1. Background and Issues

China is an aging society, and according to the National Bureau of Statistics, the working population decreased by 3.45 million in 2012

1. According to the UN (

Population Division, DESA, United Nations 2001), China’s aging process began in 1995–2000, when the ratio of the population aged 65 and over began to exceed 7%. According to the 2010 World Population Project

2, China’s aging crisis will peak in 2025–2030 when the ratio exceeds 14% and the Old Age Dependency Ratio reaches 20%, meaning that every five people in the labor force will support one person in old age. The 2010 World Population Project also states that China will join with other western countries such as Germany, Japan, and the UK to become a “super aging society”, meaning that those countries’ old age population will exceed 20% of their whole population. If we remove students of working age, unemployed young people, low-revenue employees, and retirees of working age from China’s labor force composition, the country already became a “deep aging society” in 2010 (

Hu and Yang 2012). In theory, before a country becomes an aging society, it should end its pay-as-you-go pension system and build a dual pension system with a combination of a national basic pension and an individual savings pension.

The current Basic Pension Insurance for Urban Employees (BPIUE) was initiated in 1991 and implemented nationwide in 1997 in accordance with the

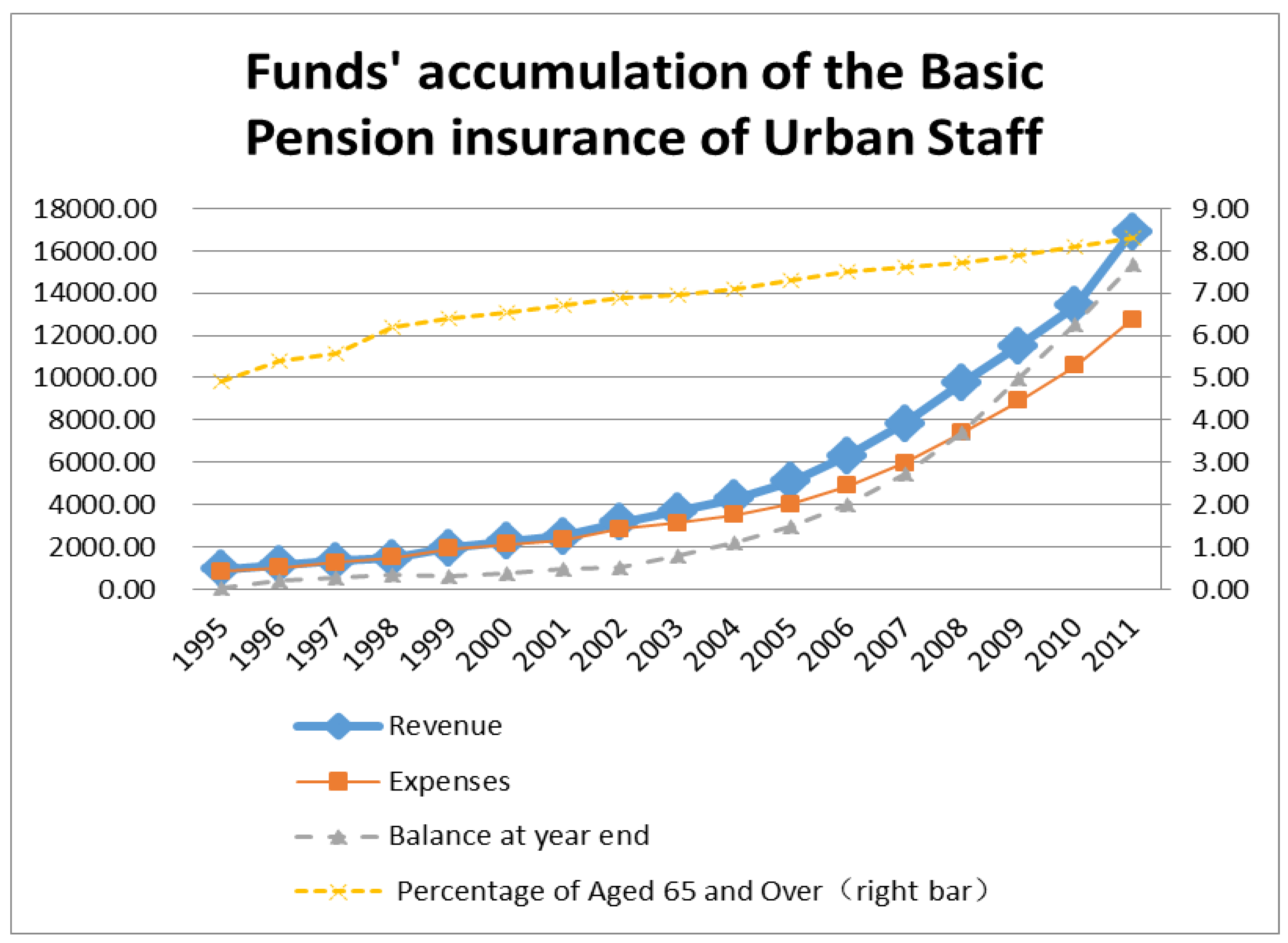

Decision on establishing a unified basic pension insurance system for enterprise employees by the State Council. The system required enterprises to contribute 20% of total wages to a social pooling account, and for employees, 8% of total wages were to be deposited into individual accounts. At the time, China was becoming an aging society. Between 2001 and 2011, the proportion of the population aged 65 years and over increased from 6.7% to 8.3%, and the internal alimony ratio of the BPIUE was only 3:1 (three contributing employees for one recipient). During the same time period, however, the annual cumulative balance of the pension fund rose from 9.8 billion yuan in 2001 to 1.5365 trillion yuan by the end of 2011 (

Figure 1)

3. Meanwhile, the financial subsidies from central and local governments increased from 40.8 trillion yuan in 2002 to 227.2 trillion yuan in 2011

4; as a result, funds in the individual accounts of employees were misappropriated to pay for others’ pensions, and by the end of 2011, the cumulative amount owed to the now empty accounts was more than 2 trillion yuan (

Zheng 2013, p. 2). The system no longer breaks even.

