Effect of Religiosity, Perceived Risk, and Attitude on Tax Compliant Intention Moderated by e-Filing

Abstract

:1. Introduction

2. Literature Review

2.1. Religiosity

2.2. Perceived Risk

2.3. Attitude

2.4. e-Filing

2.5. Tax Compliant Intention

3. Research Methods and Materials

- :

- endogenous latent variable matrix

- :

- exogenous latent variable matrix

- :

- matrix of path coefficients of endogenous latent variables to endogenous latent variables

- :

- matrix of path coefficients of exogenous latent variables to endogenous latent variables

- :

- inner model error matrix

- y:

- indicator matrix for endogenous latent variables

- x:

- indicator matrix for exogenous latent variables

- Y:

- matrix for endogenous latent variables

- X:

- matrix for exogenous latent variables

- λy:

- loading matrix for endogenous latent variables

- λx:

- loading matrix for exogenous latent variables

- v:

- error for endogenous latent variable

- u:

- error for exogenous latent variable

4. Results and Discussion

- (1)

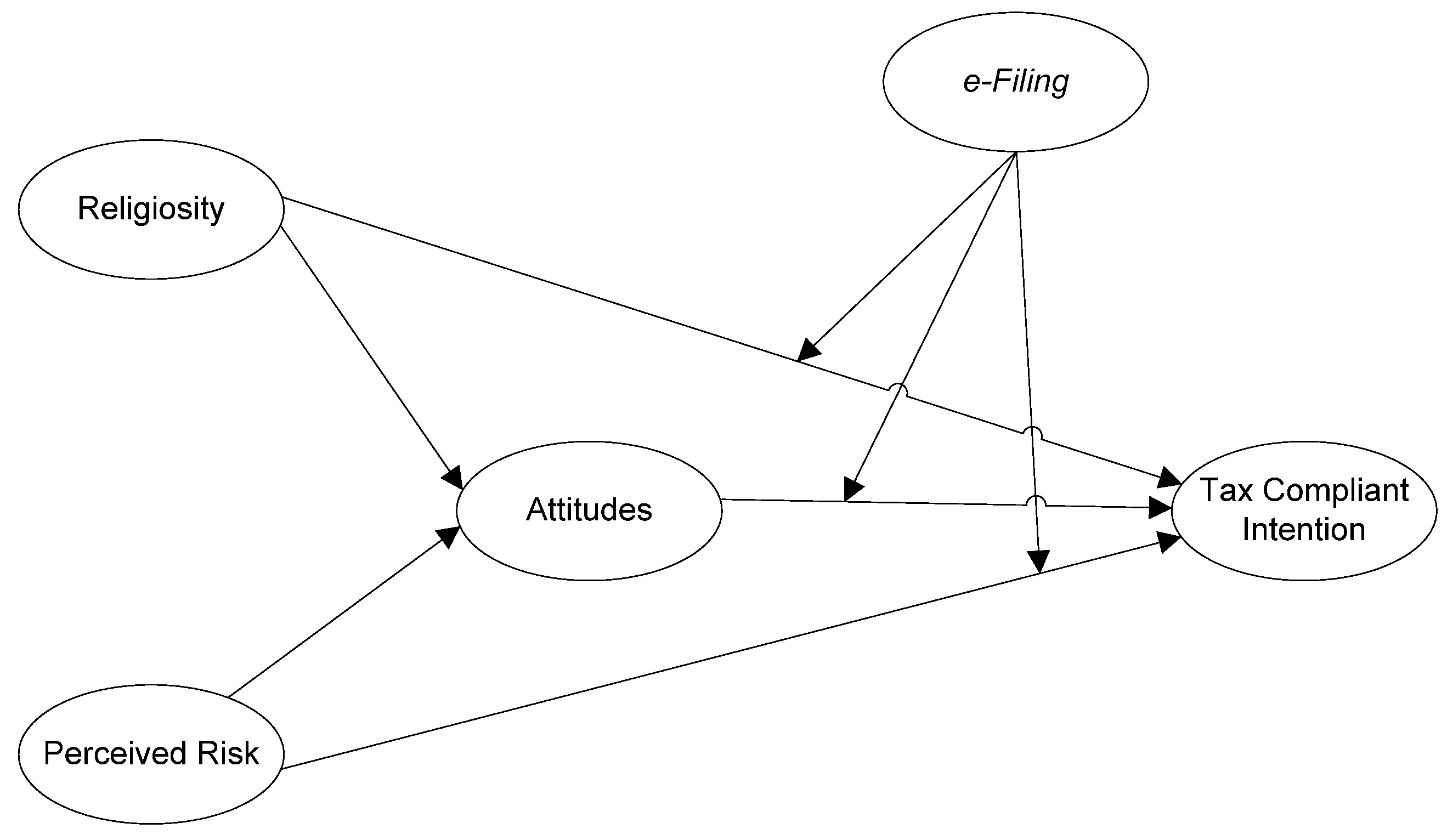

