The Potential Impact of Different Taxation Scenarios towards Sugar-Sweetened Beverages on Overweight and Obesity in Brazil: A Modeling Study

Abstract

:1. Introduction

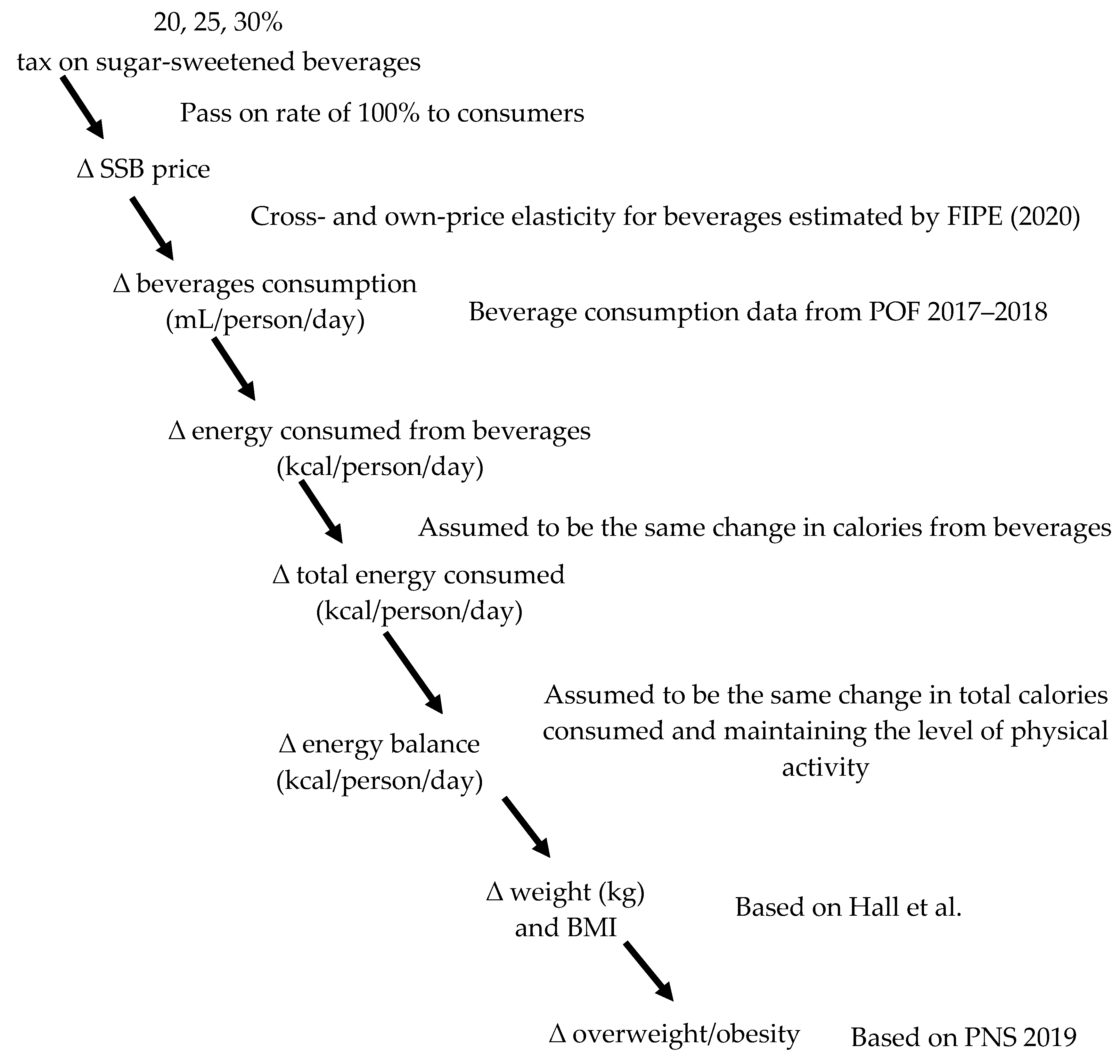

2. Methods

2.1. Data and Assumptions

2.2. Price Elasticity and Pass-on Rate

2.3. Data Sources, Sampling, and Consumption of SSBs in Brazil

2.4. Prevalence of Overweight and Obesity in Brazil

2.5. Modeling

2.6. Changes in Calorie Consumption

2.7. Changes in Body Weight and BMI

2.8. Change in Overweight and Obesity Prevalence

2.9. Sensitivity Analyses

3. Results

3.1. Changes in SSB Consumption and Energy Intake

3.2. Changes in BMI

3.3. Change in Overweight and Obesity Prevalence

3.4. Sensitivity Analyses

4. Discussion

Study Strengths and Limitations

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

References

- Ng, M.; Fleming, T.; Robinson, M.; Thomson, B.; Graetz, N.; Margono, C.; Mullany, E.C.; Biryukov, S.; Abbafati, C.; Abera, S.F.; et al. Global, Regional, and National Prevalence of Overweight and Obesity in Children and Adults during 1980–2013: A Systematic Analysis for the Global Burden of Disease Study 2013. Lancet 2014, 384, 766–781. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Brazilian Institute of Geography and Statistics. National Health Survey 2019: Primary Health Care and Anthropometric Information; Brazilian Institute of Geography and Statistics: Rio de Janeiro, Brazil, 2020; 66p. Available online: https://biblioteca.ibge.gov.br/visualizacao/livros/liv101758.pdf (accessed on 6 November 2022).

- Global Health Metrics. Global burden of 369 diseases and injuries in 204 countries and territories, 1990–2019: A systematic analysis for the Global Burden Disease Study 2019. Lancet 2020, 396, 1204–1222. [Google Scholar] [CrossRef] [PubMed]

- World Health Organization. Brazil First Country to Make Specific Commitments in UN Decade of Action on Nutrition. Available online: https://www.who.int/news/item/22-05-2017-brazil-first-country-to-make-specific-commitments-in-un-decade-of-action-on-nutrition (accessed on 6 November 2022).