In this context, the following questions are raised:

Is the BPIUE a social insurance model? What is the nature of the individual pension savings accounts of employees?

During the course of China’s aging, how could the BPIUE funds continue to achieve an ever-increasing cumulative balance? Why does the plan still need government subsidies despite the ever-increasing cumulative balance? Where do the government subsidies go?

What is the impact of the China’s aging on the BPIUE, and can the BPIUE achieve sustainable development in China?

Beginning with these three questions and based on China’s social background, this paper reveals the policy mistakes of the BPIUE and the reasons for the fund balances, and then it explores the issue of sustainability for China’s pension system.

2. Theoretical Analysis: The Revenue-Expenditure Balance is the Essential Attribute of Pension Insurance

Insurance is risk savings plus a compensation contract, and it must maintain its own revenue-expenditure balance. In general, no individual or institution can guarantee insurance. Social insurance is different from social welfare (sometimes in the form of social assistance), and it should emphasize individual intergenerational transfers, not income re-distribution between groups orchestrated by the government using financial payments (

Feldstein 1999). Since Bismarck founded the insurance model in 1883 (

Kolmar 2007), social insurance has required employers to fulfill their obligation of contributions; employee contributions were later added. Contribution amounts from employees may be associated with their salaries; however, Germany has not yet established individual savings accounts for contributing employees. Social insurance plans emphasize contributions from both employers and employees, and contribution amounts are matched with the employee’s salary (

Feldstein 2005). The biggest difference between social insurance and social welfare is that social welfare represents “civil rights”, while social insurance represents “event rights” (

Feldstein 2005). Therefore, the UK’s first State Basic Pension Law requires a minimum of 45 years’ contribution to National Insurance to receive a full pension payment (the requirement for the number of contributing years is reduced for women in lieu of a family responsibility protection clause) (

Blake 2003). Under the UK’s 2012 Universal Credit, those with sufficient contributions to social insurance can directly apply for unemployment insurance and family benefits and receive payments for a longer period; those who have not fulfilled their social insurance payment obligations must be means-tested by the government and are subject to numerous restrictions regarding the amount of benefits and the eligibility period. This dichotomy shows that the UK’s social safety net adheres to basic social insurance-based principles, and social welfare and social assistance are secondary

5.

A successful social insurance scheme focuses on financial sustainability and requires certain actuarial calculations. It differs from commercial insurance by its compulsory nature and the financial support it receives from the government (

Kolmar 2007), making the results of social insurance similar to a redistribution of wealth. However, the government’s financial investment is a limited liability to ensure the functioning of social insurance rather than the acceptance of full responsibility for the entire scheme. Otherwise, the government would face extreme political and financial pressure that would ultimately result in an unsustainable social insurance scheme (

Casamatta et al. 2000;

Angrisani et al. 2012).

Initially, pensions entered the market as commercial insurance and as a disguised tool for personal and family savings (

Dokeland and Nordahl 2008). Pension systems distributed profits and market risks between customers and shareholders of a commercial insurance company on an actuarial basis while taking into consideration contribution amounts, asset allocation, benefit commitments, and profit sharing (

Dokeland and Nordahl 2008, p. 383). Social pension insurance that developed with reference to commercial insurance emphasizes mutual social assistance, risk sharing and other factors, and unlike commercial insurance, it is impossible for a social pension insurance system to solely emphasize contributions and benefit payments (

Sinn 2004;

Williamson and Deitelbaum 2005;

Feldstein 1999). Therefore, from the beginning of the establishment of social insurance systems, governments of various countries have chosen combination models that include pay-as-you-go (PAYG) and defined contributions. PAYG does not emphasize asset accumulation, and the system directly pays the current retired population with the current employees and employers’ contributions as payment transfer tools. As a separate fund, PAYG differs from the government transfer payment system that uses tax revenue (

Feldstein 1999).

Some analysts believe that social insurance can avoid the adverse selection, moral hazard, exclusion of low-income groups, and reduction of free-rider effects of commercial insurance (

Angrisani et al. 2012). Social insurance is most beneficial to the unemployed, low-income population and to the elderly who have no children to support them. As a result, social insurance plays a major role in the basic protection of an entire society based on shared risk and collective provisions and by favoring low-wage workers. For families who are unable or unwilling to have children due to family or other reasons, PAYG can offer the support that is provided by children in other families and offer some benefit from an investment in the human capital of the next generation. Therefore, PAYG is equivalent to maternity insurance (

Williamson and Deitelbaum 2005).

Feldstein (

1999) believes that adopting PAYG reflects political needs, that is, the government gets extra-budgetary windfall to reduce its financial burden, and the cost of the system is repaid with tax revenue from future generations. As a result, the government is constantly expanding coverage to maintain public support for the system (

Feldstein 1999 p. 10), which has become the government’s preferred choice for the establishment of social security.

However, there have been doubts raised about PAYG since its establishment. From the perspective of Samuelson economics, the premise for the sustainable development of a PAYG pension system is high population growth and a high growth rate of social productivity (

Samuelson 1958). Since the late 20th century, the PAYG system has faced the challenge of an aging population in countries all over the world and particularly in industrialized countries, where the total fertility rate is low and life expectancy continues to rise (

Cremer and Pestieau 2000;

Sanz and Velázquez 2007;

Williamson et al. 2012).

