The Impact of the Regulatory Sandbox on the Fintech Industry, with a Discussion on the Relation between Regulatory Sandboxes and Open Innovation

Abstract

:1. Introduction

2. Fintech Industry and Fintech Regulatory Sandboxes

3. Previous Researches and Hypotheses

4. Methodology

4.1. Methods

4.1.1. Scheme of Analysis

4.1.2. Pre–Post Analysis

4.1.3. Comparison Analysis

4.1.4. Regression Analysis

4.2. Variables and Data

4.2.1. Variables

4.2.2. Set Analysis Target and Period

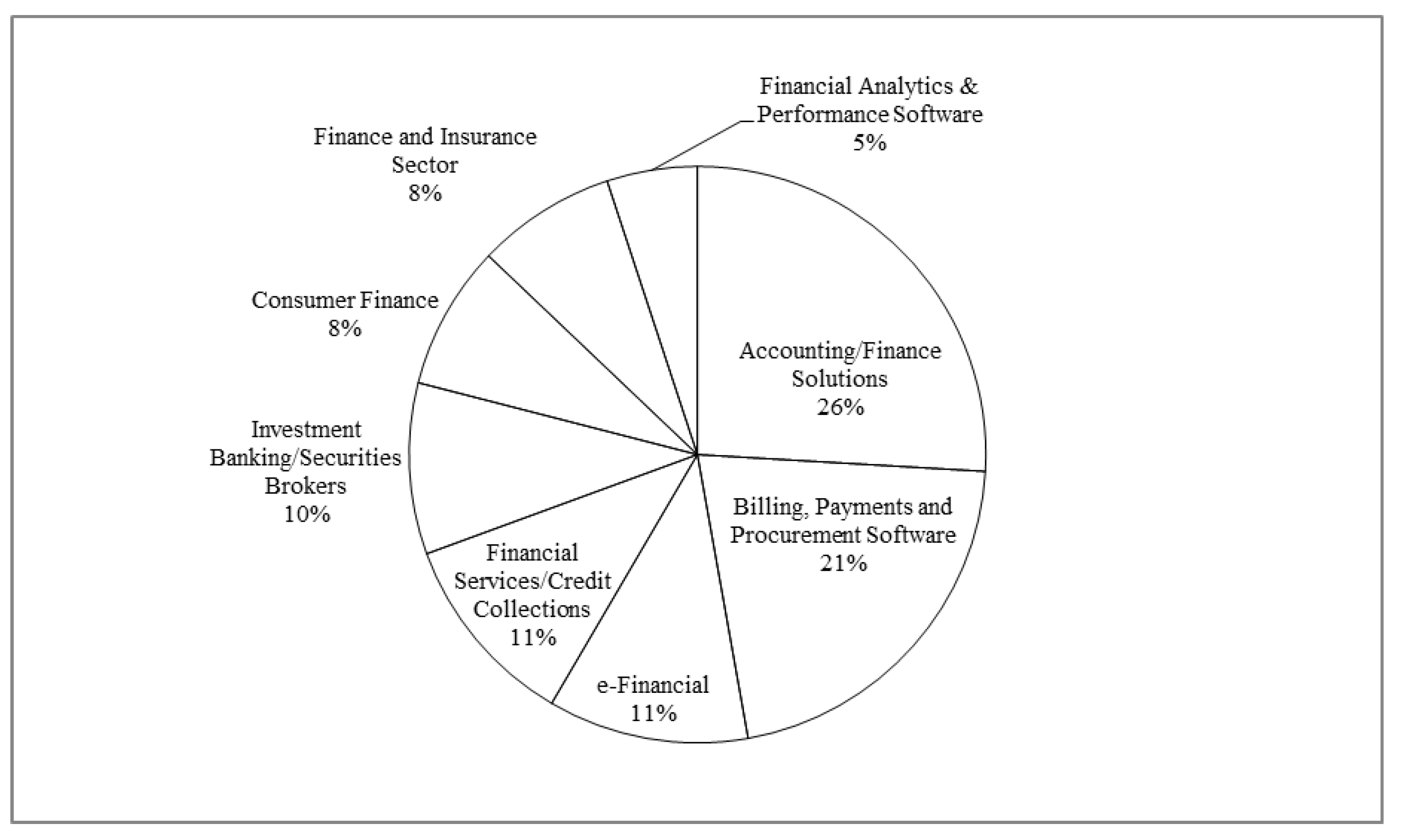

4.2.3. Data Collection

5. Results

5.1. Pre–Post Analysis

5.2. Comparison Analysis

5.3. Regression Analysis

6. Discussion: The Relation between Regulatory Sandbox and Open Innovation

6.1. Summary of the Research Results

6.2. Regulatory Sandbox and Open Innovation

6.3. Regulatory Sandbox and Open Innovation in Fintech

Author Contributions

Funding

Conflicts of Interest

References

- ASIC. ASIC Regulatory Guide 257; ASIC: Brisbane, Australia, 2017.

