1. Introduction

With globalization of the world economy, expansion in capital transactions, and increased financialization of commodity markets, the network between stock, foreign exchange, and commodity markets has been strengthened. As a result, global investors have come to consider the returns and risks of these markets together when composing their portfolios. Similarly, policy makers trying to stabilize these financial markets must consider their linkages when designing and implementing policy. Thus, for global investors, financial hedgers, portfolio managers, and policy makers, a clear understanding of return and volatility spillover system and the causality between these financial markets is essential.

Although there is a wide body of research related to the above end-users’ needs, most preceding studies target and include only some of these financial markets. For this reason, prior studies only partially describe causal interrelationships and information transmission between these markets, but not the overall picture. Specifically, in studies analyzing spillover effects between these financial markets, research where the foreign exchange market is a focus in the analysis is limited. Most studies that have analyzed spillover effects of foreign exchange markets have examined the co-movement amongst major foreign exchange markets or information transmission between the foreign exchange and stock markets. Thus, there are few studies that can be used by foreign exchange market investors and policy makers to understand interdependence between the foreign exchange and other financial markets.

This study aims to identify the spillovers and nonlinear dependence between currency, commodity, and stock markets, and global risk factors. The latter factors relate to stock and oil market price shocks. More concretely, we investigate the spillover effects and nonlinear causal dependence between seven major currency markets, commodity market (oil and gold), the global stock market, and proxy variables for global risk factors in the form of volatility indices (OVX and VIX). For this purpose, we employ three main methodologies: multi-scale decomposition analysis, nonlinear Granger causality testing, and a directional spillover network approach. This three-stage approach allows identification of the series that make major contributions to spillovers, interdependence properties (linear or non-linear Granger causality), and spillover network characteristics at different time horizons.

The contributions of this study are four-fold. First, we focus on the role of currency markets to uncover return relationships amongst the various financial markets. Moreover, we explore the role of global risk factors in these relationships. Second, we identify these relationships by applying both spillover network and directional spillover index approaches, using the spillover network graph to understand the ‘big’ picture. Third, most prior studies analyze relationships between variables only in the time domain, whereas we employ multi-scale decomposition analysis to reveal these relationships at short, medium, and long horizons (i.e., time and frequency domains). This method allows us to have a more thorough understanding of the relationships. Fourth, most prior studies assume linear relationships between variables, whereas we extend the analysis to nonlinear causality between variables to better capture relationships.

Our main findings are summarized as follows. First, from the multi-scale decomposition analysis, we find that the Granger causality results and the direction and strength of return spillovers changes with decomposition level. Second, the results of nonlinear Granger causality tests identify significant variations in both the significance and direction of Granger causality relationships between the decomposed currency and other series at different timescales, especially for the decomposed oil, gold, and OVX series. Third, from the directional spillover indices, the EUR is determined as the largest contributor of connectedness to other series, followed by the CHF. Spillover network figures of the original series highlight the primary role played by the stock market as a net transmitter of return connectedness, and the strong impact it has on the AUD, CAD, and GBP currencies. The central role that the EUR plays within the network is also identified, with it being a net transmitter of connectedness to gold, oil, the GBP, JPY, and CHF. Finally, the EUR shows its highest magnitude of net transmission to stock prices for long horizons and to the gold price and CHF for short horizons.

The paper is organized as follows.

Section 2 reviews the related literature.

Section 3 describes the sample data.

Section 4 explains the methodology employed in this study.

Section 5 summarizes and explains the empirical results.

Section 6 provides conclusions.

2. Review of Related Literature

Globalization of markets and increases in international trade and capital flows have complicated the relationships between currency exchange rates and thus increased the importance of examining these relationships as a research topic. Most studies on this topic consider the return and volatility spillover relationships between major currencies’ exchange rates but have failed to reach consensus on their characteristics. Bubák et al. [

1] discover intra-regional volatility spillovers among the Central European (CE) currency markets and no significant spillovers from the EUR/USD to the CE currency markets. Antonakakis [

2] identifies significant return and volatility connectedness between major foreign exchange rates, which have been lower since the introduction of the euro. Sehgal et al. [

3] revealed the existence of return and volatility spillovers in exchange markets and that futures markets have an important influence on these spillovers. Sehgal et al. [

4] investigated the currency market interdependency among South Asian countries and found that there is not much co-movement in the currency market of this region. Salisu et al. [

5] provided statistical evidence to support return and volatility connectedness between major currencies. Kočenda and Moravcová [

6] identified that volatility transmission among EU currencies increases substantially during periods of distress. Huynh et al. [

7] provided evidence of asymmetric spillovers and connectedness amongst nine USDexchange rates, and that volatility spillovers are stronger than the return linkages.

