Optimizing Warehouse Building Design for Simultaneous Revenue Generation and Carbon Reduction in Taiwan: A Fuzzy Nonlinear Multi-Objective Approach

Abstract

1. Introduction

2. Literature Review

3. Methodology

3.1. Research Structure

3.2. Case Assumptions

3.3. Case Methodology

4. Sample Problem and Results

4.1. Case Introduction

4.2. Fuzzy Nonlinear Multi-Objective Method for TCQR

5. Discussion

6. Conclusions

6.1. Research Conclusions

- (1)

- Investment Revenue: Investment revenue is crucial for reducing carbon emissions, but development cannot be achieved if investors find a given venture unprofitable. In the long term, SPPPs generate clean energy without emitting carbon dioxide or other harmful gases. Additionally, SPPPs provide a source of revenue by selling green energy.

- (2)

- Emissions Management: Adopting a crash mode methodology expedites the construction of SPPPs, showcasing a critical mode of time management [33]. The primary achievement of this approach is the reduction in carbon emissions during construction via the minimization of construction time.

- (3)

- Methodology Choice: Fuzzy nonlinear multi-objective programming suits complex systems with high uncertainty and fuzzy objectives. Compared with NSGA-II, it is better at dealing with large-scale deterministic multi-objective problems; depending on the characteristics of the problem, researchers should select the more suitable model for their particular problem.

6.2. Research Recommendations

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

References

- Kumar, P.; Gupta, S.; Dagar, V. Sustainable energy development through non-residential rooftop solar photovoltaic adoption: Empirical evidence from India. Sustain. Dev. 2024, 32, 795–814. [Google Scholar] [CrossRef]

- Ronyastra, I.M.; Saw, L.H.; Low, F.S. Techno-economic analysis with financial risk identification for solar power plant as post-mining land use in Indonesia. Energy Sustain. Dev. 2024, 80, 101462. [Google Scholar] [CrossRef]

- Alzarrad, M.A.; Moynihan, G.P.; Hatamleh, M.T.; Song, S. Fuzzy multicriteria decision-making model for time-cost-risk trade-off optimization in construction projects. Adv. Civ. Eng. 2019, 2019, 7852301. [Google Scholar] [CrossRef]

- Ghadir, H.; Shayannia, S.A.; Miandargh, M.A. Solving the problem of time, cost, and quality trade-off in project scheduling under fuzzy conditions using meta-heuristic algorithms. Discret. Dyn. Nat. Soc. 2022, 2022, 6401061. [Google Scholar] [CrossRef]

- Egwunatum, S.I.; Oboreh, J.C. Factors limiting knowledge management among construction small and medium enterprises. J. Eng. Proj. Prod. Manag. 2022, 12, 25–38. [Google Scholar] [CrossRef]

- Aminbakhsh, S.; Abdulsattar, A.M. Optimizing Three-Dimensional Trade-Off Problem of Time–Cost–Quality over Multi-Mode Projects with Generalized Logic. Buildings 2024, 14, 1676. [Google Scholar] [CrossRef]

- Tarigan, E. Rooftop PV system policy and implementation study for a household in Indonesia. Int. J. Energy Econ. Policy 2020, 10, 110–115. [Google Scholar] [CrossRef]

- Komurlu, R.; Kalkan Ceceloglu, D.; Arditi, D. Exploring the Barriers to Managing Green Building Construction Projects and Proposed Solutions. Sustainability 2024, 16, 5374. [Google Scholar] [CrossRef]

- Briera, T.; Lefèvre, J. Reducing the cost of capital through international climate finance to accelerate the renewable energy transition in developing countries. Energy Policy 2024, 188, 114104. [Google Scholar] [CrossRef]

- Muñoz, Y.; Suárez, C.A.; Castro, A.O.; López, O.J. Technical and financial analysis for the implementation of small-scale self-generation projects, based on grid-tied photovoltaic solar energy, for residential users under Colombian regulations. Int. J. Energy Econ. Policy 2024, 14, 197–205. [Google Scholar] [CrossRef]

