We analyze a class of contractual relationships with external enforcement and complete, but unverifiable, information. Two players interact over four phases of time, as follows. In Phase 1, the players write a contract. The contract directs an external enforcer (a court, for example) on how to intervene in the fourth phase, as a function of verifiable information.

In Phase 3, the players make decisions that are verifiable, but are not payoff relevant. For example, the parties may send messages to the external enforcer; the messages have no direct effect on the players’ payoffs.

In Phase 4, productive decisions and external enforcement occur. Interaction in this phase defines the physical outcome, which is denoted d. Let D be the set of feasible physical outcomes; we assume D is independent of the realized state. Fourth-phase interaction is constrained by technology and the institutional environment, as discussed later in this section.

2.1. Standard Mechanism Design Analysis

To this point, our description of contractual relationships has not indicated the precise structure of interaction in the third and fourth phases. A fully-specified model of any particular contractual relationship requires a more detailed account. In the standard mechanism-design approach to studying contract, theorists simplify the analysis by making (sometimes implicitly) three assumptions. First, theorists assume that all of the payoff relevant aspects of

D are either directly verifiable to the external enforcer or are directly controlled by the external enforcer. Second, whenever they assume that an aspect of

D is not directly controlled by the external enforcer, theorists assume that the external enforcer can compel fines or transfers that can be used to levy arbitrarily harsh punishments on individual players. For example, it is common in the literature to assume that, in Phase 4, the parties make verifiable decisions about (a) whether to trade an intermediate good and (b) a monetary transfer from one party to the other. After these decisions, the external enforcer can compel transfers or fines.

4These two assumptions motivate theorists to treat d as a “public decision”—that is, a decision made by the external enforcer. In other words, the players’ verifiable actions are modeled, for all intents and purposes, as alienable (taken out of the players’ hands). This assumption is commonly justified by noting that “forcing contracts” can be used to compel the players to take any specific action as a function of other verifiable events, in particular, the messages sent to the external enforcer in the Phase 3.

The third assumption theorists usually make is that the technology of interaction in Phase 3 is unrestricted. To be more precise, it is assumed that players have the opportunity to send and receive messages sequentially and simultaneously. It will be enough to assume that, in Phase 3, the players simultaneously and independently send messages to the external enforcer. Let be the set of possible message profiles.

These assumptions justify treating the players’ Phase 1 contracting problem as a standard mechanism-design problem, with fundamentals given by . The contract formed by the players in Phase 1 specifies a game form, which is defined by a message space, M, and an externally enforced mapping, . The game form can be equivalently written in terms of payoff outcomes, as , where is defined by for every . Then, for every state θ, the game form defines an induced game, , that is played in Phase 3. The game form is called a mechanism. Note that we focus on static mechanisms.

Behavior in the Phase 3 is modeled by Nash equilibrium, so the players’ contracting problem is one of “Nash implementation” ([

15]). A mechanism, along with a selection of equilibrium in each state, implies a

state-contingent value function,

, that gives the resulting payoff vector as a function of the state.

5 The revelation principle ([

17,

18] justifies constraining attention to (a)

direct revelation mechanisms, where players send reports of the state (so

), and (b) truthful reporting equilibrium, where each player honestly reports the state.

For a direct revelation mechanism

, we write

for the payoff outcome of the message game when player 1 sends message

and player 2 reports

. Thus, when the players send reports

and

in state

θ, the payoff is

. Whether truthful reporting is a Nash equilibrium in every state is captured by:

Definition 1: Mechanism is called incentive-compatible if, for each and all , and .

Implementation of a state-contingent value function is defined by:

Definition 2: Mechanism is said to implement value function v if it is incentive-compatible and for all .

Furthermore, we say that value function

v is

implementable if a mechanism exists that implements it. We let

V denote the set of all implementable value functions.

