Rise and Fall of the Materiality Matrix: Lessons from a Missed Takeoff

Abstract

:1. Introduction

“What approaches to MM adoption emerge over time and why?”

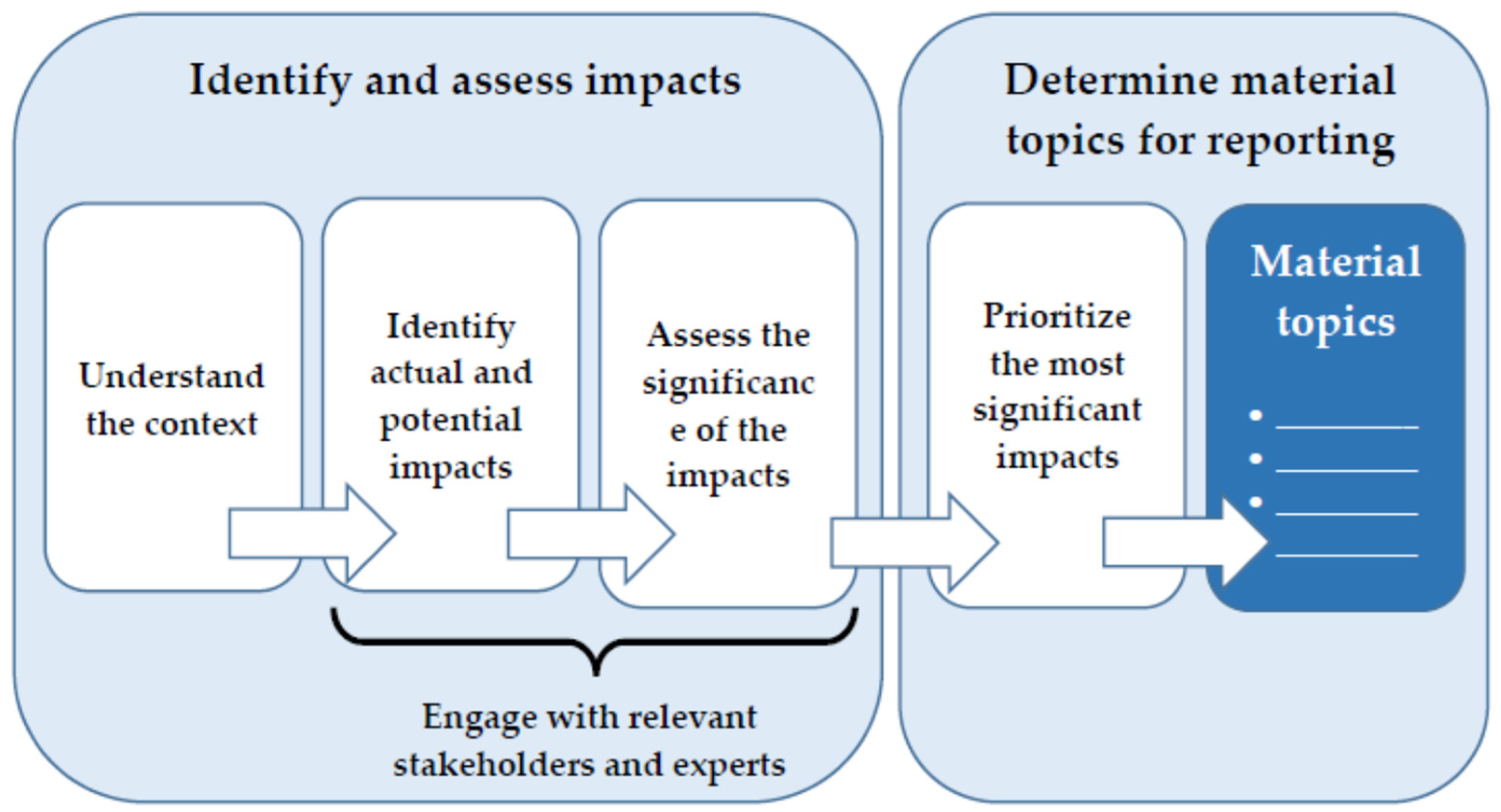

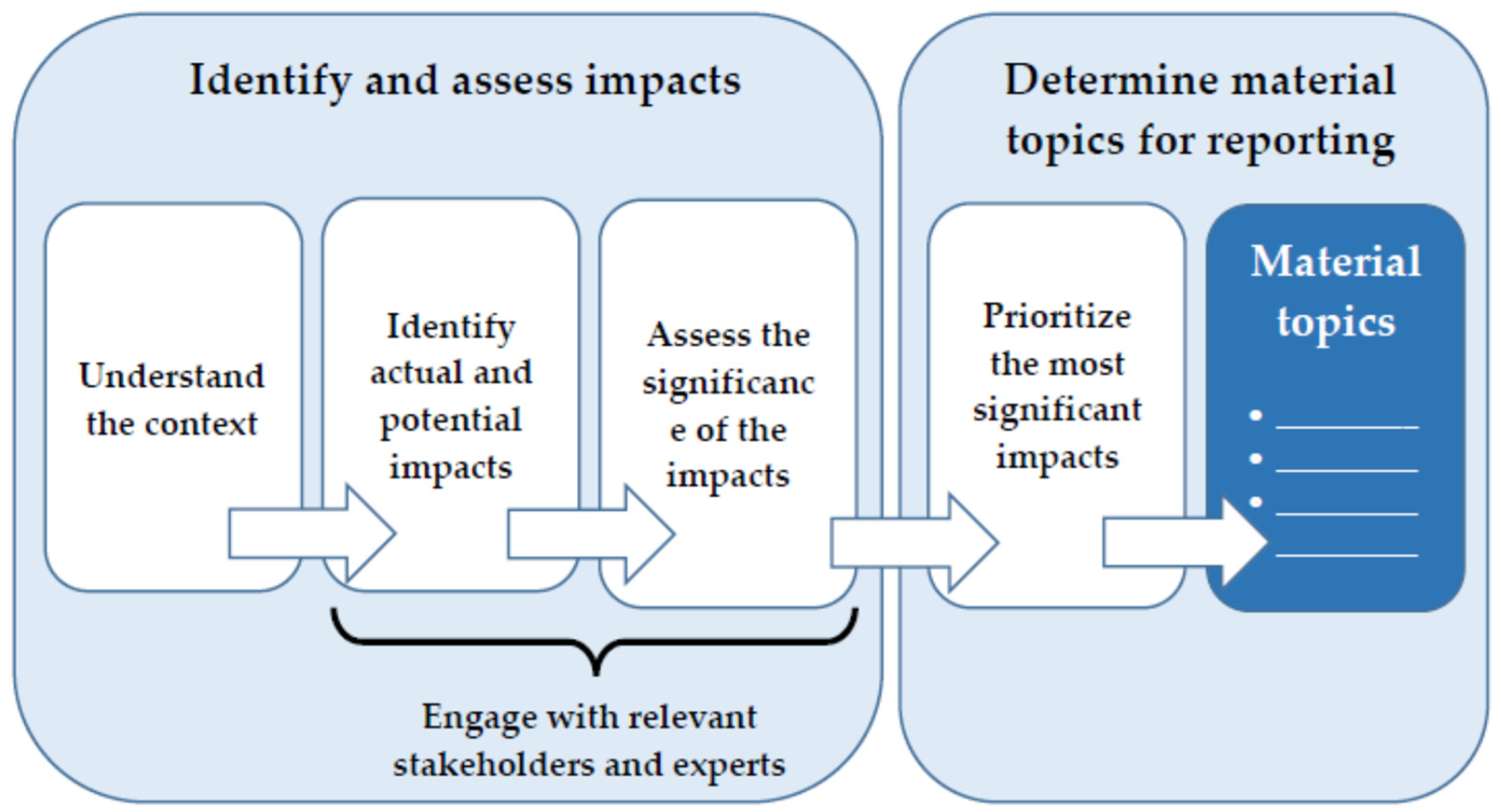

2. Background: The Materiality Matrix in the Evolution of Standard Setters’ Approaches to Materiality Analysis

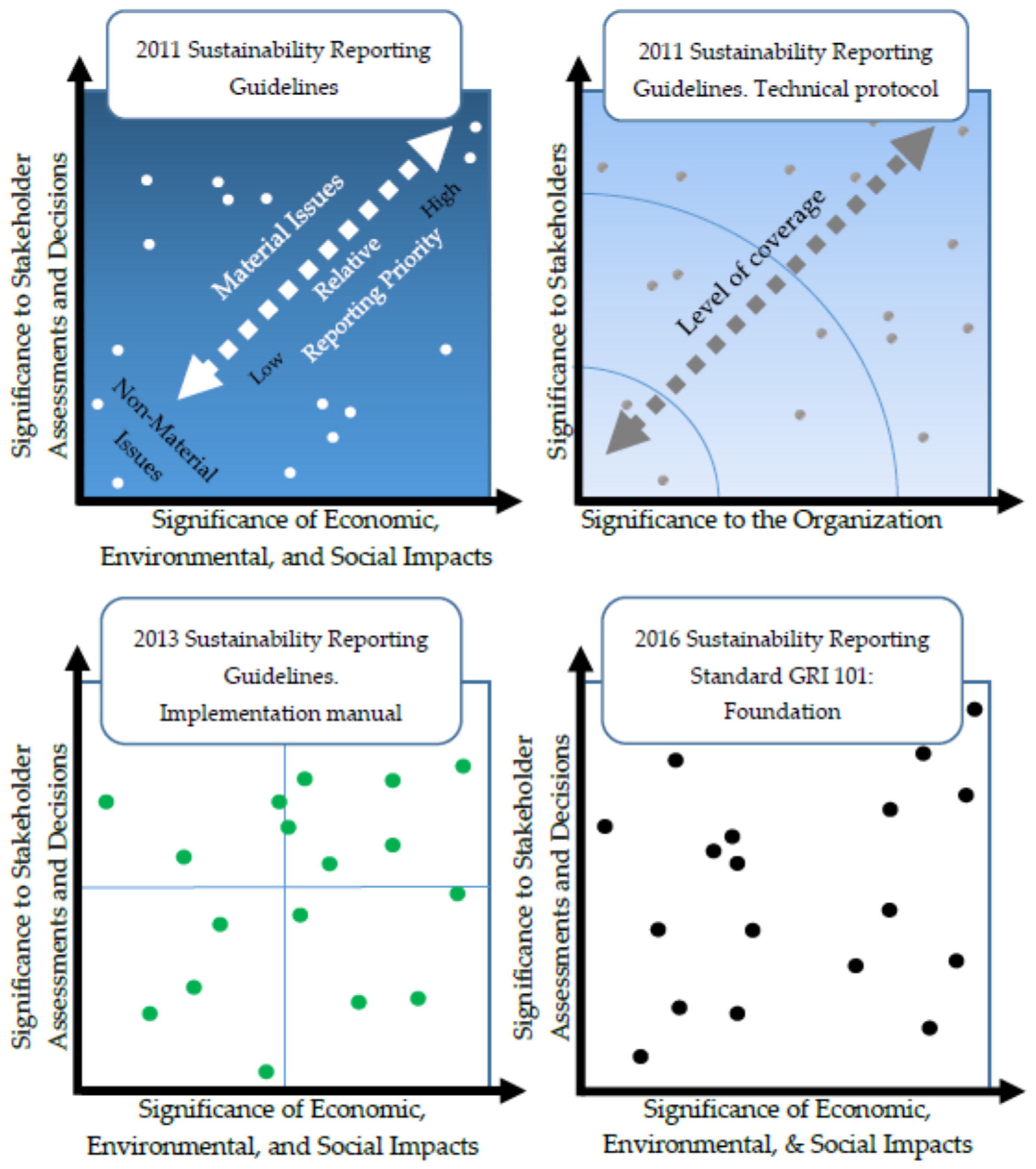

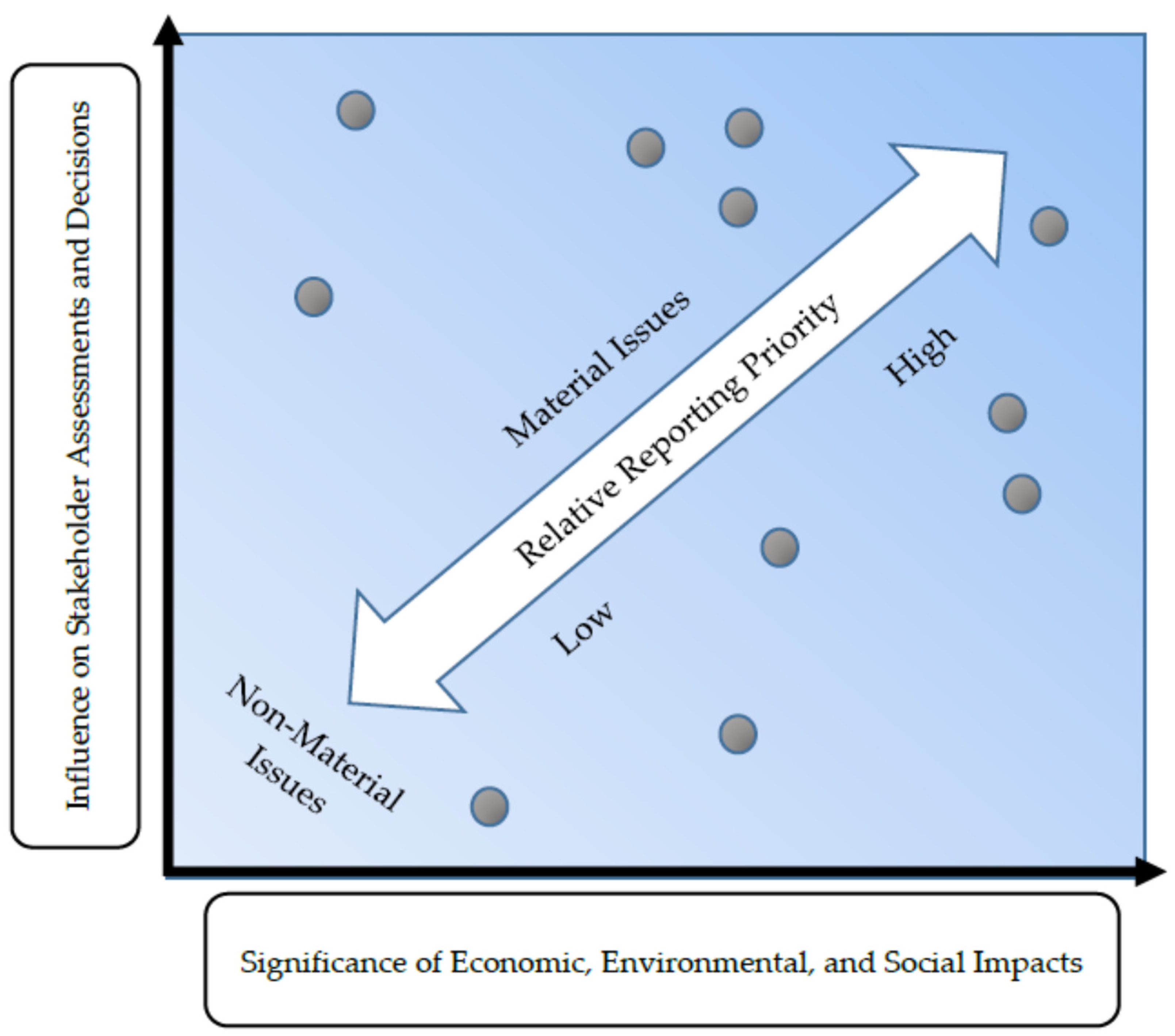

2.1. Origins and Spread of the Materiality Matrix

2.2. Decline of the Materiality Matrix in the GRI’s Approach

3. From the Literature to the Research Question

- (i)

- (ii)

- Materials provided to experiment participants (Backof et al. 2020);

- (iii)

- Data scoring (Gerwanski et al. 2019; Mio et al. 2020; Farooq et al. 2021; Sepúlveda-Alzate et al. 2021);

- (iv)

- Variable and index operationalization (De Cristofaro and Gulluscio 2019; Slacik and Greiling 2019; Ortar 2020; Ruiz-Lozano et al. 2021; Tibiletti et al. 2021).

