Drinking Poison to Quench Thirst: Local Government Land Financial Dependence and Urban Innovation Quality

Abstract

:1. Introduction

2. Research Hypothesis

3. Empirical Research

3.1. Empirical Modelling

3.2. Variable Definitions

3.2.1. Dependent Variable

3.2.2. Independent Variable

3.2.3. Control Variables

3.3. Sample and Data

4. Results

4.1. Benchmark Regression Results

4.2. Robustness Tests

4.2.1. Replacing the Independent Variable

4.2.2. Replacing the Dependent Variables

4.2.3. Lagging the Independent Variable

4.2.4. Reduced Sample Time Period

4.2.5. Consider Other Functional Forms

4.3. Placebo Test

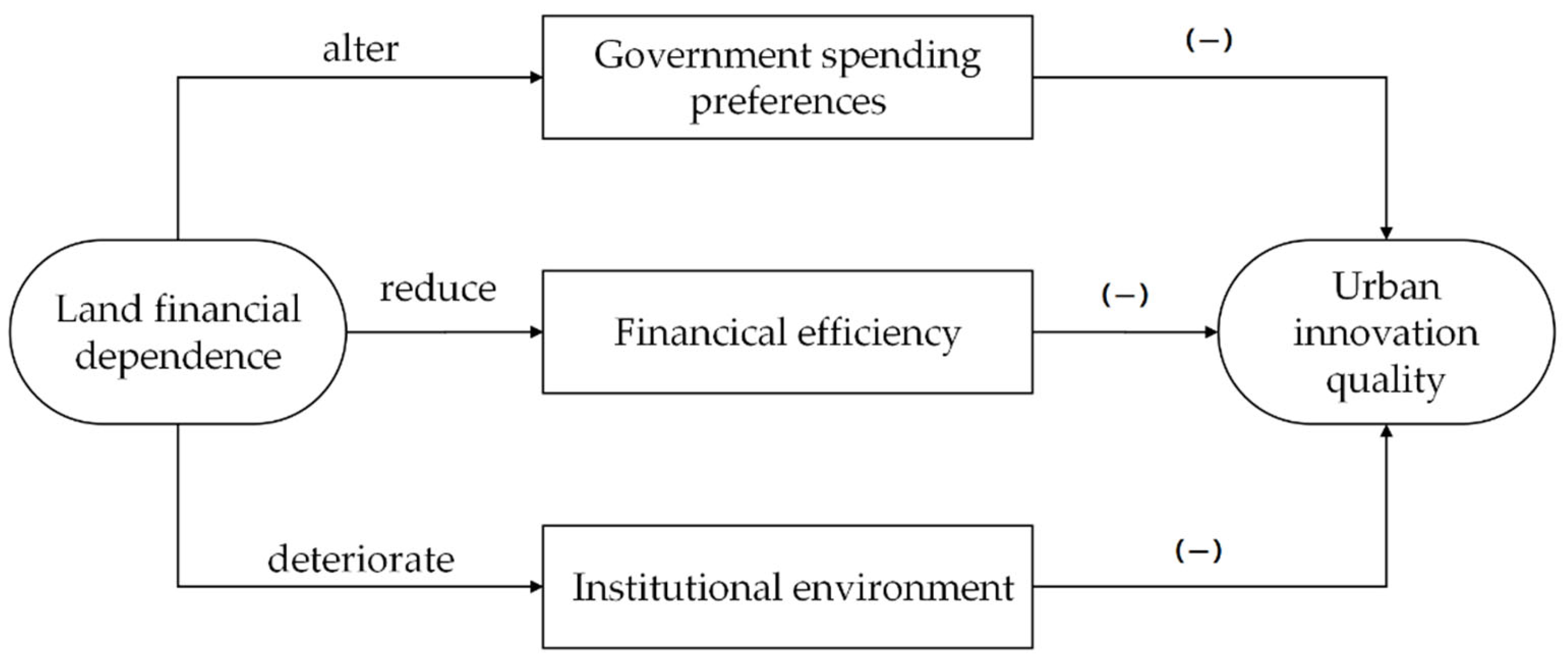

4.4. Mechanism of Impact

4.4.1. Mechanism: Land Finance Development Inhibits Urban Innovation Quality by Influencing Government Spending Preferences

