1. Introduction

People migrate from one destination to another to improve their living standards and those of their families in their home countries in the form of remittances. Remittances are items or financial instruments that migrants who are living and working abroad transfer to their families in their home countries. According to some scholars, remittances are important because of their impacts on improving the balance of payment position and living standard conditions in the recipient countries (

Ratha 2003;

Datta and Sarkar 2014;

Kannan and Hari 2020;

Qutb 2022;

Oyadeyi and Akinbobola 2022;

Oyadeyi 2023a). For at least the past three decades, migrant remittances have been regarded as an essential tool for economic development due to their effect on the recipient countries to encourage investments, boost consumption, speed up production and job creation, and indirectly boost the income of families who do not receive remittances (

Taylor 1999;

Aggarwal et al. 2006;

Lucas 2006,

2008;

Qutb 2022;

Oyadeyi 2023b,

2023c). According to

Kamuleta (

2014) and

Qutb (

2022), remittance capital flows have outperformed foreign portfolio investments and private debt flows in recent times. In fact, global remittances continued to grow even during the financial crisis, the COVID-19 pandemic, and other economic downturn events. The foregoing represent reasons why the study of global remittances continues to receive attention among scholars.

There are empirical and policy motivations to further study the role of remittance flows, although the present study examines its impact on several macroeconomic performance indicators. This derives from the attraction of remittances as a tool for macroeconomic development, which needs to be substantiated with empirical investigation. In 2020, global remittance reached roughly USD 1.1 trillion, about 0.79 percent as a percentage of global gross domestic product (GDP) (

World Development Indicator 2023). According to the

World Population Review (

2023), global migration reached over 315 million people in 2020, and most of the migrants are from developing to advanced nations, where remittances constitute about 27 percent of the GDP of the former countries (

Meyer and Shera 2017). In other words, as the relationship between global migration and remittances strengthens, it interestingly becomes more crucial to consider the macroeconomic effects of remittances in order to inform policymakers in the nations where migration is most prevalent. The topic under discussion here offers compelling justification for further research into the relationship between remittances and macroeconomic performance, with a focus on the top migrating nations (those most adversely affected by emigration). In essence, this study can be insightful and assist decision-makers in creating the best possible policies to transform the economic potential of migrant remittances into a dependable source of capital that produces steady economic growth.

The present study makes contributions to an emerging area of research given that the debate on the macroeconomic effect of remittance flows still rages on. For instance, some studies find roles for remittance inflows to improve production, consumption, investments, income distribution, savings, and poverty reduction in recipient countries (

Haas 2005;

Carling 2008;

Anyanwu and Erhijakpor 2010;

Rao and Hassan 2012;

Ustubici and Irdam 2012;

Blouchoutzi and Nikas 2014;

Dridi et al. 2019;

Kannan and Hari 2020;

Agyei 2021;

Oyadeyi 2023d;

Oyadeyi et al. 2024), while others opine that the impact of remittances on the recipient country can be ambiguous, as a rise in consumption brought about by an increase in migrant remittances may also have detrimental consequences on the recipient countries (

World Bank Group 2006;

Stojanov et al. 2019;

Koczan et al. 2021;

Bidawi et al. 2022). In the midst of these arguments, we re-examine the effects of remittances on the macroeconomic performance of top emigrating countries, given the following empirical contributions.

Therefore, the objective of this paper is to examine the effects of remittances on the macroeconomic performance of the selected countries, using both time-series and panel data approaches. This is because as the relationship between global migration and remittances strengthens, it interestingly becomes more crucial to consider the macroeconomic effects of remittances to inform policymakers in the nations where migration is most prevalent. Thus, this study focuses on the countries most affected by emigration and the effects of remittances on their economic performance. The rationale for undertaking this study is that it can be insightful and assist decision-makers in creating the best possible policies to transform the economic potential of migrant remittances into a dependable source of capital that produces steady economic growth. To reach this goal, the study uses the Feasible Quasi Generalized Least Square (FQGLS) and Dynamic Common Correlated Effects (DCCE) methods to find out how remittances affect the economies of the chosen countries. In essence, the study’s research hypothesis is to test whether an increased inflow of remittances positively affects a country’s macroeconomic performance.

