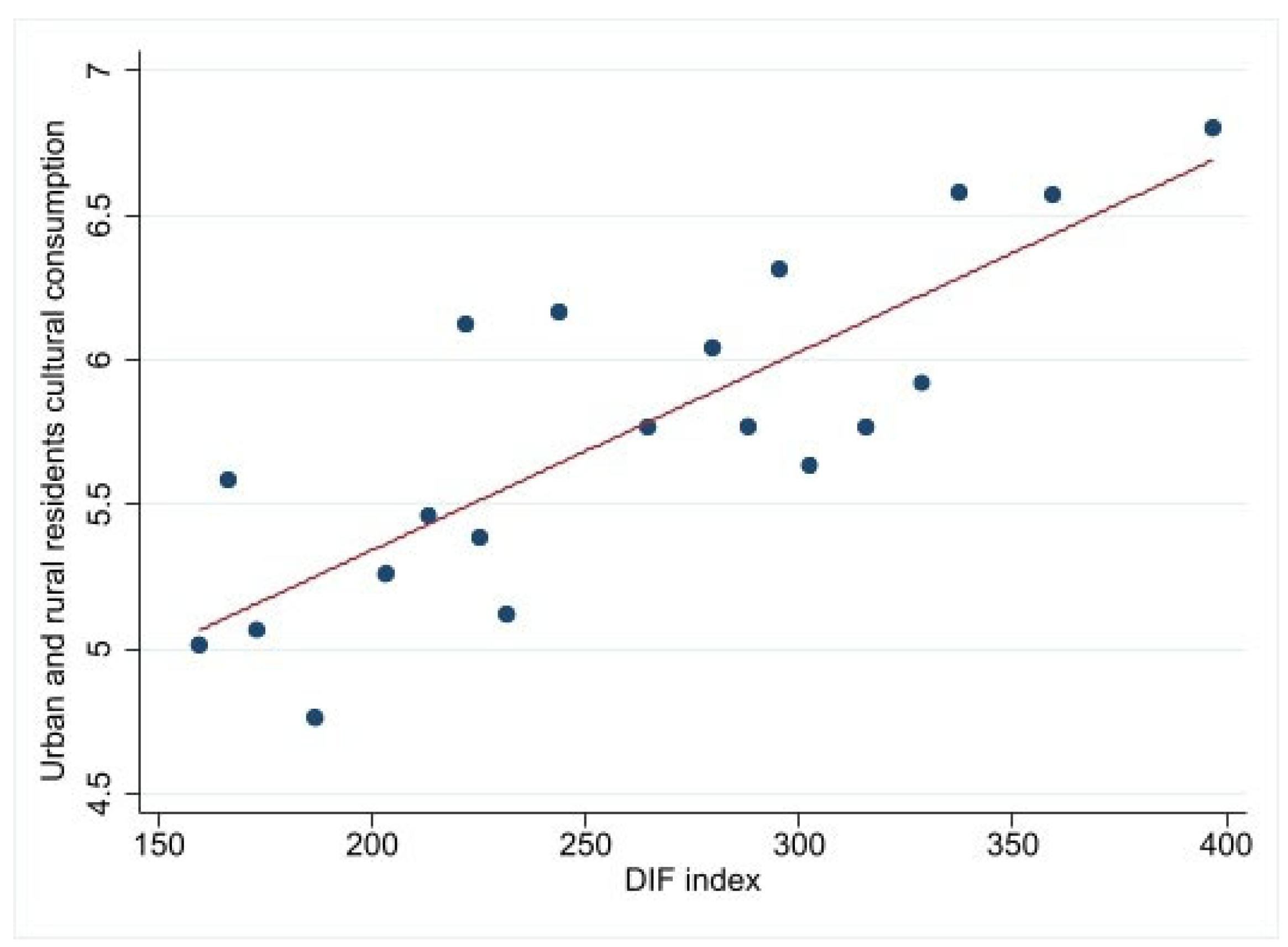

The independent variable is DIF. Under the prevailing approach in the extant literature [35], this paper uses the DIF Index published by Peking University as a proxy variable representing the level of development of DIF. It is currently China’s most authoritative data for DIF research, with high credibility. The paper presents a scatter diagram of DIF and cultural consumption of urban and rural residents in Figure 2.

