1. Introduction

Land is one of the most critical inputs in any production function (Chakravorty, 2013 [

1]). Its use is possibly the most essential feature that determines urban structure and urban growth, while its value shapes the dynamics of the real estate markets. The land leverage hypothesis states that houses with greater land leverage (i.e., land accounts for a large fraction of the house value) experience a higher price appreciation in a market where there are no increases in the construction cost (Bostic et al., 2007 [

2]). For example, a study investigating the Washington, DC metropolitan area from 2000 to 2013 found that variations in land leverage during boom periods notably predicted variations in house prices during bust periods; in addition, land prices were much more volatile than house prices (Davis et al., 2017 [

3]).

There are other reasons why the value of land is important, for instance the fact that land value represents a large portion of an individual household’s wealth (e.g., Bostic et al., 2007 [

2], Bourassa et al. [

4]). From a local government’s perspective, land value and land-use regulations reciprocally affect each other; such regulations can be related to urban structure (e.g., McMillen & MacDonald, 2002 [

5]), urban growth (e.g., Capozza & Helsley, 1989 [

6]), or property taxes. Finally, land value is also relevant nationally, being an important part of the National Balance Sheet (e.g., Wentland et al., 2020 [

7]). Although land values play such a critical role in the economy, data on them are often difficult to access.

Given the dearth of information on land values, land price is typically measured using one of the following decomposition methods: the vacant land method, the construction cost method, or the hedonic regression method. In the housing prices literature, it has long been acknowledged that housing characteristics should be controlled for in order to maintain a constant quality of the housing price index. Similarly, a well-established fact in the price decomposition literature is that the physical attributes of a house, especially its age, cannot be ignored if one is to obtain a constant-quality price index. However, the literature on the importance of land features is still relatively scarce. Like other price indices, the ideal land price index should represent changes in land prices that are comparable in quality over time.

The importance of geographic features (e.g., proximity to a waterbody, mountains, or wetlands) in urban development and housing supply has generated a growing literature focused on measuring the role of amenities. For instance, Burchfield et al. (2006) [

8] related terrain ruggedness and access to underground water to the density and compactness of new real estate development. Saiz (2010) [

9] showed that residential development is considerably constrained by the presence of steep-sloped terrain and found that most areas with inelastic housing supply are severely land-constrained by their topography.

This paper attempts to fill the gap in the decomposition literature by modeling land slope, a proxy for land quality and a factor that possibly discounts land prices, in order to estimate quality-adjusted land price indices. Similar to having constant-quality housing structure price indices, having constant-quality land price indices also requires the properties of the land (e.g., land area and location) to remain constant over time. Of equal importance is the need to take into account the physical attributes of land, especially the land’s slope, as these attributes can impose constraints on land development and use. On the one hand, sloping land adds complexity to construction (e.g., extra drainage and extra work in stepping the foundations) and limits land use, hence increasing the construction cost and discounting the land value. On the other hand, sloping land may afford better views, which could increase the property value.

This paper adopts and extends the builder’s model (Diewert et al., 2011 [

10]) by incorporating the terrain slope to estimate the hedonic pricing of land and to construct constant-quality land price indices; this is done based on data from selected neighborhoods with hilly features from Auckland, New Zealand during the period 2007–2016. Land parcel slopes are prepared in three steps. First, terrain slopes are calculated from the 2013 1-m Digital Elevation Data (DEM) for Auckland. Mean terrain slopes are then calculated for each land parcel extracted from the map of New Zealand Primary Land Parcels. The Address Information Management System (AIMS) from Land Information New Zealand (LINZ) is then used to link land parcels to sales data. In the literature of property appraisal, the residual method of valuation helps the property developers identify a piece of land’s re-development value (e.g., Pagourtzi et al., 2003 [

11]). However, the residual valuation method requires an estimate on development costs, including the project’s construction cost and investor’s profit, based on extensive forecasting and many assumptions, making the method susceptible to small changes in the assumptions (Isaac, 1996 [

12]). In the builder’s model, the use of the exogenous price of the structure per square meter to value the property’s structure makes sure that the land value is the residual value of the property transaction value.