The framework of the study involves estimating the models by selecting eleven out of twenty top emigrating countries (based on data availability) for the analyses of the research objective such that the scope of the study comprises nine (9) emerging countries (Bangladesh, China, India, Mexico, Pakistan, the Philippines, Indonesia, Myanmar, and Egypt) and two (2) advanced economies (Germany and the United Kingdom). The data were sourced based on the top twenty emigrating countries, according to the

World Population Review (

2023). From the country list, the handpicked countries were selected as a result of data availability for the sampled period. Our analyses consist of how remittance flows to these countries impact four various measures of macroeconomic performance, namely, nominal output (nominal GDP), real output (real GDP), nominal output per capita (GDP per capita), and real output per capita (real GDP per capita). These are explored over a collective study of the countries as panels and individual country analyses, using suitable panel data and time-series econometric data analysis techniques. In addition to the robustness checks mentioned above, different analyses of models with and without the role of the control variable and taking into account the macroeconomic environment of the countries being studied were also carried out. This was done to get rid of the effect of outliers. In all, these endeavors produce interesting findings that yield relevant policy prescriptions rendered in the concluding section.

The rest of the paper is designed as follows:

Section 2 expands on the stylized facts on remittance and its nexus to macroeconomic performance, while

Section 3 discusses the analytical approaches to achieving the objectives.

Section 4 analyses and presents the results, while the final section concludes the paper with policy advice for consideration.

