Impact and Mechanism of Digital Inclusive Finance on the Urban–Rural Income Gap of China from a Spatial Econometric Perspective

Abstract

:1. Introduction

2. Literature Review

3. Theoretical Analysis and Research Hypothesis

3.1. Spatial Effect of Digital Inclusive Finance on Urban–Rural Income Gap

3.2. Effect of Sub-Dimensions of Digital Inclusive Finance on Narrowing Urban–Rural Income Gap

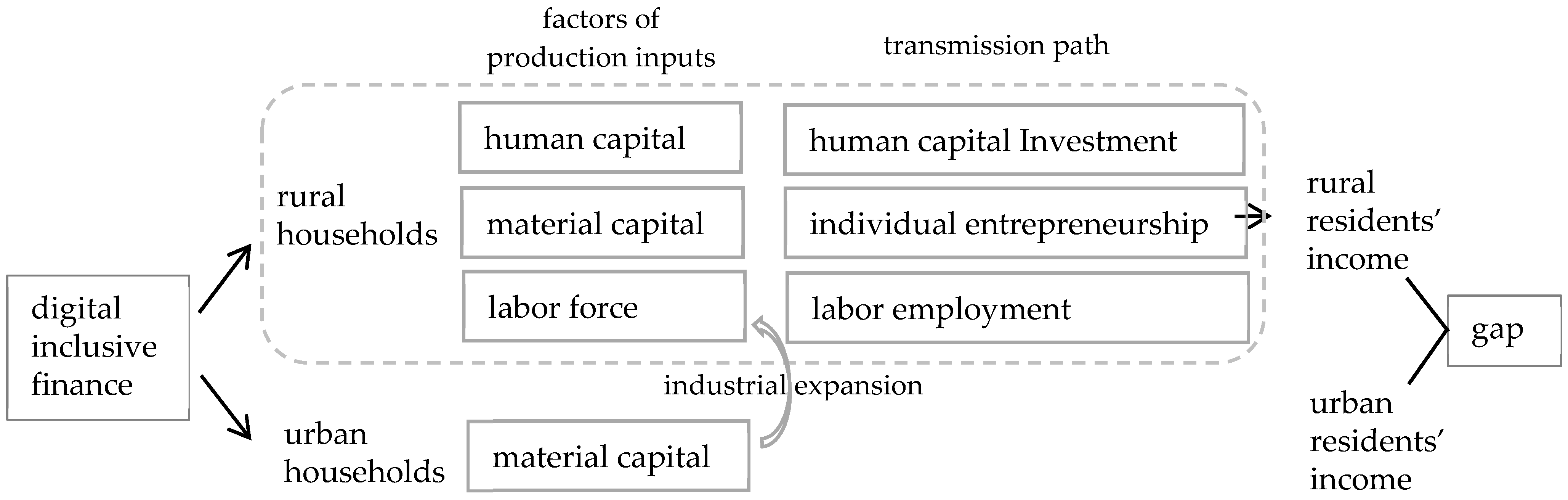

3.3. Transmission Mechanism of Digital Inclusive Finance Affecting the Urban–Rural Income Gap

