4.1. Scientific Production on Accounting Information Systems

Objective 1: How many articles specifically focused on Accounting Information Systems have been published and how has been their evolution?

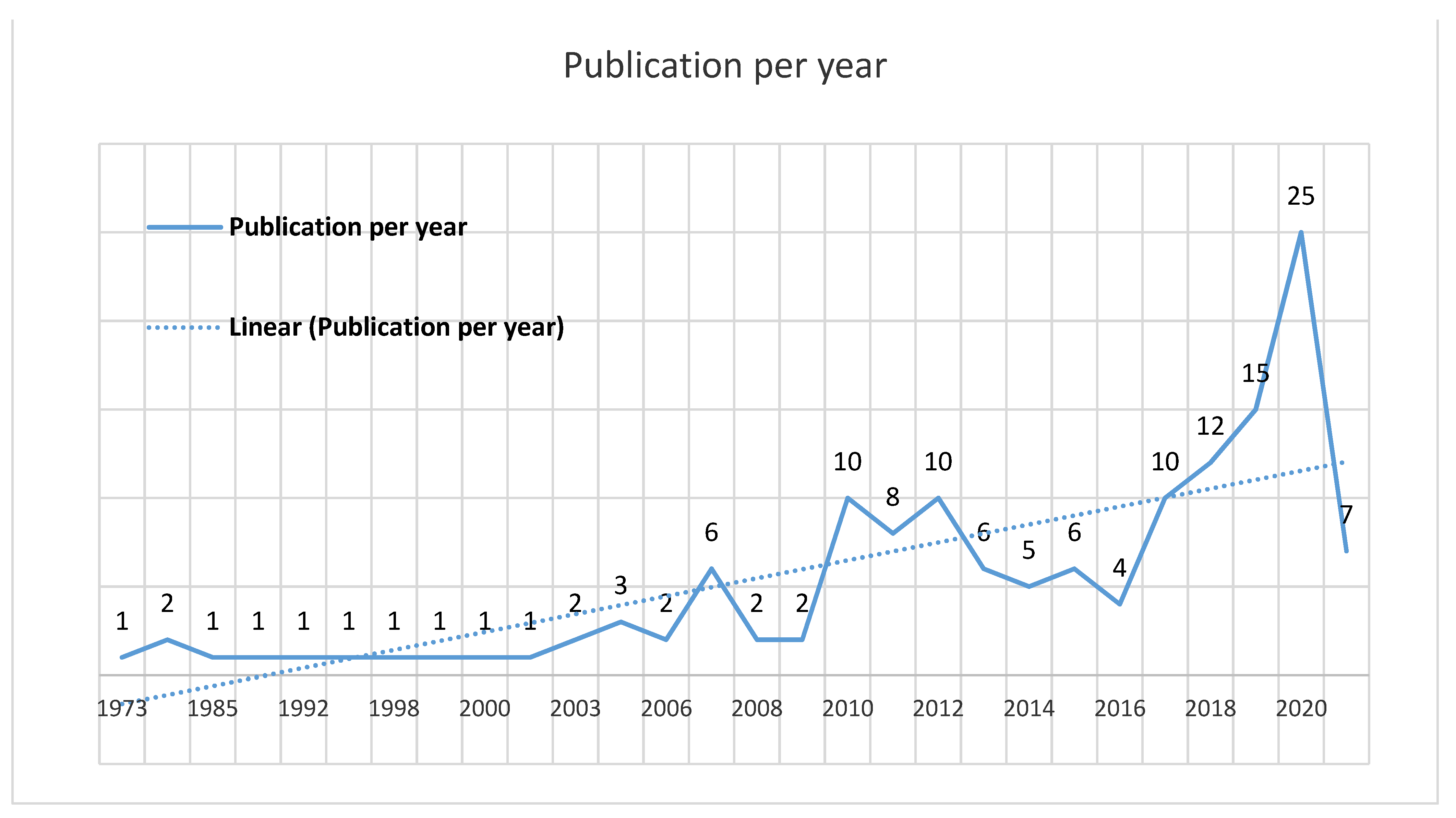

As we can see in

Figure 2, the first article published in this area in WoS database was in 1973 by Marshall titled “Determining an optimal Accounting Information System for an unidentified user”. The study´s objective was to formulate a decision model for the problem of determining an optimal system in training for an unidentified user and specify conditions that must be satisfied for an optimal system to exist [

36].

This research topic has been gaining space in researchers, however, until 2010 there was only an average of 1 article published per year on Accounting Information Systems. Since 2010 there has been a growing trend, with 2020 standing out as the year with fewest publications, and it is expected that 2021 equal or surpass 2020.

