Abstract

This study aims to analyse the role and contribution of small farms and small food businesses on the food system and food security. Drawing on a conceptual framework, methodology, and data from the EU H2020 ‘SALSA-Small farms, small food businesses and sustainable food and nutrition security’ project hereafter referred as SALSA project, this issue has been analysed in relation to four staple products (tomato, chicken, maize, and banana) in Santiago Island (Cabo Verde). The study follows a regional approach based on a detailed analysis of the territorial food systems and of the production/consumption balance of those staple products. The results show that the subsystems of production, processing, distribution, and consumption are different in the different food systems map for the four staple products, with complex and diversified interrelationships between small farms and related small businesses linking with various markets and all kinds of actors. Moreover, the evidence shows that small farms, in conjunction with small food businesses, are crucial to national food security in Santiago Island. The small farm is fundamental for greater food availability produced in the region, and the small food business is a key component playing a very important role by ensuring the stability of supply, being primarily responsible for establishing relationships to population centres.

1. Introduction

Family farming is the predominant mode of agricultural production in the world. According to [1], family farms produce about 80% of the world’s food in value terms, and they are the largest source of employment worldwide. It is estimated that 95% of the 500 million family farms are operated by small farmers in plots less than 2 ha [2,3]. Furthermore, in Sub-Saharan Africa (SSA), about 60% of the farms are smaller than one hectare and 95% of farms are smaller than 5 hectares and make up the majority of farmland in SSA [1]. Thus, small-scale farming is the dominant form of food production in the African continent and has been a central part of policy in recent decades.

Family farms in large agrarian SSA region are deeply embedded in the socio-economic life of farming communities shaping in general the social and political organisation. They encompass a diverse range of relatively small-sized structures, production, productivity, and levels of capitalisation according to their varied social, agro-ecological, and economic conditions using limited landholdings to pursue diverse agricultural and pastoral management activities. Moreover, they rely mainly on family labour, but they also employ their equally poor or poorer neighbours, using their production for both self-consumption and sale. As pointed out by [1], the informal and extra-market exchanges can be particularly relevant in the case of subsistence farming, allowing income generation and the creation of informal employment opportunities, offering a necessary survival strategy. Most contemporary family farms sell a portion of their produce, but some sell more than others [1,4,5].

Despite the old debate, which dates back at least to the end of the 19th century and is still open, small-scale farms differ from large-scale farms with more labour and a more intensive use of modern inputs. Data from some studies show that small farms display less productivity per hectare [6]. However, recent studies show high productivity levels of small farmers in Africa [7].

Agricultural activities and food production chains are key elements for a sustainable growth process and quality of life in any regions [8]. Family farmers in Africa are crucial for food security [7,9]. In addition to their importance in food production, they play a strategic role in social protection (e.g., poverty security, reduced inequalities, and gender relations). Its importance has been highlighted in the various regional African dialogues. The CAADP (Comprehensive Africa Agriculture Development Programme), the Regional Conference, recommended that governments should finance small-scale farmers to increase agricultural productivity and ensure food security and nutrition on the continent. The contribution of small farms to poverty alleviation, food security, and sustainability in SSA is a relevant development research topic raised by African and international authorities [10,11,12].

The food system approach was considered the best suited to investigate the contribution of small farms and food companies to the various dimensions of food and nutrition security [7,13].

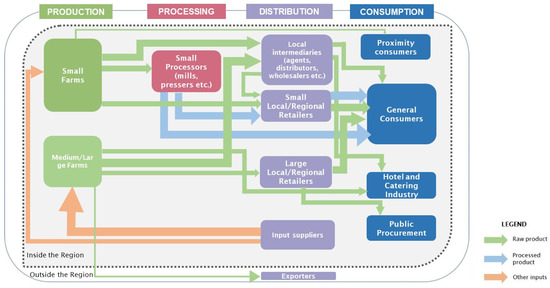

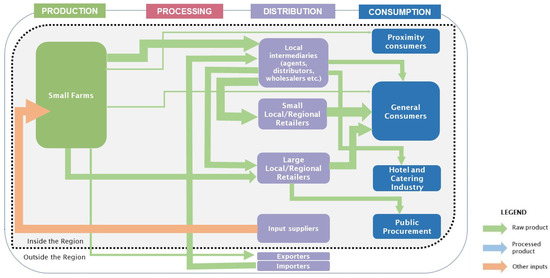

The purpose of this paper is to characterise the food systems in Santiago that are so far unknown. Taking into account the configuration of the regional food system in Figure A1 and Figure A2, we will map out the different actors as well as examine the contribution of small farms to the Food and Nutrition Security in Cabo Verde, specifically in Santiago Island. We assess this role of small farms and small food business applying a system perspective in the analysis of food systems on four staple products (tomato, chicken, maize, and banana), which will allow capturing the diversity of their related sectors (vegetables, animal production, cereals, fruits). The main reasons for the choice of these staple products, supported by stakeholders and key informants, were that they are largely produced and consumed in Cabo Verde.

Food security in Cabo Verde is not simply an agricultural, economic, or public health issue, but it is also an important social and political issue with many implications concerning the presence and the role of small farms and related small food business.

Since food security in Cabo Verde has not been extensively investigated so far, the characterisation of food systems represents an indispensable tool for the analysis of the current food security problem in Cabo Verde, combining multiple data collection methods. Previous research has dealt with the role and importance that agricultural production, namely irrigated farming and rainfed farming have on food security, income, and improving the quality of life of families [14,15]. Other research aimed to study local factors of resilience to the threat of rising international prices and the responses of rural households [16], such as studying the behaviour of food supply to institutional markets through family farming, seeking to compare the behaviour of the national market with the international market for basic food products [17,18]. Recent literature shows interest on the objectives of public policies towards food security in Cabo Verde [19]. At the environmental level, noteworthy studies related to combating desertification, based on soil and water management [20,21]. Regarding agricultural systems, [22] frames the food problem in terms of security rather than self-sufficiency. Therefore, it is important to invest in the development of farming systems where all agricultural practice takes into account a balanced relationship between man and the environment. The four sectors are thus described with a focus on relationships, processes, contexts, and roles that small farms play in the light of food and nutrition security dimensions. These analyses allow better understanding on how small farms interact with food systems in the local, regional, and global chains. As such, we contribute to describe the relations between production, consumption, and integration in the market and how they can affect the food and nutrition security. Hence, the research questions we address in this study are: What are the formal and informal key connections for small farms? Which actors are involved in the regional food system? What is the contribution of small farms to regional food systems? The results from this study will allow a better perception of the food systems and the role of small farm and small food business to food and nutrition security in Santiago Island.

2. Materials and Methods

2.1. Study Area: Geography and Climatic Characterisation

The archipelago of Cabo Verde, with a total land area of 4.033 km2, belongs to the group of West African countries. It is located in the middle of the Atlantic Ocean, off the coasts of Senegal and Mauritania, about 500 km from the African continent. It consists of 10 islands divided in two groups: Barlavento (Santo Antão, São Vicente, Santa Luzia, São Nicolau, Sal, and Boavista) and Sotavento (Maio, Santiago, Fogo, and Brava), with an exclusive maritime area of about 700,000 km2 [23,24,25]. It also consists of 8 islets (Branco, Raso, Grande, Luís Carneiro, Cima, and the islets of Rombo and Secos). In terms of relief and being of volcanic origin, the archipelago presents two distinct situations: flat islands (Sal, Boavista, and Maio) and the other more rugged islands where the highest points are located, such as Pico do Fogo (2829 m) in Fogo island, Pico de Antónia (1819 m) on Santiago island, and Topo de Coroa (1600 m) on Santo Antão island.

