Corporate Sustainability Reporting and Stakeholders’ Interests: Evidence from China

Abstract

:1. Introduction

2. Related Literature and Institutional Background

2.1. Stakeholders and Sustainability Reporting

2.2. Uniqueness of Sustainability Reporting in China

2.3. Sustainability Reporting Standards

2.4. The Connection between SR and Stakeholders’ Concerns

3. Research Methodology

3.1. Sample Selection and Content Analysis

3.2. Survey Process

4. Results

4.1. Results of Content Analysis of the ESG Reports

4.2. Results of Questionnaire Survey

4.3. Connection between Corporate Sustainability Reporting and Stakeholder Needs

5. Results Discussion and Policy Implications

5.1. Results Discussion

5.1.1. Stakeholder Theory Perspective

5.1.2. Signaling Theory Perspective

5.2. Policy Implications and Recommendations

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Industry | Stock Code | Location | GRI | SOE | Sustainability Dimensions | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Environment | Economic | Society | Consumer | LA&HR | GOR | Total | |||||

| Energy | 600792.SH | Yunnan | * | 3 | 3 | 3 | 1 | 11 | 8 | 29 | |

| 600387.SH | Zhejiang | 0 | 5 | 0 | 0 | 0 | 6 | 11 | |||

| Materials | 600019.SH | Shanghai | * | ** | 16 | 1 | 15 | 9 | 15 | 4 | 60 |

| 600585.SH | Anhui | 13 | 2 | 9 | 5 | 14 | 2 | 45 | |||

| Capital goods | 601766.SH | Beijing | * | ** | 9 | 1 | 29 | 0 | 7 | 1 | 47 |

| 600031.SH | Beijing | 6 | 3 | 14 | 2 | 10 | 0 | 35 | |||

| Commercial and professional services | 300012.SZ | Guangdong | * | 7 | 0 | 8 | 3 | 11 | 5 | 34 | |

| 603568.SH | Zhejiang | 7 | 1 | 3 | 0 | 4 | 2 | 17 | |||

| Transportation | 000507.SZ | Guangdong | * | 17 | 2 | 8 | 4 | 9 | 5 | 45 | |

| 000905.SZ | Fujian | 7 | 0 | 15 | 0 | 0 | 0 | 22 | |||

| Automobiles and components | 600104.SH | Shanghai | * | 12 | 5 | 28 | 4 | 11 | 3 | 63 | |

| 601633.SH | Hebei | 14 | 1 | 9 | 8 | 3 | 6 | 41 | |||

| Consumer durables and apparel | 600690.SH | Shandong | * | 13 | 2 | 21 | 8 | 21 | 4 | 69 | |

| 000651.SZ | Guangdong | 5 | 3 | 6 | 13 | 7 | 5 | 39 | |||

| Consumer services | 002033.SZ | Yunnan | * | 2 | 3 | 5 | 4 | 10 | 2 | 26 | |

| 300859.SZ | Xinjiang | 0 | 4 | 0 | 0 | 2 | 3 | 9 | |||

| Media | 000156.SZ | Zhejiang | * | 7 | 6 | 10 | 17 | 8 | 3 | 51 | |

| 600959.SH | Jiangsu | 0 | 0 | 8 | 1 | 0 | 2 | 11 | |||

| Retailing | 601828.SH | Shanghai | * | 8 | 6 | 10 | 10 | 17 | 2 | 53 | |

| 600739.SH | Liaoning | 3 | 4 | 6 | 0 | 11 | 3 | 27 | |||

| Food and staples retailing | 300783.SZ | Anhui | * | 8 | 0 | 23 | 4 | 6 | 7 | 48 | |

| 601116.SH | Zhejiang | 0 | 5 | 4 | 0 | 0 | 6 | 15 | |||

| Food, beverage, and tobacco | 600600.SH | Shandong | * | 12 | 4 | 12 | 3 | 9 | 5 | 45 | |

| 000596.SZ | Anhui | 3 | 4 | 3 | 2 | 6 | 2 | 20 | |||

| Household and personal products | 603605.SH | Zhejiang | * | 14 | 5 | 9 | 4 | 15 | 5 | 52 | |