6 That is:

2.2. The Standard Model of Mechanism Design with Ex Post Renegotiation

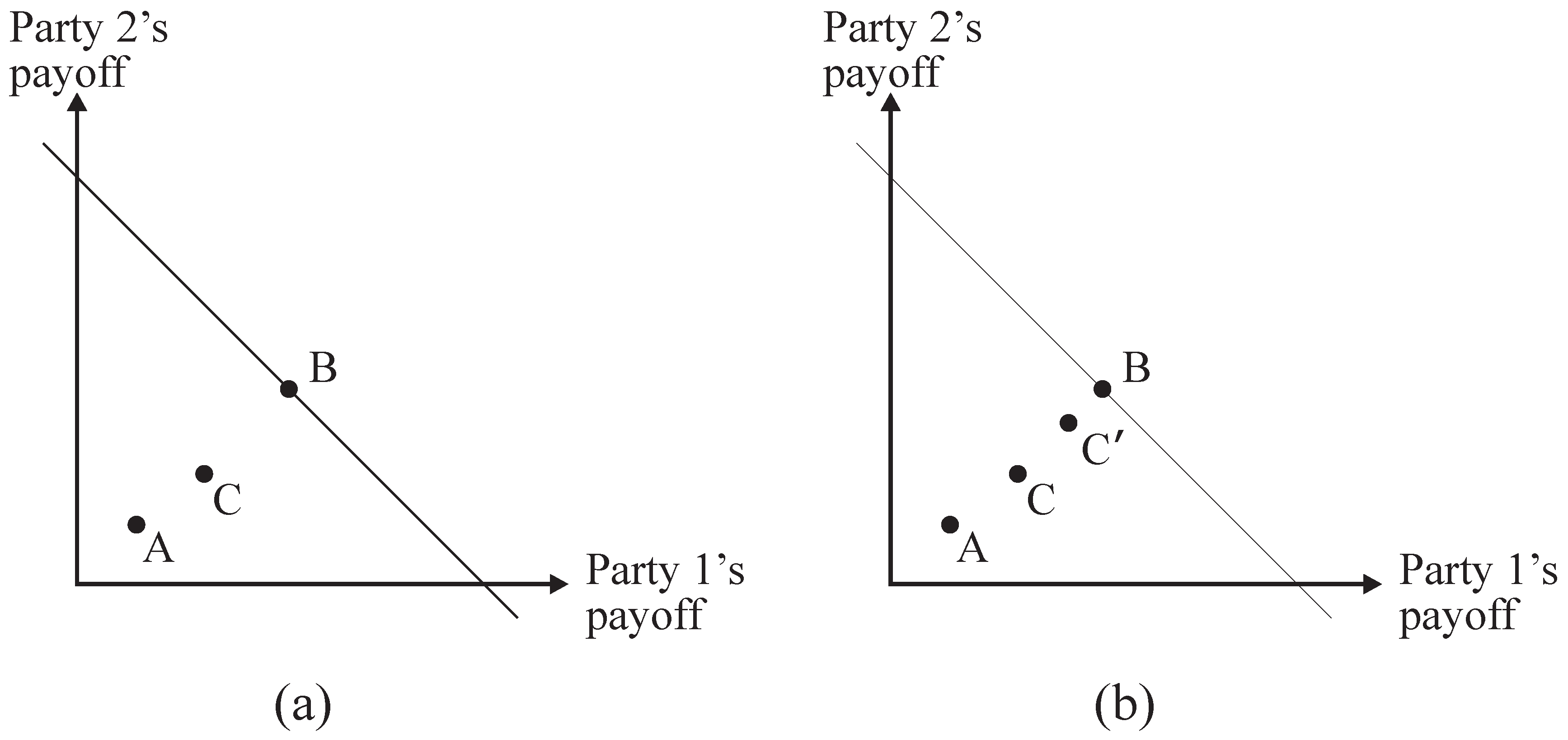

A key ingredient of the standard mechanism-design model is that the parties are committed to their chosen mechanism and, thus, to the public decision their messages prescribe. However, most real enforcement institutions do not allow such commitment. For example, it is not technologically feasible for a public court to administer an arbitrarily chosen mechanism. In addition, public courts do not enforce contracts verbatim, so, even if full enforcement of mechanisms were possible, institutional constraints limit the contracts that parties can choose.