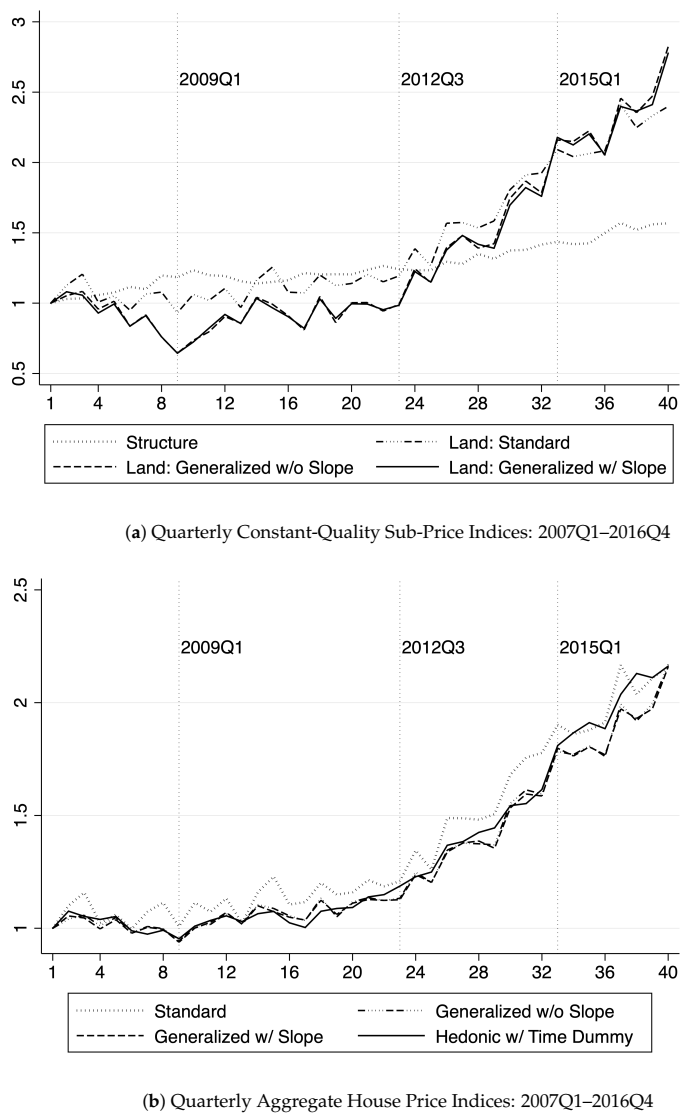

Results reveal a slope discount on the price of land per square meter, controlling for land size, land location (i.e., based on school enrollment zone), floor area, age of the house (i.e., in decades), and numbers of rooms. The constant-quality land price indices moderately decrease after controlling for terrain slope, whereas the imputed Fisher chained house price index remained almost unchanged. On the whole, land slope does appear to be an important hedonic characteristic associated with land and hence with house values. However, when the land slope composition does not change over time, having a slope as an additional land characteristic generates minimum effects on the quality-adjusted land price indices.

2. Materials and Methods

2.1. Four Methods to Compute House Price Indices

There are four primary methods for computing price indices for residential properties: stratification, repeat-sales, appraisal-based methods, and hedonic approaches. More details about computing property price indices can be found in Bailey et al. (1963) [

13], Bourassa et al. (2006) [

14], Clapp and Giaccotto (1992) [

15], De Vries et al. (2009) [

16], Wallace and Meese (1997) [

17], Wood et al. (2005) [

18], and Shiller (1991) [

19]. Most recently, Lopez and Hewings (2018) [

20] also introduced a method that is based on the repeat-sales (i.e., Case–Shiller) method, while being more flexible; this idea was first suggested by McMillen (2012) [

21]. The hedonic regression method is typically the best approach for constructing a constant-quality residential property price index. A typical hedonic estimator expresses housing prices or their logarithm as a linear function of structural and location attributes. The commonly used hedonic approaches for computing price indices include the hedonic imputation method and the hedonic price method with dummy variables for time.