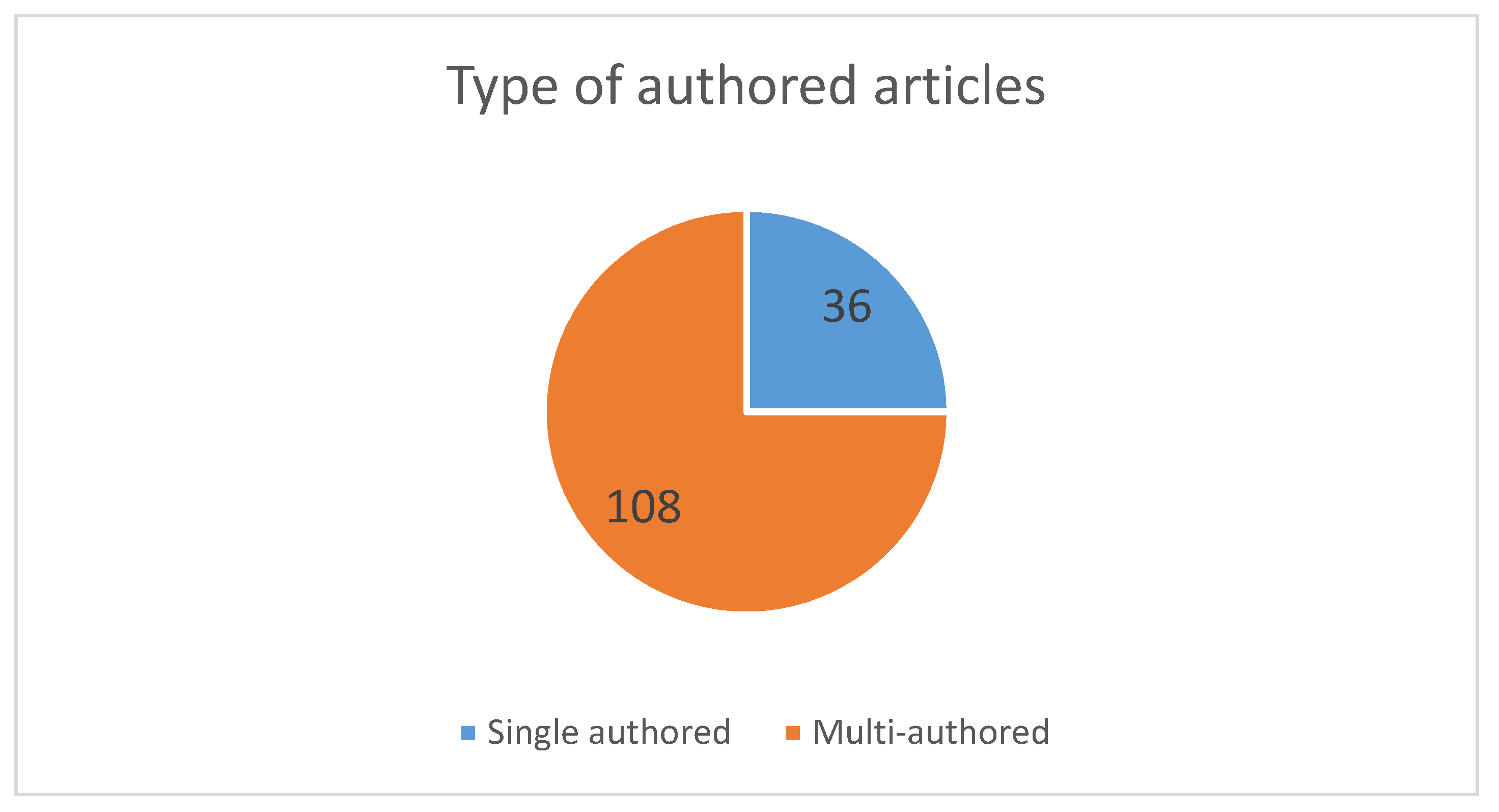

In addition, we verify that, of the 144 publications, only 25% (36) were produced by one author, 75% (108) were multi-authored.

Figure 3 presents the single and multi-authored publications.

Objective 2: Which journals, authors, countries/regions and organizations have more publications specifically focused on Accounting Information Systems, as well as the most frequent keywords?

In a total of 109 journals and according to

Table 1, the “Journal of Asian Finance Economics and Business” is the journal with more publications in the time period under study (6 publications), followed by the “International Journal of Accounting Information Systems”, with 5 publications, “Journal of Information Systems”, with 4 and “Global Business Review”, “Management Theory and Studies for Rural Business and Infrastructure” and “Pertanika Journal of Social Science and Humanities”, with 3 each. Other journals only have 2 or 1 publication in the timeline under study.

Table 1 presents the journals with 2 or more publications, as well as its 2019 impact factor.

For the calculation of h-index, the study sample of 144 articles on the subject of “accounting information systems” and the time base of 1973 to 15 May 2021, were considered. With a total of 322 authors, authors with more than two publications in the timeline under study are Povilas Domeika, Ilham Hidayah Napitupulu, Carmela Rizza, Daniela Ruggeri are the authors with more publications (3). The other 7 authors have published 2 articles.

Table 2 shows the publication per author.

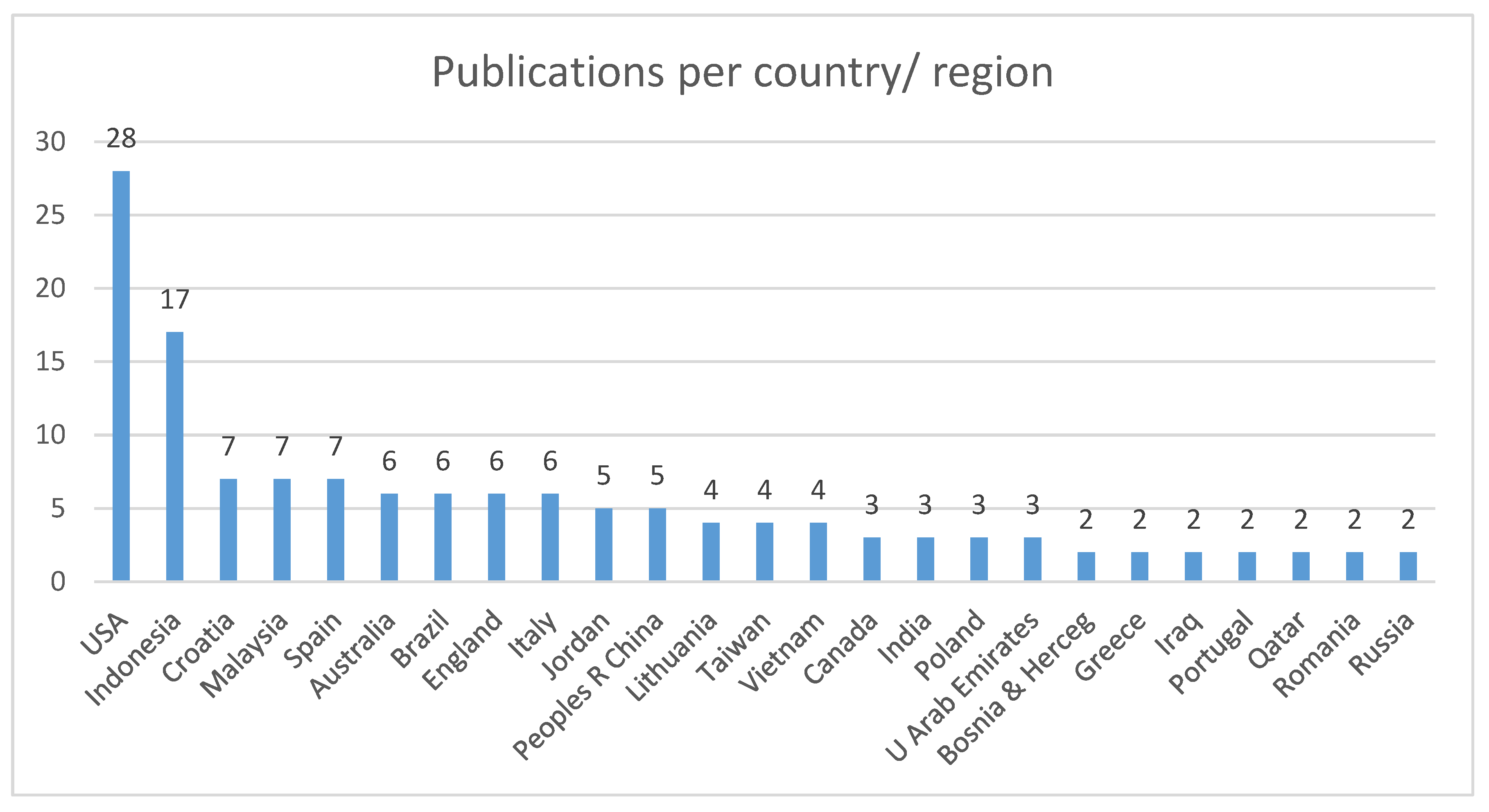

Figure 4 shows the countries/regions with more than 2 publications in the timeline under study. In a total of 57 countries/regions with publications on Accounting Information Systems, the United States of America (USA) is the region with most publications in the area, with 28 publications. The second most published country is Indonesia, with 17 publications, following Croatia, Malaysia and Spain with 7 and Australia, Brazil, England and Italy with 6. All other countries have less than 5 publications to date this research.

