1. Introduction

China is a large agricultural country where agricultural land is the foundation of the rural social and economic system [

1,

2]. The system of agricultural land is not only closely related to agriculture, rural areas and farmers, but also directly affects the overall development level of the national economy. China’s agricultural land system has its own particularities. Land belongs to the state or collective, and private ownership is not allowed. In the past, the law prohibited the mortgage of agricultural land. In recent years, the separation of the ownership, contracting rights and management rights of agricultural land was proposed, and mortgage financing of land management rights was allowed in China [

3,

4,

5,

6]. The rural land mortgage system has Chinese characteristics. The Central Committee of the Communist Party of China (CPC) has long promoted comprehensive rural reform and supply-side structural reform, and the reform of the agricultural land system has been the core content [

7,

8,

9]. After a long period of practice, the system of agricultural land mortgaging in developed countries is relatively mature [

10,

11]. With the introduction of the concept of land use transition into China [

12,

13,

14,

15], woodland and cultivated land have been the hot spots of land use transition research [

16,

17]. The transfer of rural land contractual management rights belongs to the recessive transformation of land use. The mortgage of rural land management rights is a way of rural land circulation, which will have an important impact on the transformation of land use. Rural land management rights mortgage loans can enable farmers to obtain more credit funds, which is conducive to agricultural development and rural revitalization.

The mortgage financing of farmland management rights is an important means for the government to support agriculture through the financial market and plays a positive and effective role in the development of rural finance [

18,

19,

20]. However, as a new financial product, there are still many obstacles and restrictive factors in the financing of farmland mortgages in China. Among them, the risk problem is the greatest obstacle, which restricts the development of farmland mortgage financing and affects the implementation of mortgage financing through farmland management rights. Therefore, based on promoting land circulation, preventing and controlling the default risk of the mortgage of farmland management rights, and minimizing the cost of financial institutions supporting agriculture, rural areas and farmers have become a topic of wide concern to the state and all sectors of society.

In this regard, many studies have addressed risk types, empirical cases and the risk control of farmland management right mortgages. Agricultural land mortgage financing entails many types of risks, such as credit, nature, market (operation) and policy (system) [

21,

22,

23,

24,

25]. The risks of agricultural land mortgage financing are reflected in the risk of farmers’ livelihood and the repayment source risk of banks at the micro level and in the rural social risk and rural financial risk at the macro level [

26]. The regression analysis method and AHP method were used to demonstrate the factors that affect credit risk and predict the probability of default [

27,

28,

29]. Studies have shown that the bank credit system, relevant systems, mortgage and disposal conditions, and risk compensation and sharing mechanisms were the key points of risk management [

26,

30].

In addition, the unclear property rights of farmland as collateral and high market transaction costs were the main causes of the risks perceived by financial institutions, such that the institutions did not actively lend to farmers who applied for loans with such collateral [

31,

32]. A prerequisite for effective agricultural land mortgage development is the development of effective instruments for the risk management of creditors in the pledging of agricultural land [

33]. Yin [

34] conducted empirical research on the risk measurement of mortgage loans on rural land contracts and management rights in Heilongjiang Province.

Previous studies on rural land mortgages have mainly focused on the willingness of actors on the supply and demand sides, financial innovation mechanisms and performance, and loan risk evaluation systems, and these studies mainly used the questionnaire method or model prediction within a certain area. The content of such surveys reflects the ideas of the respondents, not the objective situation, and conclusions based on such information lack scientific support. The above studies are important, but there is no precedent for statistics of rural land mortgage default cases nationwide.

In recent years, with the help of big data, legal judgment documents are increasingly applied to many fields [

35,

36]. This article uses the empirical research method to study the cases of rural land mortgage default judged by the first instance of the national court during 2014–2020. The 724 default cases in this article are all confirmed cases by the court and the data are true and reliable. According to the phenomenon of rural mortgage default, the formation mechanism of rural land mortgage loans is analyzed. Along with the court cases, the competent department of agricultural land mortgage finance of Heilongjiang Province is investigated. The research method of this article is highly objective and rigorous. It is of great significance to understand the characteristics of rural land mortgage default from all over the country and to reduce the risk of default.