- Malik, V.S.; Pan, A.; Willett, W.C.; Hu, F.B. Sugar-Sweetened Beverages and Weight Gain in Children and Adults: A Systematic Review and Meta-Analysis. Am. J. Clin. Nutr. 2013, 98, 1084–1102. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Schlesinger, S.; Neuenschwander, M.; Schwedhelm, C.; Hoffmann, G.; Bechthold, A.; Boeing, H.; Schwingshackl, L. Food Groups and Risk of Overweight, Obesity, and Weight Gain: A Systematic Review and Dose-Response Meta-Analysis of Prospective Studies. Adv. Nutr. 2019, 10, 205–218. [Google Scholar] [CrossRef] [Green Version]

- Bes-Rastrollo, M.; Sayon-Orea, C.; Ruiz-Canela, M.; Martinez-Gonzalez, M.A. Impact of Sugars and Sugar Taxation on Body Weight Control: A Comprehensive Literature Review: Added Sugars and Obesity. Obesity 2016, 24, 1410–1426. [Google Scholar] [CrossRef]

- Hu, F.B.; Malik, V.S. Sugar-Sweetened Beverages and Risk of Obesity and Type 2 Diabetes: Epidemiologic Evidence. Physiol. Behav. 2010, 100, 47–54. [Google Scholar] [CrossRef] [Green Version]

- Brazilian Institute of Geography and Statistics. National Health Survey 2017–2018: Analysis of Personal Food Consumption in Brazil; Brazilian Institute of Geography and Statistics: Rio de Janeiro, Brazil, 2020; 120p. Available online: https://biblioteca.ibge.gov.br/visualizacao/livros/liv101742.pdf (accessed on 6 November 2022).

- Colchero, M.A.; Popkin, B.M.; Rivera, J.A.; Ng, S.W. Beverage Purchases from Stores in Mexico under the Excise Tax on Sugar Sweetened Beverages: Observational Study. BMJ 2016, 352, h6704. [Google Scholar] [CrossRef] [Green Version]

- Salgado, M.V.; Penko, J.; Fernandez, A.; Konfino, J.; Coxson, P.G.; Bibbins-Domingo, K.; Mejia, R. Projected Impact of a Reduction in Sugar-Sweetened Beverage Consumption on Diabetes and Cardiovascular Disease in Argentina: A Modeling Study. PLoS Med. 2020, 17, e1003224. [Google Scholar] [CrossRef]

