1. Introduction

Innovation is recognised as a core element in enhancing long-term economic growth and the ultimate choice for countries and regions to achieve high-quality economic growth [

1,

2,

3]. Therefore, to achieve rapid economic growth, emerging markets tend to encourage innovative activities and promote ‘brute force’ economic growth by increasing the number of patents [

4]. However, this approach ignores the differences between different types of patents. At the same time, the value of even the same type of patent is very different, and an increase in the number of patents alone is not sufficient to promote high-quality economic growth. Even among patents of the same type, the difference in value can be so great that an increase in the number of patents alone is insufficient to promote high-quality economic growth. For example, in China, the total number of patents granted to Chinese firms increased from 55,000 to 1,720,800 between 1998 and 2017, an average annual growth of nearly 20%. In contrast, the number of patent applications in China surpassed that in the United States in 2011. However, a large gap remains between China and the US in terms of key technological innovations [

5,

6]. In the same period, China’s gross domestic product (GDP) growth rate is about 12.7%. The GDP growth rate is obviously lower than the patent growth rate and is accompanied by excessive depletion of natural resources and serious environmental pollution [

7,

8]. Therefore, academics and government organizations are increasingly focusing on enhancing innovation quality, specifically the overall value of patents [

9].

Concurrently, local governments in China exhibit a pronounced dependency on land finance (LFD), a phenomenon extensively documented in the literature [

10,

11]. The genesis of land finance is widely attributed to the fiscal adjustments from the 1994 tax-sharing reform, which redefined the revenue allocation between local and central governments. This reform delineated three primary tax categories: central, local, and shared taxes. Notably, the value-added tax (VAT), previously a significant local revenue source, was reclassified as a shared tax, with distributions of 75% to the central government and 25% to local governments, thereby reducing local government revenues from 80% pre-reform to 45% [

12]. Despite diminishing revenues, local governments faced undiminished obligations to provide public services and promote economic development, necessitating alternative revenue sources to address fiscal shortfalls [

13].

Further compounding this issue is the legal framework established by China’s Land Management Law (unaltered until 2020), which legalized land finance by mandating government expropriation and state ownership conversion of urban land for developmental use [

14]. This law effectively granted local governments a monopoly over urban land supply. Following the 1998 housing reform, which marked the real estate industry’s transition to marketization, the discrepancy between the earnings from urban land concessions and acquisition costs has consistently expanded [

15]. Given that budgetary incomes, particularly from the construction and real estate sectors, accrue to local jurisdictions, local authorities naturally prioritize construction sector development [

12]. Moreover, the absence of upper-level government regulation over land transfer revenue management and the local discretion in utilizing these funds foster an intrinsic motivation for land finance implementation, culminating in acute Local Government Land Finance Dependence (LGLFD) [

16]. Empirically, in 2020, revenue from local government land concessions surpassed RMB 8.4 trillion (US

$1.17 trillion), underscoring the scale and impact of this dependence.

The land finance strategy of local governments has had a profound impact on China’s socio-economy. On the one hand, local governments earn fiscal revenues from land concessions, land leases, and land taxes [

17,

18], easing fiscal pressures, and at the same time investing these revenues in infrastructure construction, which promotes rapid economic growth in a short period of time [

19,

20]. On the other hand, low-cost industrial land reduces the production costs of enterprises, while land finance revenue is used to subsidise enterprises through taxes and various incentives [

21,

22], which further promotes economic development. Not only that, LGLFD promotes the prosperity of the regional property market [

23], which not only fosters the rapid growth of the regional economy and brings more fiscal revenue for local governments, but also accelerates the process of urbanisation in emerging markets [

24,

25,

26].

Although there is a near consensus on the role of land finance in boosting the economy, there is still disagreement on its effectiveness in influencing innovation. Optimistic scholars argue that local governments earn land grant spreads through land financing and use the acquired funds to construct local infrastructure in the region [

27], which provides better conditions for enterprises to innovate [

28,

29]. At the same time, low-cost industrial land reduces enterprises’ production costs; thus, they have more funds to spend on innovation activities [

30]. In addition, land financing increases the linkage between enterprises and regional economic development, reduces the financial constraints and uncertainties that firms face when conducting innovative activities [

31], and contributes to innovative activities. However, opponents argue that excessive spending on infrastructure by local governments reduces the government’s financial support for innovation and inhibits enterprises’ innovative behaviour [

32,

33]. Moreover, the granting of industrial land at lower prices allows low-end industries, which should have been eliminated to have better living spaces. The over-competitive market environment inhibits the development of innovative industries, which has an obvious ‘crowding out effect’ on innovation; thus, it is not conducive to improving innovation efficiency [

34,

35,

36]. Worse still, the excessive intervention of land finance in the economy undermines the market environment of fair competition, causing enterprises with innovative capabilities to lose their willingness to further improve their level of innovation due to a lack of policy support [

35].