For the hedonic imputation method, a hedonic regression is initially estimated for each time period separately. For example, consider that there are

and

houses with

K characteristics

and

sold in period 0 and period 1, respectively. The following hedonic functions are estimated first:

where

is the predicted sale price of house

i sold in period

t. Next, the change in the quality-controlled house price between two periods is constructed as the price difference between the observed house price in one period and the imputed price; this is only done if the attributes from one period were evaluated at the same estimated prices in the other period. The price of the housing characteristics of period 0, which was imputed in period 1, is denoted as

. Similarly, the price of the housing characteristics of period 1, which was imputed in period 0, is denoted as

. Holding housing characteristics constant but separate across both period 0 and period 1, we can construct, for example, the following quality-adjusted imputed house price indices:

Other important imputed price indices include the Fisher, Geometric-Paasche, Geometric-Laspeyres, and Törnqvist price indices (Hill & Melser, 2008 [

22]).

As its name suggests, the hedonic price method with time-dummy variables utilizes cross-sectional data on house prices, which is then expressed in a single equation as a linear combination of time dummies and quality-controlled structural and location attributes. The equation is written as follows:

where

represents a set of dummy variables that take on the value of 1 if house

i is sold at time

t and of 0, otherwise. Moreover,

is interpreted as the quality-adjusted price difference between time

t and the baseline time.

A notable problem with the hedonic approaches is that there is often a high correlation between the explanatory variables, which makes the estimated coefficients unstable. As discussed in OECD et al. (2013) [

23], multicollinearity is less of a concern if the purpose is to construct an overall constant-quality house price index. However, when the parameters of interest are the coefficients of the physical attributes (e.g., the number of bedrooms) and when the goal is to decompose the overall price index into the land price index and the price index of the housing structure, multicollinearity can be a problem. Schwann (1998) [

24] and Diewert et al. (2011, 2015, 2016) [

10,

25,

26] provide a discussion on multicollinearity.

2.2. Standard Builder’s Model

The builder’s model was first discussed by Diewert (2008) [

27] and then introduced by Diewert et al. (2011) [

10]. It aims to decompose residential price indices into two sub-price indices: a quality-adjusted price index for the housing structure and a price index for the land on which the property is built. This derivation originates from a cost of production approach. From a builder’s perspective, the sales price of any property after completion is its expected cost. The expected cost of a property is denoted as the sum of the housing structure cost and the cost of the land on which it is built. The cost of the structure is calculated by multiplying the floor area of the property (e.g., in square meters) by the unit cost of construction (e.g., construction cost per square meter). The cost of the land is calculated by multiplying the land area (e.g., square meters) by the unit cost of land (e.g., cost per square meter). The assumption that the values of land and those of the housing structures are additive is suggested in most of the literature. This includes but is not limited to Bostic et al. (2007) [

2], Diewert (2008) [

27], Diewert et al. (2011, 2015, 2016) [

10,

25,

26], De Haan and Diewert (2013) [

28], and Francke and van de Minne (2017) [

29]. Mathematically, the basic builder’s model has the following formula:

where

represents the sales price of property

i at time

t;

and

are the prices of the land and of the housing structure per square meter at time

t, respectively;

is the land area of property

i at time

t; and

is the floor area of property

i at time

t. The error terms

are assumed to be heteroskedastic, not serially correlated, and mean independent of the covariates.