- Canella, D.S.; Levy, R.B.; Claro, R.M.; Monteiro, C.A. Food consumption: Too much sugar (1987–2009). In Old and New Health Diseases in Brazil from Geisel to Dilma, 1st ed.; Monteiro, C.A., Levy, R.B., Eds.; HUCITEC:NUPENS/USP: São Paulo, Brazil, 2015; Volume 1, pp. 43–55. [Google Scholar]

- Institute for Clinical and Healthcare Effectiveness. The Hidden Side of Sugary Drinks in Brazil Buenos Aires, Argentina. 2020. Available online: https://actbr.org.br/uploads/arquivos/IECS-e-Infografi%CC%81as-bebidas-azucaradas-Brasil.pdf (accessed on 6 November 2022).

- Alcaraz, A.; Vianna, C.; Bardach, A.; Espinola, N.; Perelli, L.; Balan, D.; Cairoli, F.; Palacios, A.; Comolli, M.; Instituto de Efectividad Clínica y Sanitaria; et al. O Lado Oculto das Bebidas Açucaradas no Brasil, Buenos Aires, Argentina. November 2020. Available online: https://www.iecs.org.ar/azucar (accessed on 21 November 2022).

- Briggs, A.D.M.; Mytton, O.T.; Kehlbacher, A.; Tiffin, R.; Rayner, M.; Scarborough, P. Overall and Income Specific Effect on Prevalence of Overweight and Obesity of 20% Sugar Sweetened Drink Tax in UK: Econometric and Comparative Risk Assessment Modelling Study. BMJ 2013, 347, f6189. [Google Scholar] [CrossRef] [Green Version]

- Briggs, A.D.; Mytton, O.T.; Madden, D.; O’Shea, D.; Rayner, M.; Scarborough, P. The Potential Impact on Obesity of a 10% Tax on Sugar-Sweetened Beverages in Ireland, an Effect Assessment Modelling Study. BMC Public Health 2013, 13, 860. [Google Scholar] [CrossRef]

- Cabrera Escobar, M.A.; Veerman, J.L.; Tollman, S.M.; Bertram, M.Y.; Hofman, K.J. Evidence That a Tax on Sugar Sweetened Beverages Reduces the Obesity Rate: A Meta-Analysis. BMC Public Health 2013, 13, 1072. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Basu, S.; Vellakkal, S.; Agrawal, S.; Stuckler, D.; Popkin, B.; Ebrahim, S. Averting Obesity and Type 2 Diabetes in India through Sugar-Sweetened Beverage Taxation: An Economic-Epidemiologic Modeling Study. PLoS Med. 2014, 11, e1001582. [Google Scholar] [CrossRef] [PubMed]

- Manyema, M.; Veerman, L.J.; Chola, L.; Tugendhaft, A.; Sartorius, B.; Labadarios, D.; Hofman, K.J. The Potential Impact of a 20% Tax on Sugar-Sweetened Beverages on Obesity in South African Adults: A Mathematical Model. PLoS ONE 2014, 9, e105287. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Schwendicke, F.; Stolpe, M. Taxing Sugar-Sweetened Beverages: Impact on Overweight and Obesity in Germany. BMC Public Health 2017, 17, 88. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Phonsuk, P.; Vongmongkol, V.; Ponguttha, S.; Suphanchaimat, R.; Rojroongwasinkul, N.; Swinburn, B.A. Impacts of a Sugar Sweetened Beverage Tax on Body Mass Index and Obesity in Thailand: A Modelling Study. PLoS ONE 2021, 16, e0250841. [Google Scholar] [CrossRef]

- Vecino-Ortiz, A.I.; Arroyo-Ariza, D. A Tax on Sugar Sweetened Beverages in Colombia: Estimating the Impact on Overweight and Obesity Prevalence across Socio Economic Levels. Soc. Sci. Med. 2018, 209, 111–116. [Google Scholar] [CrossRef]

- Itria, A.; Borges, S.S.; Rinaldi, A.E.M.; Nucci, L.B.; Enes, C.C. Taxing Sugar-Sweetened Beverages as a Policy to Reduce Overweight and Obesity in Countries of Different Income Classifications: A Systematic Review. Public Health Nutr. 2021, 24, 5550–5560. [Google Scholar] [CrossRef]

