A New Philosophy for the Development of Regional Energy Planning Schemes

Abstract

:1. Introduction

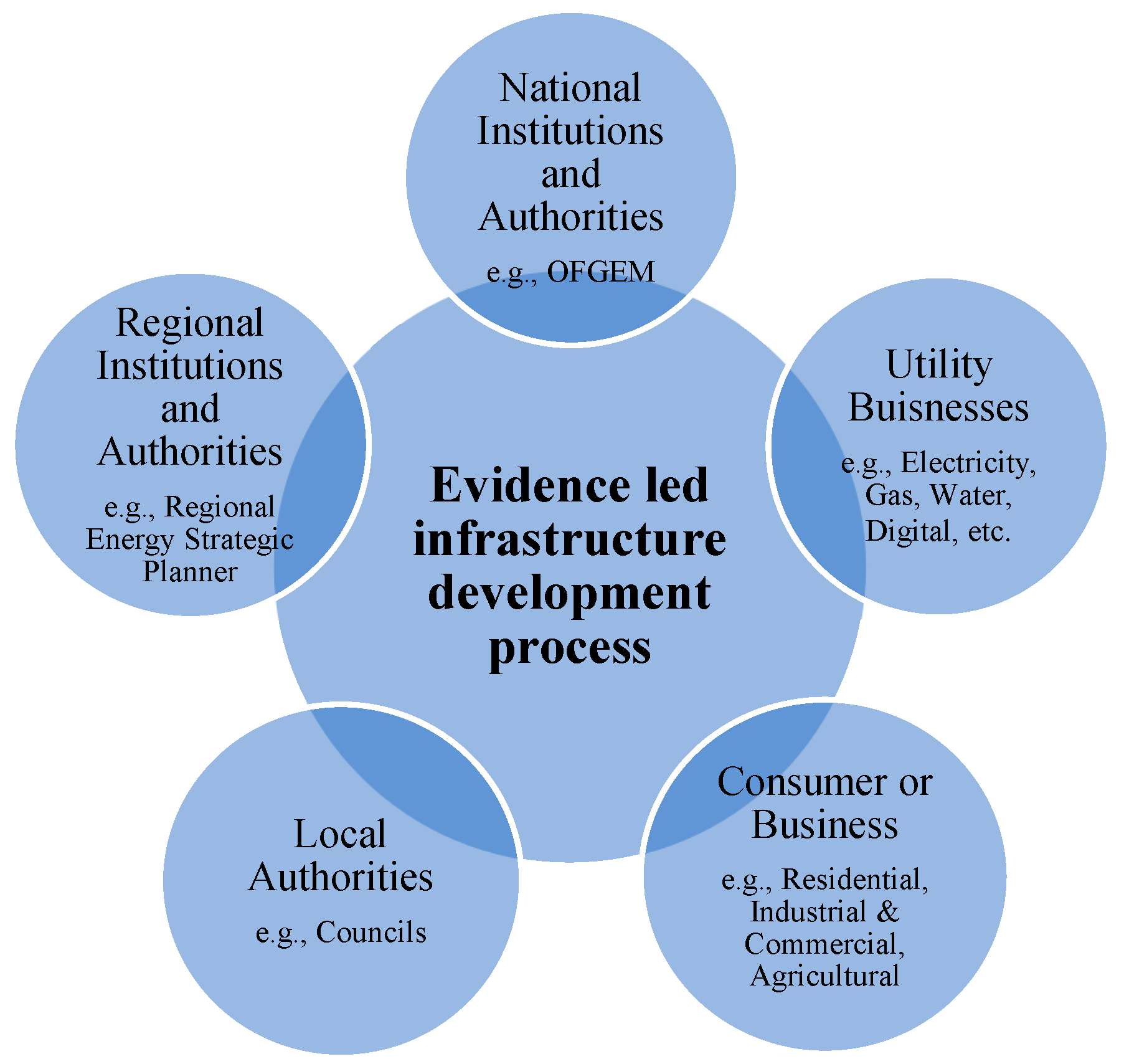

1.1. Energy Planning Framework in the UK

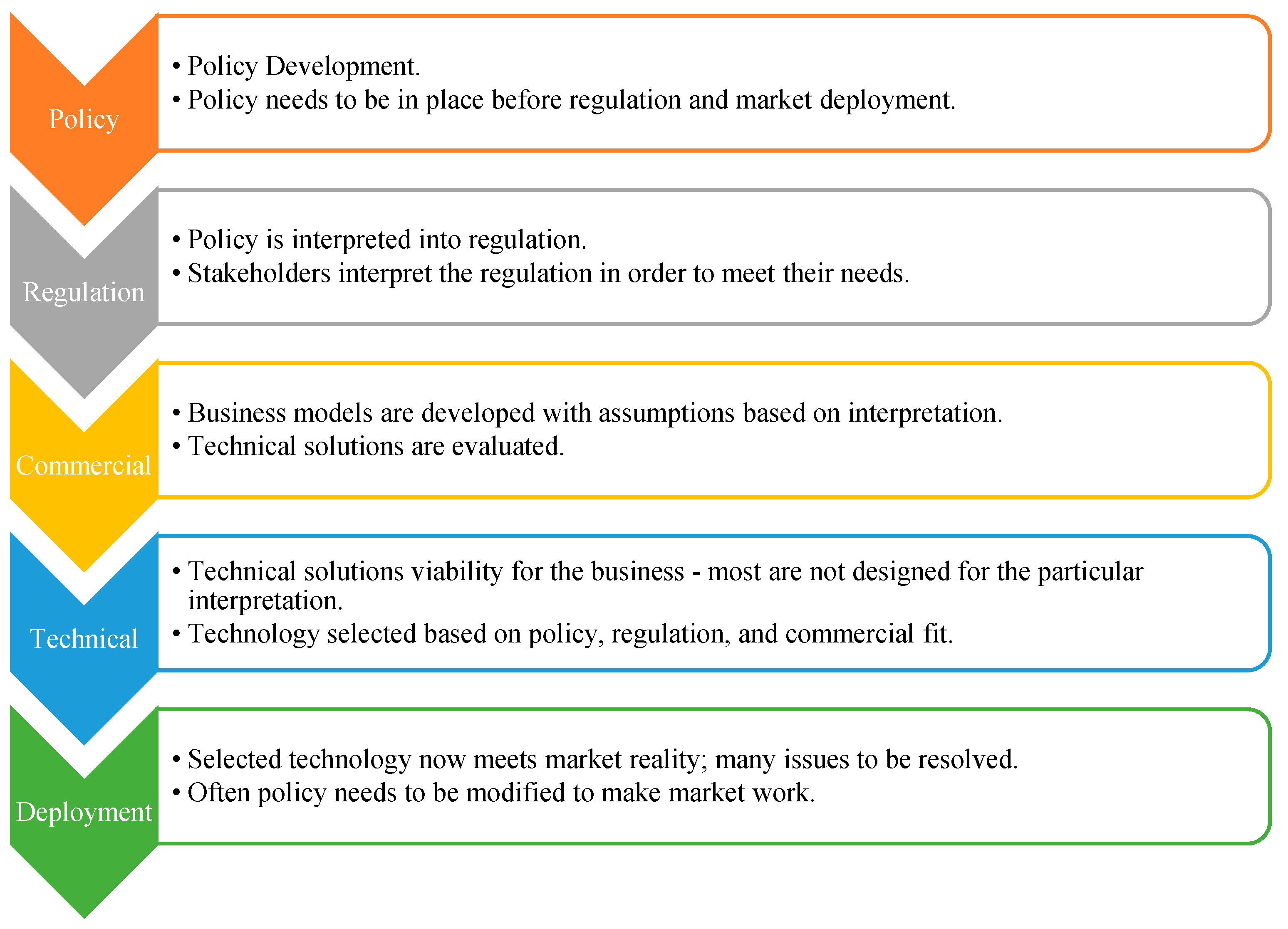

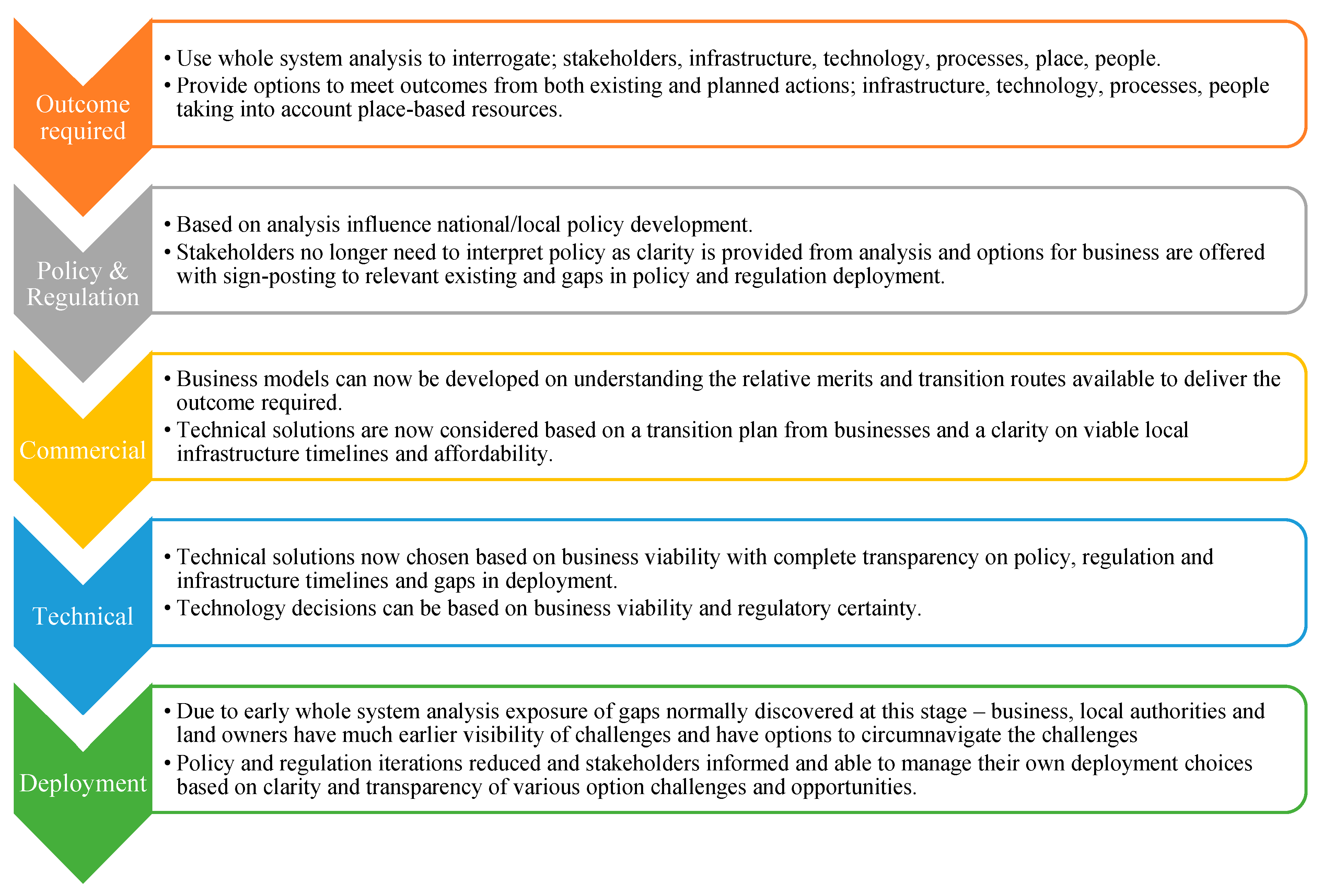

- (i)

- Policy development: Policies are developed with ambitions to meet organisational goals and market requirements under a set of external conditions affecting the organisation.

- (ii)

- Interpretation of policy into regulation: A well-defined policy is then incorporated into regulation, which is a framework intended to deliver the outlined requirements for organisations and businesses to deliver the desired outcomes defined by the policy intent.

- (iii)

- Developing commercial or business plans: Business models for organisations are developed based on the predetermined policy, regulations, infrastructure availability, and other external conditions. Under these conditions, business models assess technical solutions to match the needs of targeted market segments that may belong to one or many types of the organisations depicted in Figure 1, depending on the business goals.

- (iv)

- Implementing technical solutions: Technical solutions are chosen under the umbrella of defined policy and regulations and foresight of infrastructure availability to ensure a commercial fit for meeting anticipated market needs. Solutions with regulatory uncertainty, foreseeable infrastructure deficits, and risks of losing market competitiveness are not often considered in the short and medium terms.

- (v)

- Deployment of solutions: Deployment of the technical solutions to meet market needs could face a range of problems arising from unclear policy, delay in regulatory framework development, overestimation or underestimation of infrastructure deployment and market needs, etc. The identified market barriers might then lead to the development of organisational policies, and hence, repeating the process over the planning horizons of the participating organisations.

