Portuguese Wood Pellets Market: Organization, Production and Consumption Analysis

Abstract

:1. Introduction

2. Materials and Methods

2.1. Framework

2.2. Collection of Information and Sampling Products Available on the Market

2.3. Survey Conducted with Consumers

2.4. Survey for Wood Pellets Manufacturers and Distributors

3. Literature Review

4. Results and Discussion

4.1. Products Available in the Domestic Market

4.2. Characterization of Wood Pellet Consumption

4.3. Wood Pellet Producers

4.4. Market Analysis

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Bang, G. Energy security and climate change concerns: Triggers for energy policy change in the United States? Energy Policy 2010, 38, 1645–1653. [Google Scholar] [CrossRef]

- Bilen, K.; Ozyurt, O.; Bakırcı, K.; Karslı, S.; Erdogan, S.; Yılmaz, M.; Comaklı, O. Energy production, consumption, and environmental pollution for sustainable development: A case study in Turkey. Renew. Sustain. Energy Rev. 2008, 12, 1529–1561. [Google Scholar] [CrossRef]

- Balat, M.; Ayar, G. Biomass energy in the world, use of biomass and potential trends. Energy Sour. 2005, 27, 931–940. [Google Scholar] [CrossRef]

- Bildirici, M.E. Economic growth and biomass energy. Biomass Bioenergy 2013, 50, 19–24. [Google Scholar] [CrossRef]

- Field, C.B.; Campbell, J.E.; Lobell, D.B. Biomass energy: The scale of the potential resource. Trends Ecol. Evol. 2008, 23, 65–72. [Google Scholar] [CrossRef] [PubMed]

- Kopetz, H. Build a biomass energy market. Nature 2013, 494, 29–31. [Google Scholar] [CrossRef] [PubMed]

- Searcy, E.; Flynn, P.; Ghafoori, E.; Kumar, A. The relative cost of biomass energy transport. Appl. Biochem. Biotechnol. 2007, 137, 639–652. [Google Scholar] [PubMed]

- Herbert, G.J.; Krishnan, A.U. Quantifying environmental performance of biomass energy. Renew. Sustain. Energy Rev. 2016, 59, 292–308. [Google Scholar] [CrossRef]

- Hohenstein, W.G.; Wright, L.L. Biomass energy production in the United States: An overview. Biomass Bioenergy 1994, 6, 161–173. [Google Scholar] [CrossRef]

- Hall, D.O. Biomass energy. Energy Policy 1991, 19, 711–737. [Google Scholar] [CrossRef]

- Jåstad, E.O.; Bolkesjø, T.F.; Trømborg, E.; Rørstad, P.K. The role of woody biomass for reduction of fossil GHG emissions in the future North European energy sector. Appl. Energy 2020, 274, 115360. [Google Scholar] [CrossRef]

- Dominković, D.F.; Bačeković, I.; Ćosić, B.; Krajačić, G.; Pukšec, T.; Duić, N.; Markovska, N. Zero carbon energy system of South East Europe in 2050. Appl. Energy 2016, 184, 1517–1528. [Google Scholar] [CrossRef] [Green Version]

- Nunes, L.; Matias, J.; Catalão, J. A review on torrefied biomass pellets as a sustainable alternative to coal in power generation. Renew. Sustain. Energy Rev. 2014, 40, 153–160. [Google Scholar] [CrossRef]

- Ilieva, J.; Baron, S.; Healey, N.M. Online surveys in marketing research. Int. J. Mark. Res. 2002, 44, 1–14. [Google Scholar] [CrossRef]

- Van Selm, M.; Jankowski, N.W. Conducting online surveys. Qual. Quant. 2006, 40, 435–456. [Google Scholar] [CrossRef]

- Lefever, S.; Dal, M.; Matthíasdóttir, Á. Online data collection in academic research: Advantages and limitations. Br. J. Educ. Technol. 2007, 38, 574–582. [Google Scholar] [CrossRef]

- Keusch, F. Why do people participate in Web surveys? Applying survey participation theory to Internet survey data collection. Manag. Rev. Q. 2015, 65, 183–216. [Google Scholar]

- Mellis, A.M.; Bickel, W.K. Mechanical Turk data collection in addiction research: Utility, concerns and best practices. Addiction 2020, 115, 1960–1968. [Google Scholar] [CrossRef] [PubMed]

- Dillman, D.A. Mail and Internet Surveys: The Tailored Design Method—2007 Update with New Internet, Visual, and Mixed-Mode Guide; John Wiley & Sons: Hoboken, NJ, USA, 2011. [Google Scholar]

- Swietochowski, A.; Dabrowska, M.; Lisowski, A. Friction properties of pellets made of wood and straw. Eng. Rural Dev. 2018. [Google Scholar] [CrossRef]

- Maliga, G.; Patil, A. The aspects of combustion and co-combustion biomass. Nat. Gas 1824, 228, 33. [Google Scholar]

- Ahn, Y.; Chen, Y.; Chen, H.; Helm, R.; Nelson, E.; Shields, K.; Stringer, R.; Bailie, R. Research and Evaluation of Biomass Resources/Conversion/Utilization Systems (Market/Experimental Analysis for Development of a Data Base for a Fuels from Biomass Model); Quarterly Technical Progress Report; 1 November 1979–31 January 1980; Gilbert Associates, Inc.: Reading, PA, USA, 1980. [Google Scholar]

- Hathaway, S.A.; Lin, J.; Mahon, D.; Magrino, T.; Duster, K. Densified Biomass as an Alternative Army Heating and Power Plant Fuel; Construction Engineering Research Lab (Army): Champaign, IL, USA, 1980. [Google Scholar]

- Haase, S. The Program. Wood Pellet Manufacturing in Colorado: An Opportunity Analysis: Final Report. 1993. Available online: https://books.google.com/books?id=-Ec_AAAAMAAJ&printsec=frontcover#v=onepage&q&f=false (accessed on 18 October 2021).

- Bentzen, J.; Smith, V.; Dilling-Hansen, M. Sustainable Energy Supply in Rural Areas: Availability and Competitivity in the Danish Wood Pellet Branch; Bruun og Soerensen Energiteknik A/S: Aarhus, Denmark, 1996. [Google Scholar]

- Aruna, P.; Laarman, J.G.; Araman, P.A.; Cubbage, F. An analysis of wood pellets for export: A case study of Sweden as an importer. For. Prod. J. 1997, 47, 49–52. [Google Scholar]

- Hillring, B.; Vinterback, J. Wood pellets in the Swedish residential market. For. Prod. J. 1998, 48, 67. [Google Scholar]

- Hillring, B. Regional prices in the Swedish wood-fuel market. Energy 1999, 24, 811–821. [Google Scholar] [CrossRef]

- Hillring, B. The Swedish wood fuel market. Renew. Energy 1999, 16, 1031–1036. [Google Scholar] [CrossRef]

- Hugues, J. The pellet stoves market in USA. Bois Energ. 1999. [Google Scholar]

- Roos, A.; Graham, R.L.; Hektor, B.; Rakos, C. Critical factors to bioenergy implementation. Biomass Bioenergy 1999, 17, 113–126. [Google Scholar] [CrossRef]

- Vinterbäck, J. Wood Pellet Use in Sweden: A Systems Approach to the Residential Sector. Ph.D. Thesis, Deptartment of Forest Management and Products, Swedish University of Agricultural Sciences, Uppsala, Sweden, 2000. [Google Scholar]