Figure 2.

A scatter diagram of DIF and cultural consumption of urban and rural residents.

3.1.3. Control Variables

The cultural consumption of residents is influenced not only by the advancement of DIF but also by other factors in the real world. This paper employs the strategy used in the existing literature of adding control variables at the individual, household, and provincial levels to reduce the impact of omitted variables [15,36]. At the individual level, the analysis includes a range of classical variables, such as the gender, age, education, and health status of respondents. The household-level controls encompass a range of variables, including family size, the ratio of elderly dependents to the family labor force, the ratio of children to the family labor force, the net worth of the household, and the household’s liabilities. Furthermore, the provincial level of the traditional financial development variable is introduced to account for discrepancies in traditional financial development across regions. After deleting missing values and samples of residents with extreme outliers in the variables, this paper collected a total sample of 35,946 residents, comprising 17,998 urban and 17,948 rural residents. The descriptive statistics for the primary variables are presented in Table 1.

Table 1.

Descriptive statistics.

This paper also used a t-test on a sample of urban and rural residents’ cultural consumption to better understand whether there are differences between both groups and whether these differences are statistically significant. The results demonstrate that the mean value of rural residents’ cultural consumption is less than that of urban residents, with a statistically significant difference at the 1% level. This indicates a notable disparity in cultural consumption between urban and rural residents.

3.2. Data Source

The data utilized in this study are derived from three primary sources of matched data. First, the CFPS provides data on residents’ cultural consumption and control factors relating to household characteristics. This database is updated biennially and includes multidimensional income, expenditure, and assets. The survey offers substantial empirical evidence to support this paper. This paper starts with 2013, a critical year in the development of DIF in China, and analyzes data from CFPS 2014, 2016, 2018, and 2020. Second, the DIF index released by Peking University provides data to monitor the development of DIF in China [37]. As a crucial instrument for tracking the advancement of digital financial services in China, the index offers a comprehensive overview of their breadth of coverage, depth of usage, and degree of digitization. This makes it an invaluable resource for policymakers, financial institutions, and researchers. Third, control variables, such as the level of traditional financial development, are based on data from previous years’ China Statistical Yearbooks.

3.3. Empirical Model

To accurately identify the impact of DIF on residents’ cultural consumption, this paper constructs a benchmark regression model as follows:

In the model, the subscripts , , and are used to denote households, provinces, and years, respectively. is the logarithm of cultural consumption expenditure of resident households; is the DIF of the province where the resident is located; are the control variables; and are household-fixed effects and year-fixed effects, respectively; is the random perturbation term. To address the potential issue of reverse causality, the DIF is delayed by one period. The objective of this paper is to examine the coefficient . In conjunction with previous research [8,15], this paper provides the following explanation for . A significant positive value of indicates that DIF facilitates the growth of cultural consumption among urban and rural residents. Conversely, a significant negative value of indicates that DIF has a restrictive effect on the cultural consumption of residents. In the absence of a significant value, the impact of DIF on residents’ cultural consumption is considered inconsequential.

4. Results and Discussion

4.1. Baseline Regression

Before conducting the regression test, the variance inflation factor (VIF) is used to test for multicollinearity for all explanatory variables of the panel data. The result shows that the maximum VIF value is 1.46, which is less than the upper limit of the multicollinearity value of 10, so there is no multicollinearity between variables. Then, the Hausman test was conducted on the full-sample panel data, and the results showed that the Hausman statistics were all significant at the 1% level, which rejected the original hypothesis that the random effect model was better than the fixed effect model. Accordingly, this paper selects the two-way fixed effect model to identify the impact of DIF on the cultural consumption of urban and rural residents.