4. Empirical Methods and Data Description

4.1. Spatial Econometric Model Selection

4.1.1. Global Spatial Autocorrelation Based on Moran’s Index

4.1.2. Local Spatial Autocorrelation Based on LISA Indicators

4.1.3. Spatial Lag Model and Spatial Error Model

4.2. Mediating-Effect Model: Transmission Mechanism Test

4.3. Descriptive Statistics of Data

5. Empirical Results and Discussion

5.1. Spatial Autoregression Analysis

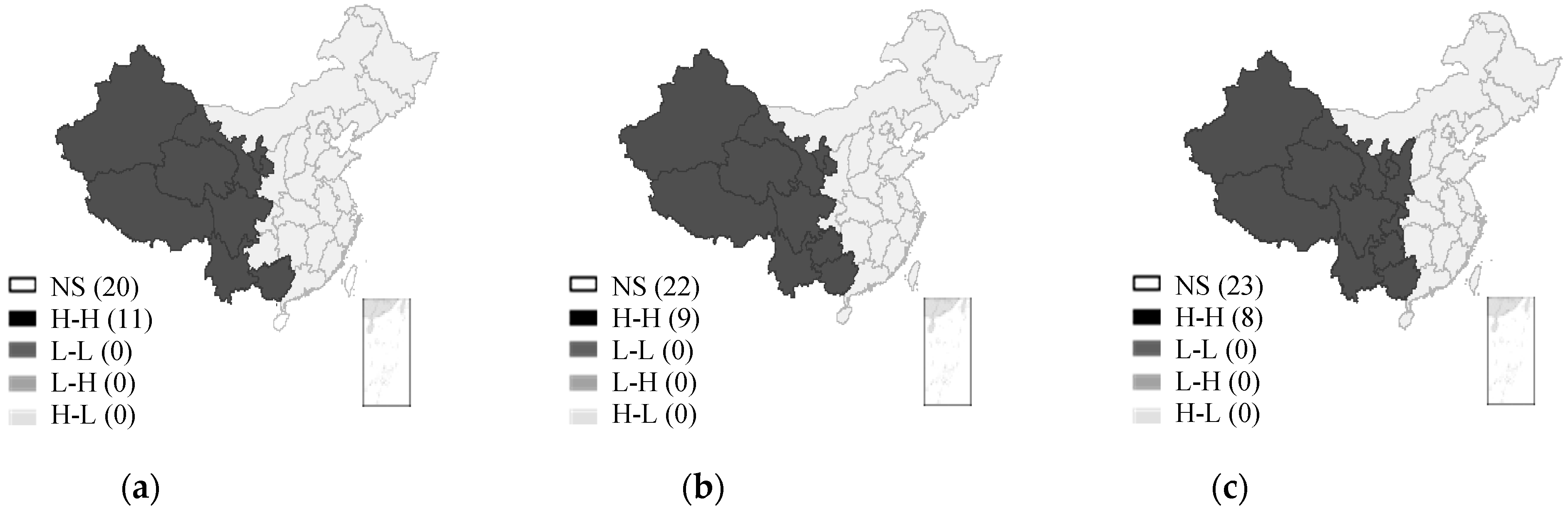

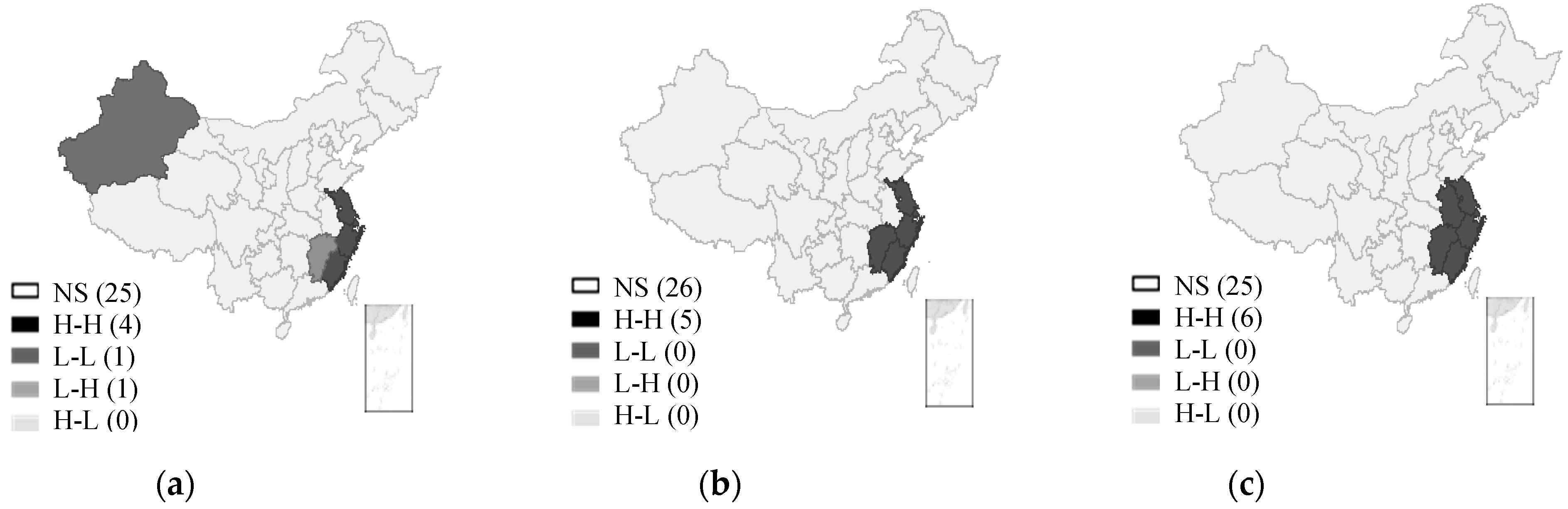

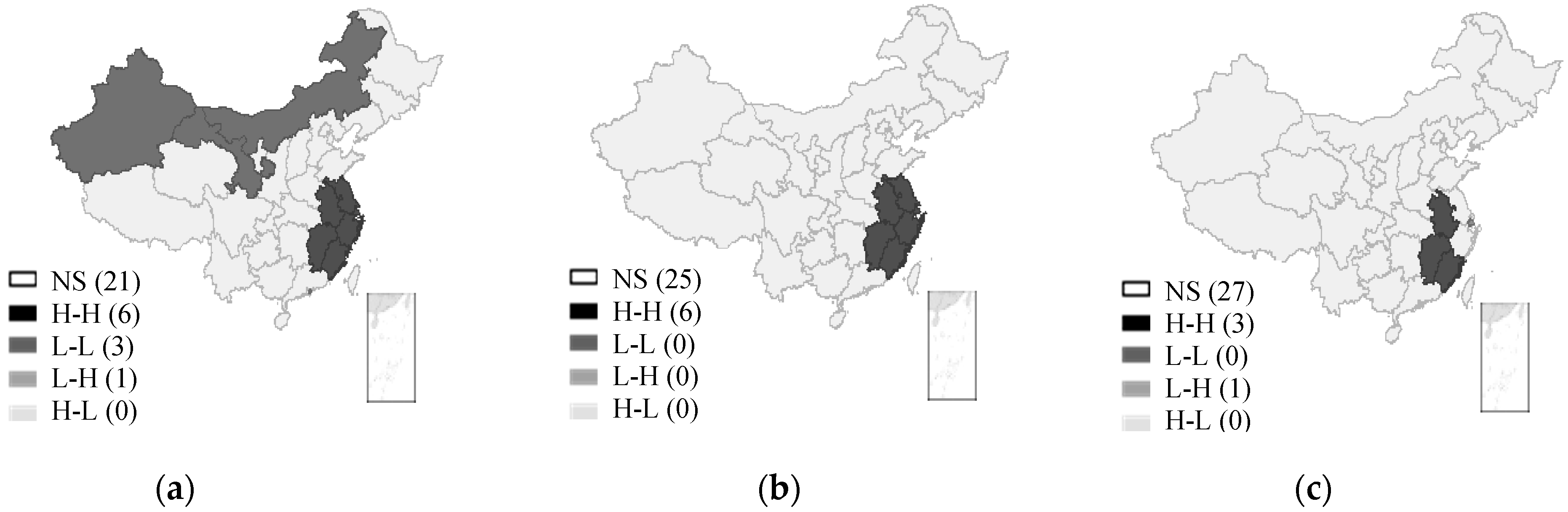

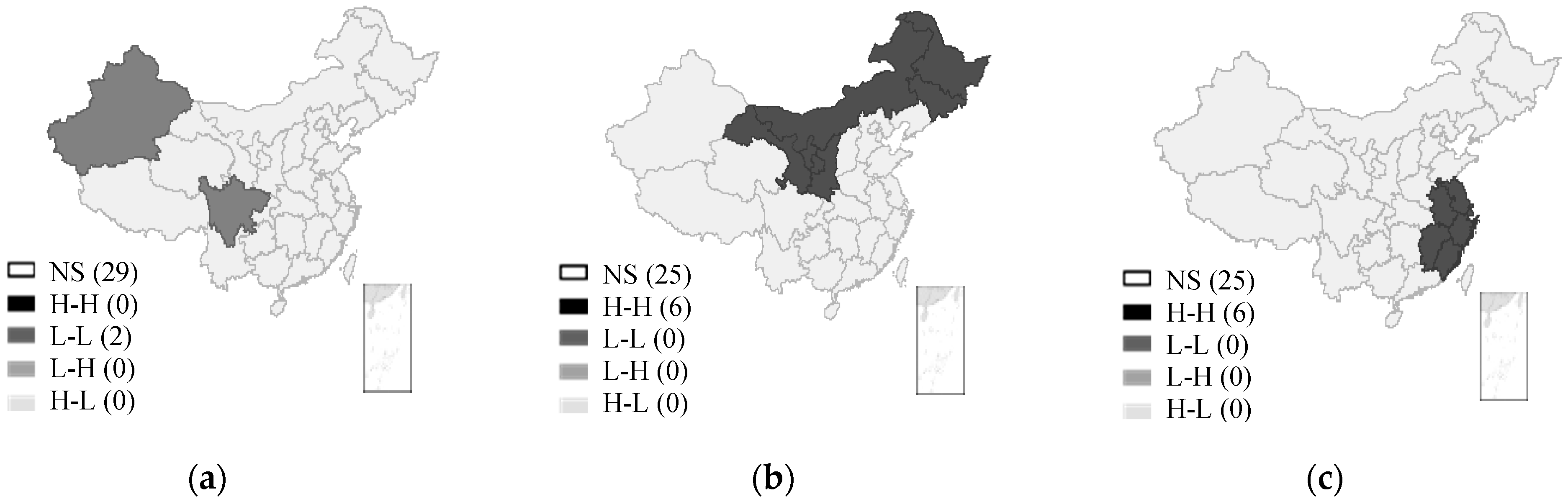

5.2. Spatial Distribution Characteristics of Income Gap and Digital Inclusive Finance

5.3. Regression Results of the Impact of Digital Inclusive Finance on the Urban–Rural Income Gap

5.4. Analysis of Transmission Mechanism

5.5. Robustness Test

6. Conclusions and Policy Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- McKinnon, R.I. The Value-Added Tax and the Liberalization of Foreign Trade in Developing Economies: A Comment. J. Econ. Lit. 1973, 11, 520–524. [Google Scholar]

- King, R.G.; Levine, R. Finance, Entrepreneurship and Growth. J. Monet. Econ. 1993, 32, 513–542. [Google Scholar] [CrossRef]

- Greenwood, J.; Jovanovic, B. Financial Development, Growth and the Distribution of Income. J. Political Econ. 1990, 98, 1076–1107. [Google Scholar] [CrossRef]

- Clarke, G.; Xu, L.; Zou, H.F. Finance and Income Inequality: What Do the Data Tell Us? South. Econ. J. 2006, 72, 578–596. [Google Scholar]

- Jeanneney, S.G.; Kpodar, K. Financial Development and Poverty Reduction: Can There be a Benefit without a Cost? J. Dev. Stud. 2011, 10, 143–163. [Google Scholar] [CrossRef]