Since the 1980s–1990s, many countries have begun to adjust their PAYG systems. On one hand, PAYG and defined benefits (DB) are used as basic pensions to maintain low standards of living (

Williamson et al. 2012). On the other hand, countries have introduced mandatory individual savings accounts (DC model) as the second pillar of pensions (Pillar II). In the 1980s, Chile changed its DB model of PAYG to the DC model with cumulative individual balances (

Calvo and Williamson 2008). In the 1990s, Australia adopted the same measures. With prodding from the World Bank and other international organizations, developed countries with advanced-aging populations and developing countries that had just become aging societies have strengthened their individual savings account systems; as a result, the dual pension system structure has been implemented all over the world. The PAYG principle is preserved in the first pillar mostly through welfare and security (such as elderly, widow, and disability security payments in the US) and social assistance (such as Australia’s assistance payment), while fewer and fewer systems adhere to the German Bismarck social insurance model. The second pillar is individual savings. As noted by Peter F.

Drucker (

1999, p. 94), unanticipated situations include reduced coverage and decreased social insurance payments.

Individual savings accounts are personal property, and individual pension fund accounts have a greater need for specialized, market-oriented management and operations that preserve and increase the value of the accounts in the capital market (

Dokeland and Nordahl 2008). The government’s role is only to establish policy and adjust the rules on taxation and the related laws and regulations, and commercial institutions or social organizations administer the specific account management, fund management, and benefit payment activities. Some scholars regard this practice as personalization (

Williamson and Deitelbaum 2005) or marketization (

Fanti and Gori 2012), while others regard it as a public-private partnership or public governance by the government and commercial institutions (

Dong and Ye 2003).

In summary, the above theoretical analysis shows that the model and qualification determination for social insurance are different from social welfare, and social security is not merely a system of payment transfer with an emphasis on contributions, as is especially the case for pension insurance. Social security has a greater emphasis on long-term liability operations and the sustainability of sufficient contributions and other sources of funds for adequate cumulative balances. Social welfare programs do not need to consider the amount of revenue and expenditures, which are fully taken care of by the financial budget, whereas social pension insurance systems must strictly consider the sources of revenue and contributions and pursue a long-term balance of revenue and expenditures. Social insurance systems cannot shoulder high long-term levels of debt or become too large of a financial burden for the government. Meanwhile, within the PAYG pension system, the difference between pooling accounts and individual accounts with individual contributions also needs to be clarified. The PAYG system creates a public account and forms a quasi-public good; individual accounts emphasize individual contribution records and fund accumulation, and they create increased value through financial and capital markets, which reduces the need for mutual and intergenerational social support and strengthens the connection between individual responsibility and rights.

Therefore, social insurance and welfare should be divorced from PAYG and individual accounts, and although sometimes they can be integrated (e.g., in the welfare system of the UK and other European countries, social insurance contributions are a criterion for higher benefit payments, but those with no contributions can also be means-tested and receive some benefit if eligible), their boundaries should be maintained; otherwise, there will be a mismatch between responsibilities and rights, resulting in free-riding, fewer sources of funds, and difficulties in sustaining the system.

3. BPIUE Demonstrates the Transformation from Working Unit Security to Social Security

BPIUE demonstrates the transformation from working unit security to social security for the pensions of employees of Chinese enterprises. Since 1951, China’s rural areas have used the people’s commune system, and the basic livelihood of rural residents is protected by social mutual assistance (

Williamson and Deitelbaum 2005). Labor insurance implemented in cities and towns is based on a model of “contribution [3% of total wages] from working units supplemented by social mutual assistance”, upon which Williamson, Dong, Feldstein, Hussain, et al. have conducted a thorough and detailed analysis (

Hussain 1994;

Feldstein 1999;

Dong and Ye 2003;

Williamson and Deitelbaum 2005;

Hu and Yang 2012). During the Cultural Revolution from 1967–1976, social mutual assistance ceased to exist, pension insurance was entirely borne by working units, and pension payments were more than 80% of wages. Moreover, children could take their parents’ place and a permanent job (iron rice bowl) could be passed to the next generation. State-owned enterprises, the public sector, and government agencies implemented the same system so there was no two-tier pension system for workers at the time. However, the old industrial enterprises and state-owned enterprises bore a heavy burden of the welfare system (

Hussain 1994).

In 1985, China’s state-owned enterprises implemented the labor contract system, breaking the “iron rice bowl” system of lifetime employment, and urban workers began to consider social risks such as employment, unemployment, illness, and family difficulties (

Hussain 1994;

Williamson and Deitelbaum 2005). In 1991, the State Council proposed the idea of social pension insurance for employees

6, which ended the history of work unit insurance and adopted the social pooling and PAYG model. In 1995, the State Council stressed that based on the PAYG model and considering the aging of the population, workers’ individual savings accounts should be established, and enterprise contributions of 3% of wages should be deposited into workers’ individual accounts

7. The funds in individual accounts could not be withdrawn before retirement unless the workers had settled abroad or died.