| 300957.SZ | Yunnan | 16 | 4 | 9 | 3 | 9 | 7 | 48 | |||

| Healthcare equipment and services | 688139.SH | Shandong | * | 14 | 2 | 26 | 4 | 10 | 8 | 64 | |

| 688050.SH | Beijing | 4 | 5 | 18 | 1 | 12 | 3 | 43 | |||

| Pharmaceuticals, biotechnology, and life sciences | 000538.SZ | Yunnan | * | 10 | 3 | 18 | 6 | 5 | 14 | 56 | |

| 603392.SH | Beijing | 12 | 5 | 10 | 0 | 5 | 7 | 39 | |||

| Banks | 601665.SH | Shandong | * | 6 | 1 | 18 | 9 | 12 | 7 | 53 | |

| 601187.SH | Fujian | 4 | 5 | 21 | 7 | 7 | 0 | 44 | |||

| Diversified financials | 600837.SH | Shanghai | * | 6 | 5 | 30 | 10 | 7 | 10 | 68 | |

| 300033.SZ | Zhejiang | 7 | 4 | 7 | 4 | 7 | 3 | 32 | |||

| Insurance | 601318.SH | Guangdong | * | 7 | 4 | 22 | 16 | 8 | 5 | 62 | |

| 601628.SH | Beijing | ** | 3 | 4 | 23 | 18 | 4 | 11 | 63 | ||

| Software and services | 600570.SH | Zhejiang | * | 13 | 4 | 28 | 3 | 18 | 8 | 74 | |

| 600845.SH | Shanghai | ** | 0 | 5 | 8 | 2 | 13 | 5 | 33 | ||

| Technological hardware and equipment | 601138.SH | Guangdong | * | 15 | 5 | 10 | 0 | 23 | 15 | 68 | |

| 002415.SZ | Zhejiang | ** | 10 | 6 | 7 | 7 | 10 | 8 | 48 | ||

| Semiconductors and semiconductor equipment | 603501.SH | Shanghai | * | 9 | 0 | 6 | 3 | 18 | 10 | 46 | |

| 002459.SZ | Hebei | 16 | 4 | 11 | 6 | 15 | 9 | 61 | |||

| Telecommunication services | 600050.SH | Beijing | * | ** | 3 | 3 | 47 | 21 | 18 | 5 | 97 |