5. Conclusions

The reform of rural land ownership, contract rights and management rights not only represent an innovation of the rural land system with Chinese characteristics but is also the only way to develop modern agriculture. At present, rural land mortgage has been carried out all over the country, but the empirical research on rural land mortgage default is few. According to the court’s judgment, this paper comprehensively analyzed the characteristics of defaults in different regions of China during 2014–2020 and explained them. This can provide a reference for the governance of default risk of rural land mortgage. In the field of recessive transformation of agricultural land use, the topic is also worth studying.

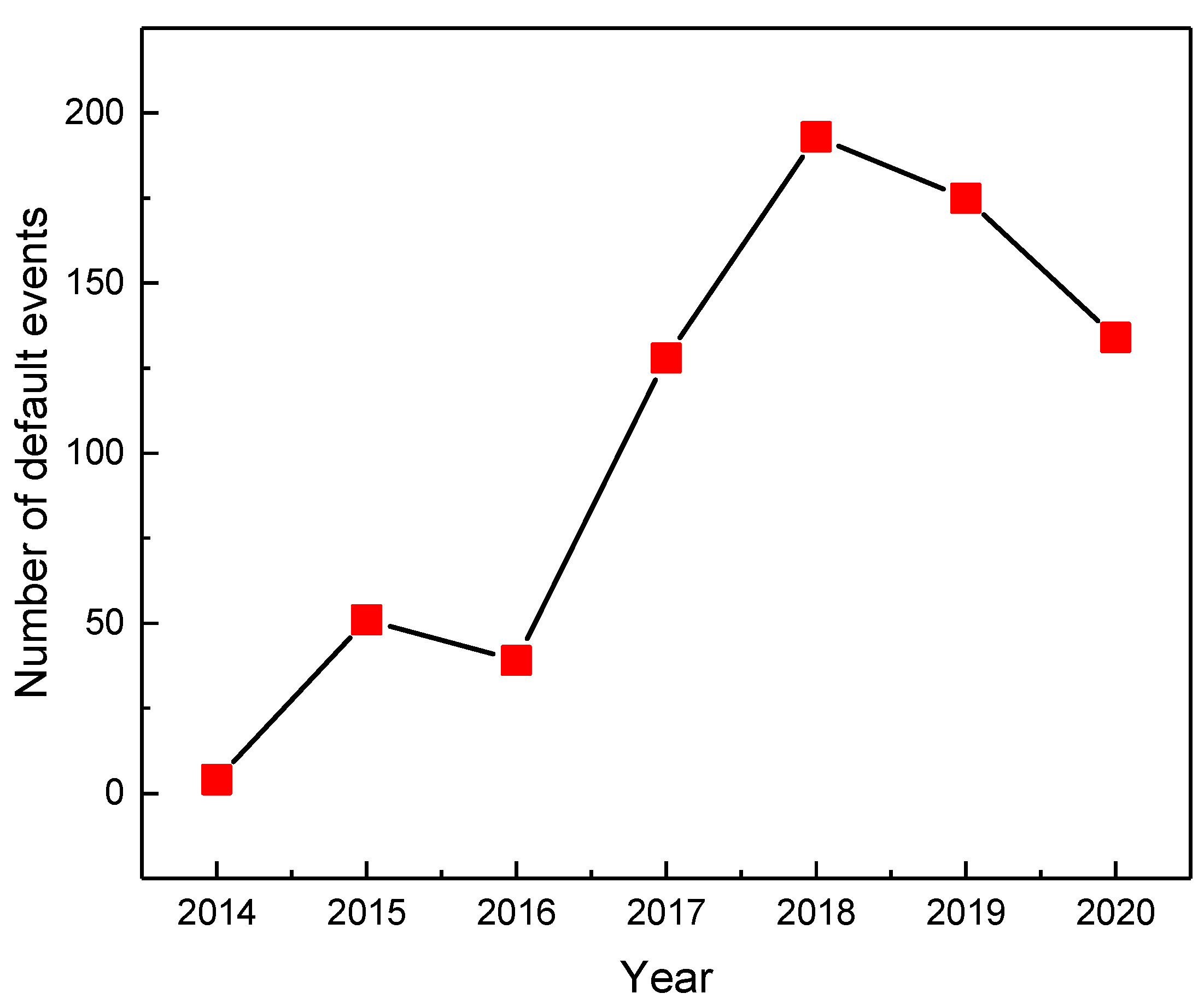

The number of farmland mortgage defaults reached a peak in 2018, and since then, the value declined year by year, which confirmed that after the separation of the management rights of contracted rural land from the management rights of contracted land, farmers’ farmland mortgage loans could be protected by law, and the default risk of farmland mortgage still exists, but it has been reduced.