However, it has been difficult to decentralize the decision-making on how to operate the two accounts to local governments to shift the pooling responsibility. The migration of insured workers and the transfer of social insurance to other municipal governments have been difficult to manage. It was not until 1997 that the State Council required the establishment of a social pension insurance system that “combined social pooling and individual accounts” (in other words, a combination of DB and DC) for urban employees nationwide

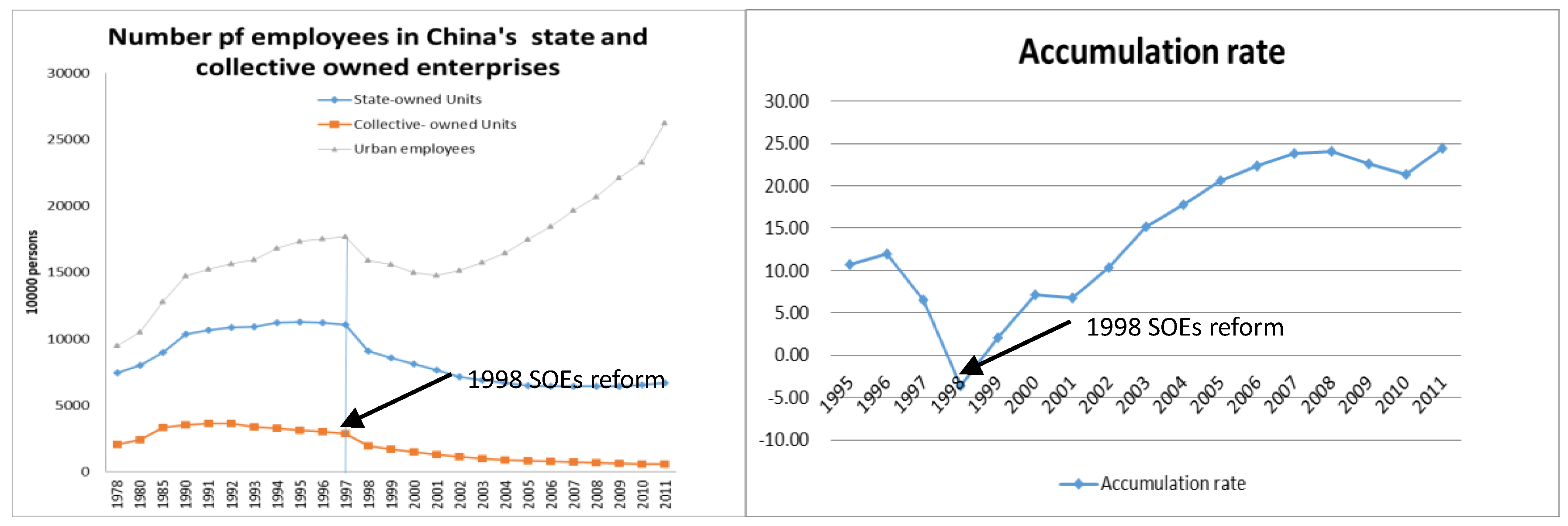

8, and according to Premier Zhu Rongji, this system was the matching measure for the reform of state-owned enterprises. During the reform of state-owned enterprises during 1997 and 1998, more than 20 million workers were laid off

9, and because most of them had retired early, the average retirement age was only 47

10. Prior to being laid off, the workers did not have any pension accumulation, and because of the lack of applicable laws and regulations and appropriate budgetary arrangements by the central government, local governments had to misappropriate funds in employees’ savings accounts to pay for the pensions of these “middle-aged” workers who had retired early, which began the problem of the empty individual accounts. However, even with the misappropriations, the funds were not sufficient to meet the demand for pension payments, so in the same year the central government transferred payments to local governments of approximately 10 billion yuan.

The 2005 State Council document

11 directed that all of the employee contributions of 3% of wages should be deposited into social pooling accounts, and from that moment, enterprises no longer contributed to employees’ individual pension accounts. Retired workers became the responsibility of community management, and social insurance institutions were responsible for pension payments, which were issued by a bank. The traditional work unit security was transformed into social security under social management.

4. BPIUE Has Been Distorted Since 1998

4.1. Funds in Individual Accounts Were Misappropriated to Pay for Workers of State-Owned Enterprises with Early Retirement

The 1997 Urban Employees’ Pension reform was the most important one in China’s pension history. Two systems and accounts were established after the reform. The employers pay the social pooling account which is a Pay-as-you-go system and the employees pay their individual accounts as individual savings. And the unemployed and rural area people were taken out of this system to establish another pension system which is semi means-tested and semi tax financed. This paper focuses on the urban employees’ pension system.

The original intention of the 1997 reforms was to establish a model that combined SP (Social pooling) and IA (Individual Accounts), which are DB and DC (

Hu and Yang 2012). It not only preserved the basic protections, transfer payments, and risk sharing of the PAYG system but also established individual savings accounts to respond to the impact of an aging population. However, the aforementioned State Council document was not ratified as law and only took effect as an administrative law in China. So far, there is still no judicial system for employees’ individual pension accounts, and there are no investment strategies or pension markets. Accounts and funds are managed by social insurance agencies of the local governments, and there are no unified national resident files. Municipal governments have set up pension insurance agencies that manage both social pooling funds and funds in individual accounts, and the balance after pension payments is turned over to the fiscal accounts of the government for the purchase of government savings bonds.

To analyze the accumulation rate at year end of the BPIUE, assuming that

represents the annual fund revenue,

represents the annual fund expenditures,

represents the annual fund balance at year end, and

, then the annual fund’s balance rate

is:

From 1996–1998, the reform of state-owned enterprises was implemented in China, and by the end of 1998, more than 20 million workers were laid off and most of them retired early, at an average age of only 47. These workers did not have any pension accumulation, but the length of their service in the state-owned enterprises was recognized by the policy of the State Council (deemed-as contributions). However, there was no budget for pension payments, so the local governments had to misappropriate funds from individual accounts. In addition, there was no legal impediment to this action because the SP and IA accounts had been mixed. From 1995–1998, the accumulation rate of the BPIUE continued to decline (

Figure 2) and began to increase since 1998 to now

12.

