1. Introduction

This study focuses on the role of financial development in economic growth in Central, Eastern and South-Eastern European (CESEE) countries from the beginning of the post-communist era up to the period of the global financial crisis (GFC) and afterwards (1995–2014).

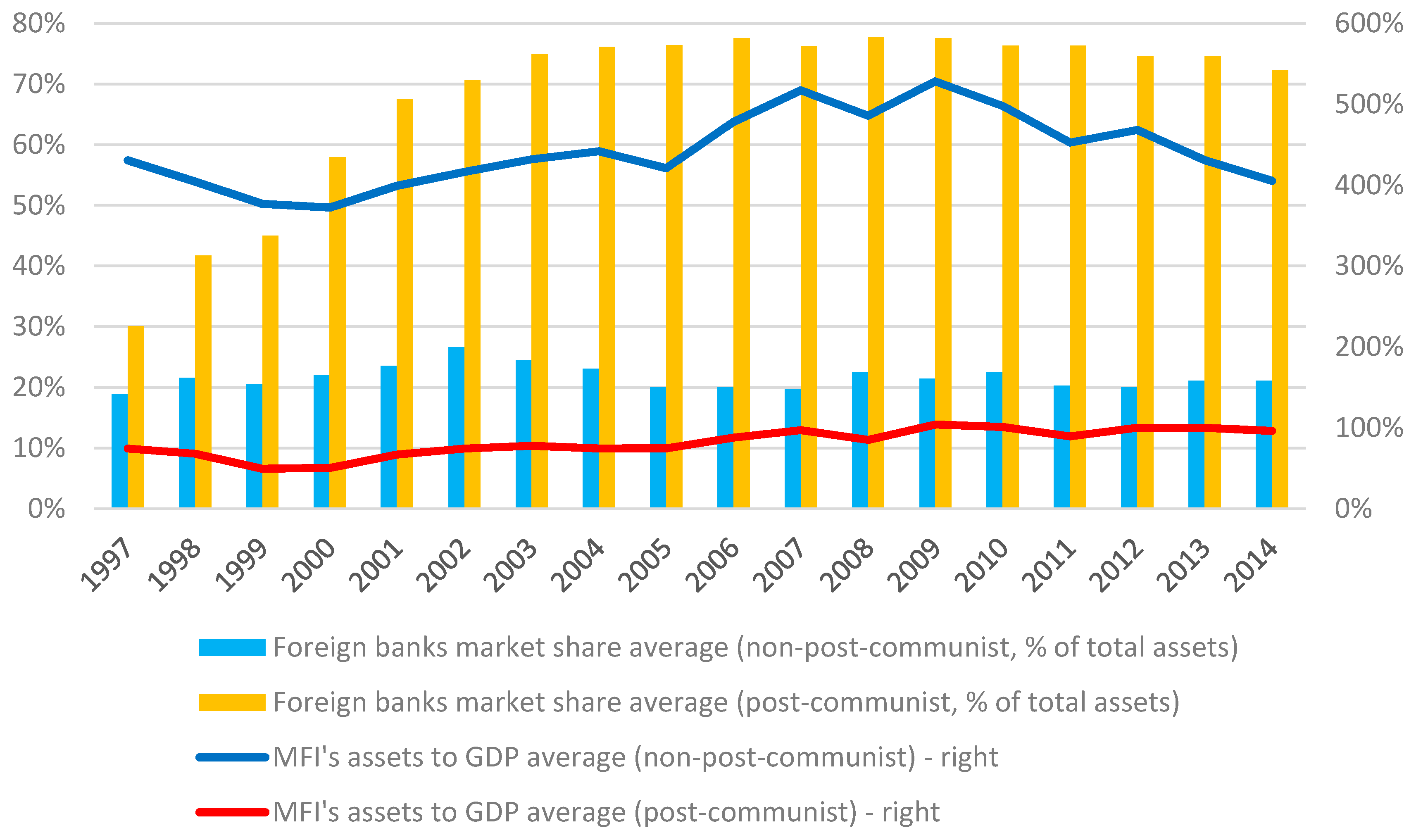

At the beginning of the economic and political transformations that took place in post-communist countries, there was a huge gap in the level of economic and financial development between this group of countries and advanced economies. However, the transformation period in post-communist countries has been marked by dynamic development. One of the key challenges has been the privatisation of state-owned banks and enterprises, as well as the liberalisation of market entry for private investors, both domestic and foreign. Foreign bank entry was especially high in the post-communist economies in the late 1990s and early 2000s, which contributed to the growth of nascent banking systems. According to [

1], this partly reflected waves of reforms, including the opening up of Eastern Europe and other transition economies, as well as rapid financial globalisation before the GFC. This trend peaked in 2007 and slowed markedly after the outbreak of the crisis. The share of foreign-owned banks in banking sector assets in CESEE countries (see

Table 1) ranges from 19% in Kosovo to 95% in Estonia. The stake of foreign-owned banks is below 50% in only five out of twenty countries (Kosovo, Ukraine, Belarus, Slovenia and Hungary).