- The direct effect of religiosity on attitude has a path coefficient of 0.239 and a p-value of 0.001 (less than 0.05). There is a significant direct effect of religiosity on attitude. Considering that the path coefficient is positive, it can be concluded that when the religiosity increases, the attitude will also increase.

- (2)

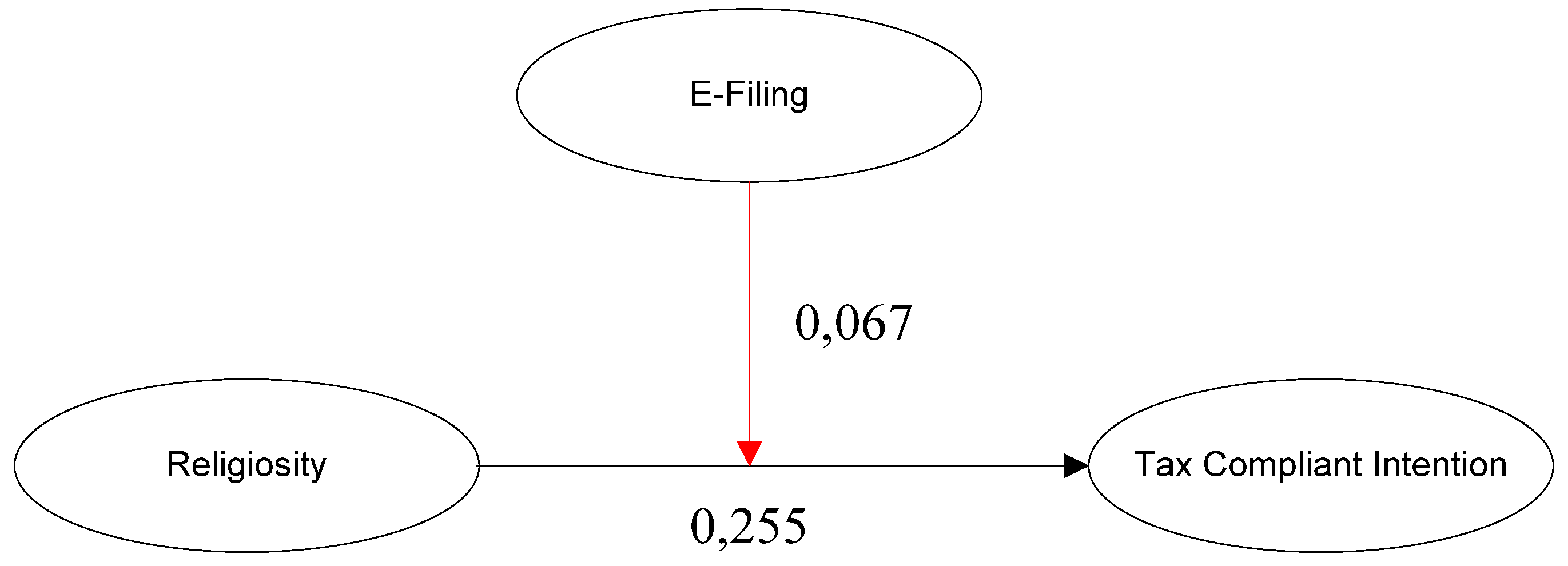

- The direct effect of religiosity on tax compliant intention has a path coefficient of 0.255 and p-value < 0.001 (less than 0.05). There is a significant direct effect of religiosity on tax-compliant intention. Considering that the path coefficient is positive, it can be concluded that the higher the religiosity, the higher the intention to comply with taxes.

- (3)

- The direct effect of perceived risk on attitude has a path coefficient of −0.207 and a p-value of 0.004 (less than 0.05). There is a significant direct effect of perceived risk on attitude. Considering that the path coefficient is negative, it can be concluded that the higher the perceived risk, the lower the attitude will be.