- Brest, P.; Gilson, R.J.; Wolfson, M.A. Essay: How investors can (and can’t) create social value. J. Corp. L. 2018, 44, 205. [Google Scholar]

- Stala-Szlugaj, K.; Olczak, P.; Kulpa, J.; Soltysik, M. Methodology for Selecting a Location for a Photovoltaic Farm on the Example of Poland. Energies 2024, 17, 2394. [Google Scholar] [CrossRef]

- Leewiraphan, C.; Ketjoy, N.; Thanarak, P. An assessment of the economic viability of delivering solar PV rooftop as a service to strengthen business investment in the residential and commercial sectors. Int. J. Energy Econ. Policy 2024, 14, 226–233. [Google Scholar] [CrossRef]

- Imasiku, K. A solar photovoltaic performance and financial modeling solution for grid-connected homes in Zambia. Int. J. Photoenergy 2021, 2021, 8870109. [Google Scholar] [CrossRef]

- Balducci, P.; Mongird, K.; Wu, D.; Wang, D.; Fotedar, V.; Dahowski, R. An evaluation of the economic and resilience benefits of a microgrid in Northampton Massachusetts. Energies 2020, 13, 4802. [Google Scholar] [CrossRef]

- Mashhadizadeh, M.; Dastgir, M.; Salahshour, S. Economic appraisal of investment projects in solar energy under uncertainty via fuzzy real option approach (case study: A 2-MW photovoltaic plant in South of Isfahan, Iran). Adv. Math. Financ. Appl. 2019, 3, 29–51. [Google Scholar] [CrossRef]

- Nuriyev, M. Z-numbers based hybrid MCDM approach for energy resources ranking and selection. Int. J. Energy Econ. Policy 2020, 10, 9950. [Google Scholar] [CrossRef]

- Thomasi, V.; Siluk, J.C.M.; Rigo, P.D.; Rosa, C.B.; Garcia, E.D.; Cassel, R.A.; Ramos, C.F.D.S. A model for measuring the photovoltaic project performance in energy auctions. Int. J. Energy Econ. Policy 2022, 12, 501–511. [Google Scholar] [CrossRef]

- Mohammadi, A.; Sheikholeslam, F. Intelligent optimization: Literature review and state-of-the-art algorithms (1965–2022). Eng. Appl. Artif. Intell. 2023, 126, 106959. [Google Scholar] [CrossRef]

- Bellman, R.E.; Zadeh, L.A. Decision-making in a fuzzy environment. Manag. Sci. 1970, 17, B-141–B-273. [Google Scholar] [CrossRef]

- Leandry, L.; Sosoma, I.; Koloseni, D. Basic fuzzy arithmetic operations using α-cut for the Gaussian membership function. J. Fuzzy Ext. Appl. 2022, 3, 337–348. [Google Scholar]

- Yang, J.; Liu, C.; Mi, Y.; Zhang, H.; Terzija, V. Optimization operation model of electricity market considering renewable energy accommodation and flexibility requirement. Glob. Energy Interconnect. 2021, 4, 227–238. [Google Scholar] [CrossRef]

- Middelhauve, L.; Baldi, F.; Stadler, P.; Maréchal, F. Grid-aware layout of photovoltaic panels in sustainable building energy systems. Front. Energy Res. 2021, 8, 573290. [Google Scholar] [CrossRef]

- Grisales-Noreña, L.F.; Montoya, O.D.; Cortés-Caicedo, B.; Zishan, F.; Rosero-García, J. Optimal power dispatch of PV generators in AC distribution networks by considering solar, environmental, and power demand conditions from Colombia. Mathematics 2023, 11, 484. [Google Scholar] [CrossRef]

- Zimmermann, H.J. Applications of fuzzy set theory to mathematical programming. Read. Fuzzy Sets Intell. Syst. 1993, 795–809. [Google Scholar] [CrossRef]