Recognizing the real commitment problem, theorists have been led to study renegotiation of contracts. The following story illustrates the possibility of “

ex post renegotiation.”

7 Suppose the players agree to mechanism

in Phase 1; state

θ is realized in Phase 2; and, in Phase 3, the parties send reports of the state,

and

. Then, just after the reports are sent and assuming that the players each know the other’s report, the players realize that the external enforcer is poised to select public decision

in Phase 4. However, if

d is

inefficient in the realized state—that is, there is another public decision,

, such that

—then the players have an incentive to alter what their mechanism prescribes, instructing the external enforcer to make a different public decision than

d.

8 That is, the players can substitute some

for

, just before the external enforcer makes the public decision. If the players can renegotiate in this way, then they cannot commit to their original mechanism; instead, the original mechanism sets the default point for possible renegotiation contingent on the state.

9To model

ex post renegotiation, theorists have used the following clever trick (following [

1]). They specify a “renegotiation function”

, which gives the renegotiated public decision,

, as a function of the actual state,

θ, and the decision,

d, that the original mechanism prescribes. That is,

. Assuming that the players rationally anticipate renegotiation, this changes the induced game that they play in Phase 3. Rather than the message profile

yielding payoff vector

in state

θ, as would be the case without renegotiation, this message profile instead yields payoff vector

Accordingly, one can redefine the utility function to incorporate the renegotiation activity,

h. For every state

θ and every public decision

d, define:

Then, a setting of mechanism design with

ex post renegotiation, given by

, is equivalent to the standard mechanism-design problem defined by

.

2.3. A More General Approach

The analytical method described in the previous subsection is shorthand for explicitly modeling renegotiation activity. Although it has been useful in the literature, this shorthand method is not well-suited for studying settings in which renegotiation entails a cost. For example, suppose renegotiation requires payments to an attorney. To study this setting using the literature’s trick, one would have to define utility function to embody these payments. However, then we have a payoff-relevant aspect of strategic interaction (transfers made to a third party) that is not specified in the fundamentals of the mechanism-design problem. This contradicts the mechanism-design ideal—that all payoff-relevant aspects of interaction are included in the “outcome.” As a result, we cannot represent formally, for example, whether the external enforcer can take an action that achieves the same payoffs that could be reached with renegotiation. This is critical, because we need to compare, in payoff terms, the renegotiation technology with other technologies. Note as well that the renegotiation activity cannot be put in terms of the literature’s “h” function without including its payoff-relevant aspects in the definition of the “outcome.” Thus, it is not obvious even how to define whether renegotiation occurs.

The proper way of analyzing renegotiation while adhering to the mechanism-design framework is to (i) represent renegotiation activity in the fundamentals of the mechanism-design problem and (ii) represent noncontractibility of renegotiation behavior as a constraint on mechanism design. To make sense of this exercise, let us start from scratch by reviewing the building blocks of mechanism design.

Broadly speaking, in any design setting, the players are to interact in a “grand game.” Some aspects of the grand game are open to design, whereas other aspects are exogenously determined. In the standard mechanism-design model, the set of “public decisions” (outcomes) and their payoff consequences are exogenously given, but it is assumed that one can design a game form that arbitrarily maps to this set. Thus, to the extent that the public decisions represent individual actions of the players, these actions are assumed to be verifiable.

Renegotiation activity must be specified in the grand game as well. Because it generally is payoff relevant, we adhere to convention by including it in the specification of the outcome. In principle, an outcome could specify both a bargaining protocol (the manner in which renegotiation takes place) and the players’ actual behavior in this protocol. The key assumption is that renegotiation activity is non-contractible, so that the players cannot commit to how they will renegotiate.