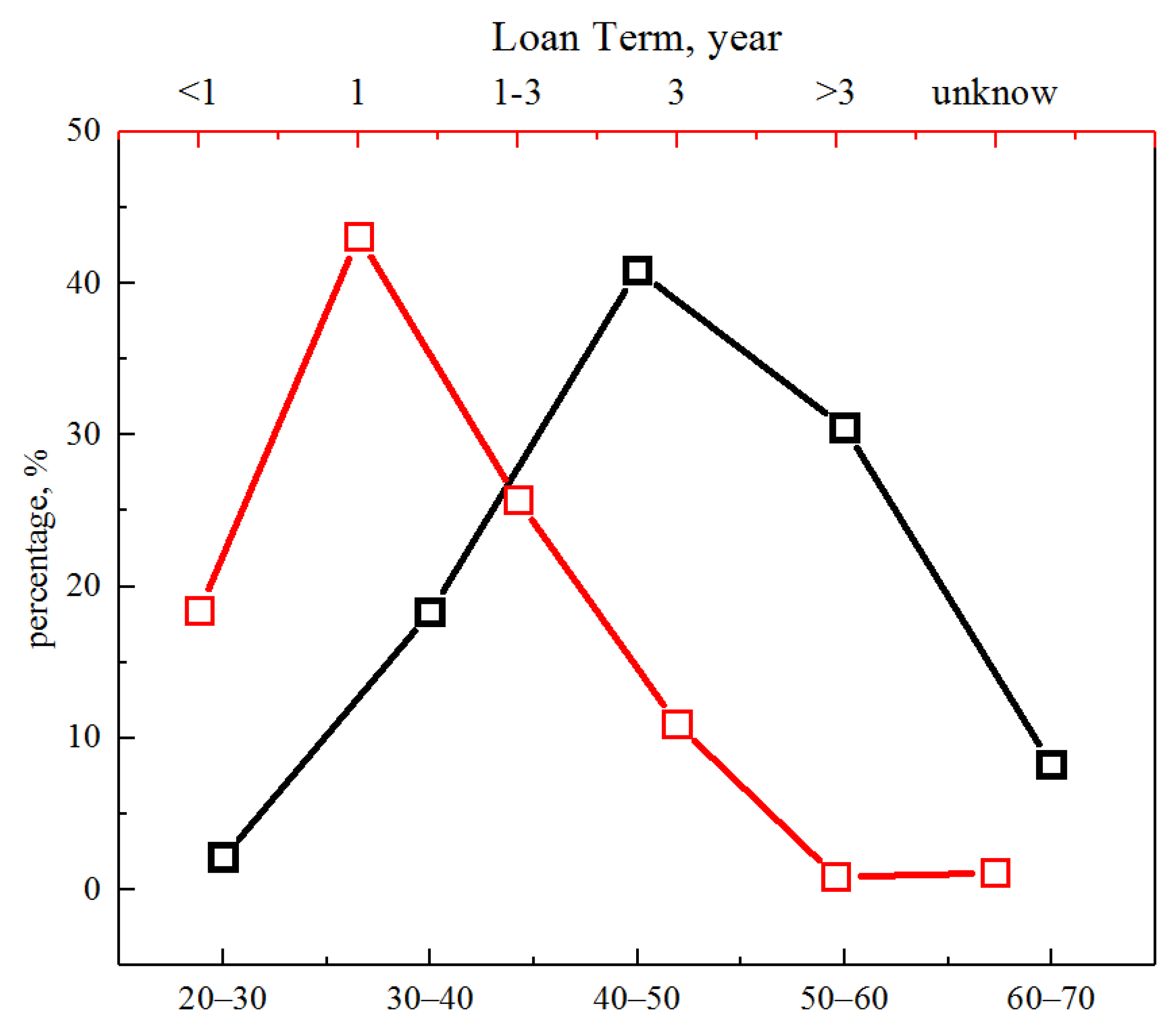

The mortgage loan defaults for rural land management rights amounting to less than CNY 100,000 accounted for the largest proportion, 54.7%. A small loan amount can promote a balanced distribution between the loan amount and the borrower’s income and effectively disperse the liquidity risk. These borrowers may have a weak ability in avoiding risk and could be prone to moral hazard. For these borrowers, more preferential loans or financial assistance should be considered. The default events of mortgage loans for rural land management rights concerned mainly 1-year short-term loans, which was consistent with the actual situation. To reduce the risk of farmers’ default, the term of bank loans was generally limited to one year.

China’s financial institutions mainly issue short-term agricultural loans (within 3 years), with a typical loan term of 12 months. Default cases are concentrated in the loan term of 6–12 months, of which defaults in the loan term of 12 months accounts for more than 40%.

The average age of agricultural labor force is 48.5 years old. Nearly 50-year-old men have become the main force of agriculture, of which more than 60% are full-time agricultural producers. Therefore, most of the households with loan demand and behavior are those whose head of household is over 40 years old, which also leads to the farmers in this age group may become the main body of default.

Natural disasters are the main cause of farmers’ default. The annual loss of grain caused by drought alone in China is as high as more than 30 billion kg, about 6% of the total grain output in the same period. The failure of agricultural land management caused by natural disasters makes farmers unable to repay loans and result in default.