In essence, the hedonic regression defined in Equation (

6) only works for newly built properties. To acknowledge the fact that properties sold at time

t include not only newly built properties but also existing older properties, and that older properties are usually worth less than newer properties because of the depreciation of their housing structure over time, Equation (

6) is commonly modified by incorporating the age of a property into the baseline builder’s model:

Here,

represents the age of property

i at time

t, while

represents the net straight-line deprecation rate as the housing structures of properties age. One can also assume that deprecation rates change over time:

Common units of measurement for

include years and decades. Therefore,

can be either the net depreciation rate per year or per decade. Reasonable net annual depreciation rates are in the 0.5–2% range.

If properties are well-maintained or renovated over time, the deterioration of aging properties can be slowed down and, in some cases, older properties may even command a premium. Knight and Sirmans (1996) [

30] found that houses with lower-than-average maintenance levels depreciate 0.9% faster per year, while Harding et al. (2007) [

31] found that well-maintained houses depreciate 0.5% less per year when compared to the average house. Moreover, older structures can produce functional obstacles (Rubin, 1993 [

32]), which can then negatively affect property values. Nevertheless, as housing structures age, some of their aspects may lead to a positive effect on their property value, for example if their design is characteristic to a specific time period. This is recognized as the vintage effect (Coulson & Lahr, 2005 [

33]) and can even offset the negative effects of age. For example, Meese and Wallace (1991) [

34] found that housing prices increase with age.

Coulson and McMillen (2008) [

35] extend the method proposed by McKenzie (2006) [

36] to estimate the time, age, and cohort (i.e., vintage) effects simultaneously. Their results show a U-shaped effect of age on housing prices. On the one hand, property prices decrease significantly in the first few years post-construction, while, on the other hand, very old houses have notably high price premia. More recently, Francke and van de Minne (2017) [

29] estimated all three age effects on property structures, as well as the time effect on land values. As the builder’s model only includes age as a predictor of the housing structure value,

should be interpreted as the net effect of age on the structure of a property. Then,

can be interpreted as being the older structures measured in the units of new or more recent structures. Therefore, due to maintenance information being unavailable, very old structures have been excluded from the model. Burnett-Isaacs et al. (2017) [

37] defined old houses as those older than 60 years.

The problem with the straight-line method of modeling depreciation is that the value of the structure can become negative if the structure is old. Therefore, the geometric method is commonly used in national-level research as an alternative to the straight-line method. The builder’s model with geometric depreciation has the following form:

where

represents the net geometric deprecation rate as the housing structures of properties age. With geometric depreciation, structures deteriorate at a constant rate over time, whereas with a straight-line depreciation structures deteriorate by constant amounts. In practice, empirical studies suggest that it is more appropriate to use the geometric method for residential properties (Chinloy, 1977 [

38]; Malpezzi et al., 1987 [

39]).

2.3. Generalization of Standard Builder’s Model

Diewert (2008) [

27] suggested that the basic hedonic decomposition can be generalized to incorporate more of the attributes used in the standard hedonic model; this can be done in the following way. Suppose

are

M determinant attributes for the quality of land and

are

H determinant attributes for the quality of the housing structure; then, the generalized builder’s model with geometric depreciation is:

where

is the quality-adjusted price for land at time

t, and

is the quality-adjusted price for a housing structure at time

t. In the literature, location-related attributes are generally used to control for the quality of land. These typically include the distance to the city business center, the zone (e.g., zip code or school zone), and the street pattern of the land on which a property is built, such as if there is an intersection of two streets or a cul-de-sac. Recent work by Pan et al. (2018) [

40] suggests that the distance from the Central Business District (CBD) is just one of the many attributes valued by consumers, and hence the land-use changes in a metropolitan region may reflect multiple dimensions of accessibility. Structure characteristics that are controlled for consist of physical attributes such as the number of bathrooms or bedrooms.

For this paper, the school enrollment zone will be incorporated into the model as one of the land characteristics and the numbers of rooms, including both bedrooms and bathrooms, will be used as an additional structural attribute in the generalized model:

In this specification, both school zones and numbers of rooms are entered as dummy variables. In addition, to avoid the dummy variable trap, one group from each variable is dropped.