- Seven, U.; Coskun, Y. Does Financial Development Reduce Income Inequality and Poverty? Evidence from Emerging Countries. Emerg. Mark. Rev. 2016, 26, 34–63. [Google Scholar] [CrossRef]

- Park, D.; Shin, K. Economic Growth, Financial Development, and Income Inequality. Emerg. Mark. Financ. Trade 2017, 53, 2794–2825. [Google Scholar] [CrossRef]

- Fowowe, B. The Effects of Financial Inclusion on Agricultural Productivity in Nigeria. J. Econ. Dev. 2020, 22, 61–79. [Google Scholar] [CrossRef]

- Peng, H.; Wang, J.; Wen, L.; Ding, P.; Zhu, Y.J. Is the Development of Inclusive Finance Truly Able to Alleviate Poverty?—An Empirical Study Based on Spatial Effect and Threshold Effect. Emerg. Mark. Financ. Trade 2022, 58, 2505–2521. [Google Scholar] [CrossRef]

- Chakravarty, S.R.; Pal, R. Inclusive Finance in India: An Axiomatic Approach. J. Policy Model. 2013, 35, 813–837. [Google Scholar] [CrossRef]

- Ran, M.S.; Chen, L.; Li, W. Financial Deepening, Spatial Spillover, and Urban–Rural Income Disparity: Evidence from China. Sustainability 2020, 12, 1450. [Google Scholar] [CrossRef]

- Schmied, J.; Marr, A. Financial Inclusion and Poverty: The Case of Peru. Reg. Sect. Econ. Stud. 2017, 16, 1–26. [Google Scholar]

- Beck, T.; Pamuk, H.; Ramrattan, R.; Burak, R.U. Payment Instruments, Finance and Development. J. Dev. Econ. 2018, 133, 162–186. [Google Scholar] [CrossRef]

- Li, J.; Wu, Y.; Xiao, J. The Impact of Digital Finance on Household Consumption: Evidence from China. Econ. Model. 2020, 86, 317–326. [Google Scholar] [CrossRef]

- Lian, X.; Mu, Y.; Zhang, W. Digital Inclusive Financial Services and Rural Income: Evidence from China’s Major Grain-producing Regions. Financ. Res. Lett. 2023, 53, 103622. [Google Scholar] [CrossRef]

- Liu, J.; Puah, C.H.; Arip, M.A.; Jong, M.C. Impacts of Digital Financial Inclusion on Urban-Rural Income Disparity: A Comparative Research of the Eastern and Western Regions in China. Economies 2023, 11, 282. [Google Scholar] [CrossRef]

- Zhang, X.; Zhang, J.; Wan, G.; Luo, Z. Fintech, Growth and Inequality: Evidence from China’s Household Survey Data. Singap. Econ. Rev. 2020, 65, 75–93. [Google Scholar] [CrossRef]

- Li, M.; Feng, S.; Xie, X. Spatial Effect of Digital Financial Inclusion on the Urban-rural Income Gap in China-Analysis Based on Path Dependence. Econ. Res. 2023, 32, 2106279. [Google Scholar] [CrossRef]

- Krugman, P. Geography and Trade; MIT Press: Cambridge, UK, 1991. [Google Scholar]

- Ji, X.M.; Wang, K.; Xu, H.; Li, M.C. Has Digital Financial Inclusion Narrowed the Urban-Rural Income Gap: The Role of Entrepreneurship in China. Sustainability 2021, 13, 8292. [Google Scholar] [CrossRef]

- Beck, T.; Demirguc-Kunt, A.; Levine, R. Finance, Inequality and the Poor. J. Econ. Growth 2007, 12, 27–49. [Google Scholar] [CrossRef]

- Sarma, M. Index of Financial Inclusion; Working Paper No. 215; Indian Council for Research on International Economic Relations: New Delhi, India, 2008. [Google Scholar]