- Mohammadjafari, A.; Ghannadpour, S.F.; Bagherpour, M.; Zandieh, F. Multi-Objective Multi-mode Time-Cost Tradeoff modeling in Construction Projects Considering Productivity Improvement. arXiv 2024, arXiv:2401.12388. [Google Scholar] [CrossRef]

- Dong, W.; Shah, H.C. Vertex methods for computing functions of fuzzy variable. Fuzzy Sets Syst. 1987, 24, 65–78. [Google Scholar] [CrossRef]

- Yager, R.R. Concepts, theory, and techniques a new methodology for ordinal multi-objective decisions based on fuzzy sets. Decis. Sci. 1981, 12, 589–600. [Google Scholar] [CrossRef]

- Liou, T.S.; Wang, M.J.J. Ranking fuzzy numbers with integral value. Fuzzy Sets Syst. 1992, 50, 247–255. [Google Scholar] [CrossRef]

- Alwulayi, S.; Debbage, K. Factors Affecting the Willingness to Adopt Residential Rooftop Solar Panels: Evidence from Saudi Arabia. Arab. World Geogr. 2024, 27, 141–149. [Google Scholar] [CrossRef]

- Sama, J.D.L.C.; Some, K. Solving fuzzy nonlinear optimization problems using null set concept. Int. J. Fuzzy Syst. 2024, 26, 674–685. [Google Scholar] [CrossRef]

- Pham, V.H.S.; Nguyen Dang, N.T.; Nguyen, V.N. Achieving improved performance in construction projects: Advanced time and cost optimization framework. Evol. Intell. 2024, 17, 2885–2897. [Google Scholar] [CrossRef]

- Chiang, K.L. Delivering Goods Sustainably: A Fuzzy Nonlinear Multi-Objective Programming Approach for E-Commerce Logistics in Taiwan. Sustainability 2024, 16, 5720. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

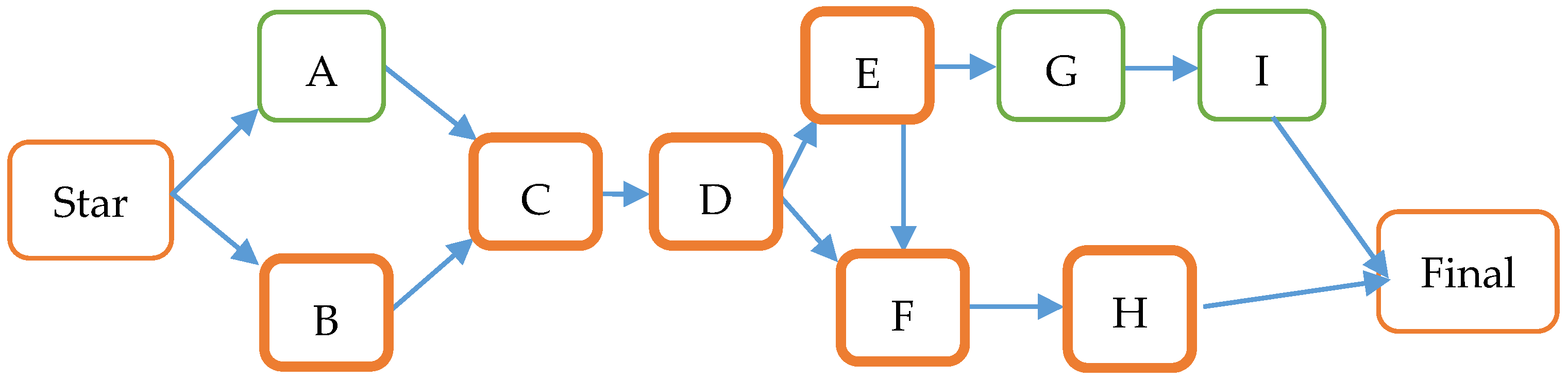

| Item | Prerequisites | Time (Days) | Cost (TWD) | Quality (%) | Quality Cost (TWD/%) | ||||