- ASIC. ASIC Fintech Regulatory Sandbox; ASIC: Brisbane, Australia, 2019.

- Blind, K. The influence of regulations on innovation: A quantitative assessment for OECD countries. Res. Policy 2012, 41, 391–400. [Google Scholar] [CrossRef]

- Lee, W.S.; Hong, B. The Status of Fintech and Its Related Legal Problems. Youngsan Law J. 2015, 12, 219–256. [Google Scholar]

- CBinsights. CBinsights 2019 Fintech Trends to Watch; CBinsights: New York, NY, USA, 2019. [Google Scholar]

- CGAP. CGAP Regulatory Sandboxes and Financial Inclusion; CGAP: Washington, DC, USA, 2017. [Google Scholar]

- Cliford Chance. Cliford Chance European Fintech Regulation an Overview; Cliford Chance: London, UK, 2017. [Google Scholar]

- Chen, A.C.M. Regulatory Sandbox and Competition of Financial Technologies in Taiwan. Available online: https://dev.competitionpolicyinternational.com/regulatory-sandbox-and-competition-of-financial-technologies-in-taiwan/ (accessed on 16 June 2020).

- Cumming, D.J.; Schwienbacher, A. Fintech venture capital. Corp. Gov. Int. Rev. 2018, 26, 374–389. [Google Scholar] [CrossRef]

- Diemers, D.; Lamaa, A.; Salamat, J.; Steffens, T. Developing a FinTech ecosystem in the GCC; PWC: Abu Dhabi, United Arab Emirates, 2015; Available online: https://www.strategyand.pwc.com/m1/en/reports/developing-a-fintech-ecosystem-in-the-gcc.pdf (accessed on 16 June 2020).

- FCA. FCA Regulatory Sandbox; FCA: London, UK, 2015. [Google Scholar]

- Vives, X. The Impact of Fintech on Banking. Eur. Econ. 2017, 2, 97–105. [Google Scholar]

- Magnuson, W. Regulating Fintech. Vanderbilt Law Rev. 2018, 71, 1167–1226. [Google Scholar]

- The Economist. The Fintech Revolution: A Wave of Startups is Changing Finance for the Better; The Economist: London, UK, 2015; Volume 415. [Google Scholar]

- EY. EY FinTech Adoption Index 2017; EY: London, UK, 2017. [Google Scholar]

- FCA. FCA Regulatory Sandbox-Cohort 5; FCA: London, UK, 2019. [Google Scholar]

- Chen, M.A.; Wu, Q.; Yang, B. How Valuable Is FinTech Innovation? Rev. Financ. Stud. 2019, 32, 2062–2106. [Google Scholar] [CrossRef] [Green Version]

- Arner, D.W.; Barberis, J.N.; Buckley, R.P. The Evolution of Fintech: A New Post-Crisis Paradigm? Social Science Research Network: Rochester, NY, USA, 2015. [Google Scholar]

- Finextra. The Role of Regulatory Sandboxes in Fintech Innovation; Finextra: London, UK, 2019. [Google Scholar]

- Brnovich, M. Regulatory Sandboxes Can Help States Advance Fintech; American Banker: New York, NY, USA, 2017; Available online: https://www.americanbanker.com/opinion/regulatory-sandboxes-can-help-states-advance-fintech (accessed on 16 June 2020).

- Yang, D.; Li, M. Evolutionary Approaches and the Construction of Technology-Driven Regulations. Emerg. Mark. Financ. Trade 2018, 54, 3256–3271. [Google Scholar] [CrossRef]

- HKMA. Fintech Supervisory Sandbox (FSS); HKMA: Hong Kong, China, 2019.

