Abstract

The automotive industry is evolving due to the increasing adoption of Electric Vehicles (EVs). This transition has impacted automotive vehicles and led to profound changes in the supply chain ecosystem. Through a comprehensive review of the available literature and industry reports, this research investigates the automotive industry’s transition towards EVs and subsequent supply chain transformation, focusing on the changing roles of automotive suppliers. In this paper, we assess these transformations from economic, environmental, and strategic viewpoints. We examine the impact of these changes on supplier relationships, supplier OEM collaboration, and new entrants’ potential for disruption, as well as propose strategies for suppliers to effectively navigate this transformation, ensuring competitiveness in the evolving EV landscape. Finally, we discuss opportunities and challenges in EV supply chain research.

1. Introduction

Any evolving supply chain produces changing perspectives, understanding, and management styles that provide new opportunities and challenges. As the automotive industry rapidly transitions from a market based on the internal combustion engine (ICE) to a market including a growing share of Electric Vehicles (EVs), its supply chain must adapt to ensure its members’ competitiveness and survival [1,2,3]. This study aims to address the lack of comprehensive research focusing specifically on changes in supplier relationships, supplier OEM collaboration, and new entrants’ potential for disruption to guide suppliers in identifying strategies for competitive advantage.

The automotive industry has long been a strong contributor to the economic health of many developed nations [4,5]. Unfortunately, those economic contributions have also contributed to negative environmental issues associated with its primary product, the automobile [6,7]. As a complex, manufactured product, the ICE automobile not only causes environmental issues from sourcing its raw materials but also results in life-use issues from emissions and end-of-life issues that contribute to substantial atmospheric, water, biodiversity, and land issues. Fossil fuels and products that use fossil fuels are the largest contributors to global climate change, representing more than 75% of greenhouse gas (GHG) emissions and approximately 90% of carbon dioxide (CO2) emissions [8,9].

To address this, world governments have begun to clearly address inter-connected environmental issues by providing the automotive industry clear economic guidance focused on reducing the negative impacts of their titular product, primarily through restrictions on petroleum-powered vehicles, while also enhancing the positive aspects, primarily through financial subsidies to support the market growth of EVs. For example, economic restrictions and subsidies are intended to drive EV market growth to more than 60% of vehicles sold by 2030 [10,11].

Recognizing these environmental challenges and opportunities and wishing to retain economic strength and competitiveness, the automotive industry has responded by leveraging technology to develop advanced products, such as EVs, that meet consumer needs while still adhering to environmental restrictions. Complementary to government-related economic drivers to the EV market, the industry also finds itself at the hands of other disruptive market drivers, such as geopolitical motivation for energy independence, pandemic-related supply chain network changes increasing near-shoring and re-shoring trends, and populist nationalist interests. The pandemic disrupted supply chains and brought domestic clarity regarding unwanted dependency on global relationships. In addition, the drop in emissions from COVID-19-shuttered industries allowed for temporary air quality improvements that provided a clear indicator of the full scope of industrial impact, strongly increasing public support for conversion to EVs from traditional vehicles [12,13]. This awakening led to a populist reaction and push for greater energy and supply chain independence, including increased interest in EVs.

While our research focuses on the complexities of the EV supply chain ecosystem, it is not our intention to portray ICE vehicles as solely disadvantageous nor to suggest that EVs possess only positive attributes. Instead, our study critically examines the structure of the EV supply chain, exploring why its advancement has not been as rapid or robust as anticipated [14,15], despite the industry’s gradual shift from ICE to EVs and the increasing global emphasis on sustainability and technological innovation.

This research is motivated by the compelling need to understand how the automotive supply chain adapts to these significant shifts. With EVs poised to dominate the automotive market, understanding the evolving roles of automotive suppliers is crucial [16,17]. Suppliers who have historically focused on components for ICE vehicles must now pivot to cater to the unique demands of EV production. This transition presents both challenges and opportunities, reshaping the industry’s landscape. Suppliers must navigate changes in material sourcing and component manufacturing, as well as collaborate effectively with Original Equipment Manufacturers (OEMs) in order to stay relevant. Therefore, this study provides a timely exploration of how automotive suppliers adapt to this paradigm shift.

Two important research questions guide this study: Firstly, how are supplier relationships and collaboration with OEMs evolving in the wake of the EV transition? Secondly, what is the potential impact of new entrants on the automotive supply chain, particularly in the context of EVs? Addressing these questions is vital to understanding the broader implications of the EV revolution for the automotive industry. This article aims to analyze the changing dynamics within the EV supply chain ecosystem. By doing so, it seeks to provide valuable insights for automotive suppliers, OEMs, policymakers, and other stakeholders in the industry, ensuring they are well-equipped to navigate and thrive in this rapidly evolving landscape. This article further aims to discuss opportunities and challenges for future EV supply chain research.

This paper is structured to provide a comprehensive examination of the evolving landscape of the EV supply chain. Section 2 begins with an exploration of the current EV supply chain ecosystem, setting the stage by establishing a baseline understanding of its intricacies and stakeholders. Section 3 builds upon this foundation, delineating the shifts required for traditional automotive suppliers to adapt and thrive in the emerging EV market. The paper then transitions into a comparative analysis in Section 4, where the nuances between ICE and EV supply chains are examined, highlighting the unique challenges and demands of the EV sector. Following this, Section 5 presents the transformative forces reshaping the industry, from technological innovations to strategic partnerships. In Section 6, the paper identifies gaps in current research, fostering a dialogue on future directions. Section 7 connects theoretical perspectives with practical implications. The paper concludes with Section 8, which summarizes the key insights of this paper and clarifies the paper’s contributions to the field. Each section is connected to explain the complexities of the EV supply chain’s ongoing evolution.

2. The EV Supply Chain Ecosystem

The EV Supply Chain Ecosystem is a complex and multifaceted network that plays a crucial role in the evolving landscape of the automotive industry [17,18]. It encompasses various processes and stakeholders, from raw material sourcing and battery manufacturing to vehicle assembly and end-of-life management. It is instrumental in driving innovation and sustainability in transportation, reflecting the global shift towards more eco-friendly and technologically advanced mobility solutions.

2.1. Scope of the EV Supply Chain Ecosystem

The ecosystem refers to the complex network of interconnected stakeholders producing, distributing, and maintaining EVs and encompasses the entire lifecycle of an EV, from raw material extraction to vehicle end-of-life management. Consisting of the complex and interconnected network of various stakeholders involved in the entire lifecycle of an EV, from the sourcing of raw materials to the final stages of vehicle use and servicing, the ecosystem is wide-reaching.

The sourcing of raw materials involves mining operations that extract essential elements like lithium and rare earth elements, which are critical for manufacturing EV components [19]. Processing plants and the transportation of these materials comprise the first stage of the supply chain [20,21]. The battery manufacturing and industrial factories include battery cells, modules, and packs that are assembled with a focus on the storage and management of electrical energy, which is central to the functioning of EVs. Vehicle design and manufacturing include engineering design spaces and vehicle assembly lines. It involves the integration of batteries, electric motors, and other vital components into the design and build of EVs. Parts and components suppliers represent a range of smaller facilities providing essential pieces, such as semiconductors, electrical systems, power electronics, and thermal management systems, showcasing the diversity of suppliers contributing to the EV manufacturing process [22]. Charging infrastructure with a series of charging station icons signifies the development, installation, and maintenance of the necessary infrastructure required for recharging EVs [23] Regarding software and connectivity, the EV ecosystem includes elements that suggest developing software solutions for vehicle operation [24,25]. This includes systems for battery management, driver assistance, and platforms that facilitate the integration of smart grids and the Internet of Things (IoT). Finally, dealership buildings and other sales platforms represent the sales and distribution network, indicating the channels through which EVs reach consumers and businesses. In sum, the EV supply chain ecosystem encompasses the complexity and breadth of all that supports the lifecycle of EVs.