2. Stylized Facts

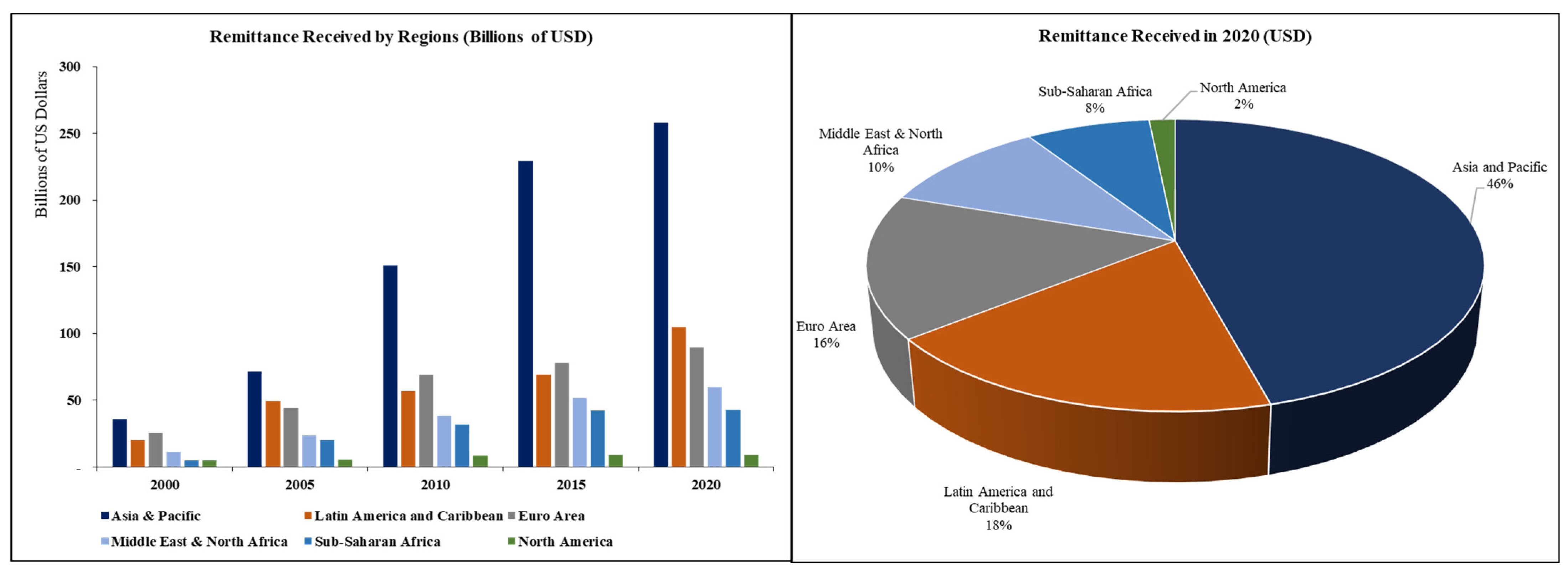

Remittance, as we know it, is a form of capital flow due to the movement of people among countries. Remittance payments grew steadily over the last 20 years in the period of focus in the study. The Asia and Pacific region received the most remittances during the period under investigation. They constitute roughly 46 percent of the total remittances received as of 2020. The region with the second biggest receipts of remittances is the Latin America and Caribbean region, which had roughly 18 percent of the total 2020 remittances. The charts also show that North America receives far fewer remittances globally, while Sub-Saharan Africa is not the greatest beneficiary of remittances when compared with other regions. These results point to the conclusion that the regions that are less developed, such as Asia, Latin America, and the Caribbean, and the combined Middle East and Sub-Saharan African region, receive more from global remittances than other regions (especially the advanced countries of Europe and America).

Figure 1 identifies the top countries where most migrants come from as of 2020. The chart showed that most migrants come from emerging markets and developing economies (EMDEs). The top EMDE countries people emigrate from include countries such as India, Mexico, China, the Philippines, Pakistan, and a host of others listed in

Figure 1. People migrate to advanced economies due to the level of development and industrialization in these countries, to seek a better life and job opportunities and then remit some of the incomes they earn back to their families in their home country. According to the United Nations Department of Economic and Social Affairs, Population Division (UNDESA), some of the people in advanced countries migrate to destinations such as the United States (US), the United Kingdom (UK), France, Germany, Spain, Australia, and others (

UNDESA 2020). Furthermore, the chart affirms that countries facing high levels of geopolitical risk, such as Pakistan, the Philippines, and Bangladesh, feature prominently in the list of countries people emigrate from. From the list, India had the highest number of emigrants and the highest number of emigrants per population. A reason for this may be due to their overpopulation as well as their high levels of poverty, which make their citizens leave the country to seek greener pastures. Mexicans also feature very high on the list, as 8.6 percent of their population migrated, mostly to the US. Many other countries, such as the Philippines, Myanmar, and the UK, also have high levels of emigrants per population. By location, the Asian region has the highest number of emigrants globally, as seven of the eleven countries examined come from that region, while two European countries (Germany and the UK), one North American country (Mexico), and one North African country (Egypt) feature prominently on the list of countries that were examined.

Figure 2 and

Figure 3 present the remittance flows to the top emigrating countries across regions and across countries, respectively. Of the selected countries, India received the largest remittances globally since 2000. It rose from USD 12.9 billion in the year 2000 to USD 83.1 billion in 2020, a rise of about 544 percent over the 21-year period. Furthermore, India’s remittance inflow grew steadily over the 21-year period, averaging USD 53 billion in 2010 and rising to USD 83.1 billion by 2020. It is expected that in the future, India will continue to receive the largest remittance inflows globally. Mexico and the Philippines have both received the second and third largest remittances globally after India since 2000. Currently, remittances from Mexico (USD 42.9 billion) rank higher than those from the Philippines (USD 34.9 billion), even though their positions have been swapped on several occasions over the period.

Remittance inflows from Egypt and Pakistan rank highly on the list at USD 29.6 billion and USD 26.1 billion, respectively. Remittance inflows from China, Bangladesh, and Germany as of 2020 are very close to one another, between USD 18.9 billion and USD 21.8 billion. Remittances fell from a high of USD 33 billion in 2015 in China to USD 18.9 billion in 2020, implying that fewer Chinese citizens are migrating from the country within those 5 years. Finally, remittance inflows from Indonesia, the United Kingdom, and Myanmar fell below USD 10 billion as of 2020, with Indonesia having the highest inflows at USD 9.7 billion, the United Kingdom coming in second at USD 3.2 billion, and Myanmar coming in third at USD 2.2 billion. Remittance inflows into the United Kingdom fell from roughly USD 5.4 billion in 2000 to roughly USD 3.2 billion in 2020, peaking at USD 6.6 billion in 2007 during the global financial crisis.

Figure 4a,b illustrate the comparison between remittance inflows, foreign direct investment (FDI) inflows, foreign portfolio investment (FPI) inflows, and official development assistance (ODA) inflows.