Given the importance of foreign ownership within the local banking system of CESEE countries, there is a need to investigate whether these countries have benefited, in terms of higher economic growth, from the presence and relevance of foreign-owned banks.

Our major contribution to the debate on finance and growth lies in identifying the role that foreign-owned banks play in fostering economic growth. Their role can be examined according to two main strands of literature, which interpret their presence either as: (i) an important source of innovation, competition and efficiency, with positive spill-over effects for the functioning of the banking system of the host country; or (ii) a source of credit contraction in the credit markets of host countries, for a variety of reasons, among which exposure to the financial troubles, either firm-specific or systematic, of their parent company is at present the most significant (see [

1] for an extensive survey and updated analysis of the trends and worldwide impact of foreign banking). Accordingly, the impact of foreign-owned banks on the economic development of the host country is expected to be different. We trace the potential role of foreign-owned banks using two main measures: the decomposition of domestic credit to the private sector (as a ratio to GDP) according to the ownership structure of banks and the ratio of foreign-owned bank lending to total domestic credit.

The pioneering works by [

2,

3,

4] triggered further analyses on the finance and growth nexus. The end of the twentieth and the beginning of the twenty-first century marked an increase in empirical and cross-country research on the implications of the development and structure of financial systems. In particular, the debate focused at first on the overall impact of the financial system and its depth on economic growth, causality and channels of influence, as well as the conditions necessary to achieve its positive relationship with GDP. The agenda then shifted to comparisons between bank- and market-based financial systems. The debate following the onset of the GFC has tended to employ a systemic perspective to analyse the fragility and limits of “oversized” financial systems in contributing to economic growth.

Notwithstanding these achievements, measures of financial development used in the literature are those traditionally proposed in the seminal works by [

5,

6]. However, the empirical literature on finance and growth tends to suffer from an insufficiently precise link between theory and measurement [

7]. If theory focuses on particular functions provided by the financial sector—producing information, exerting corporate governance, facilitating risk management, pooling savings and easing exchange—and how these functions influence resource allocation decisions and economic growth, empirical works too frequently fail to directly measure these financial functions and employ the simple “size” of the financial system as a proxy for financial development. Our measurement strategy helps tackle this important issue. Our study seeks to contribute to this issue by proposing the decomposition of the “size” of the banking market, distinguishing between state-owned, privately owned and foreign-owned banks and banks owned by development banks. This can help to highlight whether the lending behaviour of banks of diverse types of ownership—and efficiency—fosters (or dampens) economic growth differently. Further, we complement our measure of bank development with a new measure of stock market development that underlines the role of financial markets in supporting non-financial companies, i.e., the true engine of the growth of an economy.

Our results cast doubt on the idea that bank credit fosters economic growth and that foreign-owned banks are a source of innovation, with positive spill-over effects in host banking markets. Conversely, we discover the channels through which financial development was conducive to higher growth in our sample of countries: on the one hand, the credit extended by banks owned by development banks, which was important in influencing the real economy; on the other hand, the development of stock markets, to the extent that these do not experience extremely volatile periods such as occurred at the start of 2008.

The paper is organised as follows.

Section 2 reviews the relevant literature.

Section 3 describes the model, the sample and the variables.

Section 4 presents and discusses the empirical results, while

Section 5 concludes the paper.

2. Literature Review

Many of the efforts of empirical research are devoted to delivering a final word, using sound and sophisticated econometric models, about the causal links between finance and growth, so as to address biases introduced by measurement error, reverse causation and problems relating to omitted variables [

8]. The empirical literature is far from having reached a consensus, despite decades of evidence. Prominent qualitative surveys in the field include [

7,

8,

9]. More recent surveys based on meta-analysis, which include [

10,

11], uncover the causes of the degree of heterogeneity in the empirical literature, such as the choice of financial variable proxies, the kind of data used (e.g., the number of countries or time periods under investigation) and the research design (e.g., addressing or ignoring the issue of endogeneity).

Although complete unanimity does not exist, the bulk of empirical research on the mechanisms through which finance affects growth suggests that [

7]: (a) countries with better-functioning banks and markets grow faster; (b) simultaneity bias does not seem to drive these conclusions; and (c) better-functioning financial systems ease the external financing constraints that impede firm and industrial expansion.