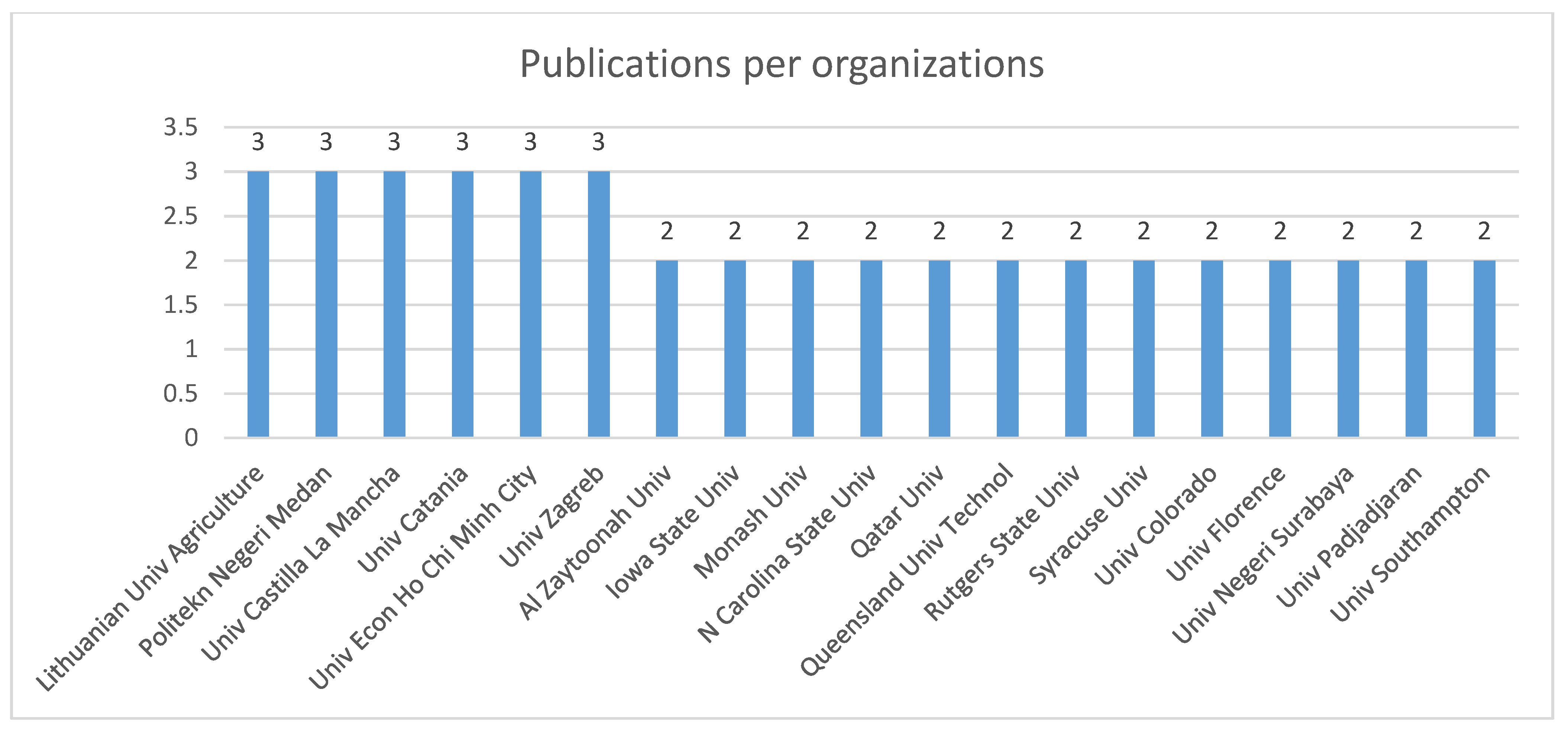

In a total of 213 organizations with publications on Accounting Information Systems, Lithuanian University of Agriculture, Politekn Negeri Medan, University Castilla La Mancha, University of Catania, University of Economics Ho Chi Minh City and University Zagreb stand out with 3 publications in timeline under study. This is followed by another 13 organizations with 2 publications as shown in

Figure 5.

The remaining 194 organizations have only published one article in the Accounting Information Systems area.

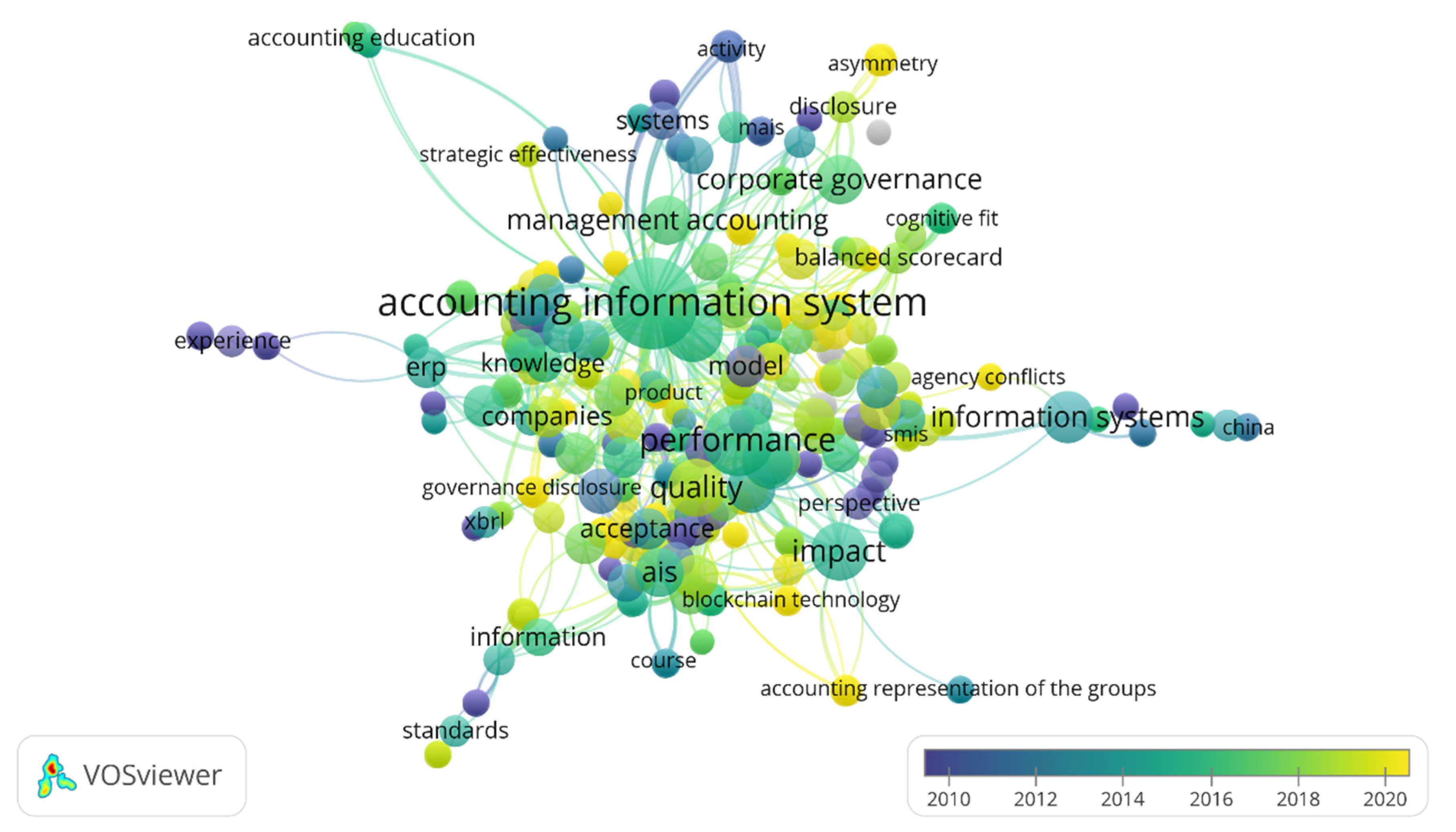

After analyzing the total keyword occurrence, we conclude that the most used keywords were “Accounting Information Systems”, Performance”, “Management Accounting” and “Information System”, as shown in

Figure 6. These keywords meet the research topics, representing research trends in the field of Accounting Information Systems.