2.4. Builder’s Model with Terrain Slope

The hedonic literature often adjusts for the quality of housing structures, but there is also a need for quality adjustments when it comes to land characteristics. Cheshire and Sheppard (1995) [

41] pointed out that, as land itself is a composite good, land price represents a composite of the price of pure land, the price of the neighborhood and environmental characteristics, and the price of the embodied local public goods.

The theory of land use has its origin in the monocentric city model developed by Alonso (1964) [

42], Mills (1967) [

43], and Muth (1969) [

44]. The traditional monocentric city model treats land as a featureless flat plain, so that locations only differ in their distances to the Central Business District (CBD). Thus, the model predicts that the land prices and the housing density are both higher in those areas closer to the CBD. Later urban economic models extend the monocentric city model to include environmental amenities such as open space (e.g., Anderson & West, 2006 [

45]; Geoghegan, 2002 [

46]; and Irwin, 2002 [

47]) and to allow for multi-centric structures (e.g., Anas & Kim, 1996 [

48]; McDonald & McMillen, 1990 [

49]; Wieand, 1987 [

50]), in order to explain a more complex spatial structure. In addition, more recent literature relaxes the featureless flat plain assumption commonly used in urban economic models. For example, Keenan et al. (2018) [

51] developed a conceptual model of what they called climate gentrification and found that price appreciation is positively affected by the incremental increase in elevation in the Miami-Dade County, Florida, which supports the elevation hypothesis. Similarly, Ye and Becker (2017) [

52] studied seventeen US cities and found that high-income households prefer to live at higher elevation levels. They also found that the standard deviation of the elevation and that of the relative altitude both positively affect the density and the housing value gradients.

This paper will focus on the terrain slope. If a particular area is flat, then the topography may not influence a house’s location and layout; however, on a sloping site, the topography is likely to significantly influence house design. (Flat areas are never strictly horizontal. Instead, they are characterized by gentle slopes that are often hardly noticeable to the naked eye.) Sloping sites present a number of challenges and generally require a greater design input when compared to flat sites. For example, they usually require additional geodetic assessments of slope stability and earthworks before the actual house construction stage. Depending on the steepness of the slope, sloping sites usually have to be cut, filled, and/or retained in order to prepare level plinths on which concrete slab foundations and floors can be laid out.)Increasingly, new houses in New Zealand are built on a concrete slab.) Building on a sloping site may also require additional drainage and sewers. Therefore, the overall construction costs on sloping sites are higher than the overall construction costs on flat sites, which is essentially attributable to the additional amount of cutting, filling, and engineered retaining walls. These costs generally increase with the degree of the slope.

Consequently, in mountainous regions, land slopes might also significantly contribute to the formation of quality-adjusted land prices. Around Auckland, land is visibly uneven, with many houses having been constructed along sloping driveways. If the sample of houses sold in period t consists of more houses on sloping sites than the sample of similarly structured houses sold in previous periods, then changes in topographical characteristics should not be interpreted as changes in land prices over time. If the slope negatively affects housing prices, then it is important to control for this slope; otherwise, the land price index for period t will be underestimated.

We acknowledge that the degree of slope places substantial limitations on the use of land and may add considerable costs to construction due to earthworks projects. Therefore, land slope is modeled as a determinant of land price; other determinants included in the model are land size and the school enrollment zone, which represent the location and the public service associated with a site, respectively. The model can be written as follows:

where

is the constant-quality land price index (i.e., the “pure” price of land per square meter), and

is the constant-quality structure price index.

On the one hand, if the ideal site for residential housing is that which provides the desired degree of space at the lowest costs, the difficulty of building on sloping land could mean that the price of a sloping site may be considerably lower than that of a flat site, hence decreasing property values. On the other hand, sloping land may provide better views, hence increasing property values. Due to data limitations, we could not obtain the cost of slope-induced earthwork or the cost of slope-induced superior. Therefore, the estimated coefficient of the slope should be interpreted as the joint effect of these two opposing forces.