- MM typically describes firms’ orientation to sustainability more accurately than the GRI content index (Pizzi et al. 2020);

- MM allows the easy identification of most material issues (Ortar 2020);

- MM both visualizes the overall materiality assessment and helps to consider the baseline SDGs-related responsibilities (Costa et al. 2022);

- MM explains the dynamics of sustainability-oriented value creation and business models (Geldres-Weiss et al. 2021);

- MM creates a multi-stakeholder context that fosters virtuous paths of co-creation of value and sustainable society (Formisano et al. 2017);

- As it is instantly and visually observable, MM is a powerful mechanism of communication (Bavagnoli et al. 2014);

- MM is an effective model for assessing the impact of issues using different sizes for different bulks (Bavagnoli et al. 2014);

- MM provides summaries (Farooq and de Villiers 2019) and preliminary maps (Morrós 2017);

- MM shows the same communication advantages of graphs (Gelmini et al. 2015) outlined by Beattie and Jones (2002), namely, to capture attention, to allow direct data acquisition, to simplify data retrieval, and to enliven data presentation;

- MM is a tool that simplifies the inherent complexity of assessing material sustainability issues, stakeholder engagement, and the societal pursuit of sustainable development (Adams et al. 2021).

- MM design requires a lot of time (Aureli et al. 2020) and energy (Taubken and Feld 2018).

- Along the lines of Beattie and Jones (2002), Gelmini et al. (2015) stress that MM creates risks of graphical infidelity, namely selectivity (e.g., x-axis re-labelled “Potential Impact on Our Business”), measurement distortion (e.g., an item’s size being unrepresentative of its relevance), and presentation enhancement (e.g., an item’s emphatization through colours).

- Among the several x-axis labels chosen (Jones et al. 2016a), companies sometimes substitute the GRI’s label for “success to the organisation” and similar labels. This inward focus involves the risk of omitting impacts with little effect on the organisations’ success (Guix et al. 2019), regardless of how much they relate to a particular business plan or strategy (McElroy 2011).

- The lack of detailed guidance makes the y-axis the more complex axis (Bellantuono et al. 2016), since it merges divergent stakeholders’ voices rather than precisely portraying converging instances and conflicting interests (Puroila and Mäkelä 2019). This compromise, although it could marginalize certain stakeholders, provides an illusory consensus among stakeholders that implies a weak comparability between reports (Reimsbach et al. 2020).

- Sometimes companies report only on issues that score highly on both axes (top-right quadrant), essentially omitting significant issues that are relevant to stakeholders (top-left quadrant) (Guix et al. 2019);

- The heterogeneous design of MM (e.g., axes and quadrants) allows companies to manipulate the data to suit their needs (Guix et al. 2018);

- Sometimes a lack of correlation between MM and the report’s content occurs (Sepúlveda-Alzate et al. 2021).

- Companies do not usually disclose background information on how exactly the matrix was constructed, e.g., how issues are ranked and the threshold set (Puroila and Mäkelä 2019).

- Since most of the reports give no clue as to how the material issues were placed in the matrix, it seems that “that there is a focus on moving dots around a matrix and not on the underlying drivers of sustainability performance” (Cohen 2014).

- MM “effectiveness is somewhat limited since it doesn’t show the priorities of different groups, industrial benchmarks used by peers and investors to compare performance, characteristics such as “innovation” that represent resilience and adaptability to changing times”, industry key sustainability performance indicators as well as does not “provide for future disruptive events or changes in stakeholder priorities that may change the mix” (Morrós 2017, p. 115).

What approaches to MM adoption emerged over time and why?

4. Research Design and Methodology

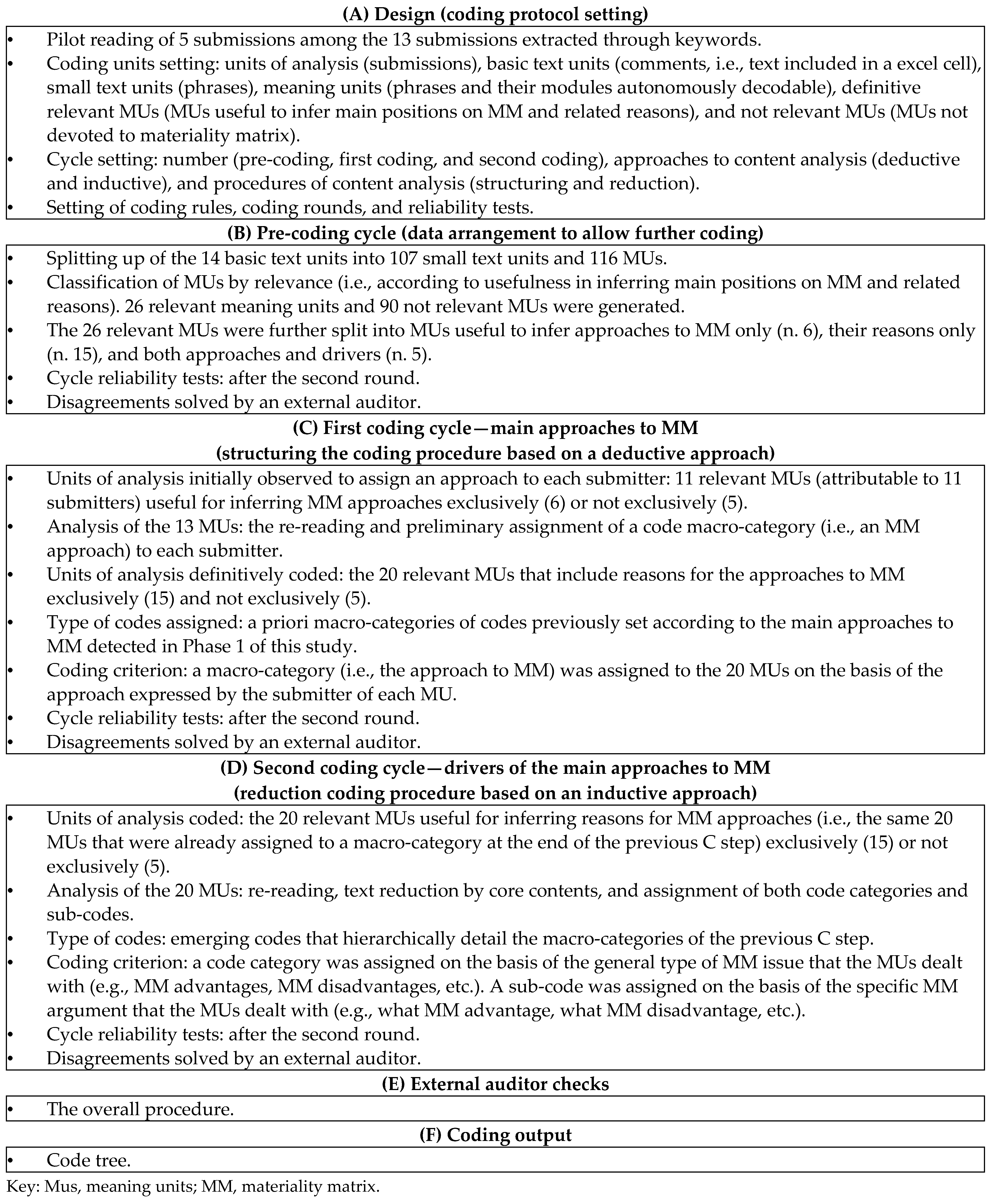

4.1. Research Design

4.2. Phase 1: Materials and Methods

4.3. Phase 2: Materials and Methods

5. Results

5.1. Results of Phase 1 (Materiality Matrix Adoption): Evolution, Approaches, and GRI Compliance

- The evolution of MM adoption and non-adoption;

- Approaches to MM publication;

- MM adoption and GRI-compliant association.

