Fractional Riccati Equation and Its Applications to Rough Heston Model Using Numerical Methods

Abstract

:1. Introduction

Organization of the Paper

2. Fractional Adams–Bashforth–Moulton Method and Its Error Analysis

3. Option Pricing Models, Implied Volatility, Characteristic Functions of the Option Pricing Models

- Introduce the famous Black–Scholes pricing model and discuss about implied volatility as well as its importance in the financial market.

- Focus on one of the most famous financial model amongst the practitioners—classical Heston model and the newly developed rough Heston model.

- Display its characteristic functions and its connection to call option pricing formula using the inversion of characteristic function.

3.1. Black–Scholes Model and Implied Volatility

3.2. Classical Heston Model and Rough Heston Model

- The model reproduce several stylized facts of low frequency stock data, e.g., the leverage effect, time-varying volatility and fat tails.

- It generates similar shapes and dynamics for the implied volatility surface.

- Efficient computation for the classical Heston model using the explicit formula for the characteristic function of the asset log-price (we will discuss it later).

3.3. Characteristic Functions and Their Connection to Call Option Pricing

4. Small and Long Time Expansion of Solution for the Fractional Riccati Equation

4.1. Small Time Expansion on Solution of Fractional Riccati Equation

4.2. Large Time Expansion on Solution of Fractional Riccati Equation

5. Multipoint Padé Approximation Method for Fractional Riccati Equation

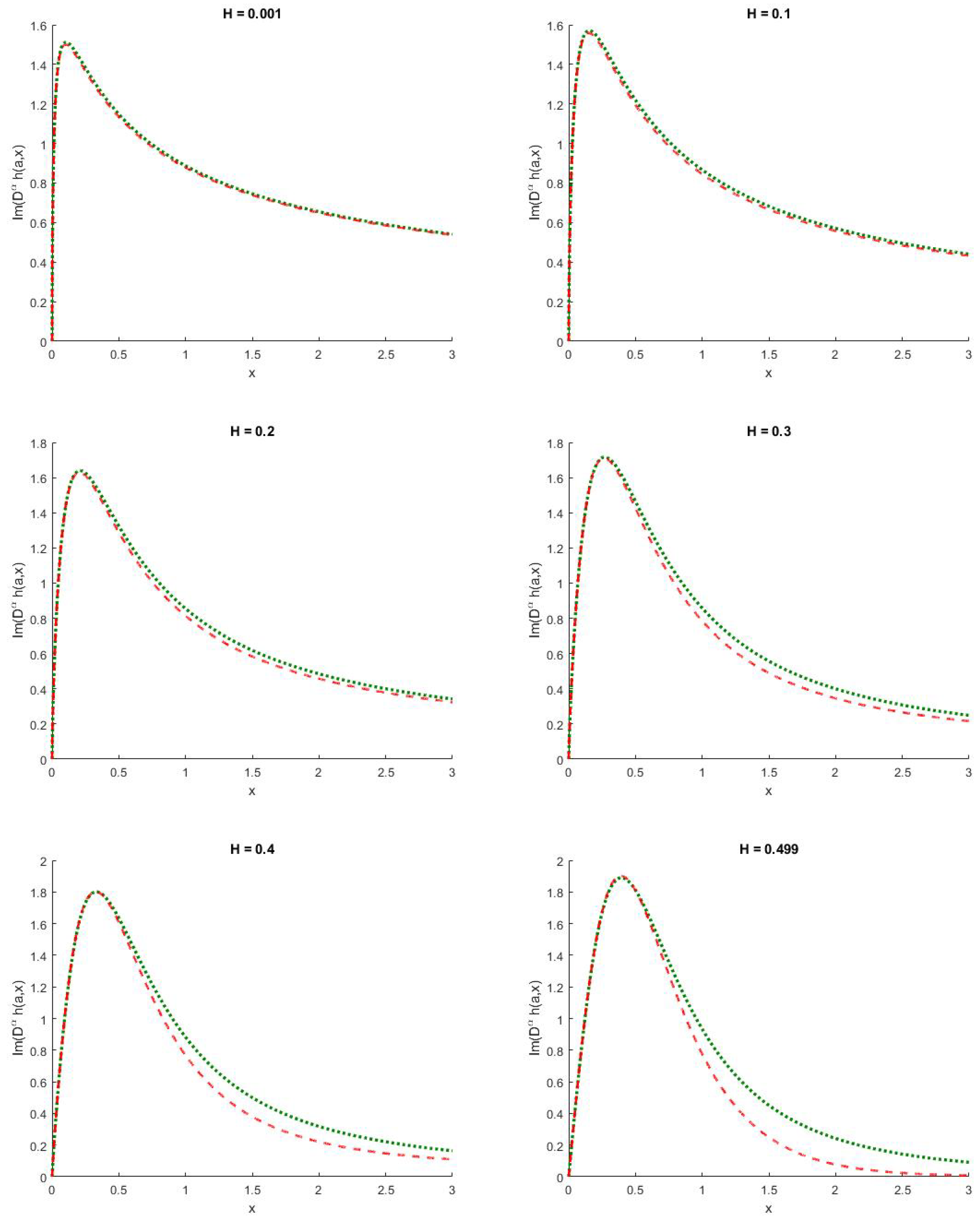

6. Numerical Experiment And Performances

7. Concluding Remarks

Author Contributions

Funding

Conflicts of Interest

Appendix A. Riemann–Liouville Fractional Integrals and Fractional Derivatives

Appendix B. Mittag–Leffler Function

References

- Hull, J.; White, A. The pricing of options on assets with stochastic volatilities. J. Financ. 1987, 42, 281–300. [Google Scholar] [CrossRef]

- Heston, S.L. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 1993, 6, 327–343. [Google Scholar] [CrossRef] [Green Version]

- Renault, E.; Touzi, N. Option hedging and implied volatilities in a stochastic volatility model 1. Math. Financ. 1996, 6, 279–302. [Google Scholar] [CrossRef]

- Lee, R.W. Implied volatility: Statics, dynamics, and probabilistic interpretation. In Recent Advances in Applied Probability; Springer: Berlin, Germany, 2005; pp. 241–268. [Google Scholar]