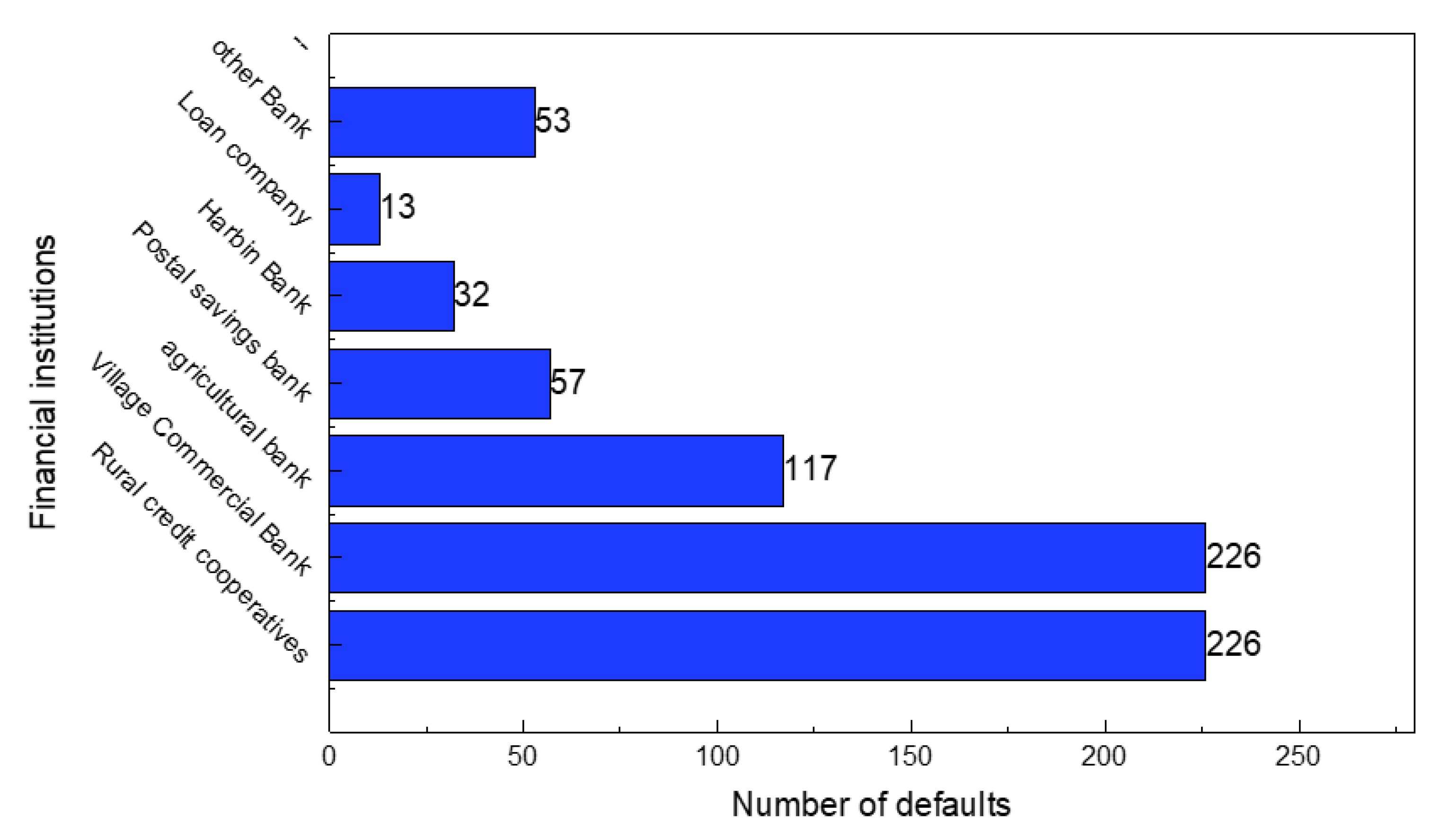

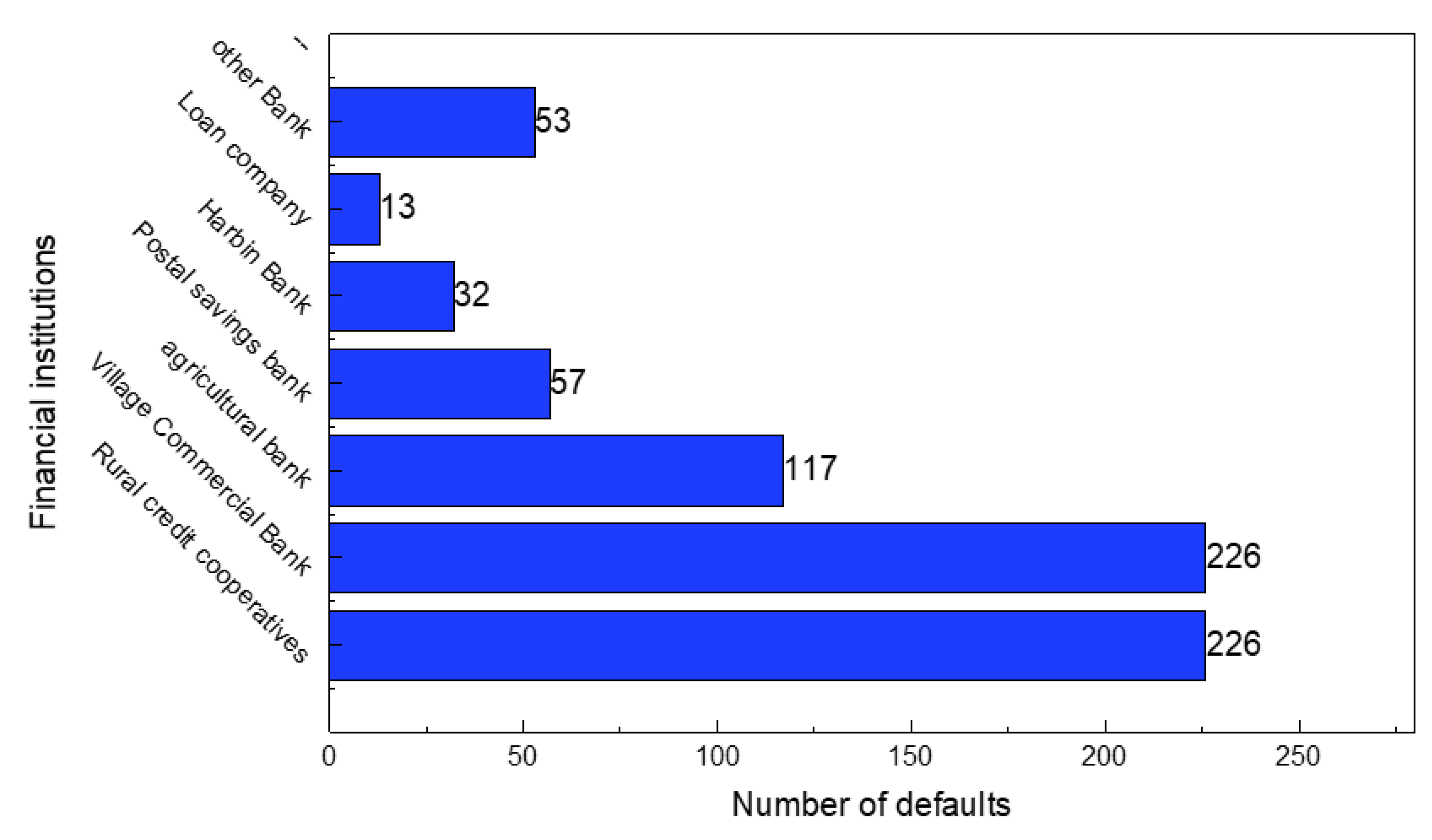

There are few financial institutions involved in farmland mortgage, which are not easy to share risks. It is recommended to expand financial institutions involved in farmland mortgage. These findings are not only a summary of the current situation of rural land mortgage default in China, but also the first-hand information on empirical research on rural land mortgage default, which can provide reference for the governance of rural land mortgage default risk.

The deficiency of this article lies in that this article makes only descriptive statistics on the default judgments of rural land management right mortgage loans from 2014 to 2020 in China, the data obtained from the court judgments can truly reflect the farmers’ default. There are also limitations regarding cases of defaults that were addressed by the court. For example, some cases of “de facto default” have not been granted a trial, so this part of the data cannot be obtained from the court. We discussed only the default cases judged by the court