- ICLG. Switzerland: Fintech 2019; ICLG: London, UK, 2019. [Google Scholar]

- ING. The FinTech Index; ING: Amsterdam, The Netherlands, 2016. [Google Scholar]

- Sifintech. Four FinTechs Approved to Enter the Sierra Leone Sandbox Programme; Sifintech: London, UK, 2018. [Google Scholar]

- SFC. Welcome to the Fintech Contact Point; SFC: Hong Kong, China, 2019. [Google Scholar]

- ITA. Top Markets Report: Financial Technology; ITA: Washington, DC, USA, 2016. [Google Scholar]

- Jagtiani, J.; John, K. Fintech: The Impact on Consumers and Regulatory Responses. J. Econ. Bus. 2018, 100, 1–6. [Google Scholar] [CrossRef]

- Jones, L. Guest editorial: Poverty reduction in the FinTech age. Enterp. Dev. Microfinance 2018, 29, 99–102. [Google Scholar] [CrossRef]

- KPMG. The Pulse of Fintech 02 2017; KPMG: Amstelveen, The Netherlands, 2017. [Google Scholar]

- KPMG. 2018 Fintech100; KPMG: Amstelveen, The Netherlands, 2018. [Google Scholar]

- Lee, I.; Shin, Y.J. Fintech: Ecosystem, business models, investment decisions, and challenges. Bus. Horiz. 2018, 61, 35–46. [Google Scholar] [CrossRef]

- MAS. Response to Feedback RECEIVED–FinTech Regulatory Sandbox Guidelines; MAS: Singapore, 2016.

- Leong, C.; Tan, B.; Tan, F.T.C.; Xiao, X.; Sun, Y. Nurturing a FinTech ecosystem: The case of a youth microloan startup in China. Int. J. Inf. Manag. 2017, 37, 92–97. [Google Scholar] [CrossRef]

- Stern, A.D. Innovation under regulatory uncertainty: Evidence from medical technology. J. Public Econ. 2017, 145, 181–200. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- MAGNITT. 5 UAE Regulator Initiatives to Bring Fintech to The Next Level; About the fintech regulatory sandbox of UAE; MAGNITT: Dubai, UAE, 2019. [Google Scholar]

- Roh, C.-Y.; Kim, S. Medical innovation and social externality. J. Open Innov. Technol. Mark. Complex. 2017, 3, 3. [Google Scholar] [CrossRef] [Green Version]

- Milian, E.Z.; Spinola, M.D.M.; de Carvalho, M.M. Fintechs: A literature review and research agenda. Electron. Commer. Res. Appl. 2019, 34, 100833. [Google Scholar] [CrossRef]

- Porter, M.E.; Claas van der, L. Toward a New Conception of the Environment-Competitiveness Relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- PWC. Global FinTech Report 2017; PWC: London, UK, 2017. [Google Scholar]

- Samjong KPMG. Samjong Insight; Samjong KPMG: Seoul, Korea, 2017. [Google Scholar]

- Gozman, D.; Liebenau, J.; Mangan, J. The Innovation Mechanisms of Fintech Start-Ups: Insights from SWIFT’s Innotribe Competition. J. Manag. Inf. Syst. 2018, 35, 145–179. [Google Scholar] [CrossRef]

- Business Insider. The FCA’s Fintech Sandbox is Already Delivering Value; Business Insider: New York, NY, USA, 2018; Available online: https://www.businessinsider.com/fca-fintech-sandbox-delivers-value-2018-10 (accessed on 17 May 2019).

- Fairchild, R. An entrepreneur’s choice of venture capitalist or angel-financing: A behavioral game-theoretic approach. J. Bus. Ventur. 2011, 26, 359–374. [Google Scholar] [CrossRef]

- Cohen, J.; Cohen, P.; West, S.G.; Aiken, L.S. Applied Multiple Regression/Correlation Analysis for the Behavioral Sciences; Routledge: Abingdon, UK, 2013; ISBN 978-1-134-80094-0. [Google Scholar]

- Gompers, P.; Kovner, A.; Lerner, J.; Scharfstein, D. Venture capital investment cycles: The impact of public markets. J. Financ. Econ. 2008, 87, 1–23. [Google Scholar] [CrossRef] [Green Version]

- Yun, J.J.; Liu, Z. Micro- and Macro-Dynamics of Open Innovation with a Quadruple-Helix Model. Sustainability 2019, 11, 3301. [Google Scholar] [CrossRef] [Green Version]