- (i)

- Overall, the majority of the companies (52 companies, i.e., 86.67% of the sample) publish an MM at least once over the period 2014–2020 in their NFRs.

- (ii)

- The yearly percentage of companies that present an MM increases over time and ranged between 63.33% in 2014 and 78.33% in 2017 (Figure 5). Hence, MM adoption never reached 100% because companies that ignored the visual persisted over the period and even recovered in 2019 and 2020.

- (A)

- In favour of MM adoption, i.e., cases of both steady adoption over the period and trends revealing a gradual or clear preference towards MM adoption;

- (B)

- Against MM adoption, i.e., cases of both steady non-adoption over the period and trends revealing MM abandonment or puzzling behaviours.

5.2. Results of Phase 2 (Opinions on Materiality Matrix Adoption): Content Analysis of GRI Stakeholders’ Comments

- Explicitly against MM removal (i.e., concerns about the consequences of MM removal; MM abandonment without a clear alternative creates negative consequences);

- Explicitly in favour of retaining MM (i.e., requests to include MM in the new standard; MM must be retained; a two-dimensional matrix is preferable; the standard should mention that companies can publish MMs);

- Tacitly in favour of MM (i.e., MM can be cited within the statement of GRI use).

- Explicitly in favour of MM removal (i.e., MM removal is a welcome change; the elimination of both double criteria and MM is appreciated; the move away from the matrix approach is supported; MM is no longer needed).

6. Discussion and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | In 2017, some respondents to the IIRC consultation on a revised International <IR> Framework mentioned or implied an expectation regarding the inclusion of an MM (IIRC 2017, p. 7). IIRC replied that MM “is more commonly associated with sustainability reports than with the Framework’s concept of materiality” (Ibidem). |

References

- AccountAbility. 2006. The Materiality Report. Aligning Strategy, Performance and Reporting. Available online: www.accountability.org/about-us/publications/materiality.html (accessed on 5 October 2022).

- Adams, Carol A., Abdullah Alhamood, Xinwu He, Jie Tian, Le Wang, and Yi Wang. 2021. The Double-Materiality Concept. Application and Issues. Project Report. Global Reporting Initiative. Available online: https://dro.dur.ac.uk/33139/1/33139.pdf (accessed on 28 February 2022).

- Aureli, Selena, Mara Del Baldo, Rosa Lombardi, and Fabio Nappo. 2020. Nonfinancial reporting regulation and challenges in sustainability disclosure and corporate governance practices. Business Strategy and the Environment 29: 2392–403. [Google Scholar] [CrossRef]

- Backof, Ann G., Eric M. Negangard, and Jennifer Winchel. 2020. CSR Restatements and the Contagion Effect: An Experimental Investigation of Issue Materiality and Intent. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3388115 (accessed on 18 June 2022).

- Bavagnoli, Francesco, Maurizio Comoli, Lorenzo Gelmini, and Patrizia Riva. 2014. An open question in the integrated reporting: Materiality or conciseness? SSRN Electronic, September 18. [Google Scholar] [CrossRef]

- Beattie, Vivien, and Michael J. Jones. 2002. Measurement distortion of graphs in corporate reports: An experimental study. Accounting, Auditing and Accountability Journal 15: 546–64. [Google Scholar] [CrossRef] [Green Version]

- Bellandi, Francesco. 2017. Materiality in Financial Reporting: An Integrative Perspective. Bingley: Emerald Publishing Limited. [Google Scholar]

- Bellantuono, Nicola, Pierpaolo Pontrandolfo, and Barbara Scozzi. 2016. Capturing the stakeholders’ view in sustainability reporting: A novel approach. Sustainability 8: 379. [Google Scholar] [CrossRef] [Green Version]

- Bernstein, Leopold A. 1967. The concept of materiality. The Accounting Review 42: 86–95. [Google Scholar]

- Calabrese, Armando, Roberta Costa, Nathan Levialdi Ghiron, and Tamara Menichini. 2019. Materiality analysis in sustainability reporting: A tool for directing corporate sustainability towards emerging economic, environmental and social opportunities. Technological and Economic Development of Economy 25: 1016–38. [Google Scholar] [CrossRef] [Green Version]

- Campbell, David. 2017. Content analysis. In The Routledge Companion to Qualitative Accounting Research Methods. Edited by Zahirul Hoque, Lee D. Parker, Mark A. Covaleski and Kathryn Haynes. New York: Routledge, pp. 354–71. [Google Scholar]

- Campra, Maura, Paolo Esposito, and Rosa Lombardi. 2020. The engagement of stakeholders in nonfinancial reporting: New information-pressure, stimuli, inertia, under short-termism in the banking industry. Corporate Social Responsibility and Environmental Management 27: 1436–44. [Google Scholar] [CrossRef]

- Cho, Charles H., Giovanna Michelon, and Dennis M. Patten. 2012a. Enhancement and obfuscation through the use of graphs in sustainability reports. Sustainability Accounting, Management and Policy Journal 3: 74–88. [Google Scholar] [CrossRef]

- Cho, Charles H., Giovanna Michelon, and Dennis M. Patten. 2012b. Impression management in sustainability reports: An empirical investigation of the use of graphs. Accounting and the Public Interest 12: 16–37. [Google Scholar] [CrossRef]

- Cohen, Elaine. 2014. Why the Materiality Matrix is Useless. CSR Reporting. Available online: http://csr-reporting.blogspot.com/2014/12/why-materiality-matrix-is-useless.html (accessed on 22 February 2022).

- Cooper, Stuart, and Giovanna Michelon. 2022. Conceptions of materiality in sustainability reporting frameworks: Commonalities, differences and possibilities. In Handbook of Accounting and Sustainability. Edited by Carol A. Adams. Cheltenham: Edward Elgar Publishing, pp. 44–66. [Google Scholar]

- Costa, Roberta, Tamara Menichini, and Gennaro Salierno. 2022. Do SDGs Really Matter for Business? Using GRI Sustainability Reporting to Answer the Question. European Journal of Sustainable Development 11: 113–13. [Google Scholar] [CrossRef]

- Creswell, John W. 2014. Research Design. Qualitative, Quantitative, and Mixed Methods Approaches, 4th ed. New York: SAGE. [Google Scholar]

- Cȕre, Tuvana, Emel Esen, and Arzu Özsözgün Çalişkan. 2020. The role of graphs in environmental disclosures: An empirical evidence from Turkey. Eurasian Business and Economics Journal 22: 12–27. [Google Scholar] [CrossRef]

- Damian, Maria Ionela, Sorana Mihaela Manoiu, Carmen Giorgiana Bonaci, and Jiři Strouhal. 2014. Bearer plants: Stakeholders’ view on the appropriate measurement model. Accounting and Management Information Systems 13: 719–38. [Google Scholar]

- De Cristofaro, Tiziana. 2022. Materiality. In Encyclopedia of Sustainable Management. Edited by Samuel O. Idowu, René Schmidpeter, Nicholas Capaldi, Liangrong Zu, Mara Del Baldo and Rute Abreu. Cham: Springer, pp. 1–10. [Google Scholar] [CrossRef]

- De Cristofaro, Tiziana, and Carmela Gulluscio. 2019. Integrated Reporting and Materiality Process Disclosure in European Sustainability Oriented Companies. In Integrated Reporting: Antecedents, Perspectives/Outlooks, for Organizations and Stakeholders. Edited by Samuel O. Idowu and Mara Del Baldo. Cham: Springer International Publishing, pp. 267–90. [Google Scholar]

- Eccles, Robert G., Michael P. Krzus, and Liv A. Watson. 2012. Integrated Reporting Requires Integrated Assurance in Effective Auditing for Corporates: Key Developments in Practice and Procedures. Edited by Joe Oringel. London: Bloomsbury Information Ltd., pp. 161–78. [Google Scholar]

- Eccles, Robert G., Michael P. Krzus, and Simon Ribot. 2015. The Integrated Reporting Movement. Meaning, Momentum, Motives, and Materiality. Hoboken: John Wiley and Sons. [Google Scholar]

- Edgley, Carla. 2014. A genealogy of accounting materiality. Critical Perspectives on Accounting 25: 255–71. [Google Scholar] [CrossRef]