- Zhang, H.; Yuan, F.; Cui, Y.; Li, G. Research on the Construction and Measurement of Inclusive Finance Evaluation Index System. Procedia Comput. Sci. 2022, 199, 1152–1159. [Google Scholar] [CrossRef]

- Allen, F.; Demirguc-Kunt, A.; Klapper, L.; Peria, M.S.M. The Foundations of Financial Inclusion: Understanding Ownership and Use of Formal Accounts. J. Financ. Intermediat. 2016, 27, 1–30. [Google Scholar] [CrossRef]

- Liu, G.; Huang, Y.; Huang, Z. Determinants and Mechanisms of Digital Financial Inclusion Development: Based on Urban-Rural Differences. Agronomy 2021, 11, 1833. [Google Scholar] [CrossRef]

- Li, Z. Peasant Migration: Historical Changes in the Past 70 Years and Prospects for the Next 30 years. China Rural Suvey 2019, 5, 2–16. (In Chinese) [Google Scholar]

- Wen, Z.; Zhang, L.; Hou, J.; Liu, H. Testing and Application of the Mediating Effects. Acta Psychol. Sin. 2004, 36, 614–620. (In Chinese) [Google Scholar]

- Aghion, P.; Fally, T.; Scarpetta, S. Credit Constraints as a Barrier to the Entry and Post-entry Growth of Firms. Econ. Policy 2007, 22, 732–779. [Google Scholar] [CrossRef]

- Zhao, D.; Li, H. Research on Cultivation of Rural Youth Entrepreneurship under the Background of New Urbanization. J. Agric. 2017, 7, 127–136. (In Chinese) [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Mark | Variable Definitions | Mean | Sd | Min | Max |

|---|---|---|---|---|---|---|

| Response variable | urban–rural income gap | Theil Index | 0.098 | 0.044 | 0.020 | 0.227 |

| Core explanatory variables | DIFI | index of digital inclusive finance/100 | 1.872 | 0.851 | 0.162 | 3.777 |

| DIFB | index of coverage breadth of digital inclusive finance/100 | 1.666 | 0.851 | 0.020 | 3.539 | |

| DIFD | index of depth usage of digital inclusive finance/100 | 1.825 | 0.850 | 0.068 | 4.004 | |

| DIFDD | index of digitization of digital inclusive finance/100 | 2.640 | 1.160 | 0.076 | 4.537 | |

| Other control variable | IS | value added of the tertiary sector/regional GDP | 0.458 | 0.095 | 0.297 | 0.810 |

| URB | urban population/total population of the region | 0.561 | 0.133 | 0.227 | 0.896 | |

| GI | government expenditure/regional GDP | 0.281 | 0.213 | 0.110 | 1.379 | |

| OPE | (import amount + export amount)/regional GDP | 0.252 | 0.275 | 0.012 | 1.419 | |

| EDU | average years of education per capita in the region | 9.042 | 1.127 | 4.222 | 12.503 | |

| FDD | loan balance of financial institutions/regional GDP | 1.349 | 0.466 | 0.650 | 3.083 | |

| FDB | number of bank branches/total population of region | 1.661 | 0.289 | 1.104 | 2.331 | |

| mediating variables | HCI | the number of persons with higher education (10,000 persons) | 503.29 | 307.19 | 6.69 | 1443.20 |

| ENT | the number of self-employed persons (10,000 persons) | 368.15 | 293.10 | 25.40 | 1470.10 | |

| LE | the sum of employment figures in private enterprises and non-private urban units (10,000 persons) | 1052.74 | 903.30 | 43.90 | 5019.20 |

| Year | Urban Residents’ per Capita Disposable Income | Rural Residents’ per Capita Disposable Income | Urban–Rural Income Gap | DIF | DIFB | DIFD | DIFDD |

|---|---|---|---|---|---|---|---|

| 2011 | 0.450 *** | 0.536 *** | 0.524 *** | 0.478 *** | 0.416 *** | 0.624 *** | 0.003 |