4.2. Unbalanced Regional Burden and Pension Fund Balances

For the BPIUE, the social pooling account is managed by municipal governments, and 10% is controlled by provincial governments as adjustment funds. When workers migrate to different areas, they often encounter resistance from the local government in carrying over the pension insurance relationship. Local governments are required to maintain their own balances of revenue and expenditures, and the State Council has compromised to allow local governments to retain 8% out of the 20% enterprise contribution, while the worker must carry the remaining 12% (

Dong and Ye 2003).

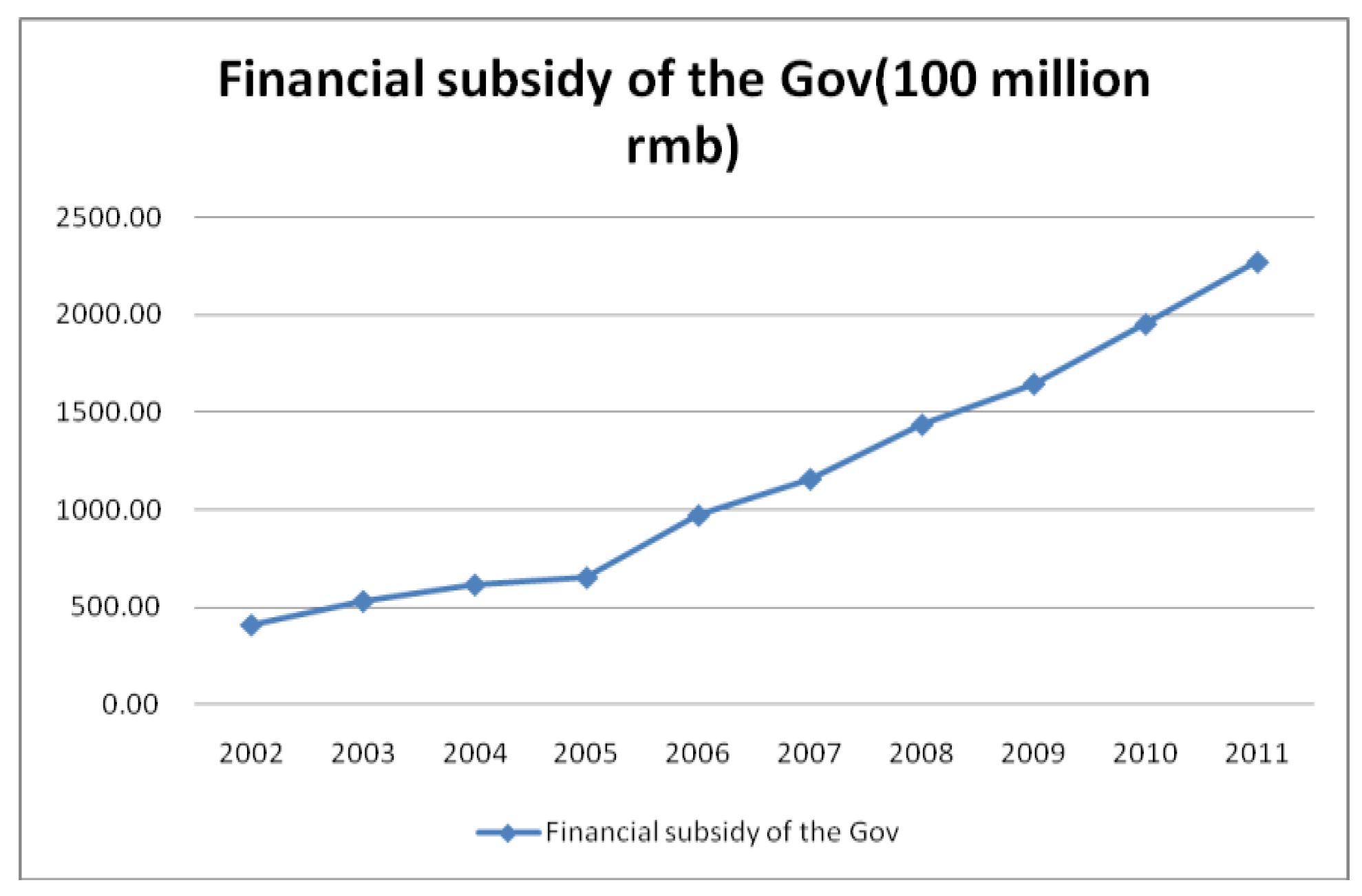

Meanwhile, in the old industrial bases of northeast and northwest China, there are a large number of laid-off workers and workers in early retirement after the implementation of the reforms of the state-owned enterprises, and the amount of the pension payments is huge; so far, there are 14 provinces that have exhausted the 20% enterprise contributions and the 8% employee contributions, yet they still cannot meet the demand to pay the pensions of the retired workers. As a result, payment transfers from the central government to local governments have continued to increase, and government financial subsidies have increased to 220 billion yuan in 2012 from 40 billion yuan in 2001 which is shown in

Figure 3.

At the same time, the economically developed areas in the southeast coastal region have attracted a large amount of rural surplus labor, so these local governments have positive balances in their BPIUE funds. Currently, 17 provinces and municipalities are able to meet the payment demands and have accumulated balances before exhausting the 28% contribution. Guangdong Provincial Government can meet the payment demands with only 20% of the contribution. By the end of 2012, the cumulative balance of the BPIUE exceeded 2.3 trillion yuan.