- Edgley, Carla, Michael J. Jones, and Jill Atkins. 2015. The adoption of the materiality concept in social and environmental reporting assurance: A field study approach. The British Accounting Review 47: 1–18. [Google Scholar] [CrossRef] [Green Version]

- Farooq, Muhammad Bilal, and Charles de Villiers. 2019. Understanding how managers institutionalise sustainability reporting: Evidence from Australia and New Zealand. Accounting, Auditing and Accountability Journal 32: 1240–69. [Google Scholar] [CrossRef]

- Farooq, Muhammad Bilal, Zaman Rashid, Dania Sarraj, and Fahad Khalid. 2021. Examining the extent of and drivers for materiality assessment disclosures in sustainability reports. Sustainability Accounting, Management and Policy Journal 12: 965–1002. [Google Scholar] [CrossRef]

- Ferrero-Ferrero, Idoya, Raúl León, and María Jesús Muñoz-Torres. 2021. Sustainability materiality matrices in doubt: May prioritizations of aspects overestimate environmental performance? Journal of Environmental Planning and Management 64: 432–63. [Google Scholar] [CrossRef]

- Formisano, Vincenzo, Maria Fedele, and Mario Calabrese. 2017. Materiality matrix: A comparison between relevant indicators for banks and stakeholder. Paper presented at the 20th Excellence in Services International Conference (EISIC) Proceedings, Verona, Italy, September 7–8; Available online: https://sites.les.univr.it/eisic/wp-content/uploads/2018/07/20-EISIC-Formisano-Fedele-Calabrese.pdf (accessed on 18 June 2022).

- Garcia-Torres, Sofia, Marta Rey-Garcia, and Laura Albareda-Vivo. 2017. Effective disclosure in the fast-fashion industry: From sustainability reporting to action. Sustainability 9: 2256. [Google Scholar] [CrossRef]

- Geldres-Weiss, Valeska V., Nicolàs Gambetta, Nathaniel Massa, and Skania L. Geldres-Weiss. 2021. Materiality matrix use in aligning and determining a firm’s sustainable business model archetype and triple bottom line impact on stakeholders. Sustainability 13: 1065. [Google Scholar] [CrossRef]

- Gelmini, Lorenzo, Francesco Bavagnoli, Maurizio Comoli, and Patrizia Riva. 2015. Waiting for Materiality in the Context of Integrated Reporting: Theoretical Challenges and Preliminary Empirical Findings. In Sustainability Disclosure: State of the Art and New Directions. Edited by Lucrezia Songini and Anna Pistoni. Studies in Managerial and Financial Accounting. Bingley: Emerald Group Publishing Limited, vol. 30, pp. 135–63. [Google Scholar] [CrossRef]

- Gerwanski, Jannik, Othar Kordsachia, and Patrick Velte. 2019. Determinants of materiality disclosure quality in integrated reporting: Empirical evidence from an international setting. Business Strategy and the Environment 28: 750–70. [Google Scholar] [CrossRef]

- GRI—Global Reporting Initiative. 2006. Sustainability Reporting Guidelines. 2000–2006 GRI Version 3.0. Available online: https://www.globalreporting.org (accessed on 28 February 2020).

- GRI—Global Reporting Initiative. 2011a. Sustainability Reporting Guidelines. 2000–2011 GRI Version 3.1. Available online: https://www.globalreporting.org (accessed on 28 February 2020).

- GRI—Global Reporting Initiative. 2011b. Technical Protocol. Applying the Report Content Principles. GRI Version 3.1. Available online: https://www.globalreporting.org (accessed on 28 February 2020).

- GRI—Global Reporting Initiative. 2013. G4 Sustainability Reporting Guidelines. Implementation Manual. Available online: https://www.globalreporting.org (accessed on 28 February 2020).

- GRI—Global Reporting Initiative. 2016. GRI 101: Foundation. Available online: https://www.globalreporting.org/standards/media/1036/gri-101-foundation-2016.pdf (accessed on 26 May 2020).

- GRI—Global Reporting Initiative. 2021. GRI 3: Material Topics 2021. Available online: https://www.globalreporting.org/how-to-use-the-gri-standards/gri-standards-english-language/ (accessed on 28 March 2021).

- GRI—Global Reporting Initiative. 2022. GRI Universal Standards 2021 Frequently Asked Questions (FAQs) January 2022. Available online: https://www.globalreporting.org/media/zauil2g3/public-faqs-universal-standards.pdf (accessed on 12 August 2020).

- GSSB—Global Sustainability Standards Board. 2019. Review of GRI’s Universal Standards—Project Proposal. Available online: https://www.globalreporting.org/media/tyghiekh/universal_standards_final_project_proposal_approved.pdf (accessed on 28 March 2022).

- GSSB—Global Sustainability Standards Board. 2020. GRI Universal Standards: GRI 101, GRI 102, and GRI 103—Exposure Draft (June 2020). Available online: https://www.globalreporting.org/standards/media/2605/universal-exposure-draft.pdf (accessed on 28 March 2022).

- GSSB—Global Sustainability Standards Board. 2021a. GRI Universal Standards Project—GSSB Basis for Conclusions. Summary of Public Comments on the Exposure Draft of the Standards, and GSSB Responses (October 2021). Available online: https://www.globalreporting.org/media/0ymfh0xu/gssb-basis-for-conclusions_gri-universal-standards-project.pdf (accessed on 28 March 2022).

- GSSB—Global Sustainability Standards Board. 2021b. Item 08—GRI Universal Standards Project—Revised GRI 103: Material Topics for GSSB Discussion (February 2021). Available online: https://www.globalreporting.org/media/s4qlicgs/item-08-gri-universal-standards-project-revised-gri-103-material-topics.pdf (accessed on 28 March 2022).

- Guix, Mireia, Maria Jesús Bonilla-Priego, and Xavier Font. 2018. The process of sustainability reporting in international hotel groups: An analysis of stakeholder inclusiveness, materiality and responsiveness. Journal of Sustainable Tourism 26: 1063–84. [Google Scholar] [CrossRef]

- Guix, Mireia, Xavier Font, and Maria Jesús Bonilla-Priego. 2019. Materiality: Stakeholder accountability choices in hotels’ sustainability reports. International Journal of Contemporary Hospitality Management 31: 2321–38. [Google Scholar] [CrossRef] [Green Version]

- Hicks, Ernest L. 1964. Materiality. Journal of Accounting Research 2: 158–71. [Google Scholar] [CrossRef]

- Higgins, Keith, Alan Beller, John White, and Mary Schapiro. 2017. The SEC and improving sustainability reporting. Journal of Applied Corporate Finance 29: 22–31. [Google Scholar] [CrossRef]

- Holmes, William. 1972. Materiality—Through the looking glass. Journal of Accountancy 133: 44–49. [Google Scholar]

- Holsti, Ole R. 1969. Content Analysis for the Social Sciences and Humanities. Reading: Addison-Wesley. [Google Scholar]

- Hsieh, Hsiu-Fang, and Sarah E. Shannon. 2005. Three approaches to qualitative content analysis. Qualitative Health Research 15: 1277–88. [Google Scholar] [CrossRef]

- IIRC—International Integrated Reporting Council. 2013. Materiality. Background Paper for <IR>. Available online: https://www.integratedreporting.org/wp-content/uploads/2013/03/IR-Background-Paper-Materiality.pdf (accessed on 10 June 2022).

- IIRC—International Integrated Reporting Council. 2015. Materiality in <IR>. Guidance for the Preparation of Integrated Reports (November 2015). Available online: https://www.integratedreporting.org/wp-content/uploads/2015/11/1315_MaterialityinIR_Doc_4a_Interactive.pdf (accessed on 10 June 2022).

- IIRC—International Integrated Reporting Council. 2017. International <IR> Framework Implementation Feedback. Summary Report. Available online: http://www.integratedreporting.org/wp-content/uploads/2017/10/Framework_feedback_Sum2017.pdf (accessed on 10 June 2022).