10 In other words, actual renegotiation behavior must constitute an equilibrium, and this will depend on what occurred earlier in the game.

11To represent the renegotiation opportunity, we suppose that interaction in Phase 4 of the contractual relationship consists of renegotiation activity followed by a public action that the external enforcer compels. Let us denote the public action as x, and let X be the set of possible public actions. By way of interpretation, the external authority either directly controls x, or x is verifiable and can be compelled by the threat of external punishment.

At the beginning of Phase 4, there is a

default public action,

, that the players know will be chosen by the external enforcer if they do not renegotiate it. That is,

is the public action specified by the players’ contract for the given message profile from Phase 3. We summarize renegotiation activity in terms of (i) the renegotiated public action,

, and (ii) the vector of transfers and expenditures made by the players during the renegotiation process, which we denote by

t. Assume that

, where

Here,

is the transfer to player

i. Note that the total transfer is nonpositive; if it is negative, then the players’ jointly have a renegotiation expenditure.

As an example, an outcome of renegotiation may be “Each player pays $200 to an attorney, who modifies their contract so that ‘trade nothing’ is put in place of ‘trade 68 bushels of wheat at $15 per bushel’.” This specification of renegotiation activity is represented by , where and .

We use the term

minimal renegotiation activity to mean that the default public action is not renegotiated. Specifically, if

is the default public action, then minimal renegotiation activity is the case of

, where

. This concept will be important for stating the Renegotiation-Proofness Principle in

Section 3.

Renegotiation activity is non-contractible, due to either technological or institutional limitations, and therefore, the external enforcer does not control it. However, at the end of Phase 4, the enforcer compels x. Failure to renegotiate implies , so that the enforcer selects the default public action. Since the players know the state when they renegotiate, the renegotiation activity is described by some function, , that represents how is conditioned on the state, θ. Let Γ be the set of all such functions. Furthermore, we write , where and .

The physical outcome in Phase 4 is

, the default public action paired with the renegotiation activity. Thus, we have

. We assume that payoffs are additive in renegotiation expenditures. That is, there is a function

, such that, in every state

and for each outcome

, the payoff vector is

Thus, the players’ payoffs depend only on the state, the public action and any transfers and expenditures made during renegotiation.