- Lewis, A.L. Option Valuation under Stochastic Volatility II; Finance Press: Newport Beach, CA, USA, 2009. [Google Scholar]

- Medvedev, A.; Scaillet, O. Approximation and calibration of short-term implied volatilities under jump-diffusion stochastic volatility. Rev. Financ. Stud. 2007, 20, 427–459. [Google Scholar] [CrossRef] [Green Version]

- Bates, D.S. Jumps and stochastic volatility: Exchange rate processes implicit in deutsche mark options. Rev. Financ. Stud. 1996, 9, 69–107. [Google Scholar] [CrossRef]

- Gatheral, J.; Jaisson, T.; Rosenbaum, M. Volatility is rough. Quant. Financ. 2018, 18, 933–949. [Google Scholar] [CrossRef]

- Mandelbrot, B.B.; Van Ness, J.W. Fractional Brownian motions, fractional noises and applications. SIAM Rev. 1968, 10, 422–437. [Google Scholar] [CrossRef]

- Fukasawa, M. Asymptotic analysis for stochastic volatility: Martingale expansion. Financ. Stoch. 2011, 15, 635–654. [Google Scholar] [CrossRef] [Green Version]

- Alòs, E.; León, J.A.; Vives, J. On the short-time behavior of the implied volatility for jump-diffusion models with stochastic volatility. Financ. Stoch. 2007, 11, 571–589. [Google Scholar] [CrossRef] [Green Version]

- Comte, F.; Renault, E. Long memory in continuous-time stochastic volatility models. Math. Financ. 1998, 8, 291–323. [Google Scholar] [CrossRef]

- Cheridito, P. Mixed fractional Brownian motion. Bernoulli 2001, 7, 913–934. [Google Scholar] [CrossRef]

- El Euch, O.; Rosenbaum, M. The characteristic function of rough Heston models. Math. Financ. 2019, 29, 3–38. [Google Scholar] [CrossRef] [Green Version]

- El Euch, O.; Fukasawa, M.; Rosenbaum, M. The microstructural foundations of leverage effect and rough volatility. Financ. Stoch. 2018, 22, 241–280. [Google Scholar] [CrossRef] [Green Version]

- Bennedsen, M.; Lunde, A.; Pakkanen, M.S. Hybrid scheme for Brownian semistationary processes. Financ. Stoch. 2017, 21, 931–965. [Google Scholar] [CrossRef] [Green Version]

- McCrickerd, R.; Pakkanen, M.S. Turbocharging Monte Carlo pricing for the rough Bergomi model. Quant. Financ. 2018, 18, 1877–1886. [Google Scholar] [CrossRef] [Green Version]

- Abi Jaber, E.; El Euch, O. Multifactor Approximation of Rough Volatility Models. SIAM J. Financ. Math. 2019, 10, 309–349. [Google Scholar] [CrossRef] [Green Version]

- Abi Jaber, E. Lifting the Heston model. Quant. Financ. 2019, 19, 1995–2013. [Google Scholar] [CrossRef]

- El Euch, O.; Gatheral, J.; Rosenbaum, M. Roughening Heston. Available online: https://ssrn.com/abstract=3116887 (accessed on 25 March 2019).