- Jebe, Ruth. 2017. Corporate Sustainability Reporting and Material Information: An Empirical Study of Materiality under the GRI and Frameworks. Connecticat Journal of International Law 33: 95–135. [Google Scholar]

- Jones, Michael J. 2011. The nature, use and impression management of graphs in social and environmental accounting. Accounting forum 35: 75–89. [Google Scholar] [CrossRef]

- Jones, Peter. 2016. Materiality in corporate sustainability reporting: A research note on the UK’s leading food retailers. International Journal of Management Cases 18: 42–56. [Google Scholar]

- Jones, Peter, Daphne Comfort, and David Hillier. 2016a. Managing materiality: A preliminary examination of the adoption of the new GRI G4 guidelines on materiality within the business community. Journal of Public Affairs 16: 222–30. [Google Scholar] [CrossRef]

- Jones, Peter, Daphne Comfort, and David Hillier. 2016b. Materiality and external assurance in corporate sustainability reporting: An exploratory study of Europe’s leading commercial property companies. Journal of European Real Estate Research 9: 147–70. [Google Scholar] [CrossRef] [Green Version]

- Jones, Peter, Daphne Comfort, and David Hillier. 2016c. Materiality in corporate sustainability reporting within UK retailing. Journal of Public Affairs 16: 81–90. [Google Scholar] [CrossRef]

- Jørgensen, Sveinung, Aksel Mjøs, and Lars J. T. Pedersen. 2021. Sustainability reporting and approaches to materiality: Tensions and potential resolutions. Sustainability Accounting, Management and Policy Journal 13: 341–61. [Google Scholar] [CrossRef]

- Karagiannis, Ioannis, Panagiotis Vouros, Nikolaos Sioutas, and Konstantinos Evangelinos. 2022. Mapping the maritime CSR agenda: A cross-sectoral materiality analysis of sustainability reporting. Journal of Cleaner Production 338: 130139. [Google Scholar] [CrossRef]

- Krippendorff, Klaus. 2004. Content Analysis. An Introduction to Its Methodology. London: Sage. [Google Scholar]

- Kuisma, Jouko. 2017. Managing Corporate Responsibility in the Real World. Cham: Palgrave Macmillan. [Google Scholar]

- Kurniawan, Putu S., Dewi I. G. P. Banu, Sujana Astawa, and Luh G. K. Dewi. 2019. An Analysis of Information Materiality on Corporate Sustainability Report: A Comprehensive Study from Mining Industry in Indonesia. Advances in Economics, Business and Management Research 69: 91–97. [Google Scholar] [CrossRef] [Green Version]

- Lai, Alessandro, Gaia Melloni, and Riccardo Stacchezzini. 2017. What does materiality mean to integrated reporting preparers? An empirical exploration. Meditari Accountancy Research 25: 533–52. [Google Scholar] [CrossRef] [Green Version]

- Lakshan, A. M. I., Mary Low, and Charl de Villiers. 2021. Challenges of, and techniques for, materiality determination of non-financial information used by integrated report preparers. Meditari Accountancy Research 30: 626–60. [Google Scholar] [CrossRef]

- Lombard, Mattew, Jennifer Snyder-Duch, and Cheryl C. Bracken. 2002. Content analysis in mass communication: Assessment and reporting of intercoder reliability. Human Communication Research 28: 587–604. [Google Scholar] [CrossRef]

- López-Arceiz, Francisco J., Cristina Del Río, and Ana J. Bellostas. 2020a. Sustainability performance indicators: Definition, interaction, and influence of contextual characteristics. Corporate Social Responsibility and Environmental Management 27: 2615–30. [Google Scholar] [CrossRef]

- López-Arceiz, Francisco J., Rafael Santamaría Aquilué, and Cristina Del Río. 2020b. Sustainability for European investors: Evidence from a sustainable ranking. Revista de Contabilidad-Spanish Accounting Review 23: 148–66. [Google Scholar] [CrossRef]

- Lubinger, Melanie, Judith Frei, and Dorothea Greiling. 2019. Assessing the materiality of university G4-sustainability reports. Journal of Public Budgeting, Accounting and Financial Management 31: 364–91. [Google Scholar] [CrossRef]

- Madasu, Pardhasaradhi. 2019. Growing Relevance of ‘Materiality’ in Sustainability Reporting. Srusti Management Review 12: 14–23. [Google Scholar]

- Mathur, Sandeep, and Ravinder Kumar. 2019. Materiality analysis of SCM issues for Competitive Advantage: Study of an Indian FMEG Organization. In IOP Conference Series: Materials Science and Engineering, Paper presented at the 2nd International Conference on Computational & Experimental Methods in Mechanical Engineering, Greater Noida, India, May 3–5. Greater Noida: GL Bajaj Institute of Technology and Management, vol. 691. [Google Scholar]

- Mayring, Philipp. 2014. Qualitative Content Analysis. Theoretical Foundation, Basic Procedures and Software Solution. Available online: https://www.ssoar.info/ssoar/handle/document/39517 (accessed on 17 September 2022).

- McElroy, Mark W. 2011. Are Materiality Matrices Really Material? December 2. Available online: http://www.sustainablebrands.com/news_and_views/articles/are-materiality-matrices-really-material (accessed on 7 March 2022).

- Merkl-Davies, Doris M., and Niamh Brennan. 2007. Discretionary disclosure strategies in corporate narratives: Incremental information or impression management? Journal of Accounting Literature 26: 116–96. [Google Scholar]

- Mio, Chiara. 2013. Materiality and Assurance: Building the link. In Integrated Reporting: Concepts and Cases That Redefine Corporate Accountability. Edited by Cristiano Busco, Mark L. Frigo, Angelo Riccaboni and Paolo Quattrone. Berlin/Heidelberg: Springer International Publishing, pp. 79–94. [Google Scholar]

- Mio, Chiara, and Marco Fasan. 2013. Materiality from Financial Towards Non-Financial Reporting. Working Paper Series 19/2013; Venice: Università Ca’ Foscari. Available online: http://virgo.unive.it/wpideas/storage/2013wp19.pdf (accessed on 27 May 2022).

- Mio, Chiara, and Marco Fasan. 2014. The Determinants of Materiality Disclosure in Integrated Corporate Reporting. Working Paper Series 9/2014; Venice: Università Ca’ Foscari. [Google Scholar] [CrossRef]

- Mio, Chiara, Marco Fasan, and Antonio Costantini. 2020. Materiality in integrated and sustainability reporting: A paradigm shift? Business Strategy and the Environment 29: 306–20. [Google Scholar] [CrossRef]

- Morrós, Ribera Jordi. 2017. Materiality in sustainability reporting: Multiple standards and looking for common principles and measurement. The case of the seven biggest groups in Spain. European Accounting and Management Review 4: 108–47. [Google Scholar] [CrossRef]

- O’Dwyer, Brendan. 2003. Conceptions of corporate social responsibility: The nature of managerial capture. Accounting, Auditing and Accountability Journal 16: 523–57. [Google Scholar] [CrossRef] [Green Version]

- Oprişor, Tudor. 2014. Contributions to an improved framework for integrated reporting. AMIS 2014: 1043. [Google Scholar]

- Oprişor, Tudor. 2015. Auditing integrated reports: Are there solutions to this puzzle? Procedia Economics and Finance 25: 87–95. [Google Scholar] [CrossRef] [Green Version]

- Ortar, Liad. 2016. From flexibility to specificity: Practical lessons from comparing materiality in sustainability reports of the world’s largest financial institutions. International Journal of Corporate Strategy and Social Responsibility 1: 44–64. [Google Scholar] [CrossRef]

- Ortar, Liad. 2020. Materiality Matrixes in Sustainability Reporting: An Empirical Examination. Journal of Strategic Innovation and Sustainability 15: 108–33. [Google Scholar] [CrossRef]

- Owen, David L., Tracey A. Swift, Christopher Humphrey, and Mary Bowerman. 2000. The new social audits: Accountability, managerial capture or the agenda of social champions? European Accounting Review 9: 81–98. [Google Scholar] [CrossRef]