4.4.2. Mechanism: Land Finance Development Reduces Financial Efficiency and Inhibits Urban Innovation Quality

4.4.3. Mechanism: Land Finance Development Deteriorates the Institutional Environment and Inhibits the Urban Innovation Quality

4.5. Heterogeneity Analysis

4.5.1. Regional Heterogeneity

4.5.2. Urban Size Heterogeneity

4.5.3. City Administrative Level Heterogeneity

5. Conclusions and Policy Implications

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Goh, A.L. Towards an innovation-driven economy through industrial policy-making: An evolutionary analysis of Singapore. Innov. J. Public Sect. Innov. J. 2005, 10, 34. [Google Scholar]

- Acemoglu, D.; Akcigit, U.; Alp, H.; Bloom, N.; Kerr, W. Innovation, reallocation, and growth. Am. Econ. Rev. 2018, 108, 3450–3491. [Google Scholar] [CrossRef]

- Zhao, Y.D. Legal environment, technological innovation, and sustainable economic growth. Front. Psychol. 2022, 13, 929359. [Google Scholar] [CrossRef] [PubMed]

- Liu, X.; Kong, M.; Tong, D.; Zeng, X.; Lai, Y. Property rights and adjustment for sustainable development during post-productivist transitions in China. Land Use Policy 2022, 122, 106379. [Google Scholar] [CrossRef]

- Hu, A.G.Z.; Zhang, P.; Zhao, L. China as number one? Evidence from China’s most recent patenting surge. J. Dev. Econ. 2017, 124, 107–119. [Google Scholar] [CrossRef]

- Zhou, W. High-Quality Manufacturing for China’s Stable Growth. China Econ. Transit. Dangdai Zhongguo Jingji Zhuanxing Yanjiu 2020, 3, 120–125. [Google Scholar] [CrossRef]

- Liu, S.; Hou, P.; Gao, Y.; Tan, Y. Innovation and green total factor productivity in China: A linear and non-linear investigation. Environ. Sci. Pollut. Res. Int. 2022, 29, 12810–12831. [Google Scholar] [CrossRef] [PubMed]

- Jin, B.; Han, Y.; Kou, P. Dynamically evaluating the comprehensive efficiency of technological innovation and low-carbon economy in China’s industrial sectors. Socio Econ. Plan. Sci. 2023, 86, 101480. [Google Scholar] [CrossRef]

- Barro, R.J. Quantity and Quality of Economic Growth; Banco Central de Chile: Santiago, Chile, 2002. [Google Scholar]

- Peterson, G.; Kaganova, O. Integrating Land Financing into Subnational Fiscal Management; The World Bank Policy Research Working Paper Series: Washington, DC, USA, 2010. [Google Scholar] [CrossRef]

- Fan, X.; Qiu, S.; Sun, Y. Land finance dependence and urban land marketisation in China: The perspective of strategic choice of local governments on land transfer. Land Use Policy 2020, 99, 105023. [Google Scholar] [CrossRef]

- Sun, X.; Zhou, F. Land Finance and the Tax-sharing System: An Empirical Interpretation. Social. Sci. China 2014, 35, 47–64. [Google Scholar] [CrossRef]

- Qun, W.; Yongle, L.; Siqi, Y. The incentives of China’s urban land finance. Land Use Policy 2015, 42, 432–442. [Google Scholar] [CrossRef]

- Liu, S.; Xiong, X.; Zhang, Y.; Guo, G. Land System and China’s Development Mode. China Ind. Econ. 2022, 39, 34–53. [Google Scholar] [CrossRef]

- Zhong, S.; Li, X.; Ma, J. Impacts of land finance on green land use efficiency in the Yangtze River Economic Belt: A spatial econometrics analysis. Environ. Sci. Pollut. Res. 2022, 29, 56004–56022. [Google Scholar] [CrossRef] [PubMed]

- Wang, Z.; Zhang, M. The Distributional Effects Associated with Land Finance in China: A Perspective Based on the Urban–Rural Income Gap. Land 2023, 12, 1771. [Google Scholar] [CrossRef]

- Wu, F. Land financialisation and the financing of urban development in China. Land Use Policy 2022, 112, 104412. [Google Scholar] [CrossRef]

- Ding, C. Land policy reform in China: Assessment and prospects. Land Use Policy 2003, 20, 109–120. [Google Scholar] [CrossRef]