Table 2 presents the results of the baseline regressions examining the impact of DIF on the cultural consumption of urban and rural residents. Columns (1) to (3) illustrate the findings for the regressions above. The coefficients are estimated using stepwise regression, with column (1) representing the result of the model regression using the total sample. This demonstrates a positive impact of DIF on cultural consumption at the 1% statistical level. The model results, tested separately for the urban and rural samples, are presented in columns (2) and (3). A comparison of the coefficients reveals that the marginal impact of DIF on the cultural consumption of rural residents is significantly higher than that of urban residents. In the sample of urban residents, the regression coefficient for DIF is 0.012, which is significant at the 1% level. The economic impact is that for every standard deviation increase in DIF, urban residents’ cultural consumption increases by 12.6%. Similarly, in the sample of rural residents, the regression coefficient of DIF is 0.046, which is statistically significant at the 1% level. The economic impact of this is that for every one standard deviation increase in DIF, rural residents’ cultural consumption will rise by 56.5%. Therefore, the regression results for both groups are statistically and economically significant. The urban-rural difference is also significant using the Chow test. These results prove that DIF promotes cultural consumption for both urban and rural residents and will have a greater impact on rural residents.

Table 2.

Baseline regression results.

The regression results for the control variables show that none of the control variables at the individual level significantly affect the cultural consumption of urban and rural residents. The reason for this may be that for most households, these variables change very little or even remain unchanged over a short period, resulting in their effect being absorbed by household fixed effects. In household demographic characteristics, household size and the child dependency ratio positively correlate with the residents’ cultural consumption. In particular, the child dependency ratio is significant in the urban sample and not in the rural sample. This may be because parents in urban households can support their children’s participation in educational and cultural activities more than in rural households. Elderly dependency ratios negatively correlate with household cultural consumption, mainly due to precautionary savings motives. When the rate of older people in a household rises, household expenditures on support for the elderly increase, and the need to save for emergencies increases. This reduces the residents’ ability and desire to purchase cultural goods. In household resource characteristics, as in previous studies [38], increases in household assets and liabilities positively correlate with residents’ cultural consumption expenditures. This may be because a moderate level of debt can increase current disposable income and ease liquidity constraints, helping households realize smoothing consumption. Finally, there is no significant relationship between traditional finance and cultural consumption. This is consistent with existing studies.

4.2. Endogeneity Test

In this part, the paper discusses probable endogeneity issues. This paper uses a fixed-effects model and incorporates control variables to tackle the endogeneity issue of omitted variables, particularly those that do not change over time at the personal level. However, the problem of omitted variables remains. At the same time, the DIF index may contain measurement errors. All these issues can cause endogeneity problems in our regression model. The instrumental variable method is applied to control endogeneity.

Based on the theory of instrumental variable selection and existing research, this paper uses the spherical distance from the provincial capital city to Hangzhou as the instrumental variable for provincial DIF. Combined with previous studies, the rationale for selecting this is as follows [39]. First, the spherical distance between the province’s capital city and Hangzhou does not directly affect cultural consumption. Therefore, it meets the instrumental variable’s exclusivity criteria. Second, Hangzhou is known as the Internet capital and the location of Alibaba’s headquarters. The geographic distance between a location and Hangzhou can frequently indicate the extent of IT and DIF development. This is consistent with the relevance of instrumental variable selection. Since this work uses the DIF index with time variation as a proxy variable for DIF, the instrumental variables should change with time. As a result, this paper uses the spherical distance from each provincial capital city to Hangzhou City multiplied by the average value of the DIF index for all provinces (excluding the province where the respondent is located) as an instrumental variable to express time change.

As demonstrated in the preceding analysis, this paper employs the least squares method for regression. The results in the first stage are presented in Table 3, columns (1) and (3). The instrumental variables are significantly and negatively correlated with DIF at the 1 percent level, indicating that the further one is from Hangzhou, the lower the level of DIF development. This aligns with expectations. In the second stage, estimation is conducted via instrumental variables. The results in columns (2) and (4) of Table 3 demonstrate that the Cragg–Donald Wald F and Kleibergen–Paak rk LM statistics are sufficiently elevated, indicating that the instrumental variables have been appropriately selected. The use of weak instrumental variables is not an issue. The positive impact of DIF is statistically significant at the 1% level for both urban and rural residents. Furthermore, the coefficient observed in the rural sample is more significant than that observed in the urban sample, indicating that the baseline regression results remain valid after addressing endogeneity concerns.