The following hypotheses summarize the possible effect of land slope on its hedonic price :

Hypothesis 1(H1). If slope-induced construction difficulty has a greater influence than the slope-associated view, then a negative relationship between house price and land slope is expected.

Hypothesis 2(H2). If the slope-associated view is more important than the slope-induced difficulty to build, then a positive relationship between house price and land slope is expected.

Hypothesis 3(H3). If the slope-induced construction difficulty and the slope-associated view are either equally important or are neither an important house price determinant, then a statistically non-significant relationship between house price and land slope is expected.

When it comes to computing the quality-adjusted land price indices, the following cases summarize the possible changes in land price indices once we control for land slope:

- Case 1:

If the slope has a negative (positive) effect on the housing price, and if the sample of houses sold in period t consists of more houses built on sloping sites than the sample of similarly structured houses sold in the baseline period, then controlling for slope would adjust the land price index for period t upward (downward).

- Case 2:

If the slope has a negative (positive) effect on the housing price, but the amount of houses sold that were also built on sloping sites does not differ between period t and the baseline period, then controlling for slope would not affect the land price index for period t.

- Case 3:

If the slope has no significant effect on the housing price, regardless of the land slope composition over time, then controlling for slope would not affect the land price index.

2.5. Data

The analysis in this paper relies on a data set that combines information on housing sales and on land parcel slopes of sold houses.

2.5.1. Sales Data

Property-level sales data on three Auckland school enrollment zones between January 2007 and December 2016 was purchased from Quotable Value Limited (QV), powered by CoreLogic NZ Ltd, an entity responsible for conducting property market valuations in New Zealand. The data encompasses the Double Grammar Zone (i.e., an overlapping area of enrollment zones of the Auckland Grammar School and Epsom Girls’ Grammar School), the Selwyn College zone, and the One Tree Hill College zone.

Sales data contain information on sales price, sales date, property address, and a set of structural property attributes. The analysis is targeted at all types of houses, but it excludes apartments. We include residential properties with fully detached or semi-detached houses that are situated on their own clearly defined piece of land, while removing those units with missing or misreported information. Outliers for sales price, land area, floor area, bedrooms, and bathrooms are dropped by year of sale within each school zone. First, the bottom 1% and the top 3% of sales prices are dropped. Then, the top 1% of land areas are trimmed, followed by the top 1% of floor areas. The data set is further filtered by eliminating those observations with the number of bathrooms and the number of bedrooms being in the top 1%. We also exclude houses that were built before the 1950s. The final sample contains 5657 observations for the period 2007–2016.

Two land characteristics of the sales data used in this analysis are the land area (m

) and the school enrollment zone in which the land is located. Structural characteristics used in the analysis include the building’s age and its floor area (m

). The original age of the building is coded in decade-long construction periods, such as the 1940s and the 2010s. Following Diewert et al. (2015) [

25], the original age of the building is recoded into decade age using the following procedure: the most recent construction period for any of the houses sold between 2007 and 2009 was the 2000s. Hence, the age variable for the construction decade is calculated as (2000–construction period)/10. From 2010 onward, the newest houses sold were built in the 2010s. Hence, the corresponding age variable is calculated as (2010–construction period)/10. After this recoding procedure, a house built in the 2000s and sold between 2007 and 2009 has a decade age of 0, whereas a house built in the 2000s that was sold in 2010s has a decade age of 1.

Table 1 presents the descriptive statistics for the sample of interest. On average, the houses in the sample were built two decades ago. The sample’s mean sales price is 1,164,640 NZ dollars (NZ

$), with an average land and floor area of about 580 m

and 217 m

, respectively.

2.5.2. Computing the Land Slope

The land slope used in this paper is obtained from a light detection and ranging (LiDAR) 1-meter resolution digital elevation model (DEM) fitted to the map of New Zealand Primary Land Parcels using ArcGIS. Both maps are converted to the New Zealand Transverse Mercator 2000 (NZTM2000) projection for analysis.