- Pesci, Caterina, Ericka Costa, and Teerooven Soobaroyen. 2015. The forms of repetition in social and environmental reports: Insights from Hume’s notion of ‘impressions’. Accounting and Business Research 45: 765–800. [Google Scholar] [CrossRef] [Green Version]

- Pesci, Caterina, Luca Fornaciari, Alice Medioli, Silvia Triani, and Teerooven Soobaroyen. 2020. Can Graphs in Sustainability Reports Actually Manage Impressions? An Analysis from the Investors’ Perspective. In Accounting, Accountability and Society. Edited by Mara Del Baldo, Jesse Dillard, Maria-Gabriella Baldarelli and Massimo Ciambotti. Cham: Springer, pp. 225–43. [Google Scholar]

- Pizzi, Simone, Andrea Venturelli, and Fabio Caputo. 2020. The “comply-or-explain” principle in directive 95/2014/EU. A rhetorical analysis of Italian PIEs. Sustainability Accounting, Management and Policy Journal 12: 30–50. [Google Scholar] [CrossRef]

- Puroila, Jenni, and Hannele Mäkelä. 2019. Matter of opinion: Exploring the socio-political nature of materiality disclosures in sustainability reporting. Accounting, Auditing and Accountability Journal 32: 1043–72. [Google Scholar] [CrossRef]

- Reimsbach, Daniel, Frank Schiemann, Rüdiger Hahn, and Eric Schmiedchen. 2020. In the eyes of the beholder: Experimental evidence on the contested nature of materiality in sustainability reporting. Organization and Environment 33: 624–51. [Google Scholar] [CrossRef]

- Reuter, Marek, and Martin Messner. 2015. Lobbying on the integrated reporting framework: An analysis of comment letters to the 2011 discussion paper of the IIRC. Accounting, Auditing and Accountability Journal 28: 365–402. [Google Scholar] [CrossRef]

- Ruiz-Lozano, Mercedes, Marta De Vicente-Lama, Pilar Tirado-Valencia, and Magdalena Cordobes-Madueno. 2021. The disclosure of the materiality process in sustainability reporting by Spanish state-owned enterprises. Accounting, Auditing and Accountability Journal 35: 385–412. [Google Scholar] [CrossRef]

- Saenz, Cesar. 2019. Creating shared value using materiality analysis: Strategies from the mining industry. Corporate Social Responsibility and Environmental Management 26: 1351–60. [Google Scholar] [CrossRef]

- Sepúlveda-Alzate, Yully M., Maria A. García-Benau, and Mauricio Gómez-Villegas. 2021. Materiality assessment: The case of Latin American listed companies. Sustainability Accounting, Management and Policy Journal 13: 88–113. [Google Scholar] [CrossRef]

- Slacik, Johannes, and Dorothea Greiling. 2019. Compliance with materiality in G4-sustainability reports by electric utilities. International Journal of Energy Sector Management 14: 583–608. [Google Scholar] [CrossRef]

- Sydow, Jörg, Georg Schreyögg, and Jochen Koch. 2009. Organizational path dependence: Opening the black box. Academy of Management Review 34: 689–709. [Google Scholar] [CrossRef] [Green Version]

- Tan, Yongtao, Chenyang Shuai, Liyin Shen, Lei Hou, and Guomin Zhang. 2020. A study of sustainable practices in the sustainability leadership of international contractors. Sustainable Development 28: 697–710. [Google Scholar] [CrossRef]

- Taubken, Norbert, and Tim Y. Feld. 2018. Impact measurement and the concept of materiality—New requirements and approaches for materiality assessments. Nachhaltigkeits Management Forum Sustainability Management Forum 26: 87–100. [Google Scholar] [CrossRef]

- Tibiletti, Veronica, Pier Luigi Marchini, Katia Furlotti, and Alice Medioli. 2021. Does corporate governance matter in corporate social responsibility disclosure? Evidence from Italy in the “era of sustainability”. Corporate Social Responsibility and Environmental Management 28: 896–907. [Google Scholar] [CrossRef]

- Torelli, Riccardo, Federica Balluchi, and Katia Furlotti. 2019. The materiality assessment and stakeholder engagement: A content analysis of sustainability reports. Corporate Social Responsibility and Environmental Management 27: 470–84. [Google Scholar] [CrossRef]

- Tucker, Basil, and Zahirul Hoque. 2017. Mixed methods for understanding accounting issues. In The Routledge Companion to Qualitative Accounting Research Methods. Edited by Zahirul Hoque, Lee D. Parker, Mark A. Covaleski and Kathryn Haynes. London: Routledge, pp. 301–20. [Google Scholar]

- Varachia, Zakiyyah, and Yaeesh Yasseen. 2020. The use of graphs as an impression management tool in the annual integrated reports of South African listed entities. Journal of Economic and Financial Sciences 13: 1–11. [Google Scholar] [CrossRef]

- Weber, Robert P. 1990. Basic Content Analysis. London: Sage. [Google Scholar]

- Wee, Marwin, Ann Tarca, Lee Krug, Walter Aerts, Penelope Pink, and Matthew Tilling. 2016. Factors Affecting Preparers’ and Auditors’ Judgements about Materiality and Conciseness in Integrated Reporting. London: ACCA. Available online: https://research.tilburguniversity.edu/en/publications/factors-affecting-preparers-and-auditors-judgements-about-materia (accessed on 20 April 2022).

- White, Marilyn, and Emily E. Marsh. 2006. Content analysis: A flexible methodology. Library Trends 55: 22–45. [Google Scholar] [CrossRef]

- Zhou, Yining, and Geoff Lamberton. 2011. Stakeholder diversity versus stakeholder general views: A theoretical gap in sustainability materiality conception. Paper presented at the 1st World Sustainability Forum, Basel, Switzerland, November 1–30. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Reference | Sample Analysed and Reports Examined | Percentages Found by Years | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Country | Industry | No | Report | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | |

| Ortar (2016) | W | Banks | 5 | SR | 0.45 ¶ | ||||||||||||

| Tibiletti et al. (2021) | Italy | C-I | 200 | SRR | 25.4 † | 25.4 † | 25.4 † | ||||||||||

| Eccles et al. (2012) | W | C-I | 800 | SR | 8.88 ¶ | ||||||||||||

| Bavagnoli et al. (2014) | EUR | C-I | 32 | IR | 28 | ||||||||||||

| Slacik and Greiling (2019) | W | ELU | - | SR | 58 | ||||||||||||

| Jebe (2017) | W | C-I | 96 | SR, IR | 37.5 | ||||||||||||

| De Cristofaro and Gulluscio (2019) | EUR | C-I | 108 | IR | 69.44 | ||||||||||||

| Karagiannis et al. (2022) | W | MAR | 42 | SR | 42.86 | ||||||||||||

| Lubinger et al. (2019) | W | UNI | 33 | SR | 48.48¶ | ||||||||||||

| Torelli et al. (2019) | Italy | C-I | 152 | NFR | 66 | ||||||||||||

| Costa et al. (2022) | W | TOU | 49 | SR | 43% | ||||||||||||

| Phase Feature | Phase 1 (Quantitative) | Phase 2 (Qualitative) |

|---|---|---|

| Fraction of research question answered | What approaches to MM adoption emerged over time? | Why did certain approaches to MM adoption emerge? |

| How viewpoints on MM are captured | Indirectly | Directly |

| Focused insiders | NFRs preparers | GRI stakeholders |

| Data source | 2014–2020/21 non-financial reports | Public comments on Exposure Draft of the Universal Standards GRI 103: Material Topics (GSSB 2020) |

| Rationale | Both MM publication and non publication as tacit proof of preparers’ positions about MM adoption | Comments on MM as explicit proof of insiders’ opinions of MM |

| Analysed aspects (tools of analysis used are indicated between brackets) | Evolution of MM publication (percentages and graphs) | Submitters examined by approaches, category, and country (absolute values) |

| Approaches to MM adoption (descriptive statistics) | Approaches to MM (qualitative content analysis) | |

| Association between MM adoption and GRI compliance (Chi-square) | Arguments expressed on MM (qualitative content analysis) |