Table 3.

Endogeneity test results.

4.3. Robustness Tests

In this paper, we control for the effects of household net worth and household liabilities in the baseline regressions to verify the robustness of the benchmark regressions [35], as shown in columns (1) to (3) of Table 2. Despite controlling for these factors, DIF continues influencing cultural consumption among urban and rural residents. These findings are further substantiated by the regression results with instrumental variables in columns (4) and (5) of Table 2.

Furthermore, the paper employs the following robustness tests: First, the 2020 sample was excluded from the analysis. As illustrated in Figure 1, there is a notable decline in cultural consumption expenditures among urban and rural residents in 2020, potentially introducing bias into the empirical results. Therefore, the 2020 sample was excluded from the regression analysis. The results of the model in Table 4, columns (1) and (2), demonstrate that the impact of DIF on urban and rural residents’ cultural consumption is consistent with benchmark regression. Second, the sample of the four municipalities directly governed by the central government was removed. There may be significant differences in unique development characteristics between the four cities directly administered by the central government and the other provinces, which may also bias the empirical results. Therefore, the samples from these cities were excluded, and the regressions were rerun. The results presented in columns (3) and (4) are consistent with benchmark regression. Third, the dependent variable is replaced. Previous studies have focused on testing the impact of DIF on the absolute amount of residents’ cultural consumption. However, the present study tests the impact of DIF on the relative amount of residents’ cultural consumption. The regression results in columns (5) and (6) indicate that DIF enhances the proportion of cultural consumption among urban and rural residents within total consumption. Notably, this effect is more pronounced among rural residents, aligning with the results of the benchmark regression.

Table 4.

Robustness test results.

4.4. Mechanism Examination

4.4.1. Mechanism Examination of Liquidity Constraints

To validate the liquidity constraints mechanism, the “household liquidity constraint” concept is introduced as a proxy variable. This is calculated by comparing the liquid assets of the sample households in urban and rural areas with their respective medians. A household is subject to liquidity constraints if its liquid assets are below the median value. In this instance, 1 is assigned, whereas 0 is assigned in contrast. The model results are presented in columns (1) and (2) of Table 5. The impact coefficients indicate that DIF has a greater effect on liquidity relief for rural households. Moreover, the discrepancy between the two variables has been found to pass the Chow test. These results prove that DIF promotes the growth of cultural consumption among urban and rural residents by alleviating their liquidity constraints, which has a greater impact on rural residents.

Table 5.

Mechanism examination results.

4.4.2. Mechanism Examination of Precautionary Savings

As previously theorized, the internet insurance service provided by DIF can potentially diminish the necessity for precautionary savings, encouraging current consumption. In empirically testing this mechanism, while the CFPS questionnaire did not directly inquire about precautionary savings among households, it did address questions about household commercial insurance expenditures. Increased commercial insurance expenditure mitigates the risk of loss of income or significant medical expenses resulting from unemployment or health problems. Furthermore, it reduces households’ concern about future uncertainty, lowering precautionary savings. Accordingly, household commercial insurance expenditure is a proxy variable for precautionary savings. The model results in columns (3) and (4) of Table 5 demonstrate that DIF facilitates enhanced household risk-coping ability, thereby reducing precautionary savings. Furthermore, the coefficient of influence and Chow test results indicate that DIF exerts a more pronounced impact on urban households. The results suggest that the development of DIF promotes cultural consumption in urban and rural areas by reducing precautionary savings, and the impact is greater for urban residents.