| 2012 | 0.448 *** | 0.539 *** | 0.518 *** | 0.477 *** | 0.390 *** | 0.620 *** | 0.278 *** |

| 2013 | 0.360 *** | 0.559 *** | 0.530 *** | 0.450 *** | 0.384 *** | 0.577 *** | 0.107 |

| 2014 | 0.358 *** | 0.561 *** | 0.499 *** | 0.446 *** | 0.355 *** | 0.549 *** | 0.014 |

| 2015 | 0.348 *** | 0.556 *** | 0.559 *** | 0.409 *** | 0.349 *** | 0.586 *** | 0.407 *** |

| 2016 | 0.349 *** | 0.554 *** | 0.557 *** | 0.430 *** | 0.358 *** | 0.593 *** | 0.116 |

| 2017 | 0.343 *** | 0.555 *** | 0.558 *** | 0.492 *** | 0.398 *** | 0.575 *** | 0.138 |

| 2018 | 0.344 *** | 0.553 *** | 0.547 *** | 0.538 *** | 0.420 *** | 0.588 *** | 0.594 *** |

| Variables | Urban–Rural Income Gap | Robustness Test Ratio of Urban and Rural Residents’ Income | |||||||

|---|---|---|---|---|---|---|---|---|---|

| (1) OLS | (2) SLM | (3) SEM | (4) SLM | (5) SLM | (6) SLM | (7) OLS | (8) SLM | (9) SEM | |

| DIF | −0.0117 *** (0.0022) | −0.0039 ** (0.0016) | −0.0104 *** (0.0021) | - | - | - | −0.1697 *** (0.0228) | −0.0744 *** (0.0221) | −0.1357 *** (0.0290) |

| DIFB | - | - | - | −0.0045 *** (0.0017) | - | - | - | - | - |

| DIFD | - | - | - | - | −0.0007 (0.0012) | - | - | - | - |

| DIFDD | - | - | - | - | - | −0.0022 *** (0.0007) | - | - | - |

| IS | 0.0702 *** (0.0211) | 0.0526 *** (0.0159) | 0.0245 (0.0175) | 0.0552 *** (0.0162) | 0.0386 ** (0.0152) | 0.0450 *** (0.0147) | 1.0568 *** (0.2790) | 0.6748 *** (0.2334) | 0.4066 * (0.2556) |

| URB | −0.3440 *** (0.0484) | −0.2401 *** (0.0307) | −0.2610 *** (0.0335) | −0.2336 *** (0.0314) | −0.2645 *** (0.0299) | −0.2549 *** (0.0291) | −2.5759 *** (0.5119) | −1.7671 *** (0.4450) | −1.7741 *** (0.4867) |

| GI | 0.0299 (0.0377) | −0.0138 (0.0179) | 0.0065 (0.0187) | −0.0149 (0.0178) | −0.0176 (0.0181) | −0.0119 (0.0182) | 0.0209 (0.2927) | 0.0023 (0.2611) | 0.1628 (0.2691) |

| OPE | −0.0388 *** (0.0116) | −0.0255 *** (0.0081) | −0.0288 *** (0.0096) | −0.0259 *** (0.0082) | −0.0170 ** (0.0076) | −0.0235 *** (0.0076) | −0.3087 ** (0.1396) | −0.2590 ** (0.1187) | −0.3492 ** (0.1386) |

| EDU | 0.0040 (0.0032) | 0.0040 * (0.0023) | 0.0018 (0.0023) | 0.0037 * (0.0022) | 0.0039 * (0.0023) | 0.0034 (0.0022) | 0.0736 * (0.0396) | 0.0485 (0.0329) | 0.0184 (0.0333) |

| FDD | 0.0103 *** (0.0035) | 0.0101 *** (0.0026) | 0.0078 *** (0.0027) | 0.0104 *** (0.0026) | 0.0091 *** (0.0026) | 0.0091 *** (0.0025) | 0.1058 ** (0.458) | 0.0656 * (0.0379) | 0.0335 * (0.0399) |

