CryptoNet: Using Auto-Regressive Multi-Layer Artificial Neural Networks to Predict Financial Time Series

Abstract

:1. Introduction

2. Related Work

3. Methods Used For Forecasting

3.1. Technical Analysis

3.2. Fundamental Analysis

3.3. Time Series Forecasting

3.4. Machine Learning in Stock Market

3.5. Neural Networks in Stock Market

3.6. CryptoNet

4. Architecture

4.1. Autoregressive Model

4.2. Neural Network Auto-Regressive Model

4.3. System Configuration

4.3.1. Outputs Neurons

4.3.2. Hidden Neurons

4.3.3. Input Neurons

4.3.4. Bias

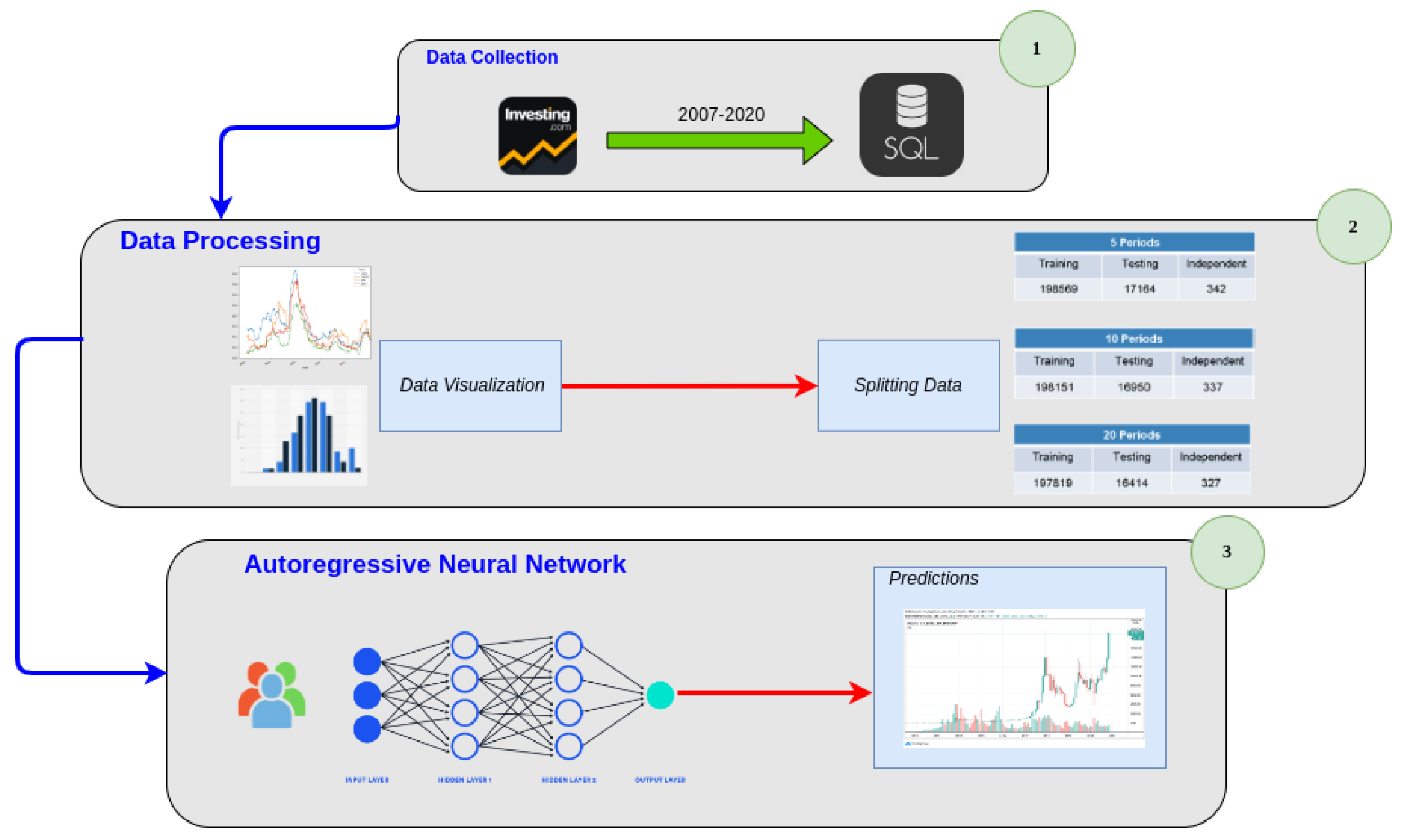

5. Experiments

5.1. Dataset

5.2. Learning Algorithm

5.3. Simulator Architecture

5.4. Proposed Configurations

6. Experimental Results and Discussions

6.1. Use-Case Example

6.2. Limitations

7. Conclusions and Future Work

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Dzikevičius, A.; Saranda, S.; Kravcionok, A. The accuracy of simple trading rules in stock markets. Econ. Manag. 2010, 15, 910–916. [Google Scholar]