2.2. Scale of the EV Supply Chain Ecosystem

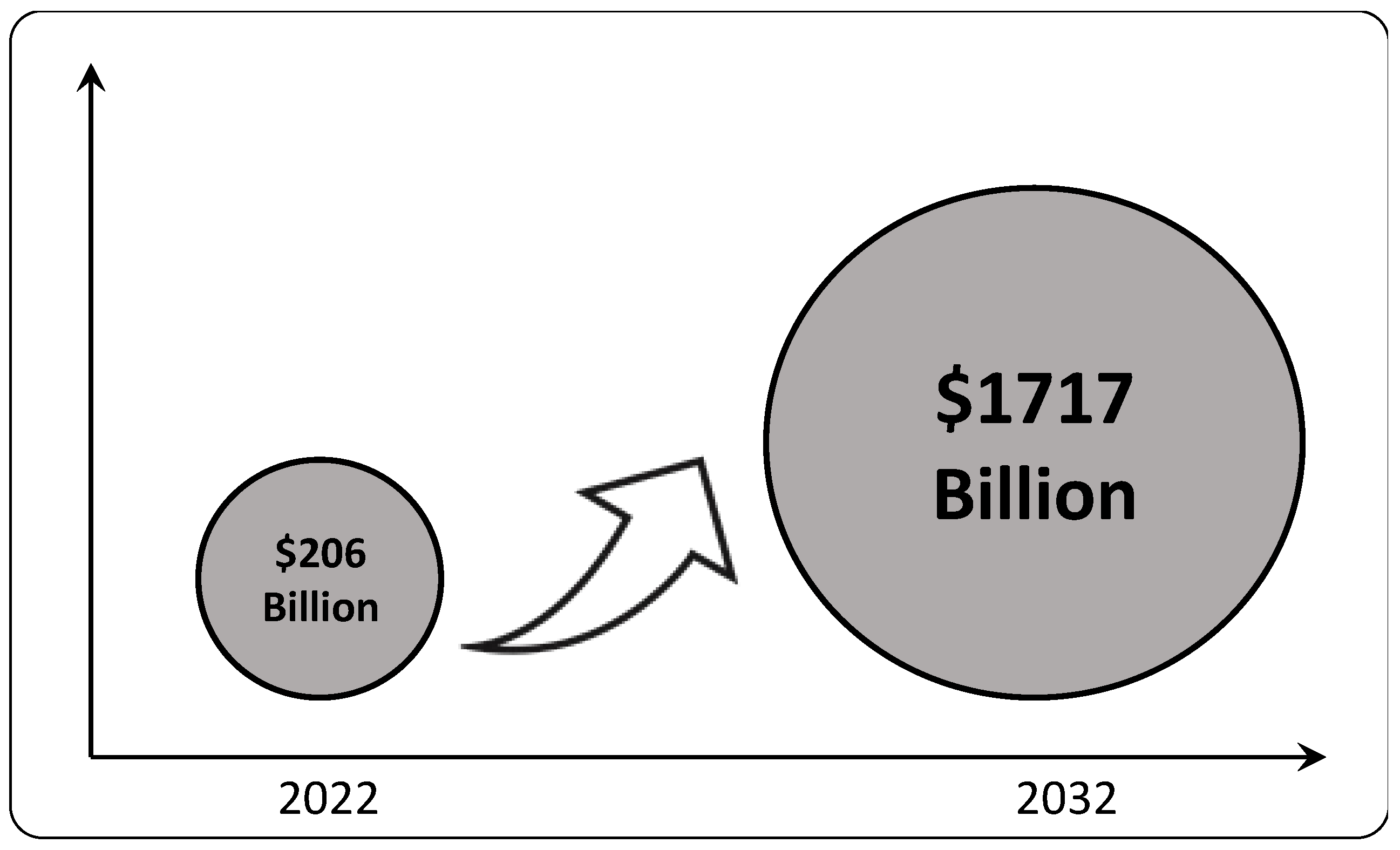

The global EV market size is a measure of the total sales and revenue generated from the sale of EVs across the world. It encompasses various segments, including battery EVs (BEVs), plug-in hybrid EVs (PHEVs), and hybrid EVs (HEVs) [26]. The market size is determined by factors such as the number of units sold, the average selling price of EVs, the total value of EV-related services, and the investment in EV infrastructure. Additionally, it considers the scale of operations of EV manufacturers, the size of the consumer base, government incentives and subsidies, advancements in EV technology, and the global push towards sustainability and reduction in carbon emissions. This market size is indicative of the adoption rate of EVs. It is a crucial indicator of the EV industry’s growth trajectory and its impact on the automotive market as a whole.

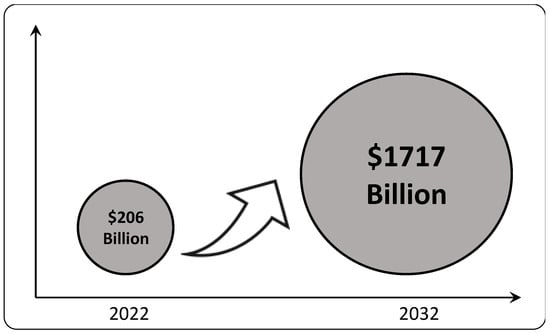

As of 2022, the global EV market is estimated to grow from USD 206 billion to USD 1717 billion by 2032, showcasing a compound annual growth rate (CAGR) of 21.26% (See Figure 1) [27]. This growth signifies an increasing shift towards sustainable transportation, supported by advancements in EV technology, expanding charging infrastructure, and favorable government policies to reduce carbon emissions. This market size strongly indicates the EV industry’s expanding role in the global automotive sector, reflecting growing consumer demand and the concerted push for cleaner energy solutions.

Figure 1.

Global EV Market Growth Projection—Source: Authors’ own work.

The scale of an EV Supply Chain Ecosystem can also be defined by the breadth and depth of its infrastructure and operations required to support the entire lifecycle of EVs [28]. It includes the capacity of raw material extraction and processing facilities that supply critical materials like lithium and cobalt; the extent and efficiency of battery manufacturing plants; the robustness of vehicle design and production capabilities; the breadth of the parts and components supplier network; the reach and accessibility of the charging infrastructure; the sophistication of software and connectivity solutions for vehicle operation and integration with energy grids; and the coverage of sales, service, and recycling networks [23]. Scale is also reflected in the ecosystem’s ability to adapt and grow with evolving market demands and technological advancements, ensuring a stable supply chain supporting a rising global fleet of EVs.

Three key measures that can be used to gauge the scale of an EV Supply Chain Ecosystem could include production capacity, raw material sourcing, and the charging and maintenance infrastructure.

Production Capacity: This measure would reflect the total number of EVs manufacturers can produce in a given timeframe. It encompasses the capacity of battery production, assembly lines for vehicle manufacturing, and the availability of essential components like electric motors and power electronics. This measure indicates the ecosystem’s ability to meet market demand. It is influenced by factors such as the size and number of manufacturing facilities, workforce availability, and the efficiency of manufacturing processes.

Raw Material Sourcing: The scale of raw material sourcing would be measured by the geographic spread and volume of raw materials, such as lithium, cobalt, and nickel, secured for battery production [20]. This could be assessed by the number and capacity of mining operations, the sustainability and diversity of supply sources, and the partnerships established with raw material providers. A broad and resilient sourcing network is crucial for stability in the supply chain, given that raw materials are the foundational inputs for EV manufacturing.

Charging and Maintenance Infrastructure: The scale and density of the charging infrastructure, including public charging stations and service centers, are key indicators of the scale of the EV supply chain ecosystem [23]. The number of charging points, their geographical coverage, and the availability of rapid charging options reflect the readiness of the ecosystem to support the growing EV fleet. Additionally, the capacity to provide maintenance and after-sales services, including the availability of spare parts and the network of service centers, is vital for sustaining the long-term operation of EVs on the road.

These measures would provide a quantitative assessment of the EV supply chain ecosystem’s ability to support EV production, distribution, and maintenance and facilitate their adoption at scale.

3. Transitioning to the EV Supply Chain Ecosystem

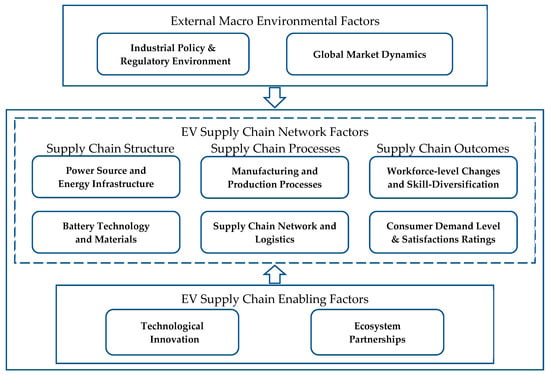

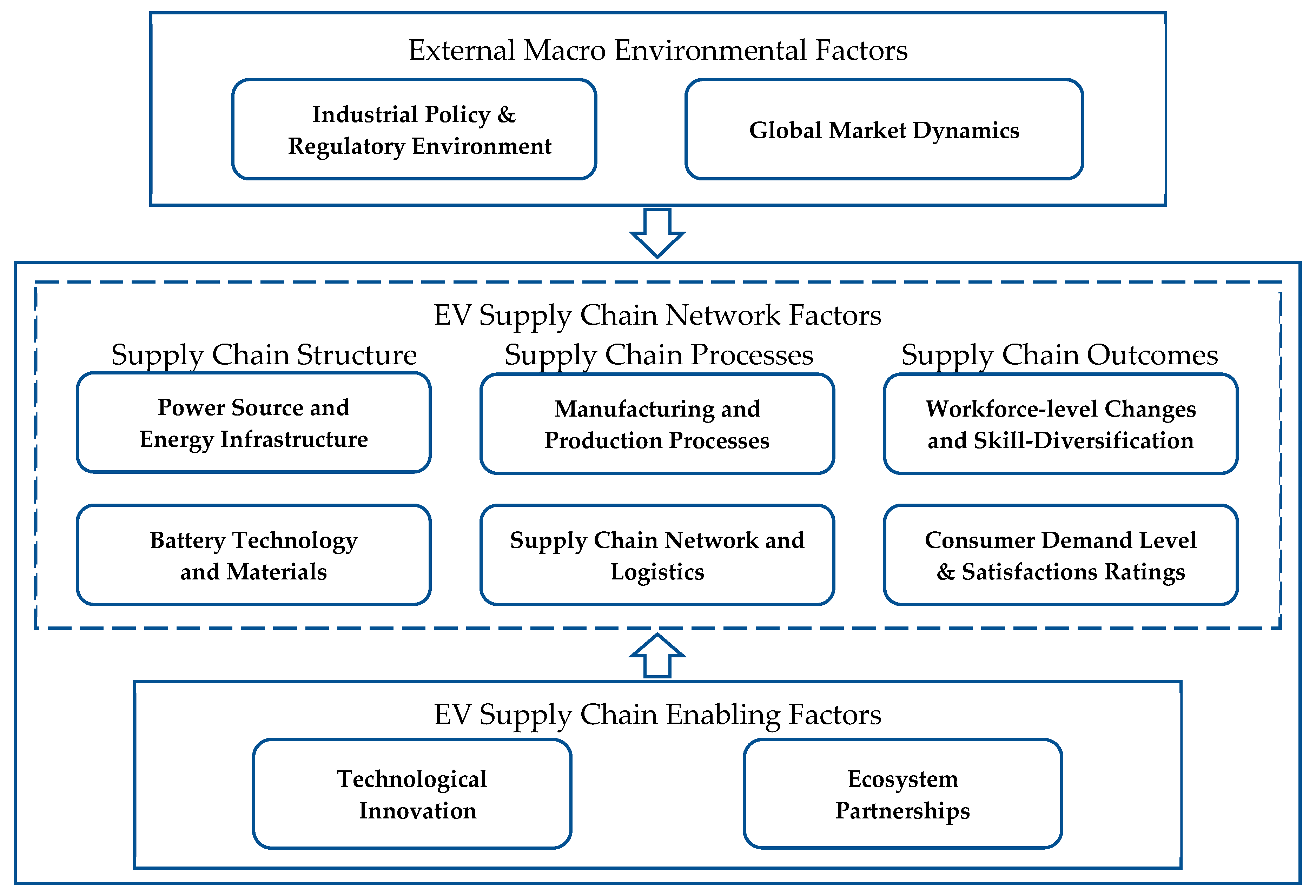

In examining the transition from a traditional ICE supply chain ecosystem to an EV supply chain ecosystem, key elements related to its ecosystem need to be examined closely. Figure 2 shows the scope of the EV supply chain network in terms of several factors. The external macro-environmental factor includes the variables of industrial policy initiatives (e.g., massive government support, regulatory requirements, climate control mandates) and global market dynamics (e.g., market demand patterns, geopolitical alliances, strategic trade negotiations, investments of global firms). The EV supply chain enabling factor includes the variables of technological innovation (e.g., battery technology advancement, digitalization, and artificial intelligence (AI) connectivity, renewable energy, and smart grids) and ecosystem partnerships (e.g., collaboration network between OEM and suppliers, public and private partnerships and cross-industry coordination, circular economy systems) [29].

