From AI Knowledge to AI Usage Intention in the Managerial Accounting Profession and the Role of Personality Traits—A Decision Tree Regression Approach

,

,  ,

,

,

,

Abstract

1. Introduction

2. Literature Review

3. Materials and Methods

3.1. Participants

3.2. Instruments

3.3. Procedure

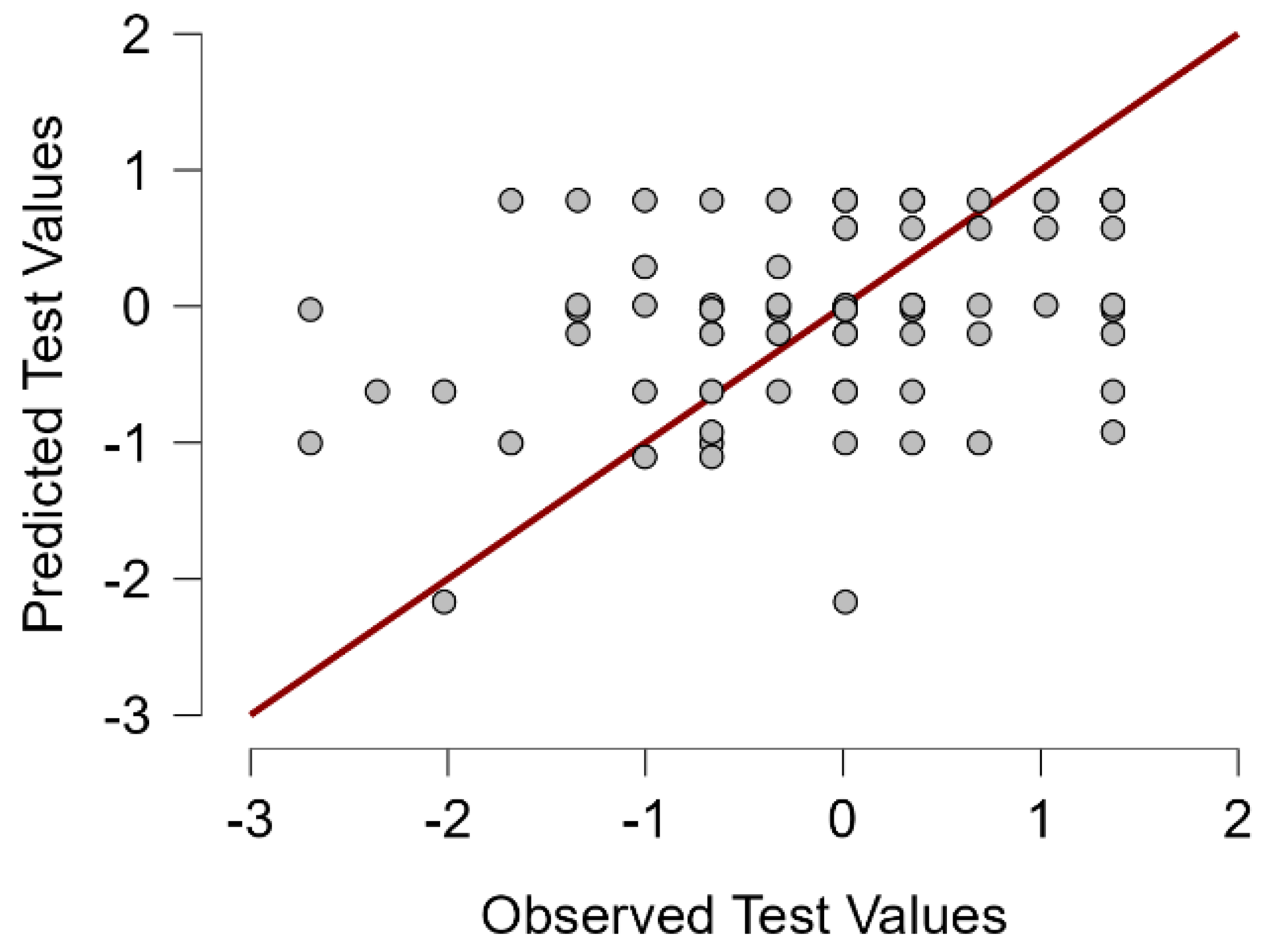

4. Results

5. Discussion

5.1. Relationship with the Literature

5.2. Practical Implications

5.3. Methodological Considerations and Limitations

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Flavián, C.; Pérez-Rueda, A.; Belanche, D.; Casaló, L.V. Intention to use analytical artificial intelligence (AI) in services–the effect of technology readiness and awareness. J. Serv. Manag. 2022, 33, 293–320. [Google Scholar] [CrossRef]