| 601698.SH | Beijing | ** | 3 | 5 | 62 | 0 | 9 | 5 | 84 | ||

| Utilities | 003816.SZ | Guangdong | * | ** | 22 | 5 | 33 | 0 | 22 | 23 | 105 |

| 600905.SH | Beijing | ** | 18 | 4 | 17 | 0 | 4 | 7 | 50 | ||

| Real estate | 600383.SH | Guangdong | * | 0 | 0 | 17 | 0 | 10 | 3 | 30 | |

| 600606.SH | Shanghai | 4 | 5 | 14 | 0 | 0 | 0 | 23 | |||

| Total | 388 | 158 | 720 | 222 | 453 | 264 | 2205 | ||||

| Average per report | 8.08 | 3.29 | 15.00 | 4.63 | 9.44 | 5.50 | 45.94 | ||||

| Range | 0–22 | 0–6 | 0–62 | 0–21 | 0–23 | 0–23 | 9–105 | ||||

| GRI adopters | 233 | 70 | 436 | 143 | 301 | 162 | 1345 | ||||

| Non-GRI adopters | 155 | 88 | 284 | 79 | 152 | 102 | 860 | ||||

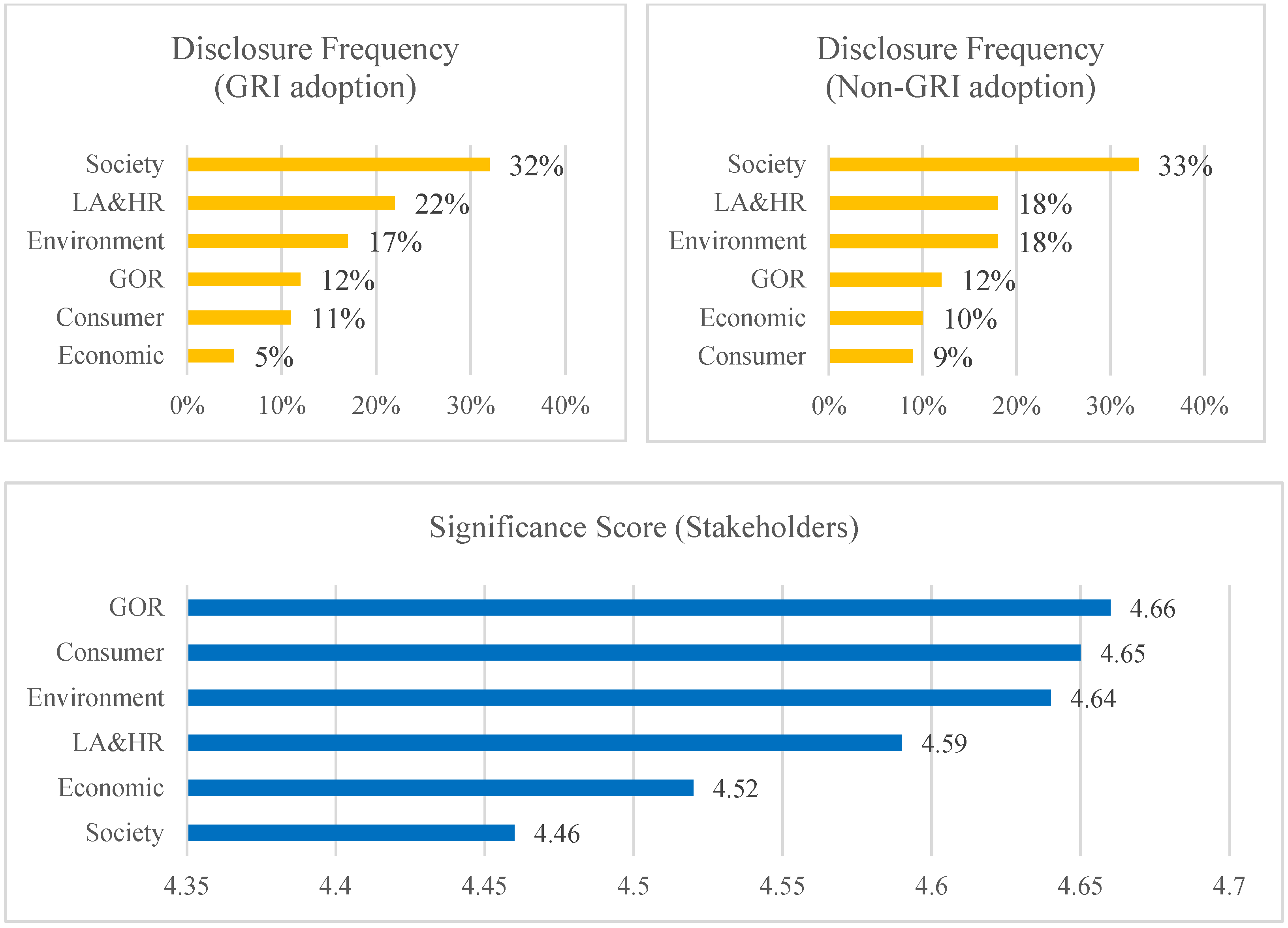

| Percentage of GRI adopters | 17% | 5% | 32% | 11% | 22% | 12% | 100% | ||||

| Percentage of non-GRI adopters | 18% | 10% | 33% | 9% | 18% | 12% | 100% | ||||

| Percentage of total | 18% | 7% | 33% | 10% | 21% | 12% | 100% | ||||

| Dimensions | Items | Mean | Std. Dev. |

|---|---|---|---|

| Environment | Work on national strategy of carbon neutrality and reduction of carbon emissions | 4.72 | 0.61 |

| Utilize clean and renewable energy and minimize the negative impact of climate change | 4.69 | 0.66 | |

| Control the release of pollution (e.g., wastewater, noise, greenhouse gas, and solid wastes) | 4.73 | 0.60 | |