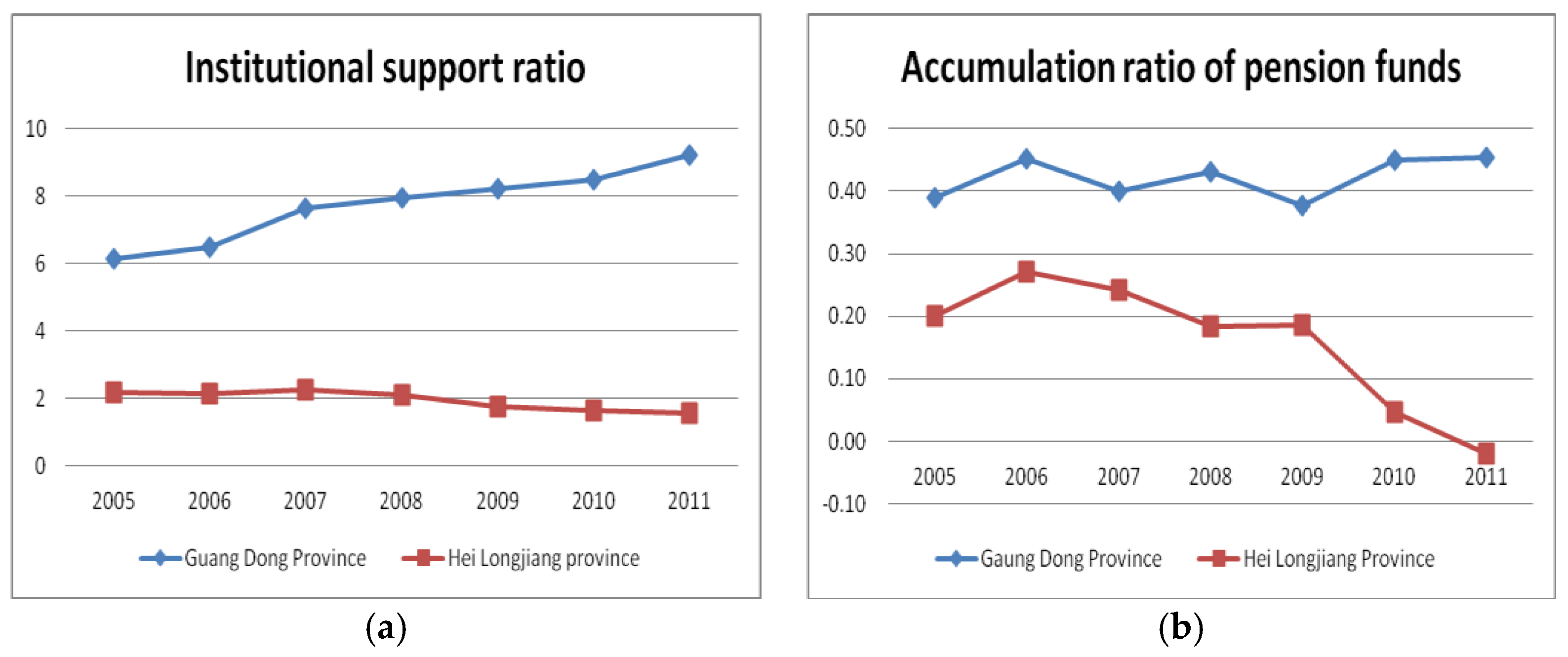

Using the examples of Guangdong and Heilongjiang provinces to examine regional differences, the results show that in 2011 the proportion of the elderly population over age 65 was 8% and 6%, respectively. Guangdong Province has been a destination for the migration of rural labor, while Heilongjiang Province is an old industrial base with many state-owned enterprises from the planned economy period. Therefore, Heilongjiang Province now has many retired older workers, with less inflow of rural labor. We compared the distribution of workers enrolled in the BPIUE and the ratio of support within the system for the two provinces in 2012.

is defined as the number of workers enrolled and who contributed to the BPIUE in province

during year

,

is defined as the number of workers who receive a pension in province

during year

, and the ratio of support within the system is:

The data show (

Figure 4) that the ratio of support within the system in Guangdong increased from 6:1 in 2005 to 9:1 of 2011, while the ratio of support in Heilongjiang Province declined. In addition, since 2005, the balance in Guangdong Province has increased significantly and is currently close to 50%, while the balance in Heilongjiang Province is negative.