- Cotton, R.; Giffard, A. Introducing Wood Pellet Fuel to the UK; Renewable Heat and Power Ltd.: Crown, UK, 2001. [Google Scholar]

- Alakangas, E.; Paju, P. Wood Pellets in Finland—Technology, Economy and Market; OPET Report 5; OPET Finland: Helsinki, Finland, 2002. [Google Scholar]

- Madlener, R.; Gustavsson, L. Socio-Economics of the Diffusion of Innovative Bioenergy Technologies: The Case of Small Pellet Heating Systems in Austria. Soc.-Econ. Asp. Bioenergy Syst. 2003. [Google Scholar]

- Kaygusuz, K.; Türker, M. Biomass energy potential in Turkey. Renew. Energy 2002, 26, 661–678. [Google Scholar] [CrossRef]

- Mölder, A. Heating System Analysis in Jogeva District, Estonia. 2003. Available online: https://www.theseus.fi/bitstream/handle/10024/20539/aino_nro1.pdf?sequence=3&isAllowed=y (accessed on 18 October 2021).

- Bartolelli, V.; Cantarella, M.; Caserta, G.; Viparelli, P. European Bioenergy Networks Biomass; Country Report of ITALY; ITABIA: Roma, Italy.

- Aleksandrova, N.B. Characteristics of Creation of the Wood Pellets Market in Russia. J. Sib. Fed. Univ. Humanit. Soc. Sci. 2008, 1, 443–454. [Google Scholar]

- Wang, C.; Yan, J. Feasibility analysis of wood pellets production and utilization in China as a substitute for coal. Int. J. Green Energy 2005, 2, 91–107. [Google Scholar] [CrossRef]

- Yagi, K.; Nakata, T. Economics and a policy option on wood pellet fuel in Japan. J. Jpn. Inst. Energy 2006, 85, 451–460. [Google Scholar] [CrossRef]

- Tarasov, D. Wood Pellet Markets in Russia. 2009. Available online: https://insurance.cms-lists.org/host-https-lutpub.lut.fi/handle/10024/45518 (accessed on 18 October 2021).

- Rakitova, O.; Ovsyanko, A.; Sikkema, R.; Junginger, M. Wood Pellets Production and Trade in Russia, Belarus & Ukraine; Pelletsatlas: Market Research Report WP; 2009; Available online: https://www.researchgate.net/publication/273256481_Wood_Pellets_Production_and_Trade_in_Russia_Belarus_Ukraine (accessed on 18 October 2021).

- Mikołajczak, E. The analysis of pellet market in Poland. Ann. Wars. Univ. Life Sci.-SGGW For. Wood Technol. 2009, 69, 65–70. [Google Scholar]

- Pigaht, M.; Janssen, R.; Passalacqua, F.; Zaetta, C.; Grassi, G.; Sandovar, A.; Vegas, L.; Tsoutsos, T.; Karapanagiotis, N.; Fjällström, T. Pellets in Southern Europe—New Resources, New Products, New Markets. 2004. Available online: http://www.cres.gr/pellets/index_files/pdf/Paper_2004_01_29%20wip-munich%20de.pdf (accessed on 18 October 2021).

- Passalacqua, F.; Zaetta, C. Pellets in Southern Europe. The state of the art of pellets utilisation in Southern Europe. New perspectives of pellets from agri-residues. In Proceedings of the Proceedings of the 2nd World Conference on Biomass for Energy, Industry and Climate Protection, Rome, Italy, 10–14 May 2004. [Google Scholar]

- Laschi, A.; Marchi, E.; González-García, S. Environmental performance of wood pellets’ production through life cycle analysis. Energy 2016, 103, 469–480. [Google Scholar] [CrossRef]

- Smith, T.P.; Junginger, H.M. Analysis of the global production location dynamics in the industrial wood pellet market: An MCDA approach. Biofuels Bioprod. Biorefin. 2011, 5, 533–547. [Google Scholar] [CrossRef]

- Sjølie, H.K.; Solberg, B. Greenhouse gas emission impacts of use of Norwegian wood pellets: A sensitivity analysis. Environ. Sci. Policy 2011, 14, 1028–1040. [Google Scholar] [CrossRef]

- Xian, H.; Colson, G.; Mei, B.; Wetzstein, M.E. Co-firing coal with wood pellets for US electricity generation: A real options analysis. Energy Policy 2015, 81, 106–116. [Google Scholar] [CrossRef]

- Monteiro, E.; Mantha, V.; Rouboa, A. The feasibility of biomass pellets production in Portugal. Energy Sour. Part B Econ. Plan. Policy 2013, 8, 28–34. [Google Scholar] [CrossRef]

- Monteiro, E.; Mantha, V.; Rouboa, A. Portuguese pellets market: Analysis of the production and utilization constrains. Energy Policy 2012, 42, 129–135. [Google Scholar] [CrossRef]

- Nunes, L.; Matias, J.; Catalão, J.P. Economic and sustainability comparative study of wood pellets production in Portugal, Germany and Sweden. In Proceedings of the International Conference on Renewable Energies and Power Quality, Cordoba, Spain, 8–10 April 2014; pp. 526–531. [Google Scholar]

- Nunes, L.; Matias, J.C.; Catalao, J.P. Wood pellets as a sustainable energy alternative in Portugal. Renew. Energy 2016, 85, 1011–1016. [Google Scholar] [CrossRef]

- Lopes, S.I.; Nunes, L.J.; Curado, A. Designing an Indoor Radon Risk Exposure Indicator (IRREI): An Evaluation Tool for Risk Management and Communication in the IoT Age. Int. J. Environ. Res. Public Health 2021, 18, 7907. [Google Scholar] [CrossRef] [PubMed]

- Nunes, L.J.; Matias, J.C.; Catalao, J.P. Application of biomass for the production of energy in the Portuguese textile industry. In Proceedings of the 2013 International Conference on Renewable Energy Research and Applications (ICRERA), Madrid, Spain, 20–23 October 2013; pp. 336–341. [Google Scholar]

- Nunes, L.; Matias, J.; Catalão, J. Analysis of the use of biomass as an energy alternative for the Portuguese textile dyeing industry. Energy 2015, 84, 503–508. [Google Scholar] [CrossRef]

- Nunes, L.J.; Godina, R.; Matias, J.C.; Catalão, J.P. Economic and environmental benefits of using textile waste for the production of thermal energy. J. Clean. Prod. 2018, 171, 1353–1360. [Google Scholar] [CrossRef]