In fact, a wealth of literature supports the positive and statistically significant, albeit non-linear, influence of a deepening financial system on economic growth. Besides theoretical modelling, most of the literature on growth and finance has focused on broad cross-section panels of countries with long-term data (for surveys, see [

7,

12,

13]), showing that: (i) the finance and growth relationship differs among countries and depends on their level of economic development (e.g., the positive effect is most evident in low- to middle-income countries; see [

14] for evidence for less developed countries); and (ii) financial sector deepening also reduces economic growth volatility. Granger causality seems to exist from financial development to economic growth and that the channels include improvements in resource allocation, accumulation of knowledge and productivity growth, rather than capital accumulation [

9]. However, empirical studies unwittingly suffer from the drawback of choosing an appropriate, yet debatable, measure of financial development [

15]. The strand of research linking finance to growth began with King and Levine, who used panel data for 80 countries during 1960–1989 and found that various measures of financial development levels were positively related to GDP per capita growth via productivity improvements [

5,

16]. In addition using vector error correction models, it was proved, for main industrialised economies, a long-run causality between measures of financial intensity and real per capita levels of output [

17]. The positive relationship between the exogenous components of financial development and economic growth was also confirmed by [

18] for a panel of 74 countries over the 1960–1995 period., In addition to banks, stock markets also were found to contribute to growth in long-run capital accumulation and productivity improvements [

19]. Therefore, they should be analysed simultaneously. For a sample of 13 EU countries during 1976–2005, a long-run equilibrium relationship between the development of banking and stock markets and economic growth was found, but also a negative short-run effect between liquidity and economic development [

20].

However, only a limited number of empirical studies tackle the growth and finance nexus in transition economies and sub-regions such as CESEE countries, in which this link is significantly weaker. For a data sample of 146 countries during 1975–2005 the finance-growth nexus shows a heterogeneous impact across regions, i.e., it is weaker for low-income countries [

21]. In Middle East and North African countries, the banking sector makes a lower contribution to economic growth than in the rest of the world, while in Europe and Central Asia, the impact is greater. These differences are partly due to varied access to financial services and the degree of banking competition. The literature has focused on developed and high-income economies, as opposed to catch-up countries with younger and relatively less developed financial systems. The financial sectors in EU accession countries were found to share similar structures, characterised by a relatively low financial deepening level, underdeveloped stock markets, the dominant role of banks and a high degree of foreign presence [

22]. In such an environment, a relatively weak contribution of the financial sector to economic growth is confirmed in South-Eastern Europe over 1993–2001, which may be due to the socialist legacy, as well as the failure to establish robustly and prudently functioning legal and regulatory frameworks [

23]. This weak evidence of the link between financial development and economic growth in transition Central and Eastern European countries was also confirmed by [

24], who argued that this is due to differences in fiscal and monetary discipline and the low enforcement capacity of governments that are excessively committed to bailout policies. A study using panel data from 25 transition countries during 1993–2000, supported the conclusion that the amount of bank credit to the private sector does not contribute to economic growth, as a result of soft budget constraints and banking crises in these economies [

25]. The lack of a positive and significant relationship between financial development and economic growth in 13 CESEE countries in 1994–1999 was likewise proven by [

26]. An overall weak relationship between bank development and growth in nine EU accession countries in 1996–2000 was found by [

27] and no impact of stock market development on growth. Similarly, the weakness of the link for 16 CESEE countries during the 1991–2011 period was confirmed by [

28], and was explained mainly by the high stock of NPL and banking crisis experiences. In the same vein, evidence by [

29], focusing on 10 new European Union members in 1994–2007, suggested that the stock and credit markets in these economies are still underdeveloped and that their contribution to economic growth is limited, owing to low financial depth.

However, using longer panel data for 27 transition economies over the period 1989–2004, strong evidence to the contrary was provided by [

30], namely that financial development has a positive and significant link to economic growth. This supports the previous assumption of [

22] that proper financial development in a conducive environment may have just started in these economies. In a large set of countries for the period 1980–2009, including in Eastern Europe and Central Asia, no specific relationship was found between bank development, stock market development and economic growth [

31]. The study concluded, that in order to achieve a long-run positive finance and growth relationship, as established by [

19], those countries needed to increase domestic credit to the private sector and domestic savings to attract a higher level of investments. A recent study used a panel co-integration approach to analyse the role of financial deepening in economic growth over the period from 1970 to 2007 for 20 developed and 17 emerging countries in Africa, Asia and Latin America [

32]. Unfortunately, CESEE countries were not included in the sample since the use of such a long time horizon is not possible for these countries. The study found that the impact of financial and trade openness differed for the two groups of countries. For developing countries, trade openness and financial deepening were more important than for developed ones. However, the time series did not cover the period of the global financial crisis.