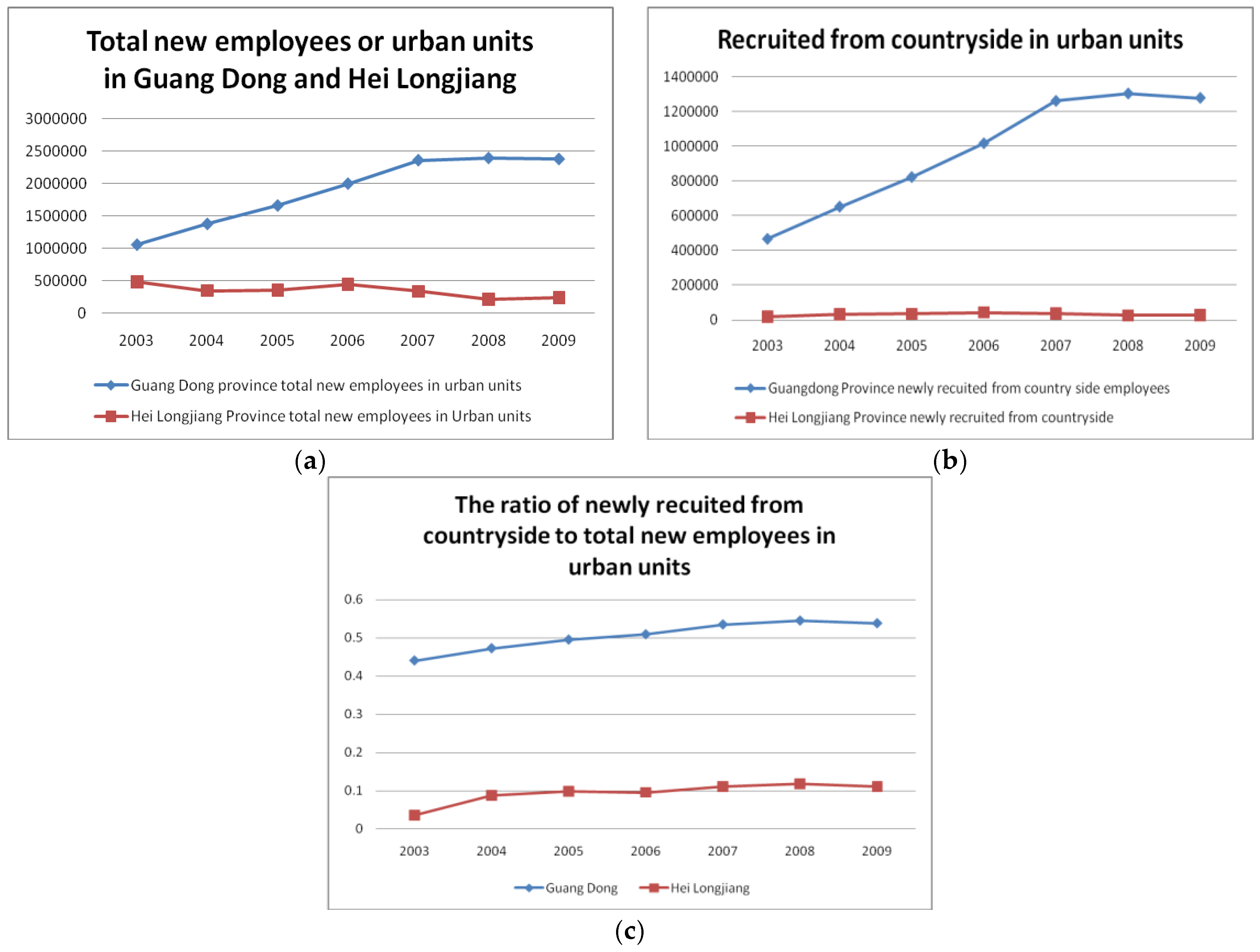

The differences in the balances are also reflected by new employees and their sources in urban work units in Guangdong Province and Heilongjiang Province over the years, as shown in

Figure 5a–c.

Figure 5a shows the number of new employees in urban work units in Heilongjiang Province and Guangdong Province each year; the number of new employees in Guangdong Province is higher, with approximately 2.5 million in 2011, while the number of new employees in Heilongjiang is less than 50,000.

Figure 5b shows that the number of workers who migrated from the countryside to the city in Guangdong is more than 1.2 million per year, while the figure is less than 50,000 in Heilongjiang.

Figure 5c shows that the reason for such a high number of new employees in Guangdong Province is that the province attracts a large amount of rural labor (from 2008–2011, more than 50% of the new labor in urban work units was from the countryside). The influx of rural labor into Guangdong Province also contributes to the balance in the province’s social insurance fund by allowing the province to maintain a higher level of fund contributions to help cope with the impact of aging. However, in some provinces, such as Heilongjiang Province, there is no influx of rural labor and the regions are old industrial bases with more retired workers; inevitably, the impact of aging is larger, so that in Heilongjiang Province, the BPIUE has been unable to meet the demands for payment using revenue from the same year since 2011. (

Figure 4b).

4.3. Analysis of the Cumulative Balances of the BPIUE

China became an aging society in 2005, and the proportion of the elderly population age 65 or over is now more than 7% of the total population; therefore, the pressure for pension payments is increasing. There have been mounting demands to stop the misappropriation of funds in workers’ individual accounts and to increase their value through investment, and the 2005 State Council document on pension reform specified that the entire 20% enterprise contribution should be deposited into social pooling accounts. In terms of deposits, the social pooling accounts and the individual accounts are separated. Since 2006, considering only contributions to pooling accounts and not contributions to individual accounts, multiplying

at the end of year by 20/28 should accurately reflect the revenue of the pooling fund. The annual balance of the following year is

:

If contributions to individual accounts are excluded from fund revenue, then the portions of the individual accounts should likewise be excluded from fund expenditures and balances; therefore, is reduced accordingly.

However, according to the provisions of the 2005 State Council document, the BPIUE pays for the basic pension, including the basic pension of the social pooling accounts (calculated according to the average wage of the local community, the individual contribution base, and the number of years of contribution) and the pensions of the individual accounts. The pensions for the individual accounts equal the balance in the individual account divided by a specified number of months; according to the fifth census in 2000, the average life expectancy in China is 71.4 years, so people retiring at age 60 will receive a pension for 139 months, and people who survive beyond 139 months will still receive pension payments. This analysis shows that the BPIUE funds in the two accounts are mixed, the BPIUE is still a PAYG system with a defined benefit plan, and there is no separate investment or management for individual accounts.

In the formula, accumulation represents the cumulative balance of individual accounts at the time of each employee’s retirement, and m is the number of months of pension payments. m is determined according to actuarial calculations of life expectancy such that the older the retirement age is, the smaller m is, and the amount of the monthly pension payment is therefore higher.

Due to the continuous depreciation of the funds in individual accounts, the pension replacement ratio of the BPIUE has decreased from the initial 58% to below 50%, and enterprise workers are increasingly discontent. Beginning in 2006, the central government promised an increase of 10% per year in the BPIUE, and by 2012, the per capita monthly pension reached 1721 yuan.