Cabo Verde is located in a vast area of arid and semi-arid climate under the influence of the Sahel, which crosses the African continent. The climate is dry, arid, and semi-arid of tropical type in the continuity of the Sahelian region, and it is characterised by a great scarcity and irregularity of rainfall, which for centuries has limited agriculture and hindered the challenge of economic development in the country. Often times, the severe droughts caused severe food shortages. There are two seasons: the very short rainy season (from August to October), where most precipitation is concentrated and where torrential rains occur. The driest and coolest season occurs from December to June, with the months of November and July being considered months of transition [26]. Moderate and relatively uniform temperatures are recorded throughout the year due to maritime influence with average monthly amplitudes ranging between 20 and 26 °C.

2.2. Study Area: Socio-Economic and Agricultural Sector

The total population of Cabo Verde is 531,239 inhabitants, of which the island of Santiago houses 59% [27], divided into urban population with 61.8% and rural population with 38.2% [28]. In terms of spending, 52% of Cabo Verdean’s budget is for food and housing, of which only 26% is spent on food, especially on cereals and cereal products, followed by vegetables, tubers, meat, milk, cheeses and eggs, fish, etc. namely in rice, bread and bakery products, poultry meat, pork, beef, sausages, bananas, maize, etc. [29].

Agriculture is a very important sector in Santiago, with a strong impact not only on the island’s domestic market, contributing to the supply of food products on the island but also at the national level. Table 1 illustrates the socio-economic and agricultural profile of Santiago Island. Although there is still no study on post-harvest losses in Cabo Verde, [30] points loss levels that can reach 24% to 45% due to low technology in harvesting, storage, and transportation. Additionally, agriculture in Cabo Verde is marked by the lack of use of technology, since all agricultural operations (from planting to harvest) are essentially manual, contributing to a longer and less efficient operation than machine operations.

Table 1.

Basic data for Santiago region.

The agricultural sector employs 34.8% of the active population [29], assuming great importance in the country’s socio-economic development. There are 20.772 family farms on the island, which is equivalent to about 59.1% of the country’s total. Cabo Verdean farming is mostly centred in the mountainous islands, especially the agricultural islands of Santiago, Santo Antão, Fogo, and São Nicolau. According to the 2015 general agricultural census [31], 59.1% of all arable land is located in Santiago and it is the second most important in terms of irrigated area, with approximately 33.7% of the total irrigated area [32], which demonstrates the agricultural importance of this island. However, arable area represents only 10% of the country’s territory.

Agriculture, to a large extent, consists of subsistence activity, based on small traditional family units. The majority of the farms are for self-consumption, with only a small part of the production (15–20%) going to the local market [33,34]. About 73% (33.309) of farms are rainfed followed by irrigation 18.9% (8.580); the rest is mixed [31]. The average area does not exceed 1 to 1.5 hectares.

Due to the low and irregular yield, Cabo Verdean agriculture is unable to meet the country’s needs, as it cannot cover more than 10–15% of the national food consumption needs [32,35]. It should be recalled that between 1990 and 1996, agricultural production did not cover more than 9.2% of food needs [36]. In this way, demand constraints have always been based on the trade possibilities involving the import of food goods where the international community plays a key role. At the top of imports are cereals (rice, maize, and wheat).

The rainfed farming is not very diversified. The main crops are maize in association with several varieties of beans (i.e., Lablab dolichos, Vigna unguiculata, Phaseolus vulgaris, Phaseolus lunatus and Cajanus cajan). Maize has an average production of 300 kg/ha and beans have an average production 90 kg/ha. Sugarcane production is one of the most important irrigated crops occupying particularly in Santo Antão and Santiago in between 45–80% of their agricultural areas. Sugarcane is only used for the production of a distilled spirit called “grog”. The production of horticultural crops and tubers has increased considerably in the last decade as a result of crop diversification. In addition, papaya and banana production have been improved and expanded, influencing the improvement of the diet of peasant families [37].

Livestock is a complementary activity to agriculture, it is carried out in 92.1% of farms, constituting an important sector in Cabo Verde. Animal production is concentrated in goats, pigs, and chickens, not neglecting some cattle, horses, and sheep, and it satisfies about 95% of the national demand for meat and eggs. The largest concentration of livestock activities is on the island of Santiago [38]. With regard to poultry farming, traditional and intensive forms of production occur, which compete with the massive importation of frozen chickens.

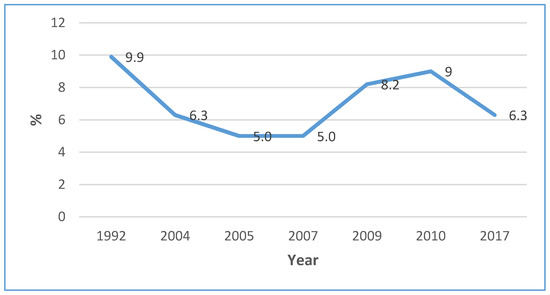

Agribusiness activities consist of the production, processing, and primary marketing (direct or after processing) to consumers. The contribution of agriculture, forestry, and livestock farming (Figure 1) has, over time, fluctuated and has been decreasing over the last decades [37].

Figure 1.

Agricultural sector contribution to Gross Domestic Product (GDP). Source: [39].

In addition to food production, the provision of jobs and income to the farming family, small farms, and small food business today is particularly relevant for supporting the rural livelihoods of many poor and under-educated. They contribute relatively to the preservation of the environment protecting agricultural and natural resources (soil, air, and diverse crops); moreover, the preservation of human and economic occupation in rural areas and social inclusion towards buffering the effects of high levels of unemployment, economic, and environmental shocks and poverty reduction.

Agriculture and livestock are considered transformative and of strategic importance for reducing poverty and, contributing to Cabo Verde’s efforts to achieve the Sustainable Development Goals, particularly the potential for socio-economic development of the rural economy [40,41,42,43,44].

According to [45] in its IDRF [Survey of Family Expenses and Income and Living Conditions) (Portuguese acronym)] the average annual expenditure per household in Santiago is around € 7154, and the average annual expenditure per person is € 1649.

2.3. Conceptual and Analytical Framework

To analyse small farming’s contribution to food and nutrition security, the key concepts of “food and nutrition security” and “small farming” need to be clarified.

The concept of food security is constantly evolving. The least developed countries use this concept particularly for the physical and economic access of populations to food and capability to meet the basic needs of human beings in quantity and quality for a healthy life. In the case of developed countries, it is associated with the issue of risk assessment (physical, chemical, biological and socioeconomic) [48].

In addition, [49] understands food security as the guarantee of the availability of food, produced locally or from abroad, and the possibility of access to it by all human beings. The classic definition of food and nutrition security has been given in the 1996 World Food Summit [50]. According to this definition, food security exists when all people, at all times, have physical, social, and economic access to sufficient safe and nutritious food that meets their dietary needs and food preferences for an active and healthy life. In the definition of food security, four dimensions should be considered: availability, access, utilisation, and stability [50,51].

There is no universally agreed definition of small farms and family farms. However, the two categories are often interconnected, and various authors use the two terminologies when they refer to peasants (or subsistence farmers). However, the latter have a relative integration in the market and are devoted to exportable products [52].

When looking at the concept of small farming, SALSA project explicitly recognizes the tremendous heterogeneity in small farm situations and related concepts and speeches [53]. Small farms comprise a wide range of organisational and structural patterns around the world [1,54]. In this study, we will therefore use “small farm” as a more generic term along with [53]. According to the authors, the focus is on small farms, and family farms will be considered only as long as they are also small farms. Therefore, small farms are those with less than 5 hectares of land.

In Cabo Verde, the term small farms is most commonly used to indicate small family farms, based on the size of the farm. Considering the General Agriculture Census [31], 98% of farms are considered small farms and family farms. Therefore, they represent the majority of the country’s agricultural production.