Many early currency market studies have explored the linkage between currency exchange and stock markets in major economies. Amongst others, Aggarwal [

8] found that appreciation of the USD is positively correlated to U.S. stock returns, while Soenen and Hennigar [

9] identified a negative dependence between the value of the USD and sector market returns. However, Chow et al. [

10] identified a lack of relationship between the USD value and stock returns. Yang and Doong [

11] identified the asymmetric volatility linkage between currency exchange rates and stock prices of the G-7 countries.

Some studies devoted their focus to examining the linkage between currency exchange and stock markets in Asian countries. Pan et al. [

12] explored the connectedness between the two market prices for seven East Asian countries. They identify evidence of a causality from exchange rates to stock prices for most countries during the Asian crisis. Lin [

13] found the dependence from stock price shocks to the exchange rate, which is due to the capital account. Moore and Wang [

14] show that the trade balance is a major factor of the linkage in the emerging Asian markets. Jebran and Iqbal [

15] discovered bidirectional asymmetric volatility spillovers between the two markets.

More recently, this strand of literature extended to uncover the relationships between currency exchange rates and the prices of other diversifying assets such as precious metals and commodities. Amongst others, Bhar and Hammoudeh [

16] identified a positive dependence between silver and the exchange rate. Dimpfl and Peter [

17] revealed that oil and stock price volatilities are most influenced by the past volatility of gold and currency markets. Antonakakis et al. [

18] investigated dynamic conditional correlations among 14 implied volatility indices of some assets. Tian et al. [

19] determined that oil price shocks have a positive influence on the volatility of the USD/RMB exchange rate and Chinese stock prices.

Studies on the connectedness between the oil and stock markets are also related to our research. Although many studies have analyzed price and volatility transmission between these markets, no consensus has yet been reached. The empirical evidence in the literature on this relationship can be classified into four main strands as proposed by Zhu et al. [

20]. The papers in the first strand reveal the existence of a significantly negative dependence between the two market returns. This strand of literature is in line with Jones and Kaul [

21], Sadorsky [

22], and Ciner [

23]. Amongst others, Hammoudeh and Li [

24] found a negative bidirectional linkage between the two market indices. Basher and Sadorsky [

25], Chiou and Lee [

26], and Chen [

27], respectively, found strong evidence of the influence of oil price risk on stock market returns. The second strand in this categorization provides contradictory evidence in the form of positive interdependence between the two market returns. For example, El-Sharif et al. [

28] examined the linkage between the UK oil and gas sector equity prices. They found evidence that they are always linked positively. Watorek et al. [

29], Arouri and Rault [

30], and Luo and Qin [

31] also identified positive interlinkage between oil prices and stock prices of the U.S., Gulf Cooperation Council (GCC), and Chinese markets, respectively. Studies in the third strand displayed that oil price shocks have a significant influence on stock market returns, but whether the influence is positive or negative is related to various determinants [

32,

33,

34]. For example, Kilian and Park [

34] showed that the reaction of U.S. stock returns to an oil price shock can be positive or negative depending on the source of the oil shock. The final strand of studies demonstrates no significant linkage between the two markets [

35,

36,

37,

38,

39]. For example, Apergis and Miller [

37] identified that stock returns of developed countries do not react to oil market shocks. Al Janabi et al. [

39] discovered evidence no relationship between the oil and GCC stock markets.

Recently, some research explored the linkage between oil market uncertainty and stock returns [

31,

40,

41,

42,

43,

44]. Amongst others, Dutta [

41] revealed that there exists a long-run dependence between the implied volatility indexes of oil and the U.S. energy stock market. Mensi et al. [

44] revealed that OVX index impacts the predictability of stock prices in top oil-producing and oil-consuming countries.