- Wang, D.; Ren, C.; Zhou, T. Understanding the impact of land finance on industrial structure change in China: Insights from a spatial econometric analysis. Land Use Policy 2021, 103, 105323. [Google Scholar] [CrossRef]

- Mo, J. Land financing and economic growth: Evidence from Chinese counties. China Econ. Rev. 2018, 50, 218–239. [Google Scholar] [CrossRef]

- Almus, M.; Czarnitzki, D. The effects of public R&D subsidies on firms’ innovation activities. J. Bus. Econ. Stat. 2003, 21, 226–236. [Google Scholar] [CrossRef]

- Zhang, Y.; Wang, J.; Liu, Y.; Yue, W. Quantifying multiple effects of land finance on urban sprawl: Empirical study on 284 prefectural-level cities in China. Environ. Impact Asses 2023, 101, 107156. [Google Scholar] [CrossRef]

- Tang, P.; Shi, X.; Gao, J.; Feng, S.; Qu, F. Demystifying the key for intoxicating land finance in China: An empirical study through the lens of government expenditure. Land Use Policy 2019, 85, 302–309. [Google Scholar] [CrossRef]

- Zhang, T. Land market forces and government’s role in sprawl. Cities 2000, 17, 123–135. [Google Scholar] [CrossRef]

- Tong, D.; Chu, J.; Han, Q.; Liu, X. How land finance drives urban expansion under fiscal pressure: Evidence from Chinese cities. Land 2022, 11, 253. [Google Scholar] [CrossRef]

- Zhao, K.; Chen, D.; Zhang, X.; Zhang, X. How do urban land expansion, land finance, and economic growth interact? Int. J. Environ. Res. Public Health 2022, 19, 5039. [Google Scholar] [CrossRef] [PubMed]

- Gyourko, J.; Shen, Y.; Wu, J.; Zhang, R. Land finance in China: Analysis and review. China Econ. Rev. 2022, 76, 101868. [Google Scholar] [CrossRef]

- Zhou, Q.; Shao, Q.; Zhang, X.; Chen, J. Do housing prices promote total factor productivity? Evidence from spatial panel data models in explaining the mediating role of population density. Land Use Policy 2020, 91, 104410. [Google Scholar] [CrossRef]

- Yao, L.; Li, J.; Li, J. Urban innovation and intercity patent collaboration: A network analysis of China’s national innovation system. Technol. Forecast. Soc. 2020, 160, 120185. [Google Scholar] [CrossRef]

- Tong, D.; Chu, J.; MacLachlan, I.; Qiu, J.; Shi, T. Modelling the Impacts of land finance on urban expansion: Evidence from Chinese cities. Appl. Geogr. 2023, 153, 102896. [Google Scholar] [CrossRef]

- Tian, W.; Yu, J.; Gong, L. Promotion incentives and industrial land leasing prices: A regression discontinuity design. Econ. Res. J. 2019, 54, 89–105. [Google Scholar]

- Barney, J. Firm resource and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Gogokhia, T.; Berulava, G. Business environment reforms, innovation and firm productivity in transition economies. Eurasian Bus. Rev. 2021, 11, 221–245. [Google Scholar] [CrossRef]

- Kunce, M.; Shogren, J.F. Destructive interjurisdictional competition: Firm, capital and labor mobility in a model of direct emission control. Ecol. Econ. 2007, 60, 543–549. [Google Scholar] [CrossRef]

- Han, S.; Wang, M.; Liu, Q.; Wang, R.; Ou, G.; Zhang, L. The influence of land disposition derived from land finance on urban innovation in China: Mechanism discussion and empirical evidence. Int. J. Environ. Res. Public Health 2022, 19, 3212. [Google Scholar] [CrossRef] [PubMed]

- Wan, Q.; Ye, J.; Zheng, L.; Tan, Z.; Tang, S. The impact of government support and market competition on China’s high-tech industry innovation efficiency as an emerging market. Technol. Forecast. Soc. 2023, 192, 122585. [Google Scholar] [CrossRef]

- Chen, M.; Chen, T. Land finance, infrastructure investment and housing prices in China. PLoS ONE 2023, 18, e0292259. [Google Scholar] [CrossRef] [PubMed]

- Cheng, J.; Zhao, J.; Zhu, D.; Jiang, X.; Zhang, H.; Zhang, Y. Land marketisation and urban innovation capability: Evidence from China. Habitat. Int. 2022, 122, 102540. [Google Scholar] [CrossRef]