- Desai, M.A.; Foley, C.F.; Forbes, K.J. Financial Constraints and Growth: Multinational and Local Firm Responses to Currency Depreciations. Rev. Financ. Stud. 2007, 21, 2857–2888. [Google Scholar] [CrossRef] [Green Version]

- Rapach, D.E.; Strauss, J.K.; Zhou, G. Out-of-Sample Equity Premium Prediction: Combination Forecasts and Links to the Real Economy. Rev. Financ. Stud. 2009, 23, 821–862. [Google Scholar] [CrossRef]

- Khaidem, L.; Saha, S.; Dey, S.R. Predicting the direction of stock market prices using random forest. arXiv 2016, arXiv:cs.LG/1605.00003. [Google Scholar]

- Kusuma, R.M.I.; Ho, T.T.; Kao, W.C.; Ou, Y.Y.; Hua, K.L. Using Deep Learning Neural Networks and Candlestick Chart Representation to Predict Stock Market. arXiv 2019, arXiv:q-fin.GN/1903.12258. [Google Scholar]

- Tsantekidis, A.; Passalis, N.; Toufa, A.S.; Saitas-Zarkias, K.; Chairistanidis, S.; Tefas, A. Price Trailing for Financial Trading Using Deep Reinforcement Learning. IEEE Trans. Neural Netw. Learn. Syst. 2021, 32, 2837–2846. [Google Scholar] [CrossRef] [PubMed]

- Fülöp, M.T.; Gubán, M.; Gubán, Á.; Avornicului, M. Application Research of Soft Computing Based on Machine Learning Production Scheduling. Processes 2022, 10, 520. [Google Scholar] [CrossRef]

- Rubi, M.; Chowdhury, S.; Abdul Rahman, A.A.; Meero, A.; Zayed, N.; Islam, K.M. Fitting Multi-Layer Feed Forward Neural Network and Autoregressive Integrated Moving Average for Dhaka Stock Exchange Price Predicting. Emerg. Sci. J. 2022, 6, 1046–1061. [Google Scholar] [CrossRef]

- Ranaldi, L.; Fallucchi, F.; Zanzotto, F.M. Dis-Cover AI Minds to Preserve Human Knowledge. Future Internet 2022, 14, 10. [Google Scholar] [CrossRef]

- Cunha, P.R.; Melo, P.; Sebastião, H. From Bitcoin to Central Bank Digital Currencies: Making Sense of the Digital Money Revolution. Future Internet 2021, 13, 165. [Google Scholar] [CrossRef]

- Schöneburg, E. Stock price prediction using neural networks: A project report. Neurocomputing 1990, 2, 17–27. [Google Scholar] [CrossRef]

- Patel, J.; Shah, S.; Thakkar, P.; Kotecha, K. Predicting stock and stock price index movement using Trend Deterministic Data Preparation and machine learning techniques. Expert Syst. Appl. 2015, 42, 259–268. [Google Scholar] [CrossRef]

- Sidekerskienė, T.; Woźniak, M.; Damaševičius, R. Nonnegative Matrix Factorization Based Decomposition for Time Series Modelling. In Computer Information Systems and Industrial Management; Saeed, K., Homenda, W., Chaki, R., Eds.; Springer International Publishing: Cham, Switzerland, 2017; pp. 604–613. [Google Scholar]

- Selvamuthu, D.; Kumar, V.; Mishra, A. Indian stock market prediction using artificial neural networks on tick data. Financ. Innov. 2019, 5, 16. [Google Scholar] [CrossRef]

- Moghaddam, A.H.; Moghaddam, M.H.; Esfandyari, M. Stock market index prediction using artificial neural network. J. Econ. Financ. Adm. Sci. 2016, 21, 89–93. [Google Scholar] [CrossRef] [Green Version]