1.2. Deficiencies in the Existing Energy Planning Framework

1.3. Essential Components of Local Area Energy Planning Framework to Support Regulated Infrastructure Deployment

- (i)

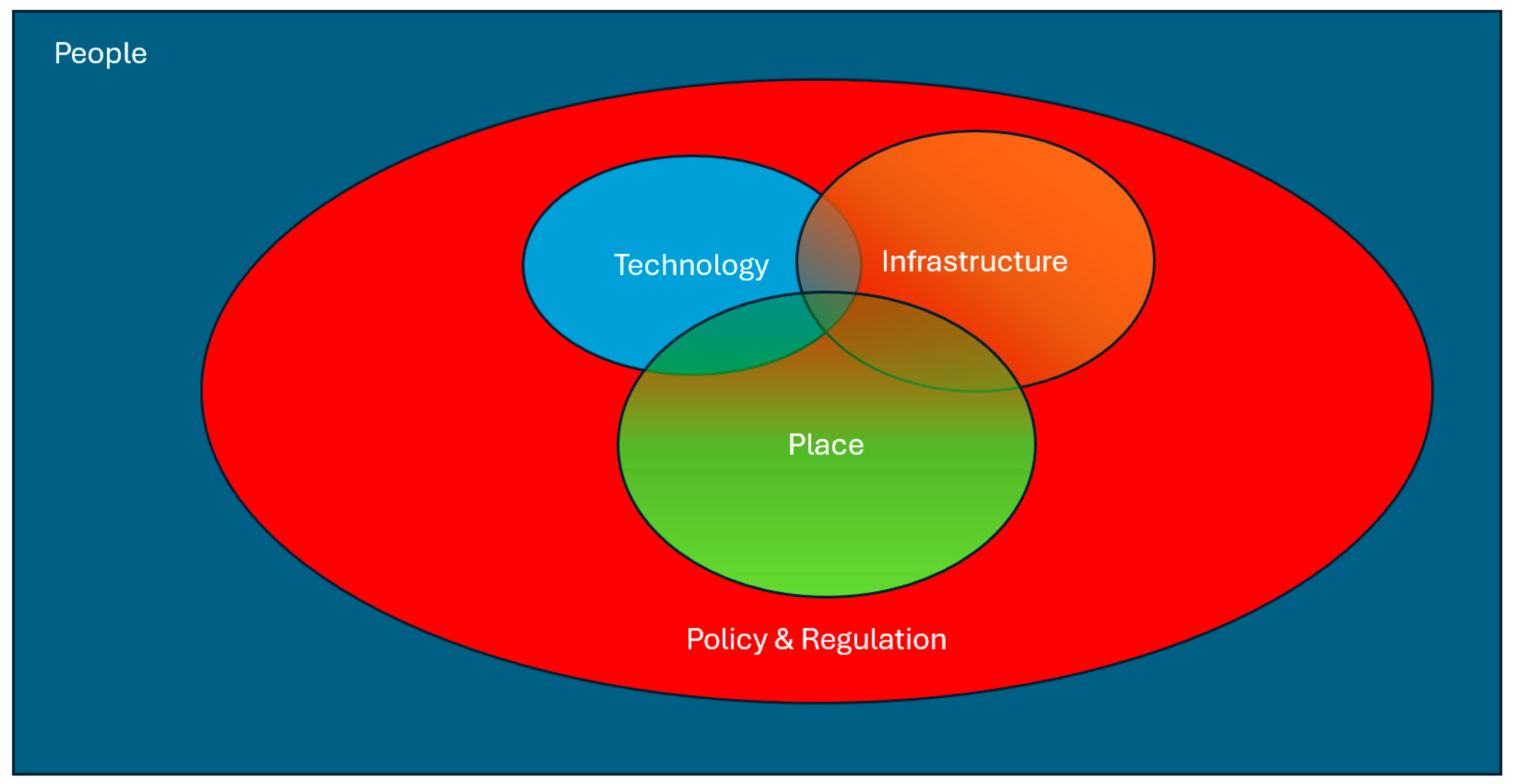

- Capturing Whole System interactions: Developing a Local Area Energy Plan to support infrastructure deployment requires addressing the interdependencies between various Whole System tiers (subsystems); here segregated into (i) Policy and Regulations, (ii) Infrastructure, (iii) Technology, (iv) Place, and (v) People. By systematically assessing these tiers in a hierarchical manner, the proposed methodology results in a cohesive strategic approach leading to effective business planning and timely infrastructure deployment. Nevertheless, complexity arises due to the high interdependency of these tiers and requires iterative feedback to be designed into the methodology, as exemplified below:Policy and Regulations: They are naturally influenced by alignment with other policies: for instance, to accrue the benefits of smart meter deployment, appropriate policies are required to give consumers some control over how their data are shared, processed, and managed [31].

- Infrastructure: Deficiencies lead to the identification of required policy interventions to accelerate and support infrastructure development projects (e.g., Contracts for Difference [32] and Rapid Decarbonisation Fund).

- Technology: Lower market availability and developmental gaps result in the design of appropriate regulations or policy support schemes (e.g., zero emission vehicle mandate; innovation funds).

- People: Evidence of the slow adoption of, or resistance to, technologies (e.g., heat pumps, hydrogen for domestic heating) is one of the inputs for allocating budget or making critical policy decisions.

Infrastructure: Other infrastructure businesses often influence these, for instance, the return on investment in energy generation projects depends on the ability of regional transmission lines to provide connections on time.- Policies and regulations: OFGEM price controls for transmission network operators (TNOs), DNOs, and national energy system operator (NESO) regulate businesses to enable fund allocations to infrastructure development and maintenance (including digital technologies).

- Technology: New technology may increase or decrease the load on networks and require development/installation of new networks, built environments, and digital infrastructure.

- Place: Certainty in regional preferences for particular technologies (e.g., based on the availability of natural resources and environment) and the magnitude of the associated infrastructure requirements support business cases for upgrading or developing regional infrastructure.

- People: Multidisciplinary skills and cross/up-skilling are required to support future infrastructure demands, adapt to changing business practises, and innovation to support prompt infrastructure delivery.

Technology: The deployment of a technology depends on supporting technologies; for instance, the effective operation of alternate fuel vehicles requires technology deployment to dispense the fuels [35].- Policies and regulations: Certainty of policy to phase out technologies drives investments made by original equipment manufacturers (OEMs) (e.g., non-zero emission vehicles [36]).

- Place: Regional resources play a significant role in the capability of a technology to perform (e.g., incident solar radiation at a location).

Place: Inward investment to facilitate economic growth and decarbonise the region is often influenced by investments that compete for the same place-based resources (e.g., land, water, feedstock, geographical formations [pumped hydro], aquifers, etc.).- Infrastructure: Locations where gas networks would be retained, repurposed, or dismantled [44] and locations with sufficient provision of electric capacity affects regional growth.

- Technology: Timely availability of technology and its capability to contribute to meeting place-based objectives, is one of the key factors influencing regional priorities (e.g., hydrogen fuel cell vehicles (H2-FCEVs) versus BEVs infrastructure and supply chains).

- People: Participation in consultations for planning consents and challenges from regional economic/skill disparity play important roles in making decisions on place-based resource allocation and innovations.

People: Decision-makers are influenced by common perspectives of communities and groups (e.g., Citizen’s advice).- Policies: Incentives and regulations (e.g., boiler upgrade scheme [29], phasing out of gas boilers) drive decisions taken by people.

- Infrastructure: Availability, reliability, and resilience of infrastructure to support people’s goals is vital to selecting appropriate solutions.

- Technology: Operational challenges, cost of upgrading, and re-skilling to ensure commercial competitiveness, and anticipated cost benefits will influence business or domestic budget allocations.

- Place: Availability of resources at a place (e.g., natural resources) is a vital attribute for decision-making.

- (ii)

- Addressing all energy and related vectors: Around 40% of the electricity requirements in the UK were met by natural gas in 2022 [45]. While electrification will increase demand on networks, adopting alternative fuels will also require a transformation of existing supply chains. Production and transport of alternative fuels (biofuels and efuels, including hydrogen) or heat (for heat networks) will increase the load on existing networks and/or require new networks. Furthermore, assessing viable feedstock for energy conversion, digital systems, water resources, etc., is crucial to developing a holistic strategy.

- (iii)

- Innovative circular economic processes: Identifying and promoting innovative circular economic processes to promote commercial competitiveness whilst ensuring resource efficiency is crucial for the optimal use of available resources in a place. Careful consideration is required for circular economic processes for electricity (e.g., V2G), heat (e.g., data centres), resources converted to energy (e.g., biomethane), and resources not converted to energy but needed as part of the solution (e.g., SF6 regeneration [46]), etc.

- (iv)

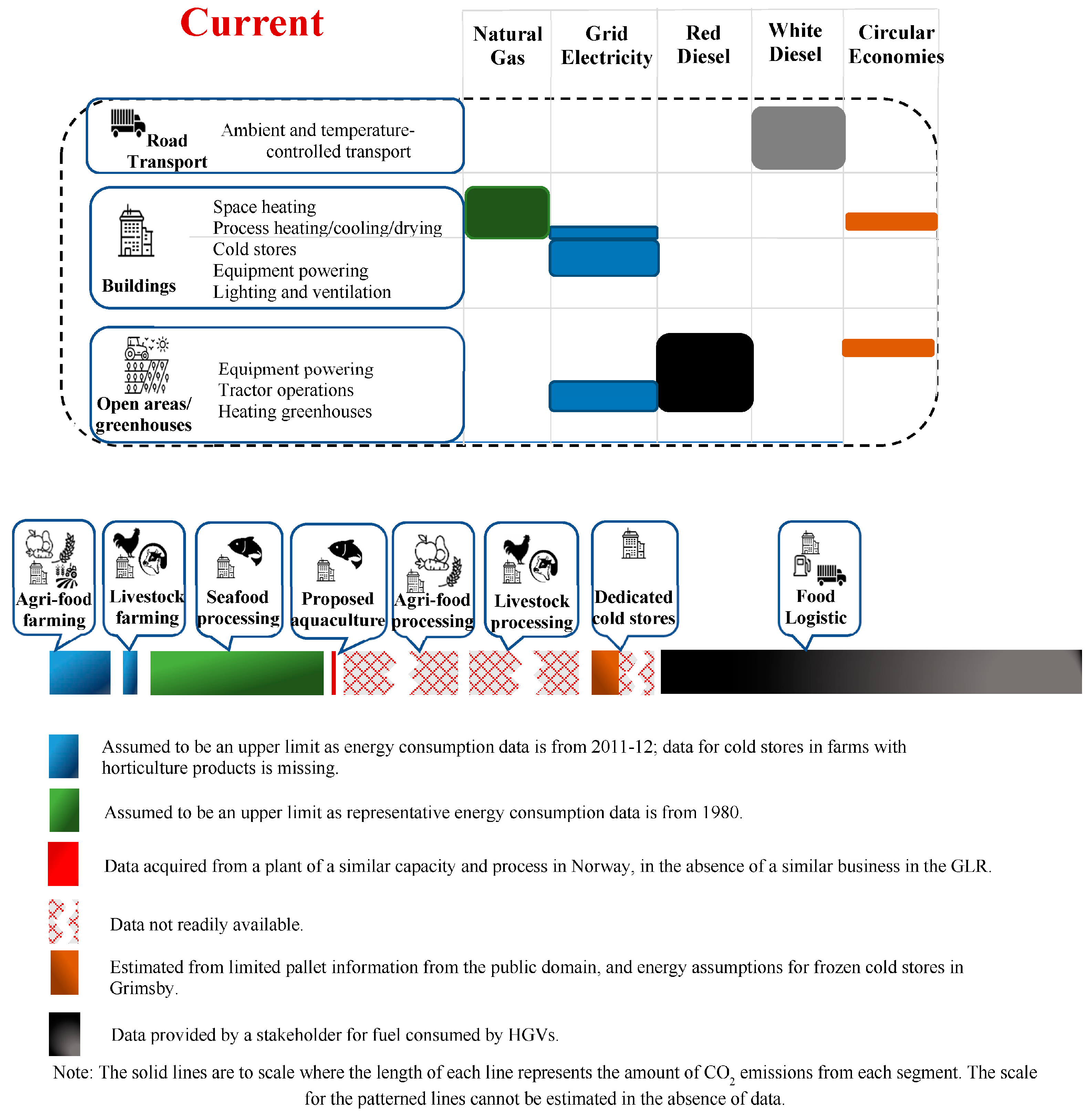

- Market segmentation: Appraising technical solutions depends on transitional (e.g., installation) and capital (e.g., boiler) costs, incentives, regulatory restrictions, energy infrastructure, and built environment at the desired location, performance, and market availability of technology, and the skills available. The relative importance of these factors depends on whether a candidate technology is used for residential, industrial, commercial, or agricultural purposes. This requires streamlined decisions related to policy, infrastructure, place, and technology to drive decarbonised heating, cooling, power, transport, and a necessary digital transformation for different market segments whilst realising the benefits of interfacing with other segments.

- (v)

- Decision support for the Whole System: Monitoring the energy requirements and external conditions helps energy consumers [47], utility companies, and authorities identify where interventions are needed. Energy planning tools [48,49] help these organisations and stakeholders to identify the required interventions. A realistic monitoring tool combined with informative signposting and knowledge sharing processes can facilitate the development and propagation of coherent assumptions. With timely and synergistic decisions made across the Whole Systems in the right direction, accelerated infrastructure deployment can be achieved while ensuring an affordable and viable outcome for people and place.