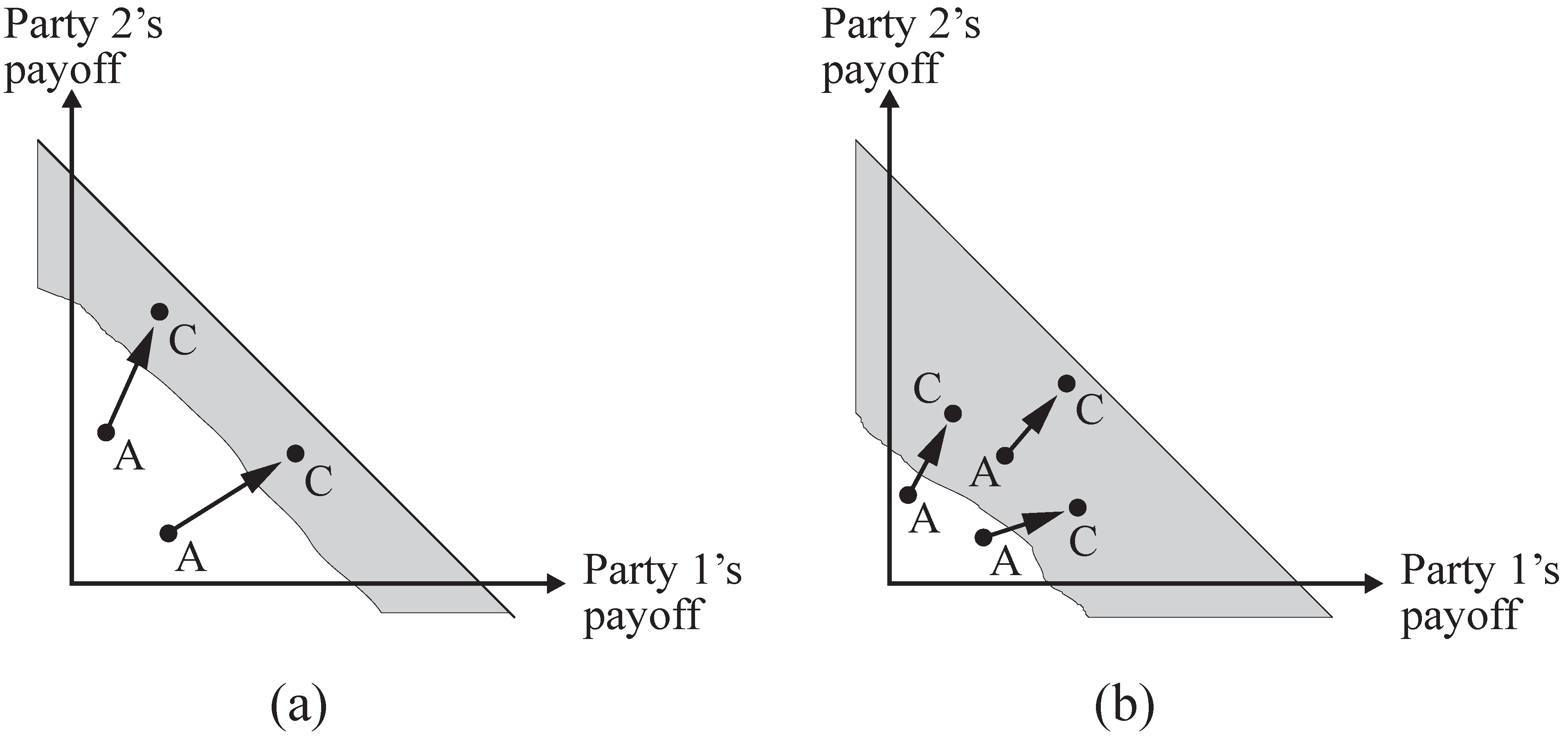

Here is a condition on public actions and payoffs that will play a role in whether the Renegotiation-Proofness Principle holds:

Definition 3: The contractual setting is said to be comprehensive if, for any state, , and any , there exists a public action, , such that .

This condition means that, for every state, any payoff vector that can be achieved through renegotiation can also be achieved with minimal renegotiation activity, with a suitably chosen default public action.

12As an example, suppose the default public action is “trade 50 units of the intermediate good at $20 per unit” and the decision is “trade 62 units of the intermediate good at $19 per unit.” Further suppose that is an efficient public action in state θ, meaning that maximizes by choice of x. Let and . Imagine that is specified as the default public action. In state θ, the players may renegotiate to select , with each player making an expenditure of 30, yielding the payoff vector . The expenditures may be money paid to an attorney whose services are required to alter a contract. Comprehensiveness would require the existence of another public action, , such that , a payoff which then could be achieved with minimal renegotiation activity . For instance, might be “trade 62 units of the intermediate good at $19 per unit and each donate 30 to charity.” Thus, a fairly broad range of contractible items is necessary for comprehensiveness.

Standard mechanism-design analysis can be employed for setting , except that there are now constraints on γ. These constraints fall into two categories. First, there may be institutional constraints. We represent these as feasibility restrictions on the renegotiation activity, as a function of the state. Specifically, in state θ and with default public action , the players’ renegotiation activity is restricted to some set . We are especially interested in how Y represents restrictions that are due to intrinsic costs of renegotiation—time spent bargaining and modifying the contract, payments made to attorneys, and so on. For example, renegotiating the default decision “sell 600 bushels of wheat at $10 per bushel” to another public action, “sell 500 bushels at $11 each”, may require a nonneglgble expenditure.