In the last few years, the most used words have been “Balanced Scorecard”, “Asymmetry”, “Accounting”, “blockchain technology” and “Governance disclosure”.

4.2. Most Cited Publications, Sources, Authors, Organizations and Countries/Regions

Objective 3: Which articles, sources, authors, organizations and countries/regions are the most cited?

With a total of 144 articles, the article with highest number of citations, with a total of 168, belongs to Pacini et al. [

36]. In this paper, authors measured the environmental performance of farming systems through the application of an Accounting Information System.

The second most cited article, with 61 citations, belongs to Córcoles et al. [

37]. This article demonstrates the need for universities to include information on intellectual capital in their Accounting Information Systems.

In third place, with 47 citations, is Brazel and Agoglia [

38] article. Authors study investigated the quality effects of work provided by both computer assurance specialists and the expertise of Accounting Information Systems auditor on auditors’ planning judgments in a complex Accounting Information Systems environment.

In fifth place is Choe’s [

39] article, with 39 citations. The author, by surveying companies through a structured questionnaire, investigated the interactions between contextual variables (task uncertainty and organizational structure), information characteristics (scope, timeliness and aggregation) and participation of users in designing the Management Accounting Information System.

In sixth place is Chen’s [

40] study, with 34 citations. The author by developing an adapted web-based learning system proposes a design model for system designers to adapt the preferences linked to each cognitive style.

Masanet-Llodra’s [

41] work is in seventh place with 33 citations. The article conducts an in-depth study on environmental management systems developed in the ceramics sector. With one citation less (32) is Eldenburg et al. [

42] article. This study, also geared towards management accounting, the research examines physicians’ response to the implementation of an activity-based costing (ABC) system developed and designed with input from physicians.

The publications identified above have more than 30 citations The remaining articles have less than 30.

Table 3 shows the articles with more than 10 citations.

According to

Table 4, the most cited authors are Giesen, G; Huirne, R; Pacini, C; Vazzana, C and Wossink, A, with 168 citations. These authors belong to the most cited article entitled “Evaluation of sustainability of organic, integrated and conventional farming systems: a farm and field-scale analysis” [

36]. The most cited journal is “Agriculture Ecosystems & Environment”. The most cited organization is North Carolina State University, with 215 citations. The most cited region, also with the most publications in the area, is the USA, with 379 citations.

4.3. Research Topics and Trend

Objective 4: Which are the main research topics and trends in Accounting Information Systems?

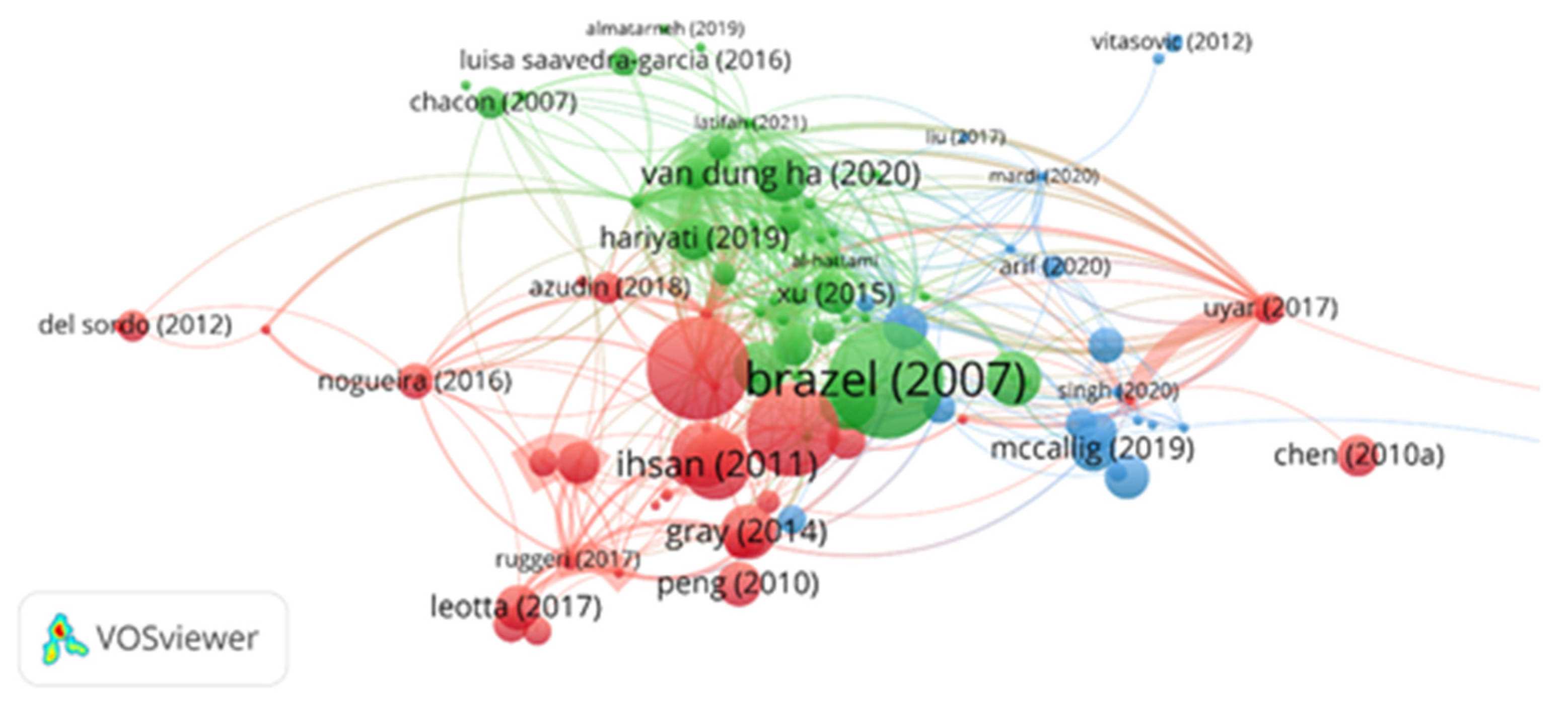

In the total of 144 articles, the software eliminated 35 articles because they had no link strength with the others. Form the 109 articles with more link strength, 44 are part of the first cluster (red), 41 are part of the second cluster (green) and 24 are part of the third cluster (blue). After bibliographic coupling through VOSviewer it was possible to verify 3 research topics, each topic with a different color represents a cluster and the lines represent the link strength between them as shown in

Figure 7.

We have identified that the main research topic will be in “research, behavior/experience/system requirements and trust relationship” (cluster red representing 40% of the total articles) and “the importance of organizational culture and management accounting and the effects for auditors, accountants, managers (decision-making), entities and countries” (cluster green representing 38% of the total articles) and “the importance of the internal control and the effects for the quality of financial information, skills development and business ethics” (cluster blue representing 22% of the total articles).