| Increase resource recycling rate and reduce recourse consumption (e.g., water, electricity, natural gas, and petrol) in the operation process | 4.74 | 0.55 | |

| Increase facility investment on recourse and energy saving and protect the environment in the entire life cycle when providing products and services | 4.63 | 0.67 | |

| Establish a green energy data center for environmental detection and analysis | 4.52 | 0.74 | |

| Sustain biodiversity and conserve flora and fauna | 4.69 | 0.65 | |

| Establish an evaluation model for environmental performance | 4.54 | 0.75 | |

| Save paper and plastic through packaging, shipment, and daily office activity | 4.54 | 0.73 | |

| Economic | Preserve the value of shareholders’ assets and increase profit distribution | 4.44 | 0.80 |

| Increase market value | 4.55 | 0.73 | |

| Disclose financial performance (e.g., sales revenue, net income, EPS, ROE, and ROI) | 4.55 | 0.73 | |

| Contribution of tax payment | 4.55 | 0.71 | |

| Society | Donate during the COVID-19 period and rollout of volunteer and charity events | 4.33 | 0.81 |

| Provide poverty alleviation and critical illness assistance | 4.40 | 0.78 | |

| Assist in infrastructure in poor areas and purchase or help to sell agricultural products in poor areas | 4.36 | 0.80 | |

| Provide public education grants for children and support special education for autistic children | 4.39 | 0.81 | |

| Provide job opportunities for female, disabled, and ethnic minorities | 4.44 | 0.79 | |

| Participate in technological innovation projects, promote industry–university–institute cooperation and global cooperation | 4.59 | 0.65 | |

| Invest in high-tech innovations and enhance R&D competence | 4.62 | 0.63 | |

| Facilitate the development of SMEs and promote and lead industry development | 4.50 | 0.71 | |

| Initiate the perspective of healthy living | 4.54 | 0.71 | |

| Consumer | Establish a customer-oriented strategy and encourage product innovation and service efficiency | 4.60 | 0.64 |

| Detect fake products and implement product recall management | 4.67 | 0.60 | |

| Protect customer privacy information and handle customer complaints properly | 4.74 | 0.57 | |

| Process client review and survey on customer satisfaction | 4.63 | 0.64 | |

| Upgrade consumer experience and explore customer communication channels | 4.64 | 0.63 | |

| LA&HR | Establish employee representative commission and encourage employee involvement in decision-making | 4.43 | 0.78 |

| Provide regular training programs for career development with a fair performance evaluation system and compensation system | 4.62 | 0.62 | |

| Ensure vocational health and safety management and purchase insurance for health, damage, and accident | 4.66 | 0.61 | |

| Keep work–life balance and provide holiday time, festival celebration, sports and entertainment activities, and a recuperate program | 4.57 | 0.66 | |

| Provide medical examinations on a regular basis and provide psychological care | 4.61 | 0.64 | |

| Eliminate discrimination on race, region, gender, disability, and nationality | 4.70 | 0.60 | |

| Increase the proportion of female managers and take care of female employees | 4.58 | 0.71 | |

| Prohibit the use of child and forced labor | 4.80 | 0.51 | |

| Offer public rental housing benefits and rental allowance | 4.49 | 0.74 | |

| Provide financial assistance for employees with family difficulties | 4.45 | 0.78 | |

| Survey on employee satisfaction and build up a working environment that features diversity and fairness | 4.59 | 0.65 | |

| GOR | Evaluate ESG performance for customers, suppliers, and employees | 4.59 | 0.64 |

| Set up risk management and internal control commission and risk rating system | 4.60 | 0.63 | |

| Establish life cycle quality management system, emergency management system, and safety inspection and training system | 4.60 | 0.65 | |

| Protect data and network security | 4.78 | 0.51 | |

| Implement anti-corruption and anti-bribery systems and whistleblower protection systems | 4.73 | 0.54 |

References

- Tsang, A.; Frost, T.; Cao, H. Environmental, social, and governance (ESG) disclosure: A literature review. Br. Account. Rev. 2023, 55, 101149. [Google Scholar] [CrossRef]