- Nunes, L.J.R.; Godina, R.; Matias, J.C.d.O. Technological innovation in biomass energy for the sustainable growth of textile industry. Sustainability 2019, 11, 528. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Questions | Possible Answers | ||

|---|---|---|---|

| 1. | Location | 1.1. | Answer in full |

| 2. | Ever heard of wood pellets? | 2.1. | Yes |

| 2.2. | No | ||

| 3. | Do you use wood pellets? | 3.1. | Yes |

| 3.2. | No | ||

| Questions | Possible Answers | ||

|---|---|---|---|

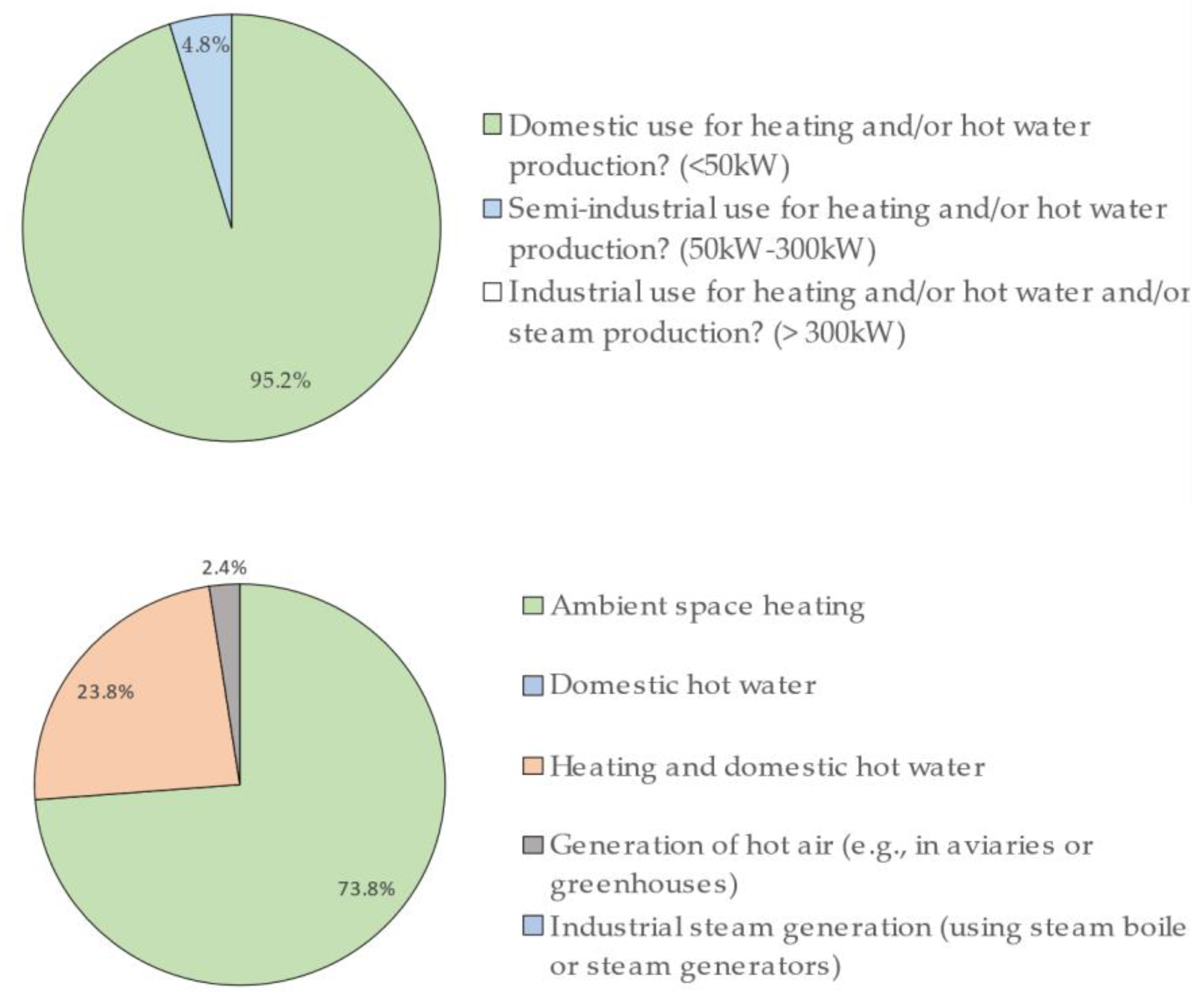

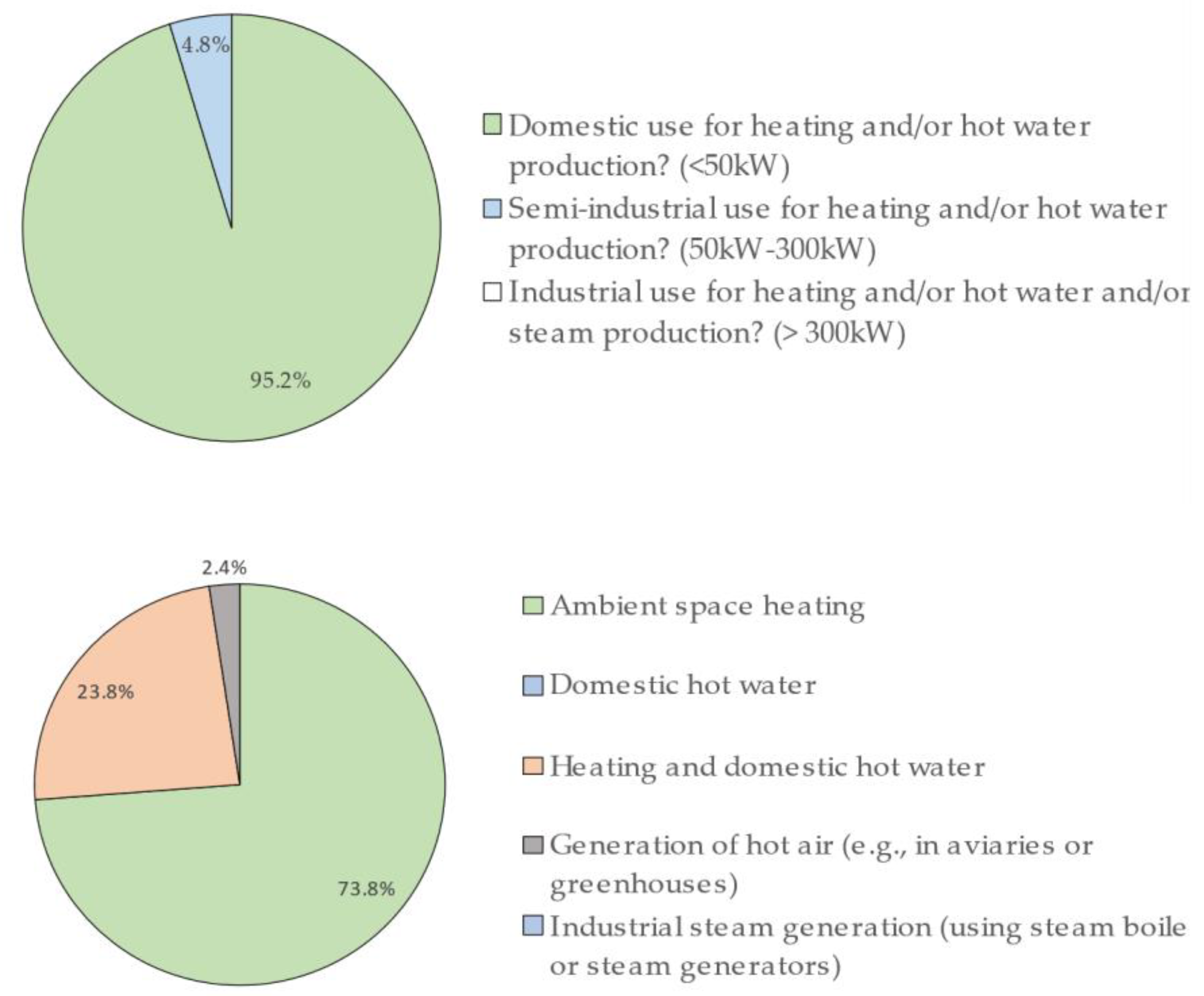

| 4. | What kind of use do you give to wood pellets? | 4.1. | Domestic use for heating and/or hot water production? (<50 kW) |

| 4.2. | Semi-industrial use for heating and/or hot water production? (50 kW–300 kW) | ||

| 4.3. | Industrial use for heating and/or hot water and/or steam production? (>300 kW) | ||

| 5. | For what purpose do you use wood pellets? | 5.1. | Ambient space heating |

| 5.2. | Domestic hot water | ||

| 5.3. | Heating and domestic hot water | ||

| 5.4. | Hot air generation (e.g., in aviaries or greenhouses) | ||

| 5.5. | Industrial steam generation (using steam boilers or steam generators) | ||

| 5.6. | Industrial ovens (for example, in bakeries or ceramic industry, among others) | ||