Table 5,

Table 6 and

Table 7 show the top 10 articles by topic. For each article, we present the title, journal, methodology, study objective, total citations and total link strength that indicates the number of publications in which two keywords occur together.

Regarding Cluster red - Research, behaviour/experience/system requirements and trust relationship, we find that this cluster includes studies focused on the investigation on Accounting Information Systems. Moreover, the interactions between contextual variables and information characteristics are critical to the development of accounting information system [

43].

This development, when successfully implemented in different types of companies, tends to generate improved financial performance [

15,

42]. Thus, literature shows that the implementation of accounting information systems, such as the “ABC” example, results in more efficient management and greater transparency and accountability [

42,

44]. The behaviour and experience of users, both individually and collectively, become critical to the successful implementation of accounting information system [

45]. This cluster also includes studies focused on the potential of accounting information systems to contribute to trusting relationships between the parties involved.

Table 5 shows the TOP 10 publications in this cluster.

Table 5.

Top 10 articles on subtopic research, behaviour/experience/system requirements and trust relationship.

Table 5.

Top 10 articles on subtopic research, behaviour/experience/system requirements and trust relationship.

| RO | Author/s (Year) | Title | Journal | Methodology | Objective | TLS |

|---|

| 1 | Choe (1998) [39] | The effects of user participation on the design of accounting information systems | Information & Management | Quantitative | This study investigated the interactions between contextual variables (task uncertainty and organizational structure), information characteristics (scope, timeliness and aggregation) and UP | 32 |

| 2 | Eldenburg, Soderstrom, Willis and Wu (2010) [42] | Behavioral changes following the collaborative development of an accounting information system | Accounting, Organizations and Society | Quantitative | Authors contribute to research on the influence of user participation on accounting system success, ABC system success and hospital accounting information systems. | 17 |

| 3 | Ihsan, SHHM Ibrahim–Humanomics (2011) [44] | WAQF accounting and management in Indonesian WAQF institutions: The cases of two WAQF foundations | Humanomics | Quantitative and qualitative | The purpose of this study is to examine accounting and management practices in two Indonesian WAQF institutions. It intends to seek evidence about how mutawallis discharge their accountability. | 1 |

| 4 | Hunton and Gibson (1999) [45] | Soliciting user-input during the development of an accounting information system: investigating the efficacy of group discussion | Accounting, Organizations and Society | Quantitative | This study reports the results of a longitudinal field experiment designed to examine the impact of group discussion when soliciting user requirements of an accounting information system | 22 |

| 5 | Gray, Chiu, Liu and Li (2014) [46] | The expert systems life cycle in AIS research: What does it mean for future AIS research? | International Journal of Accounting Information Systems | Quantitative | This paper explores the life cycle of expert systems research by accounting researchers in order to provide an overview of the role of accounting researchers in technology domains. | 6 |

| 6 | Woodward and Woodward (2001) [47] | The Efficacy of Action at a Distance as a Control Mechanism in the Construction Industry When a Trust Relationship Breaks Down: an Illustrative Case Study | British Journal of Management | Qualitative | A paper published by one of the authors (Woodward and Squires, 1996), described a situation where the accounting information system used by a geographically distant project manager to report the progress of a project to his headquarters proved inadequate for that task. The purpose of this paper is to analyze previously reported situation in the context of a perceived breakdown in the existing trust relationship between the project manager and his superior, the company’s general manager. | 39 |

| 7 | Mahama, Elbashir, Suttonc and Arnoldc (2016) [43] | A further interpretation of the relational agency of information systems: A research note | International Journal of Accounting Information Systems | Quantitative | This paper proposes a reinterpretation of the agency of information system as relational. | 27 |

| 8 | Lehman and Heagy (2008) [48] | Effects of Professional Experience and Group Interaction on Information Requested in Analyzing IT Cases | Journal of Education for Business | Quantitative | Authors investigated the effects of professional experience and group interaction on the information that information technology professionals and graduate accounting information system (AIS) students request when analyzing business cases related to information systems design and implementation. | 1 |

| 9 | Kostić, Jovanović and, Jurić, (2019) [49] | Cost Management at Higher Education Institutions–Cases of Bosnia and Herzegovina, Croatia and Slovenia | Central European Public Administration Review | Quantitative | The main aim of this paper is to overview the legal and organizational accounting systems’ characteristics focusing on external and internal reporting requirements and study the level of development and usage of cost accounting at HEIs in selected countries. | 2 |

| 10 | Kopel, Riegler, and Schneider, G (2020) [50] | Providing Managerial Accounting Information in the Presence of a Supplier | European Accounting Review | Quantitative | This paper identifies a novel effect which is crucial for the design of a management accounting information system. | 1 |

Table 6.

Top 10 articles on subtopic importance of organizational culture and management accounting and the effects for auditor accountants, managers, entities and countries.

Table 6.

Top 10 articles on subtopic importance of organizational culture and management accounting and the effects for auditor accountants, managers, entities and countries.

| RO | Author/s (Year) | Title | Journal | Methodology | Objective | TLS |

|---|

| 1 | Brazel and Agoglia (2007) [38] | An Examination of Auditor Planning Judgements in a Complex Accounting Information System Environment | Contemporary Accounting Research | Quantitative | The study investigates the effects of computer insurance specialist (CAS) and accounting information systems auditor (AIS) competence on auditor planning judgements in a complex AIS environment. | 8 |

| 2 | Chen, Huang, Chiu and Pai (2012) [40] | The ERP system impact on the role of accountants | Industrial Management & Data Systems | Quantitative | The purpose of this paper is to discuss the impact of an Enterprise Resources Planning (ERP) system on the role of accountants, to provide job qualifications for their reference. | 0 |

| 3 | Tarek, Mohamed and Hussain (2017) [51] | The implication of information technology on the audit profession in developing country: Extent of use and perceived importance | International Journal of Accounting & Information Management | Both quantitative and qualitative | This study aims to explore the impact of implementing Information Technologies on auditing profession in a developing country, namely, Egypt | 12 |

| 4 | Alewine, Allport and Shen (2016) [52] | How measurement framing and accounting information system evaluation mode influence environmental performance judgements | International Journal of Accounting Information Systems | Quantitative | This study introduces attribute framing to the General Evaluability Theory framework as important to consider when analyzing environmental decision differences across modes, because frames are often a necessary component of information presentation and different descriptions often lead to different decisions | 22 |

| 5 | Dobroszek, Zarzycka, Almasan and Circa (2019) [53] | Managers’ perception of the management accounting information system in transition countries | Economic Research-Ekonomska Istraživanja | Quantitative | This study aims to investigate managers perception from transition countries, as regards the management accounting information system. | 17 |

| 6 | Khadra, Al-Hayale and Al-Nasir (2012) [54] | Contingent Effects of System Development Life Cycle Critical Success Factors on Accounting Information System Effectiveness: Using Balance Scorecard Perspectives—Empirical Study Applied on the Jordanian Industrial Companies | International Journal of Information Technology Project Management | Quantitative | This study aims to explore the critical success factors that affect accounting information systems development fitness in Jordanian industrial companies. | 20 |