- Abdullah, A.A.H.; Almaqtari, F.A. The impact of artificial intelligence and Industry 4.0 on transforming accounting and auditing practices. J. Open Innov. Technol. Mark. Complex. 2024, 10, 100218. [Google Scholar] [CrossRef]

- Damerji, H.; Salimi, A. Mediating effect of use perceptions on technology readiness and adoption of artificial intelligence in accounting. Account. Educ. 2021, 30, 107–130. [Google Scholar] [CrossRef]

- Rawashdeh, A.; Bakhit, M.; Abaalkhail, L. Determinants of artificial intelligence adoption in SMEs: The mediating role of accounting automation. Int. J. Data Netw. Sci. 2023, 7, 25–34. [Google Scholar] [CrossRef]

- Alquhaif, A.S.; Al-Mamary, Y.H. Examining factors influencing the adoption of accounting information systems: An analysis of behavioral intentions and usage behavior. Hum. Syst. Manag. 2024. ahead of print. [Google Scholar]

- Park, J.; Woo, S.E. Who likes artificial intelligence? Personality predictors of attitudes toward artificial intelligence. J. Psychol. 2022, 156, 68–94. [Google Scholar] [CrossRef]

- Barnett, T.; Pearson, A.W.; Pearson, R.; Kellermanns, F.W. Five-factor model personality traits as predictors of perceived and actual usage of technology. Eur. J. Inf. Syst. 2015, 24, 374–390. [Google Scholar] [CrossRef]

- Fachrurrozie, F.; Nurkhin, A.; Santoso, J.T.B.; Astuti, D.P.; Mukhibad, H. Understanding the Teacher’s Intention to Use Artificial Intelligence for Accounting Learning. In Proceedings of the International Conference on Education Innovation and Social Science, Surakarta, Indonesia, 20 November 2024; pp. 17–21. [Google Scholar]

- Priya, B.; Sharma, V. Exploring users’ adoption intentions of intelligent virtual assistants in financial services: An anthropomorphic perspectives and socio-psychological perspectives. Comput. Hum. Behav. 2023, 148, 107912. [Google Scholar] [CrossRef]

- Juma’h, A.H.; Li, Y. The effects of auditors’ knowledge, professional skepticism, and perceived adequacy of accounting standards on their intention to use blockchain. Int. J. Account. Inf. Syst. 2023, 51, 100650. [Google Scholar] [CrossRef]

- Alshurafat, H.; Shbail, M.O.A.; Almuiet, M. Factors affecting the intention to adopt IT forensic accounting tools to detect financial cybercrimes. Int. J. Bus. Excell. 2024, 33, 169–190. [Google Scholar] [CrossRef]

- Jackson, D.; Allen, C. Technology adoption in accounting: The role of staff perceptions and organisational context. J. Account. Organ. Change 2024, 20, 205–227. [Google Scholar] [CrossRef]

- Almaqtari, F.A. The Role of IT Governance in the Integration of AI in Accounting and Auditing Operations. Economies 2024, 12, 199. [Google Scholar] [CrossRef]

- Tang, M.; Koopman, P.; McClean, S.T.; Zhang, J.H.; Li, C.H.; De Cremer, D.; Ng, C.T.S. When Conscientious Employees Meet Intelligent Machines: An Integrative Approach Inspired by Complementarity Theory and Role Theory. Acad. Manag. J. 2022, 65, 1019–1054. [Google Scholar] [CrossRef]

- Chourasia, S.; Dhama, A.; Bhardwaj, G. AI-Driven Organizational Culture Evolution: A Critical Review. In Proceedings of the 2024 International Conference on Communication, Computer Sciences and Engineering (IC3SE), Gautam Buddha Nagar, India, 9–11 May 2024; IEEE: Piscataway, NJ, USA; pp. 1839–1844. [Google Scholar]