|---|---|---|---|---|---|---|---|---|---|

| Normal | Crash | Normal | Crash | Normal | Crash | Normal | Crash | ||

| A | 3 | 1 | 770,000 | 831,600 | 100 | 100 | 10,100 | 38,500 | |

| B | 4 | 1 | 1,026,667 | 1,108,800 | 100 | 100 | 11,100 | 47,200 | |

| C | B | 60 | 60 | 154,000 | 154,000 | 100 | 100 | – | – |

| D | B | 60 | 60 | 462,000 | 462,000 | 100 | 100 | – | – |

| E | D | 83 | 52 | 9,800,617 | 10,584,666 | 98 | 75 | 16,000 | 70,600 |

| F | B, D | 51 | 48 | 4,825,176 | 5,211,190 | 95 | 93 | 13,500 | 54,400 |

| G | F | 51 | 48 | 4,078,001 | 4,698,600 | 95 | 93 | 7800 | 27,700 |

| H | F, G | 30 | 30 | 154,000 | 154,000 | 100 | 100 | – | – |

| I | F, G, H | 30 | 30 | 154,000 | 154,000 | 100 | 100 | – | – |

| Wd (%) | FKd (%) | Ws (%) | FKs (%) | FT (%) | FWACC (%) |

|---|---|---|---|---|---|

| 0 | – | 100 | [1.3, * 1.710546, 2.2] | [30, 30, 30] | [1.3, 1.710546, 2.2] |

| 10 | [1.635, 1.767987, 1.908] | 90 | [1.2, 1.608033, 2.1] | [30, 30, 30] | [1.202625, 1.579828, 2.0331] |

| 20 | [1.363, 1.494876, 1.635] | 80 | [1.1, 1.505167, 2] | [30, 30, 30] | [1.08445, 1.428365, 1.84525] |

| 30 | [1.09, 1.221415, 1.363] | 70 | [1, 1.401868, 1.9] | [30, 30, 30] | [0.94525, 1.256126, 1.636675] |

| 40 | [1.09, 1.09, 1.09] | 60 | [0.9, 1.298025, 1.8] | [30, 30, 30] | [0.867, 1.105815, 1.407] |

| 50 | [1.09, 1.221415, 1.363] | 50 | [0.8, 1.193483, 1.7] | [30, 30, 30] | [0.80875, 1.054772, 1.361125] |

| 60 | [1.363, 1.494876, 1.635] | 40 | [0.7, 1.088024, 1.6] | [30, 30, 30] | [0.89335, 1.107904, 1.37575] |

| 70 | [1.635, 1.767987, 1.908] | 30 | [0.8, 1.193483, 1.7] | [30, 30, 30] | [1.098375, 1.286238, 1.5117] |