| 7 | Al-Hattami (2021) [55] | Validation of the D&M IS success model in the context of accounting information system of the banking sector in the least developed countries | Journal of Management Control | Quantitative | This study aims to validate D&M IS success model (for the first time) in the context of accounting information system (AIS) of the banking sector in the least developed countries, in this case Yemen. | 74 |

| 8 | Al-Dmour, Abood and Al-Dmour (2019) [56] | The implementation of SysTrust principles and criteria for assuring reliability of AIS: empirical study | International Journal of Accounting & Information Management | Quantitative | This study aims at investigating the extent of SysTrust’s framework (principles and criteria) as an internal control approach for assuring the reliability of Accounting Information System (AIS) were being implemented in Jordanian business organizations. | 19 |

| 9 | Alamin, Wilkin, Yeoh and Warren (2020) [57] | The Impact of Self-Efficacy on Accountants’ Behavioral Intention to Adopt and Use Accounting Information Systems | Journal of Information Systems | Quantitative | The study of Libyan accountants shows that in adopting a mandated technologically enabled accounting information system, they were influenced by a range of perceptional, dispositional and environmental factors. | 15 |

| 10 | HA (2020) [58] | Impact of Organizational Culture on the Accounting Information System and Operational Performance of Small and Medium-Sized Enterprises in Ho Chi Minh City | Journal of Asian Finance, Economics, and Business | Both qualitative and quantitative | This study focuses on determining the impacts of organizational culture on accounting information system and operational performance of small and medium-sized enterprises in Ho Chi Minh City. | 7 |

Regarding the Cluster green–the importance of organizational culture and management accounting and the effects for auditors, accountants, managers, entities and countries. Information technology applications, such as enterprise resource planning (ERP) systems, are significantly changing the ways companies operate their businesses and auditors perform their duties [

38,

51]. The implementation and use of accounting information systems can increase audit-related risks and therefore auditors must keep up with technological developments and expand their knowledge and competence [

38,

51]. In addition to auditors, accountants must also keep up with evolving technology for the proper pursuit of accounting activities in new contexts [

40]. The role of accountants in society thus becomes even more demanding [

40]. Considering that organizational culture influences company’s performance, the role of information makers and the role of decision-makers (managers) is of utmost importance for the implementation of accounting information systems [

52]. The accounting information system is an important source of information for management and decision making. This type of information is provided by accountants and used by managers operating in different organizations and economies [

53].

Table 6 shows the TOP 10 publications in this cluster.

The third cluster is Cluster blue-the importance of internal control and effects on the quality of financial information, skills development and business ethics.

Stakeholders, as technology evolves, tend to demand more information [

59]. Accounting information systems capture and process accounting data and provide valuable information to all stakeholders [

60]. However, in a rapidly changing environment, continuous information system management is necessary for organizations to optimize performance results [

60]. For good performance, the quality of accounting information is enhanced because the information in this system can be used by stakeholders who need credible information about the entity [

61]. The effect of the accounting information system implementation is thus influenced by the internal control system, and the competence of human resources on the quality of financial statements [

62].

Table 7 shows the TOP 10 publications in this cluster.

The presentation of the obtained clusters allows us to verify that both internal and external factors affect the accounting information system. Thus, theories of agency and contingency are of high importance because they interfere with the implementation of accounting information systems quality [

63]. When the implementation is successful, it has a significant impact on improving the organization or company performance [

5]. However, to achieve successful decision-making, accounting information must be of high quality, relevant and useful in the decision-making process [

6]. Thus, factors external to firms, their organizational culture, internal control and the role of managers, accountants and auditors are factors that condition the accounting information system.

The company external and internal environment is contingent on the proper application of the accounting information system, so it is necessary to take into account the different interests of different agents.

Furthermore, we found that the methodology used in most studies is quantitative.

Considering the most recent publications, suggestions for future investigation and most recently used keywords, we identified the following research trends: (1) the impact of Accounting Information System in organizations (performance, innovation, reorganization of activities, information reporting); (2) the Accounting Information System Construction, (3) the importance of implementation of the Accounting Information System in small and medium-sized enterprises and Public-Sector; and (4) the factors that contribute to Accounting Information System efficiency/quality.

On one hand, literature has highlighted the enhancement of firms’ performance with the implementation of this information system [

40,

41] however, its construction has been the subject of numerous debates in literature given the improvements in business environment [

19,

20]. Thus, the topic of Accounting Information System construction will always keep pace with the evolution of technology and the constant developments in the information system [

19].

In this context, our analysis points out as future research the topics Accounting Information System and organization performance and Accounting Information System Construction.

Table 7.

Top 10 articles on the internal control importance and effects on the quality of financial information, skills development and business ethics.

Table 7.

Top 10 articles on the internal control importance and effects on the quality of financial information, skills development and business ethics.

| RO | Author/s (Year) | Title | Journal | Methodology | Objective | TLS |

|---|

| 1 | Córcoles, Penalver and Ponce (2011) [37] | Intellectual capital in Spanish public universities: stakeholders’ information needs | Journal of Intellectual Capital | Qualitative | This paper aims to demonstrate the need for universities to include information on intellectual capital in their accounting information system. | 27 |

| 2 | Córcoles, Peñalver and Ponce (2012) [59] | Demanda de información sobre capital intelectual en las Universidades públicas españolas | Cuadernos de Gestión | Qualitative | This paper objective will be to demonstrate the need for universities to incorporate information on intellectual capital in their current accounting information system. | 28 |

| 3 | Prasad and Green (2015) [60] | Organizational Competencies and Dynamic Accounting Information System Capability: Impact on AIS Processes and Firm Performance | Journal of Information Systems | Quantitative | Using the dynamic capabilities framework (Teece 2007) it proposes that a dynamic AIS capability can be developed through the synergy of three competencies: having (1) a flexible AIS, (2) a complementary business intelligence system and (3) accounting professionals with IT technical competency. | 55 |

| 4 | McCallig, Robb and Rohde (2019) [7] | Establishing the representational faithfulness of financial accounting information using multiparty security, network analysis and a blockchain | International Journal of Accounting Information Systems | Quantitative | This paper aims to develop a design for an accounting information system that will enhance the representational faithfulness of financial reporting information. | 19 |

| 5 | Tan and Low (2019) [61] | Blockchain as the Database Engine in the Accounting System | Australian Accounting Review | Quantitative | This paper examines the prediction that blockchain technology will transform accounting and the profession because transactions recorded on a blockchain can be aggregated into financial statements and confirmed as true and accurate. | 3 |

| 6 | Sumaryati, Novitasari and Machmuddah (2020) [63] | Accounting Information System, Internal Control System, Human Resource Competency and Quality of Local Government Financial Statements in Indonesia | The Journal of Asian Finance, Economics, and Business | Quantitative | This study seeks to determine the effect of the application of accounting information system (AIS), internal control system and human resource (HR) competency on the quality of local government financial statements (FS). | 10 |

| 7 | Janvrin, Payne and Byrnes (2012) [62] | The Updated COSO Internal Control—Integrated Framework: Recommendations and Opportunities for Future Research | Journal of Information Systems | Qualitative | Authors review the updated Framework and discuss the comments we (as the Environmental Scanning Committee of the American Accounting Association’s Information Systems Section) offered COSO regarding how to improve the Framework. In addition, we identify research opportunities for accounting information system scholars related to the new Framework. | 12 |