- Colchero, M.A.; Rivera-Dommarco, J.; Popkin, B.M.; Ng, S.W. In Mexico, Evidence Of Sustained Consumer Response Two Years After Implementing A Sugar-Sweetened Beverage Tax. Health Aff. 2017, 36, 564–571. [Google Scholar] [CrossRef]

- Berardi, N.; Sevestre, P.; Tépaut, M.; Vigneron, A. The Impact of a ‘Soda Tax’ on Prices: Evidence from French Micro Data. Appl. Econ. 2016, 48, 3976–3994. [Google Scholar] [CrossRef] [Green Version]

- Silver, L.D.; Ng, S.W.; Ryan-Ibarra, S.; Taillie, L.S.; Induni, M.; Miles, D.R.; Poti, J.M.; Popkin, B.M. Changes in Prices, Sales, Consumer Spending, and Beverage Consumption One Year after a Tax on Sugar-Sweetened Beverages in Berkeley, California, US: A before-and-after Study. PLoS Med. 2017, 14, e1002283. [Google Scholar] [CrossRef]

- Roberto, C.A.; Lawman, H.G.; LeVasseur, M.T.; Mitra, N.; Peterhans, A.; Herring, B.; Bleich, S.N. Association of a Beverage Tax on Sugar-Sweetened and Artificially Sweetened Beverages With Changes in Beverage Prices and Sales at Chain Retailers in a Large Urban Setting. JAMA 2019, 321, 1799. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Mariath, A.B.; Martins, A.P.B. Decade of Action on Sugary Drinks Nutrition and Taxation in Brazil: Where Are We? Cad. Saúde Pública 2021, 37, e00157220. [Google Scholar] [CrossRef] [PubMed]

- Brazil Ministry of Health/National Health Surveillance Agency. Resolution of the Collegiate Board of Directors—RDC 429, of 8 October 2020. Provides for Nutritional Labeling of Packaged Foods. Published in the Official Gazette of the Union in: 09/10/2020|Edition: 195|Section: 1|Page: 106. Available online: https://www.in.gov.br/en/web/dou/-/resolucao-de-diretoria-colegiada-rdc-n-429-de-8-de-outubro-de-2020-282070599 (accessed on 6 November 2022).

- Claro, R.M.; Levy, R.B.; Popkin, B.M.; Monteiro, C.A. Sugar-Sweetened Beverage Taxes in Brazil. Am. J. Public Health 2012, 102, 178–183. [Google Scholar] [CrossRef]

- Pereda, A.C.; Christofoletti, M.A.; Ng, S.W.; Claro, R.M.; Duran, A.C.; Monteiro, C.A. Effects of a 20% Price Increase of Sugar-Sweetened Beverages on Consumption and Welfare in Brazil; FEA-USP: São Paulo, Brazil, 2019. [Google Scholar]

- Foundation Institute of Economic Research (Fundação Instituto de Pesquisas Econômicas—FIPE). Systemic Impacts of Changes in the Consumption Pattern of Sugary Drinks, Sweetened or Not, Due to Different Tax Scenarios: Final Report—Update POF 2017/2018. São Paulo. 2020. Available online: https://actbr.org.br/uploads/arquivos/relatorio_FIPE.pdf (accessed on 6 November 2022).

- World Health Organization. Fiscal Policies for Diet and Prevention of Noncommunicable Diseases: Technical Meeting Report; WHO: Geneva, Switzerland, 2015; Available online: https://apps.who.int/iris/bitstream/handle/10665/250131/9789241511247-eng.pdf (accessed on 6 November 2022).

- Finkelstein, E.A.; Zhen, C.; Bilger, M.; Nonnemaker, J.; Farooqui, A.M.; Todd, J.E. Implications of a Sugar-Sweetened Beverage (SSB) Tax When Substitutions to Non-Beverage Items Are Considered. J. Health Econ. 2013, 32, 219–239. [Google Scholar] [CrossRef] [PubMed]