Figure 2.

Scope of EV Supply Chain Ecosystem Network—Source: Authors’ own work.

Figure 2 also shows the key variables of the EV supply chain network factor (supply chain structure, supply chain process, and supply chain outcomes) and their respective elements, power source and energy infrastructure, battery technology, and materials. It also shows manufacturing and production processes; supply chain network, logistics and workforce-level changes; skills-diversification; consumer demand level; and satisfaction ratings.

In terms of the variable elements, the supply chain structure involves power sources and energy infrastructure [30]. One of the most fundamental changes in the transition to the EV supply chain ecosystem is the shift in power sources. Traditional fossil fuel supply chains rely on the extraction, refinement, and distribution of gasoline, diesel, and other fossil fuels. In contrast, the EV supply chain centers around electricity as the primary energy source. This necessitates the development of robust charging infrastructure, including charging stations at public places, workplaces, and homes, to support the widespread adoption of EVs. The supply chain structure also includes battery technology and materials. EVs are powered by advanced battery technologies, such as lithium-ion batteries, which differ significantly from internal combustion engines in traditional vehicles. The transition involves the development of more efficient and higher-capacity batteries, advancements in battery recycling and reuse, and research into alternative materials to reduce reliance on scarce resources and enhance sustainability [31].

Secondly, the supply chain processes include manufacturing and production processes, the supply chain network, and logistics. Shifting to the EV supply chain ecosystem requires manufacturing and production process alterations [16,18]. Traditional automakers and automotive suppliers need to reconfigure their production lines to accommodate the assembly of EVs and their components, such as electric motors and batteries. This includes investing in new machinery and technologies specific to EV production. The transition from ICE to EV affects the entire supply chain network and logistics. From raw materials to finished products, the supply chain has to adapt to accommodate the specific requirements of EV components [19,21]. Suppliers must establish efficient transportation routes for batteries and other EV parts, which might differ from traditional fossil fuel counterparts. Additionally, the recycling and disposal of batteries pose unique logistical challenges.

Thirdly, supply chain outcomes encompass workforce, skill diversification, consumer demand, and satisfaction ratings. As the automotive industry embraces electric mobility, there is a growing demand for skilled workers with expertise in EV-related technologies. Existing automotive suppliers may need to upskill their workforce or hire specialists in battery technology, electric drivetrains, software integration, and other areas specific to EVs [32,33]. Simultaneously, the workforce-level changes as new job opportunities emerge in the EV sector, attracting professionals with diverse skill sets to meet the changing demands of the industry. Complementing supply-side workforce changes, the demand side has also shown changes in consumer trends. Consumer demand level and satisfaction ratings reflect the sales volume and market share of EVs in the automotive industry and report the growth and acceptance level among consumers. Customer satisfaction ratings encompass various factors such as vehicle performance, driving range, charging infrastructure accessibility, battery life, maintenance costs, and overall ownership experience. A well-developed and widely distributed charging infrastructure network with high utilization rates indicates that the EV supply chain ecosystem supports consumer needs, promotes EV adoption, and enhances customer satisfaction [30].

These diverse factors of the EV supply chain ecosystem network—both external and internal—represent some of the key changes that occur during the transition from the traditional fossil fuel supply chain ecosystem to the EV supply chain ecosystem. Each of these changes presents challenges and opportunities for stakeholders in the automotive industry as they adapt to the evolving electric mobility landscape. Table 1 provides definitions and examples of the key factors, variables, and elements shown in Figure 2.

Table 1.

Factors Affecting EV Supply Chain Ecosystem.

4. Comparing ICE and EV Supply Chains

The supply chain of EVs has certain distinguishing factors due to its current status in the product life cycle. EVs have just passed the introduction phase and are growing rapidly [26,28,34]. Most ICE vehicle supply chain elements can adapt to support the EV supply chain, but around 25% of the EV supply chain will need to be rebuilt [35]. Some essential components of ICE vehicles, like fuel, transmission, exhaust, and cooling systems, do not exist in EVs. Therefore, some suppliers will need to explore diversifying into EV components sooner to survive.

4.1. Factors from the External Macro-Environment and Supply Chain Advancement

Based on the literature review [33,36,37,38,39,40,41], three crucial factors are identified for the potential advancement of the EV supply chain: the innovation impact scope, the risk of disruption and resilience, and market change responsiveness. These factors are useful in assessing the ecosystem’s robustness, avoiding the dilution of focus that can occur with a larger set of variables. Each has the potential to contribute to or detract from the growth of the EV supply chain ecosystem.

Innovation Impact Scope: The engine design of ICE vehicles is well-established. But there remain some areas for improvement, such as autonomous driving, reducing emissions, and improving fuel efficiency [33,39,41]. However, due to fundamental limitations of the technology and fuel it uses, there is a limit to how efficient or clean an ICE vehicle can be. While there is limited scope for innovation within the ICE vehicle supply chain, manufacturers like Toyota are investigating the possibility of converting existing vehicles to run on cleaner, alternative fuels. Although EVs have been around for a while, they have only been mass-produced in recent years, leaving ample opportunity for further developments and breakthroughs. Some areas with significant scope for innovation in EVs are battery and charging technology, recycling, and sustainability.

Risk of disruption and resilience: Although the supply chains for both ICE and EV vehicles face potential disruptions, the ICE supply chain is relatively resilient to disruption. The main raw materials used in the ICE supply chain are abundant, and the supply chain is well-established. For ICE vehicles, fluctuations in commodity prices, such as steel and petroleum, geopolitical instability in regions supplying these commodities, increasingly strict emissions regulations, and global crises like pandemics still make it vulnerable to disruptions. On the other hand, the EV supply chain risks disruption due to its relative recency and limited availability, geopolitical issues surrounding raw materials like lithium, cobalt, and nickel used in batteries, bottlenecks in battery production, rapid technological changes that may outpace current infrastructure, stringent regulations on battery production and disposal, and any interruptions to the development or operation of the charging infrastructure [38,39,40]. Both supply chains have their resilience strategies, but they are at different stages of maturity. ICE supply chains have the advantage of established networks and multiple suppliers, while the resilience of EV supply chains is still developing but is boosted by rapid technological innovation and growing collaborations.

Market change responsiveness: Market change responsiveness is crucial for EV suppliers to adapt to a fast-evolving automotive landscape. This ability allows them to swiftly respond to shifts in consumer preferences towards greener transport options, technological advancements like better battery life and faster charging, and regulation changes, such as emissions standards [36,37]. Responsiveness also contributes to supply chain resilience, helping suppliers adapt to unforeseen disruptions like trade tensions or global pandemics. Being agile gives suppliers a competitive advantage by allowing them to capture a more significant market share and forge stronger relationships with automakers. Moreover, quick adaptability helps suppliers manage costs effectively, letting them adjust to fluctuating raw material prices or adopt new, cost-saving technologies [42,43]. In essence, a high level of market change responsiveness is key for EV suppliers to remain competitive, align with regulatory shifts, and meet growing consumer demand.

4.2. Comparative Aspects of Automotive Supply Chains

Beyond these three crucial factors, supply chains can also be differentiated based on eight major aspects [25,29,33,38,40]. These aspects include innovation scope, market dynamics, raw materials, the role of suppliers, infrastructure, technology use, risk of disruption and resilience, and regulations. Each aspect plays a crucial role in shaping and distinguishing the EV supply chain from the supply chain of ICE vehicles.

Table 2 presents a side-by-side comparison between ICE vehicle and EV supply chains across various features, highlighting the differences and nuances. Starting with innovation scope, ICE supply chains are labeled as “Limited”, suggesting that possibilities for innovation within this mature technology are somewhat constrained. In contrast, the EV supply chain is marked as having a “Broad” scope for innovation, reflecting the nascent and rapidly developing nature of EV technology, which is ripe with opportunities for advancement, particularly in areas such as battery technology and charging solutions [25].

Table 2.

Comparison of ICE and EV supply chains.

Regarding market dynamics, the ICE supply chain is considered “Mature”, implying a well-established market with predictable patterns and slower growth. On the other hand, the EV supply chain is characterized as “Growing”, indicating a dynamic and expanding market as consumer demand increases and technology progresses [33]. The raw materials for ICE vehicles are traditional—steel, aluminum, and plastic—widely available, and have established supply chains. Conversely, EVs rely on lithium, cobalt, and nickel, which may have more complex sourcing requirements due to their relative scarcity and the geopolitical intricacies of where they are mined. The role of suppliers in the ICE supply chain is described as “Straightforward”, likely due to the long-standing relationships and clear-cut component requirements. However, for EVs, the role is “Complex”, which could be due to the need for new supplier relationships and the integration of advanced technology components [29]. Infrastructure for ICE is “Well-established”, reflecting a comprehensive network of fuel stations and repair shops. At the same time, EVs are “Not as well-established”, pointing to the ongoing development of EV charging stations and maintenance facilities.