- Stuart, A.C.; Fuller, S.H.; Heron, N.M.; Riley, T.J. Defining CSR disclosure quality: A review and synthesis of the accounting literature. J. Account. Lit. 2023, 45, 1–47. [Google Scholar] [CrossRef]

- Mougenot, B.; Doussoulin, J.P. A bibliometric analysis of the Global Reporting Initiative (GRI): Global trends in developed and developing countries. Environ. Dev. Sustain. 2024, 26, 6543–6560. [Google Scholar] [CrossRef]

- Bradford, M.; Earp, J.B.; Showalter, D.S.; Williams, P.F. Corporate sustainability reporting and stakeholder concerns: Is there a disconnect? Account. Horiz. 2017, 31, 83–102. [Google Scholar] [CrossRef]

- Shen, H.; Lin, H.; Han, W.; Wu, H. ESG in China: A review of practice and research, and future research avenues. China J. Account. Res. 2023, 16, 100325. [Google Scholar] [CrossRef]

- Anton, A.I.; Earp, J.B. A requirements taxonomy to reduce website privacy vulnerabilities, to appear. Requir. Eng. 2004, 9, 169–185. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stockholder Approach; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Donaldson, T.; Preston, L.E. The stakeholder theory of the corporation: Concepts, evidence, and implications. Acad. Mgt. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Howarth, R.B.; Norgaard, R.B. Environmental valuation under sustainable development. Am. Econ. Rev. 1992, 82, 473–477. [Google Scholar]

- Benabou, R.; Tirole, J. Individual and corporate social responsibility. Economics 2010, 77, 1–19. [Google Scholar]

- Lins, K.V.; Servaes, H.; Tamayo, A. Social capital, trust, and firm performance: The value of corporate social responsibility during the financial crisis. J. Financ. 2017, 72, 1785–1824. [Google Scholar] [CrossRef]

- Goss, A.; Roberts, G.S. The impact of corporate social responsibility on the cost of bank loans. J. Bank. Financ. 2011, 35, 1794–1810. [Google Scholar] [CrossRef]

- Kleimeier, S.; Viehs, M. Carbon Disclosure, Emission Levels, and the Cost of Debt. Available online: https://www.researchgate.net/publication/314699310 (accessed on 7 January 2023).

- Nassos, G.P.; Avlonas, N. Practical Sustainability Strategies: How to Gain a Competitive Advantage; John Wiley & Sons: New York, NY, USA, 2020; pp. 243–274. [Google Scholar]

- Christensen, H.B.; Hail, L.; Leuz, C. Mandatory CSR and sustainability reporting: Economic analysis and literature review. Rev. Account. Stud. 2021, 26, 1176–1248. [Google Scholar] [CrossRef]

- Thoradeniya, P.; Lee, J.; Tan, R.; Ferreira, A. From intention to action on sustainability reporting: The role of individual, organizational and institutional factors during war and post-war periods. Br. Account. Rev. 2022, 54, 101021. [Google Scholar] [CrossRef]

- Deloitte. Sustainability Disclosure: Getting Ahead of the Curve. Available online: https://www2.deloitte.com/content/dam/Deloitte/us/Documents/risk/us-risk-sustainability-disclosure.pdf (accessed on 15 January 2023).

- Dingwerth, K.; Eichinger, M. Tamed transparency: How information disclosure under the global reporting initiative fails to empower. Glob. Environ. Politics 2010, 10, 74–96. [Google Scholar] [CrossRef]

- Bucaro, A.C.; Jackson, K.E.; Lill, J.B. The influence of corporate social responsibility measures on investors’ judgments when integrated in a financial report versus presented in a separate report. Contemp. Account. Res. 2020, 37, 665–695. [Google Scholar] [CrossRef]

- Grewal, J.; Serafeim, G. Research on corporate sustainability: Review and directions for future research. Found. Trends Account. 2020, 14, 73–127. [Google Scholar] [CrossRef]

- Lindgren, C.; Huq, A.M.; Carling, K. Who are the intended users of CSR reports? Insights from a data-driven approach. Sustainability 2021, 13, 1070. [Google Scholar] [CrossRef]