The term “small food business” indicates those food suppliers, processors, distributors, and retailers within a certain “size” defined in consideration of their geographical and sectorial specificities. Moreover, we will consider small food businesses that matter for small farms, i.e., they should be identified with regard to the connection they have with small farms [55]. Connections between small farms and small food business can take place both in the context of market transactions and of informal non-monetary exchanges based on reciprocity, barter, parental relations, etc. In this regard, an important role can be played by hybrid relational forms, based on elements that go beyond the mere price mechanism (mutual trust, shared feeling of community, etc.) but that nevertheless give birth to market-type relations [56].

From what was just argued, it follows that beyond the need of quantitative thresholds for the definition of “smallness”, the observation of small farms must consider the relational patterns they establish with the food system. From this perspective, a small farm can be seen as a farm who needs to engage in specific forms of relation (cooperation, informality, farm-household connections) in order to achieve goals that would otherwise be difficult for them to get. This leads us to consider the concept of food system [55].

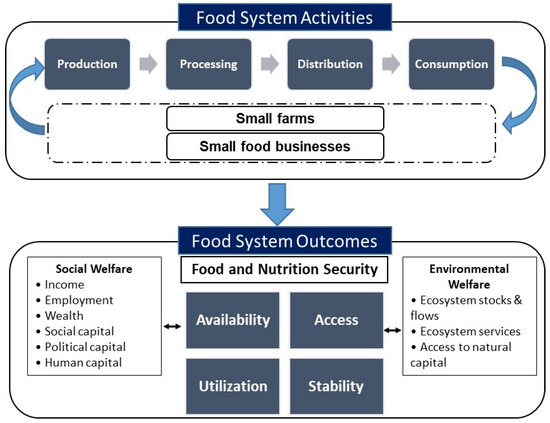

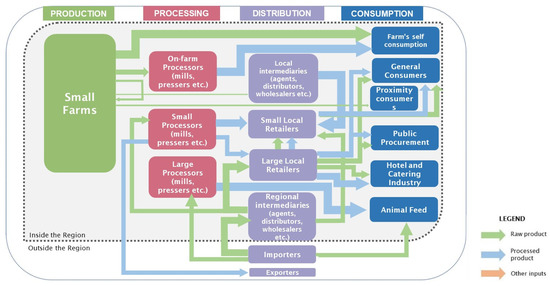

The food systems in Figure 2 provide an explicit analytical lens for understanding food security, where small farms and small food businesses are part of the food system, contributing to food availability, access, utilisation, and stability [51]. In this way, food systems can be conceptualised as comprising four sets of activities: producing food, processing food, distributing food, and consuming food [51,57,58]. These activities drive to several outcomes, many of which contribute to food security, and others relate to environmental and social welfare concerns [51].

Figure 2.

Food system representation (adapted from [51]).

Furthermore, according to Figure 2, this paper seeks to unravel the complex interrelationships between small farms, related small food businesses, and food and nutrition security.

Small farms and small food businesses contributions to food security through the links between small farms, small food businesses, and the four dimensions of food and nutrition security. So, in this case, small farms and small food businesses can contribute to food availability, food access, food utilisation, and food stability of food security by ensuring the stability of the production, distribution, and supply of food, even in situations of seasonal shocks and crises [59,60,61].

SALSA adopts a food systems perspective to explore all four dimensions of food and nutrition security and the connections between them (Figure 2). In addition, SALSA moves from the assumption that food and nutrition security depend to a great extent on the capacity of the food system to ensure access to sufficient, nutritional, and culturally acceptable food to people. Thus, farms and food business are conceptualised as food systems within this study’s components. Following these reflections, this paper uses the food system approach analysis, where a food system is considered “… all the elements (environment, people, inputs, processes, infrastructures, institutions, etc.) and activities that relate to the production, processing, distribution, preparation and consumption of food, and the outputs of these activities, including socio-economic and environmental outcomes” [62] (p. 12). However, this definition does not make any reference to the specific territory in which those food systems can be identified. They are a-spatial descriptions in which distances and geography do not play an explicit role [55]. With this approach, we intend to move beyond the simple focus on the production side, including the processes and power dynamics of different actors of production, distribution, and consumption along the supply chain.

We look at food systems as territorially based at the spatial level of reference regions, which are embedded in local areas with a set of dynamic interactions between households, enterprises, institutions, and ecological, spatial, biophysical, and technological elements. As suggested by the different studies, we take into account part of the proportion of local production that may be connected to global value chains or to the regional market or remain locally at both formal and informal levels. Therefore, we consider market, informal, and hybrid relationships to be relevant to farm connections. The different levels can range from subsistence agriculture to small farms that can depend entirely on the market to guarantee their food needs.

A relevant aspect to be aware of is that, even when we study a regional food system, interactions are not limited to the region itself, the latter being a component of a broader, in principle global, food system. Not all food produced in a certain region is delivered and consumed within a region and, on the other side, consumers cannot rely exclusively on food produced locally. This allows to improve the vertical and horizontal Food and Nutrition Security (FNS) policies and interventions [63]. It will also allow us to identify different production–consumption connections that are not exclusively market relations, i.e., including self-production, personal direct contacts, exchanges of food products within communities, offers to family members [64]. Hence, consumers mainly following a certain consumption model are not totally disconnected by distribution channels [55]. Moreover, farmers, distributors, and processors might depend on raw materials and inputs imported from other regions or to distribute and export outside of the region. Considering that we have defined the whole island of Santiago as the reference region for our study, in this case, shipping food products to other islands was designated as export. This aspect is of fundamental importance in the stability of food systems, since the contribution of small farms and small food businesses to food and nutrition security can strongly depend on the way they are connected to the food systems. Small farmers may contribute directly or indirectly to regional food and nutrition security, whether or not they are connected to consumption systems. This is particularly true when we look at the various forms of food self-consumption (for the household, but also extended to relatives, friends, and neighbours. This “extended” self-consumption practices represent a complement to everyday diet and may act as a buffer and a resilience asset in case of shocks or any breakdowns in the food system [56].

The identification of a food system within a particular region highlights the intersection between multiplicities of relational configurations, since cross-borders flows connect regions with external actors, extending influences beyond borders. Several power dynamics between actors, including some of the external actors, may have a strong influence on local actors’ behaviour, inducing the performance and shape the interconnections within the territorialised food system.

Power is a multi-dimensional construct. In developing countries, producers are confronted with asymmetric power relationships in value chains [65]. Thus, power relationships and information asymmetry are key issues to actors involved in value chains. According to [66], power stems from the ability to influence other firms to act in a desired manner for economic gains. In this context, power is related to the level of concentration and access to both key assets (physical and intangible resources) in the hands of a limited number of actors [67]. Actors who have exclusive access to physical resources (capital, land, credit, etc.) and intangible resources (market information, knowledge, personal relationships, reputation, etc.) can have the capacity to influence others in the chain.

2.4. Data Collection

The study was based on four complementary sources: (1) Desk data research, with analysis of data from various sources. Essentially in-country available published (official statistics) agricultural and economic data, sectorial studies and grey literature; (2) 14 interviews with key informants, such as, small farms, small and medium-sized retailers, small and medium-sized food processing companies, policy makers, and senior technicians of the Ministry of Agriculture, import companies and academics; (3) 35 interviews with small farmers (29 men and 6 women), as well as 5 interviews with small food businesses applied in each municipality of Santiago Island.; (4) two focus group with related stakeholders from Santiago Island; 32 stakeholders were part of the focus group and involved the following: farmers (2), producers’ cooperatives (2), slaughtering facilities (2), processors (1), retailers (2), caterers (1), other small food business (2), importers (1), advisory services (3), agricultural administration/Ministry of Agriculture (5), local administrators and policy makers (4), other programs/initiatives (4), nutritionists (2), non-governmental organisations (NGOs) (1). Stakeholders were chosen based on both a random choice, and others were indicated by the institutions.