- (vi)

- Spatio-temporal visualisation: It is crucial to visualise the transition of Whole System tiers in a spatio-temporal manner to ensure that actions are taken at the right place and time (prioritising). Monitoring progress on a spatial plane helps reduce issues caused by regional inequalities, while the temporal view justifies the timescales for processes, as indicated in Figure 2.

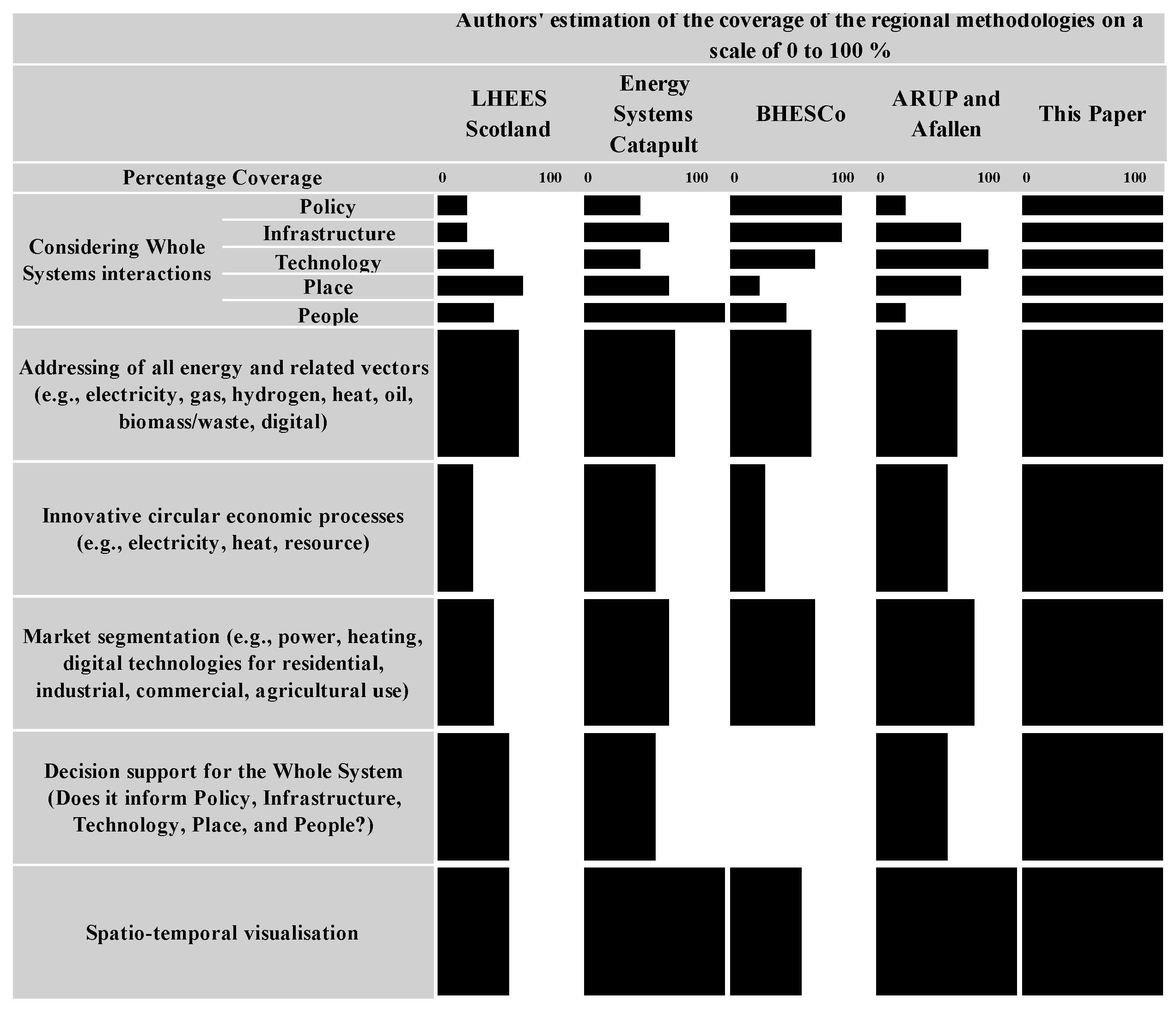

1.4. Assessment of Current Regional Energy Planning Methodologies and Gaps in Knowledge

- (i)

- Whole System interactions

- (ii)

- Addressing all energy and associated vectors

- (iii)

- Innovative circular economic processes

- (iv)

- Market segmentation

- (v)

- Decision support for the Whole System

- (vi)

- Spatio-temporal visualisation

2. Scope of Study for Developing a “Whole Systems”: LAEP Approach

3. “Whole Systems” Approach—Identifying the Decarbonisation Challenge

3.1. Step 0: Iterative Processes

3.1.1. Online Research

3.1.2. Stakeholder Engagement

3.1.3. Review Panel Feedback

3.2. Step 1: Identify Business Segments and Key Challenges

3.3. Step 2: Prepare and Distribute Surveys

3.4. Step 3: Analyse Outcomes

3.5. Step 4: Estimate Segment-Wise Usage and Wastage of Energy and Related Vectors

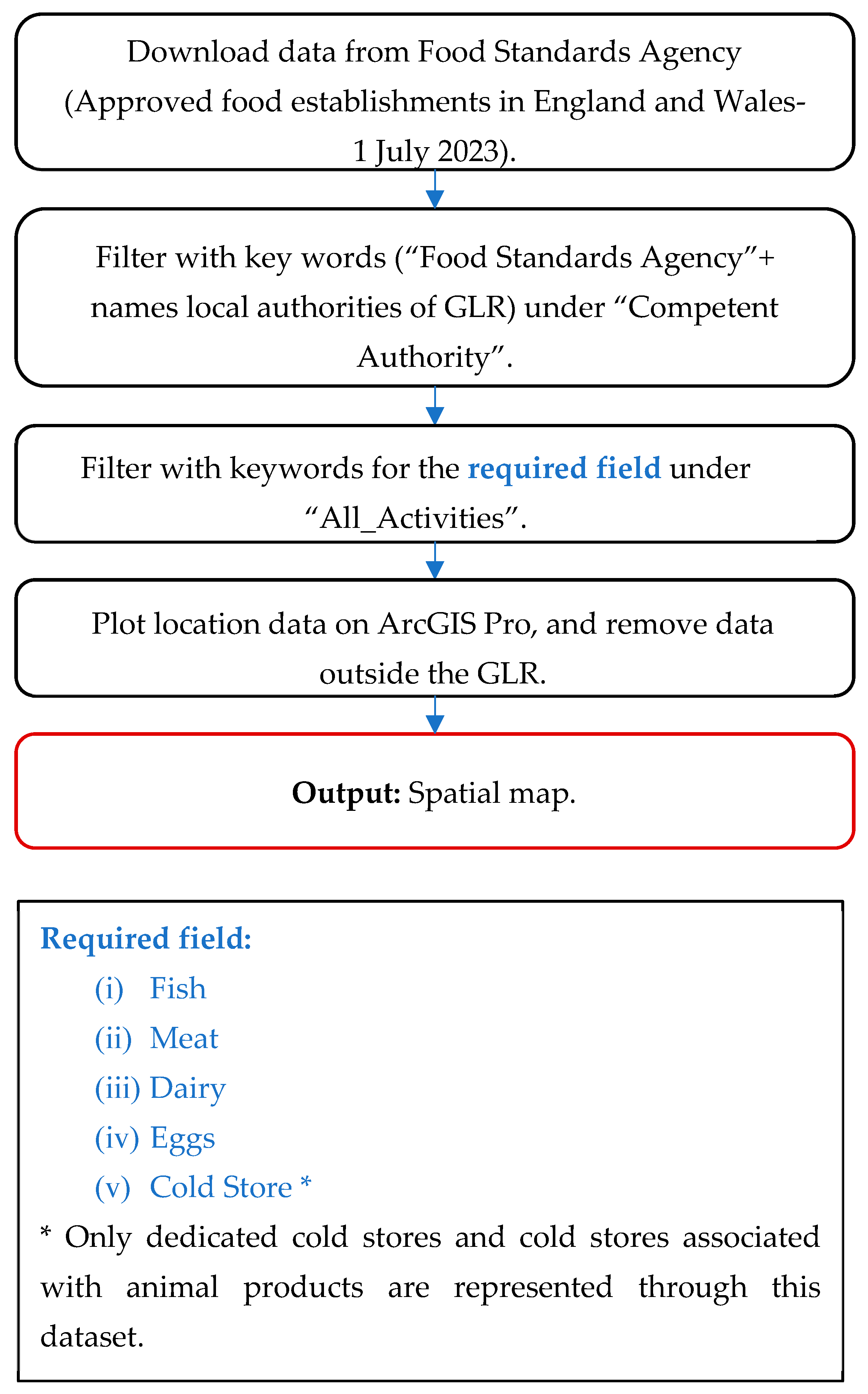

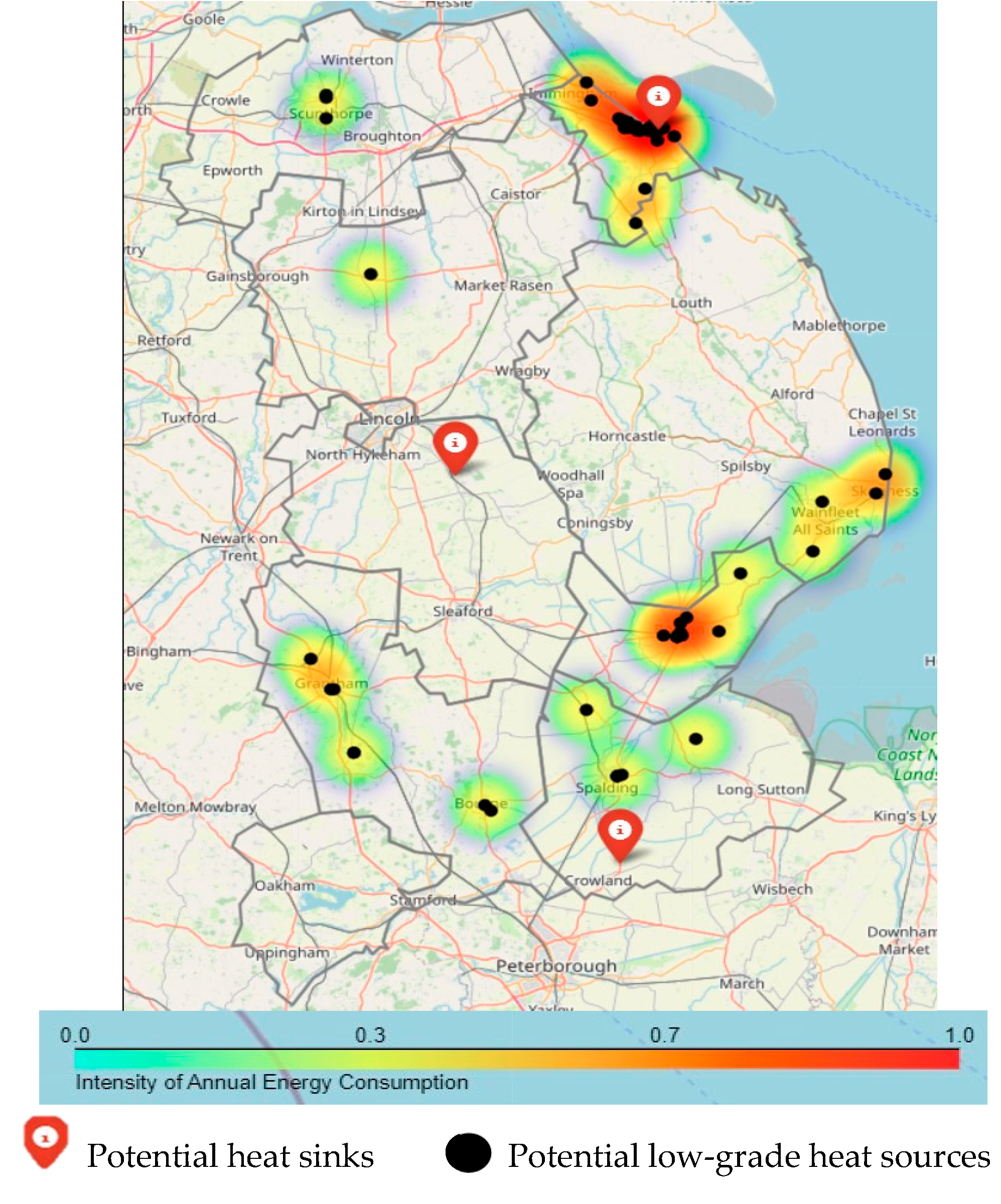

3.5.1. Spatial Map Generation for Business Segments

3.5.2. Modelling Segment-Wise Usage of Energy and Related Vectors

3.5.3. Modelling Segment-Wise Wastage of Energy and Related Vectors

Electricity

Heat (Low-Grade)

Resources That May Be Converted to Provide Energy (Biomass and Waste)

Resources That May Not Be Converted to Energy (Empty Load)

3.6. Step 5: Identify the Decarbonisation Challenge

- People

- Based on the feedback from the review panel and interaction with relevant stakeholders, there are ongoing projects to collect data for energy consumption in the food processing businesses and cold stores. However, the data might not be publicly available due to data sharing agreement constraints. Also, it has been noticed that:

- ○

- Businesses are reluctant to share data without clearly visible benefits.