| Debt Ratio (%) | α-Cut | ||||

|---|---|---|---|---|---|

| 0 | 0 | [1.3, 2.2] | 1.505272874 | 1.955272874 | 3.460545749 |

| 0.2 | [1.382109, 2.102109] | ||||

| 0.4 | [1.464218, 2.004218] | ||||

| 0.6 | [1.546327, 1.906327] | ||||

| 0.8 | [1.628437, 1.808437] | ||||

| 1 | [1.710546, 1.710546] | ||||

| 10 | 0 | [1.202625, 2.0331] | 1.391226652 | 1.806464152 | 3.197690804 |

| 0.2 | [1.278066, 1.942446] | ||||

| 0.4 | [1.353506, 1.851791] | ||||

| 0.6 | [1.428947, 1.761137] | ||||

| 0.8 | [1.504388, 1.670483] | ||||

| 1 | [1.579828, 1.579828] | ||||

| 20 | 0 | [1.08445, 1.84525] | 1.256407623 | 1.636807623 | 2.893215246 |

| 0.2 | [1.153233, 1.761873] | ||||

| 0.4 | [1.222016, 1.678496] | ||||

| 0.6 | [1.290799, 1.595119] | ||||

| 0.8 | [1.359582, 1.511742] | ||||

| 1 | [1.428365, 1.428365] | ||||

| 30 | 0 | [0.94525, 1.636675] | 1.100688093 | 1.446400593 | 2.547088686 |

| 0.2 | [1.007425, 1.560565] | ||||

| 0.4 | [1.0696, 1.484455] | ||||

| 0.6 | [1.131776, 1.408346] | ||||

| 0.8 | [1.193951, 1.332236] | ||||

| 1 | [1.256126, 1.256126] | ||||

| 40 | 0 | [0.867, 1.407] | 0.986407384 | 1.256407384 | 2.242814768 |

| 0.2 | [0.914763, 1.346763] | ||||

| 0.4 | [0.962526, 1.286526] | ||||

| 0.6 | [1.010289, 1.226289] | ||||

| 0.8 | [1.058052, 1.166052] | ||||

| 1 | [1.105815, 1.105815] | ||||

| 50 | 0 | [* 0.80875, * 1.361125] | 0.931761138 | 1.207948638 | * 2.139709777 |

| 0.2 | [0.857954, 1.299854] | ||||

| 0.4 | [0.907159, 1.238584] | ||||

| 0.6 | [0.956363, 1.177313] | ||||

| 0.8 | [1.005568, 1.116043] | ||||

| 1 | * [1.054772, 1.054772] | ||||

| 60 | 0 | [0.89335, 1.37575] | 1.000626905 | 1.241826905 | 2.24245381 |

| 0.2 | [0.936261, 1.322181] | ||||

| 0.4 | [0.979172, 1.268612] | ||||

| 0.6 | [1.022082, 1.215042] | ||||

| 0.8 | [1.064993, 1.161473] | ||||

| 1 | [1.104904, 1.107904] | ||||

| 70 | 0 | [1.098375, 1.5117] | 1.192306596 | 1.398969096 | 2.591275691 |

| 0.2 | [1.135948, 1.466608] | ||||

| 0.4 | [1.17352, 1.421515] | ||||

| 0.6 | [1.211093, 1.376423] | ||||

| 0.8 | [1.248666, 1.331331] | ||||

| 1 | [1.286238, 1.286238] |

| Item | Time (Days) | Cost (TWD) | Quality (%) | ||||||

|---|---|---|---|---|---|---|---|---|---|

| B | 1 | 2.15 | 4 | 1,026,667 | 1,067,206.75 | 1,108,800 | 100 | 100.00 | 100 |

| E | 52 | 66.29 | 83 | 9,800,617 | 10,187,613.07 | 10,584,666 | 75 | 85.99 | 98 |

| F | 48 | 49.48 | 51 | 4,825,176 | 5,015,707.33 | 5,211,190 | 93 | 94.00 | 95 |

| Item | Unit Time Cost | Unit Time Quality | |||||||

| B | −24,639.90 | −27,286.11 | −30,115.44 | 0 | 0.00 | 0 | |||

| E | −22,762.71 | −25,207.31 | −27,821.09 | 0.666 | 0.74 | 0.814 | |||

| F | −186,179.70 | −206,174.46 | −227,552.96 | 0.603 | 0.67 | 0.737 | |||

| α | Item | ||

|---|---|---|---|

| B | E | F | |

| 0 | [1, 4] | [52, 83] | [48, 51] |

| 0.2 | [1.23, 3.63] | [54.858, 79.658] | [48.296, 50.696] |

| 0.4 | [1.46, 3.26] | [57.716, 50.392] | [48.592, 50.392] |

| 0.6 | [1.69, 2.89] | [48.888, 72.974] | [48.888, 50.088] |

| 0.8 | [1.92, 2.52] | [63.432, 69.632] | [49.184, 49.784] |

| 1 | [2.15, 2.15] | [66.29, 66.29] | [49.48, 49.48] |

| Ranking | 4.65 | * 133.79 | 98.98 |

| α | Item | ||

|---|---|---|---|

| B | E | F | |

| 0 | [1,026,667, 1,108,800] | [9,800,617, 10,584,666] | [4,825,176, 5,211,190] |