As the above studies show, there is no consistent conclusion regarding the impact of LGLFD on innovation. Because high-quality innovation, a core element in guiding the green and sustainable development of emerging market economies, requires longer investment cycles, higher investment costs, and more uncertainty, does LGLFD impact urban innovation quality (UIQ)? What kind of impact? It remains to be seen. To answer this question, we theoretically analyse and empirically test the impact of LGLFD on UIQ using 3662 samples from 264 cities in China over the years 2003–2016. The results show that (1) LGLFD significantly reduces UIQ; (2) LGLFD has an inhibitory effect on UIQ, mainly by changing government spending preferences, reducing regional financial efficiency, and deteriorating the institutional environment; and (3) there is obvious heterogeneity in the effect of LGLFD on UIQ. In the eastern region, LGLFD significantly reduces UIQ, while there is no effect in the central and western regions. The inhibitory effect of LGLFD on UIQ is more prominent in big cities, much larger than that in small cities, and the inhibitory effect of LGLFD on UIQ in the central city is stronger than that in the peripheral cities.

The contributions of this study are as follows: first, it expands and improves the research framework of the consequences of LGLFD by discussing the relationship between LGLFD and UIQ; second, it discusses the path mechanism and heterogeneity of the relationship between LGLFD and UIQ, deepening the understanding of the relationship between them; and third, as innovation is the source of long-term economic growth, this study provides an important reference value for the policy formulation of improving UIQ and promoting long-term high-quality and sustainable growth of China’s economy through an in-depth study of the relationship between LGLFD and UIQ.

The remainder of this paper is organised as follows.

Section 2 formulates the research hypotheses;

Section 3 constructs the model, describes the variables, and explains the sources of the data;

Section 4 reports the empirical results; and

Section 5 draws conclusions, makes policy recommendations, and summarises the shortcomings of the paper.

2. Research Hypothesis

Since the implementation of the tax-sharing reform in China, local governments have been under dual pressure. On the one hand, the ‘GDP Championship’ has prompted local governments to urgently promote economic development, that is, local government officials seek higher economic growth targets and higher rankings among their peers due to promotion and performance appraisal pressure [

11]. On the other hand, the reduction in the proportion of tax revenue has led local governments to urgently seek new sources of funding to compensate for fiscal deficits [

16]. Land financing was created under this dual pressure. Typically, local governments adopt the strategy of granting industrial land at low prices and commercial land at high prices. Specifically, local governments offer industrial land at low prices to attract commercial investment and offer commercial land at high prices to compensate for the loss of fiscal revenues caused by industrial land concessions, which is far below the cost of compensation for agricultural land, and they also invest more of the proceeds from land concessions in productive expenditures, such as infrastructure [

37]. Although this strategy has contributed to the rapid economic development of cities, it has also had many adverse effects on UIQ.

On the one hand, cheap industrial land has allowed many inefficient and less innovative firms to survive. An important factor is that the land market can allocate land to enterprises with high productivity and innovation through market competition [

38]. Local governments have artificially kept industrial land prices low, undermining the market competition mechanism, which will lead to the preservation of inefficient and low-innovation enterprises that should have been eliminated from the market and will not be conducive to improving UIQ. On the other hand, the high price of commercial land raises the cost of housing construction and increases urban housing prices. At the same time, the growth in government investment in infrastructure development has improved the living environment of residents and the production conditions of enterprises, which may be conducive to a further increase in house prices. At the same time, the increase in government investment in infrastructure has improved the living environment for residents and production conditions for enterprises, which is conducive to the further increase in property prices. Additionally, it promotes the rapid development of the real estate industry [

27,

39]. Expensive housing prices not only increase the cost of daily production and operation but also reduce the profitability of enterprises and force them to reduce their investment in innovative activities [

40,

41].

Additionally, long-term LGLFD induces local governments to introduce policies to maintain stable housing prices. Stable housing prices can ensure that commercial land grant prices remain high, and commercial land grant revenue is key to the local government’s land finance revenue [

42]. Local government intervention in the real estate market allows the real estate sector to have more stable profits and face less uncertainty than other sectors [

35]. Enterprises are attracted to investing more capital in the real estate sector, where technological progress and innovation are limited, rather than innovative activities with higher risks, longer cycles, and more uncertain returns [

43]. Therefore, Hypothesis H1 is proposed:

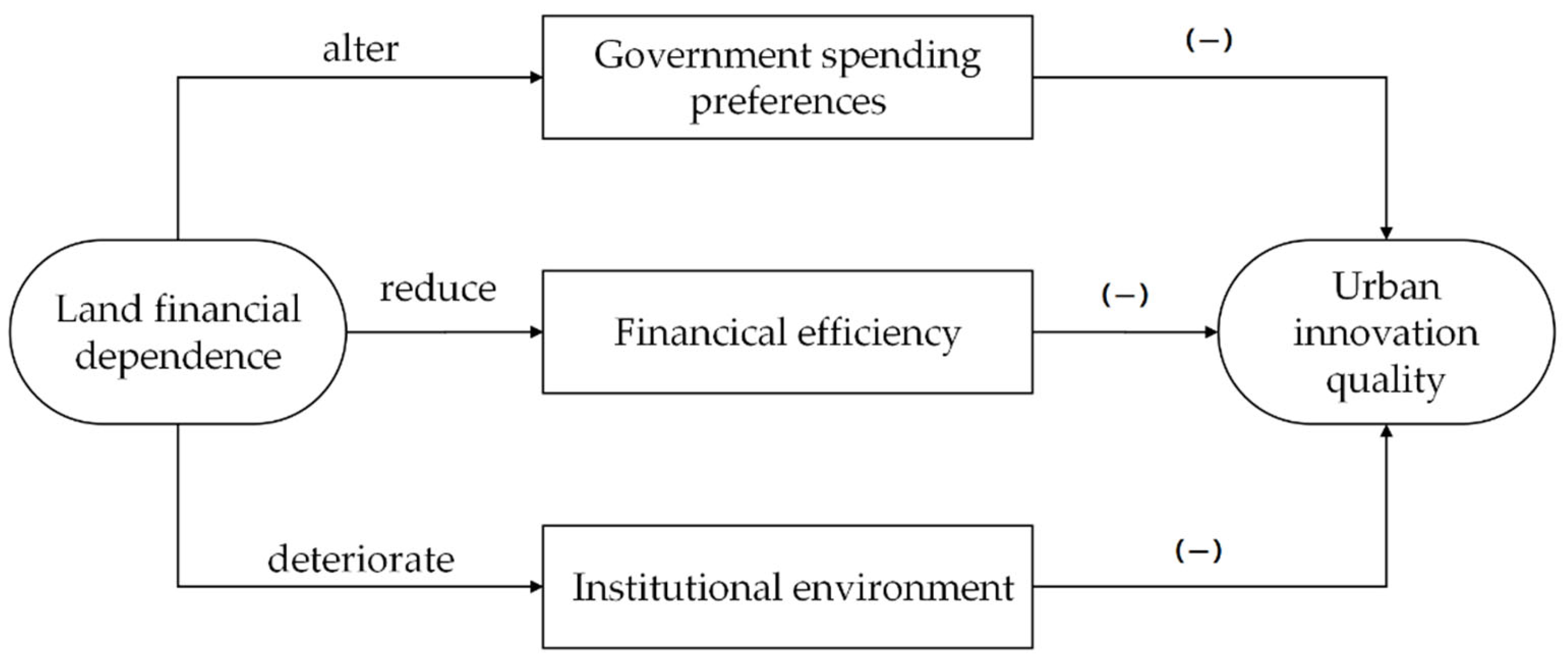

Hypothesis 1 (H1). Ceteris paribus, LGLFD can inhibit UIQ.

The enhancement of UIQ is inextricably linked to the support provided by local governments in the realms of science and education, particularly through research and development investment [

44,

45]. This nexus arises from the inherent nature of innovative investment, characterized by extended duration, gradual outcomes, and considerable uncertainty. Given the capital constraints and profit imperatives, enterprises on their own often struggle to achieve significant innovative outputs. Consequently, external financial support and guidance become crucial in elevating their innovation capabilities [

46,

47]. This need becomes more pronounced in the context of high-quality innovations, which entail higher costs and greater uncertainties, underscoring the imperative for external assistance [

48]. However, to promote rapid regional economic growth and to achieve performance goals, local governments have an inherent incentive to focus on productive investments and avoid innovation expenditures [

49,

50]. Local governments are more willing to use fiscal revenues from land grants for infrastructure and other productive expenditures while undermining research and innovation expenditures, which are long cycles, highly uncertain, and slow to produce results [

51]. When enterprises are unable to implement high-quality innovations due to their financial resources and profitability, this ‘focusing on infrastructure, not innovation’ spending preference of local governments undoubtedly fails to provide effective support for the innovative activities of enterprises. Therefore, Hypothesis H2 is proposed:

Hypothesis 2 (H2). Ceteris paribus, LGLFD alters government spending preferences, thereby hindering UIQ.