| Criteria of Inclusion | Resulting Number of Companies |

|---|---|

| Initial list of companies: companies included at least once in the RobecoSAM Yearbooks (years 2014–2021) | 1028 |

| Minus: 849 companies not included in all eight 2015–2022 Yearbooks | 179 |

| Minus: 118 companies that did not consistently receive the yearly RobecoSAM medals over the selected period | 61 |

| Minus: one company that does not publish online pdf versions in English of its NFRs | 60 (the sample) |

| Question | Theme |

|---|---|

| 1 | Key concepts in the GRI standards |

| 2 | Using the GRI standards for sustainability reporting |

| 3 and 4 | Statement of use |

| 5 | Governance |

| 6 | Identifying material topics |

| 7 and 8 | Reporting on material topics |

| 9 | Structure of the universal standards |

| 10 | Other comments |

| Panel 5A. Geographical Provenance. | ||||

| Continent | Respondents | |||

| Overall | Commenting MM | |||

| (No. 144) | % (Out of 144) | (No. 13) | % (Out of 13) | |

| Africa | 7 | 4.86 | - | - |

| Asia | 44 | 30.56 | 4 | 30.77 |

| Europe | 53 | 36.81 | 6 | 46.15 |

| America | 31 | 21.53 | 2 | 15.38 |

| Oceania | 5 | 3.47 | 1 | 7.69 |

| Not stated | 4 | 2.78 | - | - |

| Panel 5B. Categories. | ||||

| Category | Respondents | |||

| Overall | Commenting MM | |||

| (No. 144) | % (Out of 144) | (No. 13) | % (Out of 13) | |

| Business enterprise | 32 | 22.22 | 3 | 23.08 |

| Civil society organization | 23 | 15.97 | 1 | 7.69 |

| Investment institution | 10 | 6.94 | - | - |

| Labour organization | 4 | 2.78 | - | - |

| Mediating institution | 73 | 50.69 | 9 | 69.23 |

| Not stated | 2 | 1.39 | - | - |

| First Step—Detection of Choice to Publish MM according to Stability | Second Step—Aggregation of Detailed Choices of Approaches | ||||

|---|---|---|---|---|---|

| Detailed Choices | Abs | % | Approaches to MM | Abs | % |

| (a) Always published | 33 | 55.00 | A—In favour of MM adoption | 45 | 75.00 |

| (b) Always published from 2015 onwards | 4 | 6.67 | |||

| (c) Always published from 2016 onwards | 3 | 5.00 | |||

| (d) Always published from 2017 onwards | 2 | 3.33 | |||

| (e) Always published from 2018 onwards | 1 | 1.67 | |||

| (f) Not published only in 2017 and 2019 | 1 | 1.67 | |||

| (g) Not published only in 2017 and 2020 | 1 | 1.67 | |||

| (h) Never published | 8 | 13.33 | B—Against MM adoption | 15 | 25.00 |

| (i) No more published from 2018 | 1 | 1.67 | |||

| (j) No more published from 2017 | 1 | 1.67 | |||

| (k) Published only in 2016 and 2017 | 1 | 1.67 | |||

| (l) Published only in 2017 and 2018 | 1 | 1.67 | |||

| (m) Not published in 2017, 2019, and 2020 | 1 | 1.67 | |||

| (n) Published only in 2020 | 2 | 3.33 | |||

| Companies | Measures | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|---|---|---|

| Sample | Mean | 0.62 | 0.77 | 0.87 | 0.87 | 0.97 | 0.92 | 0.92 |

| Standard Deviation | 0.55 | 0.59 | 0.59 | 0.62 | 0.63 | 0.63 | 0.61 | |

| Pro MM | Mean | 0.73 | 0.93 | 1.02 | 1.07 | 1.24 | 1.18 | 1.18 |

| Standard Deviation | 0.49 | 0.49 | 0.45 | 0.49 | 0.43 | 0.44 | 0.44 | |

| Against MM | Mean | 0.27 | 0.27 | 0.40 | 0.27 | 0.13 | 0 | 0.13 |

| Standard Deviation | 0.57 | 0.57 | 0.71 | 0.57 | 0.34 | 0.00 | 0.34 |

| Year | Pro-MM Companies (No. 45) | Against-MM Companies (No. 15) | Overall (No. 60) |

|---|---|---|---|

| 2014 | 19.688 * | 1.458 | 20.400 * |

| 2015 | 8.226 | 2.292 | 15.485 * |

| 2016 | 0.520 | 0.938 | 6.319 |

| 2017 | 0.517 | 3.393 | 12.243 ** |

| 2018 | Not calculable | 3.462 | 17.111 * |

| 2019 | 0.157 | Not calculable | 25.390 * |

| 2020 | 0.157 | 4.904 | 4.432 |

| Panel 9A. The “Pro-MM Group” (7 Respondents) Examined by Stakeholder Category and Geographical Provenance. | |||||

| Continent | Country | Mediating Institution (No. 7) | Totals | ||

| Continent | Country | ||||

| Asia | Hong Kong | 1 | 2 | 1 | |

| Russian Federation | 1 | 1 | |||

| Europe | Italy | 1 | 4 | 1 | |

| Switzerland | 1 | 1 | |||

| United Kingdom | 1 | 1 | |||

| North America | United States | 1 | 1 | 1 | |

| Oceania | Australia | 1 | 1 | 1 | |

| Panel 9B. The “Against-MM Group” (4 Respondents) Examined by Stakeholder Category and Geographical Provenance. | |||||

| Continent | Country | Business Enterprise (No. 3) | Mediating Institution (No. 1) | Totals | |

| Continent | Country | ||||

| Asia | Hong Kong | 1 | - | 2 | 1 |

| Malaysia | 1 | - | 1 | ||

| Europe | Italy | 1 | - | 2 | 1 |

| United Kingdom | - | 1 | 1 | ||

| Code Macro-Categories | Code Categories | Sub-Codes | |

|---|---|---|---|

| Label | Label | No | Label ‡ |

| A. Pro-MM | MM advantages | 6 | (a2) MM fosters transparency. |

| (c1) The MM y-axis has a double potential (impact significance and scaling). | |||

| (a2) MM is useful to understand the relative importance of topics and the reasons behind their materiality. | |||

| (b3) The MM visual approach provides insights to users. | |||

| (a2) MM shows stakeholder assessments. | |||

| (a3ii) MM is understandable and applicable. | |||

| MM removal disadvantages | 4 | (e1) MM removal generates difficulties for preparers. | |

| (e2) MM removal reduces transparency on material topics evaluation. | |||

| (b4) MM reshaping would weaken the stakeholder engagement concept. | |||

| (a4) MM removal without providing alternatives will create confusion, inconsistency, and incomparability. | |||

| Expected MM features | 5 | (e4) MM should be both a decision-making and communication tool. | |

| (a2) MM should be voluntary. | |||

| (a3) MM should be presented according to the new impact-based materiality concept. | |||

| (b1) The MM axes have to be specified (e.g., impact probability/severity). | |||

| (b2) The MM axes have to be redefined. | |||

| Suggestions for MM | 2 | (e5) Both MM and other tools could be leveraged. | |

| (e6) A new MM addressing both impact significance and occurrence likelihood could be considered. | |||

| B. Against-MM | MM disadvantages | 3 | (a2) MM misleads. |

| (b3) MM encourages simplistic issue identification. | |||

| (b4) MM undermines a topic’s accountability and management controls. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

De Cristofaro, T.; Raucci, D. Rise and Fall of the Materiality Matrix: Lessons from a Missed Takeoff. Adm. Sci. 2022, 12, 186. https://doi.org/10.3390/admsci12040186

De Cristofaro T, Raucci D. Rise and Fall of the Materiality Matrix: Lessons from a Missed Takeoff. Administrative Sciences. 2022; 12(4):186. https://doi.org/10.3390/admsci12040186

Chicago/Turabian StyleDe Cristofaro, Tiziana, and Domenico Raucci. 2022. "Rise and Fall of the Materiality Matrix: Lessons from a Missed Takeoff" Administrative Sciences 12, no. 4: 186. https://doi.org/10.3390/admsci12040186