Technology use in ICE is “Mature”, indicating that the technology has reached a plateau in development, while in EVs, it is “Still in development”, suggesting ongoing innovations in electric drivetrains and battery management systems [39]. The risk of disruption and resilience is an important aspect; ICE supply chains are considered “Resilient”, having withstood various market and geopolitical challenges over time, whereas EV supply chains are seen as “Vulnerable”, possibly due to their reliance on newer technologies and the less-established nature of their supply chains [38]. Lastly, regulations for ICE are “Established”, with clear guidelines and standards in place. At the same time, EVs are “Evolving,”, reflecting the rapid changes in policy and standards as governments and industries adapt to the new reality of electric mobility.

5. EV Supply Chain Ecosystem Transformation

The EV supply chain ecosystem can be characterized by its dynamic market and the evolving role of its suppliers [31,44,45].

The EV market is distinguished by its rapid growth and innovation-driven environment. It is influenced by factors such as technological advancements (especially in battery and charging infrastructure), shifts in consumer preferences towards sustainable transportation, government policies promoting EV adoption, and the global push towards reducing carbon emissions. This market is significant because it dictates the demand for EVs, which drives the need for new supply chain structures, influences investment in research and development, and determines the pace at which the industry must evolve to meet these demands.

Suppliers in the EV supply chain ecosystem are crucial as they must adapt to the technological requirements of EV production, which differ significantly from those of traditional ICE vehicles. Suppliers must manage new materials (like lithium and cobalt for batteries), deal with new manufacturing processes (for electric motors and battery packs), and adapt to changing OEM (Original Equipment Manufacturer) expectations. The importance of understanding suppliers stems from their critical role in the overall efficiency and sustainability of the supply chain. They influence the cost, quality, and availability of EVs and are central to innovation within the industry.

Understanding the broad automotive market is key to predicting the demand trends and the scale of the infrastructure required for the EV ecosystem. It helps stakeholders to anticipate changes and align their strategies with market growth. Understanding suppliers is equally important because they are the backbone of the supply chain, and their readiness and capability to shift from traditional automotive supply chains to those required for EVs are essential for the industry’s transformation. A robust network of suppliers that can adapt to technological changes ensures a resilient supply chain capable of sustaining the growth of the EV market.

5.1. A Typology of the EV Market

The EV market refers to the automotive industry segment specializing in producing, selling, and developing electric-powered vehicles. This market has emerged as a critical area of growth due to increasing environmental concerns, technological advancements, and changes in consumer preferences [25,30,33,46]. Market characteristics that determine the nature of different EV markets may include:

- ▪

- Consumer Demand: Varies based on environmental awareness, economic factors, and government incentives. High demand often correlates with higher sales and more rapid market growth.

- ▪

- Government Policies: Strong incentives, such as subsidies, tax breaks, and emissions regulations, can accelerate the adoption of EVs [11]. Conversely, a lack of support can stifle market growth.

- ▪

- Charging Infrastructure: The availability of charging stations is crucial. Well-established networks encourage EV adoption, whereas poor infrastructure can be a barrier.

- ▪

- Technological Advancements: Breakthroughs in battery technology, such as increased energy density or faster charging capabilities, can make EVs more attractive to consumers.

- ▪

- Economic Factors: The cost of ownership, which includes the purchase price, maintenance, and operating costs, influences market characteristics. As battery costs decrease, EVs become more competitive with ICE vehicles.

- ▪

- Energy Prices: Fluctuations in the price of electricity versus fossil fuels can make EVs more or less appealing to consumers.

- ▪

- Cultural and Social Factors: Social norms and values, such as environmental consciousness, can drive market growth [47].

Technological availability and the impact factors that may determine different EV markets include:

- ▪

- Battery Technology: The state of battery technology, including energy capacity, longevity, and charge times, is a primary driver of EV functionality and, therefore, market viability [48,49].

- ▪

- Power Electronics: Advances in power electronics, which control the flow of electricity within the vehicle, can improve efficiency and performance.

- ▪

- Electric Motor Technology: The efficiency and power of electric motors influence vehicle performance, impacting consumer adoption rates [22].

- ▪

- Software and Connectivity: Integration of EVs with smart grids and the Internet of Things (IoT) for better energy management and user experience [25].

- ▪

- Materials Science: Developing lightweight materials and rare-earth elements for motors can impact vehicle efficiency and production costs [20].

- ▪

- Recycling and Sustainability: Technologies for recycling batteries and sustainable sourcing of materials can affect EVs’ long-term viability and environmental impact [50].

The interaction between these market characteristics and technological availability shapes the contours of the EV market [26,29,33,51]. For instance, markets with high technological innovation but limited charging infrastructure might focus on hybrid models or advanced battery technology that offers longer ranges. Conversely, markets with less-advanced technology but robust infrastructure may prioritize accessibility and integration with existing power grids [52]. Each market will thus have a unique profile based on how these and other factors intersect.

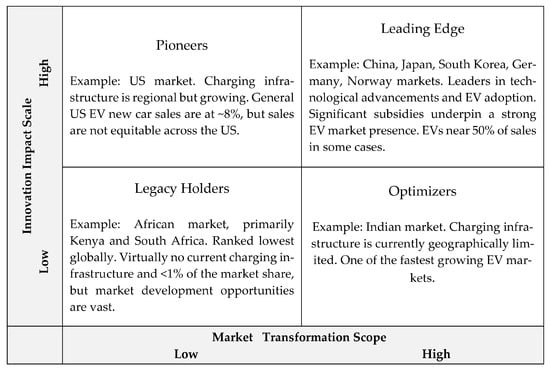

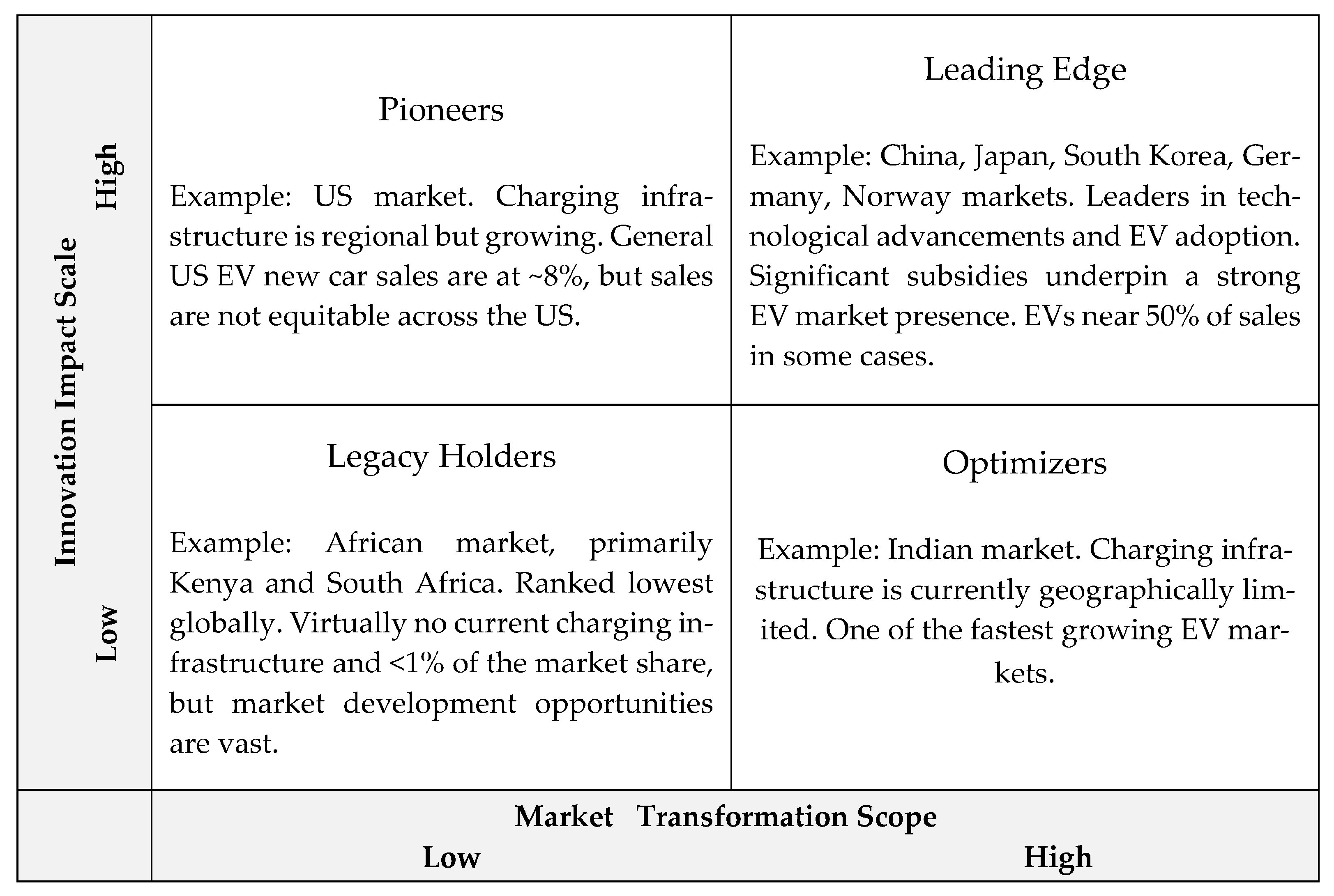

Figure 3 presents a matrix that categorizes different EV markets based on two dimensions: the Innovation Impact Scale and the Market Transformation Scope. The horizontal axis, denoting the Market Transformation Scope, measures the extent to which the EV market influences or changes the broader automotive market, ranging from low (little change from traditional markets) to high (significant market evolution due to the adoption of EVs). The vertical axis represents the Innovation Impact Scale, which gauges the impact of innovations in the EV market on the local or regional economies and industries. This scale moves from low (innovations have little impact on the market) to high (innovations significantly reshape the market). The quadrants define four types of EV markets.