The airborne Auckland LiDAR 1m DEM data was captured in 2013 for the Auckland Council by NZ Aerial Mapping & Aerial Surveying Limited. It was collected at a point density of more than 1.5 points per square meter. The 1 m DEM data was downloaded from the Land Information New Zealand (LINZ) Data Service. More information about DEM can be found at

https://data.linz.govt.nz/layer/53405-auckland-lidar-1m-dem-2013/ accessed on 9 February 2019. Elevation values are measured in meters. In ArcGIS, the unit of measure for the z (elevation) unit is also the meter, so the z-factor of value 1 is used to calculate the percentage by which the values of slopes rise in each DEM cell (i.e., the rate of change in elevation). (There are two options for the units of measurement for terrain slope: degree values and percentage elevation values. Please see

Appendix A for more information.)

The map of the New Zealand Primary Land Parcels was also downloaded using the LINZ Data service. More information about NZ Primary Parcels can be found at

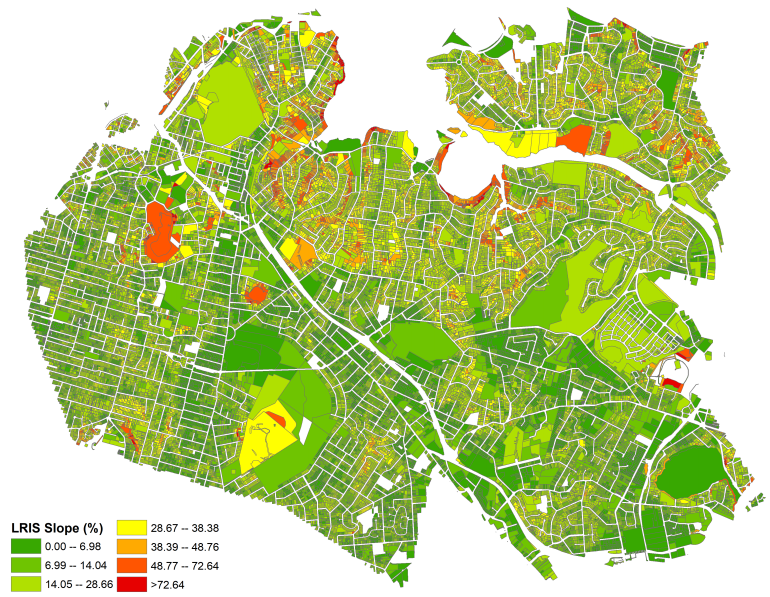

https://data.linz.govt.nz/layer/50772-nz-primary-parcels/data/ accessed on 11 February 2019. To determine the terrain slope of each land parcel, the Zonal Statistic tools in ArcGIS were used. Each land parcel on the land parcel map was treated as an input zone, and the parcel ID was used to define the zones. The raster created from the 1 m DEM contains the slope values and is then used to calculate each parcel’s mean slope. The resulting map of parcel slopes is depicted in

Figure 1. For reference, an aerial map of the study area is shown in

Figure 2.

Table 1 reports that the average slope of the sample is 18.55% or 10.51°. The slopes are then divided into six broad groups according to the slope classes from the Land Resource Information System (LRIS). (Please see

Appendix A Table A1 for a range of slope classifications from different countries.) As presented in

Table 2, the groups to be used in the analysis are: flat to gently undulating (0–3°), undulating (4–7°), rolling (8–15°), strongly rolling (16–20°), moderately steep (21–25°), and steep (26–35°). (Observations with a slope of more than 35°were also excluded from the final sample.)

Table 3 shows that 41.7% of the sample is in the rolling slope range. The correlations of the land slope with the land area, floor area, and the total number of rooms are 0.2285, 0.2148, and 0.1462, respectively.