- Hall, K.D.; Sacks, G.; Chandramohan, D.; Chow, C.C.; Wang, Y.C.; Gortmaker, S.L.; Swinburn, B.A. Quantification of the Effect of Energy Imbalance on Bodyweight. Lancet 2011, 378, 826–837. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Ma, Y.; He, F.J.; Yin, Y.; Hashem, K.M.; MacGregor, G.A. Gradual Reduction of Sugar in Soft Drinks without Substitution as a Strategy to Reduce Overweight, Obesity, and Type 2 Diabetes: A Modelling Study. Lancet Diabetes Endocrinol. 2016, 4, 105–114. [Google Scholar] [CrossRef] [PubMed]

- Barrientos-Gutierrez, T.; Zepeda-Tello, R.; Rodrigues, E.R.; Colchero-Aragonés, A.; Rojas-Martínez, R.; Lazcano-Ponce, E.; Hernández-Ávila, M.; Rivera-Dommarco, J.; Meza, R. Expected Population Weight and Diabetes Impact of the 1-Peso-per-Litre Tax to Sugar Sweetened Beverages in Mexico. PLoS ONE 2017, 12, e0176336. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Falbe, J.; Rojas, N.; Grummon, A.H.; Madsen, K.A. Higher Retail Prices of Sugar-Sweetened Beverages 3 Months After Implementation of an Excise Tax in Berkeley, California. Am. J. Public Health 2015, 105, 2194–2201. [Google Scholar] [CrossRef]

- Conde, W.L.; Borges, C. The risk of incidence and persistence of obesity among brazilian adults according to their nutritional status at the end of adolescence. Rev. Bras. Epidemiol. 2011, 14 (Suppl. S1), 71–79. [Google Scholar] [CrossRef] [Green Version]

- Veerman, J.L.; Sacks, G.; Antonopoulos, N.; Martin, J. The Impact of a Tax on Sugar-Sweetened Beverages on Health and Health Care Costs: A Modelling Study. PLoS ONE 2016, 11, e0151460. [Google Scholar] [CrossRef]

- Long, M.W.; Gortmaker, S.L.; Ward, Z.J.; Resch, S.C.; Moodie, M.L.; Sacks, G.; Swinburn, B.A.; Carter, R.C.; Claire Wang, Y. Cost Effectiveness of a Sugar-Sweetened Beverage Excise Tax in the U.S. Am. J. Prev. Med. 2015, 49, 112–123. [Google Scholar] [CrossRef] [PubMed]

- World Cancer Research Fund International. Health-Related Food Taxes: Policy Actions. Available online: https://policydatabase.wcrf.org/level_one?page=nourishing-level-one#step2=2#step3=315 (accessed on 6 November 2022).

- Colchero, M.A.; Guerrero-López, C.M.; Molina, M.; Rivera, J.A. Beverages Sales in Mexico before and after Implementation of a Sugar Sweetened Beverage Tax. PLoS ONE 2016, 11, e0163463. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Nakamura, R.; Mirelman, A.J.; Cuadrado, C.; Silva-Illanes, N.; Dunstan, J.; Suhrcke, M. Evaluating the 2014 Sugar-Sweetened Beverage Tax in Chile: An Observational Study in Urban Areas. PLoS Med. 2018, 15, e1002596. [Google Scholar] [CrossRef]

- Alvarado, M.; Unwin, N.; Sharp, S.J.; Hambleton, I.; Murphy, M.M.; Samuels, T.A.; Suhrcke, M.; Adams, J. Assessing the Impact of the Barbados Sugar-Sweetened Beverage Tax on Beverage Sales: An Observational Study. Int. J. Behav. Nutr. Phys. Act. 2019, 16, 13. [Google Scholar] [CrossRef] [PubMed]

- Brasil Ministério da Fazenda. Análise da Tributação do Setor de Refrigerantes e Outras Bebidas Açucaradas. Available online: https://www.gov.br/receitafederal/pt-br/acesso-a-informacao/acoes-e-programas/sonegacao/fraude-tributaria/operacao-deflagrada/arquivos-e-imagens/nota-imprensa-bebidas-kit-e-royalties-substituir-26-11-18.pdf (accessed on 10 October 2021).

- Pan American Health Organization. Taxation of Sweetened Beverages in Brazil. Available online: https://actbr.org.br/uploads/arquivos/ACT_relatorio-OPAS_rev04.pdf (accessed on 6 November 2022).