| 8 | Burney, Radtke and Widener(2017) [64] | The Intersection of “Bad Apples,” “Bad Barrels,” and the Enabling Use of Performance Measurement Systems | Journal of Information Systems | Quantitative | The purpose of this study is to examine the intersection of AIS and business ethics by focusing on how a specific type of AIS is used; namely, the Performance Measurement Systems | 3 |

| 9 | Arif, Yucha, Setiawan, Oktarina andMuttaqiin (2020) [65] | Applications of Goods Mutation Control Form in Accounting Information System: A Case Study in Sumber Indah Perkasa Manufacturing, Indonesia | The Journal of Asian Finance, Economics and Business | Quantitative | This study analyzes the new GMCF method applied by the company to find out how the production of Accounting Information Systems (AIS) implemented by the company can be managed properly. | 5 |

| 10 | Alawaqleh (2021) [66] | The Effect of Internal Control on Employee Performance of Small and Medium-Sized Enterprises in Jordan: The Role of Accounting Information System | The Journal of Asian Finance, Economics and Business | Quantitative | This study explores the role of the Accounting Information System (AIS) in mediating the relationship between internal control and the performance of employees. | 15 |

4.4. Structural Knowledge Groups

Objective 5: Which structural knowledge groups can be identified based on the co-citations network between articles, sources and authors?

In a total of 5821 references, Claes Fornell and David F. Larcker study titled “Evaluating Structural Equation Models with Unobservable Variables and Measurement Error” was the most co-cited with a total of 10 citations and 38 from Total link strength that indicates the number of publications in which two keywords occur together. Fornell, C.; Larcker’s [

67] study examines the statistical tests used in the analysis of structural equation models with unobservable variables and measurement error. This indicates that studies in this area of research use the Structural Equation Model technique to analyze the unobserved statistical correlation variable.

The second place with 9 citations belongs to Otley [

68] study. Otley [

68] addressed contingency theories of management accounting by surveying the development and content of these theories. In this way, they presented an improved model, based on ideas of organizational control and effectiveness, which suggests appropriate directions for future work that will be both perceptive and cumulative.

In third place with 8 citations is DeLone and LcLean’s [

69] study. Their study identified 43 specific variables posed to influence different dimensions of IS success and organized these success factors into five categories based on the Leavitt Diamond of Organizational Change: task characteristics, user characteristics, social characteristics, project characteristics and organizational characteristics.

Table 8 presents the TOP 10 most co-cited references ordered by total citations.