- (4)

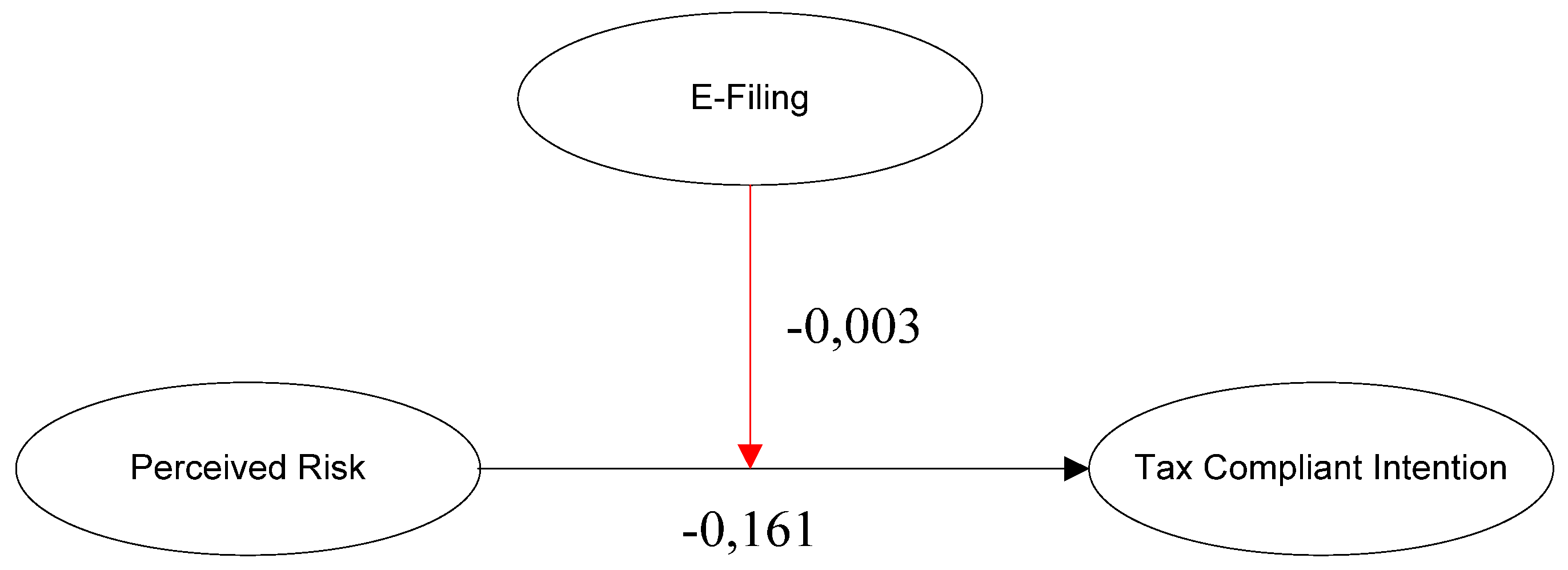

- The direct effect of perceived risk on tax compliant intention has a path coefficient of −0.161 and a p-value of 0.020 (less than 0.05). There is a significant direct effect of perceived risk on tax compliant intention. Considering that the path coefficient is negative, it can be concluded that the higher the perceived risk, the lower the tax compliant intention will be.

- (5)