- JinHyo, J.Y.; Won, D.; Park, K. Entrepreneurial cyclical dynamics of open innovation. J. Evol. Econ. Heidelb. 2018, 28, 1151–1174. [Google Scholar] [CrossRef]

- Gomber, P.; Kauffman, R.J.; Parker, C.; Weber, B.W. On the Fintech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformation in Financial Services. J. Manag. Inf. Syst. 2018, 35, 220–265. [Google Scholar] [CrossRef]

{kind=link}

| Classification | Continent | Countries |

|---|---|---|

| Introduced countries | North America | Canada |

| Europe | Denmark | |

| UK | ||

| The Netherlands | ||

| Norway | ||

| Switzerland | ||

| Asia | Brunei | |

| Hong Kong | ||

| Japan | ||

| India | ||

| Malaysia | ||

| Singapore | ||

| Taiwan | ||

| South Korea | ||

| Thailand | ||

| Middle East | Abu Dhabi | |

| Bahrain | ||

| Dubai | ||

| Oceania | Australia | |

| Africa | Sierra Leone | |

| Proposed countries | North America | USA |

| Europe | Ireland | |

| Spain | ||

| Asia | Indonesia |

| Countries | Categories | Details |

|---|---|---|

| UK | Organization in charge | FCA (Financial Conduct Authority) |

| Targets | Finance/IT companies & Fintech companies | |

| Features | Testing period in the regulatory sandbox: 3–6 months. FCA seeks to provide the appliers with five advantages: the ability to test products and services in a controlled environment, reduced time-to-market at potentially lower cost, support in identifying appropriate consumer protection, safeguards to build into new products and services, and better access to finance. * These have been the basis for other countries’ regulatory sandbox guidelines. | |

| Hong Kong | Organization in charge | HKMA (Hong Kong Monetary Authority) |

| Targets | Bank | |

| Features | Testing period in the regulatory sandbox: case-specific decisions. They do not clearly specify which regulations can be relaxed or exempted, and the level of deregulations is being set flexibly according to the circumstances of companies. | |

| Singapore | Organization in charge | MAS (Monetary Authority of Singapore) |

| Targets | Finance /IT companies & Fintech companies | |

| Features | Testing period in regulatory sandbox: case-specific decisions. The purposes of the regulatory sandboxes are a. increase efficiency; b. manage risks better; c. create new opportunities; or d. improve people’s lives. | |

| Australia | Organization in charge | ASIC (Australian Securities and Investment Commission) |

| Targets | Fintech companies | |

| Features | Testing period in the regulatory sandbox: 6~12 months. The number of investors and Investment amounts are limited. | |

| India | Organization in charge | RBI (Reserve Bank of India) |

| Targets | FinTech companies including startups, banks, financial institutions, and any other company partnering with or providing support to financial services businesses. | |

| Features | Testing period in the regulatory sandbox: case-specific decisions. Time and degree of deregulation are determined and applied on a case-by-case basis. | |

| Canada | Organization in charge | CSA (Canadian Securities Administrators) |

| Targets | Fintech companies and startups | |

| Features | Testing period in the regulatory sandbox: case-specific decisions. Registration and exemptive relief granted to firms in the CSA. Regulatory Sandbox are time limited. The time limit will be determined on a case-by-case basis. | |

| Malaysia | Organization in charge | BNM (Bank Negara Malaysia) |

| Targets | Finance and Fintech companies | |

| Features | Testing period in the regulatory sandbox: within 12 months. One of the main goals of the Malaysian fintech regulatory sandboxS is financial institutions’ efficiency and risk management. The Bank has a lot of decision-making authority. | |

| The Netherlands | Organization in charge | AFM & DNB (Autoriteit Financiële Markten & De Nederlandsche Bank) |

| Targets | Available to all financial services companies | |

| Features | Testing period in the regulatory sandbox: case-specific decisions. If something illegal happens under the monitoring by the supervisor, it can be stopped immediately. The role of the supervisor seems to be rather big. They also consider whether the appliers violate the EU laws. | |

| Japan | Organization in charge | JFSA (Japan Financial Services Agency) |

| Targets | Finance/IT companies and Fintech companies Any company, including foreign companies, can apply to use this regulatory regime in Japan. AI, IoT, big data, and blockchain projects are explicitly mentioned as the most prospective and suitable areas. | |