Figure 3.

EV Market Typology—Source: Authors’ own work.

Legacy Holder markets are characterized by a low Market Transformation Scale and low Innovation Impact Scope. These suppliers are focused on mature, traditional technologies and often find themselves in stagnant or declining markets. Their challenge lies in adapting to a rapidly evolving landscape or finding niche areas where their expertise is still valuable. They may face significant barriers to entry in the emerging EV market due to established competition and the fast pace of technological innovation. These entities must either pivot their business models to embrace new technologies or continue to serve a diminishing market segment where their current offerings remain relevant.

Pioneer markets have a low Market Transformation Scale but a high Innovation Impact Scope. They are innovators in slow-moving markets, laying the groundwork for when market dynamics inevitably shift towards EVs. Pioneers such as the Midwest US EV market suggest high innovation impact but low transformation scope. These markets are early adopters or innovators in EV technology, but the overall market shift toward EVs is still in the nascent stages. Markets identified as “Pioneers” are expected to play a critical role in regional EV adoption despite not being at the forefront of innovation. Further research is needed to understand the strategies employed by these markets to stimulate early adoption and to assess how these strategies can influence larger-scale market transformations.

Leading Edge markets have a high Innovation Impact Scope and a high Market Transformation Scope. They represent leaders in the EV field, contributing technological innovations, political and societal support, and a proven ability to support and implement broad market changes that drive continued growth.

Optimizer markets have a low Innovation Impact Scope but a high Market Transformation Scope. In this category, technological innovation is not driving forward progress. Still, macro efforts, such as political and societal support and financial subsidies, are being leveraged to drive market growth aggressively, almost as if to leapfrog over any technological limitations.

5.2. A Typology of EV Automotive Suppliers

Automotive suppliers represent a vast and diverse segment of the global manufacturing sector, varying in size from small, specialized firms to massive conglomerates that produce various components and materials for vehicle manufacturers. These suppliers are integral to the automotive industry, providing everything from minor fasteners to complex electronic systems, basic raw materials, and advanced drivetrains. Their operations span multiple continents, often embedded within intricate networks of sub-suppliers, each contributing to the final assembly of vehicles. The diversity is not just in size and product range but also in their operational strategies, technological capabilities, and market presence.

The key characteristics of the Market Change Scope typically include [53,54]:

- ▪

- Adaptability: The ability to respond to new market demands, technology shifts, and evolving consumer preferences.

- ▪

- Innovation: Developing new products, services, or processes that meet emerging market trends.

- ▪

- Agility: Quickly adjusting business strategies and operations to capitalize on market opportunities.

- ▪

- Diversification: Offering a range of products or services that cater to various market segments to mitigate the risk associated with market volatility.

- ▪

- Disruption Risk Scale factors include [55,56]:

- ▪

- Dependency on Specific Technologies or Materials: Relying heavily on certain inputs that could be subject to shortages or price volatility.

- ▪

- Regulatory Compliance: The capacity to meet changing regulatory requirements without significant difficulty or delay.

- ▪

- Operational Robustness: The overall stability of operational processes to handle disruptions without major losses.

- ▪

- Financial Stability: Sufficient capital reserves or access to credit to survive periods of disruption without catastrophic consequences.

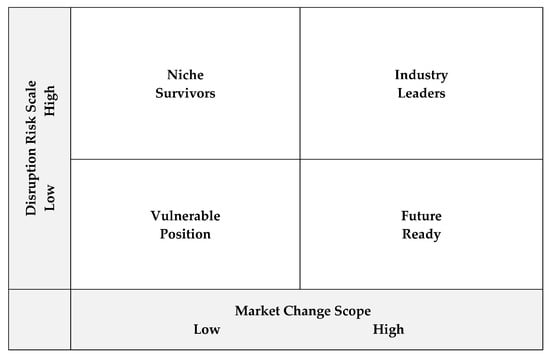

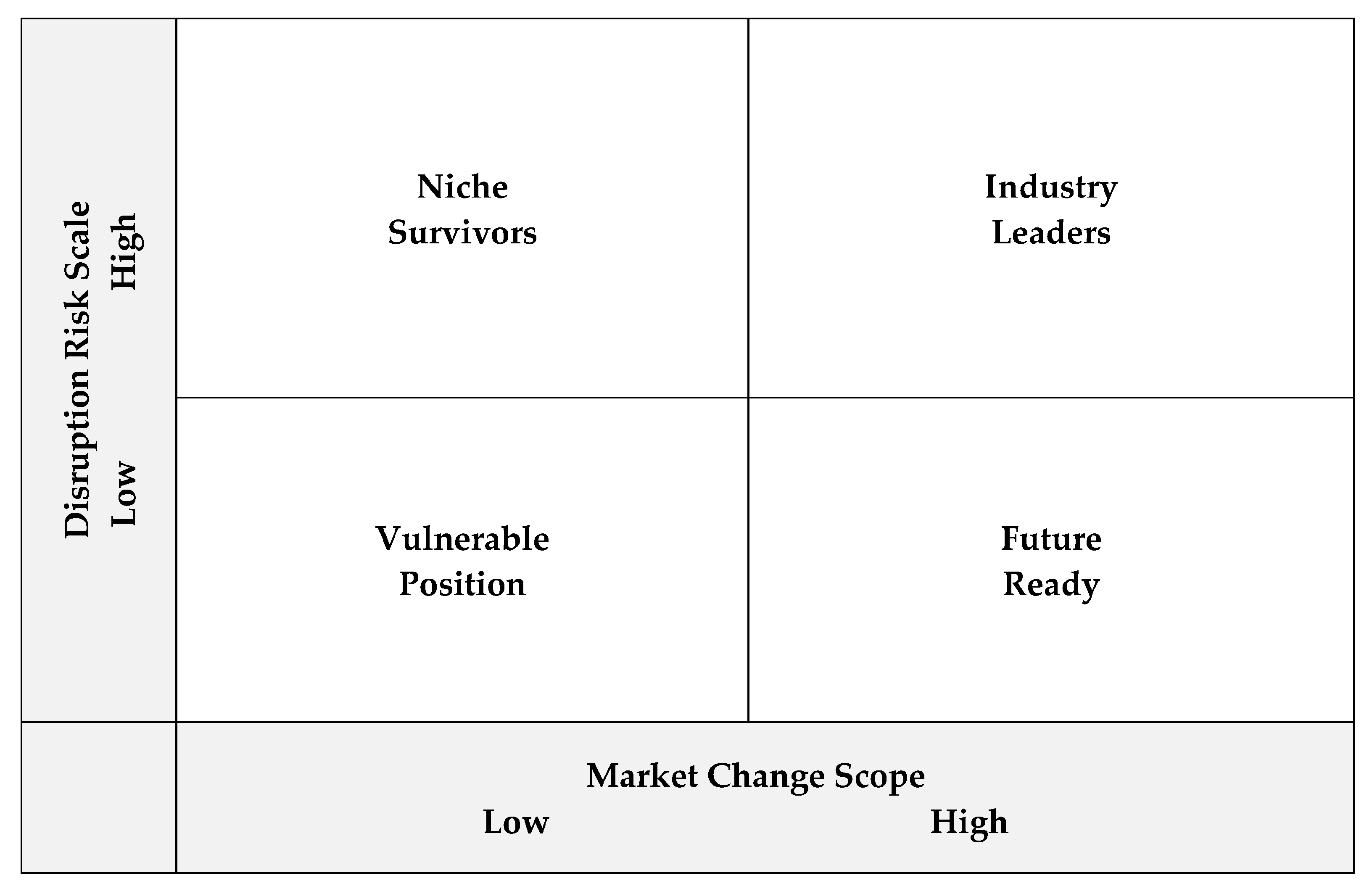

The scope for change in the market and the scale of disruption risk are essential for suppliers to understand their positioning and develop strategies to enhance their competitiveness and sustainability in the automotive industry. Suppliers must balance their innovation and adaptability with robust risk management to maintain or improve their position in the market. The automotive supplier typology presented in Figure 4 delineates four distinct categories based on their Disruption Risk Scale and Market Change Scope, shedding light on their competitive stance and adaptability in the industry.

Figure 4.

Automotive Supplier Typology—Source: Authors’ own work.

Vulnerable Position suppliers are in a precarious position with low disruption risk resilience and low market change responsiveness. Their primary strength lies in existing processes and traditional technologies, which are increasingly overshadowed by the industry’s shift towards innovation. The imminent risk for these suppliers is the potential to become obsolete in a rapidly evolving market. They must invest in innovation and adapt to digital transformations to enhance their competitiveness. Furthermore, it is imperative that they reimagine their business models to align with current technological and consumer trends.

Future Ready suppliers are characterized by their agility and capacity to swiftly adapt to market trends, a strength that positions them advantageously to capitalize on new opportunities. However, their resilience to unexpected disruptions is not as robust. For these suppliers to maintain their competitive advantage, they must establish strong risk management practices and invest in sustainable operations. Their ability to stay nimble while building a resilient framework will be crucial for their long-term sustainability and success in the industry.

Niche Survivors stand out for their high disruption risk resilience, anchored in their specialized offerings and loyal customer base within particular market niches. The challenge for these suppliers is their lower responsiveness to broader market changes, which could limit their growth potential. To secure their future and expand their market reach, they should consider strategic diversification and pursue incremental innovation that can open doors to new market segments without compromising their niche authority.

Industry Leaders positioned at the forefront of the industry demonstrate exceptional disruption risk resilience coupled with a proactive approach to market changes. They are the trendsetters, often steering the market direction with innovative solutions. To preserve their status as benchmarks in the industry, these leaders must continue to invest actively in research and development. Cultivating a culture that responds to but anticipates market movements and consumer demands will ensure they stay ahead of the curve.

Overall, this typology underscores the importance of adaptability and foresight in an industry prone to rapid changes and technological disruptions. Each category of suppliers has a unique set of strategies to deploy, ensuring they remain relevant and competitive in the dynamic automotive landscape.