Once economic and political transformations had begun, post-communist countries were treated by researchers either as a separate group of countries or as part of emerging markets. To date, foreign bank presence in CESEE countries has been analysed from four main points of view. First, researchers have analysed the market entrance of foreign banks (e.g., [

33,

34]). However, a new strand of research has since emerged, namely, the “exit” of foreign-owned banks from local markets. Second, there is a vast amount of research on the credit activity of CESEE banks (e.g., [

35,

36,

37,

38,

39]). Third, there have been analyses on the performance of banks and the impact of foreign ownership (e.g., [

40,

41,

42,

43,

44]. Fourth, market competition and the impact of foreign-owned banks have also been in focus (e.g., [

45,

46]).

This study combines two strands of empirical literature: one analysing the link between financial development and economic growth and the other focusing on the role of foreign banks in local markets. To the best of our knowledge, the first study combining the two strands by examining the effect of foreign banks on economic growth is [

47]. However, their sample (1995–2003) covered only a few post-communist countries, with many other emerging markets and advanced economies. They concluded that, thanks to foreign-owned banks, external financing constraints had been relaxed and informational barriers and legal obstacles had diminished. Our study differs from [

47] in the extended period of our analysis, which also covers the crisis and post-crisis years, as well as CESEE countries.

5. Conclusions

Our paper focuses on the role of financial development in the economic growth of CESEE countries in the post-communist era, the GFC and the period afterwards. In particular, we analyse whether CESEE countries have benefited from foreign-owned bank presence in terms of higher economic growth. Although complete unanimity does not exist, the bulk of empirical research on the mechanisms through which finance affects growth suggests that countries with a higher ratio of credit to the private sector to GDP and a higher market capitalisation to GDP grow faster. Our findings cast doubt on these results, at least in the case of CESEE economies. Moreover, our results challenge the idea that foreign-owned banks are a source of innovation with positive spill-over effects in local banking markets.

The majority of studies, conducted either at the beginning of the twenty-first century or even more recently, point to a limited, if not non-existent, relationship between financial development (bank and stock markets) and economic growth for CESEE countries. These findings have also been confirmed in other regions when post-1990 data have been used.

Nonetheless, the financial systems in CESEE countries have evolved considerably from their starting point at the beginning of the 1990s, and it would seem quite odd, prima facie, that this development had no effect on the economic growth of these economies.

Indeed, we find that bank credit could be an important source of economic growth to the extent that banks owned by development banks are involved in the process of providing credit to the private sector. They could be involved in many activities, with diversified scope and focus, targeting a broad base of customers or specific types of customers, such as SMEs or start-ups. Moreover, they could be involved in infrastructural projects that are regarded as growth-related. However, the number and relative size of such banks in CESEE countries is not considerable, which may explain why the overall credit to the private sector is far from being a catalyst of growth.

Finally, with respect to the role of stock markets, we underline a positive contribution to economic growth, except for extremely volatile periods, as at the start of 2008. Since periods of boom and bust typically characterise stock markets and are not easy to predict, excessive leverage on stock markets could be harmful to the real economy.

Our findings indicate that the future research agenda should include microeconomic data on credit composition according to the type of customer and by bank ownership, in order to qualify and clarify how bank credit policies targeted at specific market segments can foster or dampen economic growth. Foreign-owned banks in CESEE have preferred to lend primarily to households (rather than to enterprises) to enjoy “cream-skimming” in a nascent business area and to avoid or limit the adverse selection problems that typically affect the supply of loans to local firms by new entrants. This may explain the limited role of bank credit in boosting economic growth and the negative effects of foreign lending on the growth prospects of the host country. A thorough analysis of the process of bancarisation in CESEE countries warrants further investigation for the negative effects that household indebtedness may have on economic development. Taking into account the market share of foreign-owned banks in CESEE countries, these results may imply some public policy measures. If the foreign ownership of banks does not support economic growth, the reduction of their market share may be reconsidered, on condition that there is enough domestic capital to invest in the banking sector. Some countries, such as Hungary and Poland, decided to undertake such measures in recent years. However, it was mostly the result of the parent company decision to “exit” the market, either because of unfavourable financial conditions in the home country (e.g., Unicredit) or because of an evolving global strategy (e.g., GE Capital). Further in-depth analysis should be considered of the role of foreign-owned banks in each host country, taking into account its capacities and development potential.

{kind=link}

{kind=link}

{kind=link}

{kind=link}