- Callegaro, G.; Grasselli, M.; Pages, G. Rough but not so tough: Fast hybrid schemes for fractional Riccati equations. arXiv 2018, arXiv:1805.12587. [Google Scholar]

- Momani, S.; Shawagfeh, N. Decomposition method for solving fractional Riccati differential equations. Appl. Math. Comput. 2006, 182, 1083–1092. [Google Scholar] [CrossRef]

- Odibat, Z.; Momani, S. Application of variational iteration method to nonlinear differential equations of fractional order. Int. J. Nonlinear Sci. Numer. Simul. 2006, 7, 27–34. [Google Scholar] [CrossRef]

- Odibat, Z.; Momani, S. Modified homotopy perturbation method: Application to quadratic Riccati differential equation of fractional order. Chaos Solitons Fractals 2008, 36, 167–174. [Google Scholar] [CrossRef]

- Cang, J.; Tan, Y.; Xu, H.; Liao, S.J. Series solutions of non-linear Riccati differential equations with fractional order. Chaos Solitons Fractals 2009, 40, 1–9. [Google Scholar] [CrossRef]

- Jafari, H.; Tajadodi, H.; Matikolai, S.H. Homotopy perturbation pade technique for solving fractional Riccati differential equations. Int. J. Nonlinear Sci. Numer. Simul. 2010, 11, 271–276. [Google Scholar] [CrossRef]

- Raja, M.A.Z.; Khan, J.A.; Qureshi, I.M. A new stochastic approach for solution of Riccati differential equation of fractional order. Ann. Math. Artif. Intell. 2010, 60, 229–250. [Google Scholar] [CrossRef]

- Diethelm, K.; Ford, N.J.; Freed, A.D. Detailed error analysis for a fractional Adams method. Numer. Algorithms 2004, 36, 31–52. [Google Scholar] [CrossRef] [Green Version]

- Gatheral, J.; Radoicic, R. Rational approximation of the rough Heston solution. Int. J. Theor. Appl. Financ. 2019, 22, 1950010. [Google Scholar] [CrossRef]

- Thompson, I.J. Coupled reaction channels calculations in nuclear physics. Comput. Phys. Rep. 1988, 7, 167–212. [Google Scholar] [CrossRef]

- Lanti, E.; Dominski, J.; Brunner, S.; McMillan, B.; Villard, L. Padé Approximation of the Adiabatic Electron Contribution to the Gyrokinetic Quasi-Neutrality Equation in the ORB5 Code; Journal of Physics: Conference Series; IOP Publishing: Bristol, UK, 2016; Volume 775, p. 012006. [Google Scholar]

- Rakityansky, S.; Sofianos, S.; Elander, N. Pade approximation of the S-matrix as a way of locating quantum resonances and bound states. J. Phys. A Math. Theor. 2007, 40, 14857. [Google Scholar] [CrossRef] [Green Version]

- Baker, G.A.; Baker, G.A., Jr.; Graves-Morris, P.; Baker, S.S. Padé Approximants; Cambridge University Press: Cambridge, UK, 1996; Volume 59. [Google Scholar]

- Lubinsky, D.S. Rogers-Ramanujan and the Baker-Gammel-Wills (padé) conjecture. Ann. Math. 2003, 157, 847–889. [Google Scholar] [CrossRef]

- Lubinsky, D.S. Reflections on the Baker–Gammel–Wills (Padé) Conjecture. In Analytic Number Theory, Approximation Theory, and Special Functions; Springer: Berlin, Germany, 2014; pp. 561–571. [Google Scholar]

- Starovoitov, A.P.; Starovoitova, N.A. Padé approximants of the Mittag-Leffler functions. Sb. Math. 2007, 198, 1011. [Google Scholar] [CrossRef]

- Winitzki, S. Uniform approximations for transcendental functions. In International Conference on Computational Science and Its Applications; Springer: Berlin, Germany, 2003; pp. 780–789. [Google Scholar]

- Atkinson, C.; Osseiran, A. Rational solutions for the time-fractional diffusion equation. SIAM J. Appl. Math. 2011, 71, 92–106. [Google Scholar] [CrossRef]