Figure 4a demonstrates that remittances contribute the largest amount of capital flows to the selected EMDEs. Therefore, it can be assumed that remittance is critical to the growth and development of these economies, and it would be important to establish the significant contributions of remittance inflows to these economies. On the other hand,

Figure 4b shows that remittance constitutes the second largest form of inflow into the selected countries, lagging only behind FDI inflows. For countries with a higher level of industrial development, such as the United Kingdom, Germany, Indonesia, and China, FDI inflows outstrip remittance inflows during the period under investigation. But remittance remained the second-largest source of inflows for these countries (except the UK). However, the narrative changed for Mexico and Myanmar in 2018 as remittances became the highest form of inflow for these countries. These results highlight the importance of remittance in the selected economies, especially the EMDEs in both

Figure 4a,b. These findings, amongst others, were one of the reasons why the econometric analysis focused on the impacts of remittance inflows on the macroeconomy of these countries to establish the significance of remittance inflows on these economies.

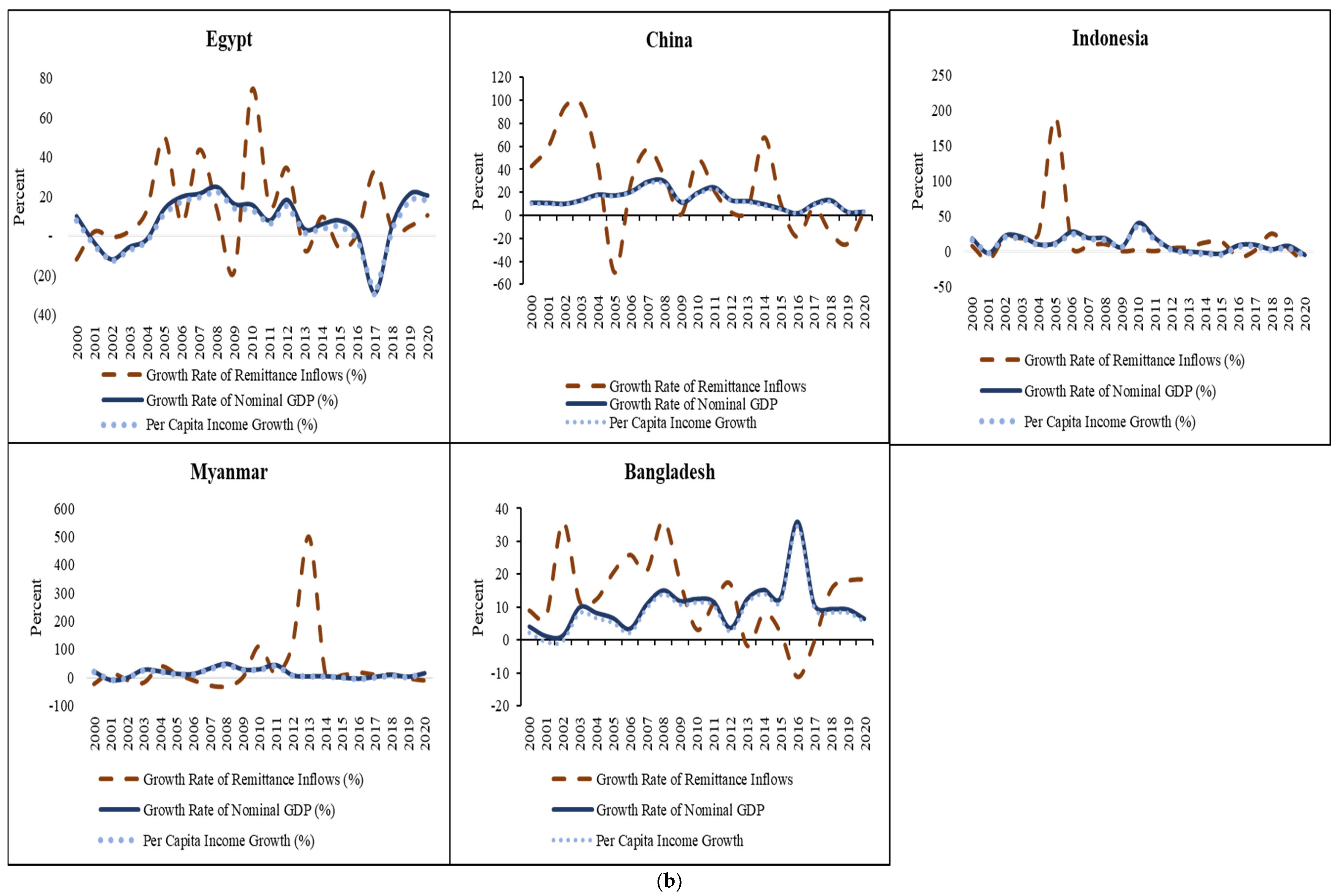

Figure 5a,b display the comparison between remittance income growth, nominal GDP growth, and per capita income growth. The essence is to ascertain the growth movement in these variables and to compare whether growth rates are in tandem or otherwise. In

