1. Introduction

Corporate takeovers are often modeled as modified English or second-price sealed bid (SPSB) auctions, where the major differences between regular and takeover auctions are high investigation costs that potential acquirers (bidders) must incur to estimate the target firms’ value, bidding costs, and the bidders’ ability to accumulate some of the target’s shares (a toehold) before making the tented offer. Fisher [

1], Hirshleifer and P’ng [

2], and Daniel and Hirshleifer [

3] show that investigation and/or bidding costs lead to a signaling jump bidding equilibrium. At and Morand [

4] argue that jump bidding in takeover auctions may be a result of a free-riding problem. Burkart [

5] shows that in private value takeover auctions, bidders with toeholds should bid above their valuation of the target. Such bidding may result in a negative profit for the winning bidder and an inefficient allocation of the object, but it leads to a higher expected price and profit for the target firm. Dodonova and Khoroshilov [

6], and Hounwanou [

7] study how toeholds affect jump bidding equilibrium. Bulow, Huang, and Klemperer [

8] consider common value takeover auctions with toeholds. They show that the bidder with the larger toehold should bid more aggressively while the bidder with the lower toehold should shade their bid. As a result, unequal toeholds lead to a lower expected price. The combination of the toehold and preemptive bidding effect, the difficulty of distinguishing the private and common value auctions, the inability to observe the bidders’ private values, and the effect of the toehold acquisition process on the target’s stock price makes it difficult to directly observe the effect of the toehold outside of laboratory studies. Hotchkiss and Mooradian [

9], and Eckbo and Thorburn [

10] analyzed bankruptcy auctions, where the effect of the toehold may be more visible. Consistent with Burkart [

5] and Bulow, Huang, and Klemperer [

8], they found that toehold leads to overbidding.

Despite the extensive experimental research on auctions (see Kagel and Levin [

11] for the most recent review), only limited experimental research was performed to test the bidders’ behavior in auction-type models of the takeover process. Khoroshilov and Dodonova [

12] conducted an experimental test of Fishman’s [

1] model of preemptive bidding in auctions with entry fees. Consistent with the model, they show that higher entry fees lead to a lower size, but a higher frequency of jump bidding, higher probability of competition preemption, and lower expected price. However, the observed quantitative effects are significantly lower than the theoretically predicted ones. Georganas and Nagel [

13] tested the model of common value takeover auction with toeholds (Bulow, Huang, and Klemperer [

8]). Consistent with the model, they show that an increase in the toehold ratio makes the bidder with a larger toehold bid more aggressively, lowers the bids of the bidder with the lower toehold, and leads to the lower expected profit for the seller. However, similar to Khoroshilov and Dodonova [

12], the absolute effect of the toeholds is significantly lower than the theoretically predicted effect. To the best of our knowledge, there has been no experimental test of Burkart’s [

5] model of private value auctions with toeholds, and this study is aimed to fill in this gap.

2. Experimental Set-Up

Following Burkart (1995), consider a 2-bidder private value SPSB auction in which bidder owns portion of the object (a “toehold”). Assume bidders are risk-neutral and their valuations of the object are independent and uniformly distributed on (0,60) interval. Since, in the case of no toeholds, bidding up to the value of the object is a weakly dominant strategy, and a change in the opponent’s toehold does not affect ones’ payoff function, for a bidder without the toehold it is still a dominant strategy to bid up to their value of the object regardless of the toehold of their opponent. At the same time, a bidder with a non-zero toehold may be willing to bid above their value of the object, hoping to increase the price and receive a higher payment for their shares. By doing so, however, they face the risk of winning the auction at the price above and ending up with a negative profit.

To find the equilibrium bidding strategies

and

, consider bidder

with value

submitting a bid

. Therefore, their expected profit can be written as:

In equilibrium, the expected profit (1) should be maximized at

. If the rival bidder has no toehold, their dominant strategy is

and, thus,

. If both bidders have equal toeholds

, in a symmetric equilibrium

, and, thus,

. In both cases, consistent with Burkart (1995), the maximization of (1) over

and setting

, results in equilibrium bidding strategies.