| 0.2 | [1,034,775, 1,100,481] | [9,878,016, 10,505,255] | [4,863,282, 5,172,093] |

| 0.4 | [1,042,883, 1,092,163] | [9,955,415, 10,425,845] | [4,901,389, 5,132,997] |

| 0.6 | [1,050,991, 1,083,844] | [10,032,815, 10,346,434] | [4,939,495, 5,093,900] |

| 0.8 | [1,059,099, 1,075,525] | [10,110,214, 10,267,024] | [4,977,601, 5,054,804] |

| 1 | [1,067,207, 1,067,207] | [10,187,613, 10,187,613] | [5,015,707, 5,015,707] |

| Ranking | 2,134,940.249 | * 20,380,254.57 | 10,033,890.33 |

| α | Item | ||

|---|---|---|---|

| B | E | F | |

| 0 | [11,100, 47,200] | [16,000, 70,600] | [13,500, 54,400] |

| 0.2 | [13,842.09, 42,722.09] | [20,114.21, 63,794.21] | [16,642.8, 49,362.8] |

| 0.4 | [16,584.18, 38,244.18] | [24,228.42, 56,988.42] | [19,785.59, 44,325.59] |

| 0.6 | [19,326.27, 33,766.27] | [28,342.63, 50,182.63] | [22,928.39, 39,288.39] |

| 0.8 | [22,068.35, 29,288.35] | [32,456.85, 43,376.85] | [26,071.19, 34,251.19] |