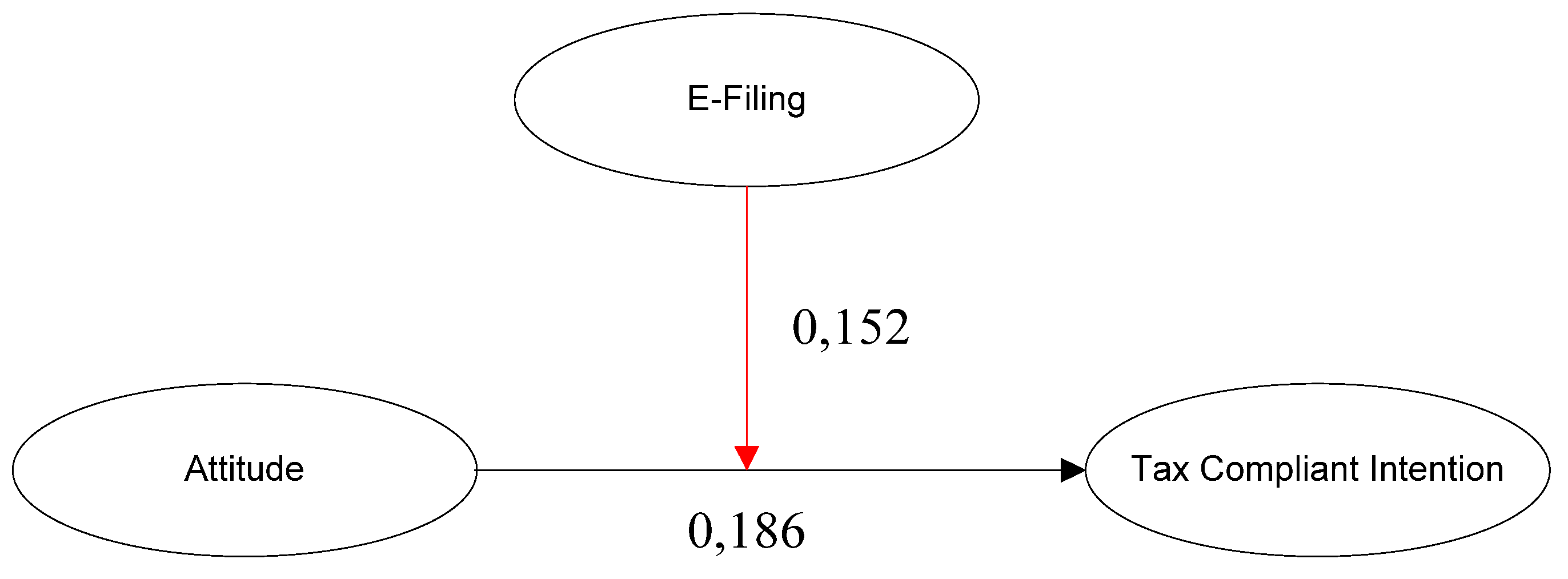

- The direct effect of attitude on tax compliant intention has a path coefficient of 0.186 and a p-value of 0.008 (less than 0.05). There is a significant direct effect of attitude on tax compliant intention. Considering that the path coefficient is positive, it can be concluded that the higher the altitude, the higher the intention to comply with taxes will be.

4.1. Moderation Effect of e-Filing on the Relationship between Religiosity on Tax Compliant Intention

4.2. Moderation Effect of e-Filing on the Relationship between Perceived Risks on Tax Compliant Intention

4.3. Moderation Effect of e-Filing on the Relationship between Attitudes on Tax Compliant Intention

4.4. Research Limitations

- Taxes are influenced by the variables of religiosity, e-Filing, perceived risk, attitudes, subjective norms, and perceptions of behavioral control. In future research, it is necessary to use variables that may affect tax compliance, such as tax avoidance, tax evasion, tax amnesty, trusted authorities, nationalism, and legal certainty. In addition, it is necessary to include variables that can represent the ability of the taxpayer, for example, financial statements, and leverage.

- Considering that it is possible for the respondents of this study to have different points of view and assessments of the research variables, it is suggested that future research search for homogeneous respondents and broaden the scope. It is also recommended to use secondary data to minimize the possibility of bias in the respondents’ perceptions obtained.

4.5. Research Implications

- Improvements and improvements are needed regarding the use of e-Filing. The use of e-Filing can be improved in terms of the ease of use of the system so that it can be easily understood by taxpayers. The government in this case needs to improve and improve the previously existing features in e-Filing to make it more user friendly, simple, and systematic.

- It is necessary to increase the religiosity element for the taxpayer community, considering that the results of this study state that religiosity can increase tax compliance attitudes and intentions. The government, through the Directorate General of Taxes under the coordination of the Ministry of Finance of the Republic of Indonesia, is advised to start incorporating elements of religion in conducting socialization related to tax compliance behavior or material related to taxation in terms of various religions in Indonesia.

- The public as taxpayers are advised to support and encourage increased religiosity, attitudes, perceived risks, and the use of e-Filing in paying taxes, which has implications for tax compliance intentions where the use of tax revenues will be returned entirely for the prosperity of the Indonesian people.