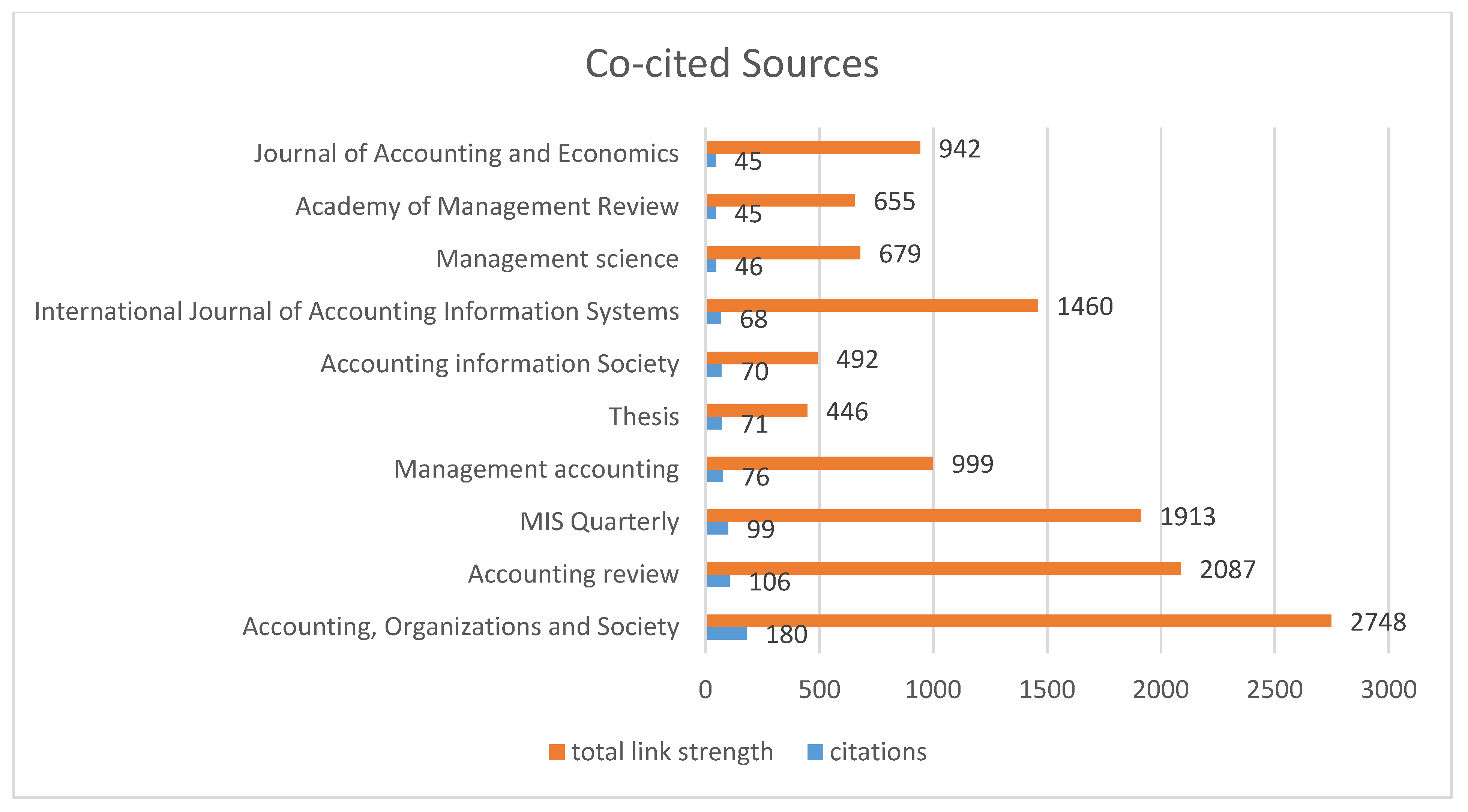

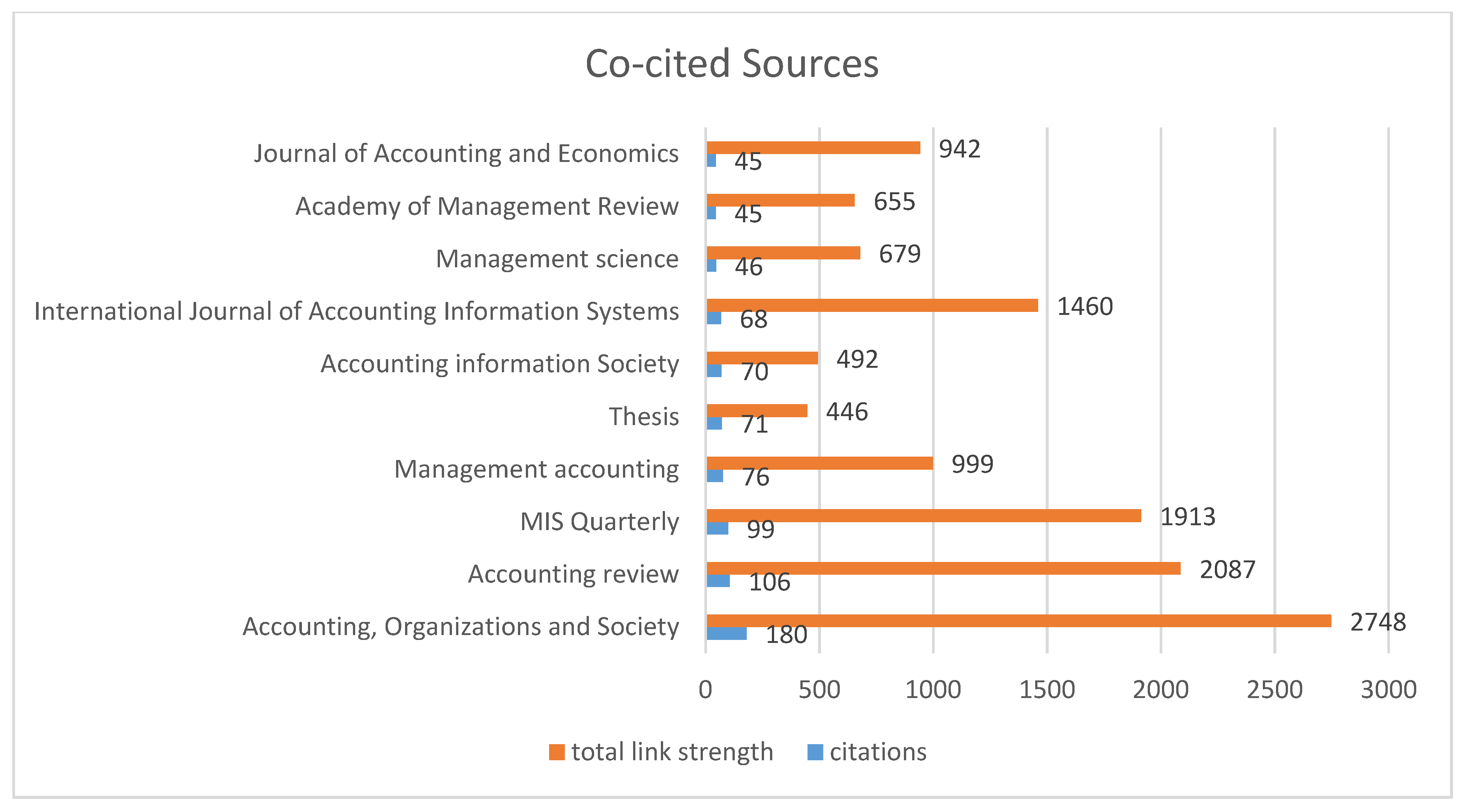

Out of a total of 3034 co-cited journals, the journal that stands out the most is Accounting Organizations and Society with 180 citations and 2748 Total link strength that indicates the number of publications in which two keywords occur together.

Figure 8 represents the most co-cited journals.

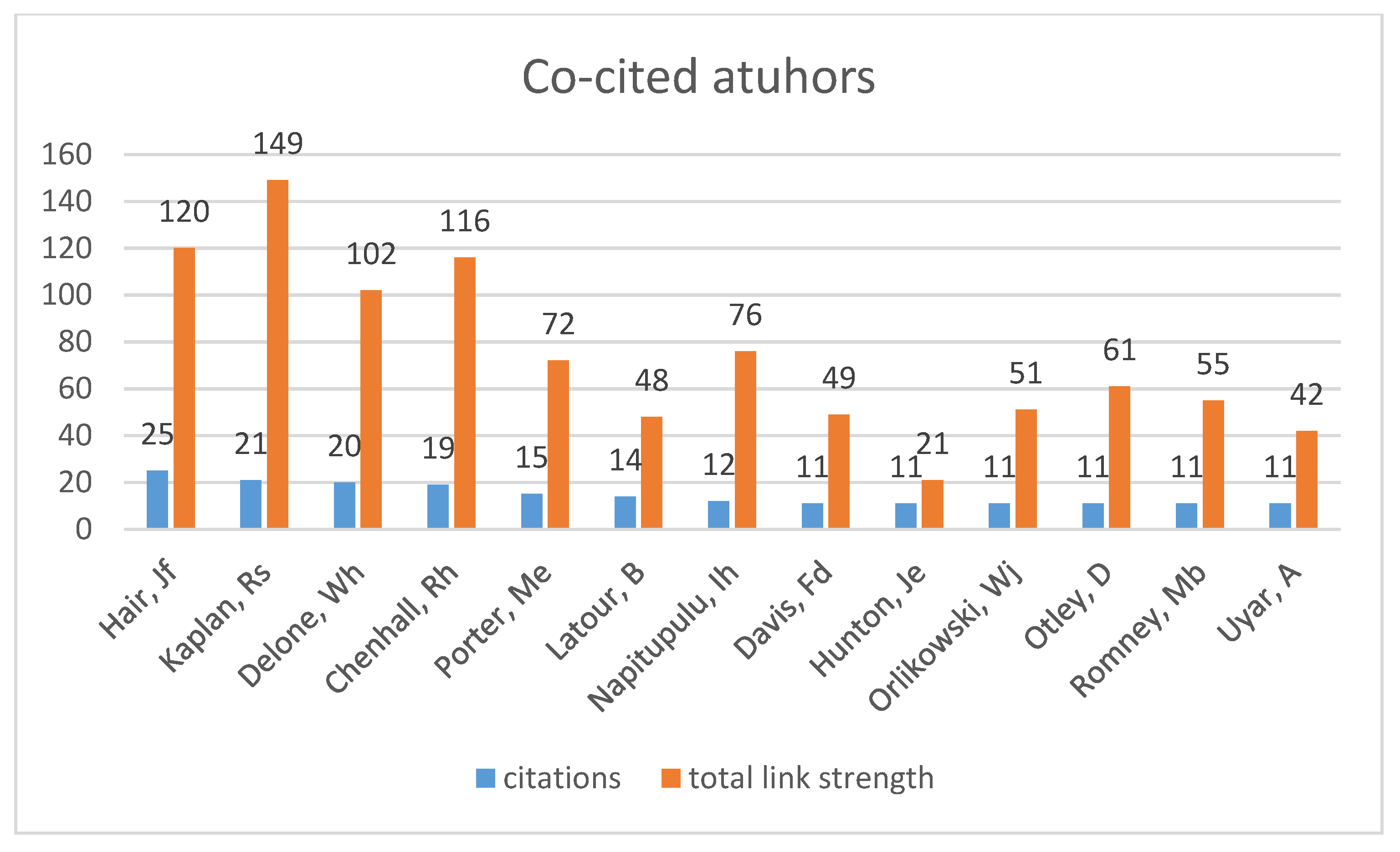

Finally, out of a total of 4575 co-cited authors Hair, JF stands out with 25 citations and 120 Total link strength who indicates the number of publications in which two keywords occur together.

Figure 9 highlights the most co-cited authors.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}