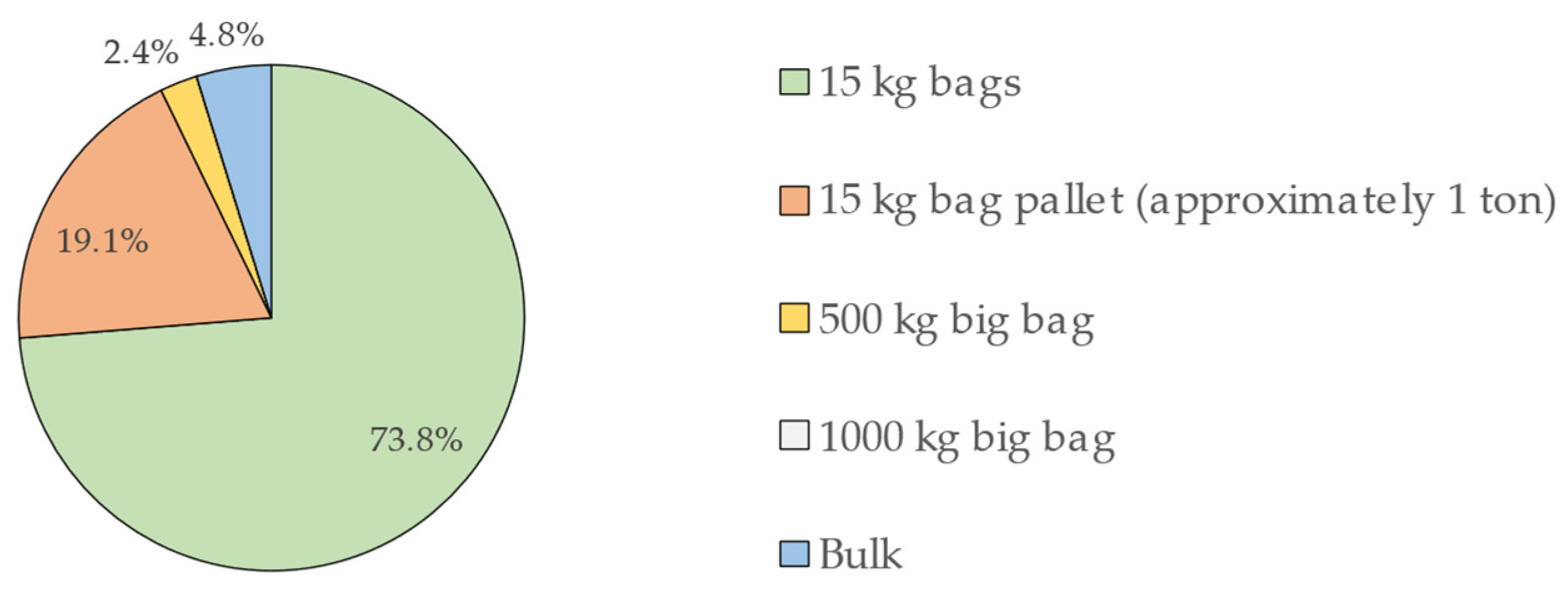

| 6. | How do you buy wood pellets? | 6.1. | 15 kg bag |

| 6.2. | 15 kg bag pallet (approximately 1 ton) | ||

| 6.3. | 500 kg big bag | ||

| 6.4. | 1000 kg big bag | ||

| 6.5. | Bulk | ||

| 7. | How much do you consume annually? (in kg) | 7.1. | Answer in full |

| 8. | How much do you buy at a time? (in kg) | 8.1. | Answer in full |

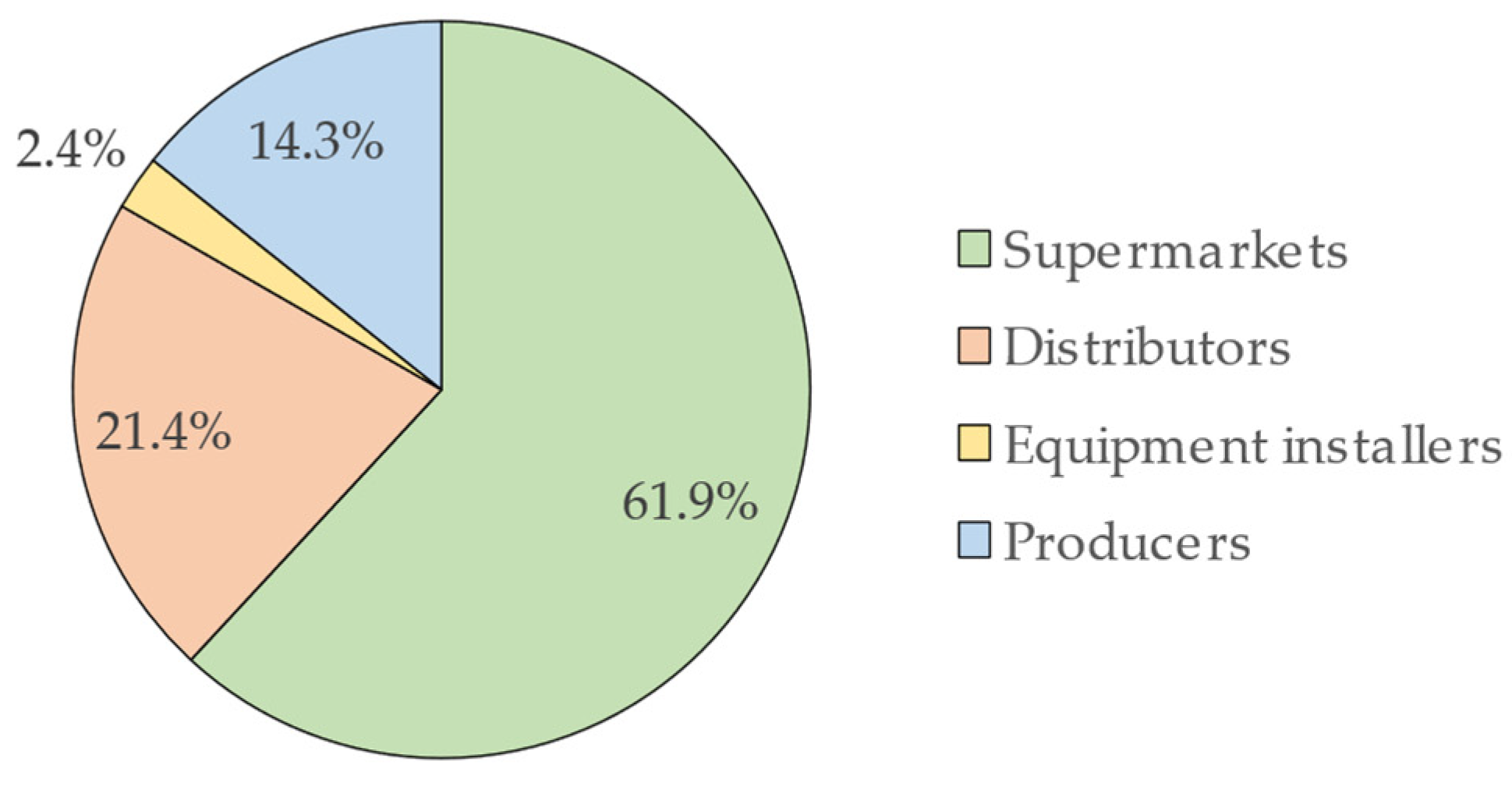

| 9. | Where do you usually buy wood pellets? | 9.1. | Supermarkets |

| 9.2. | Distributors | ||

| 9.3. | Equipment Installers | ||

| 9.4. | Producers | ||

| 10. | Since when have you used wood pellets? (years) | 10.1. | Answer in full |

| 11. | Do you remember the price of wood pellets when you first bought them? (VAT included) | 11.1. | Answer in full |

| 12. | What was the price of wood pellets the last time you bought them? (VAT included) | 12.1. | Answer in full |

| 13. | Does the amount you pay include delivery of the wood pellets at home? | 13.1. | Yes |

| 13.2. | No | ||

| Questions | Possible Answers | ||

|---|---|---|---|

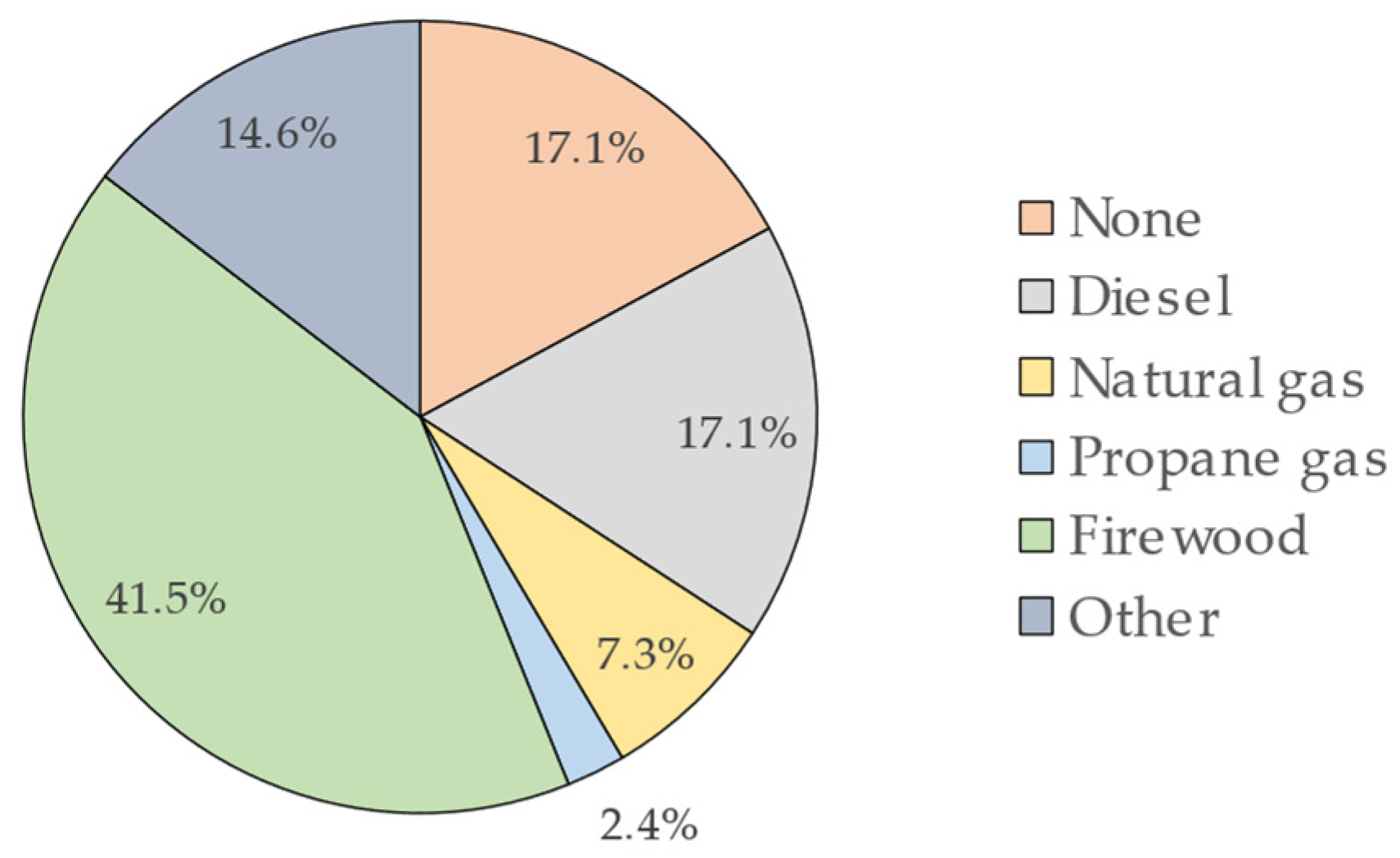

| 14. | What fuel did you use before wood pellets? | 14.1. | None |

| 14.2. | Diesel | ||

| 14.3. | Natural gas | ||

| 14.4. | Propane gas | ||

| 14.5. | Firewood | ||

| 14.6. | Other | ||

| 15. | If you answered “Other” in the previous question, may you indicate which fuel you used before the wood pellets? | 15.1. | Answer in full |

| 16. | Do you have any idea of the savings achieved in relation to the previous fuel? (approximate %) | 16.1. | Answer in full |