- The government through the Directorate General of Taxes under the coordination of the Ministry of Finance of the Republic of Indonesia is advised to measure the effectiveness of e-Filing performance in order to increase the level of taxpayer compliance. Increased taxpayer compliance will be able to assist the government in achieving tax revenue targets during the current year.

- The government, through the Directorate General of Taxes under the coordination of the Ministry of Finance of the Republic of Indonesia is advised to provide an understanding of taxes using a religiosity approach, so that the attitude of taxpayers can be better and in order to increase the level of taxpayer compliance.

- In future research, it is hoped several other variables will be combined that may become one of the driving and inhibiting factors in tax compliance intentions, for example tax avoidance, perceived behavior control, tax evasion, and others.

5. Conclusions

- (1)

- Comprehensively examines the variables that may affect the Intention to Comply in Paying Taxes.

- (2)

- Provides additional knowledge and information for the government through the Directorate General of Taxes that in order to increase the Obedience of Large Taxpayers, it is necessary to provide guidance on the Religiosity of Large Taxpayers which, in this study, is represented by the Director of Finance.

- (3)

- Provides information to the public that is important to improve taxpayer compliance because the use of tax revenues will be returned entirely for the prosperity of the people.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Ajzen, Icek. 1991. The theory of planned behavior. Organizational Behavior and Human Decision Processes 50: 179–211. [Google Scholar] [CrossRef]

- Ajzen, Icek. 2005. Attitudes, Personality, and Behavior. New York: McGraw-Hill Education. [Google Scholar]

- Bobek, Donna D., and Richard C. Hatfield. 2003. An investigation of the theory of planned behavior and the role of moral obligation in tax compliance. Behavioral Research in Accounting 15: 13–38. [Google Scholar] [CrossRef]

- Byabashaija, Warren, and Isaac Katono. 2011. The impact of college entrepreneurial education on entrepreneurial attitudes and intention to start a business in Uganda. Journal of Developmental Entrepreneurship 16: 127–44. [Google Scholar] [CrossRef]

- Calhoun, Craig. 2006. The University and the Public Good. Thesis Eleven 84: 7–43. [Google Scholar] [CrossRef]

- Chong, Zheng Rong, Jianzhong Zhao, Jian Hua Rudi Chan, Zhenyuan Yin, and Praveen Linga. 2018. Effect of horizontal wellbore on the production behavior from marine hydrate bearing sediment. Applied Energy 214: 117–30. [Google Scholar] [CrossRef]

- Elci, Meral. 2007. Effect of manifest Needs, Religiosity and selected demographics on hard working: An empirical investigation in Turkey. Journal of International Business Research 6: 97. [Google Scholar]

- Féry, Yves-André. 2003. Differentiating visual and kinesthetic imagery in mental practice. Canadian Journal of Experimental Psychology/Revue Canadienne de Psychologie Expérimentale 57: 1–10. [Google Scholar] [CrossRef]

- French, Wendell L., and Cecil H Bell. 2001. Organization Development: Behavioral Science Interventions for Organization Improvement. (No. HD38 F69). Hoboken: Prentice-Hall. [Google Scholar]

- Glock, Charles, and Rodney Stark. 1965. Is There an American Protestantism? Trenton: Transaction. [Google Scholar]

- Graafland, Johan. 2017. Religiosity, Attitude, and the Demand for Socially Responsible Products. Journal of Business Ethics 144: 121–38. [Google Scholar] [CrossRef] [Green Version]

- Hariyono, Hariyono. 2021. Do Economic Attitudes Drive to Employee Productivity? Lesson from Indonesia. The Journal of Asian Finance, Economics, and Business 8: 1009–16. [Google Scholar] [CrossRef]

- Ilyas, Wirawan B., and Richard Burton. 2013. Hukum Pajak, 6th ed. Jakarta: Salemba Empat. [Google Scholar]

- Johnson, Byron R., Sung Joon Jang, David B. Larson, and Spencer De Li. 2001. Does adolescent religious commitment matter? A reexamination of the effects of religiosity on delinquency. Journal of Research in Crime and Delinquency 38: 22–44. [Google Scholar] [CrossRef]

- Johnson, Kathryn A., Adam B. Cohen, and Morris A. Okun. 2016. God is watching you… but also watching over you: The influence of benevolent God representations on secular volunteerism among Christians. Psychology of Religion and Spirituality 8: 363–74. [Google Scholar] [CrossRef]