- ○

- Increasing energy costs had posed threats to around 100,000 small businesses in the UK [84], and many were finding it challenging to pay their energy bills.

- Place

- Interaction with relevant stakeholders indicated their interest in co-locating with other businesses to reduce energy wastage. However, the lack of knowledge about other businesses’ willingness to participate again impedes a valuable opportunity for reaping the benefits of circular economies.

- There are numerous initiatives for reducing food waste [85] and technological developments in processes to convert food and commercial waste to products of high economic value as waste-to-energy conversion is at the bottom of the waste hierarchy [86]. According to stakeholders, any decision to invest in waste-to-energy conversion projects must be supported with information about the availability of waste that cannot be utilised in a more commercially attractive way.

- Technology

- Adopting hydrogen-based tractors [87] and other technologies will depend on the future infrastructure and supply chain capabilities.

- Electrification needs to be supported by sufficient grid capacity.

- The current economic crisis impedes investment in higher initial cost decarbonisation technologies despite their long-term cost and environmental benefits.

- Infrastructure

- The lack of digital infrastructure to enable smart energy systems is a barrier to regional efficiency enhancement techniques (e.g., demand-side management).

- The current lack of evidence-based data for the timelines of alternative fuel infrastructures can be prohibitive for businesses that would otherwise positively embrace decarbonisation technologies and upskilling programmes.

- Policy/Regulations

- The Green Gas Support Scheme may result in new biomethane-to-grid connections. It is believed that the anaerobic digestor’s combined heat and power systems are optimised to meet the heating and power requirements at the site and biomethane for the grid. Such incentives tend to drive investments to achieve benefits by exporting energy, potentially increasing resource inefficiency.

- There are inefficiencies due to a lack of coherent policies. For example, The Green Gas Support Scheme [88] and Renewable Transport Fuel Obligations [89] are progressing towards reducing the percentage of agricultural crop feedstocks. However, the Boiler Upgrade Scheme [29] incentivises biomass boilers, which may use non-sustainable feedstocks [90].