| FDB | −0.0051 (0.0069) | −0.0045 (0.0050) | 0.0009 (0.0052) | −0.0044 (0.0050) | −0.0063 (0.0050) | −0.0040 (0.0050) | 0.0665 (0.0876) | 0.0699 (0.0727) | 0.1469 (0.0752) |

| Constant | 0.2410 *** (0.0399) | 0.1235 *** (0.0240) | 0.2299 *** (0.0246) | 0.1213 *** (0.0241) | 0.1353 *** (0.0248) | 0.1395 *** (0.0235) | 3.1070 *** (0.3779) | 1.3874 *** (0.3790) | 3.3245 *** (0.3567) |

| ρ/λ | - | 0.5996 *** (0.0548) | 0.6642 *** (0.0610) | 0.5986 *** (0.0544) | 0.6591 *** (0.0472) | 0.5912 *** (0.0544) | - | 0.5677 *** (0.0610) | 0.6134 *** (0.0675) |

| R2 | 0.7608 | 0.7725 | 0.7471 | 0.7699 | 0.7552 | 0.7906 | 0.6235 | 0.6438 | 0.6127 |

| LogL | - | 824.5222 | 817.4697 | 824.7878 | 821.4684 | 825.7428 | - | 162.0098 | 157.1848 |

| Hausman test statistic | 23.22 ** | 19.19 ** | 35.68 ** | 18.13 ** | 28.48 ** | 16.20 ** | 34.75 ** | 23.41 ** | 25.86 ** |

| Fixed effect | yes | yes | yes | yes | yes | yes | yes | yes | yes |

| Sample size | 248 | 248 | 248 | 248 | 248 | 248 | 248 | 248 | 248 |

| Variables | Step1 | Human Capital Investment | Individual Entrepreneurship | Labor Employment | |||

|---|---|---|---|---|---|---|---|

| Step2 | Step3 | Step2 | Step3 | Step2 | Step3 | ||

| (10) | (11) | (12) | (13) | (14) | (15) | (16) | |

| Urban–Rural Income Gap | Human Capital Investment | Urban–Rural Income Gap | Individual Entrepreneurship | Urban–Rural Income Gap | Labor Employment | Urban–Rural Income Gap | |

| DIF | −0.0117 *** (0.0022) | −0.0005 (0.0214) | −0.0113 *** (0.0021) | 0.0488 (0.0305) | −0.0111 *** (0.0048) | 0.1456 *** (0.0262) | −0.0087 *** (0.0022) |

| HCI | - | - | 0.0046 (0.0069) | - | - | - | - |

| ENT | - | - | - | - | −0.0044 (0.0048) | - | - |

| LE | - | - | - | - | - | - | −0.0180 *** (0.0055) |

| Control variable | Control | Control | Control | Control | Control | Control | Control |

| R2 | 0.7608 | 0.8494 | 0.7613 | 0.8184 | 0.7618 | 0.6984 | 0.7726 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mo, Y.; Mu, J.; Wang, H. Impact and Mechanism of Digital Inclusive Finance on the Urban–Rural Income Gap of China from a Spatial Econometric Perspective. Sustainability 2024, 16, 2641. https://doi.org/10.3390/su16072641

Mo Y, Mu J, Wang H. Impact and Mechanism of Digital Inclusive Finance on the Urban–Rural Income Gap of China from a Spatial Econometric Perspective. Sustainability. 2024; 16(7):2641. https://doi.org/10.3390/su16072641

Chicago/Turabian StyleMo, Yuan, Jing Mu, and Hui Wang. 2024. "Impact and Mechanism of Digital Inclusive Finance on the Urban–Rural Income Gap of China from a Spatial Econometric Perspective" Sustainability 16, no. 7: 2641. https://doi.org/10.3390/su16072641