Although the currency market is not included, there are studies that explore the connectedness between the oil price (and/or its volatility) and precious metal prices. For example, Ji and Fan [

45] revealed that the oil market volatility has spillover effects on non-energy commodity markets. Bouri et al. [

46] found evidence to support the presence of cointegration relationships and nonlinear causality amongst the oil, gold, and Indian stock markets. Alqahtani [

47] found that global gold volatility can transmit positive shocks to the UAE stock market and that the OVX and VIX can influence the GCC stock markets. Dutta et al. [

48] identified the presence of cointegration between oil and precious metal prices and nonlinear causality between oil and gold markets. Kang et al. [

49] discovered that the VIX has the strongest influence on the U.S. sector equity ETFs. Löwen et al. [

50] found Granger causality between VIX, GVZ, and OVX indices during the COVID-19 pandemic. Batrancea [

51] and Batrancea et al. [

52] showed the impact of fiscal pressure on the energy industry.

A review of the above studies raises the following crucially important questions: Does a stable relationship between currency and other markets exist? If so, what are the correct magnitude and sign of this linkage? If present, is the relationship constant or time-varying? In this study, we investigate the linkage between currency and other markets to address these questions.

5. Empirical Results

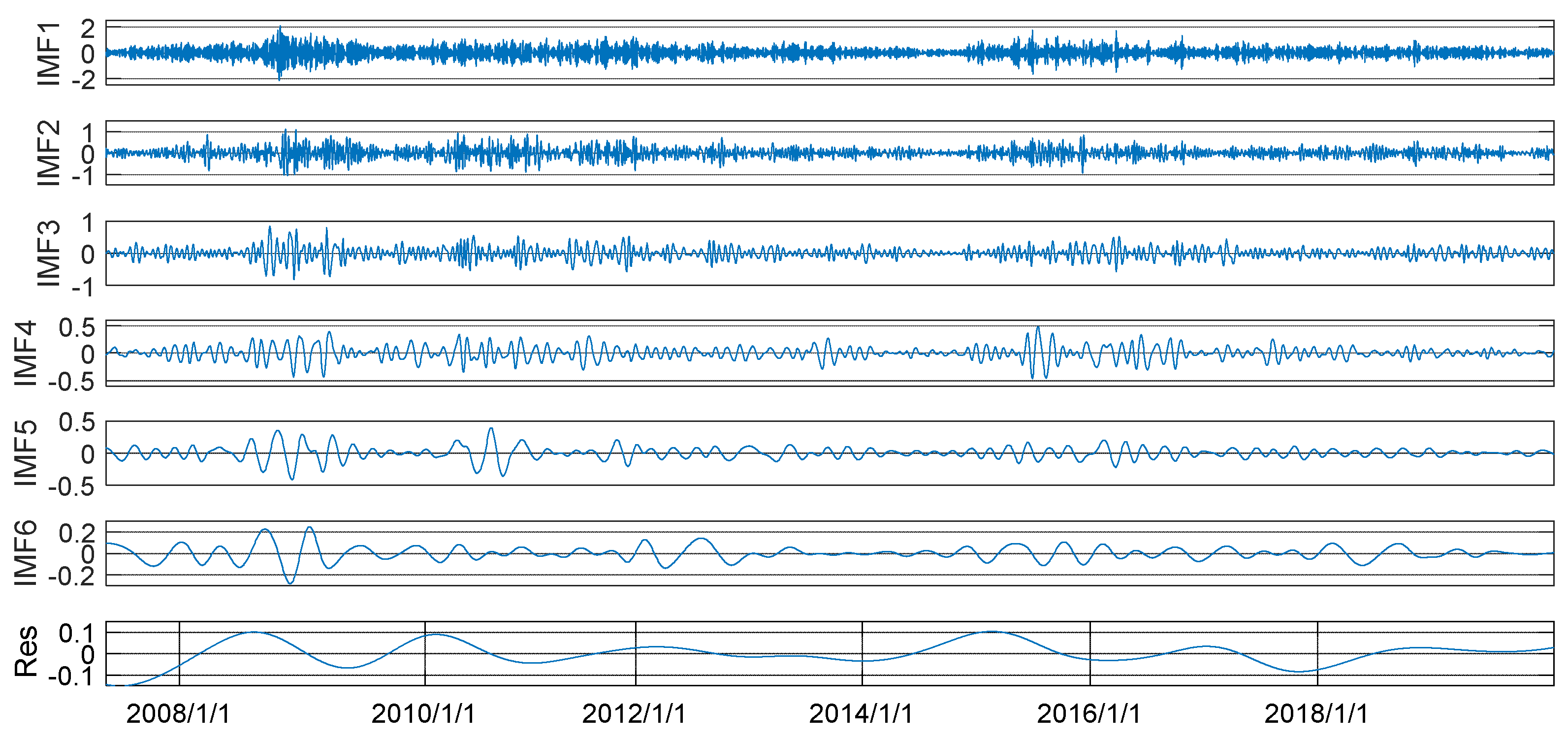

Figure 1 identifies the set of independent IMF associated with the daily returns for the EUR, illustrating the approach to timescale breakdown undertaken for each of the return/change series. IMF1 and IMF2 are associated with higher frequency, short-term timescale components. IMF3 and IMF4 are associated with medium-term timescale components, and IMF5 and IMF6 with lower frequency, longer-term timescale components. Finally, the residual (Res) identifies the underlying (moving) trend, or long-term deterministic component [