2.5. Data Analysis

This research employed a mixed methods approach, comprising qualitative and quantitative analysis. Such an approach allows providing an opportunity for triangulation and cross-validation with deep understanding of the context data of this case study. The analysis was carried out according to the methodological guidelines that specified key questions, criteria, and indicators in a common conceptual and analytical framework agreed upon by based on the SALSA project (reference).

The process follows a regional approach to understand the territorial food systems, comprising the following steps [68].

Step 1: Desk data collection and exploratory interviews with key informants. Based on the collection of available statistical information of agricultural activity, basic demographic, social, and economic data, and with cross-validations through key informant interviews with experts and key stakeholders, it allowed a basic socio-economic and agricultural profile description of Santiago Island. Semi-structured interviews with experts and other stakeholders (with different important points of view) provided information and multidisciplinary expertise that is not possible to obtain from official statistics or publications. Moreover, it also extended and validated other sources of information, namely recommendations on the most relevant key products for quantitative estimation and details to further design the food system map. As a first step for the selection of key informants for the exploratory interviews, we identify and compiled a list of the stakeholders. Then, the key informants were chosen based both on a random choice and personal knowledge. Furthermore, it allowed a selection of a range of key products (staple products) developing a production and consumption balance sheet.

Step 2: Interviews with small farms and small food businesses. This step aims to provide a clear and detailed understanding of the activities related to how small farms and small food businesses operate, the relationships between farms/businesses and households, and how they are integrated into the market. The information was gathered through a set of interviews with farmers and small business owners. The semi-structured interviews and questionnaires to farmers and intermediaries were carried out between 2 and 25 July 2017. The main variables include their background (information on the farmer’s or business owner’s age, gender and education, reasons for starting the enterprise or farming); the description of farm, crops, and production (information on size, crops or products produced, post-harvest processing, permanent and occasional labour force, family labour force, yield or productivity, distance to the nearest urban centre); and intra-household dynamics (information about processing, sales, sources of food, and their relative importance). Additionally, the relationships that farms and small businesses have with the food system, including access to inputs (seeds, fertilisers, and raw materials) and markets (relationships with buyers and intermediaries, retailers, and others), and the destination of production, household consumption, and proportion of production that remains and is consumed nearby. Finally, the subsidies or any other kind of public financial support, access to credit or finance for farming, financial, technical, or labour support were also included in the data.

Time and resource constraints only allowed for a relatively small sample. Besides, sampling was purposeful rather than random; therefore, the information from these interviews is descriptive rather than statistically representative. Small farms were chosen by the municipal delegations of the Ministry of Agriculture who were called to help in the research by helping to identify potential small farms. The sampling of small farms was based on 35 interviews selected in farms around 5 ha (no minimum size was established), ensuring that farms cover a wide geographical area within the Santiago Island. Moreover, we also included the criteria of choosing that farms have to produce each of the selected key products, from farms with different degrees of market integration, and farms with varying degrees of self-sufficiency.

Small food businesses were chosen during the exploratory survey based on the catalogue of participants at the agribusiness fair organised by the Ministry of Agriculture. The sampling of small food businesses was based on 5 interviews, with the criterion of capturing the diversity of companies, the sample includes food processing, preparation, cooking or retail businesses, and those that did not have more than 5 employees. In addition, the selected companies are related to the main products, have direct links to the small farms, and are locally owned.

Step 3: Focus groups for validation of food system analysis. The focus groups aimed to discuss the exercise carried out in Step 1 and select the four staple products. Furthermore, it allowed designing the first in-depth picture of the food system map with the identification and estimation of the key nodes and flows within the system from production to processing, distribution and consumption, and also including the boundaries of the system. Additionally, it allows enhancing the understanding of the food system and with additional information, the role of small farms and small food businesses within it.

Two focus group meetings were held with stakeholders from various areas of the agri-food chain. A first focus group meeting was held on 18 April 2017 during which a series of activities were carried out namely, selection of the staple products for each category (e.g., Cereals, Oilseeds, Vegetables/Fruits, Fruits, Grapes for Wine, Animal Products), explanation of the main reasons for choosing the four staple products, description to characterise the system was made as well as the creation, and production of the food system map for each basic product. The final selection of the four key products (Fruit, Vegetable, Cereal, and Meat) meets the criteria of being largely produced in the region, important, and relevant in terms of consumption and local diet, and important in terms of culinary, cultural, and social reasons. The second focus group meeting was held on November 24th 2017, aiming to share, discuss, and validate the results and refining the food system maps developed during the research period after the first focus group.

Step 4. Finally, in this step, the quantitative and qualitative data from the semi-structured interviews and questionnaire and from the focus group were extracted and analysed comparatively. The data analysis was done through descriptive statistical analysis to investigate averages, frequencies, patterns, and correlations between variables. Qualitative data analyses were used on describing, categorising, and interpreting participants’ perceptions and experience.

3. Results and Discussion

Given the time and budget limitations, the sample is not likely to be statistically representative, so what we are likely to have is an illustrative description, done through purposive sampling, of what small farms and small food businesses look like in each region and how they integrate and relate to each other and to the food system. Furthermore, the lack of data due to the limited knowledge of the production and the size of the farmer area do not allow us to obtain the values of the yield, so some data were obtained from the literature.

3.1. Identification of the Key Staple Products and Development of a Balance Sheet

Despite the lack of data, the choices of staple products for Santiago was based on levels of production and consumption at the national level, as well on the information from stakeholders and key informants. The four main food products identified were Fruits (Banana), Vegetables (Tomato), Cereals (Maize), and Meat (Chicken).

- Fruits (Banana): The choice of banana is justified for being the fruit produced in greater quantity in the region, with greater regularity in supplying the markets during the whole year and for being an extremely important fruit in guaranteeing food security. The banana crop, along with papaya, has an average yield per hectare that is much higher than the other fruits combined, constituting an important source of income for the producers. Additionally, its production flow is continuous. The estimated current fruit production is between 10.000 and 12.000 tons per year, of which between 6.500 and 7.000 tons are bananas. In terms of consumption, banana is the fruit most consumed by children (80%), made preferably as snack, which is justified for being affordable to families and abundant fruit supplying the market all year round [69].

- Vegetables (Tomato): The choice of tomato as a main product was because it is the most produced vegetable in Santiago Island and available all year round, grown in open fields and greenhouses, and produces up to three harvests per year. The quantity produced is higher than the quantity imported. Most of the tomato consumed is produced locally, while imported tomatoes are mainly for tourist hotels. Data provided by [70,71,72] from 2016–2018 inform that the average availability between 2007 and 2016 was about 66.867 tons/year.

- Cereals (Maize): Despite its uncertainty of production and low productivity in Cabo Verde’s bioclimatic conditions, maize is an important crop in the country’s agricultural production system, since it is the only cereal produced in the country and one of the bases of the food diet, contributing significantly to the food security of rural households. It is produced only in rainfed farming (that is, without irrigation), being highly dependent on the precipitations that are scarce and irregular. Being an integral part of almost all the typical dishes in the Cabo Verdean gastronomy, maize production is a traditional and subsistence crop, mainly for self-consumption; it is not considered a market product. However, production levels are relatively insufficient for the desired level of consumption.

- Meat (Chicken): The choice of chicken was due to its level of consumption by the population, since its low price makes it more accessible to families. Moreover, its distribution using the cold chain is already well established in the country. From the household survey [45] per capita expenditure of national consumption of chicken meat is €16.8 compared to €10.5 for pork and €9.9 for beef, which gives us a good indication of the meat most consumed in the reference region.