- Chen, M.; Chen, T.; Ruan, D.; Wang, X.; Finance, L. Land Finance, Real estate market, and Local Government debt risk: Evidence from China. Land 2023, 12, 1597. [Google Scholar] [CrossRef]

- Sun, W.; Zhang, X.; Zheng, S. Air pollution and spatial mobility of labor force: Study on the migrants’ job location choice. Econ. Res. J. 2019, 54, 102–117. [Google Scholar]

- Wang, G.M.; Salman, M. Understanding the spatial spillover effect of land finance on China’s green development: Does the moderating role of industrial structure matter? Environ. Sci. Pollut. Res. Int. 2023, 30, 95959–95974. [Google Scholar] [CrossRef] [PubMed]

- Glaeser, E.; Huang, W.; Ma, Y.; Shleifer, A. A real estate boom with Chinese characteristics. J. Econ. Perspect. 2017, 31, 93–116. [Google Scholar] [CrossRef]

- Chen, T.; Liu, L.X.; Zhou, L.-A. The crowding-out effects of real estate shocks–Evidence from China. Available at SSRN 2584302. SSRN J. 2015. [Google Scholar] [CrossRef]

- Acemoglu, D.; Moscona, J.; Robinson, J.A. State capacity and American technology: Evidence from the nineteenth century. Am. Econ. Rev. 2016, 106, 61–67. [Google Scholar] [CrossRef]

- Howell, S.T. Financing innovation: Evidence from R&D grants. Am. Econ. Rev. 2017, 107, 1136–1164. [Google Scholar] [CrossRef]

- Howell, A. Firm R&D, innovation and easing financial constraints in China: Does corporate tax reform matter? Res. Policy 2016, 45, 1996–2007. [Google Scholar] [CrossRef]

- Zhu, J.L.; Tang, Y.N.; Wei, Y.Y.; Wang, S.; Chen, Y.W. Corporate financialization, financing constraints, and innovation efficiency-Empirical evidence based on listed Chinese pharmaceutical companies. Front. Public Health 2023, 11, 1085148. [Google Scholar] [CrossRef]

- Zhou, L.; Tian, L.; Cao, Y.; Yang, L. Industrial land supply at different technological intensities and its contribution to economic growth in China: A case study of the Beijing-Tianjin-Hebei region. Land Use Policy 2021, 101, 105087. [Google Scholar] [CrossRef]

- Lichtenberg, E.; Ding, C. Local officials as land developers: Urban spatial expansion in China. J. Urban. Econ. 2009, 66, 57–64. [Google Scholar] [CrossRef]

- Cao, R.-f.; Zhang, A.-l.; Cai, Y.-y.; Xie, X.-x. How imbalanced land development affects local fiscal condition? A case study of Hubei Province, China. Land Use Policy 2020, 99, 105086. [Google Scholar] [CrossRef]

- Fan, J.; Zhou, L. Three-dimensional intergovernmental competition and urban sprawl: Evidence from Chinese prefectural-level cities. Land Use Policy 2019, 87, 104035. [Google Scholar] [CrossRef]

- Zhang, P.; Wang, Y.R.; Wang, R.Y.; Wang, T.W. Digital finance and corporate innovation: Evidence from China. Appl. Econ. 2024, 56, 615–638. [Google Scholar] [CrossRef]

- Stolbov, M.; Shchepeleva, M. Sentiment-based indicators of real estate market stress and systemic risk: International evidence. Ann. Financ. 2023, 19, 355–382. [Google Scholar] [CrossRef]

- Zhang, X.M.; Wei, C.Y.; Lee, C.C.; Tian, Y.M. Systemic risk of Chinese financial institutions and asset price bubbles. N. Am. J. Econ. Financ. 2023, 64, 101880. [Google Scholar] [CrossRef]

- Xin, F.; Zhang, J.; Zheng, W. Does credit market impede innovation? Based on the banking structure analysis. Int. Rev. Econ. Financ. 2017, 52, 268–288. [Google Scholar] [CrossRef]

- Bao, H.X.H.; Wang, Z.Y.; Wu, R.L. Understanding local government debt financing of infrastructure projects in China: Evidence based on accounting data from local government financing vehicles. Land Use Policy 2024, 136, 106964. [Google Scholar] [CrossRef]