Figure 5a, the data showed that the growth rate of remittances and income (nominal GDP and GDP per capita) followed a similar pattern for Germany and the UK throughout the period under study. Furthermore, the trend analysis showed that except for a few years during the examined period, overall, the growth in remittance inflows followed an almost similar pattern as the growth rate in nominal GDP and per capita income for India, Mexico, Pakistan, and the Philippines. Their growth rates largely fluctuated at almost similar intensity during the period under investigation. These results may point to the suggestion that remittances may have some contributions to the income level and income per capita growth in these countries. Further investigations to ascertain whether this impact is significant will be empirically tested in the next section.

In

Figure 5b, the growth rate of remittance inflows, nominal GDP, and GDP per capita for Bangladesh, China, Egypt, Indonesia, and Myanmar also fluctuated throughout the period, but the fluctuations did not follow the exact same patterns during the period under investigation, even though the patterns were very similar for some years. Furthermore, the data showed that the growth rate in remittance inflows fluctuated more than the nominal GDP and per capita income. Finally, the trend analysis showed that nominal GDP and GDP per capita followed the same trend throughout the period under investigation. These findings might imply that remittances make some contributions to these countries’ income. It is important to note that the investigation of the trend analysis is not to check if there is any causation or correlation between the variables. Rather, this section focuses on the patterns of income growth to see if there is any unique pattern in the remittance growth relationships and to ascertain the reasons for these patterns. The results showed that, in general, the patterns of remittance and income growth were similar for most periods during the investigation. However, a useful way to test the significance of these patterns will be to establish the impacts of remittance inflows on income, income per capita, and the output growth of these countries using econometric techniques, which will be discussed at length in the next sections.

3. Materials and Methods

This study examines the response of macroeconomic performance indicators in respective countries to remittance flows into the economies, with comparison for the countries with highest numbers of emigrants. In the data analysis, we look at the impacts of remittance received (remittance inflow in USD) on a number of macroeconomic indicators in the selected countries. The macroeconomic fundamentals examined are the log of nominal gross domestic product, the log of real gross domestic product, the log of nominal gross domestic product per capita, the log of real gross domestic product per capita, and inflation rate used as a control variable to measure the macroeconomic environment. For further robustness, we examine the nexus for the individual countries and as a group, using relevant time-series and panel data analytical techniques. The data are in annual frequency (1987–2021) and sourced from the

World Development Indicator (

2023). The sample used in the study contains eleven top emigrating countries (Bangladesh, China, India, Mexico, Pakistan, the Philippines, Indonesia, Myanmar, Egypt, Germany, and the United Kingdom). The choice of these eleven countries selected in this study comes from the list of the top twenty emigrating countries but is limited by data availability based on the

World Population Review’s (

2023) dataset. Therefore, the eleven countries from the top twenty list were selected based on their availability of data during the sample period. The sampled countries comprise nine emerging market countries and two developed countries. Their inclusion in the study was due to their high level of emigration outside their home countries. Using both time-series and panel data sets on the selected countries, this study will ascertain whether remittances may serve as a way of fostering the economies of the selected countries.

For the country-specific analyses, we employ the Feasible Quasi Generalized Least Squares (FQGLS) estimator (

Westerlund and Narayan 2015), which assists us in circumventing the unit root problem that characterizes many macroeconomic variables, including the ones under investigation, to address any endogeneity bias that could cloud the model due to bivariate model specification. A similar model that also accounts for nonstationarity and endogeneity bias and cross sectional dependence [Dynamic Common Correlated Effects (DCCE) model] was adopted for panel data analyses (

Chudik and Pesaran 2015;

Chudik et al. 2016;

Salisu et al. 2022).