The results of the interviews to some extent to confirm the importance of basic foods (staples products). All farmers surveyed grow one or more of the staples products, in addition to growing other crops. In a way, it can be said that the staple products that were selected represent the crops most produced by the farmers in the region of Santiago. From the sample of the 35 surveyed farmers, 46% cultivate banana, 63% cultivate tomato, 23% cultivate maize, and 57% are dedicated to chicken rearing. In relation to maize, there was little referenced, because the survey was limited to irrigated crops intended mainly for the market, although it is known that almost all farmers cultivate maize in their fields.

Regarding maize, there was little reference, because the research was limited to irrigated crops intended mainly for the market, although it is known that almost all farmers in Cabo Verde grow maize in their fields. Non-irrigated agriculture accounts for 87% of the area devoted to agriculture in Cabo Verde

3.2. Balance of Production and Consumption of Key Food Products in the Region

Based mainly on the Statistics of the Ministry of Agriculture and Environment and the National Institute of Statistics, we can see that the region is deficient in most of the main products as outlined in the Table 2: (1) maize (−89%), and (2) poultry (−89%) being the most deficient. In these two products, the problem of food security is a question of supply. Data from [73] shows that 7.533.5 tons of imports are from chicken meat, pieces, and offal, 7.004.1 ton are from tomato, 0.1 tons are from banana, and 20.493.2 tons from maize. Imports of chicken and maize are essential, reaching expressive levels. However, in the case of maize, imports account for only 88% of the deficit potential consumption. This indicates that there should be an improvement in domestic production systems, which are still based on a traditional production mode. As regards chicken meat, imports fully meet consumption levels, with the consumption deficit accounting for 49% of imported chicken meat. The surplus of banana (23%) and tomato (48%) show that these staple food products better meet the needs of domestic consumption with internal production.

Table 2.

Balance of production and consumption of relevant agricultural products in the region.

3.3. Food System: Key Nodes and Flows and Role of Small Farms and Small Food Businesses

3.3.1. Banana

• Case Study Sector

In Cabo Verde, banana cultivation has a long tradition. The Portuguese settlers may have initiated the banana cultivation in the 15th or 16th century. Since then, production of the crop has been established in the archipelago and traditionally has continued to play an important role. It has high social and economic value for the country and plays a key role in the diet and food security of the population [33,74].

According to the Agricultural Census [32], Cabo Verde has approximately 578.000 banana trees with an estimated production of 7000 tons. These data show a very low yield, which can be explained by the reduced size of the cultivated area (150–170 ha). The production of bananas in Santiago is mainly developed in flatter areas, mainly in the bottom of the valleys.

This is a crop that has assumed, especially in recent times, an increasing importance to provide income to families, especially in recent times. Banana cultivation in Santiago boosted in 2011 with the “Banana Crop Re-Launching Project”, a project co-financed by the European Union and the Cabo Verdean Government in a program to diversify agricultural production in Cabo Verde. The main objective of the project was to relaunch the banana crop by introducing “in vitro” plants, with the aim of fighting the banana pest, Fusarium oxysporum and increasing banana production. In addition, it contributes to improving the diet. For small-scale farmers, banana farming provides extra income and an alternative to unemployment and contributes to poverty reduction.

The advantage of banana crop is that it can be harvested throughout the year, allowing a stable supply of the product on the market throughout the year. In terms of food and nutritional security, bananas have numerous advantages because they contain high fibre and potassium content. The fibre contributes to regulating the digestive system, mitigating the dehydration caused by diarrhoea.

Focus group participants confirmed that there are no producer cooperatives but they are of great importance for small farms, from Santiago Island, to be able to create a cooperative to organise, coordinate, support, collect, protect, and market the banana production.

• Food System

Flows connecting the different nodes (production, processing, commercialisation, and retail) in the regional food system

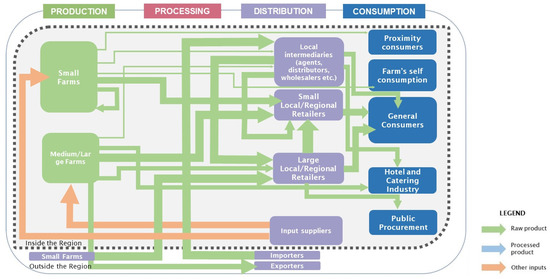

The banana food system is shown in Figure 3. Banana production is carried out by large and small farmers. The focus group found that small farmers produce more bananas than large farmers, with 90% of the bananas produced by small farms. The inputs for banana production are bought from commercial companies of exclusive sale of agricultural products, such as pesticides, fertilisers, etc., while the plants are obtained directly from the farmers. However, it is large farms that use the most inputs for banana production, (about 75% to 100% of inputs flow), namely fertiliser pesticides and other equipment. Small farms use between 25% and 50% of inputs flow (Figure 3).

Figure 3.

Regional food system for banana.

Most of the banana consumed is locally produced (about 444.9 tons). Of the 35 farmers surveyed, around 17 (48.5%) cultivate bananas. The general flow design of the banana food system was confirmed by the focus group participants. The focus group also with the findings of the main interviews shows that banana flows from small and large producers to local and regional intermediaries represent the most important and relevant flow; i.e., of the 96% of the production that is sold, more than 90% of the banana is sold to these actors. From the questionnaires, 100% of the small farms claim that they sell part of the banana produced to local and regional intermediaries. However, no clear indication on the quantities involved emerged from the interviews. Production is partly sold both from large and small producers in rural and urban areas of Santiago, and it is also exported to other islands, especially to the more tourist ones. Only large farms have a greater capacity to connect to external markets, where about 1% to 25% of the product is exported. From farmer’s interviews and the focus groups, we can add that in Santiago, farmers have a stable relationship with the intermediaries. Many of the producers choose to sell their products directly to the “Rabidantes” who go to the farms to buy the products and then sell them to the markets and other consumers. “Rabidante” is the reseller agent of an “informal” type of trade. In Cabo Verde, this type of activity hinges on a network in which men, but especially women, sell what was bought to be marketed, often outside the tax and market rules. They went to the farms to buy the products and then sell in and outside the area to the markets and other consumers, such as in urban households, small and large hotels, markets, and supermarkets, as well as in reselling to small retailers that sell in local markets, small hotels, or in informal stores or informal street vending, in addition to local supermarket chains. Both small and large farmers sell to intermediaries who then place the products on consumer market.

Small and regional intermediaries, who carry out much of the commercialisation, represent the most important supply of bananas for local area, and there are intermediaries of greater dimension. They take the product directly to the local markets, send it to other regions outside Santiago Island, and resell it to local small retailers, who in turn practice street vending and direct sales to consumers. The focus group mainly highlighted that from the total production of small and large farms, 80% to 90% of production is sold to intermediates, 10% to 15% is sold to retailers, and 1% to 5% is sold to hotels. The role of local small processors, who used banana to produce liqueurs, cakes, and fried banana, was considered strong.

The vast majority of small farms sell most of their products (about 97% to 98%), leaving a small percentage for offering (about 3%). Although other channels subsist, i.e., to a lesser extent, there are those who sell directly to consumers, but this less significant (about 1%). Self-consumption in this sense has lesser significance, since there is high market orientation, which leaves only 2% to 3% produced for household consumption. Only small farmers sell directly to the consumer due to a large producers’ market in larger quantities to medium and large retail structures.

Currently, there are not special regulations for the transport of products in order to guarantee their intrinsic quality. In addition, the chain consists of small intermediaries who carry out most of the commercialisation for local sales, placing the banana directly in the markets, in retail shops (25%), as well as in reselling to small retailers that sell in local markets (50%), small hotels (5%), or in informal stores or informal street vending (20%).