54], in the growth rate of the EUR exchange rate.

The decomposition shown in

Figure 1 allows identification of the dominance of short-term modes in generating variation in the observed data on EUR returns, with IMF1 having a range within −2 to 2, and that of IMF2 a range of just over −1 to 1. The medium-term and longer-term modes, and the residual, make a relatively smaller contribution to variability in the EUR return series. For example, the residual has a relatively small range, being within the range of −0.1 to 0.1, and thus makes a significantly smaller contribution to overall variability.

The conclusion that short-term modes dominate variation in the observed data on returns/changes is supported for each series by the data presented in

Table 2. Variances in IMF1 for each return/change series account for between 35.13 and 41.71% of the summed variances of the IMF and the residual, whereas the residual accounts for only 2.89–8.32% of this total variability. In the case of crude oil (OIL), our findings are different from those of Zhang et al. [

53], who suggest that longer-term modes, especially the residual, dominate in determining volatility. However, their result is based on the use of monthly data on the price level itself, and ending in the mid-2000s, rather than the more recent daily data on returns/changes used in this study. Our data covers a more recent and, potentially, volatile period, covering such events as the global financial crisis (GFC), European debt crisis (EDC), and the beginnings of the COVID-19 crisis periods. In the case of oil, our findings are consistent with those of Yu et al. [

61] who also use daily data.

Prior to assessing linear and nonlinear causality, the Phillips and Perron (PP) [

62] unit root test is performed to check the stationarity of the return/change series and the decomposed IMF components.

Table 3 displays the results of the PP unit root test. The test results determine rejection of the hypothesis in both the original and IMF return/change series. Thus, we conclude that all considered return/change series are stationary.

Table 4,

Table 5 and

Table 6 present results for both linear and nonlinear Granger causality tests on the original and (multi-scale) decomposed series. In each case, we test for causality and reverse causality between each of the currency exchange rate, and, respectively, the commodity, stock, and implied volatility index returns/changes.

Turning first to the results for the original return series in

Table 4. The comparison of the results of the linear and nonlinear causality tests is highly informative. The results of the nonlinear causality tests indicate a higher occurrence of reverse causality, with respect to commodity, stock, and implied volatility index returns/changes, for all currency returns except that of China’s Yuan (CNY). This likely reflects the capture of non-linearities for most of the currencies (EUR, GBP, AUD, CHF, JPY, and CAD) (e.g., Serletis et al. [

63]) and other assets, both individually and in the dynamic dependence structures between the original currency, and commodity, stock, and implied volatility index return/change series. In the case of the CNY, which displays limited evidence of Granger causality, China’s use of exchange rate targets, capital controls, and monetary policy interventions to sterilize foreign currency inflows, suggest that its exchange rate system is essentially a form of currency peg [

64]. This means that rather than being partly absorbed through shifts in the exchange rate, it will be reflected in shifts in both monetary and real variables (e.g., inflation and GDP growth).

Table 5 and

Table 6 provide similar information to that in

Table 4 but identify the distinct characteristics for Granger causality related to each of the different timescales associated with the six IMF modes determined for each return/change series.

Table 5 provides this information for the linear Granger causality test, while

Table 6 provides this information for the nonlinear test.

Like the results discussed for

Table 4, the nonlinear Granger causality tests (

Table 6) identify a greater number of causality and reverse-causality relationships between the decomposed currency

, and commodity, stock, and implied volatility index

return/change series, than is the case for the linear Granger causality tests (

Table 5). This identifies that, as with the original series, there are significant nonlinearities at each of the different modes, both individually and in the dynamic dependence structures. Again, as for the original returns, the CNY is associated with evidence of limited linear or nonlinear Granger causality relationships between its decomposed series and the decomposed series for the commodity, stock, and implied volatility index returns/changes. Exceptions relate mainly to the oil (OIL) and oil volatility (OVX) markets, with no evidence for the CNY series Granger-causing changes in the gold (GOLD) series as suggested in

Table 4.