| 1 | [24,810.44, 24,810.44] | [36,571.06, 36,571.06] | [29,213.99, 29,213.99] |

| Ranking | 53,960.44262 | * 79,871.05817 | 63,163.98592 |

| α | Item | ||

|---|---|---|---|

| B | E | F | |

| 0 | [−24,557.5, −30,014.7] | [−22,686.6, −27,728] | [−185,557, −226,792] |

| 0.2 | [−25,103.2, −29,469] | [−23,190.7, −27,223.9] | [−189,681, −222,668] |

| 0.4 | [−25,648.9, −28,923.3] | [−23,694.9, −26,719.7] | [−193,804, −218,545] |

| 0.6 | [−26,194.7, −28,377.5] | [−24,199, −26,215.6] | [−197,927, −214,421] |

| 0.8 | [−26,740.4, −27,831.8] | [−24,703.2, −25,711.5] | [−202,051, −210,298] |

| 1 | [−27,286.1, −27,286.1] | [−25,207.3, −25,207.3] | [−206,174, −206,174] |

| Ranking | −54,572.2104 | * −50,414.62215 | −412,348.9284 |

| α | Item | ||

|---|---|---|---|

| B | E | F | |

| 0 | [0, 0] | [0.666, 0.814] | [0.603, 0.737] |

| 0.2 | [0, 0] | [0.680305, 0.798705013] | [0.615952, 0.723152] |

| 0.4 | [0, 0] | [0.69461, 0.783410026] | [0.628904, 0.709304] |

| 0.6 | [0, 0] | [0.708915, 0.768115039] | [0.641856, 0.695456] |

| 0.8 | [0, 0] | [0.72322, 0.752820052] | [0.654807, 0.681607] |

| 1 | [0, 0] | [0.737525, 0.737525065] | [0.667759, 0.667759] |

| Ranking | 0 | * 1.477525065 | 1.337759181 |

| Year | FMIRR (%) | Year | FMIRR (%) |

|---|---|---|---|

| 1 | [−84.4965, −84.4018, −84.3190] | 11 | [5.8952, 5.9538, 6.0049] |

| 2 | [−44.0510, −43.8805, −43.7317] | 12 | [6.2446, 6.2985, 6.3454] |

| 3 | [−22.0282, −21.8699, −21.7319] | 13 | [6.4842, 6.5341, 6.5775] |

| 4 | [−10.6232, −10.4870, −10.3685] | 14 | [6.6451, 6.6915, 6.7318] |

| 5 | [−4.2377, −4.1211, −4.0195] | 15 | [6.7485, 6.7918, 6.8295] |

| 6 | [−0.4087, −0.3076, −0.2196] | 16 | [6.8095, 6.8502, 6.8855] |

| 7 | [2.0088, 2.0976, 2.1748] | 17 | [6.8390, 6.8772, 6.9105] |

| 8 | [3.5934, 3.6723, 3.7409] | 18 | [6.8448, 6.8809, 6.9124] |

| 9 | [4.6599, 4.7307, 4.7924] | 19 | [6.8327, 6.8670, 6.8968] |

| 10 | [5.3903, 5.4545, 5.5104] | 20 | [6.8073, 6.8398, 6.8681] |

| Item | Time (Days) | Cost (TWD) | Quality (%) | Crash Time (Days) (7) = (1) − (2) | Unit Time Cost (TWD/Day) [((3) − (4))/(7)] | Unit Time Quality (%/Day) [((5) − (6))/(7)] | |||

|---|---|---|---|---|---|---|---|---|---|

| Normal (1) | Crash (2) | Normal (3) | Crash (4) | Normal (5) | Crash (6) | ||||

| A | 3 | 1 | 770,000 | 831,600 | 100 | 100 | 2 | −30,800 | 0 |

| B | 4 | 1 | 1,026,667 | 1,108,800 | 100 | 100 | 3 | −27,377.67 | 0 |

| C | 60 | 60 | 154,000 | 154,000 | 100 | 100 | 0 | 0 | 0 |

| D | 60 | 60 | 462,000 | 462,000 | 100 | 100 | 0 | 0 | 0 |

| E | 83 | 52 | 9,800,617 | 10,584,666 | 98 | 75 | 31 | −25,291.90 | 0.74 |

| F | 51 | 48 | 4,825,176 | 5,211,190 | 95 | 93 | 3 | −128,671.33 | 0.67 |

| G | 51 | 48 | 4,078,001 | 4,698,600 | 95 | 93 | 3 | −206,866.33 | 0.67 |

| H | 30 | 30 | 154,000 | 154,000 | 100 | 100 | 0 | 0 | 0 |

| I | 30 | 30 | 154,000 | 154,000 | 100 | 100 | 0 | 0 | 0 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chiang, K.-L. Optimizing Warehouse Building Design for Simultaneous Revenue Generation and Carbon Reduction in Taiwan: A Fuzzy Nonlinear Multi-Objective Approach. Buildings 2024, 14, 2441. https://doi.org/10.3390/buildings14082441

Chiang K-L. Optimizing Warehouse Building Design for Simultaneous Revenue Generation and Carbon Reduction in Taiwan: A Fuzzy Nonlinear Multi-Objective Approach. Buildings. 2024; 14(8):2441. https://doi.org/10.3390/buildings14082441

Chicago/Turabian StyleChiang, Kang-Lin. 2024. "Optimizing Warehouse Building Design for Simultaneous Revenue Generation and Carbon Reduction in Taiwan: A Fuzzy Nonlinear Multi-Objective Approach" Buildings 14, no. 8: 2441. https://doi.org/10.3390/buildings14082441

APA StyleChiang, K.-L. (2024). Optimizing Warehouse Building Design for Simultaneous Revenue Generation and Carbon Reduction in Taiwan: A Fuzzy Nonlinear Multi-Objective Approach. Buildings, 14(8), 2441. https://doi.org/10.3390/buildings14082441