in this article. This is a work that needs to be further promoted. In follow-up research, it is necessary to conduct in-depth interviews to explore the institutional, individual, and natural causes of rural land management right mortgage default in China. It will be more helpful to reveal the formation mechanism of the default risk of rural land management rights and mortgage loans in China, clarify the current situation and characteristics of the default of rural land mortgage loans, and put forward suggestions for preventing the default risk of rural land mortgage loans.

China’s land system reform needs to pay attention to some problems. The first is clearing property relations. At present, the question as to whether rural land management right is a property right or creditor’s right is controversial, which is directly related to the protection of property right or creditor ‘s right. In addition, the content of land contract management right and land management right is not clear, which affects the practical effect of land contract management right and land management right. The second problem is a sound assessment system. At present, due to the lack of professional evaluation institutions and scientific evaluation standards, the real value of collateral cannot be accurately reflected in agricultural land mortgage. Therefore, it is necessary to improve the evaluation institutions, cultivate professional talents and improve the evaluation methods to effectively protect the legitimate rights and interests of all parties in the process of agricultural land mortgage. The third is supervision of land use. The Food and Agriculture Organization of the United Nations has set the warning line for arable land at 0.8 mu per capita, and no mortgage is allowed for arable land below 0.8 mu per capita. In the process of farmland mortgage, the tendency of farmland’s “non-agriculturalization” and “non-grain growing” should be eliminated to ensure that “the land use is not changed and the comprehensive agricultural production capacity is not destroyed” and that the red line of 1.8 billion mu of farmland will not be broken.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}