4. “Whole Systems” Approach—Overcoming the Decarbonisation Challenge

4.1. Step 6: Outline the Whole Systems Requirements

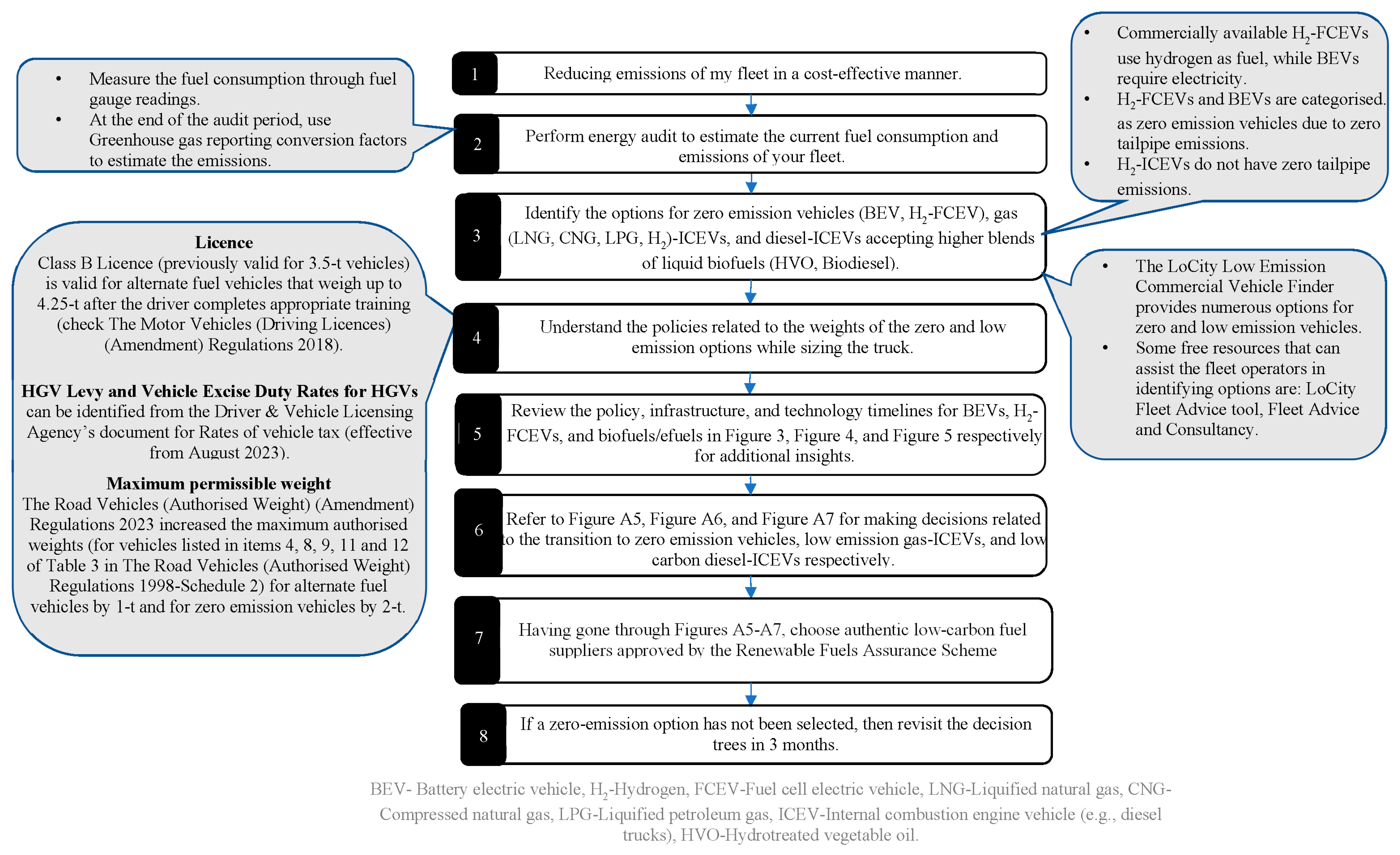

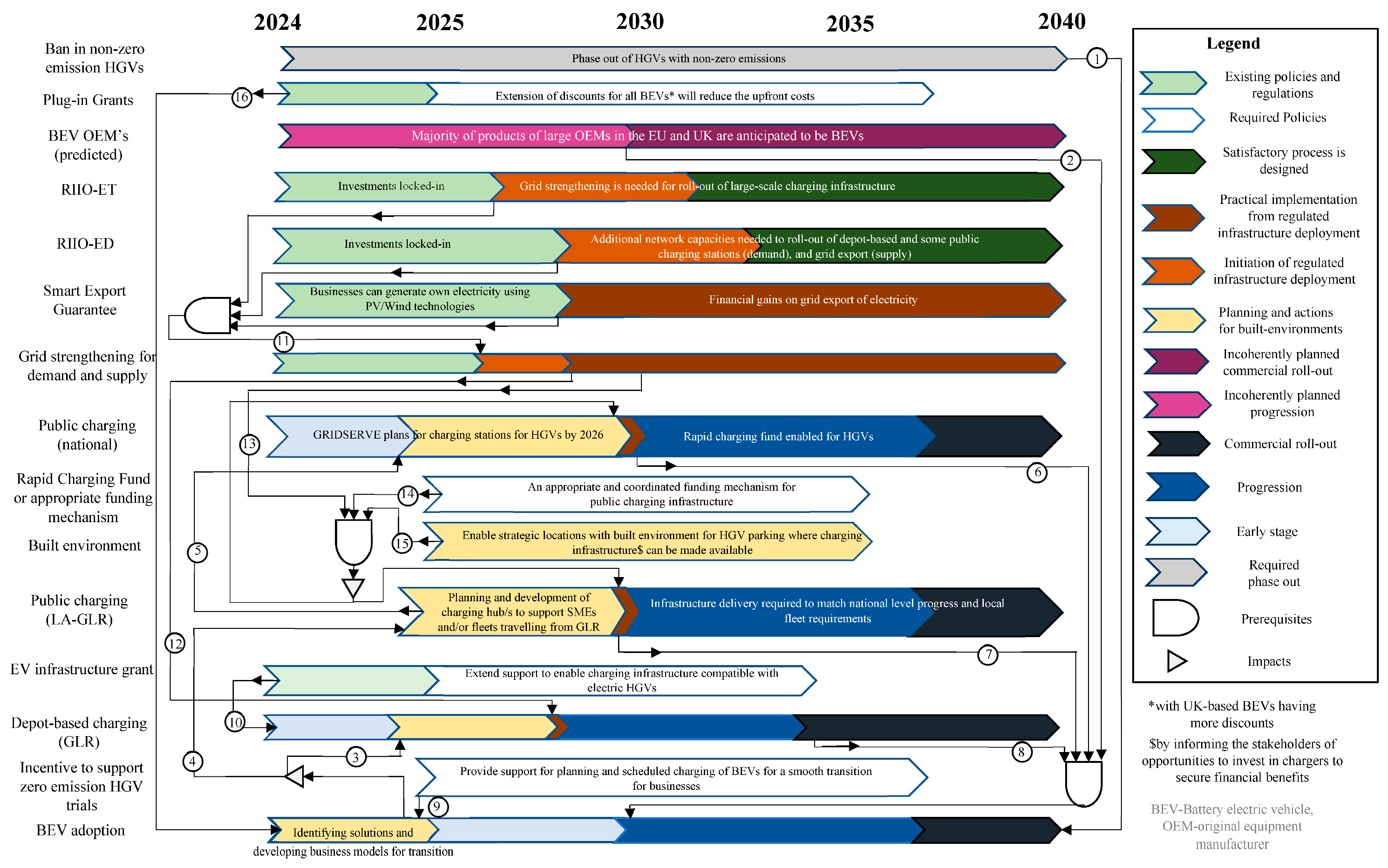

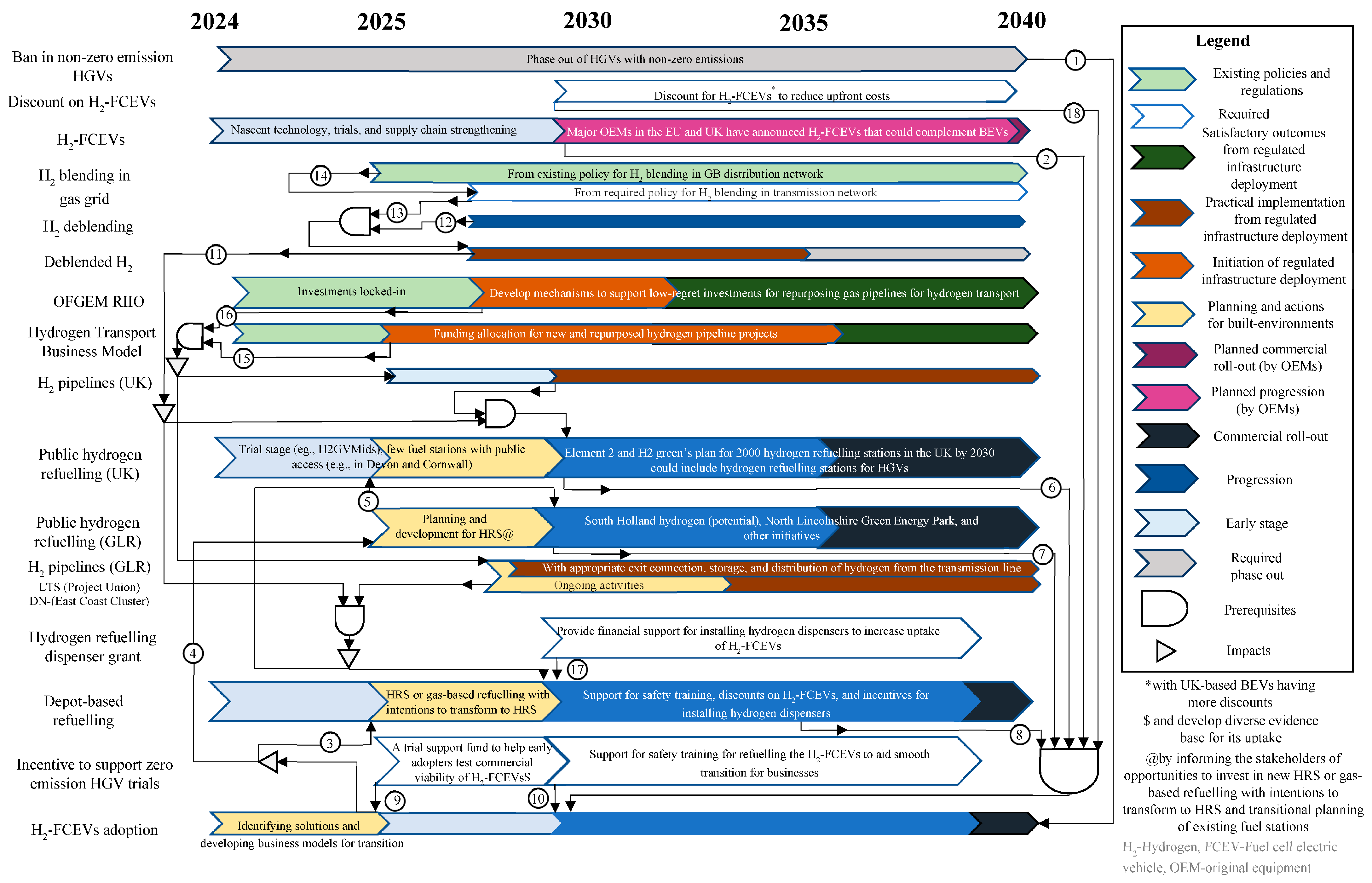

4.2. Step 7: Generate Timelines to Visualise Whole Systems Interactions

- Technology

- Infrastructure at Place

- Policy and Regulation

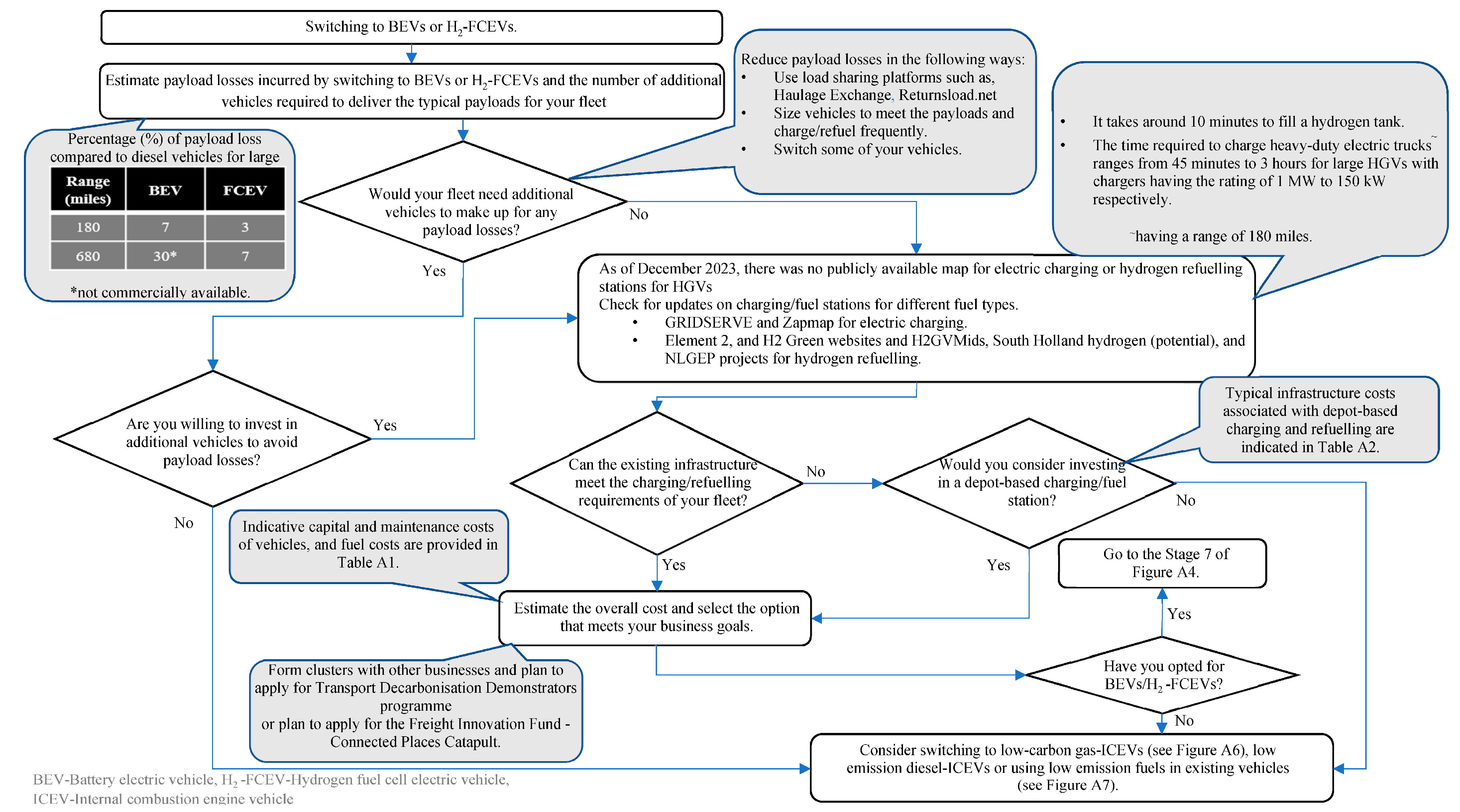

- BEVs

- H2-FCEVs

- Low-carbon-ICEVs

4.3. Step 8: Development of Decision Support Tools for Whole Systems

5. “Whole Systems” LAEP Approach for Strategic Planning—A Way Forward

5.1. Step 9: People Analysis: Stakeholder Engagement

- Social acceptability of technologies and infrastructure.

- Preferences in adopting a particular solution.

- Requirements for upskilling and cross-training the workforce.

- Willingness to participate in circular economic and skill development processes.

5.2. Step 10: Place Analysis: Stakeholder Engagement

- How does place affect specific choices?

- Viable options for imparting circular economies and other innovative place-based solutions.

- Regional resources and infrastructure capable of supporting technologies.

- Identification of strategic locations for built environments.

5.3. Step 11: Technology Analysis: Stakeholder Engagement

- Barriers and required interventions to support regional technology requirements.

- Innovations and seed funding opportunities.

- Challenges with and opportunities for technology trials.

5.4. Step 12: Infrastructure Analysis: Stakeholder Engagement

- Identify infrastructure barriers and innovative approaches to reduce the gaps.

- Estimate required investments for existing infrastructure operators.

- Attract inward investment from developers (e.g., digital infrastructure).

5.5. Step 13: Policy Analysis: Stakeholder Engagement

- Identify key policy barriers and the initiatives required.

- Increase coherency and consistency in policies across the Whole Systems.

5.6. Step 14: Verification and Validation of the Whole Systems Approach

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

- 10310: Processing and preserving potatoes (Fruit and vegetable processing).

- 10320: Manufacture of fruit and vegetable juice (Fruit and vegetable processing).

- 10390: Other processing and preserving of fruit and vegetables (Fruit and vegetable processing).

- 10710: Manufacture of bread; manufacture of fresh pastry goods and cakes (Bakery).

- 10720: Manufacture of rusks and biscuits; manufacture of preserved pastry goods and cakes (Bakery).

- 10910: Manufacture of prepared feeds for farm animals (Farm feed).

- 11010: Distilling, rectifying and blending of spirits (Drinks).

- 11020: Manufacture of wine from grapes (Drinks).

- 11030: Manufacture of cider and other fruit wines (Drinks).

- 11030: Manufacture of other non-distilled fermented beverages (Drinks).

- 11050: Manufacture of beer (Drinks).

- 10821: Manufacture of cocoa and chocolate confectionery (Others).

- 10831: Tea processing (Others).

- 10832: Production of coffee and coffee substitutes (Others).

- 10840: Manufacture of condiments and seasonings (Others)

- 10850: Manufacture of prepared meals and dishes (Others).

- 10890: Manufacture of other food products (Others).

- 01410: Raising of dairy cattle (Dairy Farms).

- 01420: Raising of other cattle and buffaloes, 01450: Raising of sheep and goats (Other grazing livestock).

- 01460: Raising of swine/pigs (Pig farms).

- 01470: Raising of poultry (Poultry farms).

| Renewable or Biofuel Content ^ | Cost of Vehicle Compared to a Diesel Truck | Maintenance Costs of Vehicle | Depot Infrastructure | Typical Fuel Requirements for Heavy-Duty HGVs | Current Fuel Cost (2023) | Tailpipe Emissions (g CO2e/mile) [128] # | Well-to-Wheel Emissions (g CO2e/mile) [128] | |

|---|---|---|---|---|---|---|---|---|

| BEV | NA | 2.2 to 2.8 times higher [129] | 10% lower (batteries operate for 1000 cycles) [130] | See Table A2 | 144 kWh/100 km [130] | GBP 0.27/kWh [131] | 0 | 640 |

| FCEV | - | 2.2 times higher [129] | 10% lower (fuel cells have a life of 10,000 hours) [130] | See Table A2 for infrastructure costs of refuelling CNG, LNG, and hydrogen at depots | 9 kg/100 km [130] | GBP 15/kg [132] | 0 | 1880 [133] @ 45–5330 [134] |

| Diesel-H2 (50% H2 ^) | - | unknown | 16.5 L of diesel and 5 kg of H2/100 km ! | 770 [135] | 930 [133] @ | |||

| LNG | 0% | 1.25 times higher [136] | Up to 25% higher [136] | 57 L/100 km ! | GBP 0.6/L [137] & | 1075 | 1450 | |

| 50% | 55 L/100 km ! | 540 * | 955 | |||||

| CNG | 0% | 26 kg/100 km ! | GBP 1.2/kg [137] | 1065 | 1285 | |||

| 50% | 25 kg/100 km ! | 533 * | 765 | |||||

| Diesel-LPG (25% LPG ^) | 0% | Up to GBP 8 k to retrofit [136] | Higher by a few hundred £s per year due to service costs [136] | LPG suppliers may install infrastructure as a part of the fuel supply contract [136] | 37 L/100 km ! | GBP 0.8/L [138,139] for LPG | 1300 | 1580 |

| 25% (LPG) | 1000 * | 1295 | ||||||

| Diesel + | 0% | - | - | - | 33 L/100 km | GBP 1.5/L [140] | 1335 | 1660 |

| Biodiesel | 30% | Similar for some manufacturers [141]; up to GBP 8 k to retrofit [136] | May need frequent filter replacements [136] | Similar to diesel [136] | 34 L/100 km ! | Similar to diesel, in some cases [142] | 965 * | 1266 |

| 100% | Requires cooling equipment compared to diesel [136] | 36 L/100 km ! | 100 * | 350 | ||||

| HVO | 100% | Similar for some manufacturers [141] | Similar to diesel [136] | Might require more storage tanks than diesel [136] | 34 L/100 km ! | GBP 1.8/L [143] | 20 * | 175 |

| Fuel Type | Capacity | Capital Cost per Station (1000 GBP) | Installation Cost per Station (1000 GBP) | Operating Cost per Station per Year (1000 GBP) |

|---|---|---|---|---|

| Electricity [148] (2019) | 150 kW | 64 | 64 | 2 |

| CNG [149] (2011) | 500 kg/day | 160 | 50 | 36 |

| 1000 kg/day | 200 | 60 | 42 | |

| 2000 kg/day | 250 | 80 | 60 | |

| LNG [149] (2011) | 500 kg/day | 73 | 10 | 22 |

| 1000 kg/day | 93 | 12 | 27 | |

| 2000 kg/day | 350 | 20 | 30 | |

| Hydrogen [148] (2019) | 400 kg/day | 2565 | 100 | 106 |

| 800 kg/day | 3420 | 180 | 144 | |

| 1200 kg/day | 4275 | 180 | 178 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

References

- Sheikhzadehbaboli, P.; Pakka, V.H.; Bustamante, J.S.; Lee, S. Electricity Substation Supply Area based Data Collation and Visualization Techniques for Local Area Energy Planning: Perspectives from UK Distribution Network Datasets. In Proceedings of the 2024 IEEE International Conference on Communications, Control, and Computing Technologies for Smart Grids, SmartGridComm 2024, Oslo, Norway, 17–20 September 2024; pp. 47–52. [Google Scholar] [CrossRef]

- Liu, Z.; Zeng, M.; Zhou, H.; Gao, J. A Planning Method of Regional Integrated Energy System Based on the Energy Hub Zoning Model. IEEE Access 2021, 9, 32161–32170. [Google Scholar] [CrossRef]

- Veichtlbauer, A.; Praschl, C.; Gaisberger, L.; Steinmaurer, G.; Strasser, T.I. Toward an Effective Community Energy Management by Using a Cluster Storage. IEEE Access 2022, 10, 112286–112306. [Google Scholar] [CrossRef]

- Wang, K.; Li, H.; Maharjan, S.; Zhang, Y.; Guo, S. Green Energy Scheduling for Demand Side Management in the Smart Grid. IEEE Trans. Green Commun. Netw. 2018, 2, 596–611. [Google Scholar] [CrossRef]

- McCusker, S.; Hobbs, B.; Ji, Y. Distributed utility planning using probabilistic production costing and generalized benders decomposition. IEEE Trans. Power Syst. 2002, 17, 497–505. [Google Scholar] [CrossRef]

- Brusco, G.; Burgio, A.; Menniti, D.; Pinnarelli, A.; Sorrentino, N. Energy management system for an energy district with demand response availability. IEEE Trans. Smart Grid 2014, 5, 2385–2393. [Google Scholar] [CrossRef]

- Sabeel, K.; Short, M.; Aggarwal, G.; Eslamy, M. Integrated Operational Planning for Smart Electric Networks in Middlesbrough, UK. In Proceedings of the ICAC 2024 29th International Conference on Automation and Computing, Sunderland, UK, 28–30 August 2024. [Google Scholar] [CrossRef]

- Littlewood, S.; Jenny, S. Regional Energy Transitions in England: The Governing Role of Combined Authorities in the Decarbonisation of Heating; IIIEE: Lund, Sweden, 2021; p. 19. [Google Scholar]

- Kaxira, A. The Governance of Anaerobic Digestion in the United Kingdom: Insights from England and Scotland. Ph.D. Thesis, University of Westminster, London, UK, 2024. [Google Scholar] [CrossRef]

- Forde, J. A Decision Support Framework for Optimal Local Delivery of Zero-Carbon Housing in England. Ph.D. Thesis, Loughborough University, Loughborough, UK, 2022. [Google Scholar] [CrossRef]

- Bale, C.S.; Foxon, T.J.; Hannon, M.J.; Gale, W.F. Strategic energy planning within local authorities in the UK: A study of the city of Leeds. Energy Policy 2012, 48, 242–251. [Google Scholar] [CrossRef]

- Local Plan Process Guide—England—Town Planning.info. Available online: https://www.townplanning.info/town-planning-in-england/development-plans/local-plan-preparation-and-process-guide/ (accessed on 19 January 2025).