- Jou, J.; Niederdeppe, J.; Barry, C.L.; Gollust, S.E. Strategic Messaging to Promote Taxation of Sugar-Sweetened Beverages: Lessons From Recent Political Campaigns. Am. J. Public Health 2014, 104, 847–853. [Google Scholar] [CrossRef]

- Soares Guimarães, J.; Mais, L.A.; Marrocos Leite, F.H.; Horta, P.M.; Oliveira Santana, M.; Martins, A.P.B.; Claro, R.M. Ultra-Processed Food and Beverage Advertising on Brazilian Television by International Network for Food and Obesity/Non-Communicable Diseases Research, Monitoring and Action Support Benchmark. Public Health Nutr. 2020, 23, 2657–2662. [Google Scholar] [CrossRef]

- Ni Mhurchu, C.; Volkova, E.; Jiang, Y.; Eyles, H.; Michie, J.; Neal, B.; Blakely, T.; Swinburn, B.; Rayner, M. Effects of Interpretive Nutrition Labels on Consumer Food Purchases: The Starlight Randomized Controlled Trial. Am. J. Clin. Nutr. 2017, 105, 695–704. [Google Scholar] [CrossRef] [Green Version]

- Duran, A.C.; Ricardo, C.Z.; Mais, L.A.; Bortoletto Martins, A.P. Role of Different Nutrient Profiling Models in Identifying Targeted Foods for Front-of-Package Food Labelling in Brazil. Public Health Nutr. 2021, 24, 1514–1525. [Google Scholar] [CrossRef]

- Fortes, M.F.; Borges, C.A.; de Miranda, W.C.; Jaime, P.C. Mapping Socioeconomic Inequalities in Local Retail Distribution. Segur. Aliment. Nutr. 2018, 25, 45–58. [Google Scholar] [CrossRef]

- Mullie, P.; Aerenhouts, D.; Clarys, P. Demographic, Socioeconomic and Nutritional Determinants of Daily versus Non-Daily Sugar-Sweetened and Artificially Sweetened Beverage Consumption. Eur. J. Clin. Nutr. 2012, 66, 150–155. [Google Scholar] [CrossRef]

- van Ansem, W.J.C.; van Lenthe, F.J.; Schrijvers, C.T.M.; Rodenburg, G.; van de Mheen, D. Socio-Economic Inequalities in Children’s Snack Consumption and Sugar-Sweetened Beverage Consumption: The Contribution of Home Environmental Factors. Br. J. Nutr. 2014, 112, 467–476. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Backholer, K.; Sarink, D.; Beauchamp, A.; Keating, C.; Loh, V.; Ball, K.; Martin, J.; Peeters, A. The Impact of a Tax on Sugar-Sweetened Beverages According to Socio-Economic Position: A Systematic Review of the Evidence. Public Health Nutr. 2016, 19, 3070–3084. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

| Sex | Age Group (Years) | 20% Tax Mean (95% CI) | 25% Tax Mean (95% CI) | 30% Tax Mean (95% CI) |