- Ciocoiu, C.N.; Radu, C.; Colesca, S.E.; Prioteasa, A. Exploring the link between risk management and performance of MSMEs: A bibliometric review. J. Econ. Surv. 2024. ahead of print. [Google Scholar] [CrossRef]

- Popa, I.; Ștefan, S.C.; Olariu, A.A.; Breazu, A.; Cioc, M.M. Predictors of employees’ work performance in online and on-site conditions: A combined use of PLS-SEM and NCA. Econ. Comput. Econ. Cybern. Stud. Res. 2024, 58, 265–279. [Google Scholar]

- Toader, C.S.; Brad, I.; Rujescu, C.I.; Dumitrescu, C.S.; Sîrbulescu, E.C.; Orboi, M.D.; Gavrilă, C. Exploring students’ opinion towards integration of learning games in higher education subjects and improved soft skills—A comparative study in Poland and Romania. Sustainability 2023, 15, 7969. [Google Scholar] [CrossRef]

- Vesselenyi, T.; Dziţac, I.; Dziţac, S.; Vaida, V. Surface roughness image analysis using quasi-fractal characteristics and fuzzy clustering methods. Int. J. Comput. Commun. Control 2008, 3, 304–316. [Google Scholar] [CrossRef]

- Ban, O.I.; Droj, L.; Tușe, D.; Droj, G.; Bugnar, N. Data processing by fuzzy methods in social sciences research: Example in hospitality industry. Int. J. Comput. Commun. Control 2022, 17, 4741. [Google Scholar] [CrossRef]

- Isac, N.; Akide, M.; Dobrin, C.; Dinulescu, R. Examining the impact of Covid-19 on employee performance and future aspirations in the context of digital economy. Econ. Comput. Econ. Cybern. Stud. Res. 2022, 56, 94–114. [Google Scholar]

- Janiesch, C.; Zschech, P.; Heinrich, K. Machine Learning and Deep Learning. Electron. Mark. 2021, 31, 685–695. [Google Scholar] [CrossRef]

- Cabrera-Paniagua, D.; Rubilar-Torrealba, R. Adaptive intelligent autonomous system using artificial somatic markers and Big Five personality traits. Knowl. Based Syst. 2022, 249, 108995. [Google Scholar] [CrossRef]

- Riedl, R. Is Trust in Artificial Intelligence Systems Related to User Personality? Review of Empirical Evidence and Future Research Directions. Electron. Mark. 2022, 32, 2021–2051. [Google Scholar] [CrossRef]

- Lee, E. The Power of Perception in Human-AI Interaction: Investigating Psychological Factors and Cognitive Biases that Shape User Belief and Behavior. arXiv 2024, arXiv:2409.15328. [Google Scholar]

- Latifah, L.; Setiyani, R.; Arief, S.; Susilowati, N. The role of personal values in forming the AI ethics of prospective accountants. Ethics Prog. 2023, 14, 90–109. [Google Scholar] [CrossRef]

- Năstase, M.; Croitoru, G.; Florea, N.V.; Cristache, N.; Lile, R. The perceptions of employees from Romanian companies on adoption of artificial intelligence in recruitment and selection processes. Amfiteatru Econ. 2024, 26, 421–439. [Google Scholar] [CrossRef]

- Wang, H.C. Distinguishing the adoption of business intelligence systems from their implementation: The role of managers’ personality profiles. Behav. Inf. Technol. 2014, 33, 1082–1092. [Google Scholar] [CrossRef]

- Calluso, C.; Devetag, M.G. The impact of technology acceptance and personality traits on the willingness to use AI-assisted hiring practices. Int. J. Organ. Anal. 2024. ahead of print. [Google Scholar] [CrossRef]

- Leitner-Hanetseder, S.; Lehner, O.M.; Eisl, C.; Forstenlechner, C. A profession in transition: Actors, tasks and roles in AI-based accounting. J. Appl. Account. Res. 2021, 22, 539–556. [Google Scholar] [CrossRef]

- Namazi, M.; Rezaei, G. Modelling the role of strategic planning, strategic management accounting information system, and psychological factors on the budgetary slack. Account. Forum 2024, 48, 279–306. [Google Scholar] [CrossRef]