- Devadoss, A.; Ligori, A. Forecasting of Stock Prices Using Multi Layer Perceptron. Int. J. Web Technol. 2013, 002, 52–58. [Google Scholar] [CrossRef]

- Behera, R.; Das, S.; Rath, S.; Misra, S.; Damaševičius, R. Comparative Study of Real Time Machine Learning Models for Stock Prediction through Streaming Data. J. Univers. Comput. Sci. 2020, 26, 1128–1147. [Google Scholar] [CrossRef]

- Abayomi-Alli, O.O.; Sidekerskienundefined, T.; Damaševičius, R.; Siłka, J.; Połap, D. Empirical Mode Decomposition Based Data Augmentation for Time Series Prediction Using NARX Network. In Proceedings of the Artificial Intelligence and Soft Computing: 19th International Conference, ICAISC 2020, Zakopane, Poland, 12–14 October 2020; Springer: Berlin/Heidelberg, Germany, 2020; pp. 702–711. [Google Scholar] [CrossRef]

- Jin, X. Do futures prices help forecast the spot price? J. Futur. Mark. 2017, 37, 1205–1225. [Google Scholar] [CrossRef] [Green Version]

- Box, G.; Jenkins, G.M. Time Series Analysis: Forecasting and Control; Palgrave Macmillan: London, UK, 1976. [Google Scholar]

- Huang, W.; Nakamori, Y.; Wang, S.Y. Forecasting stock market movement direction with support vector machine. Comput. Oper. Res. 2005, 32, 2513–2522. [Google Scholar] [CrossRef]

- Hyndman, R.; Athanasopoulos, G. Forecasting: Principles and Practice, 2nd ed.; OTexts: Melbourne, Australia, 2018. [Google Scholar]

- Heaton, J. The Number of Hidden Layers. Available online: https://www.heatonresearch.com/2017/06/01/hidden-layers.html (accessed on 28 October 2022).

- Ranaldi, L.; Fallucchi, F.; Santilli, A.; Zanzotto, F.M. KERMITviz: Visualizing Neural Network Activations on Syntactic Trees. In Metadata and Semantic Research; Garoufallou, E., Ovalle-Perandones, M.A., Vlachidis, A., Eds.; Springer International Publishing: Cham, Switzerland, 2022; pp. 139–147. [Google Scholar]

- Onorati, D.; Tommasino, P.; Ranaldi, L.; Fallucchi, F.; Zanzotto, F.M. Pat-in-the-Loop: Declarative Knowledge for Controlling Neural Networks. Future Internet 2020, 12, 218. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Bitcoin | Ether | |

|---|---|---|

| Nr. of simulating scenario | 1000 | 1000 |

| Nr. of future epochs (prediction) | 10 | 10 |

| Total epochs for training | 137 | 137 |

| Total epochs for test | 35 | 35 |

| Max value of the series () | 16.381 | 1125 |

| Min value of the series () | 1657 | 74 |

| Average value of the series () | 679 | 271 |

| Model | MAE BTC | MAE ETH | MAPE BTC | MAPE ETH |

|---|---|---|---|---|

| ARNN | 1.32573 | 72.85 | 7.672 | 9.325 |

| ARNN | 1.145 | 77.81 | 7.225 | 9.742 |

| ARNN | 1.435 | 73.91 | 7.974 | 10.045 |

| Linear Regression | 1.388 | 162.92 | 10.57 | 13.445 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ranaldi, L.; Gerardi, M.; Fallucchi, F. CryptoNet: Using Auto-Regressive Multi-Layer Artificial Neural Networks to Predict Financial Time Series. Information 2022, 13, 524. https://doi.org/10.3390/info13110524

Ranaldi L, Gerardi M, Fallucchi F. CryptoNet: Using Auto-Regressive Multi-Layer Artificial Neural Networks to Predict Financial Time Series. Information. 2022; 13(11):524. https://doi.org/10.3390/info13110524

Chicago/Turabian StyleRanaldi, Leonardo, Marco Gerardi, and Francesca Fallucchi. 2022. "CryptoNet: Using Auto-Regressive Multi-Layer Artificial Neural Networks to Predict Financial Time Series" Information 13, no. 11: 524. https://doi.org/10.3390/info13110524

APA StyleRanaldi, L., Gerardi, M., & Fallucchi, F. (2022). CryptoNet: Using Auto-Regressive Multi-Layer Artificial Neural Networks to Predict Financial Time Series. Information, 13(11), 524. https://doi.org/10.3390/info13110524