- Konz, Gregory N. P., and Francis X. Ryan. 1999. Maintaining an organizational spirituality: No easy task. Journal of Organizational Change Management 12: 200–10. [Google Scholar] [CrossRef]

- Lu, Hong, and Jiafure Wang. 2018. Entrepreneurial intention of two patterns of planned behaviour and alertness: Empirical evidence in China. The Journal of Asian Finance, Economics, and Business 5: 63–72. [Google Scholar] [CrossRef]

- Lu, Yun, Jong Hyun Jung, and Shawn Bauldry. 2019. Explaining the cross-national variation in the relationship between religious organization membership and civic organization participation. Social Science Research 83: 102310. [Google Scholar] [CrossRef]

- McClelland, David C. 1961. Achieving Society. (No. 15). New York: Simon and Schuster. [Google Scholar]

- Mohd Ali, Nor Raihana. 2013. The Influence of Religiosity on Tax Compliance in Malaysia. Doctoral dissertation, Curtin University, Bentley, WA, USA. [Google Scholar]

- Nashori, Fuad, and Bachtiar Diana Mucharam. 2007. Mengembangkan Kreativitas dalam perspektif Psikologi Islam (Yogyakarta: Menara Kudus, 2000). In Nawawi, Imam, Syarh Shahiih Muslim, Tnk: Maktabah Dahlan, tt. Pasiak, Taufik, Manajemen Kecerdasan: Memberdayakan IQ, EQ dan SQ untuk Kesuksesan Hidup. Bandung: Penerbit Mizan. [Google Scholar]

- Nguyen, Oanh Thi. 2020. Factors affecting the intention to use digital banking in Vietnam. The Journal of Asian Finance, Economics, and Business 7: 303–10. [Google Scholar] [CrossRef]

- Night, Sadress, and Juma Bananuka. 2019. The mediating role of adoption of an electronic tax system in the relationship between attitude towards electronic tax system and tax compliance. Journal of Economics, Finance and Administrative Science 25: 73–88. [Google Scholar] [CrossRef]

- Nitisusastro, Mulyadi. 2012. Perilaku Konsumen Dalam Perspektif Kewirausahaan. Bandung: Alfabeta. [Google Scholar]

- Nkundabanyanga, Stephen Korutaro, Philemon Mvura, David Nyamuyonjo, Julius Opiso, and Zulaika Nakabuye. 2017. Tax compliance in a developing country: Understanding taxpayers’ compliance decision by their perceptions. Journal of Economic Studies 44: 931–57. [Google Scholar] [CrossRef]

- Oglethorpe, Janet E., and Kent B. Monroe. 1994. Determinant of Perceived Health and Safety Risk of Selected Hazardous Product and Activities. Journal of Consumer Affairs 28: 326–46. [Google Scholar] [CrossRef]

- Oh, Ah-Hyun, and Hye-Yoon Park. 2020. The Effect of Airline’s Professional Models on Brand Loyalty: Focusing on Mediating Effect of Brand Attitude. The Journal of Asian Finance, Economics, and Business 7: 155–66. [Google Scholar] [CrossRef]

- Oktaviani, Rachmawati Meita, Pancawati Hardiningsih, and Ceacilia Srimindari. 2017. Kepatuhan Wajib Pajak Memediasi Determinan Penerimaan Pajak Penghasilan. Jurnal Akuntansi 21: 318–35. [Google Scholar] [CrossRef] [Green Version]

- Purnamasari, Pupung, and Ima Amaliah. 2015. Fraud prevention: Relevance to religiosity and spirituality in the workplace. Procedia-Social and Behavioral Sciences 211: 827–35. [Google Scholar] [CrossRef] [Green Version]

- Sarwono, Sarlito W., and Eko A. Meinarno. 2009. Psikologi Sosial. Jakarta: Salemba. [Google Scholar]

- Simmons, William Paul, and Sharon Parsons. 2005. Beliefs in conspiracy theories among African Americans: A comparison of elites and masses. Social Science Quarterly 86: 582–98. [Google Scholar] [CrossRef]

- Soemitro, Riti. 2013. Perpajakan Teori dan Kasus. Jakarta: Gramedia. [Google Scholar]

- Solimun, Adji Achmad Rinaldo Fernandes, and Nurjannah. 2017. Multivariate Statistical Method: Structural Equation Modeling Based on WarpPLS. Malang: UB Press. [Google Scholar]