6. Emerging Research Issues: Challenges and Opportunities

The EV supply chain ecosystem represents the comprehensive process that brings an EV from the drawing board to the driveway [57]. This intricate network includes extracting and sourcing essential raw materials, fabricating specialized components such as batteries and electric motors, assembling the vehicles, and distributing them to the consumer market. Beyond the manufacturing aspect, the EV supply chain also interweaves market dynamics, the development of supportive infrastructure, technological strides, and the regulatory environment, which can either accelerate or impede the proliferation of EVs. This complexity is compounded by the need for cross-sector collaboration and the transformation of traditional automotive supply chains to adapt to this emerging model. It supports a growing body of research on managing the evolving EV supply chain ecosystem [58].

6.1. Challenges for Research in EV Supply Chain Ecosystem

Research within the EV supply chain ecosystem is fraught with challenges due to its inherent uncertainties, dynamic complexities, and the need for multi-level analyses. The fast-paced evolution of EV-specific technologies, such as battery systems and electric drivetrains, combined with volatile raw material costs and shifting geopolitical influences, creates unpredictable supply and demand dynamics [31]. The dynamic nature of infrastructure development, regulatory environments, and consumer behaviors further complicates the research agenda. Additionally, the requirement to conduct nuanced analyses across various domains—from the macroscopic view of global trade to the microscopic scrutiny of consumer preferences—necessitates a cross-disciplinary approach that integrates diverse data sets and theoretical perspectives [57]. These challenges demand a versatile and robust research methodology capable of adapting to the rapid changes characteristic of the EV industry.

First, there is a high degree of uncertainty. A primary challenge in conducting research on the EV supply chain ecosystem stems from the high degree of uncertainty involved. This uncertainty is multifaceted, including rapidly evolving technology in battery and electric drivetrain systems, fluctuating raw material costs, and changing geopolitical landscapes that can affect supply chain stability [38]. For instance, the scarcity of critical minerals required for battery production, like lithium and cobalt, introduces economic and ethical considerations that can alter the supply dynamics overnight [59]. Additionally, the uncertainty in consumer adoption rates due to concerns over costs, safety, and the environmental impact of EVs further complicates demand forecasting, making it difficult for researchers to accurately predict industry trends and their ramifications.

Second, the dynamic complexity of the EV supply chain ecosystem is unsettling. The dynamic nature of the research targets within the EV supply chain ecosystem presents the second challenge. The targets constantly shift from technological innovations and infrastructure developments to regulatory policies and market behaviors. New advancements in battery technology, such as solid-state batteries, can dramatically change the research landscape by rendering current battery production and recycling models obsolete [59,60]. Infrastructure development, especially the deployment of charging stations, varies widely across different regions and evolves in response to both policy initiatives and market demand [61,62]. Additionally, the EV market is influenced by many stakeholders, including governments setting emissions standards, consumers with shifting preferences, and automakers responding to these changes, each introducing a layer of complexity to the research [63].

Third, methodological innovation is required. The requirement for multiple levels of analysis is a significant hurdle. EV supply chain ecosystem research must be conducted at the macro level, considering global supply chains and international trade policies, and at the micro level, examining individual consumer behaviors and local infrastructure developments [64]. It also demands a cross-disciplinary approach encompassing economics, engineering, environmental science, and policy analyses. This multifaceted approach requires synthesizing data and perspectives from various sources and disciplines, demanding significant time and resources to ensure comprehensive and accurate findings [65]. The interplay between these levels means that changes in one area, such as a policy shift at the national level, can have cascading effects down to the consumer level, which researchers must anticipate and account for in their studies.

6.2. Opportunities for Research in the EV Supply Chain Ecosystem

Research into the EV supply chain is both timely and critical as the automotive industry stands on the cusp of a paradigm shift from fossil fuels to electrification [66]. This transition is rife with uncertainties that impact consumer adoption and industry conversion. For consumers, the cost implications, safety considerations of new battery technologies, and the environmental ramifications of EV production and charging infrastructures are pivotal factors influencing their decision to switch to EVs. Substantial investment in new technologies, transforming existing production lines, and establishing a comprehensive charging infrastructure represent significant challenges for manufacturers and suppliers. Moreover, the synchronization of market demand with these advancements is uncertain, making research imperative to navigate and optimize the transition to a sustainable and efficient EV supply chain.

The first research opportunity examines EVs as a growing wave for the future of transportation, revealing a promising shift towards more sustainable, efficient, and innovative mobility solutions. This “wave” is driven by the urgent global need to reduce GHGs and combat climate change, alongside the technological advancements taking place that are making EVs more accessible and appealing. While the exact timing and scope of the transition remains opaque, the trajectory is clear as governments implement stringent emissions regulations, consumers grow more environmentally conscious, and automakers invest heavily in electric mobility. Research in this domain can provide valuable insights into the parameters and nuances of this transition, identifying catalysts and barriers and shaping the development of a robust EV supply chain that aligns with future market realities.

A second research opportunity exists in developing the utilization of research typologies. The two typologies presented in this paper—categorizing automotive suppliers based on disruption risk and responsiveness and classifying market responses to EV transformation—offer practical frameworks for dissecting the EV supply chain ecosystem. They allow researchers to segment and analyze the ecosystem in a structured manner, identifying which market segments are primed for innovation and which are resistant to change. These typologies can guide strategic decision-making for stakeholders and pinpoint where supportive policies or interventions could be most effective [61]. Research utilizing these frameworks can yield pragmatic strategies for fostering EV adoption, enabling a smoother industry transition, and developing resilience in the EV supply chain.

The third research opportunity involves assessing and describing the evolution of the supply chain discipline. Over the previous decades, the supply chain management discipline has matured, with methodological rigor and robust theoretical foundations now well-established. This evolution positions the field exceptionally well to engage with the complexities of the EV supply chain ecosystem. Methodologies can be refined and adapted to the unique challenges of EVs, such as integrating renewable energy sources into supply chain operations or developing circular economy models for battery recycling [67]. Theoretical frameworks honed through research on conventional automotive supply chains can now be applied and extended to understand and innovate within the EV context [68]. Consequently, research in this space can potentially drive the supply chain discipline forward and contribute significantly to the broader transition toward sustainable energy and transportation systems.

7. Discussion

This section connects theoretical perspectives with practical implications, highlighting three key points: the gap between the ecosystem’s evolution and market acceptance, the distinctive challenges in transitioning supply chains from ICE to EV, and the transformative impact of AI on the EV supply chain ecosystem. Through this discussion, we critically evaluate the industry’s progression against market demand, technological innovation, and AI integration, offering a holistic understanding of the factors driving change within the EV supply chain.

First, the transformation of the EV supply chain ecosystem involves a comprehensive evolution of the EV industry’s supply chain, which is guided by changes in market demand patterns. Despite significant transformation efforts, market responses have not trended towards broader acceptance of EVs as anticipated. Contrary to early optimistic projections, persistent low levels of EV customer demand have led even the most enthusiastic proponents to scale down their investments in the ecosystem [14,15]. This cautious approach reflects the reality that customer adoption rates and market penetration are pivotal determinants of the ecosystem’s ultimate scale and scope. This dynamic suggests that the transformation of the EV supply chain is influenced not only by technological advancements and regulatory frameworks but also by consumer acceptance and demand patterns. This scenario highlights the need for a multifaceted strategy in EV supply chain transformation, incorporating market education, incentives, and enhanced consumer experience to bridge the gap between supply chain capabilities and market uptake.

Second, this research diverges from previous studies [19,49,50,60] by presenting a comprehensive conceptual framework that delineates the distinct nature of the EV supply chain from that of ICE vehicles, focusing on the unique composition of suppliers and specific innovations required for a robust EV ecosystem. Our study counters the anecdotal evidence often found in EV supply chain research that isolates specific components without considering the broader ecosystem. It also challenges the notion that the scope and scale of EV supply chain transformation can be predicted by speculative projections of EV demand. Instead, we posit that real transformation depends on shifts in market demand patterns, offering a nuanced understanding of how these dynamics directly influence the evolution of the EV supply chain. Our dual focus provides new insights into the complexities of transitioning towards electric mobility, emphasizing the critical interplay between supply chain configuration, innovation requirements, and market demand.

Third, the changing roles of AI in the EV supply chain ecosystem are distinguished from those in the ICE vehicle supply chain due to the unique complexities and technological demands of EV manufacturing, such as precision in producing and integrating advanced electric motors, which require more sophisticated optimization and predictive analytics [69]. The emphasis on sustainability within the EV sector leads AI to focus on enhancing efficiency across the supply chain and reducing the environmental footprint, in line with the overarching goals of electric mobility [70].

AI profoundly transforms the EV Supply Chain Ecosystem through the optimization of production, enhanced management and development of energy storage, and logistics optimization. By employing AI algorithms, the EV manufacturing process achieves unparalleled efficiency and reduced downtime, ensuring intricate components like energy storage units and electric motors meet the surging demand without compromise [71]. Furthermore, AI’s role in the development of energy storage propels advancements that extend vehicle range and longevity, making EVs more affordable and attractive to consumers. On the logistics front, AI’s predictive capabilities streamline the supply chain, from material transport to demand forecasting, aligning operations with sustainability goals and ensuring the production pace matches market needs. These AI-driven improvements strengthen the EV supply chain from the initial fabrication of components to final delivery, enhancing vehicle performance, reducing environmental impact, and fostering wider consumer adoption.

8. Conclusions

This paper provides a crucial exploration of the EV supply chain ecosystem, addressing the automotive industry’s significant pivot towards electric mobility. It examines the comprehensive changes affecting the supply chain, from the redefinition of supplier roles to the emergence of new partnerships and the potential disruptions caused by new market entrants. Our analysis highlights the economic, environmental, and strategic dimensions of this transition and presents actionable insights for suppliers and OEMs to adapt to this new era.