Examination of the results presented in

Table 5 and

Table 6 highlight the significant variation in both the significance and direction of causality relationships between the decomposed currency, and commodity, stock, and implied volatility index returns/changes series at different timescales. This is most apparent for the oil, gold, and OVX decomposed series, with a decline in the number of significant causality and reverse causality relationships being identified at lower time-scales. In the case of oil, the number of decomposed currency series evidencing significant linear Granger causality from oil

to currency

declines, in general, at lower frequencies. This effect is, however, less clear when considering nonlinear Granger causality, with a higher number of currencies being identified as being impacted by oil at most timescales. A similar, but more obvious, pattern holds for gold. Although declining, the set of currencies to which this result applies varies by mode (IMF). For example, in the case of linear Granger causality, significance for the EUR is evident for IMF1, IMF2, IMF4, and IMF6, whereas for the JPY it is evident for IMF1, IMF3, IMF4, and IMF5. In the case of linear causality from currency

to oil

, the EUR appears to have a more important influence on oil at medium- and longer-term timescales, rather than at shorter-term timescales, with significant causality being identified at IMF3, IMF5, and IMF6. Again, a similar result holds for gold. Examination of the nonlinear Granger causality results support these conclusions for oil and gold.

However, in the case of the relationships between the decomposed series of exchange rate and the VIX, specifically, the results in

Table 6 suggest a lower prevalence of the VIX decomposed series, impacting the currencies’ decomposed series at intermediate timescales (IMF3 and IMF4). With respect to the decomposed series for the stock market, both the linear and nonlinear causality results, generally, show high levels of causality and reverse causality between the decomposed currency, and commodity and implied volatility index series across the different timescales, with the CNY being the exception currency. Overall, our results highlight the need to identify and understand the specific timescale that is applied in the Granger causality test, and whether linear or more complex nonlinear processes underlay these results. These will flow to the relationships likely to be identified in the spillover analysis that follows.

Table 7,

Table 8,

Table 9,

Table 10,

Table 11,

Table 12 and

Table 13 report the total static return connectedness index matrices across the currency, and commodity, stock, and implied volatility index series for both the original time series and for each of the different timescales. In

Table 7, the average value of the total return connectedness index is 32.66%, implying a moderate level of connectedness among the currency, and commodity, stock, and implied volatility index series. With respect to directional spillovers transmitted to other series (

), the EUR is determined as the largest average contributor of spillovers to the other series (73.48%), followed by the CHF (51.52%).

The EUR (59.48%) is the largest recipient of return spillovers, with an average contribution from other series (), followed by the AUD (56.47%) and CAD (53.85%). In the case of these currencies, especially the AUD, this result reflects a high level of sensitivity to trade and global financial market forces. In terms of net directional spillovers (), the stock market is the largest net transmitter of return spillovers, providing a net contribution of 37.52%, followed by the EUR (14.00%). The largest net recipients of return connectedness are the CAD and CNY, respectively, at −11.02 and −9.54%.

Table 8,

Table 9,

Table 10,

Table 11,

Table 12 and

Table 13 indicate that return spillovers between decomposed series are strongest at both the highest and lowest timescales, with IMF1 associated with the highest level of total return spillovers (25.75%) and IMF6 the next highest (24.71%). Total return spillovers decline in level from IMF1 to IMF5, with these being 18.98, 13.95, 9.56, and 5.92%, for IMF2–5, respectively. This contrasts with the general lessening in statistically significant causality at longer timescales observed for several of the decomposed series in

Table 5 and

Table 6.

Considering individual series, the pattern for total return spillovers identified above appears to hold for both return spillovers and other series. Thus, spillovers transmitted and received initially decline in level, then increase at the lowest timescale. Return spillovers “To others” and “From others” are generally highest for IMF1, with those for IMF6 being the next highest. The exception is for stock returns, where the lowest levels of spillovers and other series occur at IMF2 and IMF5, while the highest levels of spillovers and other series occur at IMF6.

Figure 2 presents the system-wide connectedness network based on the return spillover index data in

Table 8. The red (green) color of a node represents the net transmitter (recipient) of connectedness (i.e., the difference between

and

other series). The thickness of the lines and colors indicate the magnitude of the pairwise connectedness, while arrows identify the direction of net spillover.