- Mion, G.; Loza Adaui, C.R. Mandatory nonfinancial disclosure and its consequences on the sustainability reporting quality of Italian and German companies. Sustainability 2019, 11, 4612. [Google Scholar] [CrossRef]

- Hamilton, S.N.; Waters, R.D. Mainstreaming standardized sustainability reporting: Comparing Fortune 50 corporations’ and US News & World Report’s top 50 global universities’ sustainability reports. Sustainability 2022, 14, 3442. [Google Scholar] [CrossRef]

- Ervits, I. CSR reporting by Chinese and western MNEs: Patterns combining formal homogenization and substantive differences. Int. J. Corp. Soc. Responsib. 2021, 6, 6. [Google Scholar] [CrossRef]

- Ammann, M.; Bauer, C.; Fischer, S.; Müller, P. The impact of the Morningstar Sustainability Rating on mutual fund flows. Eur. Financial Manag. 2019, 25, 520–553. [Google Scholar] [CrossRef]

- Hartzmark, S.M.; Sussman, A.B. Do investors value sustainability? A natural experiment examining ranking and fund flows. J. Financ. 2019, 74, 2789–2837. [Google Scholar] [CrossRef]

- See, G. Harmonious society and Chinese CSR: Is there really a link? J. Bus. Ethics 2009, 89, 1–22. [Google Scholar] [CrossRef]

- Lattemann, C.; Fetscherin, M.; Alon, I.; Li, S.; Schneider, A.M. CSR communication intensity in Chinese and Indian multinational companies. Corp. Gov. Int. Rev. 2009, 17, 426–442. [Google Scholar] [CrossRef]

- McKinnon, J. Cultural constraints on audit independence in Japan. Int. J. Account. 1984, 20, 17–43. [Google Scholar]

- Yamagami, T.; Kokubu, K. A note on corporate social disclosure in Japan. Account. Audit. Account. J. 1991, 4, 32–39. [Google Scholar] [CrossRef]

- Haider, M.B.; Kokubu, K. Assurance and third-party comment in sustainability reporting in Japan: A descriptive study. Int. J. Environ. Sustain. Dev. 2015, 14, 207–230. [Google Scholar] [CrossRef]

- Xu, S.; Yang, R. Indigenous characteristics of Chinese corporate social responsibility conceptual paradigm. J. Bus. Ethics 2010, 93, 321–333. [Google Scholar] [CrossRef]

- Salehi, M.; DashtBayaz, M.L.; Khorashadizadeh, S. Corporate social responsibility and future financial performance: Evidence from Tehran Stock Exchange. EuroMed J. Bus. 2018, 13, 351–371. [Google Scholar] [CrossRef]

- Sisaye, S. The influence of non-governmental organizations (NGOs) on the development of voluntary sustainability accounting reporting rules. J. Bus. Socio-Econ. Dev. 2021, 1, 5–23. [Google Scholar] [CrossRef]

- Bridges, C.M.; Harrison, J.A.; Hay, D.C. The ungreening of integrated reporting: A reflection on regulatory capture. Meditari Account. Res. 2022, 30, 597–625. [Google Scholar] [CrossRef]

- Elaigwu, M.; Abdulmalik, S.O.; Talab, H.R. Corporate integrity, external assurance and sustainability reporting quality: Evidence from the Malaysian public listed companies. Asia-Pac. J. Bus. Adm. 2024, 16, 410–440. [Google Scholar] [CrossRef]

- Maignan, I.; Ralston, D.A. Corporate social responsibility in Europe and the US: Insights from businesses’ self-presentations. J. Int. Bus. Stud. 2002, 33, 497–514. [Google Scholar] [CrossRef]

- Davis, K.; Blomstrom, R.L. Business and Society: Environment and Responsibility; McGraw-Hill: New York, NY, USA, 1975; pp. 23–45. [Google Scholar]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Sundin, H.; Brown, D.A. Greening the black box: Integrating the environment and management control systems. Account. Audit. Accoun. 2017, 30, 620–642. [Google Scholar] [CrossRef]

- Global Reporting Initiative (GRI). Integrated Reporting. Available online: https://www.globalreporting.org/information/currentpriorities/integratedreporting/Pages/default.aspx (accessed on 15 January 2023).