4.4.3. Mechanism Examination of Payment Convenience

DIF enhances the convenience of payment in cultural consumption, eases cash constraints in the consumption process, and reduces the cost of finding goods while improving transaction efficiency [40]. This convenience of payment can be represented in online purchases so that online purchase decisions can be used as a proxy variable for convenience of payment. To do this, we define a dummy variable that is 1 if a family member made an online purchase; otherwise, the variable is 0. Columns (5) and (6) of Table 5 show that DIF facilitates online purchases for rural residents to a greater level than when compared to urban residents. The reason may be that the range of financial institutions that are widely available in urban areas provides greater financial flexibility to the residents, especially in terms of cultural consumption. The emphasis on participation in cultural activities and the superior cultural infrastructure in urban areas improve the convenience and quality of offline cultural experiences for urban residents, thus reducing their propensity to purchase online. This finding confirms that DIF contributes to the growth of cultural consumption among urban and rural residents by improving payment convenience, with a greater impact on rural residents.

5. Heterogeneity Analysis

The DIF index is comprised of three categories: breadth of digital financial coverage (BDFC), depth of digital financial use (DDFU), and degree of digitization of inclusive finance (DDIF). Each of the categorized indices contains a different number of sub-indices. This part chooses some categorized or sub-categorized indices to retest the impact mechanism and investigate urban-rural heterogeneity. This will allow for more in-depth research into the mechanism by which DIF influences cultural consumption and understanding why DIF has a greater impact on rural residents’ cultural consumption.

5.1. Credit Business

Heterogeneity analysis of the credit business represents a re-test of the liquidity constraint mechanism. The credit business is a sub-categorized index subordinate to the DDFU category. The availability of consumer credit can ease constraints on consumption; thus, the credit business can be employed as a proxy variable for liquidity constraints. The results of the heterogeneity analysis are presented in columns (1) and (2) of Table 6. The results demonstrate that the credit business, which reflects the liquidity constraints, has a significant positive impact on the cultural consumption of urban and rural residents. The Chow test indicates that the impact differs in degree between urban and rural areas, which is consistent with the findings of the liquidity constraint mechanism.

Table 6.

Heterogeneity analysis results.

5.2. Insurance Business

Heterogeneity analysis of the insurance business represents a re-test of the precautionary savings mechanism. The insurance business is a sub-categorized index subordinate to the DDFU category. An increase in insurance expenditure reduces households’ need for precautionary savings. Therefore, the insurance business can be a proxy variable for precautionary savings. The results of the heterogeneity analysis are presented in columns (3) and (4) of Table 6. The findings demonstrate that the insurance business exerts a consistently and significantly positive influence on the cultural consumption of urban and rural residents. The urban-rural heterogeneity of the degree of influence passes the Chow test. This heterogeneity result is consistent with the regression results for the precautionary savings mechanism.

5.3. Sub-Index Measuring Payment Convenience

Two categorized indices and one sub-categorized index, the sub-index of the DIF index, are pertinent to payment convenience. The first is the BDFC, which provides an overview of the coverage of electronic accounts and reflects the convenience of payment. The second categorical index is DDIF, which describes the level and depth of convenience of mobile payment applications in daily life and business transactions. Payment Business is a sub-categorized index under DDFU that describes electronic payment businesses’ activity and popularity. A higher index value indicates a more convenient payment system. The heterogeneity analysis of the three sub-indices represents a re-test of the payment convenience mechanism.

In this paper, the three sub-indicators are regressed on the cultural consumption of urban and rural residents, and the results are shown in columns (5) to (10) of Table 6. The model results show that the three sub-indicators contribute significantly to the cultural consumption of urban and rural residents. The Chow test confirms a significant difference between the cultural consumption of urban and rural residents. The results show that the impact of convenience of payment on the cultural consumption of rural residents is greater than that of urban residents. Thus, the payment convenience mechanism is confirmed. This result is consistent with the mechanism test described above, which used “online shopping” as a proxy variable for payment convenience. Given the wide distribution of financial institutions and relatively well-developed cultural facilities, the DIF is more likely to promote cultural consumption among urban residents by increasing the ease of payment for offline consumption rather than online shopping.

6. Conclusions and Suggestions for Policy

Promoting cultural consumption, which combines economic goals with social aspirations, has long been an important focus of consumption policy. In particular, with the rapid growth of DIF, the influence of DIF on the cultural consumption of rural and urban residents is explored individually, providing an important reference for China in promoting cultural consumption through DIF reform. Therefore, we first constructed a general equilibrium model to analyze the impact of DIF on cultural consumption and discussed the existence of urban-rural differences in this impact. Then, a series of econometric models will be used to analyze the impact and mechanism of DIF systematically. The main research conclusions are as follows.