Key takeaways from this research emphasize the urgent need for sustainable practices within the EV supply chain, including sustainable sourcing and the adoption of circular economy principles. The paper offers strategic guidance for stakeholders to enhance their competitiveness and resilience in the face of these industry-wide changes. By identifying the main challenges and opportunities within the EV supply chain, this work enriches academic discussions and serves as a valuable guide for industry professionals navigating the complexities of this transformative period in the automotive sector.

Author Contributions

Conceptualization, S.J., E.M. and P.H.; Methodology, S.J., E.M. and P.H.; Resources, S.J., E.M. and P.H.; Writing—original draft, S.J., E.M. and P.H.; Writing—review & editing, S.J., E.M. and P.H.; Project administration, S.J. and P.H. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this study are openly available at the listed references.

Conflicts of Interest

The authors declare no conflict of interest..

References

- Chaudhuri, A.; Boer, H.; Taran, Y. Supply Chain Integration, Risk Management and Manufacturing Flexibility. Int. J. Oper. Prod. Manag. 2018, 38, 690–712. [Google Scholar] [CrossRef]

- Gunasekaran, A.; Lai, K.h.; Edwin Cheng, T.C. Responsive Supply Chain: A Competitive Strategy in a Networked Economy. Omega 2008, 36, 549–564. [Google Scholar] [CrossRef]

- Fawcett, S.E.; Fawcett, A.M.; Watson, B.J.; Magnan, G.M. Peeking inside the black box: Toward an understanding of supply chain collaboration dynamics. J. Supply Chain. Manag. 2012, 48, 44–72. [Google Scholar] [CrossRef]

- Schroeder, P.; Anggraeni, K.; Weber, U. The Relevance of Circular Economy Practices to the Sustainable Development Goals. J. Ind. Ecol. 2019, 23, 77–95. [Google Scholar] [CrossRef]

- Nieuwenhuis, P.; Wells, P.E. The Global Automotive Industry, 2015th ed.; John Wiley & Sons: West Sussex, UK, 2015; ISBN 9781118802359. [Google Scholar]

- Nunes, B.; Bennett, D. Green Operations Initiatives in the Automotive Industry: An Environmental Reports Analysis and Benchmarking Study. Benchmarking 2010, 17, 396–420. [Google Scholar] [CrossRef]

- Gohoungodji, P.; N’Dri, A.B.; Latulippe, J.M.; Matos, A.L.B. What Is Stopping the Automotive Industry from Going Green? A Systematic Review of Barriers to Green Innovation in the Automotive Industry. J. Clean. Prod. 2020, 277, 123524. [Google Scholar] [CrossRef]

- Vieira, L.C.; Longo, M.; Mura, M. From Carbon Dependence to Renewables: The European Oil Majors’ Strategies to Face Climate Change. Bus. Strategy Environ. 2023, 32, 1248–1259. [Google Scholar] [CrossRef]

- Osman, A.I.; Chen, L.; Yang, M.; Msigwa, G.; Farghali, M.; Fawzy, S.; Rooney, D.W.; Yap, P.S. Cost, Environmental Impact, and Resilience of Renewable Energy under a Changing Climate: A Review. Environ. Chem. Lett. 2023, 21, 741–764. [Google Scholar] [CrossRef]

- IEA. World Energy Outlook 2022—Analysis; IEA: Paris, France, 2022. [Google Scholar]

- IRA. Inflation Reduction Act of 2022. Department of Energy, IRA; 2022. Available online: https://www.energy.gov/gdo/inflation-reduction-act (accessed on 30 December 2023).

- Tibrewal, K.; Venkataraman, C. COVID-19 Lockdown Closures of Emissions Sources in India: Lessons for Air Quality and Climate Policy. J. Environ. Manag. 2022, 302, 114079. [Google Scholar] [CrossRef] [PubMed]

- Nguyen, X.P.; Hoang, A.T.; Ölçer, A.I.; Huynh, T.T. Record Decline in Global CO2 Emissions Prompted by COVID-19 Pandemic and Its Implications on Future Climate Change Policies. Energy Sources Part. A Recovery Util. Environ. Eff. 2021, 1–4. [Google Scholar] [CrossRef]

- Carey, N.; White, J. Industry Pain Abounds as Electric Car Demand Hits Slowdown; Reuters: 2024. Available online: https://www.reuters.com/business/autos-transportation/industry-pain-abounds-electric-car-demand-hits-slowdown-2024-01-30/ (accessed on 30 December 2023).

- Whalen, J. EV Transition Cools as Demand Slows and Automakers Trim Production. The Washington Post. 2023. Available online: https://www.washingtonpost.com/business/2023/12/26/ev-demand-slows/ (accessed on 30 December 2023).

- Anderson, E.G.; Bhargava, H.K.; Boehm, J.; Parker, G. Electric Vehicles Are a Platform Business: What Firms Need to Know. Calif. Manag. Rev. 2022, 64, 135–154. [Google Scholar] [CrossRef]

- Gupta, R.; Mejia, C.; Gianchandani, Y.; Kajikawa, Y. Analysis on Formation of Emerging Business Ecosystems from Deals Activities of Global Electric Vehicles Hub Firms. Energy Policy 2020, 145, 111532. [Google Scholar] [CrossRef]

- Bhatti, G.; Mohan, H.; Raja Singh, R. Towards the Future of Smart Electric Vehicles: Digital Twin Technology. Renew. Sustain. Energy Rev. 2021, 141, 110801. [Google Scholar] [CrossRef]

- Kosai, S.; Takata, U.; Yamasue, E. Natural Resource Use of a Traction Lithium-Ion Battery Production Based on Land Disturbances through Mining Activities. J. Clean. Prod. 2021, 280, 124871. [Google Scholar] [CrossRef]

- Dunn, J.; Slattery, M.; Kendall, A.; Ambrose, H.; Shen, S. Circularity of Lithium-Ion Battery Materials in Electric Vehicles. Environ. Sci. Technol. 2021, 55, 5189–5198. [Google Scholar] [CrossRef] [PubMed]

- Baars, J.; Domenech, T.; Bleischwitz, R.; Melin, H.E.; Heidrich, O. Circular Economy Strategies for Electric Vehicle Batteries Reduce Reliance on Raw Materials. Nat. Sustain. 2020, 4, 71–79. [Google Scholar] [CrossRef]

- Husain, I.; Ozpineci, B.; Islam, M.S.; Gurpinar, E.; Su, G.J.; Yu, W.; Chowdhury, S.; Xue, L.; Rahman, D.; Sahu, R. Electric Drive Technology Trends, Challenges, and Opportunities for Future Electric Vehicles. Proc. IEEE 2021, 109, 1039–1059. [Google Scholar] [CrossRef]

- Perera, P.; Hewage, K.; Sadiq, R. Electric Vehicle Recharging Infrastructure Planning and Management in Urban Communities. J. Clean. Prod. 2020, 250, 119559. [Google Scholar] [CrossRef]

- Vdovic, H.; Babic, J.; Podobnik, V. Automotive Software in Connected and Autonomous Electric Vehicles: A Review. IEEE Access 2019, 7, 166365–166379. [Google Scholar] [CrossRef]

- Sun, X.; Li, Z.; Wang, X.; Li, C. Technology Development of Electric Vehicles: A Review. Energies 2019, 13, 90. [Google Scholar] [CrossRef]

- Rapson, D.S.; Muehlegger, E. The Economics of Electric Vehicles. Rev. Environ. Econ. Policy 2023, 17, 274–294. [Google Scholar] [CrossRef]

- Electric Vehicle Market Size to Hit USD 1716.83 Bn By 2032. Available online: https://www.precedenceresearch.com/electric-vehicle-market (accessed on 29 December 2023).

- Morgan, J. Electric Vehicles: The Future We Made and the Problem of Unmaking It. Camb. J. Econ. 2020, 44, 953–977. [Google Scholar] [CrossRef]

- Electric Vehicles and Supply Chain: PwC. Available online: https://www.pwc.com/us/en/industries/industrial-products/library/electric-vehicles-supply-chain.html (accessed on 28 December 2023).

- Das, H.S.; Rahman, M.M.; Li, S.; Tan, C.W. Electric Vehicles Standards, Charging Infrastructure, and Impact on Grid Integration: A Technological Review. Renew. Sustain. Energy Rev. 2020, 120, 109618. [Google Scholar] [CrossRef]

- Rajaeifar, M.A.; Ghadimi, P.; Raugei, M.; Wu, Y.; Heidrich, O. Challenges and Recent Developments in Supply and Value Chains of Electric Vehicle Batteries: A Sustainability Perspective. Resour. Conserv. Recycl. 2022, 180, 106144. [Google Scholar] [CrossRef]

- Sierzchula, W.; Bakker, S.; Maat, K.; Van Wee, B. The Influence of Financial Incentives and Other Socio-Economic Factors on Electric Vehicle Adoption. Energy Policy 2014, 68, 183–194. [Google Scholar] [CrossRef]

- Ziegler, D.; Abdelkafi, N. Business Models for Electric Vehicles: Literature Review and Key Insights. J. Clean. Prod. 2022, 330, 129803. [Google Scholar] [CrossRef]

- Wu, Y.; Jia, W.; Li, L.; Song, Z.; Xu, C.; Liu, F. Risk Assessment of Electric Vehicle Supply Chain Based on Fuzzy Synthetic Evaluation. Energy 2019, 182, 397–411. [Google Scholar] [CrossRef]

- Perryman, A. A Growing Appetite for EVs Tasks the Supply Chain to Scale | Supply Chain Dive. Available online: https://www.supplychaindive.com/news/electric-vehicle-battery-sourcing-material-manufacturing/596148/ (accessed on 27 January 2024).