|---|---|---|---|---|

| Male | 20 to 29 | −4.0 (−6.9; −1.2) | −5.1 (−8.6; −1.5) | −6.1 (−10.3; −1.8) |

| 30 to 39 | 3.0 (0.5; 5.5) | 3.8 (0.6; 6.9) | 4.5 (0.8; 8.3) | |

| 40 to 49 | 9.0 (7.1; 10.9) | 11.2 (8.8; 13.7) | 13.5 (10.6; 16.4) | |

| 50 to 59 | 12.1 (10.2; 10.9) | 15.1 (12.8; 17.5) | 18.2 (15.3; 21.0) | |

| 60 to 69 | 13.2 (11.3; 15.2) | 16.5 (14.1; 18.9) | 19.8 (16.9; 22.7) | |

| ≥70 | 14.8 (11.5; 18.1) | 18.5 (14.4; 22.6) | 22.2 (17.2; 22.7) | |

| All men | 6.4 (5.2; 7.5) | 7.9 (6.6; 9.3) | 9.5 (7.9; 11.2) | |

| Female | 20 to 29 | −0.1 (−2.3; 2.0) | −0.1 (−2.8; 2.6) | −0.2 (−3.4; 3.1) |

| 30 to 39 | 7.9 (6.3; 9.5) | 9.8 (7.8; 11.9) | 11.8 (9.4; 14.2) | |

| 40 to 49 | 10.4 (9.0; 11.9) | 13.1 (11.2; 14.9) | 15.7 (13.5; 17.8) | |

| 50 to 59 | 11.7 (10.0; 13.5) | 14.7 (12.5; 16.8) | 17.6 (15.0; 20.2) | |

| 60 to 69 | 15.5 (13.2; 17.8) | 19.3 (16.4; 22.2) | 23.2 (19.7; 26.6) | |

| ≥70 | 18.0 (16.1; 20.0) | 22.5 (20.0; 25.0) | 27.1 (24.1; 30.0) | |

| All women | 9.5 (8.6; 10.3) | 11.8 (10.8; 12.9) | 14.2 (13.0; 15.4) | |

| Overall | 8.0 (7.2; 8.8) | 10.0 (9.0; 11.0) | 12.0 (10.8; 13.2) |

| Sex | Age Groups | Mean Change in BMI in kg/m2 (95% CI) | ||

|---|---|---|---|---|

| Tax 20% | Tax 25% | Tax 30% | ||

| Male | 20–29 | −0.056 (−0.056; −0.055) | −0.071 (−0.071; −0.071) | −0.085 (−0.085; −0.084) |

| 30–39 | 0.042 (0.042; 0.042) | 0.053 (0.053; 0.053) | 0.063 (0.062; 0.063) | |

| 40–49 | 0.128 (0.127; 0.128) | 0.159 (0.158; 0.159) | 0.192 (0.191; 0.192) | |

| 50–59 | 0.174 (0.173; 0.174) | 0.217 (0.216; 0.217) | 0.261 (0.260; 0.262) | |

| 60–69 | 0.193 (0.192; 0.194) | 0.241 (0.240; 0.242) | 0.290 (0.289; 0.291) | |

| ≥70 | 0.219 (0.219; 0.220) | 0.274 (0.273; 0.275) | 0.329 (0.328; 0.330) | |

| All men | 0.096 (0.094; 0.098) | 0.119 (0.117; 0.122) | 0.144 (0.141; 1.146) | |

| Female | 20–29 | −0.002 (−0.002; −0.002) | −0.002 (−0.002; −0.002) | −0.003 (−0.003; −0.003) |

| 30–39 | 0.128 (0.128; 0.128) | 0.159 (0.158; 0.159) | 0.191 (0.191; 0.192) | |

| 40–49 | 0.170 (0.170; 0.171) | 0.214 (0.214; 0.215) | 0.257 (0.256; 0.258) | |

| 50–59 | 0.193 (0.193; 0.194) | 0.243 (0.242; 0.244) | 0.291 (0.290; 0.292) | |

| 60–69 | 0.260 (0.259; 0.261) | 0.324 (0.323; 0.325) | 0.389 (0.388; 0.391) | |

| ≥70 | 0.309 (0.308; 0.311) | 0.387 (0.385; 0.388) | 0.466 (0.464; 0.468) | |

| All women | 0.163 (0.162; 0.165) | 0.204 (0.202; 0.206) | 0.245 (0.243; 0.247) | |

| Overall | 0.131 (0.130; 0.133) | 0.164 (0.162; 0.166) | 0.197 (0.195; 0.199) | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Enes, C.C.; Rinaldi, A.E.M.; Nucci, L.B.; Itria, A. The Potential Impact of Different Taxation Scenarios towards Sugar-Sweetened Beverages on Overweight and Obesity in Brazil: A Modeling Study. Nutrients 2022, 14, 5163. https://doi.org/10.3390/nu14235163

Enes CC, Rinaldi AEM, Nucci LB, Itria A. The Potential Impact of Different Taxation Scenarios towards Sugar-Sweetened Beverages on Overweight and Obesity in Brazil: A Modeling Study. Nutrients. 2022; 14(23):5163. https://doi.org/10.3390/nu14235163

Chicago/Turabian StyleEnes, Carla Cristina, Ana Elisa M. Rinaldi, Luciana Bertoldi Nucci, and Alexander Itria. 2022. "The Potential Impact of Different Taxation Scenarios towards Sugar-Sweetened Beverages on Overweight and Obesity in Brazil: A Modeling Study" Nutrients 14, no. 23: 5163. https://doi.org/10.3390/nu14235163