| Features | Testing period in the regulatory sandbox: within 12 months. Japanese regulatory sandboxes also include foreign companies operating in Japan. |

| Pre–Post Analysis | Comparison Analysis | Regression Analysis | |

|---|---|---|---|

| Order | 1 | 2 | 3 |

| Purpose | To confirm the changes before and after sandbox introduction. | Comparison differences between A and B group. | Extracting the influence of factors (sandbox and others). |

| Target | Intra-group A (pre/post) | Inter-group A–B | All group |

| Methods | Paired samples t-test (or Wilcoxon W test) | Independent samples t-test (or Mann–Whitney U test) | Multiple Regression analysis |

| Assumptions |

|

| |

| Control Variables | Financial Market Development | Innovation |

|---|---|---|

| Components of the variable |

|

|

| Regression Models | Equations | Variables |

|---|---|---|

| Model 1 | Y: Dependent Variable X1: Financial market development X2: Innovation X3: Sandbox | |

| Model 2 | ||

| Model 3 | ||

| Diagnostic test |

| |

| Category | Variables | Abbr. | Operational Definition | Source |

|---|---|---|---|---|

| Dependent Variable | The change of total amount | Am_change | Growth rate of total investment | Preqin’s Global Investment Database |

| The change of average investment | Avr_change | Growth rate of average amount of investment | ||

| The change of the number of deals | Deal_change | Growth rate of the number of investment deals | ||

| Independent Variable | Sandbox introduction | Sandbox | The Regulatory Sandbox introduction (0: not introduced, 1: introduced) | Each country’s financial regulatory authority |

| Control Variable | Financial market development | Fin_Mardev | The degree of financial market development | World Economic Forum, 2017 Global Competitiveness Index Framework |