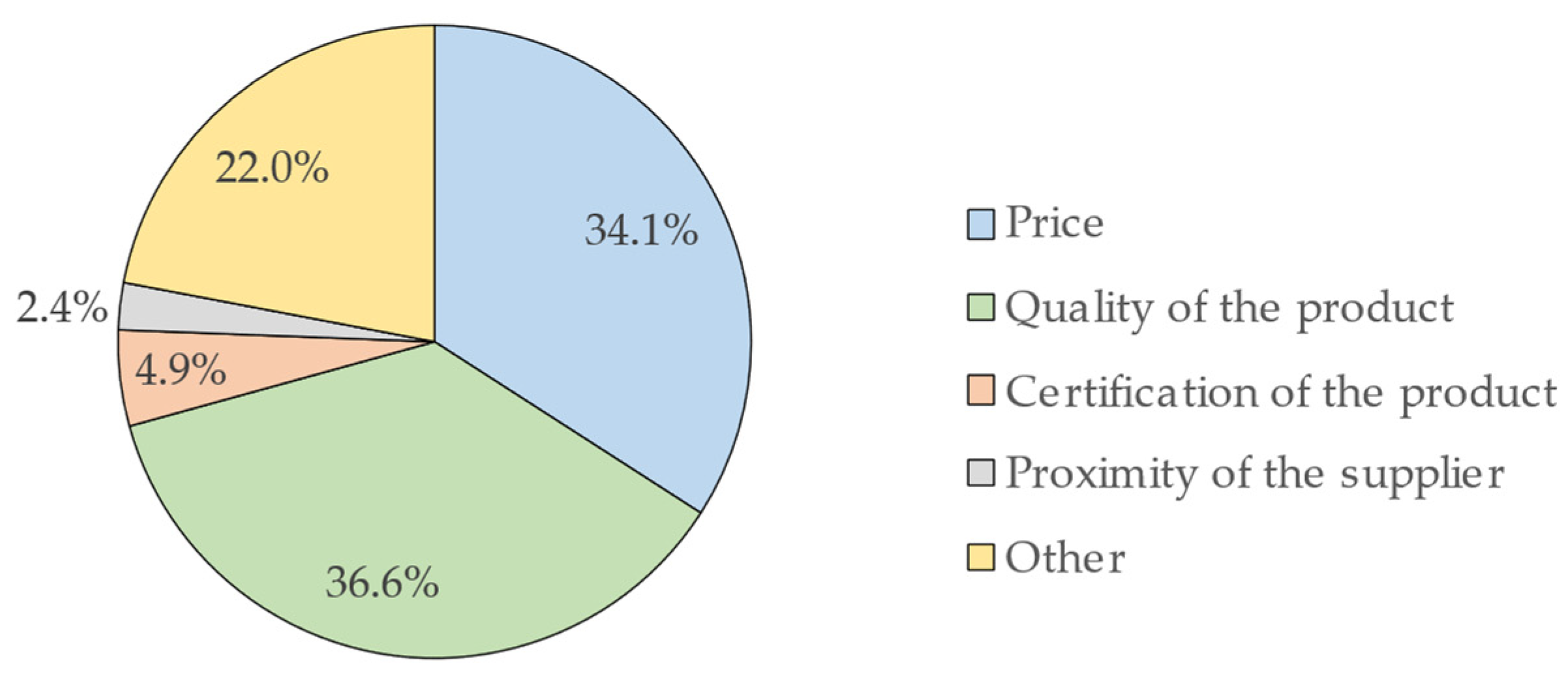

| 17. | What are your main criteria for buying wood pellets? | 17.1 | Price |

| 17.2. | Quality of the product | ||

| 17.3. | Certification of the product | ||

| 17.4. | Proximity to the supplier | ||

| 17.5. | None of the above | ||

| 18. | If you answered “None of the above” in the previous question, may you indicate which criteria you do use? | 18.1. | Answer in full |

| 19. | Do you prefer any brand? | 19.1. | Yes |

| 19.2. | No | ||

| Questions | Possible Answers | ||

|---|---|---|---|

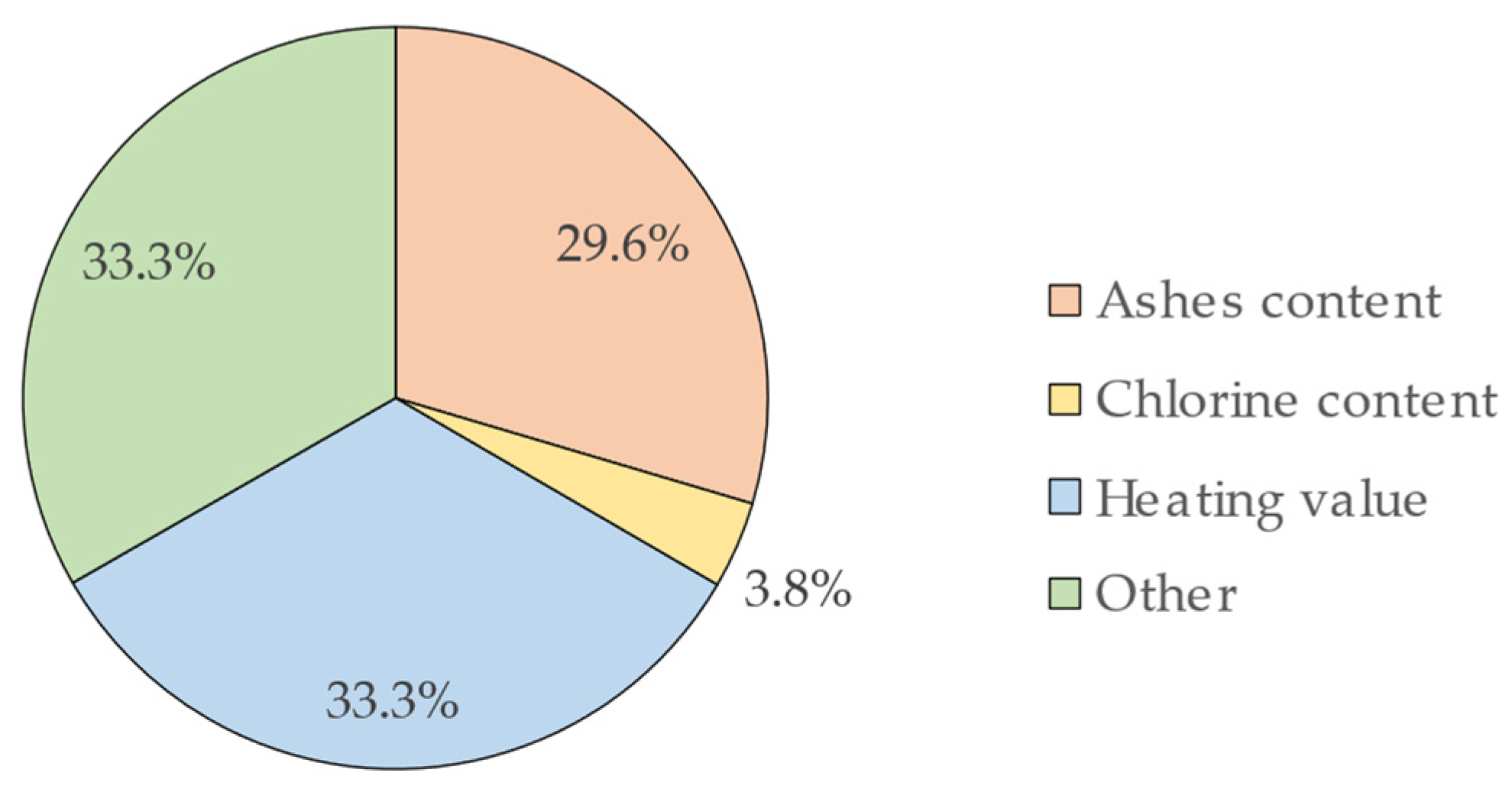

| 20. | Choose the most important property when selecting the product. | 20.1. | Ash content |

| 20.2. | Chlorine content | ||

| 20.3. | Heating value | ||

| 20.4. | None of the previous | ||

| 21. | If you answered “None of the above”, may you indicate which properties are important? | 21.1. | Answer in full |

| 22. | When you have to choose a brand of pellets that you don’t know, what is the most important negative characteristic for you? | 22.1. | Dust in the bag |

| 22.2. | Pellet size | ||

| 22.3. | Pellet color | ||

| 22.4. | None of the above | ||

| 23. | If you answered “None of the above”, may you indicate which negative characteristics are important for you? | 23.1. | Answer in full |