- Ahmadi, S.; Mayoufi, A.; Khozin, A.; Gargaz, M. The role of organizational paranoia in the formation of the Machiavellian personality of accountants with emphasis on Gardner’s theory of multiple intelligences. Int. J. Financ. Manag. Account. 2025, 10, 157–176. [Google Scholar]

- Chong, V.K.; Eggleton, I.R. The decision-facilitating role of management accounting systems on managerial performance: The influence of locus of control and task uncertainty. Adv. Account. 2003, 20, 165–197. [Google Scholar] [CrossRef]

- Xiao, Q.; Li, X. Exploring the antecedents of online learning satisfaction: Role of flow and comparison between use contexts. Int. J. Comput. Commun. Control 2021, 16, 4398. [Google Scholar] [CrossRef]

- Rad, D.; Balas, V.E.; Redeș, A.; Kiss, C.; Rad, G. An RBF neural network approach to predict preschool teachers integrative-qualitative intentional behavior based on Marzano’s model of teaching effectiveness. In Decision Making and Decision Support in the Information Era: Dedicated to Academician Florin Filip; Springer Nature Switzerland: Cham, Switzerland, 2024; pp. 213–234. [Google Scholar]

- Rad, D.; Paraschiv, N.; Kiss, C. Neural network applications in polygraph scoring—A scoping review. Information 2023, 14, 564. [Google Scholar] [CrossRef]

- Kaya, F.; Aydin, F.; Schepman, A.; Rodway, P.; Yetişensoy, O.; Demir Kaya, M. The roles of personality traits, AI anxiety, and demographic factors in attitudes toward artificial intelligence. Int. J. Hum. Comput. Interact. 2024, 40, 497–514. [Google Scholar] [CrossRef]

- Radu, V.; Radu, F.; Tabirca, A.I.; Saplacan, S.I.; Lile, R. Bibliometric analysis of fuzzy logic research in international scientific databases. Int. J. Comput. Commun. Control 2021, 16, 4120. [Google Scholar] [CrossRef]

- Wan, X.; Tian, L. User stress detection using social media text: A novel machine learning approach. Int. J. Comput. Commun. Control 2024, 19, 6772. [Google Scholar] [CrossRef]

- Liu, L.T.; Wang, S.; Britton, T.; Abebe, R. Lost in Translation: Reimagining the Machine Learning Life Cycle in Education. arXiv 2022, arXiv:2209.03929. [Google Scholar]

- Csorba, L.M.; Crăciun, M. An application of the multi-period decision trees in the sustainable medical waste investments. In Soft Computing Applications, Proceedings of the 7th International Workshop Soft Computing Applications (SOFA 2016), Arad, Romania, 24–26 August 2016; Springer International Publishing: Berlin/Heidelberg, Germany, 2018; Volume 2, pp. 540–556. [Google Scholar]

- Farcane, N.; Bunget, O.C.; Blidisel, R.; Dumitrescu, A.C.; Deliu, D.; Bogdan, O.; Burca, V. Auditors’ perceptions on work adaptability in remote audit: A COVID-19 perspective. Econ. Res. Ekon. Istraživanja 2023, 36, 422–459. [Google Scholar] [CrossRef]

- Hategan, V.P.; Hategan, C.D. Sustainable leadership: Philosophical and practical approach in organizations. Sustainability 2021, 13, 7918. [Google Scholar] [CrossRef]

- Khan, F.U.; Trifan, V.A.; Pantea, M.F.; Zhang, J.; Nouman, M. Internal governance and corporate social responsibility: Evidence from Chinese companies. Sustainability 2022, 14, 2261. [Google Scholar] [CrossRef]

- Ogrean, C.; Herciu, M. Romania’s SMEs on the way to EU’s twin transition to digitalization and sustainability. Stud. Bus. Econ. 2021, 16, 282–295. [Google Scholar] [CrossRef]

- Paraschiv, D.M.; Ţiţan, E.; Manea, D.I.; Bănescu, C.E. Quantifying the effects of working from home on privacy. An empirical analysis in the 2020 pandemic. Econ. Comput. Econ. Cybern. Stud. Res. 2021, 55, 21–36. [Google Scholar]