The bid premium, defined as the difference between the bid amount and the object’s value, can be written as:

Furthermore, as Burkart [

5] has shown, the bidding strategies (2) determine the unique equilibrium in a model when only one bidder has a toehold or both bidders have identical toeholds.

In total, 43 subjects (chosen among undergraduate Business School students) have participated in four identical sessions (1 session had 12 students, 1 had 11, and 2 had 10). At the beginning of the session, subjects were educated about standard clock-style English auctions and their equivalency to the SPSB auctions. They were told to interpret SPSB auctions as English auctions in which both bidders are not able to attend the auction but send their friends (proxies) to bid on their behalf and tell those proxies to bid up to a specific “bid up to” price

. They were also educated that in auctions without toeholds it is always optimal to bid up to their valuation of the object regardless of the bidding strategy of the other bidder. These educative instructions were given in light of the evidence that subjects in SPSB auctions do not always follow their dominant strategy (Kagel and Levin [

14]) while bidding in English auctions usually converge to the equilibrium very fast (Coppinger, Smith, and Titus [

15]). Since the goal of this study is to analyze how toeholds affect bidding behavior, it was important to make sure that subjects understand the equivalency between the two auction formats and the importance of using dominant strategies.

After the instructions, students were asked to fill in the bidding profiles by specifying their strategies in different auctions with values

drawn from a discrete uniform distribution on

. They were given a pre-filled table for the auction without toeholds with a pre-filled bidding function

and were asked to specify their bids for the symmetric auction with

, and for the asymmetric auction with

and

. For the latter, they were asked to specify their bidding for both roles: as the first and as the second bidder. After that, each auction was simulated once, for each simulation subjects were divided into pairs (in the session with 11 subjects one of the subjects played against a strategy of one of the remaining subjects chosen at random), and the total amount of money won plus a USD 15 participation fee (designed to cover possible losses) were paid to the subjects.

Appendix A and

Appendix B present the instructions given to the subjects. In total, it allowed us to collect 2961 observations. Since subjects specified their strategies before receiving any feedback, such design allows us to capture the effect of subjects’ beliefs about the best strategies based on the description of the model instead of their adaptive reaction to the realized outcomes.

3. Analysis

The theoretical bid premium function leads to several qualitative predictions. First, the benefit or overbidding increases with the size of the toehold while the costs of buying the object above one’s valuation stay the same. As a result, the bidding premium must positively depend on the size of the toehold and it is equal to zero for a bidder without a toehold. Second, a bidder with the higher valuation of the object is more likely to win the auction at an inflated price when they bid above their valuations, and, as a result, the bid premium must decrease with the bidder’s valuation . Third, as the equilibrium bidding function is independent of the rival’s toehold, so is the theoretical bid premium function . In the following analysis, we test the above predictions and compare the magnitudes of the observed and predicted values of the bid premium.