- Jbir, H.; Oros, C.; Popescu, A. Macroprudential policy and financial system stability: An aggregate study. Empir. Econ. 2023. [Google Scholar] [CrossRef]

- Wang, M.X.; Wang, Y.X. Does factor market distortion inhibit enterprise innovation? Empirical evidence from Chinese industrial enterprises. J. Knowl. Econ. 2023. [Google Scholar] [CrossRef]

- Faccio, M. Politically connected firms. Am. Econ. Rev. 2006, 96, 369–386. [Google Scholar] [CrossRef]

- Jiang, R.; Lin, G.C.S. Placing China’s land marketisation: The state, market, and the changing geography of land use in Chinese cities. Land Use Policy 2021, 103, 105293. [Google Scholar] [CrossRef]

- Sharma, P.; Cheng, L.T.W.; Leung, T.Y. Impact of political connections on Chinese export firms’ performance–Lessons for other emerging markets. J. Bus. Res. 2020, 106, 24–34. [Google Scholar] [CrossRef]

- Liu, S.Y.; Du, J.; Zhang, W.K.; Tian, X.L.; Kou, G. Innovation quantity or quality? The role of political connections. Emerg. Mark. Rev. 2021, 48, 100819. [Google Scholar] [CrossRef]

- Krammer, S.M.S.; Jiménez, A. Do political connections matter for firm innovation? Evidence from emerging markets in Central Asia and Eastern Europe. Technol. Forecast. Soc. Chang. 2020, 151, 119669. [Google Scholar] [CrossRef]

- Chen, C.J.P.; Li, Z.; Su, X.; Sun, Z. Rent-seeking incentives, corporate political connections, and the control structure of private firms: Chinese evidence. J. Corp. Fin. 2011, 17, 229–243. [Google Scholar] [CrossRef]

- Murphy, K.M.; Shleifer, A.; Vishny, R.W. Why is rent-seeking so costly to growth? Am. Econ. Rev. 1993, 83, 409–414. [Google Scholar]

- Kou, Z.; Liu, X. FIND Report on City and Industrial Innovation in China; Fudan Institute of Industrial Development, School of Economics, Fudan University: Shanghai, China, 2017. [Google Scholar]

- Hou, S.; Song, L.; Wang, J.; Ali, S. How land finance affects green economic growth in Chinese cities. Land 2021, 10, 819. [Google Scholar] [CrossRef]

- La Ferrara, E.L.; Chong, A.; Duryea, S. Soap operas and fertility: Evidence from Brazil. Am. Econ. J. Appl. Econ. 2012, 4, 1–31. [Google Scholar] [CrossRef]

- Ye, F.; Wang, W. Determinants of land finance in China: A study based on provincial-level panel data. Aust. J. Publ. Admin. 2013, 72, 293–303. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Variable Name | Sign | Calculation Method |

|---|---|---|

| Urban Innovation Quality | the innovation index compiled by Kou et al. [66] | |

| Land finance dependence | transaction price of construction land grants/budgeted revenue | |

| economic development | Econo | GDP per capita and taking the natural logarithm |

| industrial structure | Indus | Tertiary GDP/Gross Regional Product |

| financial development | Open | Total deposits and loans of financial institutions/GDP |

| level of openness | Finan | Amount of foreign capital/Gross Regional Product |

| education level | Educa | Ln (the tertiary education enrolment per 100,000 population) |

| urbanisation rate | Urbani | Year-end resident population in towns/total resident population |

| Variable | Obs | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| 3662 | 5.294 | 16.475 | 0.015 | 120.73 | |

| 3662 | 0.58 | 0.409 | 0.046 | 2.113 | |

| Econo | 3662 | 9.837 | 0.726 | 8.254 | 11.519 |

| Indus | 3662 | 36.912 | 8.316 | 19.08 | 65.28 |

| Open | 3662 | 0.021 | 0.022 | 0 | 0.11 |

| Finan | 3662 | 2.038 | 0.978 | 0.834 | 6.118 |

| Educa | 3662 | 14.215 | 18.002 | 0 | 93.49 |

| Urbani | 3662 | 0.471 | 0.171 | 0.155 | 0.946 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| −2.655 *** | −2.916 *** | −2.716 *** | −2.692 *** | |