The second constraint on

γ is behavioral: it must be consistent with an appropriate theory of bargaining behavior. In other words, the selection of an element in

Y depends on one’s theory of negotiation. At this point, we do not adopt any particular bargaining theory, but we assume that the bargaining theory identifies a single element of

for every state

θ and every default public action

. Importantly, note that this selection is a function of both

θ and

, which are given at the beginning of Phase 4. Thus, there exists a function

, such that

is the outcome of renegotiation in state

θ, given default public action

. We call

y the

renegotiation function.

13Our analysis hereinafter takes function

y as fundamental. Keep in mind that this function represents both the constraints of

Y and the theory of negotiation. For notational ease, we sometimes write

. For a specific default public action

and a state

θ, we speak of

as the

disagreement payoff, and we call

the

renegotiated payoff.

In summary, the institutional and behavioral restrictions imply that the physical outcome in Phase 4 must be an element of the subset of

D given by

The set

is precisely the set of contractible physical outcomes for the setting of mechanism design with

ex post renegotiation. Thus, the setting,

, is equivalent to the standard mechanism-design problem defined by

. In words, because some aspects of interaction in Phase 4 are not controlled by the external enforcer, implementation is constrained by the theory of how these aspects are resolved. The physical outcomes that are consistent with the renegotiation theory are simply a subset of the set of all possible physical outcomes.

14As with the basic model of mechanism design, we can define the set of payoff outcomes as follows:

We let

be the set of payoff outcomes that have minimal renegotiation activity in state

θ:

2.4. A Class of Costly Renegotiation Functions

In this subsection, we describe a parameterized class of renegotiation functions to represent the idea that the players cannot extract all of the potential surplus from changing the contractually-specified public action. For example, suppose that public action

is about to be enforced in state

θ. If there is another public action,

, for which

then the players would like to renegotiate the default public action. However, this may require an expenditure. We suppose that the players must jointly pay

α in order to re-specify the public action. Further, they must pay fraction

β of the surplus created by changing the public action. A transfer between the players is unrestricted. The costs impose constraints on the feasible renegotiation activity, which are given by:

Here,

is the indicator function that equals zero when

and equals one otherwise.

Constrained to

Y in state

θ and with default public action

, the players’ available renegotiation surplus is:

We suppose that the players choose

x to achieve this surplus and that they select transfers to split the surplus according to fixed bargaining weights

and

, where

and

. That is,

solves (

2) and gives player

i the payoff

.

The renegotiation theory embodied in Equations

1 and

2 is quite flexible. For example, we obtain the standard “free-renegotiation” case (equivalent to the setting described in

Subsection 2.2) by specifying

. We also use the term “costless renegotiation” to describe this case. If

, but

, so that

then we have the case in which the players must pay only a lump sum,

α, to make any change in the specified public action. In the extreme, we could have

, which means renegotiation is not possible. Finally, when

, but

, then there are only proportional costs of renegotiation activity. In this case, the players renegotiate to the

ex post efficient public action, but they lose some fraction of the surplus to transaction costs.

In practical terms, α and β may represent transaction costs that are inherent in the process of negotiation or expenditures that must be paid to third parties. Here is a simple and realistic foundation: for a positive integer Λ, let the state be a vector , where for . Let the public action be a similar vector , where for . In this setting, productive interaction is multidimensional. Each dimension may be interpreted as an individual component of a good or service that one player provides to the other, where means that component λ is included (“on”). The state determines the set of desired components, meaning that it is optimal to set . Let the players’ joint value of the public action be .

Suppose that the legal institution requires contract modifications to be drafted and recorded in proper legal format, so that the players must employ the services of an attorney. It takes time and effort for an attorney to prepare the document, and this cost is increasing in the number of components that the attorney has to specify. Specifically, the attorney’s cost of providing the service consists of a fixed cost, α, and a cost of for each modified component. Assume that the market for attorneys is competitive, so the players jointly pay , where δ is the number of components modified. Clearly, the players want to modify every mismatched component (where ) and will obtain exactly the payoffs described earlier in this subsection.

{kind=link}

{kind=link}

{kind=link}