- Planning Act 2008. Available online: https://www.legislation.gov.uk/ukpga/2008/29/contents (accessed on 13 January 2025).

- OFGEM. Decision on Future of Local Energy Institutions and Governance. Available online: https://www.ofgem.gov.uk/decision/decision-future-local-energy-institutions-and-governance (accessed on 9 July 2024).

- Cowell, R.; Webb, J. What do we know about the effectiveness of local energy plans? A systematic review of the research. Energy Res. Soc. Sci. 2024, 118, 103767. [Google Scholar] [CrossRef]

- The Scottish Government. Local Heat and Energy Efficiency Strategies and Delivery Plans: Guidance; Scottish Government: Edinburgh, UK, 2022. [Google Scholar]

- Local Area Energy Planning—Lowering Decarbonisation Costs. Available online: https://es.catapult.org.uk/news/local-area-energy-planning-key-to-minimising-decarbonisation-costs/ (accessed on 9 February 2025).

- Arup; Afallen. Newport City Council: Newport’s Local Area Energy Plan; Newport City Council: Newport, UK, 2022. [Google Scholar]

- Curtis, D. Partnering with The Marches LEP to Develop a Local Area Energy Plan (LAEP); BHESCo.: Brighton, UK, 2023. [Google Scholar]

- Lincolnshire County Council. Lincolnshire Freight Strategy; Lincolnshire County Council: Lincolnshire, UK, 2021. [Google Scholar]

- GRIDSERVE. GRIDSERVE to Deliver UK’s First Charging Network for Battery Electric Heavy Goods Vehicles as Part of Electric Freightway Project. Available online: https://www.gridserve.com/pressroom/gridserve-to-deliver-uks-first-charging-network-for-battery-electric-heavy-goods-vehicles-as-part-of-electric-freightway-project/ (accessed on 22 March 2024).

- Northern Gas Networks, Cadent, and National Gas. East Coast Hydrogen Delivery Plan; Cadent Gas: Coventry, UK, 2023. [Google Scholar]

- Our Transmission Network—SP Energy Networks. Available online: https://www.spenergynetworks.co.uk/pages/our_transmission_network.aspx (accessed on 13 January 2025).

- DNO—Distribution Network Operators|Energy Solutions. Available online: https://www.energybrokers.co.uk/electricity/dno-distribution-network-operators (accessed on 13 January 2025).

- Regional Energy Strategic Plan Policy Framework Consultation|Ofgem. Available online: https://www.ofgem.gov.uk/consultation/regional-energy-strategic-plan-policy-framework-consultation (accessed on 13 January 2025).

- Warbuton, E.; Mcmahon, S. Ofgem: Open Letter Regarding the Scope of the Transitional Regional Energy Strategic Plan. Available online: www.ofgem.gov.uk (accessed on 4 March 2025).

- Department for Energy Security and Net Zero. Connections Action Plan: Speeding Up Connections to the Electricity Network Across Great Britain. Available online: https://www.gov.uk/government/publications/electricity-networks-connections-action-plan (accessed on 9 July 2024).

- Department for Business, Energy and Industrial Strategy; The Rt Hon Chris Skidmore. UK Becomes First Major Economy to Pass Net Zero Emissions Law. The UK Government. Available online: https://www.gov.uk/government/news/uk-becomes-first-major-economy-to-pass-net-zero-emissions-law (accessed on 20 March 2024).

- The UK Government. The Boiler Upgrade Scheme (England and Wales) Regulations. Available online: https://www.legislation.gov.uk/uksi/2022/565/contents/made (accessed on 23 March 2024).

- Cadent. Response to Call for Evidence on the Electricity Distribution Business Plans for RIIO-2. 2022. Available online: https://www.ofgem.gov.uk/sites/default/files/2021-12/21-12-06%20RIIOED-2%20Call%20for%20Evidence%20FINAL.pdf (accessed on 9 July 2024).

- OFGEM. Data Sharing in a Digital Future: Consumer Consent Executive Summary. Available online: https://www.ofgem.gov.uk/sites/default/files/2023-11/Data%20Sharing%20in%20a%20Digital%20Future%20-%20Consumer%20Consent.pdf (accessed on 9 July 2024).

- The UK Government. Contracts for Difference. Available online: https://www.gov.uk/government/collections/contracts-for-difference (accessed on 16 April 2024).

- NHS England. NHS England Allocations: Place Based Allocation. Available online: https://www.england.nhs.uk/publication/nhs-england-allocations-place-based-allocation/ (accessed on 9 July 2024).

- The UK Government. English Devolution Accountability Framework. Available online: https://www.gov.uk/government/publications/english-devolution-accountability-framework/english-devolution-accountability-framework#annex-c-funds-for-level-2-and-level-3-areas (accessed on 9 July 2024).

- United Kingdom Petroleum Industry Association. The Future of Mobility in the UK; UKRI: London, UK, 2021. [Google Scholar]

- Department for Transport. Outcome and Response to the Consultation on When to Phase Out the Sale of New, Non-Zero Emission HGVs. The UK Government. Available online: https://www.gov.uk/government/consultations/heavy-goods-vehicles-ending-the-sale-of-new-non-zero-emission-models/outcome/outcome-and-response-to-the-consultation-on-when-to-phase-out-the-sale-of-new-non-zero-emission-hgvs (accessed on 27 March 2024).

- SMMT Media Centre. Electric and Hydrogen-Powered Trucks. Available online: https://media.smmt.co.uk/electric-and-hydrogen-powered-trucks/ (accessed on 9 July 2024).

- UK Businesses Face Delays of Up to 15 Years for Solar Installations|Solar Power|The Guardian. Available online: https://www.theguardian.com/environment/2023/may/05/uk-householders-face-delays-of-up-to-15-years-for-solar-installations (accessed on 10 February 2025).

- Klok, C.; Kirkels, A.; Alkemade, F. Alkemade. Impacts, procedural processes, and local context: Rethinking the social acceptance of wind energy projects in the Netherlands. Energy Res. Soc. Sci. 2023, 99, 103044. [Google Scholar] [CrossRef]

- ‘Hydrogen Village’ Plan in Redcar Abandoned After Local Opposition|Hydrogen Power|The Guardian. Available online: https://www.theguardian.com/environment/2023/dec/14/hydrogen-village-plan-in-redcar-abandoned-after-local-oppositiion (accessed on 16 April 2024).

- Hydrogen Pilot: Whitby Residents ‘Will Not Be Forced’ into Scheme—BBC News. Available online: https://www.bbc.co.uk/news/uk-england-merseyside-65119400 (accessed on 16 April 2024).

- PwC Green Jobs Barometer. Energy Transition Will Be Constrained by Green Skills Gap of c.200,000 Workers. Available online: https://www.pwc.co.uk/press-room/press-releases/Energy-transition-constrained-by-c200000-jobs-PwC-GJB.html (accessed on 16 April 2024).

- Department for Levelling Up, Housing, and Communities. National Planning Policy Framework. 2023. Available online: www.gov.uk/dluhc (accessed on 29 April 2024).

- Cadent. Business Plan for 2021–2026; Cadent: Coventry, UK, 2019. [Google Scholar]

- Department for Energy Security and Net Zero. Digest of UK Energy Statistics Annual Data for UK, 2022; Department for Energy Security and Net Zero: London, UK, 2023. [Google Scholar]

- Synecom. SF6 Gas Regeneration. Available online: https://www.synecom.it/en/regeneration/ (accessed on 9 July 2024).

- Muhammad, J.Y.U.; Adamu, A.A.; Alhaji, A.M.I.; Ali, Y.Y. Energy Audit and Efficiency of a Complex Building: A Comprehensive Review. Eng. Sci. 2018, 3, 36–41. [Google Scholar]

- Laveneziana, L.; Prussi, M.; Chiaramonti, D. Critical review of energy planning models for the sustainable development at company level. Energy Strat. Rev. 2023, 49, 101136. [Google Scholar] [CrossRef]

- Horak, D.; Hainoun, A.; Neugebauer, G.; Stoeglehner, G. Stoeglehner. A review of spatio-temporal urban energy system modeling for urban decarbonization strategy formulation. Renew. Sustain. Energy Rev. 2022, 162, 112426. [Google Scholar] [CrossRef]

- Energy Systems Catapult and Energy Technologies Institute. Local Area Energy Planning: Supporting Clean Growth and Low Carbon Transition; Energy Systems Catapult: Birmingham, UK, 2018. [Google Scholar]

- CENEX. An Introduction to Biofuels for Road Transport; CENEX: Loughborough, UK, 2021. [Google Scholar]

- Department for Energy Security and Net Zero; Department for Business, and Energy and Industrial Strategy. Non-Domestic National Energy Efficiency Data-Framework (ND-NEED). Available online: https://www.gov.uk/government/collections/non-domestic-national-energy-efficiency-data-framework-nd-need (accessed on 9 July 2024).

- Greater Lincolnshire Local Enterprise Partnership. Strategic Economic Plan 2014–2030. Available online: https://www.greaterlincolnshirelep.co.uk/assets/documents/Strategic_Economic_Plan_2016_Refresh.pdf (accessed on 13 January 2025).

- Rural Payments Agency. Crop Map of England (CROME) 2020. The UK Government. Available online: https://www.data.gov.uk/dataset/be5d88c9-acfb-4052-bf6b-ee9a416cfe60/crop-map-of-england-crome-2020 (accessed on 21 March 2024).

- Food Standards Agency. Approved Food Establishments in England and Wales. Available online: https://data.food.gov.uk/catalog/datasets/1e61736a-2a1a-4c6a-b8b1-e45912ebc8e3 (accessed on 21 March 2024).

- The UK Government. Advanced Company Search. Available online: https://find-and-update.company-information.service.gov.uk/advanced-search (accessed on 21 March 2024).

- ArcGIS Pro. Available online: https://pro.arcgis.com/en/pro-app/latest/get-started/download-arcgis-pro.htm (accessed on 21 March 2024).

- Department for Environment, Food, and Rural Affairs. Farm Energy Use. The UK Government. Available online: https://www.gov.uk/government/statistics/farm-energy-use (accessed on 21 March 2024).

- Department for Environment, Food, and Rural Affairs. Agricultural Land Use in England. The UK Government. Available online: https://www.gov.uk/government/statistics/agricultural-land-use-in-england (accessed on 22 March 2024).

- Jones Food Company and OECD. Company Overview; Jones Food Company: Lydney, UK, 2022. [Google Scholar]

- Georgiou, S.; Acha, S.; Shah, N.; Markides, C.N. A generic tool for quantifying the energy requirements of glasshouse food production. J. Clean. Prod. 2018, 191, 384–399. [Google Scholar] [CrossRef]

- Abundance Blog. Progress Update on Global Berry’s Nocton Site. Available online: https://medium.abundanceinvestment.com/progress-update-on-global-berrys-nocton-site-5af7497620f8 (accessed on 22 March 2024).

- Bridge Farm Horticulture. Sustainability. Available online: https://bridgefarmhorticulture.co.uk/sustainability/ (accessed on 22 March 2024).

- Team Lincolnshire. New Strawberry Variety Unlocks Year Round Production Potential. Available online: https://www.teamlincolnshire.com/news/article/193/new-strawberry-variety-unlocks-year-round-production-potential (accessed on 22 March 2024).

- AKVA Group. Tytlandsvik Aqua en Route to Full Production. Available online: https://www.akvagroup.com/news/tytlandsvik-aqua-en-route-to-full-production (accessed on 22 March 2024).

- AKVA Group. Post Smolt—Tytlandsvik Aqua Norway. Available online: https://www.akvagroup.com/land-based/turn-key-delivery/case-stories/tytlandsvik/post-smolt-tytlandsvik-aqua-norway-1 (accessed on 22 March 2024).

- Bregnballe, J. A Guide to Recirculation Aquaculture; The Food and Agriculture Organization of the United Nations: Rome, Italy, 2022. [Google Scholar] [CrossRef]

- Flogro. Sustainably Produced British Prawns. Available online: https://flogrosystems.com/ (accessed on 27 March 2024).

- Department for Levelling Up, Housing, and Communities. Greater Lincolnshire Devolution Deal; Department for Levelling Up, Housing, and Communities: London, UK, 2023. [Google Scholar]

- Seafish. UK Seafood in Numbers—2021. 2022. Available online: https://www.seafish.org/document/?id=a42c3cf8-b072-4ebe-a100-61661174a0d3 (accessed on 22 March 2024).