| (−2.627) | (−2.991) | (−2.709) | (−2.697) | |

| Econo | −13.820 *** | −13.845 *** | −14.673 *** | |

| (−4.131) | (−4.113) | (−4.372) | ||

| Indus | 0.409 *** | 0.397 *** | 0.371 *** | |

| (3.119) | (3.074) | (2.751) | ||

| Open | −91.937 *** | −88.758 ** | ||

| (−2.654) | (−2.501) | |||

| Finan | −2.016 * | −2.491 ** | ||

| (−1.673) | (−2.034) | |||

| Educa | 0.180 * | |||

| (1.745) | ||||

| Urbani | −2.233 | |||

| (−0.660) | ||||

| _cons | 1.992 *** | 113.510 *** | 120.727 *** | 129.476 *** |

| (2.726) | (3.957) | (3.934) | (4.150) | |

| N | 3662 | 3662 | 3662 | 3662 |

| Adj. R2 | 0.186 | 0.245 | 0.259 | 0.265 |

| F | 7.128 | 7.883 | 7.262 | 6.274 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

|---|---|---|---|---|---|---|---|

| 2 | −29.896 ** | ||||||

| (−2.004) | |||||||

| −1.859 *** | |||||||

| (−3.502) | |||||||

| −0.004 *** | −2.108 *** | −5.053 ** | −0.136 *** | ||||

| (−3.930) | (−3.484) | (−2.186) | (−4.050) | ||||

| −3.844 *** | |||||||

| (−3.752) | |||||||

| 1.241 | |||||||

| (1.283) | |||||||

| Control | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| City fixed | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year fixed | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 3662 | 3662 | 3662 | 3383 | 2606 | 3662 | 3662 |

| Adj. R2 | 0.263 | 0.268 | 0.399 | 0.287 | 0.203 | 0.265 | 0.909 |

| F | 6.381 | 6.261 | 14.627 | 6.791 | 4.804 | 6.076 | 250.653 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Expend_prefer | Financ_eff | Inst_envir | |

| −0.002 ** | −0.018 *** | 0.038 *** | |

| (−2.133) | (−3.211) | (4.333) | |

| Control | Yes | Yes | Yes |

| City fixed | Yes | Yes | Yes |

| Year fixed | Yes | Yes | Yes |

| N | 3662 | 3662 | 3651 |

| Adj. R2 | 0.919 | 0.336 | 0.260 |

| F | 412.404 | 55.536 | 113.977 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Eastern Regions | Midwest Regions | Big City Size | Small City Size | Central Cities | Peripheral Cities | |

| −2.959 ** | −1.864 | −5.383 *** | −0.676 *** | −8.167 ** | −1.08 ** | |

| (−2.032) | (−1.461) | (−2.857) | (−2.723) | (−2.294) | (−2.502) | |

| Control | Yes | Yes | Yes | Yes | Yes | Yes |

| City fixed | Yes | Yes | Yes | Yes | Yes | Yes |

| Year fixed | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 1666 | 1996 | 1831 | 1831 | 460 | 3202 |

| Adj. R2 | 0.336 | 0.224 | 0.395 | 0.316 | 0.702 | 0.289 |

| F | 5.798 | 6.003 | 5.915 | 6.958 | 18.524 | 8.990 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xu, S.; Yang, F.; Yang, Q.; Chang, B.; Wang, K. Drinking Poison to Quench Thirst: Local Government Land Financial Dependence and Urban Innovation Quality. Land 2024, 13, 542. https://doi.org/10.3390/land13040542

Xu S, Yang F, Yang Q, Chang B, Wang K. Drinking Poison to Quench Thirst: Local Government Land Financial Dependence and Urban Innovation Quality. Land. 2024; 13(4):542. https://doi.org/10.3390/land13040542

Chicago/Turabian StyleXu, Shiying, Fuqiang Yang, Qian Yang, Binbin Chang, and Kun Wang. 2024. "Drinking Poison to Quench Thirst: Local Government Land Financial Dependence and Urban Innovation Quality" Land 13, no. 4: 542. https://doi.org/10.3390/land13040542

APA StyleXu, S., Yang, F., Yang, Q., Chang, B., & Wang, K. (2024). Drinking Poison to Quench Thirst: Local Government Land Financial Dependence and Urban Innovation Quality. Land, 13(4), 542. https://doi.org/10.3390/land13040542