- Zeng, C.; Chen, Y.Q. Global Padé approximations of the generalized Mittag-Leffler function and its inverse. Fract. Calc. Appl. Anal. 2015, 18, 1492–1506. [Google Scholar] [CrossRef] [Green Version]

- Dumitru, B.; Kai, D.; Enrico, S. Fractional Calculus: Models and Numerical Methods; World Scientific: Singapore, 2012; Volume 3. [Google Scholar]

- Diethelm, K.; Ford, N.J.; Freed, A.D.; Luchko, Y. Algorithms for the fractional calculus: A selection of numerical methods. Comput. Methods Appl. Mech. Eng. 2005, 194, 743–773. [Google Scholar] [CrossRef] [Green Version]

- Li, C.; Tao, C. On the fractional Adams method. Comput. Math. Appl. 2009, 58, 1573–1588. [Google Scholar] [CrossRef] [Green Version]

- Black, F.; Scholes, M. The pricing of options and corporate liabilities. J. Political Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef] [Green Version]

- El Euch, O.; Rosenbaum, M. Perfect hedging in rough Heston models. Ann. Appl. Probab. 2018, 28, 3813–3856. [Google Scholar] [CrossRef] [Green Version]

- Gatheral, J. The Volatility Surface: A Practitioner’s Guide; John Wiley & Sons: Hoboken, NJ, USA, 2011; Volume 357. [Google Scholar]

- Alos, E.; Gatheral, J.; Radoičić, R. Exponentiation of conditional expectations under stochastic volatility. Quant. Financ. 2020, 20, 13–27. [Google Scholar] [CrossRef]

- Carr, P.; Madan, D. Option valuation using the fast Fourier transform. J. Comput. Financ. 1999, 2, 61–73. [Google Scholar] [CrossRef] [Green Version]

- Lewis, A. Option Valuation under Stochastic Volatility; Technical report; Finance Press: Newport Beach, CA, USA, 2000. [Google Scholar]

- Lewis, A.L. A Simple Option Formula for General Jump-Diffusion and other Exponential Lévy processes. 2001. Available online: https://ssrn.com/abstract=282110 (accessed on 15 February 2020).

- Haubold, H.J.; Mathai, A.M.; Saxena, R.K. Mittag-Leffler functions and their applications. J. Appl. Math. 2011, 2011, 298628. [Google Scholar] [CrossRef] [Green Version]

- Bateman, H. Higher Transcendental Functions [Volumes I-III]; McGraw-Hill Book Company: New York, NY, USA, 1953. [Google Scholar]

{kind=link}

{kind=link}

| u | ||||

|---|---|---|---|---|

| 0.001 | 0.0000 | 0.76% | 0.0000 | 0.47% |

| 1 | 0.0001 | 5.17% | 0.0001 | 2.53% |

| 2 | 0.0003 | 155.02% | 0.0004 | 10.88% |

| 3 | 0.0005 | 36.48% | 0.0010 | 22.30% |

| 4 | 0.0007 | 117.71% | 0.0016 | 37.03% |

| 5 | 0.0010 | 114.03% | 0.0023 | 53.30% |

| 6 | 0.0013 | 193.29% | 0.0030 | 64.30% |

| 7 | 0.0016 | 39.20% | 0.0038 | 69.46% |

| 8 | 0.0019 | 24.26% | 0.0047 | 71.08% |

| 9 | 0.0022 | 19.85% | 0.0056 | 70.74% |

| 10 | 0.0026 | 17.41% | 0.0066 | 69.36% |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jeng, S.W.; Kilicman, A. Fractional Riccati Equation and Its Applications to Rough Heston Model Using Numerical Methods. Symmetry 2020, 12, 959. https://doi.org/10.3390/sym12060959

Jeng SW, Kilicman A. Fractional Riccati Equation and Its Applications to Rough Heston Model Using Numerical Methods. Symmetry. 2020; 12(6):959. https://doi.org/10.3390/sym12060959

Chicago/Turabian StyleJeng, Siow W., and Adem Kilicman. 2020. "Fractional Riccati Equation and Its Applications to Rough Heston Model Using Numerical Methods" Symmetry 12, no. 6: 959. https://doi.org/10.3390/sym12060959

APA StyleJeng, S. W., & Kilicman, A. (2020). Fractional Riccati Equation and Its Applications to Rough Heston Model Using Numerical Methods. Symmetry, 12(6), 959. https://doi.org/10.3390/sym12060959