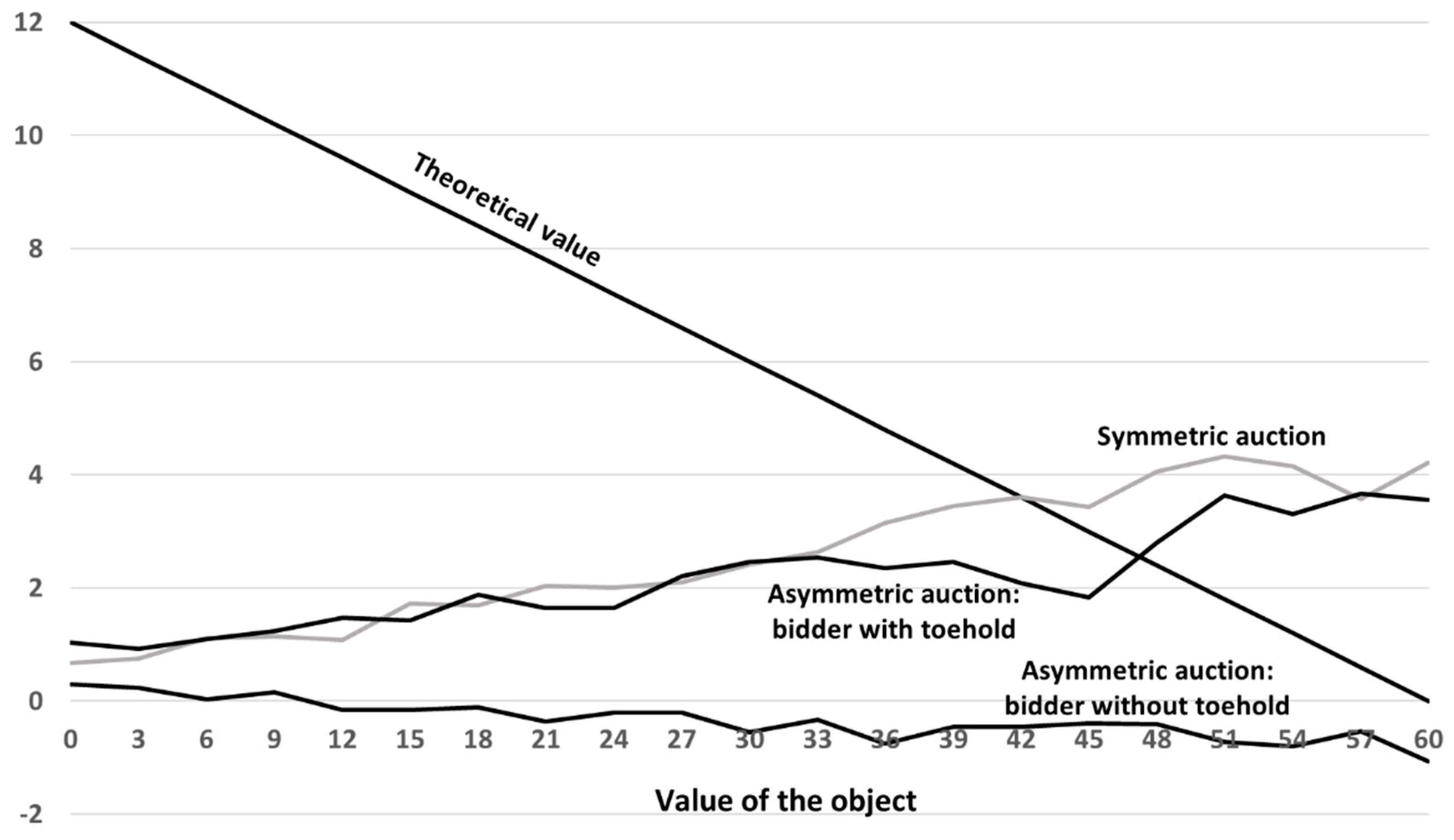

Figure 1 presents the theoretically predicted and average observed bid premiums

as a function of the object’s value

. Note that the theoretical bid premium does not depend on the other bidder’s toehold, and, for the bidder without a toehold, it is equal to zero.

For each value of the object,

Table 1 presents the statistical analysis of these bid premiums based on the 43 conditionally independent observations for each pair of the object value and the auction design (or the bidder’s role in case of the asymmetric auction). The first three columns of

Table 1 present the average values of

. To analyze how the rival bidder’s toehold affects bidding behavior, column 4 presents the average bid differences for individual bids in symmetric and asymmetric auctions for the bidder with a toehold. To analyze how well the theory estimates the magnitude of the bids, column 5 (column 6) presents the differences between the average bids in symmetric auctions (asymmetric auctions for the bidder with toehold) and the theoretically predicted bids given by (2). The numbers in brackets are the

p-values for 2-sided significance

t-tests (based on 43 observations for each signal value and auction combination) for the computed means (columns 1–3) and the differences in means (columns 4–6).

To further analyze the statistical significance of bid premiums, their difference from the theoretically predicted values, and their dependence on the object’s value,

Table 2 presents the results of two fixed-effect (within) regression analyses that control for the identity of the bidders. To analyze the significance of the bid premiums, their difference from the theoretically predicted values, and the effect of the rival bidder’s toehold, the first fixed-effect regression uses only the intercept as an independent variable. To analyze how the bid premiums depend on the object’s value, the second regression uses both the intercept and the object’s value as independent variables. The numbers in brackets are the

p-values for the estimated coefficients.