- Lai, S.; Qiu, J.; Tao, Y.; Zhao, J. Pricing for Electric Vehicle Charging Stations Based on the Responsiveness of Demand. IEEE Trans. Smart Grid 2023, 14, 530–544. [Google Scholar] [CrossRef]

- Li, K.; Shao, C.; Zhang, H.; Wang, X. Strategic Pricing of Electric Vehicle Charging Service Providers in Coupled Power-Transportation Networks. IEEE Trans. Smart Grid 2023, 14, 2189–2201. [Google Scholar] [CrossRef]

- Arribas-Ibar, M.; Nylund, P.A.; Brem, A. The Risk of Dissolution of Sustainable Innovation Ecosystems in Times of Crisis: The Electric Vehicle during the COVID-19 Pandemic. Sustainability 2021, 13, 1319. [Google Scholar] [CrossRef]

- Bohnsack, R.; Pinkse, J. Value Propositions for Disruptive Technologies: Reconfiguration Tactics in the Case of Electric Vehicles. Calif. Manag. Rev. 2017, 59, 79–96. [Google Scholar] [CrossRef]

- Hussain, A.; Musilek, P. Resilience Enhancement Strategies for and Through Electric Vehicles. Sustain. Cities Soc. 2022, 80, 103788. [Google Scholar] [CrossRef]

- Zhao, J.; Xi, X.; Na, Q.; Wang, S.; Kadry, S.N.; Kumar, P.M. The Technological Innovation of Hybrid and Plug-in Electric Vehicles for Environment Carbon Pollution Control. Environ. Impact Assess. Rev. 2021, 86, 106506. [Google Scholar] [CrossRef]

- Eckstein, D.; Goellner, M.; Blome, C.; Henke, M. The Performance Impact of Supply Chain Agility and Supply Chain Adaptability: The Moderating Effect of Product Complexity. Int. J. Prod. Res. 2015, 53, 3028–3046. [Google Scholar] [CrossRef]

- Blome, D.; Schoenherr, T.; Rexhausen, C. Antecedents and Enablers of Supply Chain Agility and Its Effect on Performance: A Dynamic Capabilities Perspective. Int. J. Prod. Res. 2013, 51, 1295–1318. [Google Scholar] [CrossRef]

- Rong, K.; Shi, Y.; Shang, T.; Chen, Y.; Hao, H. Organizing Business Ecosystems in Emerging Electric Vehicle Industry: Structure, Mechanism, and Integrated Configuration. Energy Policy 2017, 107, 234–247. [Google Scholar] [CrossRef]

- Lu, C.; Rong, K.; You, J.; Shi, Y. Business Ecosystem and Stakeholders’ Role Transformation: Evidence from Chinese Emerging Electric Vehicle Industry. Expert. Syst. Appl. 2014, 41, 4579–4595. [Google Scholar] [CrossRef]

- Al-Alawi, B.M.; Bradley, T.H. Review of Hybrid, Plug-in Hybrid, and Electric Vehicle Market Modeling Studies. Renew. Sustain. Energy Rev. 2013, 21, 190–203. [Google Scholar] [CrossRef]

- Debnath, R.; Bardhan, R.; Reiner, D.M.; Miller, J.R. Political, Economic, Social, Technological, Legal and Environmental Dimensions of Electric Vehicle Adoption in the United States: A Social-Media Interaction Analysis. Renew. Sustain. Energy Rev. 2021, 152, 111707. [Google Scholar] [CrossRef]

- Hannan, M.A.; Hoque, M.M.; Mohamed, A.; Ayob, A. Review of Energy Storage Systems for Electric Vehicle Applications: Issues and Challenges. Renew. Sustain. Energy Rev. 2017, 69, 771–789. [Google Scholar] [CrossRef]

- Mahmoudzadeh Andwari, A.; Pesiridis, A.; Rajoo, S.; Martinez-Botas, R.; Esfahanian, V. A Review of Battery Electric Vehicle Technology and Readiness Levels. Renew. Sustain. Energy Rev. 2017, 78, 414–430. [Google Scholar] [CrossRef]

- Skeete, J.P.; Wells, P.; Dong, X.; Heidrich, O.; Harper, G. Beyond the EVent Horizon: Battery Waste, Recycling, and Sustainability in the United Kingdom Electric Vehicle Transition. Energy Res. Soc. Sci. 2020, 69, 101581. [Google Scholar] [CrossRef]

- Krishnan, R.; Butt, B. “The Gasoline of the Future:” Points of Continuity, Energy Materiality, and Corporate Marketing of Electric Vehicles among Automakers and Utilities. Energy Res. Soc. Sci. 2022, 83, 102349. [Google Scholar] [CrossRef]

- Prasadh, S.H.; Gopalakrishnan, R.; Sathish, S.; Ravichandran, M. Charging Infrastructure for EVs. In The Future of Road Transportation: Electrification and Automation; CRC Press: Boca Raton, FL, USA, 2023; pp. 196–213. ISBN 9781003354901. [Google Scholar]

- Train, K.E.; Winston, C. Vehicle choice behavior and the declining market share of U.S. automakers*. Int. Econ. Rev. 2007, 48, 1469–1496. [Google Scholar] [CrossRef]

- Campbell, J.R.; Hopenhayn, H.A. Market size matters. J. Ind. Econ. 2005, 53, 1–25. [Google Scholar] [CrossRef]

- Sanci, E.; Daskin, M.S.; Hong, Y.C.; Roesch, S.; Zhang, D. Mitigation Strategies against Supply Disruption Risk: A Case Study at the Ford Motor Company. Int. J. Prod. Res. 2022, 60, 5956–5976. [Google Scholar] [CrossRef]

- Thun, J.H.; Hoenig, D. An Empirical Analysis of Supply Chain Risk Management in the German Automotive Industry. Int. J. Prod. Econ. 2011, 131, 242–249. [Google Scholar] [CrossRef]

- Zulkarnain, Z.; Leviäkangas, P.; Kinnunen, T.; Kess, P. The Electric Vehicles Ecosystem Model—Construct, Analysis and Identification of Key Challenges. Manag. Glob. Transit. 2014, 12, 253–277. [Google Scholar]

- Soares, L.O.; Reis, A.d.C.; Vieira, P.S.; Hernández-Callejo, L.; Boloy, R.A.M. Electric Vehicle Supply Chain Management: A Bibliometric and Systematic Review. Energies 2023, 16, 1563. [Google Scholar] [CrossRef]

- Marcos, J.T.; Scheller, C.; Godina, R.; Spengler, T.S.; Carvalho, H. Sources of Uncertainty in the Closed-Loop Supply Chain of Lithium-Ion Batteries for Electric Vehicles. Clean. Logist. Supply Chain. 2021, 1, 100006. [Google Scholar] [CrossRef]

- Yang, Z.; Huang, H.; Lin, F.; Yang, Z.; Lin, F.; Huang, H. Sustainable Electric Vehicle Batteries for a Sustainable World: Perspectives on Battery Cathodes, Environment, Supply Chain, Manufacturing, Life Cycle, and Policy. Adv. Energy Mater. 2022, 12, 2200383. [Google Scholar] [CrossRef]

- Yang, Z.; Chen, H.; Peng, C.; Liu, X. Exploring the Role of Environmental Regulations in the Production and Diffusion of Electric Vehicles. Comput. Ind. Eng. 2022, 173, 108675. [Google Scholar] [CrossRef]

- Kumar, R.R.; Chakraborty, A.; Mandal, P. Promoting Electric Vehicle Adoption: Who Should Invest in Charging Infrastructure? Transp. Res. E Logist. Transp. Rev. 2021, 149, 102295. [Google Scholar] [CrossRef]

- Chirumalla, K.; Reyes, L.G.; Toorajipour, R. Mapping a Circular Business Opportunity in Electric Vehicle Battery Value Chain: A Multi-Stakeholder Framework to Create a Win–Win–Win Situation. J. Bus. Res. 2022, 145, 569–582. [Google Scholar] [CrossRef]

- Kotter, R.; Shaw, S. A Micro to Macro Investigation on Electric Vehicle Policy in the UK: Work Package 3 Activity 6 Report. Work Package 3 Activity 6 Report. 2013. Available online: https://nrl.northumbria.ac.uk/id/eprint/12893/ (accessed on 5 December 2023).

- Gebhardt, M.; Beck, J.; Kopyto, M.; Spieske, A. Determining Requirements and Challenges for a Sustainable and Circular Electric Vehicle Battery Supply Chain: A Mixed-Methods Approach. Sustain. Prod. Consum. 2022, 33, 203–217. [Google Scholar] [CrossRef]

- Lefeng, S.; Shengnan, L.; Chunxiu, L.; Yue, Z.; Cipcigan, L.; Acker, T.L. A Framework for Electric Vehicle Power Supply Chain Development. Util. Policy 2020, 64, 101042. [Google Scholar] [CrossRef]

- Ribeiro da Silva, E.; Lohmer, J.; Rohla, M.; Angelis, J. Unleashing the Circular Economy in the Electric Vehicle Battery Supply Chain: A Case Study on Data Sharing and Blockchain Potential. Resour. Conserv. Recycl. 2023, 193, 106969. [Google Scholar] [CrossRef]

- Jacobides, M.G.; Cennamo, C.; Gawer, A. Towards a Theory of Ecosystems. Strateg. Manag. J. 2018, 39, 2255–2276. [Google Scholar] [CrossRef]

- Bajaj, D.K.; Siddharth, P. Artificial Intelligence (AI) in Electrical Vehicles. In Recent Advances in Energy Harvesting Technologies; River Publishers: Aalborg, Denmark, 2023; pp. 57–76. ISBN 9788770228800. [Google Scholar]

- Lee, M. An Analysis of the Effects of Artificial Intelligence on Electric Vehicle Technology Innovation Using Patent Data. World Pat. Inf. 2020, 63, 102002. [Google Scholar] [CrossRef]

- Hu, J.; Lin, Y.; Li, J.; Hou, Z.; Chu, L.; Zhao, D.; Zhou, Q.; Jiang, J.; Zhang, Y. Performance Analysis of AI-Based Energy Management in Electric Vehicles: A Case Study on Classic Reinforcement Learning. Energy Convers. Manag. 2024, 300, 117964. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).