First, DIF effectively promotes residents’ cultural consumption in China. In the benchmark regression, the coefficient of DIF is significantly positive. After a series of robustness tests, such as instrumental variable regression, the results of this paper still hold.

Second, the impact of DIF on the cultural consumption of the residents shows apparent differences between urban and rural areas. As digital financial tools have changed rural residents’ lifestyles and cultural consumption patterns, DIF has promoted rural areas more than urban areas. Third, liquidity constraints, precautionary savings, and payment convenience are the mechanism variables that DIF uses to increase the cultural consumption of urban and rural residents. Moreover, the preventive saving mechanism has a greater impact on the cultural consumption of urban residents, while the other two mechanisms have a greater impact on rural residents. Finally, the heterogeneity analysis results show that credit businesses of DIF have a greater impact on rural residents, as does DDIF. However, the insurance businesses have a greater impact in urban areas, which is consistent with the results of the mechanism test.

These conclusions have the following implications. First, with the help of DIF, residents spend more on cultural products and services to improve their quality of life, and DIF also helps to bridge the urban-rural consumption gap. Therefore, the Chinese government should make more efforts to develop DIF, which can be used as an important policy tool to promote consumption, apart from the consumption policy itself.

Second, to facilitate the smooth functioning of DIF, it is important to optimize the mechanism that promotes cultural consumption. In urban areas, a well-developed social security system and a more substantial credit environment are essential. In rural areas, besides social security systems, network coverage, and Internet usage, DIF products are suited to rural residents, and well-educated and better financial reading materials are essential for encouraging cultural consumption.

Third, the policy implications for policymakers are as follows. Policymakers should establish a sound legal framework to ensure the development of DIF. In addition, policymakers should pay attention to the public’s digital financial literacy, especially in rural areas, to ensure everyone can benefit from the digital finance revolution. This includes educational programs and campaigns to inform people about the advantages of digital financial products and the associated risks.

One critical limitation of this study is that, due to data restrictions, we cannot wholly expose the relationship between DIF development and residents’ cultural consumption. The main reason is that data from 2020 and before and the provincial-level DIF index utilized in the empirical study were generated by averaging the original county-level DIF index, which may result in measurement inaccuracies. At the same time, although this paper uses the appropriate instrumental variables and recognizes that the model is set up correctly, the results of the instrumental variables approach may only be valid in a particular sample or setting. This instrumental variable may not be universal. We will prioritize tracking the publication of the CFPS data and DIF index in future updates and conducting county-level research, assuming county-level CFPS data are available. Moreover, we will also continue to look for more universal solutions to endogeneity. Overcoming these concerns is eagerly awaited for further discussion.

Author Contributions

Conceptualization, X.S. and Z.C.; Methodology, C.W. and J.W.; Software, X.S.; Validation, X.S.; Formal analysis, X.S., C.W. and J.W.; Data curation, X.S.; Writing—original draft preparation, X.S.; Writing—review and editing, Z.C.; Supervision, Z.C. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this research are available on request from the corresponding author.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Katz-Gerro, T. Cultural consumption research: Review of methodology, theory, and consequence. Int. Rev. Sociol. 2004, 14, 11–29. [Google Scholar] [CrossRef]

- Veghes, C. Cultural Consumption as a Trait of a Sustainable Lifestyle: Evidence from the European Union. Eur. J. Sustain. Dev. 2020, 9, 125–136. [Google Scholar] [CrossRef]

- Crociata, A.; Agovino, M.; Sacco, P. Recycling waste: Does culture matter? J. Behav. Exp. Econ. 2015, 55, 40–47. [Google Scholar] [CrossRef]

- Manolika, M.; Baltzis, A. Curiosity’s pleasure? Exploring motives for cultural consumption. Int. J. Nonprofit Volunt. Sect. Mark. 2020, 25, e1640. [Google Scholar] [CrossRef]