- The Food and Drink Federation. UK Food and Drink Regional Exports Report. Available online: https://www.fdf.org.uk/fdf/resources/publications/trade-reports/fdf-uk-food-and-drink-exports-report/ (accessed on 22 March 2024).

- Seafish. Energy in the UK Seafood Processing Sector: 2018–2020 Evidence. 2023. Available online: https://www.seafish.org/document/?id=0137560b-867b-4c0f-88a9-2e59ac26d7ac (accessed on 22 March 2024).

- Cleland, A.C.; Earle, M.D.; Boag, I.F. Application of multiple linear regression to analysis of data from factory energy surveys. Int. J. Food Sci. Technol. 1981, 16, 481–492. [Google Scholar] [CrossRef]

- Law, R.; Harvey, A.; Reay, D. Opportunities for low-grade heat recovery in the UK food processing industry. Appl. Therm. Eng. 2013, 53, 188–196. [Google Scholar] [CrossRef]

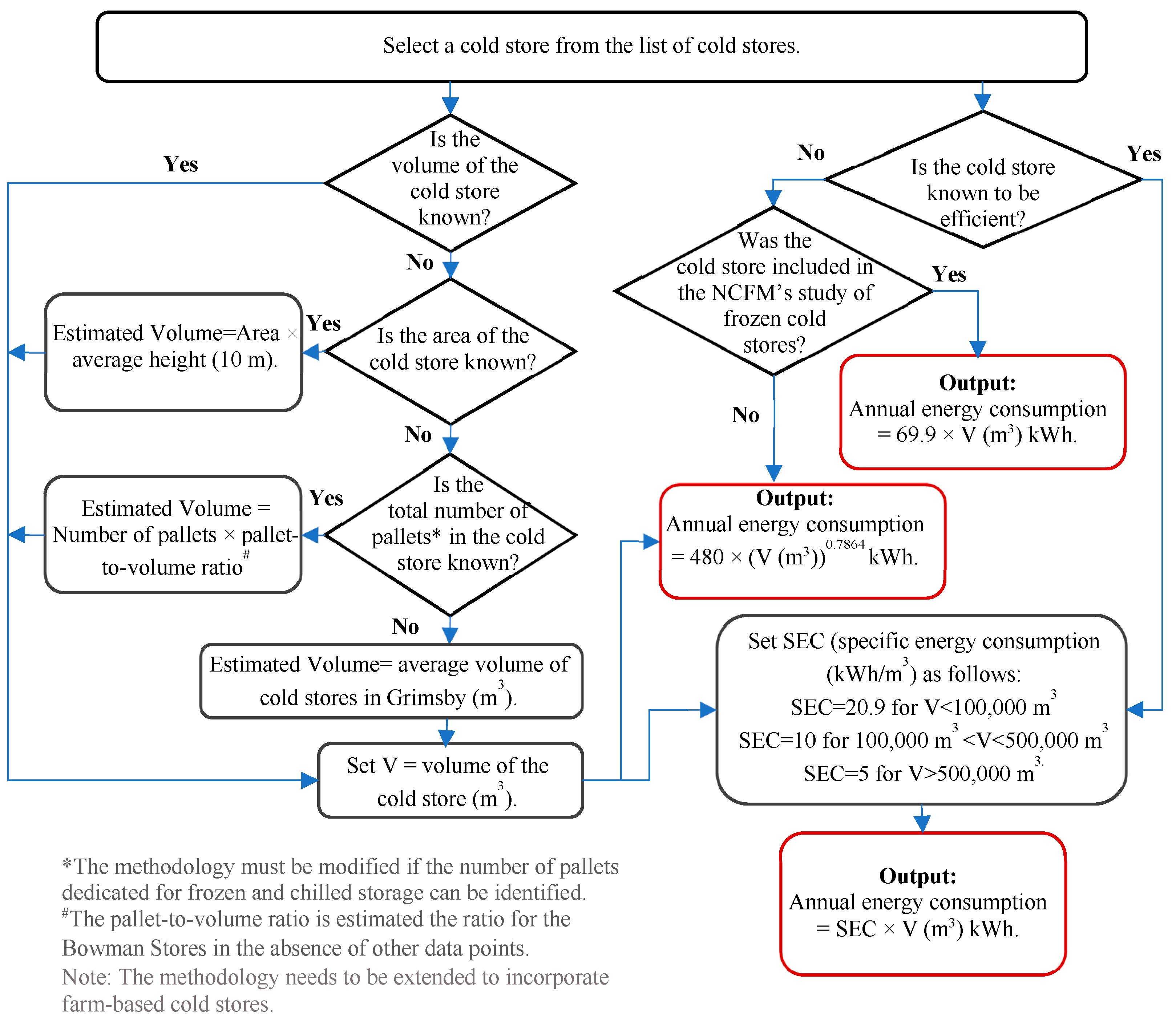

- Purnell, G.; Hammond, E.; James, C. Frozen Cold Storage Capacity in Grimsby Final Report; Grimsby Institute: Grimsby, UK, 2021. [Google Scholar]

- Americold. Cold Storage Warehouse & Supply Chain Management in Great Britain. Available online: https://www.americold.com/eu/great-britain/ (accessed on 23 March 2024).

- Cold Chain Federation. New Energy Performance ‘Best Practice’ Guidelines for Cold and Chill Refrigeration Facilities Released. 2020. Available online: https://www.coldchainfederation.org.uk/new-energy-performance-best-practice-guidelines-for-cold-and-chill-refrigeration-facilities-released/ (accessed on 22 March 2024).

- Evans, J.; Foster, A.; Huet, J.-M.; Reinholdt, L.; Fikiin, K.; Zilio, C.; Houska, M.; Landfeld, A.; Bond, C.; Scheurs, M.; et al. Specific energy consumption values for various refrigerated food cold stores. Energy Build. 2014, 74, 141–151. [Google Scholar] [CrossRef]

- National Non-Food Crops Centre. Biogas Map. The Official Information Portal on Anaerobic Digestion. Available online: https://www.biogas-info.co.uk/resources/biogas-map/ (accessed on 23 March 2024).

- Dyson Farming. Home. Available online: https://dysonfarming.com/ (accessed on 22 March 2024).

- Horton, B.; Valorising Agri-Waste. National Non-Food Crops Centre. Available online: https://www.nnfcc.co.uk/news-valorising-agri-waste (accessed on 22 March 2024).

- Zero Waste Scotland. Maximising Value from Agricultural ‘Waste’. Available online: https://www.zerowastescotland.org.uk/resources/maximising-value-agricultural-waste (accessed on 22 March 2024).

- Finger, D.C.; Saevarsdottir, G.; Svavarsson, H.G.; Björnsdóttir, B.; Arason, S.; Böhme, L. Improved Value Generation from Residual Resources in Iceland: The First Step Towards a Circular Economy. Circ. Econ. Sustain. 2021, 1, 525–543. [Google Scholar] [CrossRef]

- The Independent. Massive Energy Bill Hikes Put Hundreds of Thousands of Businesses Under Threat. Available online: https://www.independent.co.uk/news/business/energy-bills-businesses-increase-inflation-b2148644.html (accessed on 9 July 2024).

- Department for Environment, Food and Rural Affairs, and Environment Agency. Resources and Waste Strategy for England. Available online: https://www.gov.uk/government/publications/resources-and-waste-strategy-for-england (accessed on 9 July 2024).

- Department for Environment, Food, and Rural Affairs. Applying the Waste Hierarchy: Evidence Summary. Available online: https://www.gov.uk/government/publications/applying-the-waste-hierarchy-evidence-summary (accessed on 9 July 2024).

- JCB. Hydrogen-Building a Greener Future. Available online: https://www.jcb.com/en-gb/campaigns/hydrogen (accessed on 9 July 2024).

- Ofgem. Green Gas Support Scheme and Green Gas Levy. Available online: https://www.ofgem.gov.uk/environmental-and-social-schemes/green-gas-support-scheme-and-green-gas-levy (accessed on 23 March 2024).

- Department for Transport. Renewable Transport Fuel Obligation (RTFO): Compliance, Reporting and Verification. The UK Government. Available online: https://www.gov.uk/government/publications/renewable-transport-fuel-obligation-rtfo-compliance-reporting-and-verification (accessed on 22 March 2024).

- Chatham House. US-Sourced Biomass in the EU and UK: Consumption and Associated Emissions. Available online: https://www.chathamhouse.org/2021/10/greenhouse-gas-emissions-burning-us-sourced-woody-biomass-eu-and-uk/03-us-sourced-biomass (accessed on 23 March 2024).

- Statista. Leading HGV Brands in the United Kingdom. Available online: https://www.statista.com/statistics/322494/registrations-of-large-hgv-marques-in-the-united-kingdom/ (accessed on 9 July 2024).

- National Grid Group. New National Grid-Led Analysis Shows Expanding Government’s Electric Vehicle Rapid Charging Fund (RCF) Would Accelerate the Decarbonisation of All Road Transport. Available online: https://www.nationalgrid.com/new-national-grid-led-analysis-shows-expanding-governments-electric-vehicle-rapid-charging-fund-rcf (accessed on 9 July 2024).

- Department for Transport. Funding Competition: Zero Emission Road Freight—Strand 1: Electric Road Systems. The UK Government. Available online: https://apply-for-innovation-funding.service.gov.uk/competition/884/overview (accessed on 23 March 2024).

- Department for Transport. Funding Competition: Zero Emission Road Freight—Strand 2: Hydrogen Fuel Cell Vehicles. The UK Government. Available online: https://apply-for-innovation-funding.service.gov.uk/competition/885/overview (accessed on 23 March 2024).

- Department for Transport and Innovate UK. Funding Competition: Zero Emission Road Freight Battery and Hydrogen Demonstration. The UK Government. Available online: https://apply-for-innovation-funding.service.gov.uk/competition/1241/overview/30a6ba0f-ca5f-4da9-a729-d9687792ccb3 (accessed on 23 March 2024).

- Innovate UK and Department for Transport. Competition Overview—Transport Decarbonisation Demonstrators—Innovation Funding Service. The UK Government. Available online: https://apply-for-innovation-funding.service.gov.uk/competition/1790/overview/a9579ae9-74af-4f11-8caf-35c8df432365 (accessed on 23 March 2024).

- Connected Places Catapult. Freight Innovation Fund. Available online: https://cp.catapult.org.uk/programme/freight-innovation-fund/ (accessed on 23 March 2024).

- Electric Vehicle Infrastructure Grant for Staff and Fleets. Available online: https://wepoweryourcar.com/ev-infrastructure-grant-for-staff-and-fleets/ (accessed on 22 March 2024).

- The UK Government. Low-Emission Vehicles Eligible for a Plug-in Grant: Trucks. Available online: https://www.gov.uk/plug-in-vehicle-grants/trucks (accessed on 23 March 2024).

- Hydrogen Vehicle Systems. HVS Unveils UK’s First Zero-Emission Hydrogen-Electric HGV with Class-Leading 370 Mile Range. Available online: https://www.hvs.co.uk/newsroom/hvs-unveils-uks-first-zero-emission-hydrogen-electric-hgv-with-class-leading-370-mile-range (accessed on 9 July 2024).

- Energy News. UK Trio Unveils ICEBreaker Project to Transform Heavy-Duty Trucking with Hydrogen Fuel Cells. Available online: https://energynews.biz/uk-trio-unveils-icebreaker-project-to-transform-heavy-duty-trucking-with-hydrogen-fuel-cells/ (accessed on 9 July 2024).

- H2Accelerate. Whitepaper Expectations for the First Phase of the Fuel Cell Truck and Infrastructure Deployment. 2023. Available online: https://h2accelerate.eu/wp-content/uploads/2023/06/H2A-Expectations-for-the-first-phase-Final.pdf (accessed on 9 July 2024).

- National Composites Centre. UK Hydrogen Fuel Cell Electric Heavy-Duty Vehicle Supply Chain Review; National Composites Centre: Bristol, UK, 2021. [Google Scholar]

- H2Accelerate. H2Accelerate Collaboration Calls for Stronger UK Policy Framework to Support Hydrogen Trucks. Available online: https://h2accelerate.eu/h2accelerate-collaboration-calls-for-stronger-uk-policy-framework-to-support-hydrogen-trucks/ (accessed on 9 July 2024).

- Element 2. Element 2 and Tower Group Partner to Bring Hydrogen to the South West of England. Available online: https://element-2.co.uk/element-2-and-tower-group-partner-to-bring-hydrogen-to-the-south-west-of-england/ (accessed on 9 July 2024).

- H2 Green. H2 Green & Element Two. Available online: https://www.h2green.co.uk/news/h2-green-element-two/ (accessed on 23 March 2024).

- H2GVMids. Supporting the UK’s Transition to Hydrogen Powered HGVs. Available online: https://www.era.ac.uk/wp-content/uploads/2023/04/H2GVMids-supporting-the-UKs-transition-to-hydrogen-HGVs.pdf (accessed on 23 March 2024).

- Element 2. Element 2, as Part of the HyNTS Consortium, Secures Further Funding from InnovateUK to Support Real-World Trials of Hydrogen Grid De-Blending and Refuelling Technology—Element 2. Available online: https://element-2.co.uk/element-2-as-part-of-the-hynts-consortium-secures-further-funding-from-innovateuk-to-support-real-world-trials-of-hydrogen-grid-de-blending-and-refuelling-technology/ (accessed on 9 July 2024).