To summarize the above analysis, the cumulative balance of the BPIUE is shown in

Table 1 (1) the total accumulated amount of the two mixed accounts increased from 1.09 trillion yuan in 2007 to 1.54 trillion in 2011; (2) as of 2011, the accumulated amount in individual accounts was approximately 2.4859 trillion yuan, of which 270.3 billion yuan was commissioned to the National Social Security Fund Council for investment and management and 2.2156 trillion yuan was the amount missing from the empty pension accounts. Even if 1.53 trillion yuan was used to re-fund the empty accounts, there would still be a shortfall of 679 billion yuan; (3) in 2011, the financial subsidies were 220 billion yuan, and if the subsidies are excluded, the funding inadequacy reached 899 billion yuan.

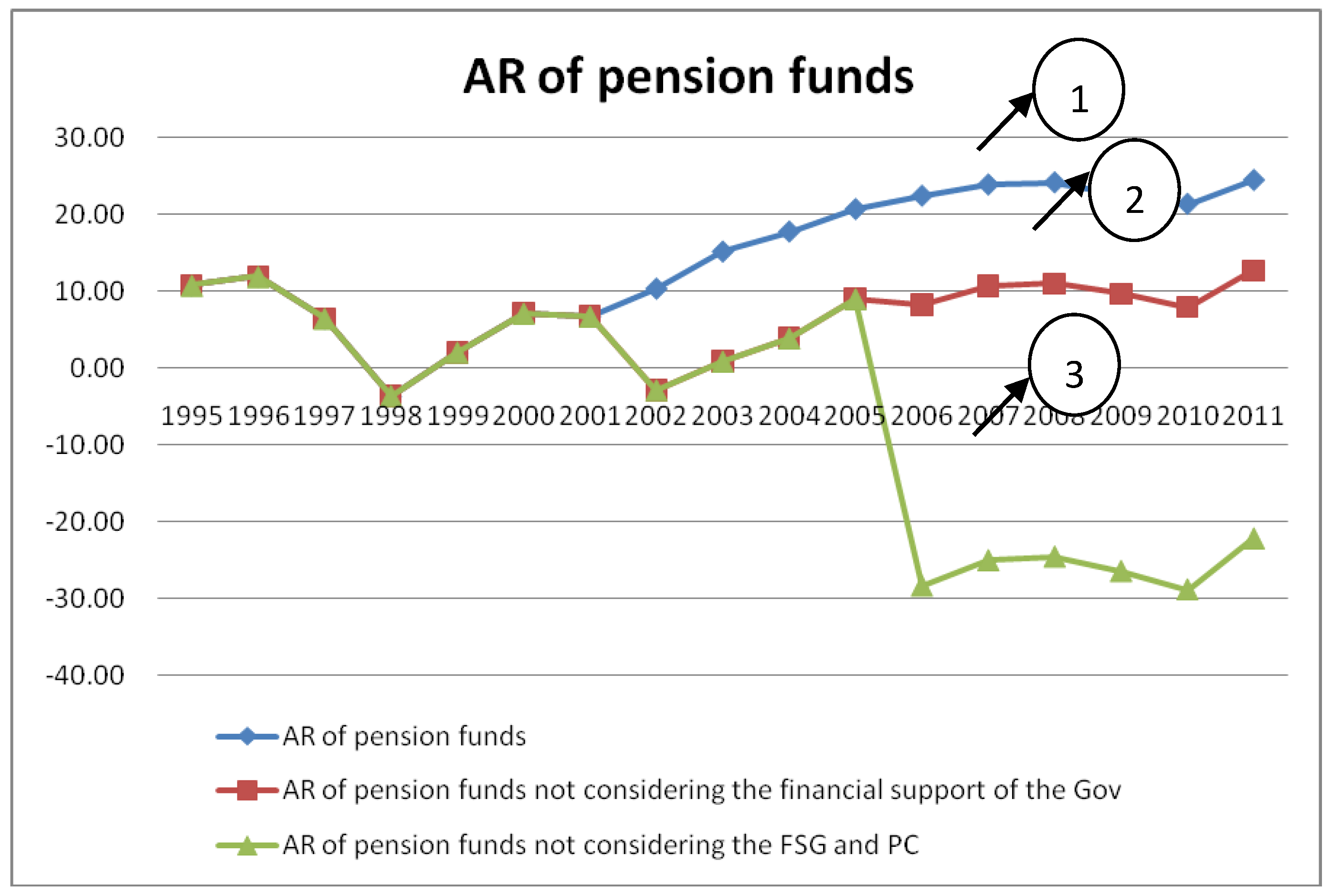

If the differences between the pooling accounts and the individual accounts are considered, and individual contributions and government subsidies are excluded from the calculation of the balance for the pooling funds, then the entire balance of the pooling funds for social pension insurance become even worse, as shown in

Figure 6.

In

Figure 6, Graph 1 represents the balance rate calculated in accordance with the statistics, and the current balances rate is more than 20%, but Graph 2 shows that beginning in 2003, the government financial subsidies are excluded from fund revenue (Financial support of the government). As a result, the balance rate since 2003 is only about half of Graph 1, and the balance rate for 2011 is only 10% of Graph 1. If the contributions to individual accounts and pooling accounts are strictly separated, that is, individual contributions are excluded from the annual fund revenue since 2006, then the balance rate of the entire pension fund is negative (as shown in Graph 3). This difference indicates that if the government subsidies and the contributions to individual accounts are excluded, the annual balance of China’s basic pension insurance fund will not be very high, and the cumulative balance rate of the entire fund will not increase as the population continues to age.

Figure 6 shows that the IA pensions in China are different from the model for individual savings and pension funds adopted in Chile, Australia, and for the U.S. 401 (k) system. So far, China’s concept is still not clear, and the line between a pension tax in disguise and nominal pension savings is not defined. Social pooling and individual accounts are mixed, and the BPIUE maintains PAYG characteristics.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}