Consistent with the theory, bidders with toeholds bid significantly above their valuation of the object (Columns 1 and 2 in

Table 1 and Model 1 of

Table 2) and the bidders without toehold do not place bids at a statistically significant premium or discount (

Table 1, Column 3). While within-subject analysis (

Table 2, Model 1, Column 3) shows a negative effect of the rival’s toehold on the bid premium for the bidders without a toehold, the estimated effect is very small (USD −0.328) relative to the value of the object (between USD 0 and USD 60 with step USD 3). It is worth noting that the experiment design does not allow bidders to receive feedback and learn from it, so, they make all their decisions based entirely on the game description, the provided instructions of the optimal strategy in auctions without toeholds, and their own beliefs of how they should alter such a strategy for auctions with toeholds.

For bidders with toeholds, the observed dependence of the bid premium on the object’s value is opposite from what the theory predicts. While the equilibrium bid premium decreases with the object’s value and converges to zero when the object’s value converges to its maximum, the observed pattern is upward sloping (significant at 1% level:

Table 2, Model 2, Columns 1 and 2): bidders bid at a higher premium when they observe higher value. While it is unclear why subjects behave in such a way, one possible explanation may be that, while subjects understand that positive toehold makes it beneficial to drive up the price, they do not realize that the benefit of such price run-up is higher and the probability of winning the auction at the inflated price is lower when their valuation is small. In addition, subjects may have thought of bid premium as a percentage of their valuation instead of a dollar value, and, as a result, they bid at a higher premium when their valuations are high. Similar to Georganas and Nagel’s (2011) study of common value auctions, we found that in private value auctions the observed effect of toeholds is consistent with the theoretical prediction that toeholds lead to higher bids, but, on average, the magnitude of this effect is lower than predicted by the theory (Columns 5 and 6 in

Table 1 and Model 1 of

Table 2). Such lower magnitude may also be explained by subjects’ risk or loss aversion.

Another important observed result is how bidders with toeholds adjust their bidding strategies based on the toehold of the rival bidder. While the within-subject analysis (

Table 2, Model 1, Column 4) shows a positive effect of the rival’s toehold, such effect is very small (USD 0.287) relative to the value of the object (between USD 0 and USD 60 with step USD 3). Furthermore, an individual analysis for each object value (

Table 1, Column 4) shows no significant effect for all non-zero values of the object. The above allows us to conclude that one’s bidding function does not depend on the size of the opponent’s toehold. While such independence is consistent with the theory, we believe it shows not the subjects’ ability to comprehend the dual effect of the change in the opponent’s strategy due to the change in their toehold, but their inability to predict the change in the opponent’s behavior. Such ignorance of the opponent’s strategy is similar to the first-level reasoning behavior (Crawford and Iriberri, [

16]). Indeed, when the rival bidder has a toehold and bids above their value, the original bidder with toehold may decide to bid even higher because they may feel there is a higher chance that they will be able to run up the price without the risk of winning the auction. In equilibrium, however, the absolute value of the slope of the bidding curve for bidders with toeholds is less than one, hence, the marginal probability of winning the auction with an extra bid is higher when the competitor has a toehold. In equilibrium, the two effects (large competitor’s bids but lower slope of their bidding curve) cancel each other and, as Burkart [

5] shows, the equilibrium bidding function (2) is independent of the rival’s toehold. However, the data shows that, contrary to the theoretical prediction, the bid premium increase with the subjects’ valuation of the object, and, therefore, the observed slope of the bidding curve for bidders with toeholds is above one, while the theory predicts it must be below one. If subjects expect the competitors to behave the same way as they would have done in the same circumstances, they must expect the bid premium to increase (instead of decrease) with the value of the object, which makes it optimal to bid more in symmetric than in asymmetric auctions. Thus, the subject’s failure to adjust their bidding behavior based on the competitor’s toehold allows us to conclude that the observed independence result is not a result of equilibrium analysis. Therefore, even if it is consistent with the theory, such consistency can be better explained by subjects making two mistakes that cancel each other, or simply by the subjects’ inability to take into account the change in competitor’s behavior due to the change in their toehold.

{kind=link}