As the main body of innovation activities, enterprises’ external financing opportunities play a key role in innovation activities [

52], while their external financing opportunities will also be affected by land finance. On the one hand, the high price of commercial land and the continuous improvement of infrastructure have increased real estate prices [

27,

39]. This has led residents to form expectations of a sustained rise in real estate prices, increasing speculative demand for the real estate market and further contributing to the rapid rise in real estate prices [

53]. Unreasonable increases in real estate prices drive the creation of real estate bubbles, which in turn increase the probability of triggering systemic risks in the financial system [

54]. On the other hand, to expand their business scale, real estate enterprises obtain loans from financial institutions through land mortgage financing [

55,

56]. The systemic risk in the financial sector is magnified again when there is an irrational rise in land prices and when financial institutions hold a large number of loans financed by land as collateral [

54]. To reduce their business risks and ensure the stable operation of the financial system, financial institutions reduce the level of financial resources placed in the market and lower financial efficiency [

57]. This undoubtedly increases the threshold and cost for enterprises to obtain external financing from financial institutions, thus reducing external financing opportunities, which in turn negatively impacts enterprise innovation. Therefore, Hypothesis H3 is proposed:

Hypothesis 3 (H3). Ceteris paribus, LGLFD reduces financial efficiency, thus hindering UIQ.

A favourable institutional environment is also an important safeguard for driving innovation. Rent-seeking theory suggests that to obtain economic benefits, when the cost of rent-seeking is less than the cost of production, enterprises or other subjects influence the government’s behaviour through rent-seeking means in order to obtain economic benefits, which leads to the crowding out of productive investment. This effect is more pronounced for innovative activities [

58]. Rent-seeking is an unavoidable phenomenon in emerging market countries where monitoring mechanisms are inadequate [

59]. Land finance has fostered tighter business–government relations, creating a conducive environment for ‘political connections’ that can facilitate corrupt practices, as documented in the literature [

60,

61]. Specifically, local governments, monopolizing urban land supplies, wield significant control over land availability and pricing. To secure urban land at reduced costs, businesses often engage in rent-seeking behaviours like lobbying and making political contributions, aiming to lower production expenses. This shift towards ‘non-innovative production activities’ diverts firms, initially focused on long-term innovation-driven growth, towards rent-seeking strategies, distorting their development agendas [

62]. Consequently, the competitive landscape shifts from market and product-based rivalry to one marred by rent-seeking and unfair practices [

63,

64,

65]. This market mechanism distortion undermines corporate innovation enthusiasm, adversely affecting urban innovation quality. Therefore, Hypothesis H4 is proposed:

Hypothesis 4 (H4). Ceteris paribus, LGLFD deteriorates the institutional environment, thereby inhibiting UIQ.

Figure 1 illustrates the research pathway map.

5. Conclusions and Policy Implications

As an important way for governments to raise extra-budgetary funds in emerging market countries [

69], LGLFD has improved the regional economy [

20], but its long-term impacts remain highly controversial. In particular, the impact on UIQ is still not unanimously concluded. This is not only closely related to long-term economic growth, but also to the overall development strategy of the country. In view of this, this study analysed and empirically tested the effect of LGLFD on UIQ based on a sample of 264 cities in China from 2003 to 2016. The results showed that LGLFD significantly inhibited UIQ. Specifically, LGLFD reduces UIQ through three main channels: changing government spending preferences, reducing financial efficiency, and deteriorating the institutional environment. Further research found significant heterogeneity in the effect of LGLFD on UIQ. From a city-region perspective, LGLFD significantly reduces UIQ in the eastern region, whereas it has no effect in the central and western regions. From the perspective of city size, LFD significantly reduced UIQ in both large and small cities; however, this reduction effect was more prominent in large cities. From the perspective of the city’s administrative level, the inhibitory effect of LFD on UIQ was stronger in central cities than in peripheral cities.

Accordingly, we make three policy recommendations. First, the central government should accelerate the reform of the fiscal and taxation system, reasonably adjust the ratio of tax revenue distribution between the central government and local governments, give local governments greater autonomy in fiscal and taxation, and gradually reduce the dependence of local governments on land-based fiscal revenues [

16]. Second, the government should change the current GDP growth-oriented performance assessment standards, urge local governments to increase the proportion of innovation-related science and education financial expenditures, and transform economic development from the original “infrastructure construction-driven” approach to an “innovation-driven” approach. Third, deepen the reform of the financial system and provide appropriate financial support to innovative enterprises to help them alleviate the financing difficulties they face in their innovative activities. Finally, accelerate the market-oriented reform of urban land grant, change the monopoly of local governments in the urban land grant market, reduce rent-seeking behaviour, and mitigate the adverse impact of distorted market mechanisms on innovation.

Although much work has been done in this study, it has some limitations. First, this study explored three mechanisms by which LGLFD affects UIQ; in fact, there may still be other mechanisms of influence, and future research should explore other possible mechanisms of influence. Second, under the pressure of competition championships, local governments may have an imitation effect, and LGLFD may show spatial correlation; however, due to the length of the article, this study does not consider the spatial spillover effect of LGLFD on UIQ, which will be the focus of our next work.

{kind=link}

{kind=link}

{kind=link}