- Oberseder, M.; Schlegelmilch, B.B.; Murphy, P.E. CSR practices and consumer perceptions. J. Bus. Res. 2013, 66, 1839–1851. [Google Scholar] [CrossRef]

- Cheng, S.; Lin, K.Z.; Wong, W. Corporate social responsibility reporting and firm performance: Evidence from China. J. Manag. Govern. 2016, 20, 503–523. [Google Scholar] [CrossRef]

- Crane, A.; Matten, D. COVID-19 and the future of CSR research. J. Manag. Stud. 2021, 58, 280–284. [Google Scholar] [CrossRef]

- Ehnert, I.; Parsa, S.; Roper, I.; Wagner, M.; Muller-Camen, M. Reporting on sustainability and HRM: A comparative study of sustainability reporting practices by the world’s largest companies. Int. J. Hum. Resour. Manag. 2016, 27, 88–108. [Google Scholar] [CrossRef]

- Hess, D. The transparency trap: Non-financial disclosure and the responsibility of business to respect human rights. Am. Bus. Law J. 2019, 56, 5–53. [Google Scholar] [CrossRef]

- Monteiro, A.P.; García-Sánchez, I.M.; Aibar-Guzmán, B. Labour practice, decent work and human rights performance and reporting: The impact of women managers. J. Bus. Ethics 2022, 180, 523–542. [Google Scholar] [CrossRef]

- Straub, D.W. Validating instruments in MIS research. MIS Q. 1989, 13, 147–169. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Sun, Y.; Wang, J.J.; Huang, K.T. Does IFRS and GRI adoption impact the understandability of corporate reports by Chinese listed companies? Account. Financ. 2022, 62, 2879–2904. [Google Scholar] [CrossRef]

- Smith, N.C. Corporate social responsibility: Whether or how? Calif. Manage. Rev. 2003, 45, 52–76. [Google Scholar] [CrossRef]

| Country | Content | SR Practice | SR Uniqueness in China | Reference |

|---|---|---|---|---|

| US and European countries | Institutional context | The market plays a leading role in economic development, and companies have more stabilized SR-related regulation regimes. | The Chinese government plays a leading role in SR standards-setting and economic development. | Ervits (2021) [24] |

| Encourage all kinds of companies in sustainability practice | Encourage more sustainable activities in state-owned companies | See (2009) [27] | ||

| India | Communication style | Rule-based | Relation-based | Lattemann et al. (2009) [28] |

| Communication quality | Well-rounded and multi-dimensional communication on SR motives, processes, and stakeholder concerns | Limited communication on SR motives, processes, and stakeholder concerns | ||

| Japan | Assurance | Credibility assurance of SR from an independent third party | Absence of SR assurance | Yamagami and Kokubu (1991) [30]; Haider and Kokubu (2015) [31] |

| Dimensions | Description | Sample Sustainable Activity |

|---|---|---|

| Environment | Activities that specify the long-term sustainable impact of a company’s operations on climate and natural resources | Established photovoltaic power generation equipment to reduce carbon dioxide emissions (600019.SH in the materials industry) |

| Economic | Activities that describe a company’s economic value generated and distributed, financial implications, and financial assistance | Increased tax payment per share (600104.SH in the automobiles and components industry) |

| Society | Activities that indicate how a company affects areas and people locally, nationally, and globally | Donated 168 billion RMB to poverty-stricken areas in Guangxi and Gansu Provinces (601766.SH in the capital goods industry) |

| Consumer | Activities that describe how a company improves consumer experience | Encouraged internet-based instead of paper-based form filling to shorten the waiting time of consumers (600050.SH in the telecommunication services industry) |

| LA&HR | Activities that indicate how a company protects employees’ human rights and improves employee satisfaction | Provided 245 h of training for employees (601828.SH in the retail industry) |

| GOR | Activities that describe how a company identifies and avoids risks | Increased the proportion of independent directors in the performance evaluation commission and auditing commission (600383.SH in the real estate industry) |