• Role of small farms and small food businesses within the food system

Small farms constitute the central step of banana value chain because they produce the majority of banana consumed within Santiago Island. Moreover, small farms are responsible for 90% of the national production of bananas. This segment is also responsible for income and jobs generation in farms, showing that refraining is important in halting rural exodus. However, the focus groups stressed the role of small farms and food business, which is associated with the availability of products for market, contribution to the diversity of products on the market, price competitiveness, freeing of Government from the responsibility of having to develop social program to feed families, providing self-employment, increased domestic production, and imports reduction.

As for small food businesses, local small and regional intermediaries, who are mainly supplied by local small farms, are very important and a fundamental key agent in the region, indispensable for maintaining the farm production of small farms, since they do not have infrastructure and capital to buy equipment or the opportunity to market banana. They are responsible for harvesting, packaging, transport, commercialisation, and distribution of the banana, placing the banana on the market available to consumers and to different food system actors and exports outside the region, as well as being responsible for the employment, and hiring casual workers to cut and load curls on rented trucks, including the driver, since there are no other agents who do so.

Local markets, grocery retailers, and supermarkets (food business establishments), supplied by local intermediaries, dominate the retail market and are considered the most significant because they are the places most frequented by consumers and also, they concentrate the sale of other products. In small towns, there are small markets, in which some producers sell their products directly to consumers and small local retailers. Local grocery stores that are mostly supplied by local producers are important because of their proximity to consumers. However, the exchanges of products between small farmers occurs frequently as stated by farmer’s interviews without specifying the quantities exchanged.

3.3.2. Tomato

• Case Study Sector

Tomato (Lycopersicon esculentum) is one of the main and most important horticultural crops produced on the Island of Santiago, and it is highly consumed. According to [75], because of the availability and increased use of locally adapted varieties, the tomato crop is currently produced all year round and without any protection, including in the hot and humid season. The variety “Calor” has contributed to the production of tomatoes throughout the year, since up to 3 crops can be grown in one year [61]. According to [76,77], tomato productivity in Santiago Island, in the hot season (from August to October) is 2.3 kg/m2 both with drip-irrigation system and with the traditional irrigation system (flooding). For the fresh season (from November to July), the productivity is 2.1 kg/m2 and 2.3 kg/m2, respectively. National tomato production has consistently increased from 200 tons per year in 1987 to 3000 tons in 1997. Furthermore, this crop is becoming increasingly important due to being stimulated by increased national demand and profitability.

• Food System

Flows connecting the different nodes (production, processing, commercialisation, and retail) in the regional food system

The tomato food system is shown in Figure 4. Tomato production is highly dependent on the flow of inputs. The inputs for the production are made through commercial companies of an exclusive sale of agricultural products, such as seeds (also from research institutions), pesticides, etc., the plants are obtained directly from the farm. Small farms account for around 100% of local production, using a drip-irrigation system. There are very few small farms specialising in horticulture, but in our sample of the 35 farmers surveyed, around 20 (57.1%) cultivate tomato. The focus group considered that small farmers produce tomato in greater quantity, according to data they produce 6.736,2 tons per year (Table 2).

Figure 4.

Regional food system for tomato.

The general flow design of tomato from primary producers to local intermediaries, of which 80% to 90% of production is exclusive of direct sale to small intermediaries was confirmed by the focus group plus with the findings from the key interview, and it is considered the most important and relevant. From small farm interviews, we can add that farmers have a stable relationship with these intermediaries. Many of the producers (about 80%) choose to sell their products directly to the intermediaries “Rabidantes” who are considered a relevant actor in commercialisation and distribution, collecting production from local farmers, placing the tomato directly in the markets, in retail shops (60%), as well as in reselling to small retailers that sell in local markets (25%), small hotels (5%), or in an informal stores or informal street vending (10%).

Also, focus group participants highlighted that 1% to 5% of the total production of small farms is sold to retailers and 1% is sold directly to consumers.

Overall, the local tomato production is largely sold and consumed in Santiago Island, and it is exported outside to other islands (about 1% to 5%), especially to the more touristic islands (Sal and Boavista), to sell to consumers and hotels. The focus group stresses the importance of a regional intermediary, who resent the tomato outside Santiago Island.

In some cases, large and medium retailers make connections with local farmers for the direct supply of vegetables, including tomato. The overwhelming majority of small farms sell most of the production, leaving a small percentage which they offer (about that 1% to 3%). To a lesser extent (less than 1%), there are those who sell directly to supermarkets and small processors and farmers’ markets; some of them have their own store. However, no clear indication of the quantities involved was given from the interviews.

Additionally, the importers are considered relevant actors. In particular, wholesaler’s businesses are extremely strong in Santiago for collecting production outside Santiago Island and selling their products in and outside the area, especially for big hotels. From the 76.68 tons imported, more than 90% flows to wholesalers, of which they place 20% to general consumers through local retailers such as supermarkets and 80% to tourist hotels and located within the reference region. The focus group stated that there are intermediaries of greater dimension. Small producers have been the major suppliers of tomatoes to institutional markets such as school canteens, hospitals, and the army. In this regard, an interesting role is played by institutional procurement, which takes place thanks to the local procurement bids. However, the exchanges of products between small farmers occurs frequently as stated by farmer’s interviews without specifying the quantities exchanged.

Despite considering farmer’s markets in the map, the flow of tomato from producers to farmer’s market is considered insignificant. However, no clear indication of the quantities involved emerges from the interviews.

Small food businesses are directed to intermediaries, supermarkets, and local grocery stores. It also emerged that in several cases, small local grocery stores are not supplied by wholesalers but rather from local producers. Small farms do not engage in direct processing; they produce for fresh consumption. Small food businesses, such as small processors, are not actually considered as relevant actors, because tomato processing does not occur. Farmers markets are also considered not relevant at the local level of Santiago Island.

• Role of small farms and small food businesses within the food system

Small farms constitute the central step of the tomato value chain; they produce the total 100% of the regional production (6.736.2 tons), and they are responsible for income and jobs generation in the farm, showing the importance to contain the rural exodus. About 13 (37.1%) of the 35 farmers interviewed have paid non-family workers, ranging from 1 to 4 workers. The important role of small farms and food businesses was stressed by the focus group, which is associated with the availability of products for market, the contribution to the diversity of products on the market, price competitiveness, freeing the State from the responsibility of having to create social program to feed families, providing self-employment, increased national production, and imports reduction.

Self-consumption has lesser significance for small farms. According to the small farms interviews, production is practically sold, which has shown a high orientation to the market. It is estimated that about 95% of production is for sales. Only 3% to 5% produced is for household consumption.

As for small food businesses, local small and regional intermediaries, who are mainly supplied by local small farms, are very important and a fundamental key agent both within and external to the Santiago Island market, which is indispensable for maintaining the production of small farms, since they do not have infrastructure and capital to buy equipment or the opportunity to market the tomato. They are responsible for harvesting, packaging, transport, commercialisation, and distribution of the tomato, placing it in the market to make it available for consumers and to different food system agents in Santiago Island and export outside, as well as being responsible for the employment, hiring casual workers to cut and load curls on rented trucks, including the driver, since there are no other agents who do so. In addition, local intermediaries sell the products to other local intermediaries, who do street vending.

Small food businesses processors are non-existent and do not constitute a central step of the tomato value chain, since most of the product is consumed in its natural state, and the post-harvest processing of the tomato is done on the farm. Local markets, grocery retailers, and supermarkets (food business establishments) dominate the retail market and are considered relevant. In small towns, there are flea markets, in which small farms sell directly to consumers but generally, they are considered not significant. On the other hand, local restaurants (different from agro-tourism caterers) do not represent relevant actors for local tomato purchase.