2.5.3. Linking Parcels with Addresses

To link the computed land parcel slopes to sales data, the Address Component data from the LINZ’s Address Information Management System (AIMS) is used. (More information about the AIMS Address Component data can be found at

https://data.linz.govt.nz/table/53354-aims-address-component/data/ accessed on 1 March 2019. AIMS Address Component data contains information on address ID, parcel ID, and on the components of each address, such as address number, street number, and road name. Parcel ID is used to link the mean slope data to the AIMS data. Address components are combined to a single full address based on the address component order; this address is then linked to the sales data.

4. Discussion

The importance of separating the housing structure from the land has been previously well established, but the practical difficulties of separating these two elements remain. Unlike structure, land is not reproducible. Land parcels differ not only in their location and size but also in their slope and other topographical features. Therefore, in order to form reliable constant-quality land price indices, it is necessary to control for those physical attributes of land that can intrinsically limit land use and thus possibly decrease land values.

This paper aimed to demonstrate how a land-specific topographical characteristic—the terrain slope—can be incorporated into the builder’s model. Based on a small neighborhood in Auckland where sloped terrain is common, our analysis revealed a so-called slope discount: Having a lower land price per square meter compensates for the difficulty and complexity of building on sloped land. This result should not be directly generalized to other locations with a sloped terrain. Instead, as discussed in

Section 2.4, it should be taken into consideration that there are two forces through which the land slope can affect land prices. The land slope may decrease land prices because of the increased complexity and cost necessary to build on such land, but it may also increase land prices due to the potential superior views. Which of these two forces is more influential may depend on the local topography. For instance, in locations where the slope can provide aesthetic advantages, such as a spectacular view of a lake or a mountain, it is reasonable to expect a price premium for sloping sites. Our findings suggest that the land slope has a negligible impact on the quality-adjusted land price index when the composition of the sloped houses sold remains stable over time. Once again, this should be interpreted cautiously, as it does not necessarily imply that the land slope is of no importance to the quality-adjusted land price indices. In 2018, the official magazine of the Registered Master Builders Association (RMBA) in New Zealand,

Building Today, reported that, although there continues to be strong demand for flat land, consumers’ attention is now turning to sloping land. Please refer to

https://www.buildingtoday.co.nz/2018/04/10/the-invisible-costs-of-building-a-house-in-nz/ accessed on 21 March 2019. There is a possibility that, over time, with an increasing amount of new houses being built on sloping land, the effect of including the land slope in quality-adjusted land price indices may become more critical. In addition, for instance, as the subdivision of hilly areas becomes a problem in Los Angeles, there might be fewer houses that are built on sloping sites and sold over time; in such a case, ignoring the variation in land slope composition would lead to biased land price indices.

Our results also seem to support the idea that using the builder’s model with only four explanatory variables (i.e., land area, location of the house, floor area, and house age) generates credible overall house price indices and reasonable sub-price indices for the land and the housing structures. However, the moderate change in land price indices after including land slopes may also be a result of our small sample size, since our study area only encompasses three neighboring school enrollment zones in Auckland. It would be also relevant to investigate this effect when applied to a larger spatial context with more sloped observations.

The other limitation of this study and possible area of investigation for future studies is the fact that the model used in this paper has a rather restrictive specification. It assumes that land price differences between school zones and across degrees of land slope do not change over time. However, it is likely that land in the most sought-after school zones may appreciate more than that in other areas. Similarly, the prices of less steep land may increase faster over time than those of steeper land due to the scarcity of such flat land, especially in hillier areas. Therefore, multiplicative interactions between these two variables and time may be important. In addition, sloping land can be subjected to higher risks due to natural hazards. For example, the city of Christchurch experienced extensive soil liquefaction in 2010 and 2011 as a result of a series of large-scale earthquakes. Port Hills, the hilly part of the city, also experienced landslides and rockfalls. Based on this, investigating the interaction between the slope of land and the risk of natural hazards would be an interesting topic for future research.

{kind=link}

{kind=link}

{kind=link}

{kind=link}