| Number | Percentage | |

|---|---|---|

| Age: | ||

| 18–25 | 207 | 50.6% |

| 25–35 | 89 | 21.8% |

| 36–45 | 58 | 14.2% |

| above 45 | 55 | 13.4% |

| Gender: | ||

| Male | 143 | 35.0% |

| Female | 266 | 65.0% |

| Specialty: | ||

| Management | 219 | 53.5% |

| Economics | 70 | 17.1% |

| Engineering | 49 | 12.0% |

| Education | 27 | 6.6% |

| Computer science | 17 | 4.2% |

| Medicine | 11 | 2.7% |

| Others | 16 | 3.9% |

| Income: | ||

| Under 50,000 RMB | 178 | 43.5% |

| 50,000–100,000 RMB | 74 | 18.1% |

| 100,001–200,000 RMB | 75 | 18.3% |

| 200,001–300,000 RMB | 47 | 11.5% |

| Above 300,000 RMB | 35 | 8.6% |

| Education: | ||

| Below high school | 8 | 2.0% |

| Associate | 28 | 6.8% |

| Bachelor’s | 293 | 71.6% |

| Master’s and above | 80 | 19.6% |

| Region: | ||

| Eastern China | 344 | 84.1% |

| Northwest | 41 | 10.0% |

| Northern China | 11 | 2.7% |

| Southern China | 8 | 2.0% |

| Central China | 3 | 0.7% |

| Others | 2 | 0.5% |

| Factor | Mean | Std. Dev. | Cronbach’s Alpha | Item Number |

|---|---|---|---|---|

| Factor 1: Environment | 4.64 | 0.67 | 0.91 | 9 |

| Factor 2: Economic | 4.52 | 0.74 | 0.79 | 4 |

| Factor 3: Society | 4.46 | 0.75 | 0.94 | 9 |

| Factor 4: Consumer | 4.65 | 0.62 | 0.87 | 5 |

| Factor 5: LA&HR | 4.59 | 0.68 | 0.93 | 11 |

| Factor 6: GOR | 4.66 | 0.60 | 0.89 | 5 |

| Total | 0.973 | 43 |

| Environment | Economic | Society | Consumer | LA&HR | GOR | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Std. Dev. | Mean | Std. Dev. | Mean | Std. Dev. | Mean | Std. Dev. | Mean | Std. Dev. | Mean | Std. Dev. | ||

| Cluster | Sustainability forerunners | 4.94 | 0.14 | 4.85 | 0.32 | 4.88 | 0.25 | 4.96 | 0.14 | 4.93 | 0.14 | 4.96 | 0.14 |

| Sustainability supporters | 4.81 | 0.31 | 4.69 | 0.43 | 4.64 | 0.46 | 4.87 | 0.24 | 4.78 | 0.31 | 4.85 | 0.27 | |

| Sustainability laggards | 4.20 | 0.56 | 4.04 | 0.58 | 3.87 | 0.52 | 4.16 | 0.52 | 4.08 | 0.51 | 4.19 | 0.53 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xu, L.; Xie, L.; Mei, S.; Hao, J.; Zhang, Y.; Song, Y. Corporate Sustainability Reporting and Stakeholders’ Interests: Evidence from China. Sustainability 2024, 16, 3443. https://doi.org/10.3390/su16083443

Xu L, Xie L, Mei S, Hao J, Zhang Y, Song Y. Corporate Sustainability Reporting and Stakeholders’ Interests: Evidence from China. Sustainability. 2024; 16(8):3443. https://doi.org/10.3390/su16083443

Chicago/Turabian StyleXu, Lu, Li Xie, Shengjun Mei, Jianli Hao, Yuqian Zhang, and Yu Song. 2024. "Corporate Sustainability Reporting and Stakeholders’ Interests: Evidence from China" Sustainability 16, no. 8: 3443. https://doi.org/10.3390/su16083443

APA StyleXu, L., Xie, L., Mei, S., Hao, J., Zhang, Y., & Song, Y. (2024). Corporate Sustainability Reporting and Stakeholders’ Interests: Evidence from China. Sustainability, 16(8), 3443. https://doi.org/10.3390/su16083443