- National Gas. Project Union; National Gas: Coventry, UK, 2022. [Google Scholar]

- Department for Energy Security and Net Zero. Hydrogen Blending in GB Distribution Networks: Strategic Decision. Available online: https://www.gov.uk/government/publications/hydrogen-blending-in-gb-distribution-networks-strategic-decision (accessed on 22 March 2024).

- INEOS. Hydrogen Pipeline Trial. 2023. Available online: https://www.ineos.com/inch-magazine/articles/issue-24/hydrogen-pipeline-trial/ (accessed on 9 July 2024).

- HyNet North West Hydrogen Pipeline. Update—23 February 2024—HyNet North West Hydrogen Pipeline. Available online: https://www.hynethydrogenpipeline.co.uk/news-updates/23-february-2024/ (accessed on 9 July 2024).

- North Lincolnshire Green Energy Park—Flixborough Industrial Estate. Available online: https://northlincolnshiregreenenergypark.co.uk/ (accessed on 27 March 2024).

- LincsOnline. Major Plans to Bring Hydrogen Plant to South Holland. Available online: https://www.lincsonline.co.uk/spalding/news/major-new-hydrogen-plan-in-the-pipeline-9296265/ (accessed on 9 July 2024).

- Transport and Environment. Ready or Not: Who Are the Frontrunners in the Global Race to Clean Up Trucks and Gain Technology Leadership? 2023. Available online: www.transportenvironment.org (accessed on 9 July 2024).

- Zemo Partnership. Decarbonising Heavy Duty Vehicles and Machinery—Proposals for a UK Renewable Diesel Incentive. 2022. Available online: https://www.zemo.org.uk/assets/reports/Decarbonising_Heavy_Duty_Vehicles_and_Machinery_Zemo_Nov2022.pdf (accessed on 9 July 2024).

- Royal Academy of Engineering. Sustainability of Liquid Biofuels; Royal Academy of Engineering: London, UK, 2017. [Google Scholar]

- Cadent. The Future Role of Gas in Transport. Available online: https://documents.cadentgas.com/view/957927673/ (accessed on 9 July 2024).

- Fleet News. Gas Networks Set Out Net Zero Road Map for HGVs. Available online: https://www.fleetnews.co.uk/news/latest-news/2021/03/26/gas-networks-set-out-net-zero-road-map-for-hgvs (accessed on 9 July 2024).

- Gasrec. Growth Plans See Gasrec Bolster Its Supply Chain. Available online: https://www.gasrec.co.uk/blog/2023/9/21/growth-plans-see-gasrec-bolster-its-supply-chain (accessed on 23 March 2024).

- ReFuels. ReFuels Commences Construction of First Bio-CNG Refuelling Station in Southeast England. Available online: https://refuels.com/news/refuels-commences-construction-of-first-bio-cng-refuelling-station-in-southeast-england/ (accessed on 23 March 2024).

- Institution of Mechanical Engineers. The Energy Hierarchy: A Powerful Tool for Sustainability. Available online: https://www.imeche.org/news/news-article/the-energy-hierarchy-a-powerful-tool-for-sustainability (accessed on 12 March 2024).

- Department for Environment, Food, and Rural Affairs. Guidance on Applying the Waste Hierarchy. 2011. Available online: https://www.gov.uk/government/publications/guidance-on-applying-the-waste-hierarchy (accessed on 22 March 2024).

- Ricardo UK Ltd. Pathways to Industrial Heat Decarbonisation; Ricardo UK Ltd.: West Sussex, UK, 2023. [Google Scholar]

- Department for Energy Security and Net Zero; Environment Agency; Department for Business, and Energy and Industrial Strategy. Energy Savings Opportunity Scheme (ESOS). The UK Government. Available online: https://www.gov.uk/guidance/energy-savings-opportunity-scheme-esos (accessed on 22 March 2024).

- Bretter, C.; Schulz, F. Public support for decarbonization policies in the UK: Exploring regional variations and policy instruments. Clim. Policy 2023, 24, 117–137. [Google Scholar] [CrossRef]

- Companies House. Nature of business: Standard Industrial Classification (SIC) Codes. Available online: https://resources.companieshouse.gov.uk/sic/ (accessed on 10 December 2023).

- Department for Energy Security and Net Zero. Greenhouse Gas Reporting: Conversion Factors 2023. The UK Government. Available online: https://www.gov.uk/government/publications/greenhouse-gas-reporting-conversion-factors-2023 (accessed on 28 March 2024).

- Element Energy—Climate Change Committee. Analysis to Provide Costs, Efficiencies and Roll-Out Trajectories for Zero-Emission HGVs, Buses and Coaches. 2020. Available online: https://www.theccc.org.uk/publication/analysis-to-provide-costs-efficiencies-and-roll-out-trajectories-for-zero-emission-hgvs-buses-and-coaches-element-energy/ (accessed on 10 July 2024).

- SynerHy. Fuel Cells vs. Batteries—How Will Truck Fleets Decarbonise? Available online: https://synerhy.com/en/2022/03/fuel-cells-vs-batteries-how-will-truck-fleets-decarbonise/ (accessed on 10 July 2024).

- AquaSwitch. Business Electricity Prices & Rates—March 2025. Available online: https://www.aquaswitch.co.uk/business-electricity-prices/ (accessed on 10 December 2023).

- Autocar. First New UK Hydrogen Fuelling Hub to Open in 2024. Available online: https://www.autocar.co.uk/car-news/new-cars/first-new-uk-hydrogen-fuelling-hub-open-2024 (accessed on 10 July 2024).

- IEA. Towards Hydrogen Definitions Based on Their Emissions Intensity; IEA: Paris, France, 2023; Available online: https://www.iea.org/reports/towards-hydrogen-definitions-based-on-their-emissions-intensity/executive-summary (accessed on 10 July 2024).

- Zemo Partnership. Well-to-Tank. Available online: https://www.zemo.org.uk/work-with-us/buses-coaches/low-emission-buses/well-to-tank.htm (accessed on 10 July 2024).

- El Hannach, M.; Ahmadi, P.; Guzman, L.; Pickup, S.; Kjeang, E. Life cycle assessment of hydrogen and diesel dual-fuel class 8 heavy duty trucks. Int. J. Hydrogen Energy 2019, 44, 8575–8584. [Google Scholar] [CrossRef]

- Low Carbon Vehicle Partnership and CENEX. The Renewable Fuels Guide; CENEX: Loughborough, UK, 2020. [Google Scholar]

- CRD Performance. LPG/CNG Conversion—Diesel Vehicles. Available online: https://www.crdperformance.com/lpg/lpg-cng-diesel-vehicles/ (accessed on 10 July 2024).

- The AA (British Motoring Association). Fuel Price Report (July 2023). Available online: https://www.theaa.com/~/media/the-aa/pdf/motoring-advice/fuel-reports/august-2023.pdf?rev=8170f66b6d374d7eaf17624913c2ab77&hash=35E5727CCCC4A7E68AA6C010797315EC#:~:text=Unleaded%20prices%20have%20risen%20from%20143.5%20p%2Flitre%20last,the%20highest%20price%20for%20unleaded%20at%20150.7%20p%2Flitre (accessed on 10 July 2024).

- Calor. BioLPG from Calor: Introducing a UK Fuel Exclusive (2018); Calor Gas: Coventry, UK, 2018. [Google Scholar]

- Department for Energy Security and Net Zero. Weekly Road Fuel Prices. Available online: https://www.gov.uk/government/statistics/weekly-road-fuel-prices (accessed on 10 December 2023).

- Zemo Partnership. Heavy Duty Vehicle Manufacturer Engine Approval for High Blend Biofuels Appendix 1—Renewable Fuels Guide; Zemo Partnership: London, UK, 2023. [Google Scholar]

- Zemo Partnership. The Renewable Fuels Guide; Zemo Partnership: London, UK, 2023. [Google Scholar]

- LUBIX. HVO Fuel Price Comparison with Fossil Diesel Is It Worth It? Available online: https://lubiq.uk/hvo-fuel-price-comparison/ (accessed on 10 December 2023).

- ULEMCo. Hydrogen Retrofit Solutions for Commercial Vehicle Applications; ULEMCo Ltd.: Liverpool, UK, 2023. [Google Scholar]

- Low Carbon Vehicle Partnership. Low Emission Freight & Logistics Trial (LEFT) Key Findings Dissemination Report; Low Carbon Vehicle Partnership: London, UK, 2020. [Google Scholar]

- CENEX. Dedicated to Gas: An Innovate UK Research Project to Assess the Viability of Gas Vehicles; CENEX: Loughborough, UK, 2019. [Google Scholar]

- CENEX. Low Carbon Truck and Refuelling Infrastructure Demonstration Trial Evaluation: Final Report to the DfT; CENEX: Loughborough, UK, 2016. [Google Scholar]

- Ricardo Energy and Environment—Climate Change Committee. Zero Emission HGV Infrastructure Requirements. Available online: https://www.theccc.org.uk/publication/zero-emission-hgv-infrastructure-requirements/ (accessed on 10 July 2024).

- LowCVP. Biomethane for Transport-HGV Cost Modelling; Low Carbon Vehicle Partnership: London, UK, 2011. [Google Scholar]

- Northern Powergrid. Guide Prices and Timescales. Available online: https://www.northernpowergrid.com/guide-prices-and-timescales (accessed on 10 July 2024).

- National Grid. Interactive Costing Tool. Available online: https://www.nationalgrid.co.uk/connections-landing/null/interactive-costing-tool (accessed on 10 July 2024).

- The UK Government. The Motor Vehicles (Driving Licences) (Amendment) Regulations 2018. Available online: https://www.legislation.gov.uk/uksi/2018/784/pdfs/uksi_20180784_en.pdf (accessed on 10 July 2024).

- Diver and Vehicle Licensing Agency. Rates of Vehicle Tax; Diver and Vehicle Licensing Agency: Swansea, UK, 2023. [Google Scholar]

- Zemo Partnership. Renewable Fuels Assurance Scheme. Available online: https://www.zemo.org.uk/work-with-us/fuels/the-renewable-fuels-assurance-scheme.htm (accessed on 10 July 2024).

- The UK Government. The Road Vehicles (Authorised Weight) (Amendment) Regulations 2023. Available online: https://www.legislation.gov.uk/uksi/2023/760/pdfs/uksi_20230760_en.pdf (accessed on 10 July 2024).

- The UK Government. The Road Vehicles (Authorised Weight) Regulations 1998. Available online: https://www.legislation.gov.uk/uksi/1998/3111/schedule/2/made (accessed on 10 July 2024).

- LoCITY. Commercial Vehicle Finder. Available online: https://commercialvehiclefinder.cenex.co.uk/?per_page=6 (accessed on 10 July 2024).

- LoCity. Fleet Advice Tool. Available online: https://www.cenex.co.uk/projects-case-studies/locity-fleet-tools-development-project/ (accessed on 10 July 2024).

- Energy Saving Trust. Fleet Advice and Consultancy for Your Business. Available online: https://energysavingtrust.org.uk/service/fleet-advice-consultancy/ (accessed on 10 July 2024).

- Gridserve. Electric Highway. Available online: https://electrichighway.gridserve.com/ (accessed on 10 July 2024).

- Zapmap. Map of Electric Charging Points for Electric Cars UK. Available online: https://www.zap-map.com/live/ (accessed on 10 July 2024).

- Element 2. Homepage. Available online: https://element-2.co.uk/ (accessed on 10 July 2024).

- H2 Green. Homepage. Available online: https://www.h2green.co.uk/ (accessed on 10 July 2024).

- Haulage Exchange. Leading Freight Exchange Platform in the UK. Available online: https://haulageexchange.co.uk/freight-exchange/ (accessed on 10 July 2024).

- Returnloads.net. The UK’s leading haulage exchange for all road transport operators. Available online: https://www.returnloads.net/ (accessed on 4 March 2025).

- myLPG.eu. LPG Stations in United Kingdom. Available online: https://www.mylpg.eu/stations/united-kingdom/ (accessed on 10 July 2024).

- UK Fuels. E-Route Online. Available online: https://www.erouteonline.com/v7/ukfuels/ (accessed on 10 July 2024).

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kamat, S.; Botting, D.; Bingham, C.M.; Albayati, I.M. A New Philosophy for the Development of Regional Energy Planning Schemes. Sustainability 2025, 17, 3295. https://doi.org/10.3390/su17083295

Kamat S, Botting D, Bingham CM, Albayati IM. A New Philosophy for the Development of Regional Energy Planning Schemes. Sustainability. 2025; 17(8):3295. https://doi.org/10.3390/su17083295

Chicago/Turabian StyleKamat, Shweta, Duncan Botting, Chris M. Bingham, and Ibrahim M. Albayati. 2025. "A New Philosophy for the Development of Regional Energy Planning Schemes" Sustainability 17, no. 8: 3295. https://doi.org/10.3390/su17083295

APA StyleKamat, S., Botting, D., Bingham, C. M., & Albayati, I. M. (2025). A New Philosophy for the Development of Regional Energy Planning Schemes. Sustainability, 17(8), 3295. https://doi.org/10.3390/su17083295