- Lee, H.; Heo, S. Arts and cultural activities and happiness: Evidence from Korea. Appl. Res. Qual. Life 2021, 16, 1637–1651. [Google Scholar] [CrossRef]

- Buncák, J.; Hrabovská, A.; Sopóci, J. The Way of Life and the Cultural Consumption of Social Classes in Slovak Society. Sociologia 2019, 51, 25–43. [Google Scholar] [CrossRef]

- Neilson, J. Intra-cultural consumption of rural landscapes: An emergent politics of redistribution in Indonesia. J. Rural Stud. 2022, 96, 89–100. [Google Scholar] [CrossRef]

- Shi, Y.; Cheng, Q.; Wu, Y.; Lin, Q.; Xu, A.; Zheng, Q. Promoting or Inhibiting? Digital Inclusive Finance and Cultural Consumption of Rural Residents. Sustainability 2023, 15, 2719. [Google Scholar] [CrossRef]

- Zhong, Q.; Hilbert, M.; Frey, S. Breaking the Structural Reinforcement: An Agent-Based Model on Cultural Consumption and Social Relations. Soc. Sci. Comput. Rev. 2023, 41, 848–870. [Google Scholar] [CrossRef]

- Yuan, X.; Li, H. Digital Finance Affects the Consumption Path of Urban Digital Finance and Residents: The Expansion of Digital Finance to Consumption in the Perspective of Space Spillover. J. Knowl. Econ. 2024, 15, 9903. [Google Scholar] [CrossRef]

- Hu, N.; Hou, G. Mobile payment, digital inclusive finance, and residents’ consumption behavior research. PLoS ONE 2024, 19, e0288679. [Google Scholar] [CrossRef] [PubMed]

- Aguiar, L.; Martens, B. Digital music consumption on the Internet: Evidence from clickstream data. Inf. Econ. Policy 2016, 34, 27–43. [Google Scholar] [CrossRef]

- Hylland, O.; Kleppe, B. Accountable countability. Digital cultural consumption among young people and the tools used to measure it. Cult. Trends 2023, 33, 341–357. [Google Scholar] [CrossRef]

- Beck, T.; Pamuk, H.; Ramrattan, R.; Uras, B. Payment instruments, finance and development. J. Dev. Econ. 2018, 133, 162–186. [Google Scholar] [CrossRef]

- Hu, D.; Zhai, C.; Zhao, S. Does digital finance promote household consumption upgrading? An analysis based on data from the China family panel studies. Econ. Model. 2023, 125, 106377. [Google Scholar] [CrossRef]

- Li, J.; Wu, Y.; Xiao, J. The impact of digital finance on household consumption: Evidence from China. Econ. Model. 2020, 86, 317–326. [Google Scholar] [CrossRef]

- Wang, J.; Yin, Z.; Jiang, J. The effect of the digital divide on household consumption in China. Int. Rev. Financ. Anal. 2023, 87, 102593. [Google Scholar] [CrossRef]

- He, Y.; Li, K.; Wang, Y.P. Crossing the digital divide: The impact of the digital economy on elderly individuals? Consumption upgrade in China. Technol. Soc. 2022, 71, 102141. [Google Scholar] [CrossRef]

- Bruhn, M.; Love, I. The Real Impact of Improved Access to Finance: Evidence from Mexico. J. Financ. 2014, 69, 1347–1376. [Google Scholar] [CrossRef]

- Manshad, M.; Brannon, D. Haptic-payment: Exploring vibration feedback as a means of reducing overspending in mobile payment. J. Bus. Res. 2021, 122, 88–96. [Google Scholar] [CrossRef]

- Song, Q.; Li, J.; Wu, Y.; Yin, Z. Accessibility of financial services and household consumption in China: Evidence from micro data. N. Am. Econ. Financ. 2020, 53, 101213. [Google Scholar] [CrossRef]

- Bayir, T. Hedonic and utilitarian consumption with compulsive buying relationship use of credit card: A research on online marketplace. J. Mehmet Akif Ersoy Univ. Econ. Adm. Sci. Fac. 2021, 8, 420–441. [Google Scholar] [CrossRef]