| 24. | Do you prefer certified pellets? | 24.1. | Yes |

| 24.2. | No | ||

| Questions | Possible Answers | ||

|---|---|---|---|

| 1. | Company name | Answer in full | |

| 2. | Location (municipality) | Answer in full | |

| 3. | Do you have your own production? | 3.1. | Yes |

| 3.2. | No | ||

| 4. | Do you use your own brand? | 4.1. | Yes |

| 4.2. | No | ||

| 5. | What brand do you use in the marketing of pellets? | 5.1. | Answer in full |

| 6. | Annual production capacity (in the case of producers) or annual sales capacity (in the case of distributors) (t/year)? | 6.1. | Answer in full |

| 7. | In what year did you start activity (with effective production)? | 7.1. | Answer in full |

| 8. | What raw materials do you use in production? | 8.1. | Answer in full |

| 9. | Are you ENplus certified? | 9.1. | Yes |

| No | |||

| 10. | Do you have any other certifications? (quality, HSW, environment, RDI, etc.) | 10.1. | Yes |

| 10.2. | No | ||

| 11. | If yes in the previous question, may you indicate which ones? | 11.1. | Answer in full |

| 12. | What kind of pellets do you produce? | 12.1. | Industrial |

| 12.2. | Domestic | ||

| 13. | In what formats do you sell pellets? | 13.1. | 10 kg bags |

| 13.2. | 15 kg bags | ||

| 13.3. | 500 kg big bags | ||

| 13.4. | 1000 kg big bags | ||

| 13.5. | 1250 kg big bags | ||

| 13.6. | Bulk | ||

| 14. | Does your company export? | 14.1. | Yes |

| 14.2. | No | ||

| 15. | What percentage of your production goes to export? | 15.1. | Answer in full |

| 16. | Which are the most important countries you export to? | 16.1. | United Kingdom (England, Scotland, Ireland and Wales) |