For the country-specific analyses, we capture the relationship between remittances and macroeconomic performance indicators such that macroeconomic performance in the current period (

) is determined by remittance inflows in the previous period (

), as follows:

The specification in Equation (1) cannot be estimated directly with the least squares technique given that the dependent and explanatory variables, like several other macroeconomic variables, exhibit a stochastic trend that make them nonstationary and therefore present persistence effect. The conventional econometric technique would also prove spurious due to endogeneity bias since a single predictor is considered and other possible regressors are suppressed to maintain focus, and the model is also a dynamic model. The FQGLS technique helps to correct for these effects in addition to any possible heteroscedasticity by pre-weighting the data by the inverse of the standard error of the residual obtained from Equation (1). Hence, the adoption of this method precludes the need to evaluate unit root tests and include several predictors in the model. Several additional details of the technique can be found in

Sharma (

2021);

Salisu et al. (

2021,

2023);

Adediran et al. (

2021). These are captured in Equation (2) as follows:

There are four variants of the variable: nominal output, nominal output per capita, real output, and real output per capita are all expressed in log form and included one at a time, and inflation is included as a control variable. The predictor variable, , is measured as remittance inflow in USD. With these variants and the foregoing econometric effects, we estimate Equation (2) to obtain the respective coefficients that define the impacts of remittance flows on the respective macroeconomic variables in each of the selected top emigrating countries.

In addition to the time-series analyses, we proceed with the group analyses for the top emigrant panel with the DCCE approach that accounts for salient data properties such as nonstationarity and endogeneity bias and cross-sectional dependence as follows.

where

for the number of emigrating countries and

for the number of time period considered in each panel;

has been previously defined as the respective macroeconomic performance indicators: the log of nominal and real gross domestic products, the log of nominal and real GDP per capita, and inflation rate;

is the measure of remittance inflow into the economy expressed in USD;

is inflation used as a control variable; the inclusion of

and

introduce cross-sectional average to correct the respective models for endogeneity bias due to the dynamic nature of the models as

and

are included to correct for persistence;

and

are the two-way error terms of the models that can be divided into time-variant (

) component, time-invariant factor loadings (

and

), and the remainder error (

and

);

and

are the heterogenous parameters of interest analogous to

coefficients obtained in the time-series analysis and are determined through Wald test:

and

.

5. Conclusions

This study examines how remittance inflow affects macroeconomic performance in top emigrating countries. We select eleven countries, based on data availability, from the top twenty emigrating countries as published in the

World Population Review (

2023). This list produces a mixture of emerging and advanced countries, which ensures that this study is more robust, unlike past similar studies that mostly focus on specific countries. All variables are measured in USD and are sourced from the World Development Indicators between 1987 and 2021. The macroeconomic indicators examined are nominal gross domestic product, real gross domestic product, nominal gross domestic product per capita, and real gross domestic product per capita, whereas remittance inflow is the predictor series and at the center of the discussion. The data analyses conducted in this study are extensive, including preliminary statistics (mean, standard deviation, coefficient of variation, and ADF tests), charts and figures, and formal analysis (time-series analysis using the Feasible Quasi Generalized Least Squares (FQGLS) estimator and panel data analysis using the Dynamic Common Correlated Effects (DCCE) model).

The preliminary results suggest that the Asia and Pacific region contributes more to the number of emigrants and also receives the most remittances. The group results show that remittance positively affects economies in terms of better economic performance. For the country-specific analyses, this outcome still largely holds true for most of the countries when nominal GDP is considered, unlike when real GDP is considered. The positive takeaway from this study is that the emigrating countries can benefit from diaspora remittance inflow in terms of improved productivity. The foregoing results indicate that the net-remittance-receiving countries could take more advantage of the diaspora remittance flow by creating a better environment that facilitates the receipt of such funds from citizens in the diaspora, as it has been shown as one of the ways of contributing to the economic growth of the countries. In countries where the results are not favorable, there may be a need for financial policies to be better targeted at remittances to ensure that the bulk of them is channeled to investment purposes rather than consumption. this study recommends improved financial systems that perform two roles: one, financial policies that facilitate the receipt of diaspora remittances to consolidate the positive impact on the economies, and two, policies that better channel the inflows from consumption into investment purposes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}