- Popa, I.; Cioc, M.M.; Breazu, A.; Popa, C.F. Identifying sufficient and necessary competencies in the effective use of artificial intelligence technologies. Amfiteatru Econ. 2024, 26, 33–52. [Google Scholar] [CrossRef]

- Popa, I.; Ştefan, S.C.; Morărescu, C.; Cicea, C. Research regarding the influence of knowledge management practices on employee satisfaction in the Romanian healthcare system. Amfiteatru Econ. 2018, 20, 553–566. [Google Scholar] [CrossRef]

- Trifan, V.A.; Pantea, M.F. Shifting priorities and expectations in the new world of work. Insights from millennials and generation Z. J. Bus. Econ. Manag. 2024, 25, 1075–1096. [Google Scholar] [CrossRef]

- Ionaşcu, I.; Ionaşcu, M.; Nechita, E.; Săcărin, M.; Minu, M. Digital Transformation, Financial Performance and Sustainability: Evidence for European Union Listed Companies. Amfiteatru Econ. 2022, 24, 94–109. [Google Scholar] [CrossRef]

- Fülöp, M.T.; Ionescu, C.A.; Măgdaș, N.; Topor, D.I.; Breaz, T.O. Acceptance of digital instruments in the accounting profession. JEEMS J. East. Eur. Manag. Stud. 2024, 29, 283–313. [Google Scholar] [CrossRef]

- Rangone, A.; Ionescu-Feleaga, L.; Bunea, M.; Sargiacomo, M. The contribution of Grigore L. Trancu-Iasi to the evolution of accounting theory, practice and profession in Romania. Account. Hist. 2024, 29, 265–294. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Relative Importance | |

|---|---|

| AI knowledge | 51.285 |

| Agreeability | 15.658 |

| Extraversion | 9.680 |

| Emotional stability | 8.518 |

| Openness | 8.494 |

| Conscientiousness | 6.365 |

| Obs. in Split | Split Point | Improvement | |

|---|---|---|---|

| AI knowledge | 447 | −0.019 | 0.269 |

| AI knowledge | 219 | −1.244 | 0.066 |

| Agreeability | 57 | 0.206 | 0.149 |

| AI knowledge | 36 | −2.163 | 0.268 |

| Agreeability | 21 | 0.722 | 0.341 |

| Emotional stability | 162 | 0.708 | 0.042 |

| Agreeability | 134 | −1.171 | 0.060 |

| Agreeability | 113 | 0.378 | 0.073 |

| AI knowledge | 228 | 0.594 | 0.140 |

| Extraversion | 109 | 0.227 | 0.138 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cuc, L.D.; Rad, D.; Cilan, T.F.; Gomoi, B.C.; Nicolaescu, C.; Almași, R.; Dzitac, S.; Isac, F.L.; Pandelica, I. From AI Knowledge to AI Usage Intention in the Managerial Accounting Profession and the Role of Personality Traits—A Decision Tree Regression Approach. Electronics 2025, 14, 1107. https://doi.org/10.3390/electronics14061107

Cuc LD, Rad D, Cilan TF, Gomoi BC, Nicolaescu C, Almași R, Dzitac S, Isac FL, Pandelica I. From AI Knowledge to AI Usage Intention in the Managerial Accounting Profession and the Role of Personality Traits—A Decision Tree Regression Approach. Electronics. 2025; 14(6):1107. https://doi.org/10.3390/electronics14061107

Chicago/Turabian StyleCuc, Lavinia Denisia, Dana Rad, Teodor Florin Cilan, Bogdan Cosmin Gomoi, Cristina Nicolaescu, Robert Almași, Simona Dzitac, Florin Lucian Isac, and Ionut Pandelica. 2025. "From AI Knowledge to AI Usage Intention in the Managerial Accounting Profession and the Role of Personality Traits—A Decision Tree Regression Approach" Electronics 14, no. 6: 1107. https://doi.org/10.3390/electronics14061107

APA StyleCuc, L. D., Rad, D., Cilan, T. F., Gomoi, B. C., Nicolaescu, C., Almași, R., Dzitac, S., Isac, F. L., & Pandelica, I. (2025). From AI Knowledge to AI Usage Intention in the Managerial Accounting Profession and the Role of Personality Traits—A Decision Tree Regression Approach. Electronics, 14(6), 1107. https://doi.org/10.3390/electronics14061107