| 16.2. | Spain (includes Andorra and Gibraltar) | ||

| 16.3. | France | ||

| 16.4. | Italy | ||

| 16.5. | Netherlands, Belgium, Luxembourg | ||

| 16.6. | Scandinavia (Sweden, Norway, Denmark and Finland) | ||

| 16.7. | Central Europe (Germany, Switzerland, Austria and France) | ||

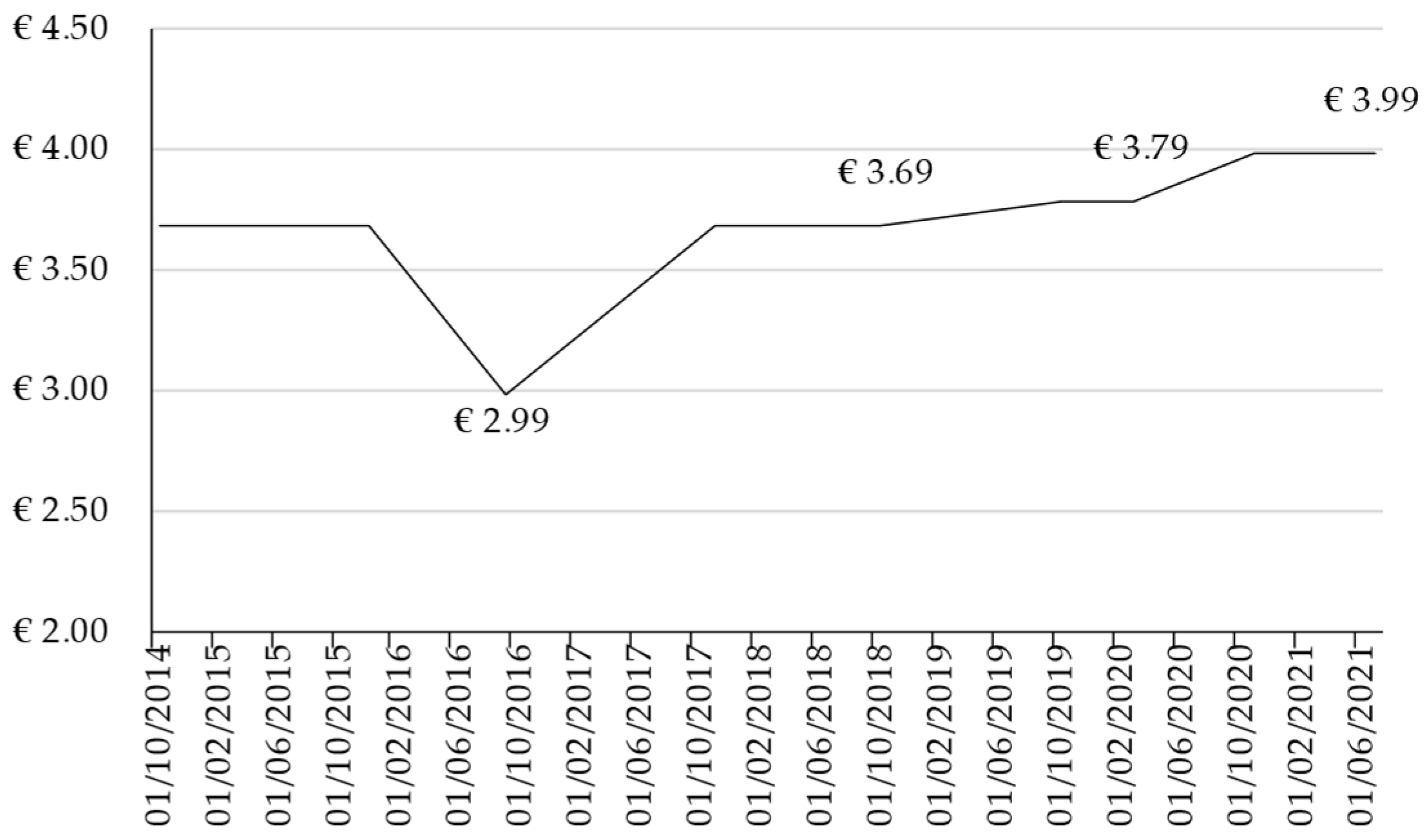

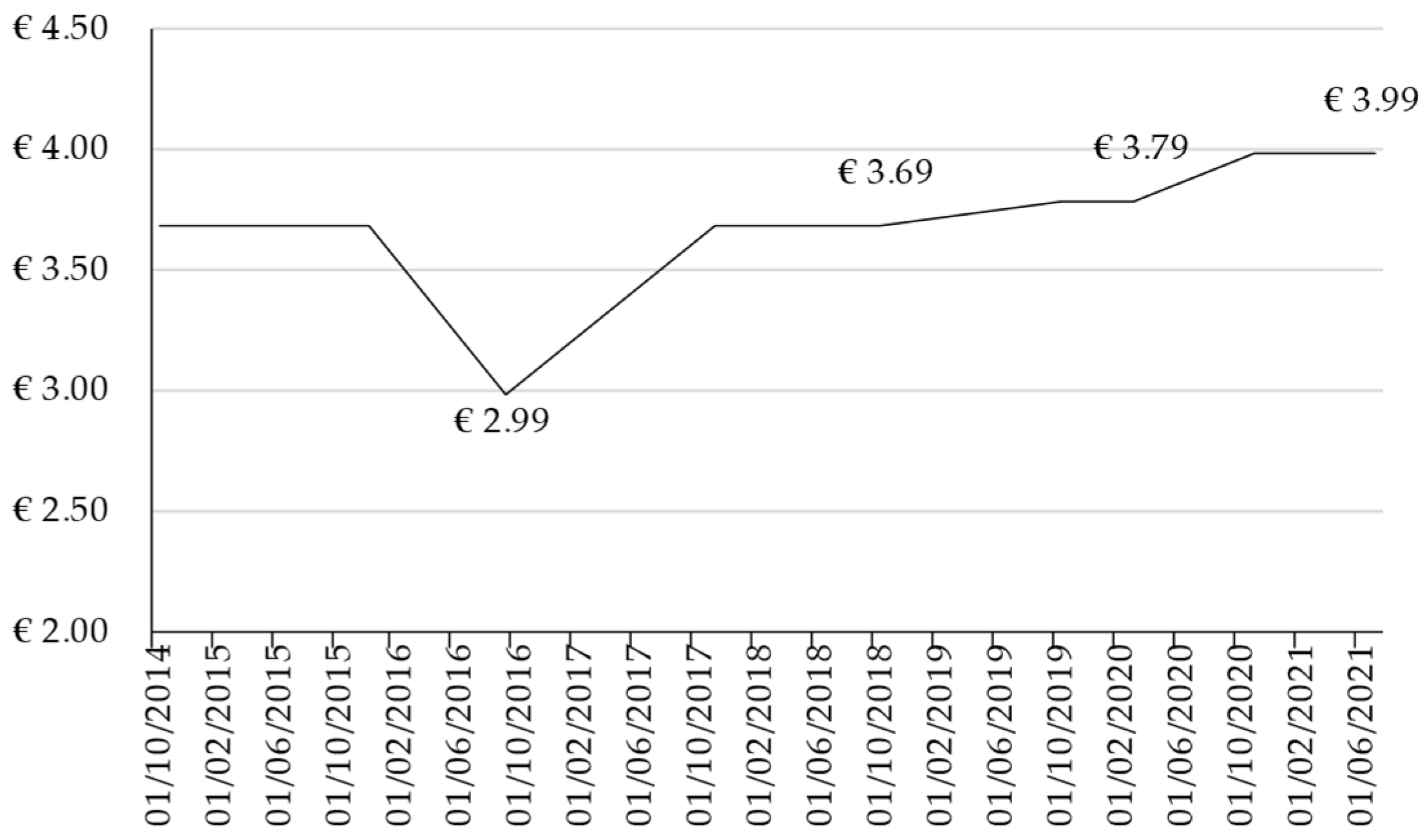

| 17. | May you indicate the average sale price of pellets in 2016, 2017, 2018 and 2019? (EUR/ton or EUR/bag—rices excluding VAT) | 17.1. | Answer in full |

| Districts | Answers (%) |

|---|---|

| Viana do Castelo | 5 |

| Braga | 7 |

| Porto | 26 |

| Vila Real | 1 |

| Bragança | 1 |

| Aveiro | 3 |

| Viseu | 5 |

| Coimbra | 3 |

| Guarda | 2 |

| Leiria | 9 |

| Castelo Branco | 1 |

| Santarém | 4 |

| Lisbon | 4 |

| Portalegre | 2 |

| Setúbal | 9 |

| Évora | 12 |

| Beja | 2 |

| Faro | 3 |

| Year | Exported Quantity (t) |

|---|---|

| 2011 | 535,457 |

| 2012 | 603,000 |

| 2013 | 818,981 |

| 2014 | 797,422 |

| 2015 | 693,694 |

| 2016 | 621,282 |

| 2017 | 513,862 |

| 2018 | 611,613 |

| 2019 | 729,351 |

| Company Name | Status | Location | Capacity (t/year) |

|---|---|---|---|

| Melpellets | Active | Melgaço | 12,000 |

| Stellep | Active | Chaves | 50,000 |

| Biodensa | Active | Celorico de Basto | 25,000 |

| Tecpellets | Active | Famalicão | 125,000 |

| Glowood | Active | Cercal | 100,000 |

| Martos | Active | Leiria | 30,000 |

| Reginacork | Active | Palmela | 35,000 |

| Ocean Pellets | Inactive | Ribeira Grande | 3000 |

| Pinewells | Active | Arganil | 125,000 |

| Nutriaguiar | Active | Vila Pouca de Aguiar | 10,000 |

| Enerpellets | Active | Pedrogão Grande | 75,000 |

| Pellets Power I | Active | Mortágua | 100,000 |

| Pellets Power II | Active | Alcácer do sal | 90,000 |

| Biohot Energia | Active | Lousada | 75,000 |

| Vimasol | Active | Celorico de Basto | 12,000 |

| JAF | Active | Oleiros | 90,000 |

| Palser | Active | Sertã | 60,000 |

| Enermontijo | Unknown | Pegões | 60,000 |

| Pelletsfirst | Active | Alcobaça | 100,000 |

| Biomad | Active | Guimarães | 10,000 |

| Castro and Filhos | Active | Guimarães | 10,000 |