Figure 2 shows the main role played by the global stock market as a net transmitter of return connectedness, and the strong impact it has, on average, on the AUD, CAD, GBP, and, to a lesser extent, the EUR and JPY. The central role that the EUR plays within the network, again on average, is also shown in

Figure 2, with it being a net transmitter of connectedness to gold, oil, the GBP, JPY, and CHF. The latter also plays a net transmitter role, especially with respect to the JPY. Although identified as net transmitters of connectedness, the magnitude of signals from the OVX and VIX is identified as being small.

Examination of

Figure 3 allows identification of important differences in net connectedness at the different timescales (modes IMF1 to IMF6) associated with each of the decomposed series. Specifically, the JPY is shown to be an overall weak net transmitter of connectedness for modes IMF2–6, exceptions being moderate net transmission to the stock market for mode IMF5, and a relatively high magnitude of net transmission to the OVX for mode IMF6. In the case of the EUR, its highest magnitude of net transmission is to the stock price for mode IMF6, to gold price for modes of IMF1 and IMF2, and to CHF for mode IMF1. Additionally, the AUD is shown to provide a low magnitude of net transmission at some timescales (IMF1, IMF3, and IMF6), with its major impact being on the CAD (IMF1, IMF3, and IMF6) and VIX (IMF3 and IMF6). Differences are also apparent with respect to the net connectedness characteristics of the decomposed series of the two implied volatility indexes. Specifically, the VIX is a net transmitter of connectedness for modes IMF1–4, the high-frequency and medium-frequency modes, while it is a net receiver for modes IMF5 and IMF6. However, the OVX is a net receiver of connectedness for modes IMF1–4, while it is a net transmitter only for IMF5 and IMF6, the lower-frequency modes. That noted, it is a moderate net transmitter to the VIX for modes IMF1 and IMF5, with stronger effects being observed for mode IMF6. These results highlight the importance of the volatility of the oil price for volatility in the stock market. Finally, both gold and the CNY, although net receivers of connectedness on average (

Figure 2), are shown to be low net transmitters of connectedness at longer timescales, IMF4 for the CNY, and IMF4 and IMF5 for gold.

6. Conclusions

The aim of this study was to explore the spillover and nonlinear interdependence between the major currency markets (CHF, JPY, AUD, CNY, CAD, EUR, and GBP), commodity markets (OIL and GOLD), stock market (MSCI ACWI), and global risk factors (OVX and VIX) due to stock and oil market price shocks. For this purpose, we used daily data spanning from 10 May 2007 to 31 January 2020 and employed three main methodologies: multi-scale decomposition analysis, nonlinear Granger causality testing, and a directional spillover network approach.

The main findings are summarized as follows. First, from the multi-scale decomposition analysis, we found that short-term modes (timescales) dominate variation in sample returns/changes for all series considered. We found that the Granger causality and the direction and strength of return spillovers change with the level of timescale decomposition. Second, the results of nonlinear Granger causality tests identify a greater number of bi-directional causality relationships between the decomposed currency and other asset return series than for the linear Granger causality tests. We find significant variation in both the significance and direction of Granger causality relationships between the decomposed currency and other series at different timescales, especially for the decomposed oil, gold, and OVX series. Third, from the measured directional spillover indices, the EUR is determined as the largest average contributor of connectedness to other series, followed by the CHF. Spillover network analysis of the original series demonstrates the primary role played by the stock market as a net transmitter of return connectedness, and the strong impact it has on the AUD, CAD, and GBP currencies. The central role that the EUR plays within the network is also identified, with it being a net transmitter of connectedness to gold, oil, GBP, JPY, and CHF. Although identified as net transmitters of connectedness, the magnitudes of signals from the OVX and VIX are found to be small. Finally, the EUR shows its highest magnitude of net transmission to the stock price at long horizons and to gold price and CHF at short horizons.

As this study focuses on the interdependence between key currency exchange rates and stock and commodity market returns, whose prices fluctuate frequently, our empirical results are important for enhancing portfolio performance, managing risk, and stabilizing financial markets. Thus, the interdependence between these markets, and their relationship with global risk factors, should be fully understood and closely monitored by relevant stakeholders. These include global investors, portfolio and risk managers, market analysts, and government and policy makers. In addition, more emphasis should be placed on the stability and sustainability of the overall financial system.

{kind=link}

{kind=link}

{kind=link}

{kind=link}