- Karlan, D.; Zinman, J. Expanding Credit Access: Using Randomized Supply Decisions to Estimate the Impacts. Rev. Financ. Stud. 2010, 23, 433–464. [Google Scholar] [CrossRef]

- Du, C.; Ouyang, Y.; Yang, Q.; Shi, Z. The impact of digital economy on household private insurance participation. Int. Rev. Econ. Financ. 2024, 95, 103456. [Google Scholar] [CrossRef]

- Hu, X.; Wang, Z.; Liu, J. The impact of digital finance on household insurance purchases: Evidence from micro data in China. Geneva Pap. Risk Insur.-Issues Pract. 2022, 47, 538–568. [Google Scholar] [CrossRef]

- Zhang, C.; Zhu, Y.; Zhang, L. Effect of digital inclusive finance on common prosperity and the underlying mechanisms. Int. Rev. Financ. Anal. 2024, 91, 102940. [Google Scholar] [CrossRef]

- Dupas, P.; Robinson, J. Why don’t the poor save more? Evidence from health savings experiments. Am. Econ. Rev. 2013, 103, 1138–1171. [Google Scholar] [CrossRef]

- Yang, W.; Vatsa, P.; Ma, W.; Zheng, H. Does mobile payment adoption really increase online shopping expenditure in China: A gender-differential analysis. Econ. Anal. Policy 2023, 77, 99–110. [Google Scholar] [CrossRef]

- Wang, X.; Liu, J. The influence mechanism of internet finance on residents’ online consumption. Financ. Res. Lett. 2024, 70, 106323. [Google Scholar] [CrossRef]

- Saleh, M.; Aqel, M. Blockchain implementation to manage banking mobile payments. J. Inf. Sci. Eng. 2021, 37, 1249–1258. [Google Scholar] [CrossRef]

- Arkes, H.; Joyner, C.; Pezzo, M.; Nash, J.; Siegel-Jacobs, K.; Stone, E. The psychology of windfall gains. Organ. Behav. Hum. Decis. Process. 1994, 59, 331–347. [Google Scholar] [CrossRef]

- Kivetz, R.; Zheng, Y. The effects of promotions on hedonic versus utilitarian purchases. J. Consum. Psychol. 2017, 27, 59–68. [Google Scholar] [CrossRef]

- Fujiki, H. The use of noncash payment methods for regular payments and the household demand for cash: Evidence from Japan. Jpn. Econ. Rev. 2020, 71, 719–765. [Google Scholar] [CrossRef]

- Yang, C.; Wang, X. Income and cultural consumption in China: A theoretical analysis and a regional empirical evidence. J. Econ. Behav. Organ. 2023, 216, 102–123. [Google Scholar] [CrossRef]

- Ma, H.; Yin, Y.; Liu, Z.; Bai, Y. A study of the impact of digital finance usage on household consumption upgrading: Based on financial asset allocation perspective. Int. Rev. Econ. Financ. 2024, 96, 103628. [Google Scholar] [CrossRef]

- Yang, B.; Ma, F.; Deng, W.; Pi, Y. Digital inclusive finance and rural household subsistence consumption in China. Econ. Anal. Policy 2022, 76, 627–642. [Google Scholar] [CrossRef]

- Guo, F.; Wang, J.; Wang, F.; Kong, T.; Zhang, X.; Cheng, Z. Measuring China’s digital financial inclusion: Index compilation and spatial characteristics. China Econ. Q. 2020, 19, 1401–1418. [Google Scholar]

- Gao, X.; Li, J. The nexus between internet use and consumption diversity of rural household. Heliyon 2024, 10, e35433. [Google Scholar] [CrossRef]

- Su, Z.; Cao, R. Impact of Digital Inclusive Finance on Urban Carbon Emission Intensity: From the Perspective of Green and Low-Carbon Travel and Clean Energy. Sustainability 2023, 15, 12623. [Google Scholar] [CrossRef]

- Dong, J.; Zang, X. Digital finance’s impact on household service consumption-the perspective of heterogeneous consumers. Appl. Econ. 2024, 56, 7014–7029. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).