| ATGreen | In construction | Guarda | 180,000 |

| Futerra | Active | Valongo | 90,000 |

| Pellets do Rodão Lda | Disabled | Vila Velha de Rodão | Unknown |

| YGE as | Disabled | Oliveira de Azeméis | Unknown |

| Biobriquette | Disabled | Penacova | Unknown |

| Soltotal | Active | Montemor-o-Velho | 6000 |

| Green Edge | Active | Cuba | 12,000 |

| Delitimbers | In construction | Proença-a-Nova | Unknown |

| Aleatory Concept | Active | Penacova | 15,000 |

| Briquettes Raro | Active | Vila Nova de Gaia | 50,000 |

| Smartfire | Active | Albergaria-a-Velha | Unknown |

| Sanitop | Active | Viana do Castelo | Unknown |

| Carvoaveiro | Active | Ílhavo | Unknown |

| OZ Energia Pellets | Active | Lisboa | Unknown |

| Siro | Active | Mira | 12,000 |

| XPZ | Disabled | Esposende | Unknown |

| Four Pellets | Disabled | Barcelos | Unknown |

| Ambipellets | Disabled | Póvoa de Lanhoso | Unknown |

| Thermowall II | Disabled | Braga | Unknown |

| Nicepellets | Disabled | Ílhavo | Unknown |

| CMC | Active | Alcobaça | 15,000 |

| 2016 | 2017 | 2018 | 2019 | |

|---|---|---|---|---|

| Industrial wood pellets | 116 EUR/t | 105 EUR/t | 108 EUR/t | 112 EUR/t |

| Domestic wood pellets | 150 EUR/t | 155 EUR/t | 160 EUR/t | 165 EUR/t |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nunes, L.J.R.; Casau, M.; Ferreira Dias, M. Portuguese Wood Pellets Market: Organization, Production and Consumption Analysis. Resources 2021, 10, 130. https://doi.org/10.3390/resources10120130

Nunes LJR, Casau M, Ferreira Dias M. Portuguese Wood Pellets Market: Organization, Production and Consumption Analysis. Resources. 2021; 10(12):130. https://doi.org/10.3390/resources10120130

Chicago/Turabian StyleNunes, Leonel J. R., Margarida Casau, and Marta Ferreira Dias. 2021. "Portuguese Wood Pellets Market: Organization, Production and Consumption Analysis" Resources 10, no. 12: 130. https://doi.org/10.3390/resources10120130

APA StyleNunes, L. J. R., Casau, M., & Ferreira Dias, M. (2021). Portuguese Wood Pellets Market: Organization, Production and Consumption Analysis. Resources, 10(12), 130. https://doi.org/10.3390/resources10120130