3.3.3. Maize

• Case Study Sector

Maize as well as rice (imported) is one of the staple products that constitute the basic food of the region of Santiago. Maize is the only cereal produced in the country, accounting for about 10–20% of the national cereal consumption needs in a good production year. The cultivated area in Cabo Verde was in 2011 about 31.318 ha, with a production of 5.569 tons and a low yield of 0.178 tons/ha. The Santiago Island accounted for approximately 61% of maize acreage with 19.026 ha and a production of 2.949 tons, or 53% of national production [47]. However, production is insufficient for the desired level of consumption, forcing the region to import more than 80% of its consumption, so that international import trade plays a key role in the country’s food supply.

Additionally, [78] indicate that Cabo Verdeans consume an average of 23 kg of maize per year. In 2001, about 15.368,042 tons were imported, rising in 2014 to 23.838,860 tons [73].

• Food System

Flows connecting the different nodes (production, processing, commercialisation, and retail) in the regional food system

The maize food system is shown in Figure 5. Maize is exclusively produced by small farmers (100% of the 3.183 tons/year regional production). In addition, the 35 farmers interviewed cultivate maize.

Figure 5.

Regional food system for maize.

The results of the surveys showed that the majority of the farmers’ production is destined for self-consumption, as 63% of the farmers stated that more than 85% of their production is destined for self-consumption, which makes self-consumption one of the most important flows from small farms production. A small proportion (10%) is leaving for market commercialisation, such as seed and as cereal for direct feeding, allowing some income for farmers. Such flow is particularly vulnerable since local primary production is exposed and depends on environmental and climatic stresses, especially erratic rainfall patterns. This vulnerability affects subsequent productions, since part of the seeds is used for production, while a less expressive flow is selling seeds to other small farms (3%). To a lesser extent, there are those who sell directly to consumers and intermediaries (2%), but there is no clear indication on the quantities involved. Sales to restaurants and catering services are not relevant for local small farms.

Maize is a staple product that is imported, along with rice and wheat. Imports are of essential character, reaching expressive levels. Thus, international import trade plays a key role in the country’s food supply. The importers are considered relevant actors; the wholesaler’s businesses are extremely strong in Santiago. Some large wholesalers engage in direct processing for retailers. Maize is imported through large importers, in which 3 operators control 95% of the imports. These subsequently sell to small retailers (constituted by grocery stores, supermarkets, restaurants, local markets, and hotels) and small processors, where maize serves as raw material for other agro-industrial transformation, the production of maize derivatives, such as prepared maize for “cachupa” (Traditional Cabo Verdean dish, made of maize and beans stewed with meat or fish, cassava, banana, and boiled vegetables) or for the production of animal feed, amongst others. This flow is vulnerable to international prices and can easily suffer from the uncertainties from the larger producing countries.

Another important importer of maize is the animal feed factories, which produce animal feed products that, in turn, are sold to livestock companies. For instance, even though the focus group participants highlighted that a high percentage of imported maize is intended for animal feed, no clear indication on the quantities involved emerged from the interviews. Our findings show that the relationships between the small farms and the remaining actors in the chain are minor compared to the relationship with the importers. Direct sales from local small farms to consumers are not significant, and some small farms deliver part of their maize production to intermediaries. Small local retailers are not supplied by local small farms.

Small food businesses processing companies consists of small local productions, namely processing into flour, animal feed, cakes, and pastries, which are sold in certain stores. Small farms also engage in the direct processing of maize in households. The “cachupa” and the “cuscus” are the most traditional dishes, but other maize food such as “camoca”, “fidjoz”, “xerém”, and “maize flour” are also common. Besides “cachupa”, there is a variety of cakes, fried, sweet and savoury foods made from maize.

• Role of small farms and small food businesses within the food system

Small farms have an important role because they produce most of the maize consumed. Santiago’s small farmers contributes to 62.5% of maize national production. Nevertheless, they do not respond to consumption demand with a deficit of 89% on total consumption (Table 2). Their production minimises the effects of poverty and the risk of hunger by meeting part of the domestic food needs.

Processors constitute a lesser dynamic segment, since they play a smaller role in the domestic supply. There are important products of the local gastronomy, but the amount processed is relevant only for maize flour.

Importers and wholesalers, by having a greater capital capacity, have a preeminent role by supplying larger quantities to respond to Santiago Island consumption. Importers are highly important maize suppliers for the maintenance of the animal feed factories for local animal farms.

Large retailers and local grocery stores that mainly market imported maize represent important local retailers because of the proximity to the consumers. However, restaurants are deemed as key potential buyers from large wholesalers.

3.3.4. Chicken Meat

• Case Study Sector

Santiago Island livestock production is concentrated in the production of poultry, pigs, goats, rabbits, cattle, equines, and sheep, of which poultry represents about 66.9% from the livestock animals. According to the 2004 Agriculture Census, there are about 244,394 chickens in Cabo Verde. The livestock production covers about 90% of the country’s meat consumption needs [79].

Despite the fact that several poultry farms existed in the past, with the fall in meat prices due to the market opening, the integration of Cabo Verde into the World Trade Organization with consequent market liberalisation, and the drastic reduction of customs duties, only the farms with good production capacity and of innovation survived. In addition, it was accompanied by lower prices for poultry imports, mainly from Holland, which represents strong competition for domestic companies with negative impacts on domestic sales.

The system is characterised by the combination of a few large farms specialising in poultry production, domestic/family production of “land chickens” in small family farms, and the importation of frozen chicken of national and foreign origin.

• Food System: Flows connecting the different nodes (production, processing, commercialisation, and retail) in the regional food system

The chicken food system is shown in Figure 6. Chicken production is locally made by large and small farmers, although large farmers produce in greater quantity. Of the 35 farmers surveyed, around 20 (57.1%) raised chickens, with a total of 3098 animals. The majority flow from the small farms exclusively to intermediates and retailers (80%). Overall, the local chicken production is largely consumed in the region, but it is also imported outside from other islands.

Figure 6.

Regional food system for chicken.

Regarding the commercialisation of poultry, many of the producers choose to sell their products directly to the intermediaries “rabidantes”. They go to the farms to buy the products and then sell to other consumers, such as urban households, small hotels, markets, as well as reselling to small retailers that sell in local markets, or in informal street vendors, who make barbecue chicken. In addition, large and medium retailers’ in urban markets, supermarkets, restaurants, butchers, and others retailers make connections with local farmers for direct supply. Small farms can sell directly to consumers but to a lesser extent. From the focus group, intermediaries, small retailers just as local restaurants represent one of the main sales channels of chicken by small farms. Moreover, lower sales levels are directed to supermarkets and local grocery stores. It also emerged that in several cases, small local grocery stores are not supplied by wholesalers but rather from local producers.

Sales to restaurants and catering are relevant for wholesalers. Importing chicken to Santiago constitutes very important flows. Santiago is the island with the largest representation in almost all products and animals imported, with 69% poultry meat, 43% of eggs and egg-product of consumption, 100% of day-old chicks, and 12% of fertile eggs. In particular, wholesalers’ businesses are extremely strong in Santiago Island for collecting outside the region and selling their products in the region and other islands, especially for big hotels. Wholesalers normally establish a contract of direct supply form the importers. Holland is a key exporter to Cabo Verde of frozen whole chicken, chicken parts, and offal. Another important flow is from the large farms from other islands to small retailers in Santiago Island. Large-scale producers from other islands export their production to Santiago Island through regional intermediaries, which subsequently place the products in the commercial and catering companies, which in turn resell to small food businesses.

Small and large farms can easily suffer from the market competition imposed by wholesalers with regard to imported chicken, as they are threatened by cheaper import products.