- Susanti, Rita. 2016. Hubungan religiusitas dan kualitas kehidupan kerja dengan organizational citizenship behavior (OCB) pada karyawan. Jurnal Psikologi 11: 94–102. [Google Scholar]

- Tran-Nam, Binh. 2015. An integrated approach to the economic measurement of the costs of tax complexity. In Tax Simplification. Alphen aan den Rijn: Kluwer Law International, pp. 55–75. [Google Scholar]

- Weaver, Gary R., and Bradley R. Agle. 2002. Religiosity and ethical behavior in organizations: A symbolic interactionist perspective. Academy of Management Review 27: 77–97. [Google Scholar] [CrossRef]

- Wibowo, Hermansyah Andi, and Martina Rahmawati Masitoh. 2018. Measuring religiosity and its effects on attitude and intention to wea r a hijab: Revalidating the scale. In Increasing Management Relevance and Competitiveness. Boca Raton: CRC Press, pp. 237–40. [Google Scholar]

- Worthington, Everett L., Chelsea L. Greer, Joshua Hook, Don Davis, Aubrey L. Gartner, David J. Jennings Ii, Lucy Norton, Daryl R. Van Tongeren, Todd W. Greer, and Loren Toussaint. 2010. Forgiveness and spirituality in organizational life: Theory, status of research, and new ideas for discovery. Journal of Management Spirituality and Religion 7: 119–34. [Google Scholar] [CrossRef]

- Yusoff, Siti Norfazlina, and Saidatulakmal Mohd. 2017. How Well-Informed Are Taxpayers On Their Income Tax Payment? Journal of Global Business and Social Entrepreneurship (GBSE) 3: 53–59. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Indicator | Correlation | Result |

|---|---|---|---|

| Religiosity (X1) | Faith (ideological) (X1.1) | 0.752 | Valid |

| Religious Practices (X1.2) | 0.753 | Valid | |

| Appreciation (X1.3) | 0.789 | Valid | |

| Knowledge (intellectual) (X1.4) | 0.667 | Valid | |

| Practice (Consequences) (X1.5) | 0.827 | Valid | |

| Perceived Risk (X2) | Financial Risk (X2.1) | 0.780 | Valid |

| Functional Risk (X2.2) | 0.835 | Valid | |

| Physical Risk (X2.3) | 0.782 | Valid | |

| Psychological Risk (X2.4) | 0.807 | Valid | |

| Social Risks (X2.5) | 0.696 | Valid | |

| Time Risk (X2.6) | 0.748 | Valid | |

| e-Filing (M1) | Frequency of Use (M1.1) | 0.775 | Valid |

| The simplicity of the System (M1.2) | 0.760 | Valid | |

| Comprehensive Security (M1.3) | 0.725 | Valid | |

| Attitude (Y1) | Behavioral Belief (Y1.1) | 0.735 | Valid |

| Evaluation of Behavioral Belief (Y1.2) | 0.799 | Valid | |

| Tax Compliant Intention (Y2) | Personal Tendency to Behave (Y3.1) | 0.676 | Valid |