| Innovation | Innovation | The degree of national innovation capability |

| Region | A Group (Nine Countries) | B Group (Nine Countries) |

|---|---|---|

| West Europe | UK, The Netherlands | France, Germany, Ireland, Spain, Belgium |

| Asia | Singapore, Hong Kong, India, Malaysia, Japan | China, South Korea |

| North America | Canada | US |

| Oceania | Australia | New Zealand |

| Sandbox | Am_change | Avr_change | Deal_change | |

|---|---|---|---|---|

| Mean | 0 | −0.232 | 0.0864 | −0.230 |

| 1 | 0.377 | 1.57 | −0.388 | |

| Median | 0 | −0.218 | 0.0221 | −0.230 |

| 1 | 0.327 | 1.26 | −0.404 | |

| Standard deviation | 0 | 0.404 | 0.509 | 0.326 |

| 1 | 0.322 | 1.06 | 0.265 | |

| Skewness | 0 | 1.44 | 0.327 | 0.324 |

| 1 | 0.322 | 0.913 | 0.875 | |

| Std. error skewness | 0 | 0.717 | 0.717 | 0.717 |

| 1 | 0.717 | 0.717 | 0.717 | |

| Shapiro-Wilk | 0 | 0.124 | 0.954 | 0.355 |

| 1 | 0.453 | 0.589 | 0.452 |

| Test | Statistic | df | p | ||

|---|---|---|---|---|---|

| Pre_Invest | Post_Invest | Student’s t | −2.54 | 8.00 | 0.017 |

| Wilcoxon W | 3.00 | 0.010 | |||

| Shapiro–Wilk | 0.867 | 0.113 | |||

| Pre_Avr | Post_Avr | Student’s t | −3.22 | 8.00 | 0.006 |

| Wilcoxon W | 0.00 | 0.002 | |||

| Shapiro–Wilk | 0.804 | 0.023 | |||

| Pre_Deal | Post_Deal | Student’s t | 3.06 | 8.00 | 0.992 |

| Wilcoxon W | 44.00 | 0.995 | |||

| Shapiro–Wilk | 0.890 | 0.199 |

| Test | Statistic | df | p | ||

|---|---|---|---|---|---|

| Pre_Invest | Post_Invest | Student’s t | −3.54 | 16 | 0.001 |

| Mann–Whitney U | 8.00 | 0.001 | |||

| Shapiro–Wilk | 0.925 | 0.158 | |||

| Levene’s | 0.0843 | 16 | 0.775 | ||

| Pre_Avr | Post_Avr | Student’s t | −3.77 | 16 | <0.001 |

| Mann–Whitney U | 5.00 | <0.001 | |||

| Shapiro–Wilk | 0.955 | 0.516 | |||

| Levene’s | 3.4436 | 16 | 0.082 | ||

| Pre_Deal | Post_Deal | Student’s t | 1.13 | 16 | 0.863 |

| Mann–Whitney U | 29.00 | 0.851 | |||

| Shapiro–Wilk | 0.925 | 0.161 | |||

| Levene’s | 0.8642 | 16 | 0.366 |

| Hypothesis | Model | R | R² | Adjusted R² | S.E. of Estimate | ΔR² | ΔF | p |

|---|---|---|---|---|---|---|---|---|

| 1 | 0.252 | 0.064 | 0.005 | 0.471677 | 0.064 | 1.085 | 0.313 | |

| H1 | 2 | 0.350 | 0.122 | 0.005 | 0.471583 | 0.059 | 1.006 | 0.376 |

| 3 | 0.738 | 0.544 | 0.447 | 0.351677 | 0.422 | 12.972 | 0.01 | |

| 1 | 0.072 | 0.005 | −0.057 | 1.140832 | 0.005 | 0.084 | 0.776 | |

| H2 | 2 | 0.172 | 0.030 | −0.100 | 1.163652 | 0.024 | 0.379 | 0.798 |

| 3 | 0.755 | 0.571 | 0.479 | 0.801119 | 0.541 | 17.648 | 0.007 | |

| 1 | 0.308 | 0.094 | 0.038 | 0.293877 | 0.094 | 1.678 | 0.214 | |

| H3 | 2 | 0.377 | 0.142 | 0.027 | 0.295466 | 0.047 | 0.828 | 0.316 |

| 3 | 0.542 | 0.293 | 0.142 | 0.277488 | 0.151 | 3.007 | 0.169 |

| Hypothesis | Predictor | B | S.E. | Stand. B. | t | p |

|---|---|---|---|---|---|---|

| H1 | Intercept | −1.154 | 0.847 | −1.362 | 0.195 | |

| Fin_MarkDev | −0.119 | 0.162 | −0.158 | −0.733 | 0.476 | |

| Innovation | 0.306 | 0.170 | 0.361 | 1.802 | 0.093 | |

| Sandbox | 0.647 | 0.180 | 0.704 | 3.602 | 0.003 | |

| H2 | Intercept | 0.192 | 1.930 | 0.100 | 0.922 | |

| Fin_MarkDev | −0.596 | 0.369 | −0.337 | −1.615 | 0.129 | |

| Innovation | 0.554 | 0.387 | 0.278 | 1.432 | 0.174 | |

| Sandbox | 1.720 | 0.409 | 0.798 | 4.201 | 0.001 | |

| H3 | Intercept | −1.563 | 0.668 | −2.339 | 0.035 | |

| Fin_MarkDev | 0.184 | 0.128 | 0.386 | 1.441 | 0.172 | |

| Innovation | 0.099 | 0.134 | 0.184 | 0.736 | 0.474 | |

| Sandbox | −0.246 | 0.142 | −0.422 | −1.734 | 0.105 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Goo, J.J.; Heo, J.-Y. The Impact of the Regulatory Sandbox on the Fintech Industry, with a Discussion on the Relation between Regulatory Sandboxes and Open Innovation. J. Open Innov. Technol. Mark. Complex. 2020, 6, 43. https://doi.org/10.3390/joitmc6020043

Goo JJ, Heo J-Y. The Impact of the Regulatory Sandbox on the Fintech Industry, with a Discussion on the Relation between Regulatory Sandboxes and Open Innovation. Journal of Open Innovation: Technology, Market, and Complexity. 2020; 6(2):43. https://doi.org/10.3390/joitmc6020043

Chicago/Turabian StyleGoo, Jayoung James, and Joo-Yeun Heo. 2020. "The Impact of the Regulatory Sandbox on the Fintech Industry, with a Discussion on the Relation between Regulatory Sandboxes and Open Innovation" Journal of Open Innovation: Technology, Market, and Complexity 6, no. 2: 43. https://doi.org/10.3390/joitmc6020043

APA StyleGoo, J. J., & Heo, J.-Y. (2020). The Impact of the Regulatory Sandbox on the Fintech Industry, with a Discussion on the Relation between Regulatory Sandboxes and Open Innovation. Journal of Open Innovation: Technology, Market, and Complexity, 6(2), 43. https://doi.org/10.3390/joitmc6020043