Poultry sales to consumers are done mainly by small food businesses (grocery stores, markets, and in the butchers inside supermarkets. In addition, processed meat in particular from roasts consumed in restaurants and retail purchases of frozen chicken represent the largest flows of consumption. Thus, small food businesses, including small processors, are considered relevant actors for this product.

Large farms and wholesalers have been the major suppliers of chicken to institutional markets such as school canteens, hospitals, and the army. In this regard, an interesting role is played by institutional procurement. On the other hand, farmer’s markets are considered not relevant at the local level for Santiago Island.

• Role of small farms and small food businesses within the food system

Small farms are responsible for income and jobs generation in the farm, showing the importance of containing the rural exodus. These producers contributes for the food supply in the domestic market with 444.9 tons/year, although they do not produce the majority of the (chicken) consumed within Santiago Island. Small farms contributes to only 20% of regional chicken produced. Moreover, self-consumption has a significant importance for small farms; according to the small farmers’ interviewees, production is mostly consumed, which shows a self-consumption-oriented production. This flow represent at least 50% of the farmers’ production.

The focus group stressed the important role of small farms and small food businesses associated with the availability of products for the market, contribution to the diversity of products for market, price competitiveness, freeing the State from the responsibility of feeding families, providing self-employment, increased domestic production, and imports reduction. In 2002, it was estimated that 80% of national production came from industrial units and 20% came from small semi-industrial units [80].

Small food businesses assume a fundamental key role in maintaining farm production, because they are essential for the commercialisation of chicken products. Small intermediaries are very important for chicken availability for the final consumer, placing more than 80% of the purchased chicken directly in large and small retailer’s shops. In addition, they place 5% in local grocery stores and 5% in small hotels. Restaurants with less than 5% represent important local sales because of the proximity to the consumer. On the contrary, they do not constitute a central step for processing, which is embedded in the small farm activity.

3.4. Governance and Other Factors Influencing Food Security

3.4.1. Agricultural Support and Policies

The situation of food security and its vulnerability is also dependent on the levels of support and commitment of public policies in supporting production and commercialisation. In Cabo Verde, the measures and policies have almost always been carried out by the State through the Ministry of Agriculture and Environment, which is strongly supported by international cooperation. These policies and strategies are designed to support and spur growth and build resilience of the agriculture sector mainly through the leveraging of modern technologies (drip-irrigation). With respect to interactions with governance structures, 40% of the small farms and small food businesses say they do not have access to agricultural advisory services, either for production or for commercialisation from the government institutions. Furthermore, 66% say they do not have access to credit and do not benefit from direct subsidies from the State, while 34% say they have access, with a credit available from commercial banks, microcredit institutions and NGOs.

Farmers who receive or have received some support from the Ministry of Agriculture consider this support to be of the utmost importance for increasing their incomes. However, the feeling of 80% of farmers interviewed was that rural policies failed to create social and economic alternatives or improve the situation of small farmers. Furthermore, focus group participants pointed out that there are insufficient policies and support measures targeted at small farms (a support program for small farms and a support program for semi-substance farms). In this way, agricultural support will be a key component to increase food productivity and production, especially with small farms [81].

3.4.2. Production Efficiency

Production efficiency has been more related to capital-led intensification (mechanisation, improved seeds and inputs), which embraces a mixed input–output structure. Food security is increasingly dependent on the higher productivity of land and labour towards food availability to cope with the increased population density in Santiago’s urban areas. Farming in Santiago performs a very crucial function of the socio-economic safety net in rural areas, allowing people to settle in the rural areas avoiding rural exodus, but its technical efficiency is low. Technical efficiency means production of maximum amount of output with incorporation of minimum possible amount of inputs [82]. The equipment used for planting and harvest is usually old and is essentially manual, contributing to a low efficiency with a decrease in labour efficiency, as well as the level of use of fertilisers and pesticides. Furthermore, one of the major constraints in Santiago Island is due to the aridity of the climate and reduced availability of irrigation water and arable land for farming.

According to [77], the average productivity of tomato on Santiago is 2.4 kg/m2; in turn, [43] informs that maize crop productivity is 300 kg/ha. These low productivity, pointing to a low level of technical efficiency, stem from the lower technical utilisation of resources.

Production inefficiencies are also coupled with the structural small-scale of farms and small food businesses (lack of scale), which is also an obstacle to access to new and larger markets, since the production and distribution capacity is limited in both physical and financial terms. Moreover, small farms produce without any coordination with the markets and do not make use of the opportunities provided by cooperation in terms of production efficiency.

Thus, production efficiency is an aspect to take into account, because according to [83], productive efficiency provides opportunities for farmers to produce more farm income, which leads to a rise in the welfare level of the household.

3.4.3. Level of Prices and Purchasing Power of Consumers

Price variations are one of the main planning and decision-making tools for both producers (more market-oriented) and consumers. Furthermore, they cause instability in producers’ incomes and consumer spending.

Most of the Santiago farmers (86% of the farmers interviewed) produce for the market, selling, on average, more than 90% of their staple products, while consuming or offering the rest of the yield to family, friends, and workers. In Santiago Island, the instability caused by the aridity of the climate and the reduced availability of water causes large fluctuations in the price of food products, which may be a disincentive to production in periods of falling prices or causing overproduction in periods of high prices. With regard to market relations, the respondents cited low purchasing power (38%) as one of the most important constraints in the food system.

Small farmers have little power in setting up sale prices for all four key products in Santiago. This is because they depend on the prices established by with small suppliers and retailers.

High producer prices and profitability in recent years have created optimism among small farmers producing staple products, especially banana and tomato. However, high food prices can easily affect the local accessibility to healthy and nutritious food, with a consequent impact, for example, on the nutritional quality and on the occasion to alter the diet.

According to [45], the share of household spending on food and non-alcoholic drinks in the family budget in Santiago Island is around 27.7%. In this context, access to food is important for the well-being of families. For the staples foods studied, the sales prices in the retailers vary, being on average banana (1.71 €/kg), tomato (1.80 €/kg), and chicken (4.51 €/kg). However, the average salary in Cabo Verde (deductions and taxes applied) is about 224.80 €. This situation signals the need for local consumers to pay competitive prices. It is important to mention that these prices would be much higher if it did not include part of the production of small farms and small food businesses. The data show differences in access to food; the poorest communities are the ones that face the most problems in terms of food vulnerability, because they pay a higher price for essential food and have a low income compared to other urban communities.

The consumption of imported chicken is mainly due to consumer’s purchasing power. The very low meat price by regional importers is considered a threat to 98% of small farms and small food businesses. Processing is poorly developed and limited because of financial investment and the sense of opportunity, which is justified in general by the poor purchasing power of the population. For 90% of small farmers selling to the market and small food businesses, the tourism market outlines a crucial opportunity since is characterised by a strong purchasing power, as well as a relevant willingness to pay.

3.4.4. Market Organisation

Market organisation also plays a role in food security issues. However, market organisation in Santiago Island faces several constraints, coupled with the permanent threat of water shortages, poor logistic distribution from the field to the final consumer, poor national market access (irregular and uncertain inter-island transport), lack of knowledge of the dynamics and cyclical trends of the market, poor financing, and low investment. This scenario is compounded by post-harvest losses, which are mainly due to the lack of structures supporting marketing, such as packaging and processing centres, which will significantly reduce the internal availability of food. According to [30], the levels of losses can reach 24% to 45% throughout the value chain, mainly in commercialisation.

There are at higher national levels of agribusiness fairs organised by the State structures and lower levels that essentially access farmer’s markets (e.g., municipal markets built by municipal governments). The existence of these types of markets, especially in major urban centres, represents a strong outlet for agricultural products and the consequent maintenance of the production and distribution of small farms and small food businesses. The focus group indicated that solidarity purchasing groups or consumer cooperatives can be particularly relevant for farming production in Santiago Island.