| The decision to Be Compliant (Y3.2) | 0.872 | Valid |

| Variable | Alpha-Cronbach | Conclusion |

|---|---|---|

| Religiosity (X1) | 0.792 | Reliable |

| Perceived Risk (X2) | 0.754 | Reliable |

| e-Filing (M1) | 0.755 | Reliable |

| Attitude (Y1) | 0.751 | Reliable |

| Tax Compliant Intention (Y2) | 0.756 | Reliable |

| Variable | Indicator | Weight | p-Value |

|---|---|---|---|

| Religiosity (X1) | Faith (ideological) (X1.1) | 0.291 | <0.001 |

| Religious Practices (X1.2) | 0.284 | <0.001 | |

| Appreciation (X1.3) | 0.259 | <0.001 | |

| Knowledge (intellectual) (X1.4) | 0.262 | <0.001 | |

| Practice (Consequences) (X1.5) | 0.255 | <0.001 | |

| Perceived Risk (X2) | Financial Risk (X2.1) | 0.266 | <0.001 |

| Functional Risk (X2.2) | 0.245 | <0.001 | |

| Physical Risk (X2.3) | 0.246 | <0.001 | |

| Psychological Risk (X2.4) | 0.250 | <0.001 | |

| Social Risks (X2.5) | 0.251 | <0.001 | |

| Time Risk (X2.6) | 0.233 | <0.001 | |

| e-Filing (M1) | Frequency of Use (M1.1) | 0.410 | <0.001 |

| Simplicity of the System (M1.2) | 0.399 | <0.001 | |

| Comprehensive Security (M1.3) | 0.410 | <0.001 | |

| Attitude (Y1) | Behavioral Belief (Y1.1) | 0.559 | <0.001 |

| Evaluation of Behavioral Belief (Y1.2) | 0.559 | <0.001 | |

| Tax Compliant Intention (Y2) | Personal Tendency to Behave (Y3.1) | 0.558 | <0.001 |

| Decision to Be Compliant (Y3.2) | 0.558 | <0.001 |

| Relations between Variables | Hypothesis | Path Coefficient | p-Value | Conclusion |

|---|---|---|---|---|

| Religiosity → attitude | H1 | 0.239 | 0.001 | Significant |

| Religiosity → tax compliant intention | H2 | 0.255 | <0.001 | Significant |

| perceived risk → attitude | H3 | −0.207 | 0.004 | Significant |

| perceived risk → tax compliant intention | H4 | −0.161 | 0.020 | Significant |

| attitude → tax compliant intention | H5 | 0.186 | 0.008 | Significant |

| Indirect Effect | Coefficient | p-Value | Conclusion | ||

|---|---|---|---|---|---|

| Independent | → | Dependent | |||

| Religiosity (X1) | → | Tax Compliant Intention (Y2) | 0.044 | 0.215 | Not significant |

| Perceived Risk (X2) | → | Tax Compliant Intention (Y2) | −0.039 | 0.247 | Not significant |

| Quality Index | Criteria | Statistics Value | Conclusion |

|---|---|---|---|

| Average path coefficient (APC) | Significant if p < 0.05 | 0.162 (p = 0.010) | Significant |

| Average R-squared (ARS) | Significant if p < 0.05 | 0.137 (p = 0.020) | Significant |

| Average adjusted R-squared (AARS) | Significant if p < 0.05 | 0.115 (p = 0.036) | Significant |

| Average block VIF (AVIF) | Accept if ≤ 5 Ideal if ≤ 3.3 | 1.101 | Ideal |

| Average full collinearity VIF (AFVIF) | Accept if ≤ 5 Ideal if ≤ 3.3 | 1.110 | Ideal |

| Tenenhaus GoF (GoF) | Small ≥ 0.1 Medium ≥ 0.25 Large ≥ 0.36 | 0.277 | Medium |

| Sympson’s paradox ratio (SPR) | Accept if ≥ 0.7 Ideal if = 1 | 1.000 | Ideal |

| R-squared contribution ratio (RSCR) | Accept if ≥ 0.9 Ideal if = 1 | 1.000 | Ideal |

| Statistical suppression ratio (SSR) | Accept if ≥ 0.7 | 1.000 | Accept |

| Nonlinear bivariate causality direction ratio (NLBCDR) | Accept if ≥ 0.7 | 1.000 | Accept |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Utama, M.S.; Nimran, U.; Hidayat, K.; Prasetya, A. Effect of Religiosity, Perceived Risk, and Attitude on Tax Compliant Intention Moderated by e-Filing. Int. J. Financial Stud. 2022, 10, 8. https://doi.org/10.3390/ijfs10010008

Utama MS, Nimran U, Hidayat K, Prasetya A. Effect of Religiosity, Perceived Risk, and Attitude on Tax Compliant Intention Moderated by e-Filing. International Journal of Financial Studies. 2022; 10(1):8. https://doi.org/10.3390/ijfs10010008

Chicago/Turabian StyleUtama, Mekar Satria, Umar Nimran, Kadarisman Hidayat, and Arik Prasetya. 2022. "Effect of Religiosity, Perceived Risk, and Attitude on Tax Compliant Intention Moderated by e-Filing" International Journal of Financial Studies 10, no. 1: 8. https://doi.org/10.3390/ijfs10010008

APA StyleUtama, M. S., Nimran, U., Hidayat, K., & Prasetya, A. (2022). Effect of Religiosity, Perceived Risk, and Attitude on Tax Compliant Intention Moderated by e-Filing. International Journal of Financial Studies, 10(1), 8. https://doi.org/10.3390/ijfs10010008